Compliance of Woodside Petroleum with AASB Conceptual Framework

VerifiedAdded on 2023/06/12

|15

|2336

|63

AI Summary

The report analyses the compliance of Woodside Petroleum with the AASB conceptual framework for financial reporting. It discusses the objectives, recognition criteria, fundamental and enhancing qualitative characteristics of the framework. The report concludes that Woodside Petroleum complies with all the required standards and principles of AASB conceptual framework.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s Note

Contemporary Issues in Accounting

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1CONTEMPORARY ISSUES IN ACCOUNTING

Abstract

The aim of the report is to analyse the compliance of Woodside Petroleum with the AASB

conceptual framework. It can be observed that Woodside Petroleum complies with all the

required standards and principles of AASB conceptual framework for the purpose of their

financial reporting.

Abstract

The aim of the report is to analyse the compliance of Woodside Petroleum with the AASB

conceptual framework. It can be observed that Woodside Petroleum complies with all the

required standards and principles of AASB conceptual framework for the purpose of their

financial reporting.

2CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Conceptual Framework Objectives..................................................................................................3

Recognition Criteria.........................................................................................................................8

Fundamental Qualitative Characteristics.......................................................................................10

Enhancing Qualitative Characteristics...........................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Table of Contents

Introduction......................................................................................................................................3

Conceptual Framework Objectives..................................................................................................3

Recognition Criteria.........................................................................................................................8

Fundamental Qualitative Characteristics.......................................................................................10

Enhancing Qualitative Characteristics...........................................................................................11

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

3CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The main purpose of this report is to analyse and evaluate different financial standards

and principles of conceptual framework for accounting. In the recent years, business

organizations all over the work is facing different types of issues related to their financial

accounting due to the non-compliance with required accounting standards and principles. In

order to avoid these issues, business entities are needed to follow the regulations and standards of

accounting conceptual framework. In Australia, the Australian Accounting Standard Board

(AASB) has provided the necessary financial standards and regulations through the release of

accounting conceptual framework with the assistance of International Accounting Standard

Board (IASB) (aasb.gov.au 2018). All the business entities listed under Australian Stock

Exchange (ASX) must comply with these regulations and standards for the accurate preparation

and presentation of financial reports. For the purpose of this study, Woodside Petroleum Limited

is taken into consideration. Woodside Petroleum is a major Australian oil and gas company

having global presence and the company is renowned for their world-class capabilities. It need to

be mentioned that the company is listed under ASX in the name of ‘WPL’ (woodside.com.au

2018).

Conceptual Framework Objectives

As per the above discussion, AASB and IASB have developed the accounting conceptual

framework for bringing accuracy in the process of financial reporting for the Australian business

entities. In order to achieve this objective, AASB has introduced three objectives of its

conceptual framework that the companies are required to achieve through their financial

reporting. They are mentioned below:

Introduction

The main purpose of this report is to analyse and evaluate different financial standards

and principles of conceptual framework for accounting. In the recent years, business

organizations all over the work is facing different types of issues related to their financial

accounting due to the non-compliance with required accounting standards and principles. In

order to avoid these issues, business entities are needed to follow the regulations and standards of

accounting conceptual framework. In Australia, the Australian Accounting Standard Board

(AASB) has provided the necessary financial standards and regulations through the release of

accounting conceptual framework with the assistance of International Accounting Standard

Board (IASB) (aasb.gov.au 2018). All the business entities listed under Australian Stock

Exchange (ASX) must comply with these regulations and standards for the accurate preparation

and presentation of financial reports. For the purpose of this study, Woodside Petroleum Limited

is taken into consideration. Woodside Petroleum is a major Australian oil and gas company

having global presence and the company is renowned for their world-class capabilities. It need to

be mentioned that the company is listed under ASX in the name of ‘WPL’ (woodside.com.au

2018).

Conceptual Framework Objectives

As per the above discussion, AASB and IASB have developed the accounting conceptual

framework for bringing accuracy in the process of financial reporting for the Australian business

entities. In order to achieve this objective, AASB has introduced three objectives of its

conceptual framework that the companies are required to achieve through their financial

reporting. They are mentioned below:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4CONTEMPORARY ISSUES IN ACCOUNTING

1. It is the objective of the conceptual framework of AASB to provide the users of financial

information with all the necessary information related with the economic resources of the

business entities so that they can judge the financial standing of those organizations

(aasb.gov.au 2018).

2. It is the second objective of the AASB conceptual framework to provide the users with

all the required information about the necessary economic phenomena of the business

entities so that they can judge the financial performance of those companies over the

years (aasb.gov.au 2018).

3. It is the third objective of AASB conceptual framework to provide the users with the

information about the necessary aspects for their determination of the change in financial

performance of the business entities over the years (aasb.gov.au 2018).

Now, it is required to determine whether Woodside Petroleum has become able to achieve all

these three objectives of AASB conceptual framework through their financial reporting.

1. It is the objective of the conceptual framework of AASB to provide the users of financial

information with all the necessary information related with the economic resources of the

business entities so that they can judge the financial standing of those organizations

(aasb.gov.au 2018).

2. It is the second objective of the AASB conceptual framework to provide the users with

all the required information about the necessary economic phenomena of the business

entities so that they can judge the financial performance of those companies over the

years (aasb.gov.au 2018).

3. It is the third objective of AASB conceptual framework to provide the users with the

information about the necessary aspects for their determination of the change in financial

performance of the business entities over the years (aasb.gov.au 2018).

Now, it is required to determine whether Woodside Petroleum has become able to achieve all

these three objectives of AASB conceptual framework through their financial reporting.

5CONTEMPORARY ISSUES IN ACCOUNTING

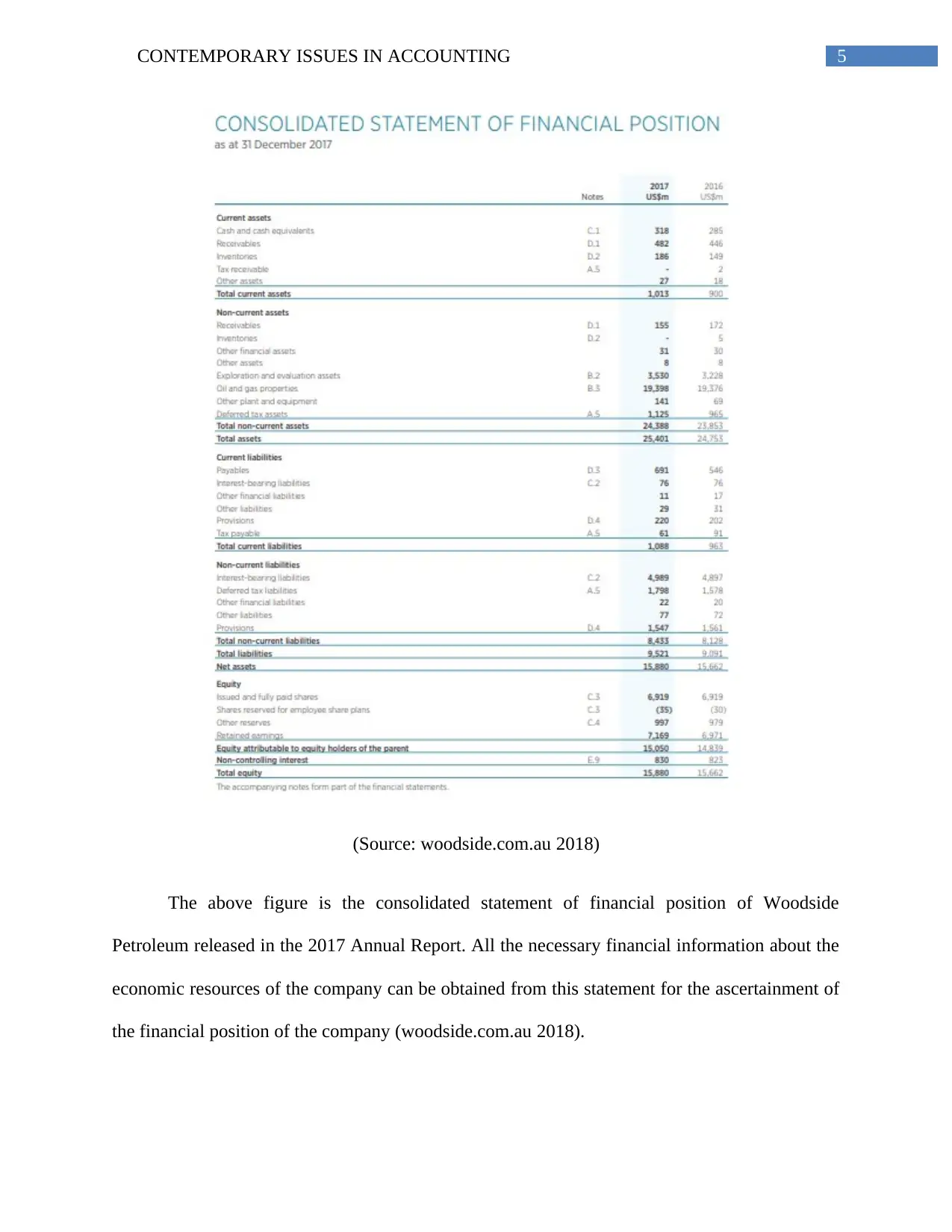

(Source: woodside.com.au 2018)

The above figure is the consolidated statement of financial position of Woodside

Petroleum released in the 2017 Annual Report. All the necessary financial information about the

economic resources of the company can be obtained from this statement for the ascertainment of

the financial position of the company (woodside.com.au 2018).

(Source: woodside.com.au 2018)

The above figure is the consolidated statement of financial position of Woodside

Petroleum released in the 2017 Annual Report. All the necessary financial information about the

economic resources of the company can be obtained from this statement for the ascertainment of

the financial position of the company (woodside.com.au 2018).

6CONTEMPORARY ISSUES IN ACCOUNTING

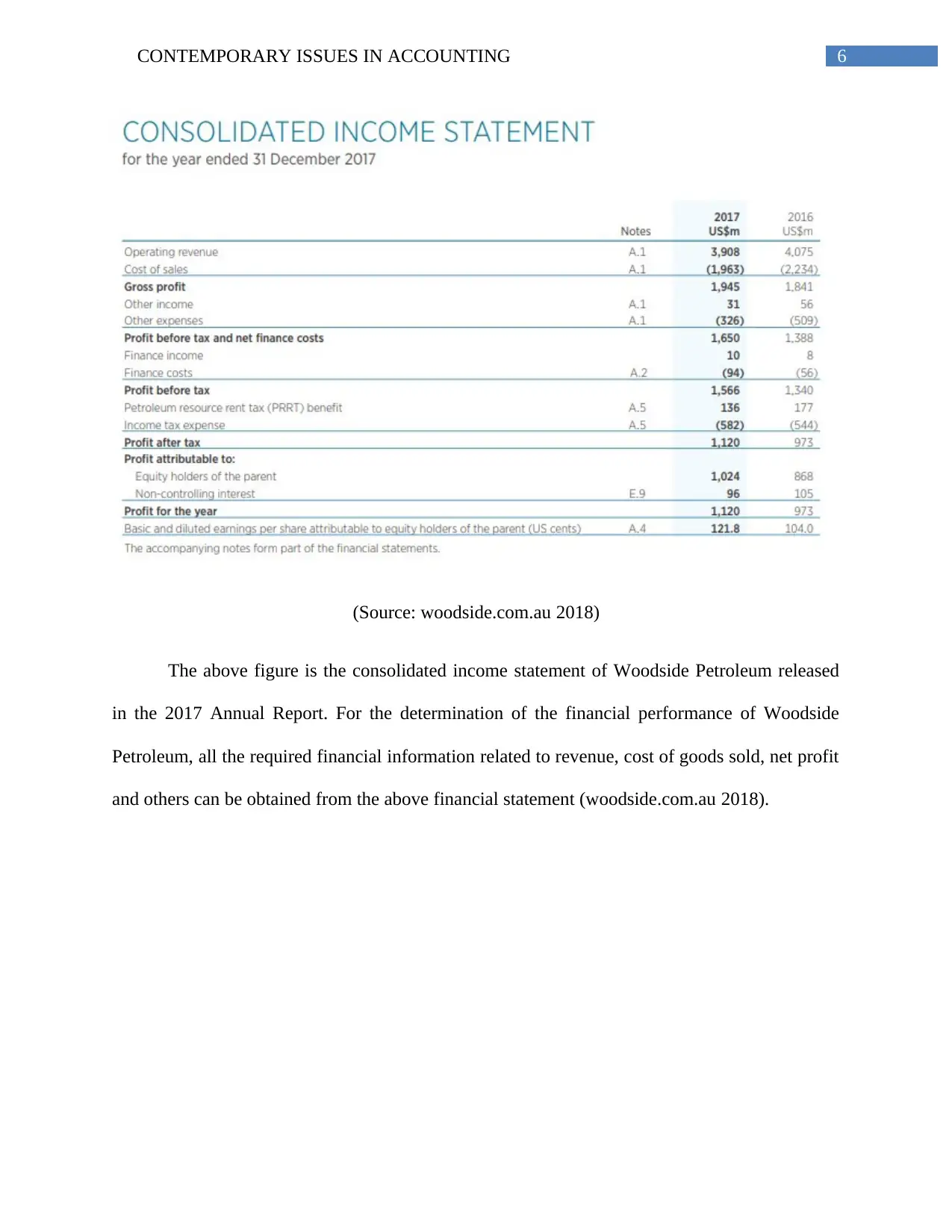

(Source: woodside.com.au 2018)

The above figure is the consolidated income statement of Woodside Petroleum released

in the 2017 Annual Report. For the determination of the financial performance of Woodside

Petroleum, all the required financial information related to revenue, cost of goods sold, net profit

and others can be obtained from the above financial statement (woodside.com.au 2018).

(Source: woodside.com.au 2018)

The above figure is the consolidated income statement of Woodside Petroleum released

in the 2017 Annual Report. For the determination of the financial performance of Woodside

Petroleum, all the required financial information related to revenue, cost of goods sold, net profit

and others can be obtained from the above financial statement (woodside.com.au 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

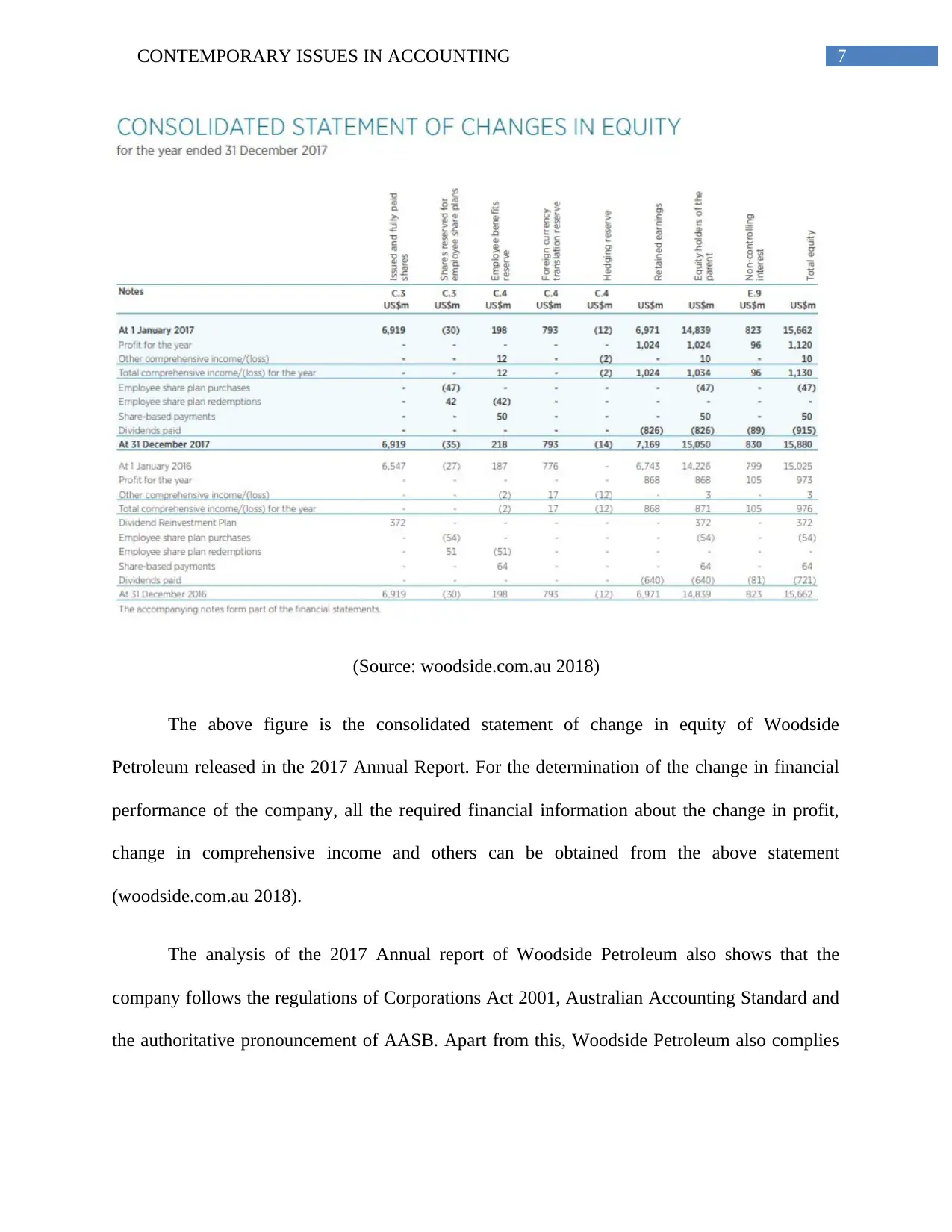

(Source: woodside.com.au 2018)

The above figure is the consolidated statement of change in equity of Woodside

Petroleum released in the 2017 Annual Report. For the determination of the change in financial

performance of the company, all the required financial information about the change in profit,

change in comprehensive income and others can be obtained from the above statement

(woodside.com.au 2018).

The analysis of the 2017 Annual report of Woodside Petroleum also shows that the

company follows the regulations of Corporations Act 2001, Australian Accounting Standard and

the authoritative pronouncement of AASB. Apart from this, Woodside Petroleum also complies

(Source: woodside.com.au 2018)

The above figure is the consolidated statement of change in equity of Woodside

Petroleum released in the 2017 Annual Report. For the determination of the change in financial

performance of the company, all the required financial information about the change in profit,

change in comprehensive income and others can be obtained from the above statement

(woodside.com.au 2018).

The analysis of the 2017 Annual report of Woodside Petroleum also shows that the

company follows the regulations of Corporations Act 2001, Australian Accounting Standard and

the authoritative pronouncement of AASB. Apart from this, Woodside Petroleum also complies

8CONTEMPORARY ISSUES IN ACCOUNTING

with the standards of IASB and International Financial Reporting Standards (IFRS) for the

purpose of their financial reporting (woodside.com.au 2018).

Recognition Criteria

Apart from the above-discussed objectives, the conceptual framework of AASB has

provided the ASX listed companies with some criteria for the recognition of the major financial

elements and they are assets, liabilities, equity, revenue and expenses. All the companies are

required to comply with these recognition criteria. Now, it is required to determine whether

Woodside Petroleum complies with all the recognition criteria or not.

Asset: For the recognition of assets, entities are required to follow these two criteria:

It is probable that the business organization will receive the future economic benefits

embodied with the asserts, and

The cost of the assets can be measured reliably (aasb.gov.au 2018).

Woodside Petroleum has different kinds of assets. According to AASB 116, the company

measures their fixed assets like oil and property, property, plant and equipment at cost value

after deducting accumulated depreciation and impairment costs. The amount of trade receivables

is recognized are recognized at fair value and measured at amortized costs. In addition,

inventories are also recognized at lower of cost and net realizable value. Thus, it can be seen that

the costs of the assets are measurable and the company becomes benefitted from these assets

(woodside.com.au 2018).

Liability: Liabilities are recognized in case of the fulfilment of the following criteria:

with the standards of IASB and International Financial Reporting Standards (IFRS) for the

purpose of their financial reporting (woodside.com.au 2018).

Recognition Criteria

Apart from the above-discussed objectives, the conceptual framework of AASB has

provided the ASX listed companies with some criteria for the recognition of the major financial

elements and they are assets, liabilities, equity, revenue and expenses. All the companies are

required to comply with these recognition criteria. Now, it is required to determine whether

Woodside Petroleum complies with all the recognition criteria or not.

Asset: For the recognition of assets, entities are required to follow these two criteria:

It is probable that the business organization will receive the future economic benefits

embodied with the asserts, and

The cost of the assets can be measured reliably (aasb.gov.au 2018).

Woodside Petroleum has different kinds of assets. According to AASB 116, the company

measures their fixed assets like oil and property, property, plant and equipment at cost value

after deducting accumulated depreciation and impairment costs. The amount of trade receivables

is recognized are recognized at fair value and measured at amortized costs. In addition,

inventories are also recognized at lower of cost and net realizable value. Thus, it can be seen that

the costs of the assets are measurable and the company becomes benefitted from these assets

(woodside.com.au 2018).

Liability: Liabilities are recognized in case of the fulfilment of the following criteria:

9CONTEMPORARY ISSUES IN ACCOUNTING

It is probable that the business organization will have to sacrifice the future economic

benefits embodied with the liabilities, and

The cost of the liabilities can be measured reliably (aasb.gov.au 2018).

The presence of different liabilities can be seen in Woodside Petroleum. The company

measures the value of trade payables at amortized when goods and services are received and the

company has to repay them at fair value. Provisions are recognized in case the company has any

present financial obligation due to the occurrence of any past events. Woodside Petroleum has to

pay all of their borrowings in the future date and they are recognized at fair value after deducting

transaction costs (woodside.com.au 2018). Thus, it can be observed that Woodside Petroleum

has to sacrifice their future benefits as the company has to pay their liabilities.

Equity: At the time of the recognition of equity, the business entities are required to follow the

same recognition criteria as the recognition of assets and liabilities (aasb.gov.au 2018).

In Woodside Petroleum, ordinary shares are classified as equity and the company

measures them at the value of consideration received. In the share capital, the cost to issue the

shares is shown as deduction (woodside.com.au 2018). Thus, it can be seen that the company

will be beneficial from the issues of shares and the cost of them can be measured.

Revenue: Business organizations recognize their revenue in the following cases:

It is probable that he inflow of the economic future benefits will be occurred to the favour

of the company, and

The outflow of the future benefits can be measured reliably (aasb.gov.au 2018).

It is probable that the business organization will have to sacrifice the future economic

benefits embodied with the liabilities, and

The cost of the liabilities can be measured reliably (aasb.gov.au 2018).

The presence of different liabilities can be seen in Woodside Petroleum. The company

measures the value of trade payables at amortized when goods and services are received and the

company has to repay them at fair value. Provisions are recognized in case the company has any

present financial obligation due to the occurrence of any past events. Woodside Petroleum has to

pay all of their borrowings in the future date and they are recognized at fair value after deducting

transaction costs (woodside.com.au 2018). Thus, it can be observed that Woodside Petroleum

has to sacrifice their future benefits as the company has to pay their liabilities.

Equity: At the time of the recognition of equity, the business entities are required to follow the

same recognition criteria as the recognition of assets and liabilities (aasb.gov.au 2018).

In Woodside Petroleum, ordinary shares are classified as equity and the company

measures them at the value of consideration received. In the share capital, the cost to issue the

shares is shown as deduction (woodside.com.au 2018). Thus, it can be seen that the company

will be beneficial from the issues of shares and the cost of them can be measured.

Revenue: Business organizations recognize their revenue in the following cases:

It is probable that he inflow of the economic future benefits will be occurred to the favour

of the company, and

The outflow of the future benefits can be measured reliably (aasb.gov.au 2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10CONTEMPORARY ISSUES IN ACCOUNTING

Woodside Petroleum recognizes their business revenue at the fair value of the considerable

received or receivable to the extent that the future economic benefits will be flown to the

company (woodside.com.au 2018).

Expenses: Business organizations recognize their expenses in the following cases:

It is probable that he outflow of the economic future benefits will be occurred against the

company, and

The consumption or loss in economic benefit can be measured reliably (aasb.gov.au

2018).

Woodside Petroleum recognizes the expenses of the business at the time of their occurrence

and they are measured at fair value (woodside.com.au 2018).

Fundamental Qualitative Characteristics

According to the conceptual framework of AASB, the financial statements of the

companies require to possess two fundamental qualitative characteristics. They are Relevance

and Faithful Representation:

Relevance: With the help of relevant financial information, the users of financial information

can make effective investment decisions (Barth, 2013). From the earlier discussion, it can be

seen that Woodside Petroleum releases all the financial statements trough the later annual report

so that the users can acquire the relevant financial information (woodside.com.au 2018).

Faithful Representation: Faithful representation ensures the correct representation of the values

of the economic phenomena of the companies (Henderson et al. 2015). From the auditor report

of Woodside Petroleum, it can be seen that the company has complied with all the required

Woodside Petroleum recognizes their business revenue at the fair value of the considerable

received or receivable to the extent that the future economic benefits will be flown to the

company (woodside.com.au 2018).

Expenses: Business organizations recognize their expenses in the following cases:

It is probable that he outflow of the economic future benefits will be occurred against the

company, and

The consumption or loss in economic benefit can be measured reliably (aasb.gov.au

2018).

Woodside Petroleum recognizes the expenses of the business at the time of their occurrence

and they are measured at fair value (woodside.com.au 2018).

Fundamental Qualitative Characteristics

According to the conceptual framework of AASB, the financial statements of the

companies require to possess two fundamental qualitative characteristics. They are Relevance

and Faithful Representation:

Relevance: With the help of relevant financial information, the users of financial information

can make effective investment decisions (Barth, 2013). From the earlier discussion, it can be

seen that Woodside Petroleum releases all the financial statements trough the later annual report

so that the users can acquire the relevant financial information (woodside.com.au 2018).

Faithful Representation: Faithful representation ensures the correct representation of the values

of the economic phenomena of the companies (Henderson et al. 2015). From the auditor report

of Woodside Petroleum, it can be seen that the company has complied with all the required

11CONTEMPORARY ISSUES IN ACCOUNTING

standards and regulations of Corporations Act 2001, Australian Accounting standard, AASB and

others that ensure the faithful representation of financial phenomena (woodside.com.au 2018).

Enhancing Qualitative Characteristics

Apart from fundamental characteristics, there are four enhancing qualitative

characteristics. They are Comparability, Verifiability, Timeliness and Understandability.

Comparability: It helps in the identification of similarities and differences in the financial

aspects of the companies (Luke 2016). The users of financial statements can compare the

financial information of Woodside Petroleum with the other companies by easily understand

them (woodside.com.au 2018).

Verifiability: Faithful representation helps the users in verifying the financial information of the

companies (Biondi and Lapsley 2014). As the financial statements of Woodside Petroleum are

faithfully presented, users can easily verify the information (woodside.com.au 2018).

Timeliness: It helps the users in getting required financial information at correct time (Birt,

Muthusamy and Bir 2017). The timely release of financial statements by Woodside Petroleum

helps the users in getting the required financial information at the correct time (woodside.com.au

2018).

Understandability: It helps the users in comprehending the financial treatments of the

companies (Limijaya 2017). With the help of reasonable financial knowledge, the users can

understand the financial information of Woodside Petroleum (woodside.com.au 2018).

standards and regulations of Corporations Act 2001, Australian Accounting standard, AASB and

others that ensure the faithful representation of financial phenomena (woodside.com.au 2018).

Enhancing Qualitative Characteristics

Apart from fundamental characteristics, there are four enhancing qualitative

characteristics. They are Comparability, Verifiability, Timeliness and Understandability.

Comparability: It helps in the identification of similarities and differences in the financial

aspects of the companies (Luke 2016). The users of financial statements can compare the

financial information of Woodside Petroleum with the other companies by easily understand

them (woodside.com.au 2018).

Verifiability: Faithful representation helps the users in verifying the financial information of the

companies (Biondi and Lapsley 2014). As the financial statements of Woodside Petroleum are

faithfully presented, users can easily verify the information (woodside.com.au 2018).

Timeliness: It helps the users in getting required financial information at correct time (Birt,

Muthusamy and Bir 2017). The timely release of financial statements by Woodside Petroleum

helps the users in getting the required financial information at the correct time (woodside.com.au

2018).

Understandability: It helps the users in comprehending the financial treatments of the

companies (Limijaya 2017). With the help of reasonable financial knowledge, the users can

understand the financial information of Woodside Petroleum (woodside.com.au 2018).

12CONTEMPORARY ISSUES IN ACCOUNTING

Conclusion

From the above discussion, it can be observed that Woodside Petroleum complies with all

the required standards and principles of Corporations Act 2001, AASB, Australian Accounting

Standard, IASB and IFRS. For the reason of all of these compliances, Woodside Petroleum does

not have to face any accounting issues. For this reason, it is required for all the ASX listed

companies to comply with the AASB conceptual framework to avoid the accounting issues.

Conclusion

From the above discussion, it can be observed that Woodside Petroleum complies with all

the required standards and principles of Corporations Act 2001, AASB, Australian Accounting

Standard, IASB and IFRS. For the reason of all of these compliances, Woodside Petroleum does

not have to face any accounting issues. For this reason, it is required for all the ASX listed

companies to comply with the AASB conceptual framework to avoid the accounting issues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13CONTEMPORARY ISSUES IN ACCOUNTING

References

Aasb.gov.au. (2018). Conceptual Framework for Financial Reporting. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed 19 Apr.

2018].

Aasb.gov.au. (2018). Definition and Recognition of the Elements of Financial Statements.

[online] Available at: http://www.aasb.gov.au/admin/file/content102/c3/SAC4_3-95.pdf

[Accessed 19 Apr. 2018].

Aasb.gov.au. (2018). Property, Plant and Equipment. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-04_COMPjun14_07-14.pdf

[Accessed 19 Apr. 2018].

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the heritage assets

problem. Qualitative Research in Accounting & Management, 11(2), pp.146-164.

Birt, J.L., Muthusamy, K. and Bir, P., 2017. XBRL and the qualitative characteristics of useful

financial information. Accounting Research Journal, 30(01), pp.107-126.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Limijaya, A., 2017. One Financial Reporting Global Language: The Ultimate Goal?. Jurnal Riset

Akuntansi dan Keuangan, 5(1), pp.1277-1292.

References

Aasb.gov.au. (2018). Conceptual Framework for Financial Reporting. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed 19 Apr.

2018].

Aasb.gov.au. (2018). Definition and Recognition of the Elements of Financial Statements.

[online] Available at: http://www.aasb.gov.au/admin/file/content102/c3/SAC4_3-95.pdf

[Accessed 19 Apr. 2018].

Aasb.gov.au. (2018). Property, Plant and Equipment. [online] Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB116_07-04_COMPjun14_07-14.pdf

[Accessed 19 Apr. 2018].

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the heritage assets

problem. Qualitative Research in Accounting & Management, 11(2), pp.146-164.

Birt, J.L., Muthusamy, K. and Bir, P., 2017. XBRL and the qualitative characteristics of useful

financial information. Accounting Research Journal, 30(01), pp.107-126.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Limijaya, A., 2017. One Financial Reporting Global Language: The Ultimate Goal?. Jurnal Riset

Akuntansi dan Keuangan, 5(1), pp.1277-1292.

14CONTEMPORARY ISSUES IN ACCOUNTING

Luke, B., 2016. Measuring and reporting on social performance: from numbers and narratives to

a useful reporting framework for social enterprises. Social and Environmental Accountability

Journal, 36(2), pp.103-123.

Woodside.com.au. (2018). About Us | Woodside Energy. [online] Available at:

http://www.woodside.com.au/About-Us/Pages/about-us.aspx [Accessed 19 Apr. 2018].

Woodsideannouncements.app.woodside. (2018). Annual Report 2017. [online] Available at:

https://woodsideannouncements.app.woodside/14.02.2018+Annual+Report+2017.pdf [Accessed

19 Apr. 2018].

Luke, B., 2016. Measuring and reporting on social performance: from numbers and narratives to

a useful reporting framework for social enterprises. Social and Environmental Accountability

Journal, 36(2), pp.103-123.

Woodside.com.au. (2018). About Us | Woodside Energy. [online] Available at:

http://www.woodside.com.au/About-Us/Pages/about-us.aspx [Accessed 19 Apr. 2018].

Woodsideannouncements.app.woodside. (2018). Annual Report 2017. [online] Available at:

https://woodsideannouncements.app.woodside/14.02.2018+Annual+Report+2017.pdf [Accessed

19 Apr. 2018].

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.