DT9417/DT9418: Wind Farm Project Economic Performance Analysis

VerifiedAdded on 2023/05/29

|54

|14585

|262

Project

AI Summary

This project assesses the economic feasibility of a proposed wind farm in Intack, County Wicklow, Ireland. The student developed a mathematical model to calculate wind power output and another to determine the Net Present Value (NPV) of the project. The analysis includes an executive summary, an introduction to wind energy in Ireland, and detailed models for wind power output and economic variables like investment costs, operations and maintenance costs, and revenue generation. Economic measures such as NPV, payback period, and cost-benefit ratio are calculated. The project also performs a sensitivity analysis under various scenarios and quantifies the greenhouse gas emissions avoided. Furthermore, site constraints, including spacing, topography, accessibility, surrounding features, ground conditions, environmental factors, and regulatory requirements, are considered. The project concludes that the wind farm is economically viable and provides detailed calculations and summaries in the appendices.

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Programme Title: ME Sustainable Infrastructure

Programme Code: DT9417 & DT9418

Module: Energy Infrastructure

Assignment Number: Assignment 1

Project Designer: Ngozi Nwajei – D18124369

Word Count: 6,846

Lecturer: Aidan Duffy

Department of Civil and Structural Engineering Dublin

Institute of Technology

Programme Title: ME Sustainable Infrastructure

Programme Code: DT9417 & DT9418

Module: Energy Infrastructure

Assignment Number: Assignment 1

Project Designer: Ngozi Nwajei – D18124369

Word Count: 6,846

Lecturer: Aidan Duffy

Department of Civil and Structural Engineering Dublin

Institute of Technology

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 1

EXECUTIVE SUMMARY

The main aim of this paper was to develop a mathematical model of a wind farm project in

Intack County of Wicklow, Ireland. A mathematical model for calculating wind power output

and another for NPV of the project have been formulated and used in Excel to perform

economic calculations of the project. The project will generate 9.7 MW of electricity and its

NPV, payback period and CBR are €69,679,384, 1.9 years and 2.7 respectively. Since NPV is

positive and CBR is greater than one, this project is economically viable and should be

implemented. The model have also been used to evaluate the economic performance of the

project under five different scenarios. Scenario 4 where wind speed and price of electricity

were increased while the O&M costs were reduced resulted to the highest NPV and CBR

values and the lowest repayment period. The wind farm in this project will also help avoid

1,259,001.8 tonnes of CO2e over the 20-year period.

Page 1

EXECUTIVE SUMMARY

The main aim of this paper was to develop a mathematical model of a wind farm project in

Intack County of Wicklow, Ireland. A mathematical model for calculating wind power output

and another for NPV of the project have been formulated and used in Excel to perform

economic calculations of the project. The project will generate 9.7 MW of electricity and its

NPV, payback period and CBR are €69,679,384, 1.9 years and 2.7 respectively. Since NPV is

positive and CBR is greater than one, this project is economically viable and should be

implemented. The model have also been used to evaluate the economic performance of the

project under five different scenarios. Scenario 4 where wind speed and price of electricity

were increased while the O&M costs were reduced resulted to the highest NPV and CBR

values and the lowest repayment period. The wind farm in this project will also help avoid

1,259,001.8 tonnes of CO2e over the 20-year period.

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 2

Table of Contents

EXECUTIVE SUMMARY ....................................................................................................... 1

1. INTRODUTION ................................................................................................................ 4

2. MODELS ........................................................................................................................... 6

2.1. Flow model diagram.................................................................................................... 7

2.2. Wind Power Output model .......................................................................................... 7

2.3. Economic model ........................................................................................................ 12

2.3.1. Investment cost .................................................................................................. 13

2.3.2. Operations and maintenance (O&M) costs ....................................................... 14

2.3.3. Revenue generated ............................................................................................. 15

3. ECONOMIC MEASURES .............................................................................................. 17

3.1. Net Present value (NPV) ........................................................................................... 17

3.2. Payback period .......................................................................................................... 18

3.3. Cost benefit ratio (CBR) ........................................................................................... 19

4. SENSITIVITY ANALYSIS ............................................................................................ 20

4.1. Scenario 1 .................................................................................................................. 20

4.2. Scenario 2 .................................................................................................................. 21

4.3. Scenario 3 .................................................................................................................. 22

4.4. Scenario 4 .................................................................................................................. 24

4.5. Scenario 5 .................................................................................................................. 25

5. GREENHOUSE GAS EMISSIONS ................................................................................ 26

6. SITE CONSTRAINTS..................................................................................................... 29

6.1. Spacing ...................................................................................................................... 29

6.2. Topography ............................................................................................................... 30

6.3. Accessibility .............................................................................................................. 30

6.4. Surrounding features ................................................................................................. 30

6.5. Ground conditions ..................................................................................................... 31

6.6. Environmental factors ............................................................................................... 31

6.7. Regulatory requirements ........................................................................................... 31

7. CONCLUSION ................................................................................................................ 32

References ................................................................................................................................ 34

Page 2

Table of Contents

EXECUTIVE SUMMARY ....................................................................................................... 1

1. INTRODUTION ................................................................................................................ 4

2. MODELS ........................................................................................................................... 6

2.1. Flow model diagram.................................................................................................... 7

2.2. Wind Power Output model .......................................................................................... 7

2.3. Economic model ........................................................................................................ 12

2.3.1. Investment cost .................................................................................................. 13

2.3.2. Operations and maintenance (O&M) costs ....................................................... 14

2.3.3. Revenue generated ............................................................................................. 15

3. ECONOMIC MEASURES .............................................................................................. 17

3.1. Net Present value (NPV) ........................................................................................... 17

3.2. Payback period .......................................................................................................... 18

3.3. Cost benefit ratio (CBR) ........................................................................................... 19

4. SENSITIVITY ANALYSIS ............................................................................................ 20

4.1. Scenario 1 .................................................................................................................. 20

4.2. Scenario 2 .................................................................................................................. 21

4.3. Scenario 3 .................................................................................................................. 22

4.4. Scenario 4 .................................................................................................................. 24

4.5. Scenario 5 .................................................................................................................. 25

5. GREENHOUSE GAS EMISSIONS ................................................................................ 26

6. SITE CONSTRAINTS..................................................................................................... 29

6.1. Spacing ...................................................................................................................... 29

6.2. Topography ............................................................................................................... 30

6.3. Accessibility .............................................................................................................. 30

6.4. Surrounding features ................................................................................................. 30

6.5. Ground conditions ..................................................................................................... 31

6.6. Environmental factors ............................................................................................... 31

6.7. Regulatory requirements ........................................................................................... 31

7. CONCLUSION ................................................................................................................ 32

References ................................................................................................................................ 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 3

APPENDIX .............................................................................................................................. 38

Appendix 1: Summary of calculations for original project ..................................................... 38

Appendix 2: Summary of calculations for scenario 1 .............................................................. 40

Appendix 3: Summary of calculations for scenario 2 .............................................................. 42

Appendix 4: Summary of calculations for scenario 3 .............................................................. 44

Appendix 5: Summary of calculations for scenario 4 .............................................................. 46

Appendix 6: Summary of calculations for scenario 5 .............................................................. 48

Page 3

APPENDIX .............................................................................................................................. 38

Appendix 1: Summary of calculations for original project ..................................................... 38

Appendix 2: Summary of calculations for scenario 1 .............................................................. 40

Appendix 3: Summary of calculations for scenario 2 .............................................................. 42

Appendix 4: Summary of calculations for scenario 3 .............................................................. 44

Appendix 5: Summary of calculations for scenario 4 .............................................................. 46

Appendix 6: Summary of calculations for scenario 5 .............................................................. 48

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 4

1. INTRODUTION

Wind is one of the cleanest, cheapest and biggest renewable energy sources in Ireland

making it a very essential resource in meeting the increasing demand for green energy in the

country. The resource does not only increase power supply throughout the country but also

lowers carbon emissions thus protecting the environment and improving people’s quality of

life (Sunderland, et al., 2013). It is estimated that by 2050, wind energy will decrease carbon

dioxide emissions by between 400 and 450 million tonnes (Sustainable Energy Authority of

Ireland, (n.d.)). The current wind power output of Ireland is approximately 2,826 MW. Just

like other countries where wind energy investments have been increasing every year and

projected to continue increasing (Krohn, et al., 2009), Ireland is also investing significantly in

wind farms.

Successful implementation of wind farm projects relies heavily on the precision of

wind resource mapping. Ireland is one of the countries with affluent wind resource hence

most of the wind farm projects are feasible. However, this does not mean that any wind farm

project can be successful in the country. It requires proper planning, consultation, accurate

collection of relevant data, benchmarking with past similar projects and application of

available technologies and other strategies to lower costs.

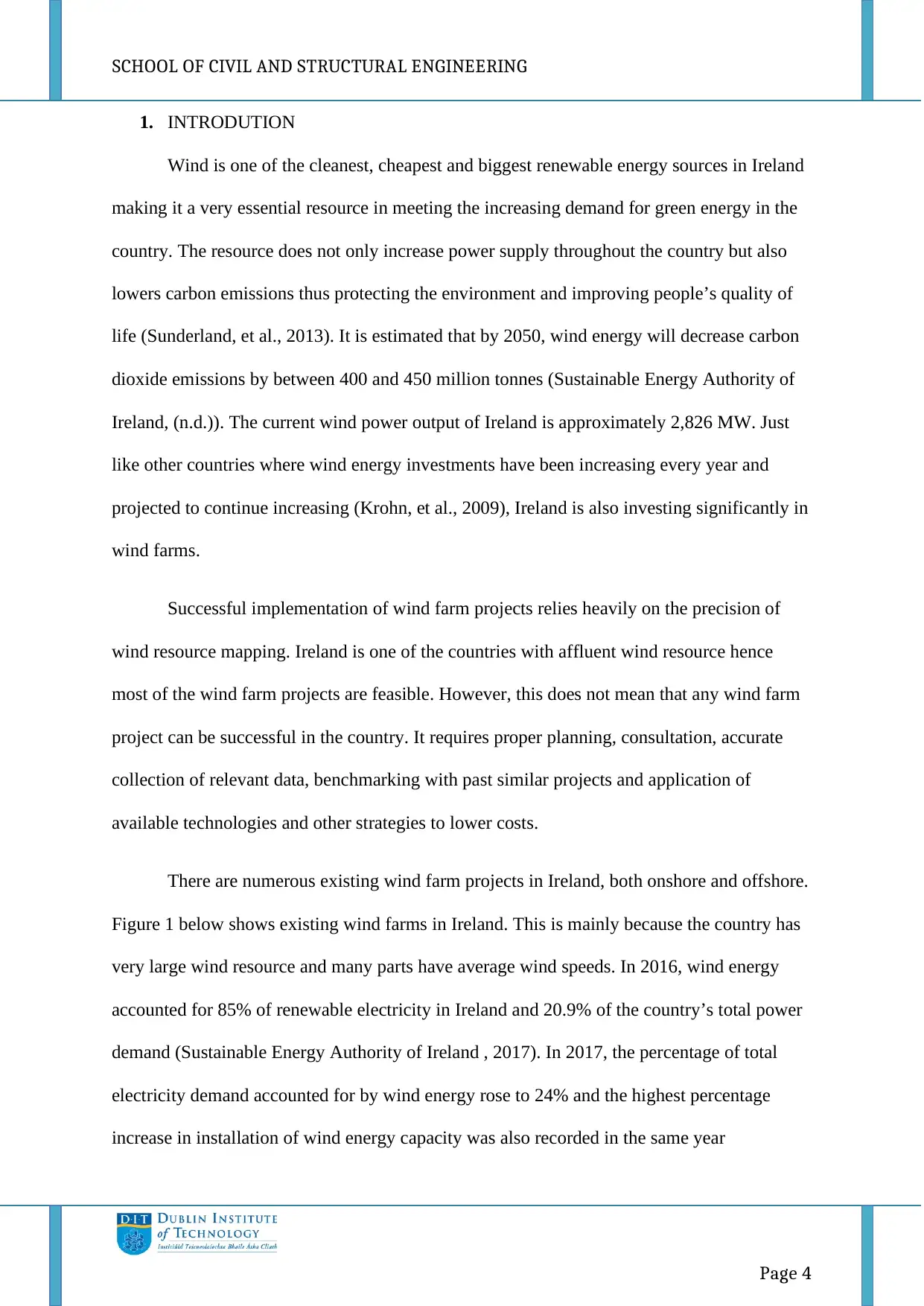

There are numerous existing wind farm projects in Ireland, both onshore and offshore.

Figure 1 below shows existing wind farms in Ireland. This is mainly because the country has

very large wind resource and many parts have average wind speeds. In 2016, wind energy

accounted for 85% of renewable electricity in Ireland and 20.9% of the country’s total power

demand (Sustainable Energy Authority of Ireland , 2017). In 2017, the percentage of total

electricity demand accounted for by wind energy rose to 24% and the highest percentage

increase in installation of wind energy capacity was also recorded in the same year

Page 4

1. INTRODUTION

Wind is one of the cleanest, cheapest and biggest renewable energy sources in Ireland

making it a very essential resource in meeting the increasing demand for green energy in the

country. The resource does not only increase power supply throughout the country but also

lowers carbon emissions thus protecting the environment and improving people’s quality of

life (Sunderland, et al., 2013). It is estimated that by 2050, wind energy will decrease carbon

dioxide emissions by between 400 and 450 million tonnes (Sustainable Energy Authority of

Ireland, (n.d.)). The current wind power output of Ireland is approximately 2,826 MW. Just

like other countries where wind energy investments have been increasing every year and

projected to continue increasing (Krohn, et al., 2009), Ireland is also investing significantly in

wind farms.

Successful implementation of wind farm projects relies heavily on the precision of

wind resource mapping. Ireland is one of the countries with affluent wind resource hence

most of the wind farm projects are feasible. However, this does not mean that any wind farm

project can be successful in the country. It requires proper planning, consultation, accurate

collection of relevant data, benchmarking with past similar projects and application of

available technologies and other strategies to lower costs.

There are numerous existing wind farm projects in Ireland, both onshore and offshore.

Figure 1 below shows existing wind farms in Ireland. This is mainly because the country has

very large wind resource and many parts have average wind speeds. In 2016, wind energy

accounted for 85% of renewable electricity in Ireland and 20.9% of the country’s total power

demand (Sustainable Energy Authority of Ireland , 2017). In 2017, the percentage of total

electricity demand accounted for by wind energy rose to 24% and the highest percentage

increase in installation of wind energy capacity was also recorded in the same year

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 5

(O'Sullivan, 2018). By 2020, it is projected that 40% of Ireland’s total power demand will be

provided by renewable energy (Irish Farmers' Association, 2013); (Sustainable Energy

Authority of Ireland, 2011). The government has formulated policies, including incentives

and purchasing of wind energy produced by individuals or private companies at higher prices,

which encourage wind energy investments from both public and private investors so as to

improve electricity supply and abate carbon dioxide emissions (Howley & Holland, 2016).

Figure 1: Wind farms in Ireland

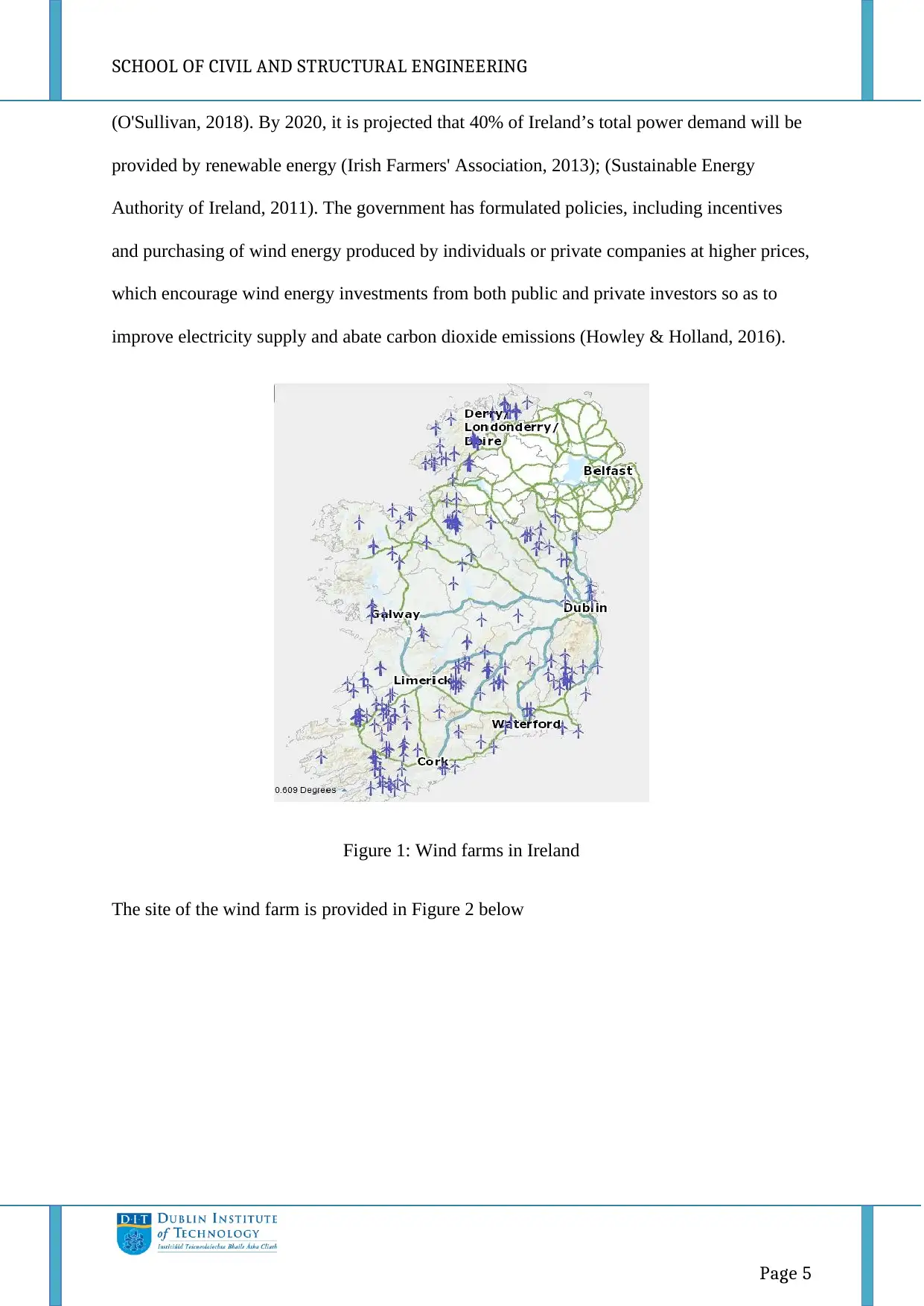

The site of the wind farm is provided in Figure 2 below

Page 5

(O'Sullivan, 2018). By 2020, it is projected that 40% of Ireland’s total power demand will be

provided by renewable energy (Irish Farmers' Association, 2013); (Sustainable Energy

Authority of Ireland, 2011). The government has formulated policies, including incentives

and purchasing of wind energy produced by individuals or private companies at higher prices,

which encourage wind energy investments from both public and private investors so as to

improve electricity supply and abate carbon dioxide emissions (Howley & Holland, 2016).

Figure 1: Wind farms in Ireland

The site of the wind farm is provided in Figure 2 below

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 6

Figure 2: Wind farm site

The aim of this study is to investigate the economic feasibility of a proposed wind

farm project in Intack, County of Wicklow, Ireland. This is done by developing a

mathematical model (energy model) of wind power output generated by the wind farm and

another model (economic model) for determining NPV of the project. The economic model

developed is used to simulate economic performance of the project under different scenarios.

Additionally, the greenhouse gas emissions that will be prevented by this project are

quantified and assessed.

2. MODELS

The model developed in this project is a mathematical model showing the relationship

between input and output variables of the wind farm. The main mathematical model is the

one showing the relationship between economic variables of the wind farm. There is also the

model of wind power output, which is dependent on different input variables including power

coefficient, wind speed, density of air and rotor swept area.

Page 6

Figure 2: Wind farm site

The aim of this study is to investigate the economic feasibility of a proposed wind

farm project in Intack, County of Wicklow, Ireland. This is done by developing a

mathematical model (energy model) of wind power output generated by the wind farm and

another model (economic model) for determining NPV of the project. The economic model

developed is used to simulate economic performance of the project under different scenarios.

Additionally, the greenhouse gas emissions that will be prevented by this project are

quantified and assessed.

2. MODELS

The model developed in this project is a mathematical model showing the relationship

between input and output variables of the wind farm. The main mathematical model is the

one showing the relationship between economic variables of the wind farm. There is also the

model of wind power output, which is dependent on different input variables including power

coefficient, wind speed, density of air and rotor swept area.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 7

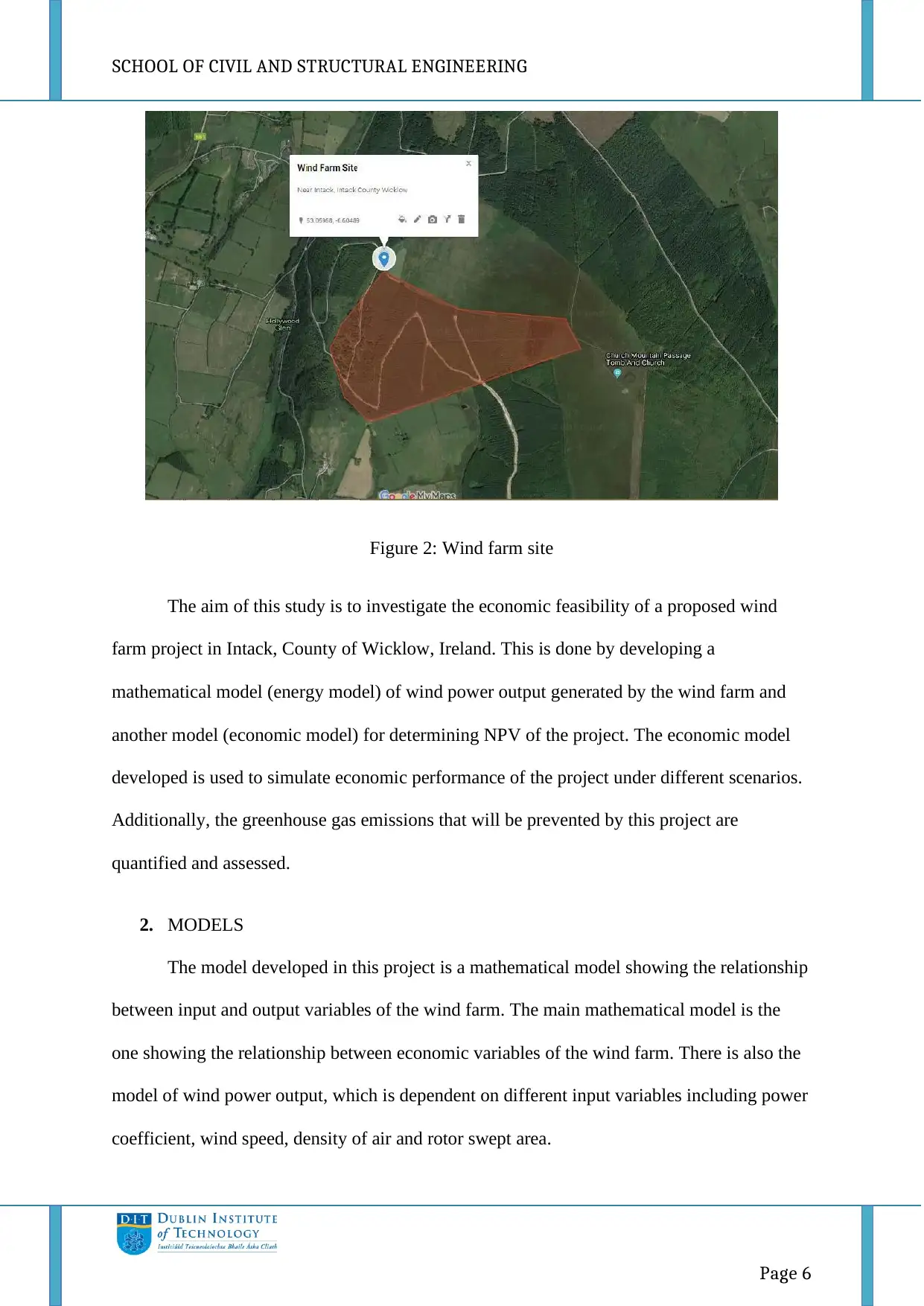

2.1. Flow model diagram

Figure 3 below is the flow model diagram of the wind farm. The wind turbines convert

kinetic energy from the wind into mechanical or rotational energy. The coupling and gear

system steps up the speed of the mechanical energy and transfers to the rotor of the generator.

The generator converts mechanical energy and electrical energy (electricity). The controller

detects the wind speed, wind direction, temperature and output from the generator then

initiates appropriate signals to control them. The transformer manipulates power voltage level

for safe transmission. The substation increases or reduces voltage before the electricity is

connected to the power grid. The power grid distributes the electricity to the final consumers.

Figure 3: Flow model diagram

2.2. Wind Power Output model

Intack, County of Wicklow is one of the regions with average wind speeds in Ireland. The

average windiest, windier and calmer months of the year in Wicklow records average wind

speeds of 18.1 mph (8.09 m/s), 14.5 mph (6.48 m/s) and 10.8 mph (4.83 m/s) respectively

(Weather Spark, 2018). It is important to note that these wind speeds are the average of the

entire Wicklow region. The wind speeds vary from one season to another. Considering that

the onshore site where the wind farm in this project is planned to be constructed is along the

coastline bordering the Irish Sea, the wind speed in the region is definitely higher than the

Wind Wind

turbines

Coupling and gear

system Generator Transformer

SubstationPower grid

Controller

Consumers

Page 7

2.1. Flow model diagram

Figure 3 below is the flow model diagram of the wind farm. The wind turbines convert

kinetic energy from the wind into mechanical or rotational energy. The coupling and gear

system steps up the speed of the mechanical energy and transfers to the rotor of the generator.

The generator converts mechanical energy and electrical energy (electricity). The controller

detects the wind speed, wind direction, temperature and output from the generator then

initiates appropriate signals to control them. The transformer manipulates power voltage level

for safe transmission. The substation increases or reduces voltage before the electricity is

connected to the power grid. The power grid distributes the electricity to the final consumers.

Figure 3: Flow model diagram

2.2. Wind Power Output model

Intack, County of Wicklow is one of the regions with average wind speeds in Ireland. The

average windiest, windier and calmer months of the year in Wicklow records average wind

speeds of 18.1 mph (8.09 m/s), 14.5 mph (6.48 m/s) and 10.8 mph (4.83 m/s) respectively

(Weather Spark, 2018). It is important to note that these wind speeds are the average of the

entire Wicklow region. The wind speeds vary from one season to another. Considering that

the onshore site where the wind farm in this project is planned to be constructed is along the

coastline bordering the Irish Sea, the wind speed in the region is definitely higher than the

Wind Wind

turbines

Coupling and gear

system Generator Transformer

SubstationPower grid

Controller

Consumers

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 8

average calmer, windier and windiest values. Therefore the wind power output in this project

is calculated using average wind speed of 18.5 mph (8.26 m/s). This value is obtained from

the IEA Wind website (IEA Wind, (n.d.)).

The amount of power output that a turbine can generate is calculated using equation 1 below

(Rozenblat, 2012)

𝑃 = 1

2 𝐶𝑝𝜌𝐴𝑉3……………………………………………………….. (1)

Where P = power output in watts (W), Cp = efficiency of the turbine, ρ = density of air in

kg/m3, A = area swept by turbine rotor in m2, and V = wind speed in m/s (REUK, (n.d.)).

The mathematical model presented in equation 1 above shows that wind power output is

directly proportional to air density, swept area of the wind turbine’s rotor, power coefficient

and cube of wind speed (Marimuthu & Kirubakaran, 2014).

The power coefficient is included in the equation because a turbine cannot generate

100% of the wind energy due to inefficiencies (Manyonge, et al., 2012); (Soriano, et al.,

2013). Equation 1 above is the mathematical model of wind power output. This model can be

used to calculate wind power generated by a turbine at different wind conditions or the power

generated by different sizes of turbines.

The turbine that has been selected for this project is Acciona AW-100/3000. The photo of the

turbine is as shown in Figure 4 below.

Page 8

average calmer, windier and windiest values. Therefore the wind power output in this project

is calculated using average wind speed of 18.5 mph (8.26 m/s). This value is obtained from

the IEA Wind website (IEA Wind, (n.d.)).

The amount of power output that a turbine can generate is calculated using equation 1 below

(Rozenblat, 2012)

𝑃 = 1

2 𝐶𝑝𝜌𝐴𝑉3……………………………………………………….. (1)

Where P = power output in watts (W), Cp = efficiency of the turbine, ρ = density of air in

kg/m3, A = area swept by turbine rotor in m2, and V = wind speed in m/s (REUK, (n.d.)).

The mathematical model presented in equation 1 above shows that wind power output is

directly proportional to air density, swept area of the wind turbine’s rotor, power coefficient

and cube of wind speed (Marimuthu & Kirubakaran, 2014).

The power coefficient is included in the equation because a turbine cannot generate

100% of the wind energy due to inefficiencies (Manyonge, et al., 2012); (Soriano, et al.,

2013). Equation 1 above is the mathematical model of wind power output. This model can be

used to calculate wind power generated by a turbine at different wind conditions or the power

generated by different sizes of turbines.

The turbine that has been selected for this project is Acciona AW-100/3000. The photo of the

turbine is as shown in Figure 4 below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 9

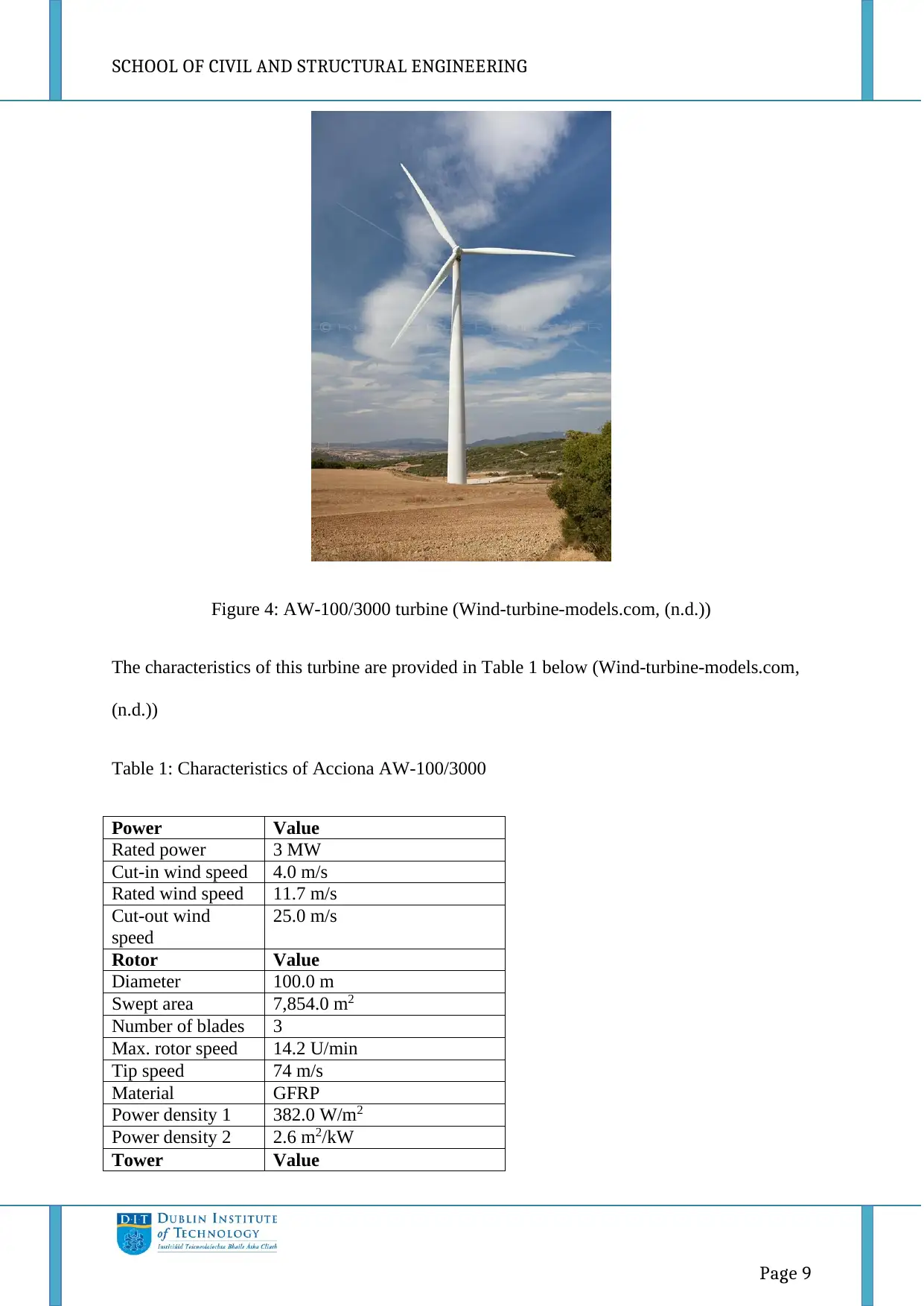

Figure 4: AW-100/3000 turbine (Wind-turbine-models.com, (n.d.))

The characteristics of this turbine are provided in Table 1 below (Wind-turbine-models.com,

(n.d.))

Table 1: Characteristics of Acciona AW-100/3000

Power Value

Rated power 3 MW

Cut-in wind speed 4.0 m/s

Rated wind speed 11.7 m/s

Cut-out wind

speed

25.0 m/s

Rotor Value

Diameter 100.0 m

Swept area 7,854.0 m2

Number of blades 3

Max. rotor speed 14.2 U/min

Tip speed 74 m/s

Material GFRP

Power density 1 382.0 W/m2

Power density 2 2.6 m2/kW

Tower Value

Page 9

Figure 4: AW-100/3000 turbine (Wind-turbine-models.com, (n.d.))

The characteristics of this turbine are provided in Table 1 below (Wind-turbine-models.com,

(n.d.))

Table 1: Characteristics of Acciona AW-100/3000

Power Value

Rated power 3 MW

Cut-in wind speed 4.0 m/s

Rated wind speed 11.7 m/s

Cut-out wind

speed

25.0 m/s

Rotor Value

Diameter 100.0 m

Swept area 7,854.0 m2

Number of blades 3

Max. rotor speed 14.2 U/min

Tip speed 74 m/s

Material GFRP

Power density 1 382.0 W/m2

Power density 2 2.6 m2/kW

Tower Value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 10

Rotor swept area, A = πr2 = π x 502 = 7,854 m2

Density of air, ρ = 1.25 kg/m3

Velocity, v = 8.26 m/s

Power coefficient, Cp = it usually ranges from 25% to 45% hence the chosen value is 35% =

0.35

𝑃 = 1

2 𝐶𝑝𝜌𝐴𝑉3 = 1

2 𝑥 0.35 𝑥 1.25 𝑥 7854 𝑥 8.263 = 𝟎. 𝟗𝟕 𝑴𝑾

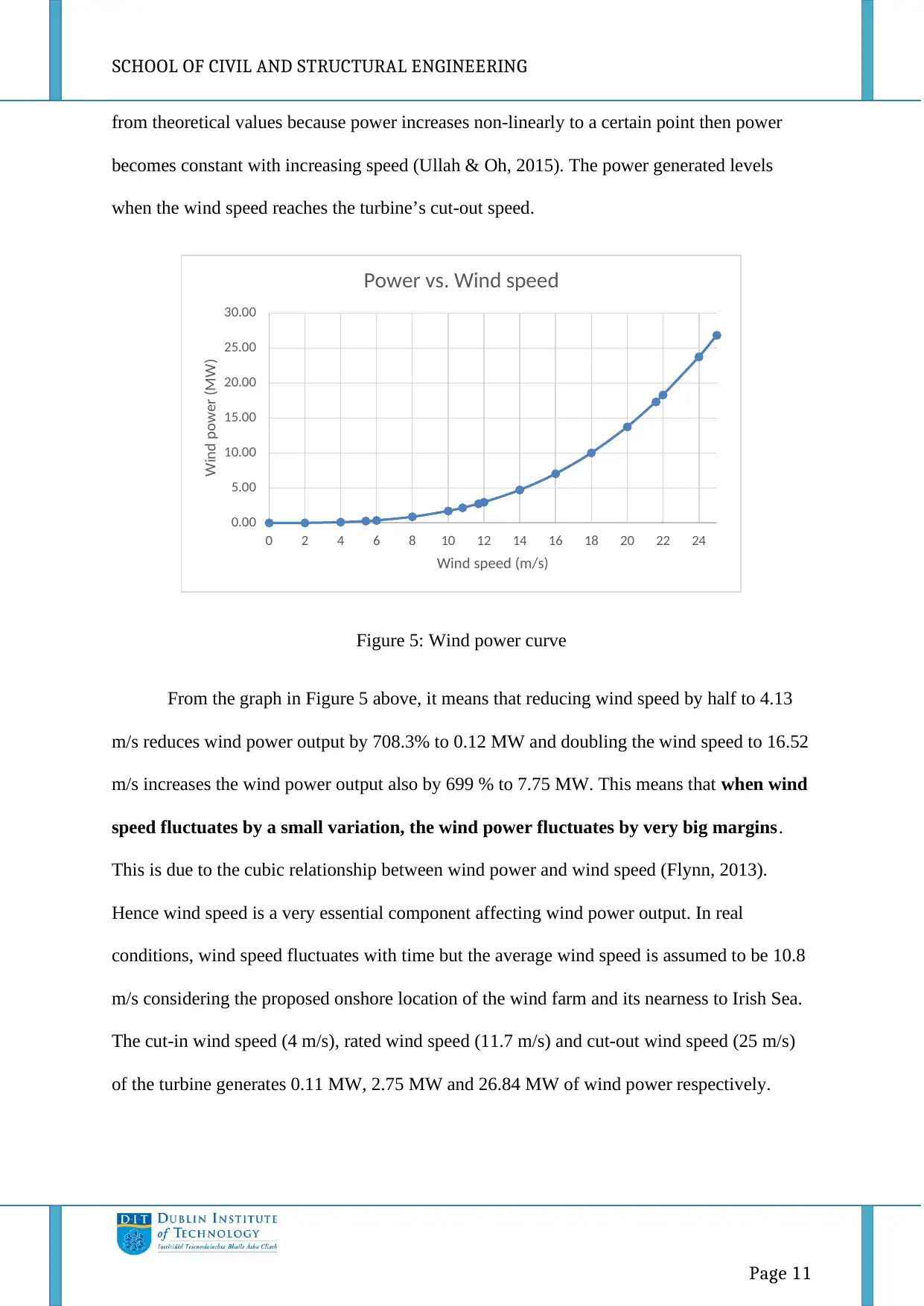

The mathematical model provided in Equation 1 above is used to simulate wind

power output from the wind turbine at different wind speeds. This is so as to determine the

effect of wind fluctuation on wind power generated. The model also helps in determining the

minimum wind power output that the turbine can produce at cut-in wind speed, rated wind

speed and cut-out wind speed. Generally, the turbine cannot produce power exceeding the

one generated at cut-out wind speed. Figure 5 below shows the relationship between wind

power output and wind speed of the turbine when all other parameters (power coefficient,

diameter of the turbine and density of air) remain constant. This graph has been drawn

through simulation of the mathematical model provided in Equation 1 using different wind

speeds. The graph in Figure 5 below is similar to a typical power-wind speed graph drawn

Type Concrete

Shape Conical

Hub height 100/120 m

Corrosion

protection

Painted

Weight Value

Rotor 66.0 tonnes

Hub 32.0 tonnes

Nacelle 118.0 tonnes

Max. tower 1,100.0 tonnes

Total weight 1,284.0 tonnes

Manufacturer Acciona Energy S.A. from

Spain

Page 10

Rotor swept area, A = πr2 = π x 502 = 7,854 m2

Density of air, ρ = 1.25 kg/m3

Velocity, v = 8.26 m/s

Power coefficient, Cp = it usually ranges from 25% to 45% hence the chosen value is 35% =

0.35

𝑃 = 1

2 𝐶𝑝𝜌𝐴𝑉3 = 1

2 𝑥 0.35 𝑥 1.25 𝑥 7854 𝑥 8.263 = 𝟎. 𝟗𝟕 𝑴𝑾

The mathematical model provided in Equation 1 above is used to simulate wind

power output from the wind turbine at different wind speeds. This is so as to determine the

effect of wind fluctuation on wind power generated. The model also helps in determining the

minimum wind power output that the turbine can produce at cut-in wind speed, rated wind

speed and cut-out wind speed. Generally, the turbine cannot produce power exceeding the

one generated at cut-out wind speed. Figure 5 below shows the relationship between wind

power output and wind speed of the turbine when all other parameters (power coefficient,

diameter of the turbine and density of air) remain constant. This graph has been drawn

through simulation of the mathematical model provided in Equation 1 using different wind

speeds. The graph in Figure 5 below is similar to a typical power-wind speed graph drawn

Type Concrete

Shape Conical

Hub height 100/120 m

Corrosion

protection

Painted

Weight Value

Rotor 66.0 tonnes

Hub 32.0 tonnes

Nacelle 118.0 tonnes

Max. tower 1,100.0 tonnes

Total weight 1,284.0 tonnes

Manufacturer Acciona Energy S.A. from

Spain

SCHOOL OF CIVIL AND STRUCTURAL ENGINEERING

Page 11

from theoretical values because power increases non-linearly to a certain point then power

becomes constant with increasing speed (Ullah & Oh, 2015). The power generated levels

when the wind speed reaches the turbine’s cut-out speed.

Figure 5: Wind power curve

From the graph in Figure 5 above, it means that reducing wind speed by half to 4.13

m/s reduces wind power output by 708.3% to 0.12 MW and doubling the wind speed to 16.52

m/s increases the wind power output also by 699 % to 7.75 MW. This means that when wind

speed fluctuates by a small variation, the wind power fluctuates by very big margins.

This is due to the cubic relationship between wind power and wind speed (Flynn, 2013).

Hence wind speed is a very essential component affecting wind power output. In real

conditions, wind speed fluctuates with time but the average wind speed is assumed to be 10.8

m/s considering the proposed onshore location of the wind farm and its nearness to Irish Sea.

The cut-in wind speed (4 m/s), rated wind speed (11.7 m/s) and cut-out wind speed (25 m/s)

of the turbine generates 0.11 MW, 2.75 MW and 26.84 MW of wind power respectively.

0.00

5.00

10.00

15.00

20.00

25.00

30.00

0 2 4 6 8 10 12 14 16 18 20 22 24

Wind power (MW)

Wind speed (m/s)

Power vs. Wind speed

Page 11

from theoretical values because power increases non-linearly to a certain point then power

becomes constant with increasing speed (Ullah & Oh, 2015). The power generated levels

when the wind speed reaches the turbine’s cut-out speed.

Figure 5: Wind power curve

From the graph in Figure 5 above, it means that reducing wind speed by half to 4.13

m/s reduces wind power output by 708.3% to 0.12 MW and doubling the wind speed to 16.52

m/s increases the wind power output also by 699 % to 7.75 MW. This means that when wind

speed fluctuates by a small variation, the wind power fluctuates by very big margins.

This is due to the cubic relationship between wind power and wind speed (Flynn, 2013).

Hence wind speed is a very essential component affecting wind power output. In real

conditions, wind speed fluctuates with time but the average wind speed is assumed to be 10.8

m/s considering the proposed onshore location of the wind farm and its nearness to Irish Sea.

The cut-in wind speed (4 m/s), rated wind speed (11.7 m/s) and cut-out wind speed (25 m/s)

of the turbine generates 0.11 MW, 2.75 MW and 26.84 MW of wind power respectively.

0.00

5.00

10.00

15.00

20.00

25.00

30.00

0 2 4 6 8 10 12 14 16 18 20 22 24

Wind power (MW)

Wind speed (m/s)

Power vs. Wind speed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 54

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.