Woolworths Auditor's Report: Independence, Remuneration, & Key Matters

VerifiedAdded on 2023/06/07

|12

|3548

|281

Report

AI Summary

This report provides a comprehensive analysis of an auditor's report, focusing on auditor independence, non-audit services, auditor remuneration, and key audit matters. It examines the Woolworths Group audited report for the period ending June 25, 2017, detailing compliance with independence requirements, the nature and scope of non-audit services provided, and the factors influencing auditor remuneration. Key audit matters, such as the exit of the home improvement business and the carrying value of Big W PPE, are discussed, along with the audit procedures used to assess them. The report also elaborates on the role of the audit committee, the distinction between management and auditor responsibilities, and the treatment of material subsequent events. The analysis highlights the essential elements that auditors consider during an audit exercise, providing insights into the complexities of financial statement auditing and the importance of independent oversight.

Executive Summary

This report generally focuses on the audit report an auditor prepares after an audit exercise.

It will put emphasis on auditor’s independence, non-audit services offered by the auditor as

well as the auditor’s remuneration. The report captures key audit matters encountered during

the audit exercise. It further explains the audit committee as a crucial vital element to an audit

exercise.

An independent opinion is normally expressed by an auditor after the completion of an audit

exercise which normally takes into consideration all the material subsequent events after the

reporting period. It’s the responsibility of the auditor to give the findings from his analysis and

the report will not let go of what role the management play in the success of an audit exercise

as well as differentiate the role for the two parties.

This report generally focuses on the audit report an auditor prepares after an audit exercise.

It will put emphasis on auditor’s independence, non-audit services offered by the auditor as

well as the auditor’s remuneration. The report captures key audit matters encountered during

the audit exercise. It further explains the audit committee as a crucial vital element to an audit

exercise.

An independent opinion is normally expressed by an auditor after the completion of an audit

exercise which normally takes into consideration all the material subsequent events after the

reporting period. It’s the responsibility of the auditor to give the findings from his analysis and

the report will not let go of what role the management play in the success of an audit exercise

as well as differentiate the role for the two parties.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Content Page

Executive Summary……………………………………………………………………………………………………………………1

Introduction……………………………………………………………………………………………………………………………3

Main Body....................................................................................................................................4

Auditors Independence Requirements....................................................................................4

Non Audit Services...................................................................................................................4

Auditors Remuneration............................................................................................................5

Key Audit Matters.....................................................................................................................6

Audit Committee......................................................................................................................7

Audit opinion............................................................................................................................8

Directors and Management Responsibility Versus Auditors Responsibility............................9

Material Subsequent events....................................................................................................9

Conclusion..............................................................................................................................10

References..............................................................................................................................11

Executive Summary……………………………………………………………………………………………………………………1

Introduction……………………………………………………………………………………………………………………………3

Main Body....................................................................................................................................4

Auditors Independence Requirements....................................................................................4

Non Audit Services...................................................................................................................4

Auditors Remuneration............................................................................................................5

Key Audit Matters.....................................................................................................................6

Audit Committee......................................................................................................................7

Audit opinion............................................................................................................................8

Directors and Management Responsibility Versus Auditors Responsibility............................9

Material Subsequent events....................................................................................................9

Conclusion..............................................................................................................................10

References..............................................................................................................................11

Introduction

Auditors are generally concerned with analyzing Company accounts and to give a report as to

whether according to their analysis the reviewed information is error free and show the true

state of affairs of a company opeartions.

This report will focus on Woolworths Group audited report for the period ending 25th June

2017. It will try to elaborate the key elements that are essential in an auditor’s report such as

independence, any non-audit services the auditors may offer to the company, the auditors

remuneration and the factors that may lead to the differences in the pay an auditor is entitled

to from one year to another.

There are crucial matters that auditors pay attention to during an audit that require special

assessment and treatment to avoid making wrong conclusion. The report will discuss some of

this key audit matters as stated by the executive committee which is a representative of the

management. It will also elaborate the distinction between the role of an auditor and the

management during an audit exercise.

Subsequent events are also a crucial element in an audit exercise. The report will look into the

subsequent events from Woolworths Group and try to explain whether they were adjusting or

non-adjusting events.

In brief it will explain crucial elements for one to pay attention at as far as accounts auditing is

concerned (Abdoli and Eftekhari, 2010).

Auditors are generally concerned with analyzing Company accounts and to give a report as to

whether according to their analysis the reviewed information is error free and show the true

state of affairs of a company opeartions.

This report will focus on Woolworths Group audited report for the period ending 25th June

2017. It will try to elaborate the key elements that are essential in an auditor’s report such as

independence, any non-audit services the auditors may offer to the company, the auditors

remuneration and the factors that may lead to the differences in the pay an auditor is entitled

to from one year to another.

There are crucial matters that auditors pay attention to during an audit that require special

assessment and treatment to avoid making wrong conclusion. The report will discuss some of

this key audit matters as stated by the executive committee which is a representative of the

management. It will also elaborate the distinction between the role of an auditor and the

management during an audit exercise.

Subsequent events are also a crucial element in an audit exercise. The report will look into the

subsequent events from Woolworths Group and try to explain whether they were adjusting or

non-adjusting events.

In brief it will explain crucial elements for one to pay attention at as far as accounts auditing is

concerned (Abdoli and Eftekhari, 2010).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Main Body

1. Auditors Independence Requirements

An audit exercise is normally carried out by an independent person who is not involved in the

business of the company they intend to audit. Independence calls for auditors to ensure that

they don’t have an interest in the business of their clients but are solely carrying out the

exercise with utmost integrity and professionalism (Mat Zain, Wahab and Foo, 2010).

The auditor of Woolworths Limited has complied with the independence requirements as seen

in his declaration stating that there were no contraventions whatsoever as far as auditor’s

independence requirements as given by the corporations Act 2001 is concerned and neither

was there contravention of professional conduct (Sultana, Singh and Van der Zahn, 2014).

The directors’ report also confirms that the auditor did not compromise with independence

requirement even in the provision of non-audit services.

2. Non Audit Services

According to Ra, Kim and Jeon (2016) non-audit services refer to any task that an auditor maybe

involved in during an audit exercise that does not involve the review and analysis of financial

statements. Such services are vital as they help identify weaknesses in operations and auditors

give guidance on the appropriate measures to undertake to correct deficiencies or measures

that will ensure the business enjoys competitive advantage (Malek and Saidin, 2013).

The auditors of Woolworth provide the following non audit services to their client:

From the auditors pay it is evident that the auditors provided the following non audit services:

i) Services in relation to regulation and compliance.

ii) Tax adherence services.

iii) Other services not in relation to the audit of financial statements.

This are further explained below.

a) Risk Assessment

The auditors assessed the four types of risks the business could face (Strategic, Financial,

operational and compliance) and further stated how the same could be mitigated.

1. Auditors Independence Requirements

An audit exercise is normally carried out by an independent person who is not involved in the

business of the company they intend to audit. Independence calls for auditors to ensure that

they don’t have an interest in the business of their clients but are solely carrying out the

exercise with utmost integrity and professionalism (Mat Zain, Wahab and Foo, 2010).

The auditor of Woolworths Limited has complied with the independence requirements as seen

in his declaration stating that there were no contraventions whatsoever as far as auditor’s

independence requirements as given by the corporations Act 2001 is concerned and neither

was there contravention of professional conduct (Sultana, Singh and Van der Zahn, 2014).

The directors’ report also confirms that the auditor did not compromise with independence

requirement even in the provision of non-audit services.

2. Non Audit Services

According to Ra, Kim and Jeon (2016) non-audit services refer to any task that an auditor maybe

involved in during an audit exercise that does not involve the review and analysis of financial

statements. Such services are vital as they help identify weaknesses in operations and auditors

give guidance on the appropriate measures to undertake to correct deficiencies or measures

that will ensure the business enjoys competitive advantage (Malek and Saidin, 2013).

The auditors of Woolworth provide the following non audit services to their client:

From the auditors pay it is evident that the auditors provided the following non audit services:

i) Services in relation to regulation and compliance.

ii) Tax adherence services.

iii) Other services not in relation to the audit of financial statements.

This are further explained below.

a) Risk Assessment

The auditors assessed the four types of risks the business could face (Strategic, Financial,

operational and compliance) and further stated how the same could be mitigated.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

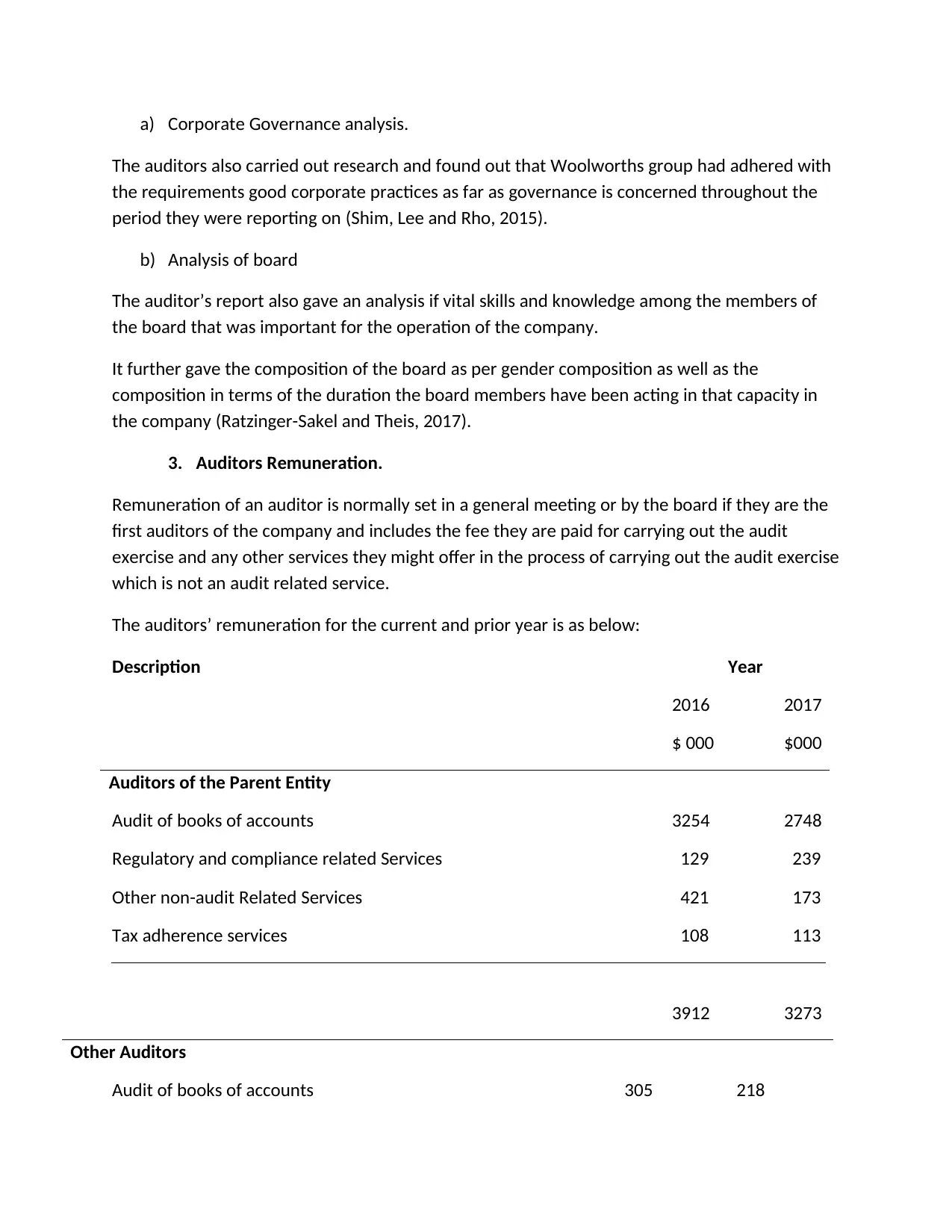

a) Corporate Governance analysis.

The auditors also carried out research and found out that Woolworths group had adhered with

the requirements good corporate practices as far as governance is concerned throughout the

period they were reporting on (Shim, Lee and Rho, 2015).

b) Analysis of board

The auditor’s report also gave an analysis if vital skills and knowledge among the members of

the board that was important for the operation of the company.

It further gave the composition of the board as per gender composition as well as the

composition in terms of the duration the board members have been acting in that capacity in

the company (Ratzinger-Sakel and Theis, 2017).

3. Auditors Remuneration.

Remuneration of an auditor is normally set in a general meeting or by the board if they are the

first auditors of the company and includes the fee they are paid for carrying out the audit

exercise and any other services they might offer in the process of carrying out the audit exercise

which is not an audit related service.

The auditors’ remuneration for the current and prior year is as below:

Description Year

2016 2017

$ 000 $000

Auditors of the Parent Entity

Audit of books of accounts 3254 2748

Regulatory and compliance related Services 129 239

Other non-audit Related Services 421 173

Tax adherence services 108 113

3912 3273

Other Auditors

Audit of books of accounts 305 218

The auditors also carried out research and found out that Woolworths group had adhered with

the requirements good corporate practices as far as governance is concerned throughout the

period they were reporting on (Shim, Lee and Rho, 2015).

b) Analysis of board

The auditor’s report also gave an analysis if vital skills and knowledge among the members of

the board that was important for the operation of the company.

It further gave the composition of the board as per gender composition as well as the

composition in terms of the duration the board members have been acting in that capacity in

the company (Ratzinger-Sakel and Theis, 2017).

3. Auditors Remuneration.

Remuneration of an auditor is normally set in a general meeting or by the board if they are the

first auditors of the company and includes the fee they are paid for carrying out the audit

exercise and any other services they might offer in the process of carrying out the audit exercise

which is not an audit related service.

The auditors’ remuneration for the current and prior year is as below:

Description Year

2016 2017

$ 000 $000

Auditors of the Parent Entity

Audit of books of accounts 3254 2748

Regulatory and compliance related Services 129 239

Other non-audit Related Services 421 173

Tax adherence services 108 113

3912 3273

Other Auditors

Audit of books of accounts 305 218

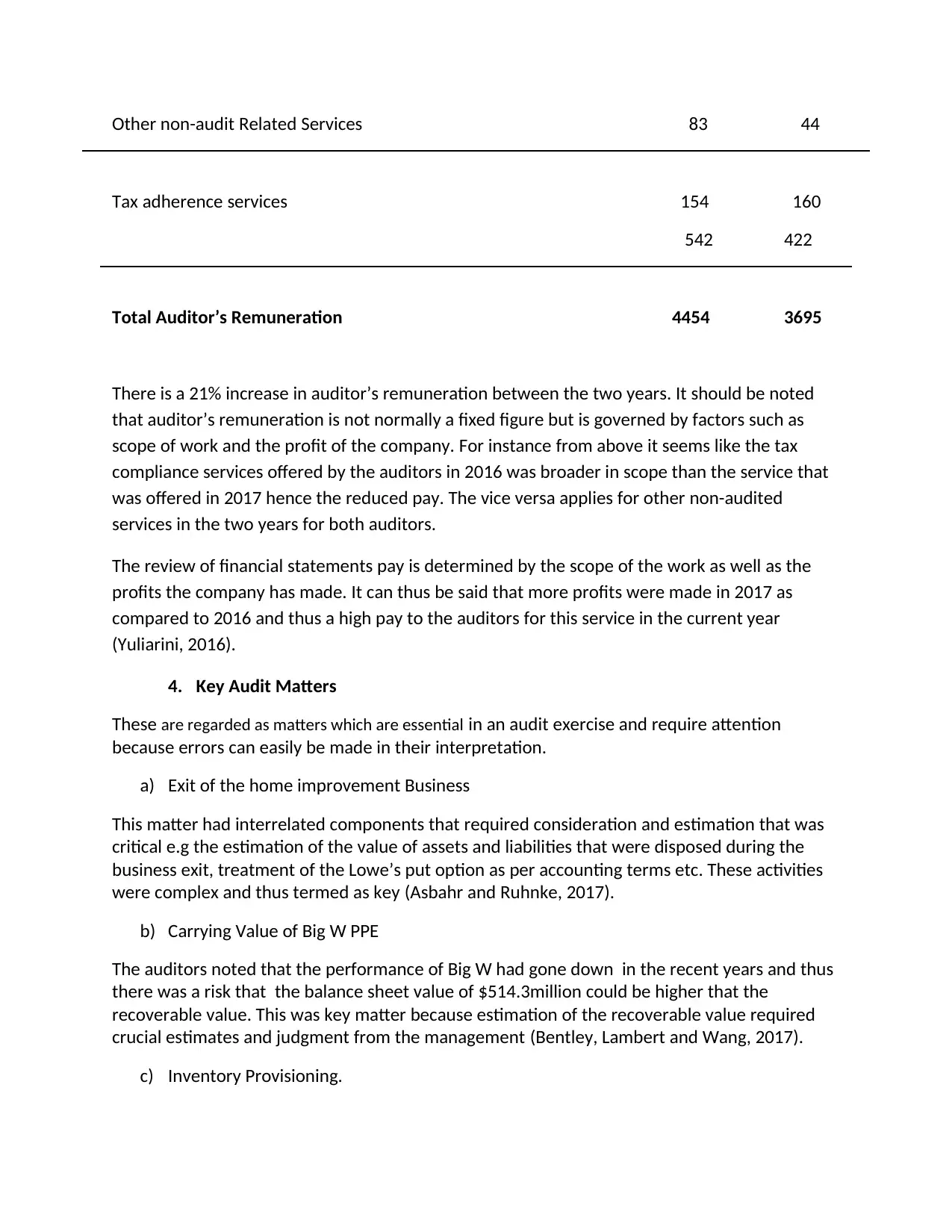

Other non-audit Related Services 83 44

Tax adherence services 154 160

542 422

Total Auditor’s Remuneration 4454 3695

There is a 21% increase in auditor’s remuneration between the two years. It should be noted

that auditor’s remuneration is not normally a fixed figure but is governed by factors such as

scope of work and the profit of the company. For instance from above it seems like the tax

compliance services offered by the auditors in 2016 was broader in scope than the service that

was offered in 2017 hence the reduced pay. The vice versa applies for other non-audited

services in the two years for both auditors.

The review of financial statements pay is determined by the scope of the work as well as the

profits the company has made. It can thus be said that more profits were made in 2017 as

compared to 2016 and thus a high pay to the auditors for this service in the current year

(Yuliarini, 2016).

4. Key Audit Matters

These are regarded as matters which are essential in an audit exercise and require attention

because errors can easily be made in their interpretation.

a) Exit of the home improvement Business

This matter had interrelated components that required consideration and estimation that was

critical e.g the estimation of the value of assets and liabilities that were disposed during the

business exit, treatment of the Lowe’s put option as per accounting terms etc. These activities

were complex and thus termed as key (Asbahr and Ruhnke, 2017).

b) Carrying Value of Big W PPE

The auditors noted that the performance of Big W had gone down in the recent years and thus

there was a risk that the balance sheet value of $514.3million could be higher that the

recoverable value. This was key matter because estimation of the recoverable value required

crucial estimates and judgment from the management (Bentley, Lambert and Wang, 2017).

c) Inventory Provisioning.

Tax adherence services 154 160

542 422

Total Auditor’s Remuneration 4454 3695

There is a 21% increase in auditor’s remuneration between the two years. It should be noted

that auditor’s remuneration is not normally a fixed figure but is governed by factors such as

scope of work and the profit of the company. For instance from above it seems like the tax

compliance services offered by the auditors in 2016 was broader in scope than the service that

was offered in 2017 hence the reduced pay. The vice versa applies for other non-audited

services in the two years for both auditors.

The review of financial statements pay is determined by the scope of the work as well as the

profits the company has made. It can thus be said that more profits were made in 2017 as

compared to 2016 and thus a high pay to the auditors for this service in the current year

(Yuliarini, 2016).

4. Key Audit Matters

These are regarded as matters which are essential in an audit exercise and require attention

because errors can easily be made in their interpretation.

a) Exit of the home improvement Business

This matter had interrelated components that required consideration and estimation that was

critical e.g the estimation of the value of assets and liabilities that were disposed during the

business exit, treatment of the Lowe’s put option as per accounting terms etc. These activities

were complex and thus termed as key (Asbahr and Ruhnke, 2017).

b) Carrying Value of Big W PPE

The auditors noted that the performance of Big W had gone down in the recent years and thus

there was a risk that the balance sheet value of $514.3million could be higher that the

recoverable value. This was key matter because estimation of the recoverable value required

crucial estimates and judgment from the management (Bentley, Lambert and Wang, 2017).

c) Inventory Provisioning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

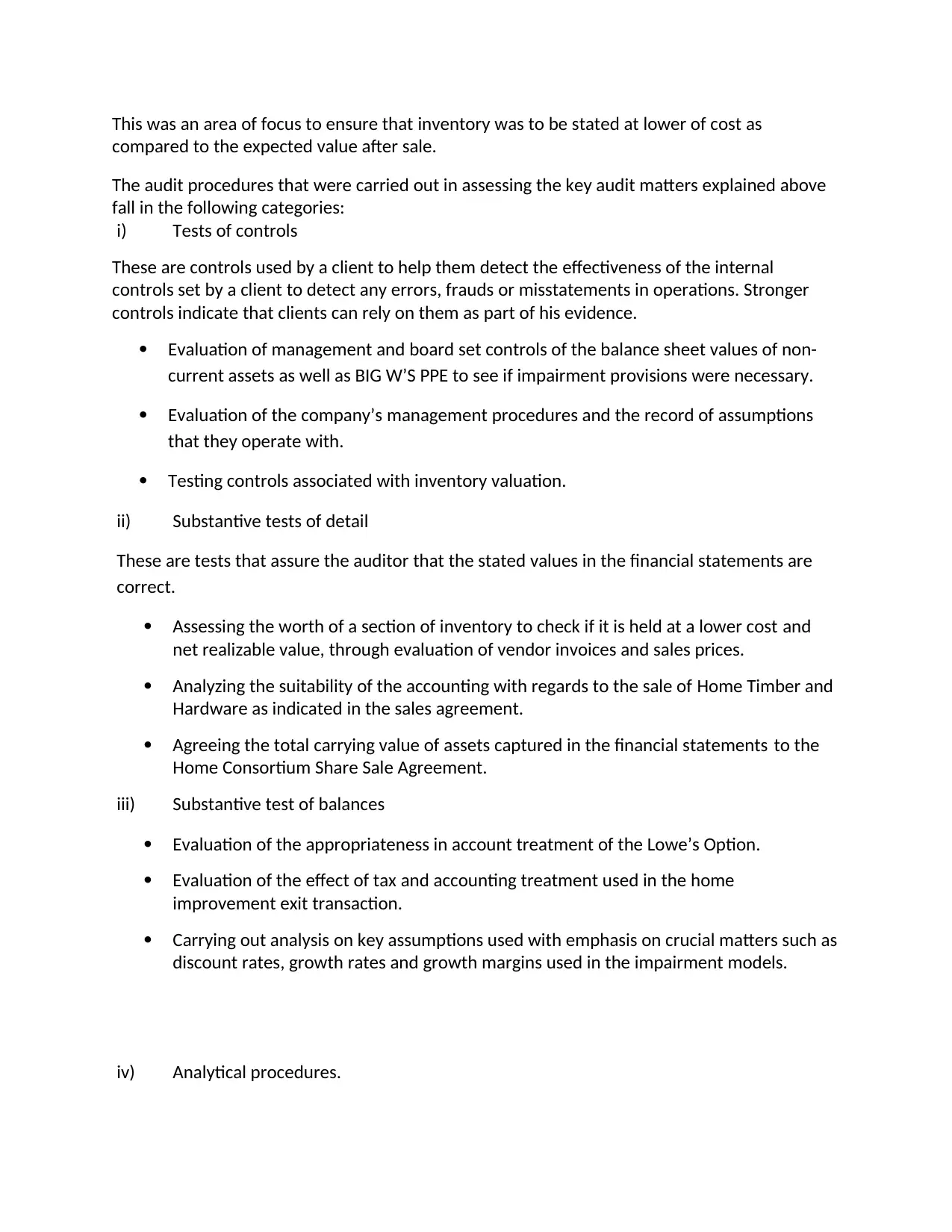

This was an area of focus to ensure that inventory was to be stated at lower of cost as

compared to the expected value after sale.

The audit procedures that were carried out in assessing the key audit matters explained above

fall in the following categories:

i) Tests of controls

These are controls used by a client to help them detect the effectiveness of the internal

controls set by a client to detect any errors, frauds or misstatements in operations. Stronger

controls indicate that clients can rely on them as part of his evidence.

Evaluation of management and board set controls of the balance sheet values of non-

current assets as well as BIG W’S PPE to see if impairment provisions were necessary.

Evaluation of the company’s management procedures and the record of assumptions

that they operate with.

Testing controls associated with inventory valuation.

ii) Substantive tests of detail

These are tests that assure the auditor that the stated values in the financial statements are

correct.

Assessing the worth of a section of inventory to check if it is held at a lower cost and

net realizable value, through evaluation of vendor invoices and sales prices.

Analyzing the suitability of the accounting with regards to the sale of Home Timber and

Hardware as indicated in the sales agreement.

Agreeing the total carrying value of assets captured in the financial statements to the

Home Consortium Share Sale Agreement.

iii) Substantive test of balances

Evaluation of the appropriateness in account treatment of the Lowe’s Option.

Evaluation of the effect of tax and accounting treatment used in the home

improvement exit transaction.

Carrying out analysis on key assumptions used with emphasis on crucial matters such as

discount rates, growth rates and growth margins used in the impairment models.

iv) Analytical procedures.

compared to the expected value after sale.

The audit procedures that were carried out in assessing the key audit matters explained above

fall in the following categories:

i) Tests of controls

These are controls used by a client to help them detect the effectiveness of the internal

controls set by a client to detect any errors, frauds or misstatements in operations. Stronger

controls indicate that clients can rely on them as part of his evidence.

Evaluation of management and board set controls of the balance sheet values of non-

current assets as well as BIG W’S PPE to see if impairment provisions were necessary.

Evaluation of the company’s management procedures and the record of assumptions

that they operate with.

Testing controls associated with inventory valuation.

ii) Substantive tests of detail

These are tests that assure the auditor that the stated values in the financial statements are

correct.

Assessing the worth of a section of inventory to check if it is held at a lower cost and

net realizable value, through evaluation of vendor invoices and sales prices.

Analyzing the suitability of the accounting with regards to the sale of Home Timber and

Hardware as indicated in the sales agreement.

Agreeing the total carrying value of assets captured in the financial statements to the

Home Consortium Share Sale Agreement.

iii) Substantive test of balances

Evaluation of the appropriateness in account treatment of the Lowe’s Option.

Evaluation of the effect of tax and accounting treatment used in the home

improvement exit transaction.

Carrying out analysis on key assumptions used with emphasis on crucial matters such as

discount rates, growth rates and growth margins used in the impairment models.

iv) Analytical procedures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This procedure help an auditor to identify potential risk areas that will call for his attention to

avoid wrong reporting.

Evaluation of the provisions for inventory write offs to ensure that the provisions are

worthwhile.

Having the knowledge of the inventory provisioning policy giving special considerations

to outdated inventory, seasonality, and also inventory turn calculations as well as sell

through rates(Chu, Dai and Zhang, 2010).

5. Audit Committee

Audit committee normally helps auditors to remain independent and they normally give an

independent view of the operations of management and the company as a whole (Grenier,

Ballou and Philip, 2011).This committee in Woolworths limited is referred to as the Audit, Risk

Management and Compliance Committee.

The committee is made up ofnon-executive directors and majorities are independent non-

executive directors. The committee is governed by a charter that states its structure, function

and responsibilities.

a) Structure

Woolworths Limited charter dictates that the Audit committee should have at least 3 members

who must be non-executive directors. At least a single member is required to have financial

qualifications and experience which will be stated by the board. The members to the committee

are appointed by the board who also determine the chairman to the committee (Klueber, Gold

and Pott, 2018).

The chairman to the committee should not be the board chairman. The chairman has the

responsibility to report to the board issues discussed during the meeting. He also acts as a link

between the committee and other parties of interest in the company which may need

information from him such as the Chief Executive Officer, the finance director, external auditors

etc.

The committee meeting can only be done with at least two members. The overall Company

secretary acts as the secretary to the Audit committee and takes minutes for the meeting. If the

chairman is not present during the committee meeting, one of the members will be appointed

to chair the meeting (Karim, Robin and Suh, 2015).

The committee is required to meet frequently and not less than 4 times in a year. The

committee is also permitted to invite any other person to attend the audit committee meeting.

b) Functions and responsibilities

avoid wrong reporting.

Evaluation of the provisions for inventory write offs to ensure that the provisions are

worthwhile.

Having the knowledge of the inventory provisioning policy giving special considerations

to outdated inventory, seasonality, and also inventory turn calculations as well as sell

through rates(Chu, Dai and Zhang, 2010).

5. Audit Committee

Audit committee normally helps auditors to remain independent and they normally give an

independent view of the operations of management and the company as a whole (Grenier,

Ballou and Philip, 2011).This committee in Woolworths limited is referred to as the Audit, Risk

Management and Compliance Committee.

The committee is made up ofnon-executive directors and majorities are independent non-

executive directors. The committee is governed by a charter that states its structure, function

and responsibilities.

a) Structure

Woolworths Limited charter dictates that the Audit committee should have at least 3 members

who must be non-executive directors. At least a single member is required to have financial

qualifications and experience which will be stated by the board. The members to the committee

are appointed by the board who also determine the chairman to the committee (Klueber, Gold

and Pott, 2018).

The chairman to the committee should not be the board chairman. The chairman has the

responsibility to report to the board issues discussed during the meeting. He also acts as a link

between the committee and other parties of interest in the company which may need

information from him such as the Chief Executive Officer, the finance director, external auditors

etc.

The committee meeting can only be done with at least two members. The overall Company

secretary acts as the secretary to the Audit committee and takes minutes for the meeting. If the

chairman is not present during the committee meeting, one of the members will be appointed

to chair the meeting (Karim, Robin and Suh, 2015).

The committee is required to meet frequently and not less than 4 times in a year. The

committee is also permitted to invite any other person to attend the audit committee meeting.

b) Functions and responsibilities

i. Overseeing the appointment as well as performance of external auditors and ensuring

their independence is upheld.

ii. Risk management through identification, effective control measures and reporting the

same to interested parties.

iii. Evaluating and reporting on risky events or incidences the company may face.

iv. Assist the board to ensure compliance with set rules, processes and procedures as well

as reviewing and updating of the compliance framework to ensure that it is effective.

v. Review of the company financial reports with external auditors and reporting findings to

shareholders.

vi. Ensure financial policies are in compliance with set regulatory and statutory

requirements as far as accounting standards are concerned.

6. Audit opinion

This can be explained as the overall conclusion an auditor give as a general view after the

evaluation of the books of accounts as well as activities of the company.

For the audit report of Woolworths limited the auditor has given an unqualified opinion. This is

stated in the auditor’s report where they state that the financial report gives the true state of

affairs of the Company and that the company complied with Australian Accounting Standards

and the Corporations Regulations 2001(Habib, 2013).

7. Directors and Management Responsibility Versus Auditors Responsibility

The directors and the management are charged with governance of the company. They are thus

supposed to ensure that proper books of accounts are kept in accordance with the set

accounting standards. They should also ensure completeness and correctness of accounting

information to be audited. They also set internal controls and ensure they are effective and

workable (Jaber and Abu Fadda, 2016).

The auditor on the other side has a duty to analyze or examine financial statements to ensure

that they show the true state of affairs of the company and also to ascertain that they have

been prepared as per the accounting provisions set. Auditors also review internal controls to

determine their reliability and could give advice to the management on the level of its reliability

(Hegazy and Stafford, 2016).

8. Material Subsequent events

their independence is upheld.

ii. Risk management through identification, effective control measures and reporting the

same to interested parties.

iii. Evaluating and reporting on risky events or incidences the company may face.

iv. Assist the board to ensure compliance with set rules, processes and procedures as well

as reviewing and updating of the compliance framework to ensure that it is effective.

v. Review of the company financial reports with external auditors and reporting findings to

shareholders.

vi. Ensure financial policies are in compliance with set regulatory and statutory

requirements as far as accounting standards are concerned.

6. Audit opinion

This can be explained as the overall conclusion an auditor give as a general view after the

evaluation of the books of accounts as well as activities of the company.

For the audit report of Woolworths limited the auditor has given an unqualified opinion. This is

stated in the auditor’s report where they state that the financial report gives the true state of

affairs of the Company and that the company complied with Australian Accounting Standards

and the Corporations Regulations 2001(Habib, 2013).

7. Directors and Management Responsibility Versus Auditors Responsibility

The directors and the management are charged with governance of the company. They are thus

supposed to ensure that proper books of accounts are kept in accordance with the set

accounting standards. They should also ensure completeness and correctness of accounting

information to be audited. They also set internal controls and ensure they are effective and

workable (Jaber and Abu Fadda, 2016).

The auditor on the other side has a duty to analyze or examine financial statements to ensure

that they show the true state of affairs of the company and also to ascertain that they have

been prepared as per the accounting provisions set. Auditors also review internal controls to

determine their reliability and could give advice to the management on the level of its reliability

(Hegazy and Stafford, 2016).

8. Material Subsequent events

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These are activities that may take place after the end of a reporting period of a company but

before audited accounting statements have been issued.

Woolworths Ltd had one subsequent event which was the home improvement bit which was in

relation with the home improvement business exit. This happened on the 26th Of June where

the company entered into an agreement to sale shares with home consortium subject to the

sale of Lowe’s shares. Woolworth was to assume some assets as well as responsibilities (Little

et al., 2011).

Further on 4th August Lowe’s shares in Hydrox were sold by a trust with home consortium as

the beneficiary in exchange for a consideration (Herda and Lavelle, 2014).

Subsequent event Treatment

This has been treated as a non-adjusting event. It has thus not been included in the current

audit exercise.

Conclusion

The auditors in their capacity have given concrete material information on their analysis and

findings. The report is straight forward and leaves no loophole that raises unanswered

questions.

To get more clarifications on the company operations as an interested party I would request the

auditor to answer the following follow up questions in the general meeting.

The effectiveness of the Audit committee as per their assessment.

Any internal control deficiencies the auditor may have identified and the extent of its

damage to the operations.

Any material disagreement they had with the management during the audit process.

Do they propose any changes in the management of the company and if yes why.

For how long have they been auditing the company accounts and what can be his

explanation for his re appointment (Hay, 2014).

References

before audited accounting statements have been issued.

Woolworths Ltd had one subsequent event which was the home improvement bit which was in

relation with the home improvement business exit. This happened on the 26th Of June where

the company entered into an agreement to sale shares with home consortium subject to the

sale of Lowe’s shares. Woolworth was to assume some assets as well as responsibilities (Little

et al., 2011).

Further on 4th August Lowe’s shares in Hydrox were sold by a trust with home consortium as

the beneficiary in exchange for a consideration (Herda and Lavelle, 2014).

Subsequent event Treatment

This has been treated as a non-adjusting event. It has thus not been included in the current

audit exercise.

Conclusion

The auditors in their capacity have given concrete material information on their analysis and

findings. The report is straight forward and leaves no loophole that raises unanswered

questions.

To get more clarifications on the company operations as an interested party I would request the

auditor to answer the following follow up questions in the general meeting.

The effectiveness of the Audit committee as per their assessment.

Any internal control deficiencies the auditor may have identified and the extent of its

damage to the operations.

Any material disagreement they had with the management during the audit process.

Do they propose any changes in the management of the company and if yes why.

For how long have they been auditing the company accounts and what can be his

explanation for his re appointment (Hay, 2014).

References

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abdoli, M. and Eftekhari, R. (2010).Independence and Impartiality of Auditors from the

Viewpoints of Independent Auditors and Investment Companies. SSRN Electronic Journal.

Asbahr, K. and Ruhnke, K. (2017).Real Effects of Reporting Key Audit Matters on Auditors'

Judgment of Accounting Estimates. SSRN Electronic Journal.

Bentley, J., Lambert, T. and Wang, E. (2017). The Effect of Increased Audit Disclosure on

Managerial Decision Making: Evidence from Disclosing Critical Audit Matters. SSRN Electronic

Journal.

Chu, L., Dai, J. and Zhang, P. (2010).The Impact of Auditors’ Experiences with their Clients on

the Consistency and Bias in Earnings Reporting and Auditors’ Independence. SSRN Electronic

Journal.

Grenier, J., Ballou, B. and Philip, S. (2011). Enhancing Audit Committee Effectiveness with a

Licensed Audit Committee Member. SSRN Electronic Journal.

Habib, A. (2013). A meta analysis of the determinants of modified audit opinion‐

decisions. Managerial Auditing Journal, 28(3), pp.184-216.

Hay, D. (2014). Auditing, International Auditing and the International Journal of Auditing:

Editorial. International Journal of Auditing, 18(1), pp.1-1.

Hegazy, K. and Stafford, A. (2016).Audit committee roles and responsibilities in two English

public sector settings. Managerial Auditing Journal, 31(8/9), pp.848-870.

Herda, D. and Lavelle, J. (2014).Auditing Subsequent Events: Perspectives from the

Field. Current Issues in Auditing, 8(2), pp.A10-A24.

Jaber, R. and Abu Fadda, M. (2016). Awareness Level of Professional Independence

Requirements, through Assimilation of Fundamental Principles of Professional Ethics, by

Jordanian CPA Auditors, in Auditing Process: Field Study. International Journal of Economics and

Finance, 8(9), p.11.

Karim, K., Robin, A. and Suh, S. (2015). Board Structure and Audit Committee

Monitoring. Journal of Accounting, Auditing & Finance, 31(2), pp.249-276.

Klueber, J., Gold, A. and Pott, C. (2018). Do Key Audit Matters Impact Financial Reporting

Behavior?. SSRN Electronic Journal.

Little, R., Yosef, M., Nan, B. and Harlow, S. (2011). A Method for Longitudinal Prospective

Evaluation of Markers for a Subsequent Event. American Journal of Epidemiology, 173(12),

pp.1380-1387.

Malek, M. and Saidin, S. (2013). Audit Services Fee, Non-Audit Services and the Reliability of

Earnings. International Journal of Trade, Economics and Finance, pp.259-264.

Mat Zain, M., Wahab, E. and Foo, Y. (2010).Audit Quality: Do the Audit Committee and Internal

Audit Arrangements Matters?. Corporate Ownership and Control, 8(1).

Viewpoints of Independent Auditors and Investment Companies. SSRN Electronic Journal.

Asbahr, K. and Ruhnke, K. (2017).Real Effects of Reporting Key Audit Matters on Auditors'

Judgment of Accounting Estimates. SSRN Electronic Journal.

Bentley, J., Lambert, T. and Wang, E. (2017). The Effect of Increased Audit Disclosure on

Managerial Decision Making: Evidence from Disclosing Critical Audit Matters. SSRN Electronic

Journal.

Chu, L., Dai, J. and Zhang, P. (2010).The Impact of Auditors’ Experiences with their Clients on

the Consistency and Bias in Earnings Reporting and Auditors’ Independence. SSRN Electronic

Journal.

Grenier, J., Ballou, B. and Philip, S. (2011). Enhancing Audit Committee Effectiveness with a

Licensed Audit Committee Member. SSRN Electronic Journal.

Habib, A. (2013). A meta analysis of the determinants of modified audit opinion‐

decisions. Managerial Auditing Journal, 28(3), pp.184-216.

Hay, D. (2014). Auditing, International Auditing and the International Journal of Auditing:

Editorial. International Journal of Auditing, 18(1), pp.1-1.

Hegazy, K. and Stafford, A. (2016).Audit committee roles and responsibilities in two English

public sector settings. Managerial Auditing Journal, 31(8/9), pp.848-870.

Herda, D. and Lavelle, J. (2014).Auditing Subsequent Events: Perspectives from the

Field. Current Issues in Auditing, 8(2), pp.A10-A24.

Jaber, R. and Abu Fadda, M. (2016). Awareness Level of Professional Independence

Requirements, through Assimilation of Fundamental Principles of Professional Ethics, by

Jordanian CPA Auditors, in Auditing Process: Field Study. International Journal of Economics and

Finance, 8(9), p.11.

Karim, K., Robin, A. and Suh, S. (2015). Board Structure and Audit Committee

Monitoring. Journal of Accounting, Auditing & Finance, 31(2), pp.249-276.

Klueber, J., Gold, A. and Pott, C. (2018). Do Key Audit Matters Impact Financial Reporting

Behavior?. SSRN Electronic Journal.

Little, R., Yosef, M., Nan, B. and Harlow, S. (2011). A Method for Longitudinal Prospective

Evaluation of Markers for a Subsequent Event. American Journal of Epidemiology, 173(12),

pp.1380-1387.

Malek, M. and Saidin, S. (2013). Audit Services Fee, Non-Audit Services and the Reliability of

Earnings. International Journal of Trade, Economics and Finance, pp.259-264.

Mat Zain, M., Wahab, E. and Foo, Y. (2010).Audit Quality: Do the Audit Committee and Internal

Audit Arrangements Matters?. Corporate Ownership and Control, 8(1).

Ra, H., Kim, Y. and Jeon, K. (2016). The Effects of Non-Audit Services on Audit Quality : A Focus

on Auditor and Non-audit Services Type. korean management review, 45(1), p.259.

Ratzinger-Sakel, N. and Theis, J. (2017). Does Considering Key Audit Matters Affect Auditor

Judgment Performance?. SSRN Electronic Journal.

Shim, Y., Lee, J. and Rho, J. (2015).Articles : Implementation of New International Standard on

Audit (Communicating Key Audit Matters in the Independent Auditor`s Report) and Auditors

Liability Scheme. Commercial Law Review, 34(3), pp.367-406.

Sultana, N., Singh, H. and Van der Zahn, J. (2014). Audit Committee Characteristics and Audit

Report Lag. International Journal of Auditing, 19(2), pp.72-87.

Yuliarini, S. (2016). Remuneration and Management Behavior Evaluation: A Critical

Review. Archives of Business Research, 4(6).

on Auditor and Non-audit Services Type. korean management review, 45(1), p.259.

Ratzinger-Sakel, N. and Theis, J. (2017). Does Considering Key Audit Matters Affect Auditor

Judgment Performance?. SSRN Electronic Journal.

Shim, Y., Lee, J. and Rho, J. (2015).Articles : Implementation of New International Standard on

Audit (Communicating Key Audit Matters in the Independent Auditor`s Report) and Auditors

Liability Scheme. Commercial Law Review, 34(3), pp.367-406.

Sultana, N., Singh, H. and Van der Zahn, J. (2014). Audit Committee Characteristics and Audit

Report Lag. International Journal of Auditing, 19(2), pp.72-87.

Yuliarini, S. (2016). Remuneration and Management Behavior Evaluation: A Critical

Review. Archives of Business Research, 4(6).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.