Ask a question from expert

Assignment on Loan Repayment of Jackson Company

8 Pages3361 Words558 Views

Added on 2019-10-09

Assignment on Loan Repayment of Jackson Company

Added on 2019-10-09

BookmarkShareRelated Documents

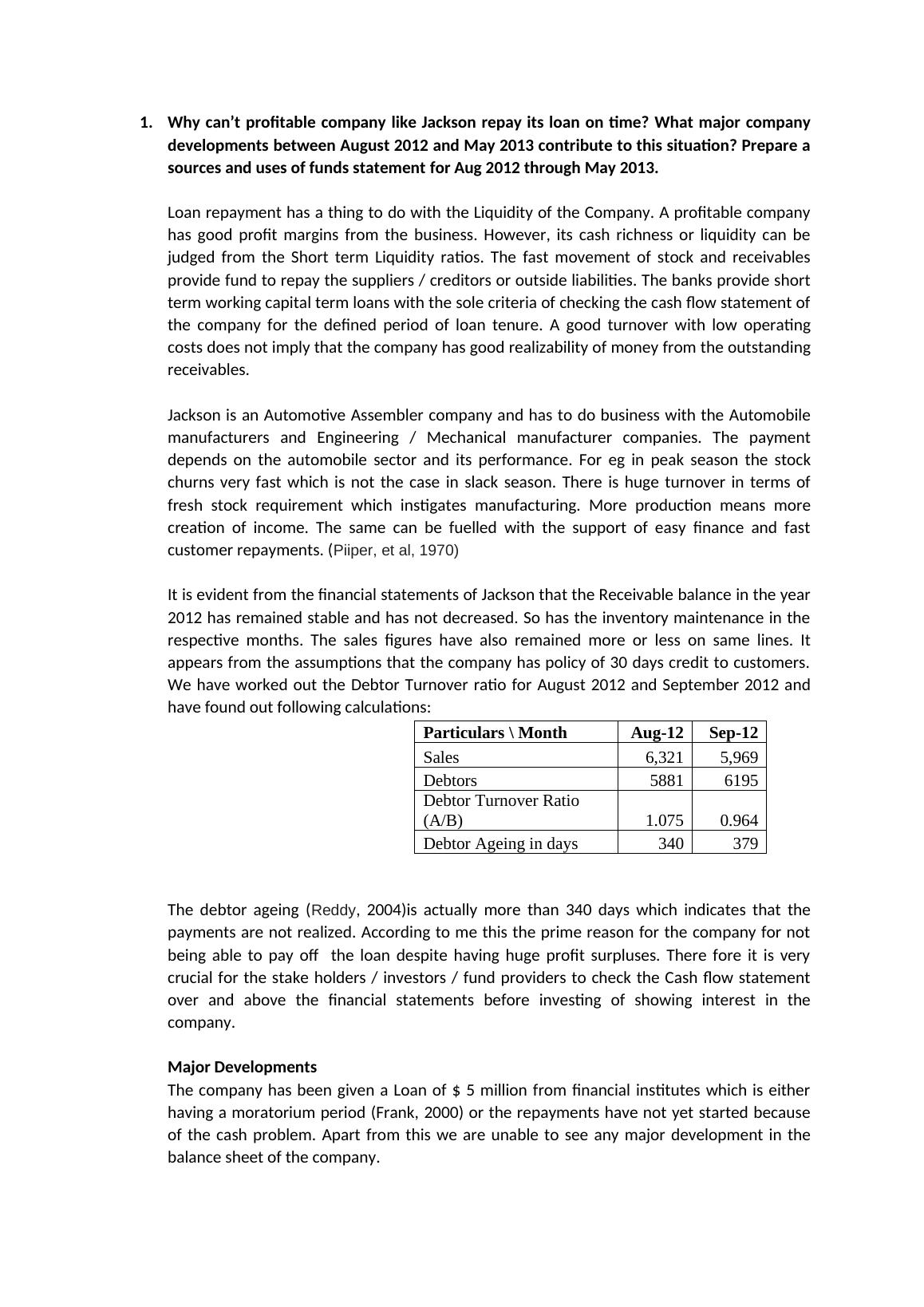

1.Why can’t profitable company like Jackson repay its loan on time? What major companydevelopments between August 2012 and May 2013 contribute to this situation? Prepare asources and uses of funds statement for Aug 2012 through May 2013.Loan repayment has a thing to do with the Liquidity of the Company. A profitable companyhas good profit margins from the business. However, its cash richness or liquidity can bejudged from the Short term Liquidity ratios. The fast movement of stock and receivablesprovide fund to repay the suppliers / creditors or outside liabilities. The banks provide shortterm working capital term loans with the sole criteria of checking the cash flow statement ofthe company for the defined period of loan tenure. A good turnover with low operatingcosts does not imply that the company has good realizability of money from the outstandingreceivables. Jackson is an Automotive Assembler company and has to do business with the Automobilemanufacturers and Engineering / Mechanical manufacturer companies. The paymentdepends on the automobile sector and its performance. For eg in peak season the stockchurns very fast which is not the case in slack season. There is huge turnover in terms offresh stock requirement which instigates manufacturing. More production means morecreation of income. The same can be fuelled with the support of easy finance and fastcustomer repayments. (Piiper, et al, 1970)It is evident from the financial statements of Jackson that the Receivable balance in the year2012 has remained stable and has not decreased. So has the inventory maintenance in therespective months. The sales figures have also remained more or less on same lines. Itappears from the assumptions that the company has policy of 30 days credit to customers.We have worked out the Debtor Turnover ratio for August 2012 and September 2012 andhave found out following calculations:The debtor ageing (Reddy, 2004)is actually more than 340 days which indicates that thepayments are not realized. According to me this the prime reason for the company for notbeing able to pay off the loan despite having huge profit surpluses. There fore it is verycrucial for the stake holders / investors / fund providers to check the Cash flow statementover and above the financial statements before investing of showing interest in thecompany.Major Developments The company has been given a Loan of $ 5 million from financial institutes which is eitherhaving a moratorium period (Frank, 2000) or the repayments have not yet started becauseof the cash problem. Apart from this we are unable to see any major development in thebalance sheet of the company.Particulars \ MonthAug-12Sep-12Sales 6,3215,969Debtors 58816195Debtor Turnover Ratio (A/B)1.0750.964Debtor Ageing in days340379

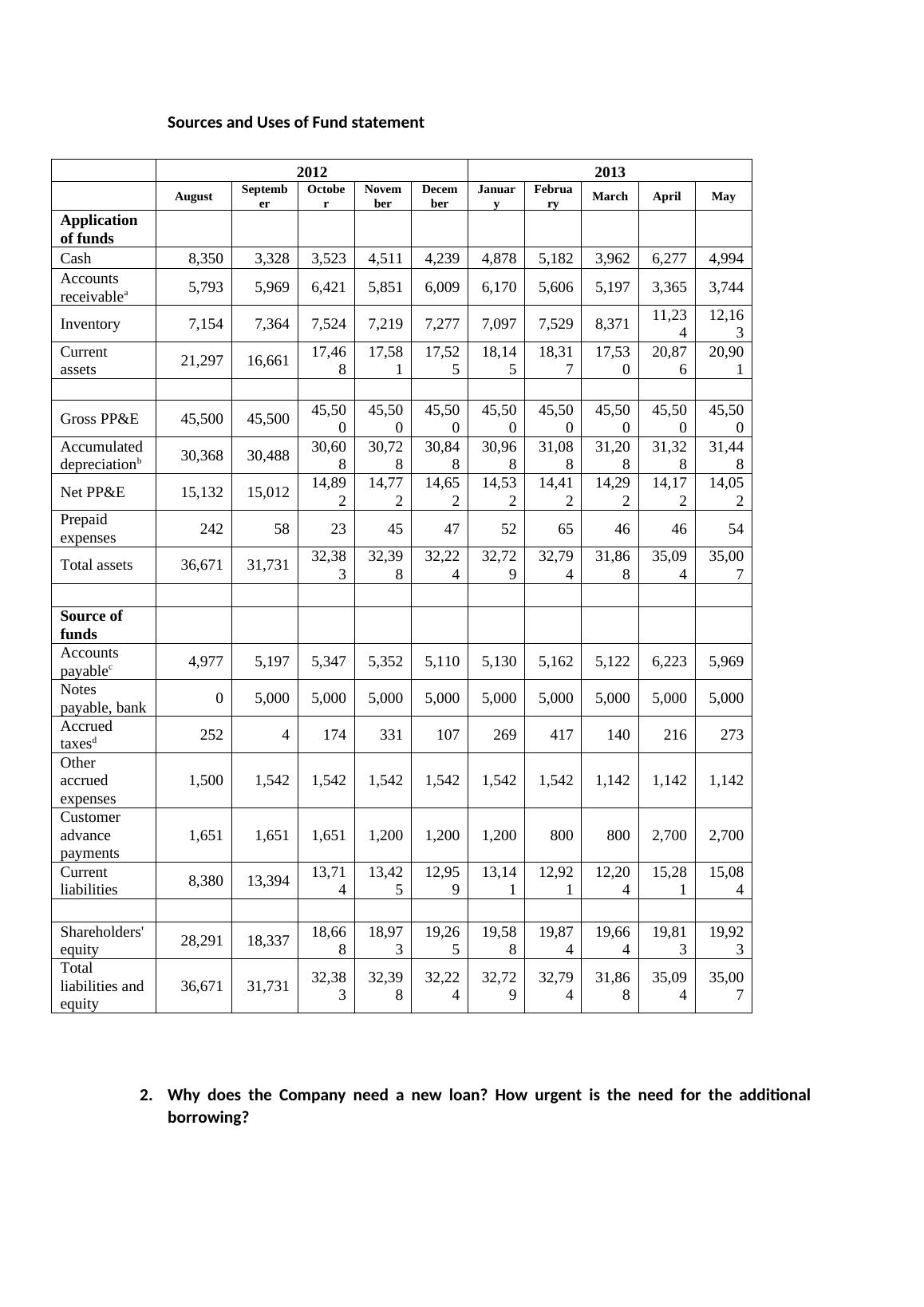

Sources and Uses of Fund statement2.Why does the Company need a new loan? How urgent is the need for the additionalborrowing?20122013AugustSeptemberOctoberNovemberDecemberJanuaryFebruaryMarchAprilMayApplication of funds Cash8,3503,3283,5234,5114,2394,8785,1823,9626,2774,994Accounts receivablea5,7935,9696,4215,8516,0096,1705,6065,1973,3653,744Inventory7,1547,3647,5247,2197,2777,0977,5298,37111,23412,163Current assets21,29716,66117,46817,58117,52518,14518,31717,53020,87620,901Gross PP&E45,50045,50045,50045,50045,50045,50045,50045,50045,50045,500Accumulated depreciationb30,36830,48830,60830,72830,84830,96831,08831,20831,32831,448Net PP&E15,13215,01214,89214,77214,65214,53214,41214,29214,17214,052Prepaid expenses242582345475265464654Total assets36,67131,73132,38332,39832,22432,72932,79431,86835,09435,007Source of funds Accounts payablec4,9775,1975,3475,3525,1105,1305,1625,1226,2235,969Notes payable, bank05,0005,0005,0005,0005,0005,0005,0005,0005,000Accrued taxesd2524174331107269417140216273Other accrued expenses1,5001,5421,5421,5421,5421,5421,5421,1421,1421,142Customer advance payments1,6511,6511,6511,2001,2001,2008008002,7002,700Current liabilities8,38013,39413,71413,42512,95913,14112,92112,20415,28115,084Shareholders'equity28,29118,33718,66818,97319,26519,58819,87419,66419,81319,923Total liabilities andequity36,67131,73132,38332,39832,22432,72932,79431,86835,09435,007

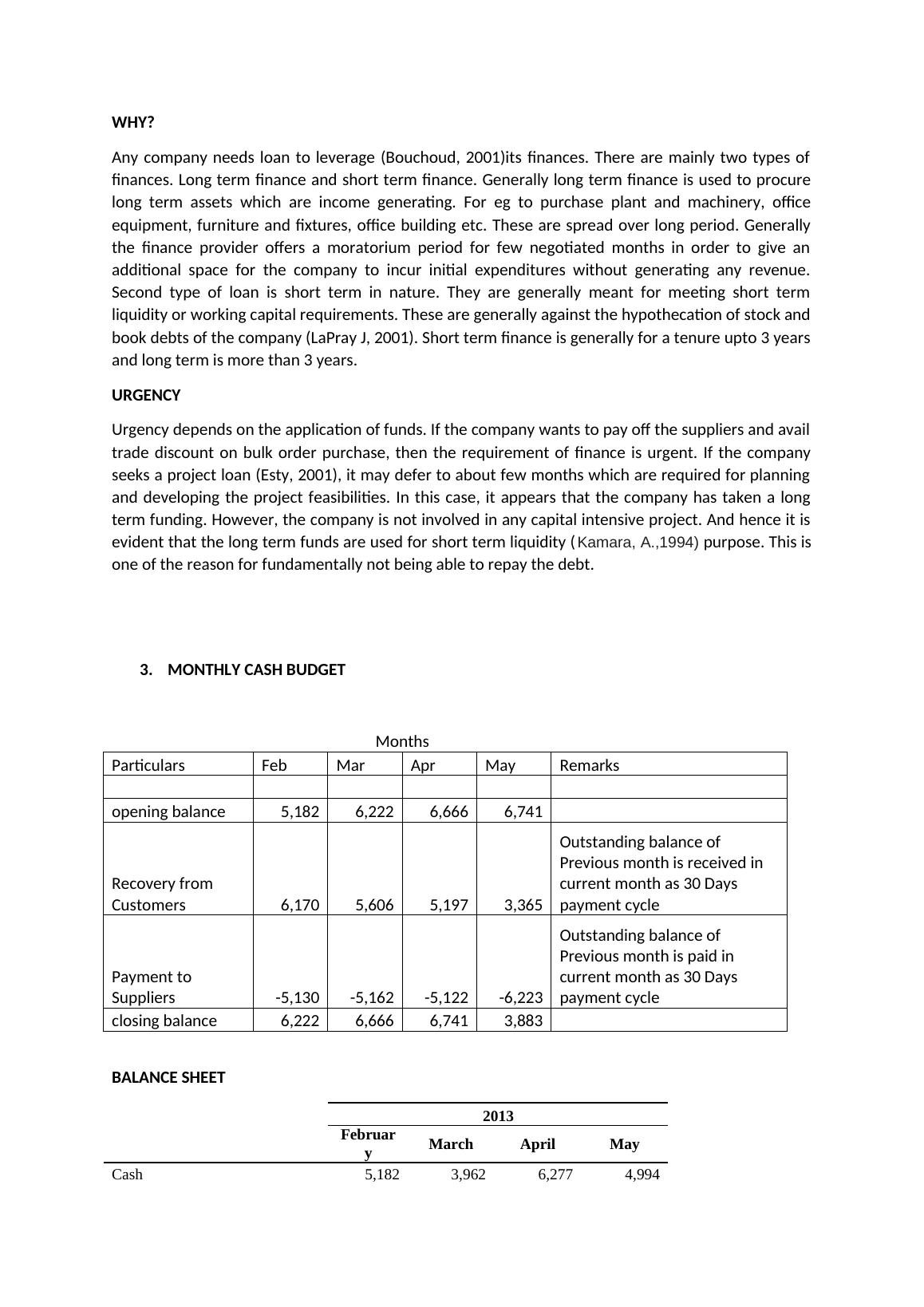

WHY?Any company needs loan to leverage (Bouchoud, 2001)its finances. There are mainly two types offinances. Long term finance and short term finance. Generally long term finance is used to procurelong term assets which are income generating. For eg to purchase plant and machinery, officeequipment, furniture and fixtures, office building etc. These are spread over long period. Generallythe finance provider offers a moratorium period for few negotiated months in order to give anadditional space for the company to incur initial expenditures without generating any revenue.Second type of loan is short term in nature. They are generally meant for meeting short termliquidity or working capital requirements. These are generally against the hypothecation of stock andbook debts of the company (LaPray J, 2001). Short term finance is generally for a tenure upto 3 yearsand long term is more than 3 years. URGENCYUrgency depends on the application of funds. If the company wants to pay off the suppliers and availtrade discount on bulk order purchase, then the requirement of finance is urgent. If the companyseeks a project loan (Esty, 2001), it may defer to about few months which are required for planningand developing the project feasibilities. In this case, it appears that the company has taken a longterm funding. However, the company is not involved in any capital intensive project. And hence it isevident that the long term funds are used for short term liquidity (Kamara, A.,1994)purpose. This isone of the reason for fundamentally not being able to repay the debt.3.MONTHLY CASH BUDGET Months Particulars FebMarAprMay Remarks opening balance 5,1826,2226,6666,741Recovery from Customers 6,1705,6065,1973,365Outstanding balance of Previous month is received in current month as 30 Days payment cycle Payment to Suppliers -5,130-5,162-5,122-6,223Outstanding balance of Previous month is paid in current month as 30 Days payment cycle closing balance6,2226,6666,7413,883BALANCE SHEET 2013FebruaryMarchAprilMayCash5,1823,9626,2774,994

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Sample Assignment on Management Accounting (pdf)lg...

|13

|1936

|27

BFM502 Programme Assessmentlg...

|6

|2392

|142

Sources of Finance and Acquisition Proposal for Newton Colg...

|6

|2540

|195

Corporate and Retail Banking Assignmentlg...

|16

|4605

|44

Financial Analysis of AGL Energy Ltdlg...

|10

|571

|141

Managerial Finance - Understanding Financial Statements and Cash Flow Statementlg...

|9

|1663

|74