Auditing and Assurance Assignment on Woolworths Company

VerifiedAdded on 2023/06/11

|11

|1925

|305

AI Summary

This report is an auditing and assurance assignment on Woolworths Company. It covers ASA 315, understanding the entity and its environment and assessing the risk of material misstatement. It also discusses the risks associated with expense accounts and how to minimize them.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

WOolworthS Company

Auditing and Assurance

Assignment -D

Name of the Author

Auditing and Assurance

Assignment -D

Name of the Author

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION.................................................................................................................................1

PART 1 AND 2.....................................................................................................................................1

ASA 315: UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING

THE RISK OF MATERIAL MISSTATEMENT..............................................................................1

PART 3..................................................................................................................................................5

INTRODUCTION.................................................................................................................................1

PART 1 AND 2.....................................................................................................................................1

ASA 315: UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING

THE RISK OF MATERIAL MISSTATEMENT..............................................................................1

PART 3..................................................................................................................................................5

INTRODUCTION

A company that operates in a society and is publicly traded is required to get its

accounts scrutinised periodically from time to time as required by the owners. For this

purpose, an auditor is appointed by the owners, i.e. shareholders, to audit and report on the

working of the company and tells about the true and fair state of affairs of financial position

and financial performance. Auditing is the process of independent examination and

evaluation of books of accounts, vouchers, entity’s control environment etc by an unbiased

person with a view to give an opinion over its truthfulness and fairness. In the ongoing report,

the company chosen is Woolworths Group. The company is a retail business giant and carries

on business throughout Australia and New Zealand. Their mission is to deliver the best

experience and quality to its customers. They have served successful business partners to

thousands of manufacturers and farmers.

PART 1 AND 2

ASA 315: UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND

ASSESSING THE RISK OF MATERIAL MISSTATEMENT

As per this auditing standard the auditor, before commencing any audit, is required to

understand the entity’s internal environment, which enables him to asses the level of risk of

material misstatement existent in entity (Woolworths Group Limited 2018). The main

responsibilities of the auditor apart from assessing the environment includes, discussing with

engagement team the susceptibility of material misstatement in entity’s financial reports,

understanding entity’s internal control components, identifying areas where substantive

procedures alone won’t be sufficient, communicating with those charged with governance the

observed weaknesses in internal control and outlining the documentation requirements

(Vîlsănoiua, and Buzenche (Matei), 2014).

Key assertions are another name given to audit assertions. These are basically the

implied or unambiguous claims and depictions that are being made by the management, who

are in case of every entity responsible for preparation and presentation of financial

statements. Through these claims, management tries to convince readers with the

appropriateness of different financial transactions, assets, liabilities and equity balances. The

assertions can be regarding presentations and disclosures also (Woolworths Group 2016).

A company that operates in a society and is publicly traded is required to get its

accounts scrutinised periodically from time to time as required by the owners. For this

purpose, an auditor is appointed by the owners, i.e. shareholders, to audit and report on the

working of the company and tells about the true and fair state of affairs of financial position

and financial performance. Auditing is the process of independent examination and

evaluation of books of accounts, vouchers, entity’s control environment etc by an unbiased

person with a view to give an opinion over its truthfulness and fairness. In the ongoing report,

the company chosen is Woolworths Group. The company is a retail business giant and carries

on business throughout Australia and New Zealand. Their mission is to deliver the best

experience and quality to its customers. They have served successful business partners to

thousands of manufacturers and farmers.

PART 1 AND 2

ASA 315: UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND

ASSESSING THE RISK OF MATERIAL MISSTATEMENT

As per this auditing standard the auditor, before commencing any audit, is required to

understand the entity’s internal environment, which enables him to asses the level of risk of

material misstatement existent in entity (Woolworths Group Limited 2018). The main

responsibilities of the auditor apart from assessing the environment includes, discussing with

engagement team the susceptibility of material misstatement in entity’s financial reports,

understanding entity’s internal control components, identifying areas where substantive

procedures alone won’t be sufficient, communicating with those charged with governance the

observed weaknesses in internal control and outlining the documentation requirements

(Vîlsănoiua, and Buzenche (Matei), 2014).

Key assertions are another name given to audit assertions. These are basically the

implied or unambiguous claims and depictions that are being made by the management, who

are in case of every entity responsible for preparation and presentation of financial

statements. Through these claims, management tries to convince readers with the

appropriateness of different financial transactions, assets, liabilities and equity balances. The

assertions can be regarding presentations and disclosures also (Woolworths Group 2016).

Substantive test of detail: the case of applying substantive procedure arises when the auditor

doubts the internal control environment of an entity. These are done in order to eliminate the

risk that auditor suspects about certain assets or transactions or other areas. They may involve

analytical procedures and test of details. Analytical procedures involve forming relationships

and comparisons among different kind of financial and/or non-financial information of the

same and/or different entities. Whereas, the test of details includes performing tasks full of

efforts to gather audit evidence like, observation, reperformance, inspection, external

confirmations (The Institute of Chartered Accountants in England and Wales 2013).

1.

Asset

Account

2(a).

Explanation of why

the account is at

risk

2(b).

Key Assertion

2(c).

Substantive test of

detail

1. INVENTORIES:

AUD 4080.4 million

The inventory is said

to be valued at lower

of cost and net

realisable value.

There is a risk as to

whether the same

process had been

followed or not.

There are chances

that the value of

inventory may not

match with the

physical count of

inventory. There

may lie

overvaluation or

VALUATION: This

key assertion deals

with the value of

assets, liabilities and

equity balances. By

value, it refers to the

appropriateness of

the valuation done.

E.g. in this case the

inventory is valued

at cost, being lower

of cost and net

realisable value.

This valuation is as

per the Australian

accounting standard

AASB 102,

OBSERVATION:

this tool involves,

direct approach of an

auditor, wherein he

himself witnesses

the physical count of

inventory being

made. Therein he

perceives the kind of

documentation done

by the concern’s

employees of the

count made by them

and matches it with

the records

maintained by the

entity in its books of

account. By this he

doubts the internal control environment of an entity. These are done in order to eliminate the

risk that auditor suspects about certain assets or transactions or other areas. They may involve

analytical procedures and test of details. Analytical procedures involve forming relationships

and comparisons among different kind of financial and/or non-financial information of the

same and/or different entities. Whereas, the test of details includes performing tasks full of

efforts to gather audit evidence like, observation, reperformance, inspection, external

confirmations (The Institute of Chartered Accountants in England and Wales 2013).

1.

Asset

Account

2(a).

Explanation of why

the account is at

risk

2(b).

Key Assertion

2(c).

Substantive test of

detail

1. INVENTORIES:

AUD 4080.4 million

The inventory is said

to be valued at lower

of cost and net

realisable value.

There is a risk as to

whether the same

process had been

followed or not.

There are chances

that the value of

inventory may not

match with the

physical count of

inventory. There

may lie

overvaluation or

VALUATION: This

key assertion deals

with the value of

assets, liabilities and

equity balances. By

value, it refers to the

appropriateness of

the valuation done.

E.g. in this case the

inventory is valued

at cost, being lower

of cost and net

realisable value.

This valuation is as

per the Australian

accounting standard

AASB 102,

OBSERVATION:

this tool involves,

direct approach of an

auditor, wherein he

himself witnesses

the physical count of

inventory being

made. Therein he

perceives the kind of

documentation done

by the concern’s

employees of the

count made by them

and matches it with

the records

maintained by the

entity in its books of

account. By this he

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

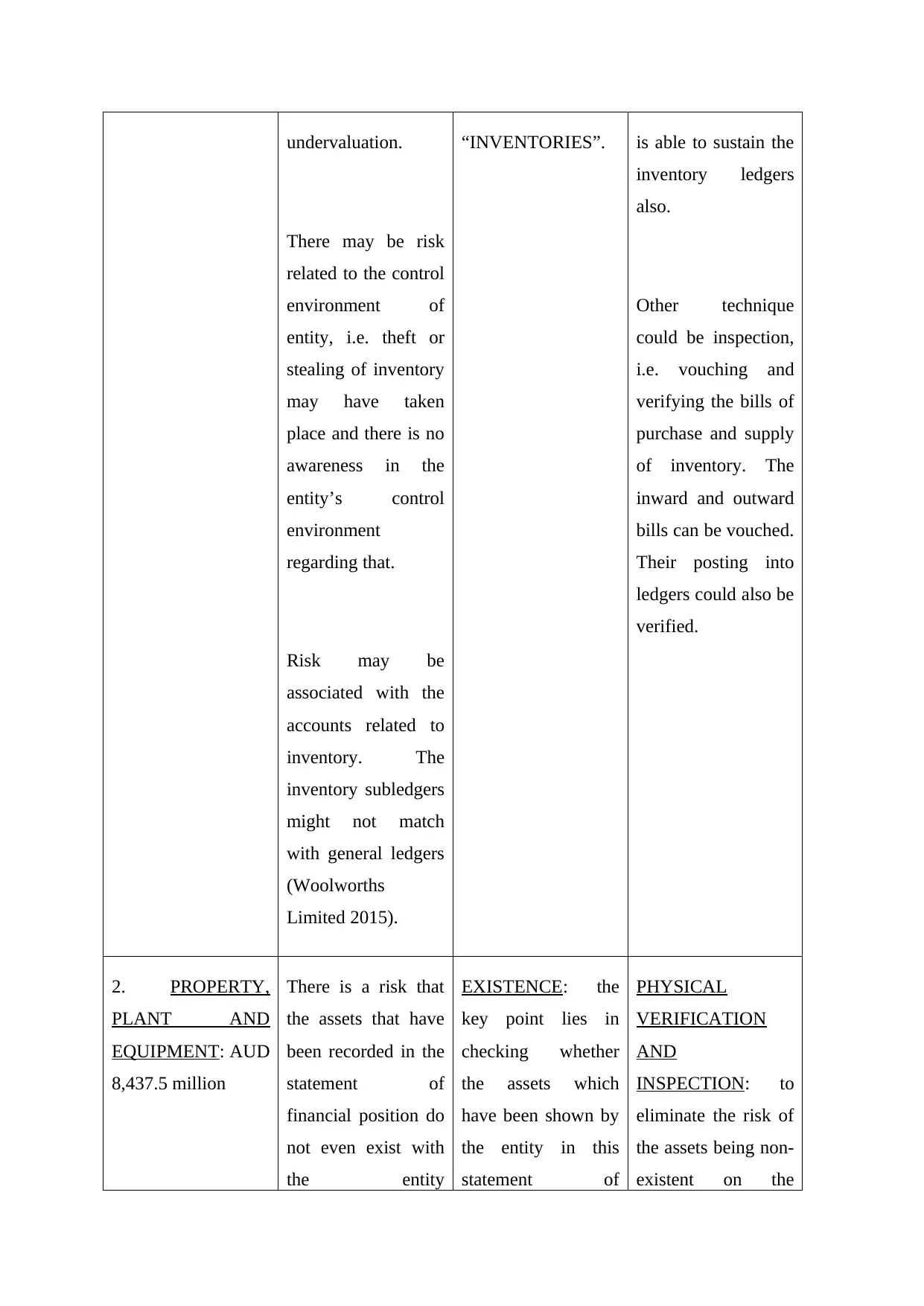

undervaluation.

There may be risk

related to the control

environment of

entity, i.e. theft or

stealing of inventory

may have taken

place and there is no

awareness in the

entity’s control

environment

regarding that.

Risk may be

associated with the

accounts related to

inventory. The

inventory subledgers

might not match

with general ledgers

(Woolworths

Limited 2015).

“INVENTORIES”. is able to sustain the

inventory ledgers

also.

Other technique

could be inspection,

i.e. vouching and

verifying the bills of

purchase and supply

of inventory. The

inward and outward

bills can be vouched.

Their posting into

ledgers could also be

verified.

2. PROPERTY,

PLANT AND

EQUIPMENT: AUD

8,437.5 million

There is a risk that

the assets that have

been recorded in the

statement of

financial position do

not even exist with

the entity

EXISTENCE: the

key point lies in

checking whether

the assets which

have been shown by

the entity in this

statement of

PHYSICAL

VERIFICATION

AND

INSPECTION: to

eliminate the risk of

the assets being non-

existent on the

There may be risk

related to the control

environment of

entity, i.e. theft or

stealing of inventory

may have taken

place and there is no

awareness in the

entity’s control

environment

regarding that.

Risk may be

associated with the

accounts related to

inventory. The

inventory subledgers

might not match

with general ledgers

(Woolworths

Limited 2015).

“INVENTORIES”. is able to sustain the

inventory ledgers

also.

Other technique

could be inspection,

i.e. vouching and

verifying the bills of

purchase and supply

of inventory. The

inward and outward

bills can be vouched.

Their posting into

ledgers could also be

verified.

2. PROPERTY,

PLANT AND

EQUIPMENT: AUD

8,437.5 million

There is a risk that

the assets that have

been recorded in the

statement of

financial position do

not even exist with

the entity

EXISTENCE: the

key point lies in

checking whether

the assets which

have been shown by

the entity in this

statement of

PHYSICAL

VERIFICATION

AND

INSPECTION: to

eliminate the risk of

the assets being non-

existent on the

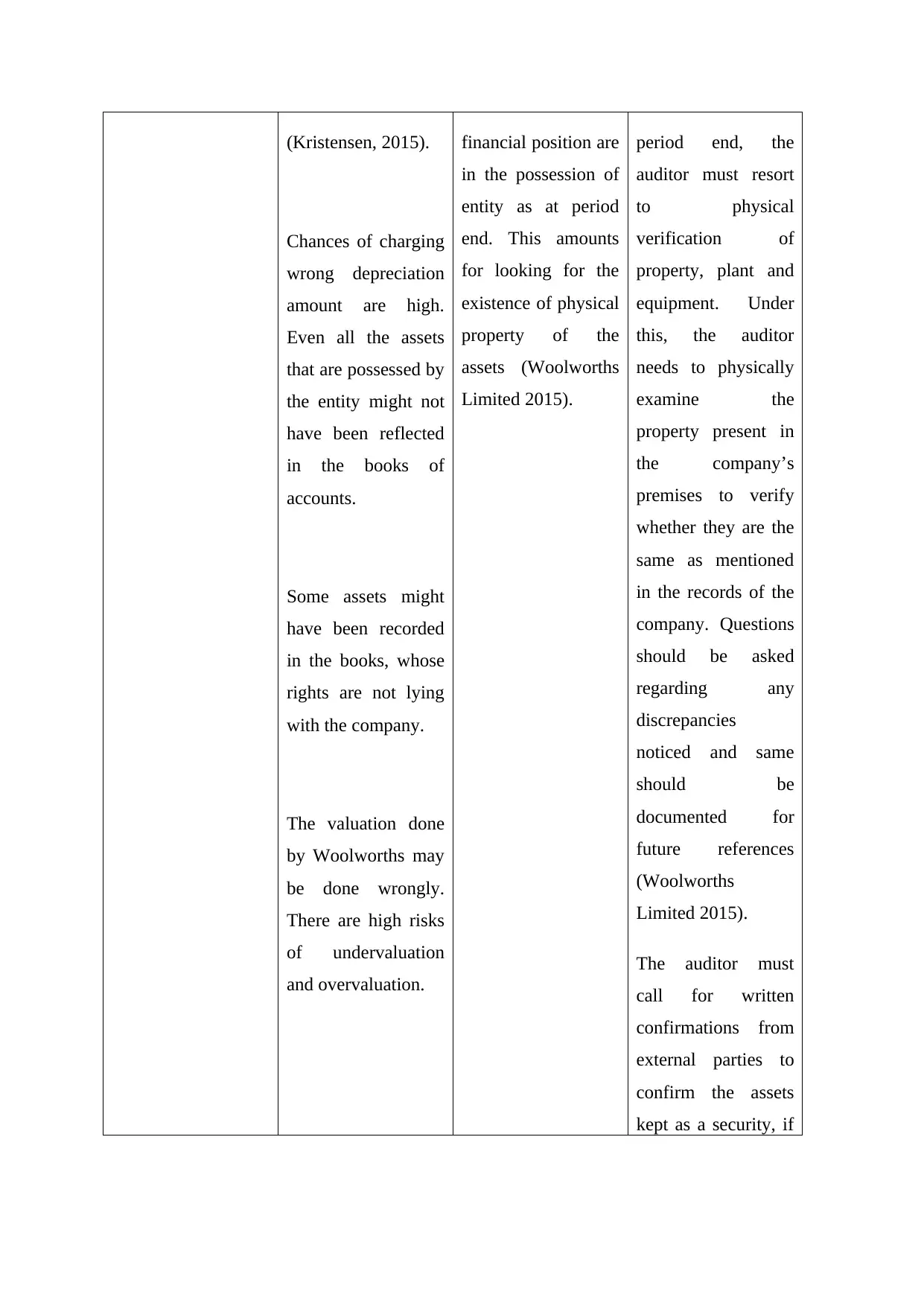

(Kristensen, 2015).

Chances of charging

wrong depreciation

amount are high.

Even all the assets

that are possessed by

the entity might not

have been reflected

in the books of

accounts.

Some assets might

have been recorded

in the books, whose

rights are not lying

with the company.

The valuation done

by Woolworths may

be done wrongly.

There are high risks

of undervaluation

and overvaluation.

financial position are

in the possession of

entity as at period

end. This amounts

for looking for the

existence of physical

property of the

assets (Woolworths

Limited 2015).

period end, the

auditor must resort

to physical

verification of

property, plant and

equipment. Under

this, the auditor

needs to physically

examine the

property present in

the company’s

premises to verify

whether they are the

same as mentioned

in the records of the

company. Questions

should be asked

regarding any

discrepancies

noticed and same

should be

documented for

future references

(Woolworths

Limited 2015).

The auditor must

call for written

confirmations from

external parties to

confirm the assets

kept as a security, if

Chances of charging

wrong depreciation

amount are high.

Even all the assets

that are possessed by

the entity might not

have been reflected

in the books of

accounts.

Some assets might

have been recorded

in the books, whose

rights are not lying

with the company.

The valuation done

by Woolworths may

be done wrongly.

There are high risks

of undervaluation

and overvaluation.

financial position are

in the possession of

entity as at period

end. This amounts

for looking for the

existence of physical

property of the

assets (Woolworths

Limited 2015).

period end, the

auditor must resort

to physical

verification of

property, plant and

equipment. Under

this, the auditor

needs to physically

examine the

property present in

the company’s

premises to verify

whether they are the

same as mentioned

in the records of the

company. Questions

should be asked

regarding any

discrepancies

noticed and same

should be

documented for

future references

(Woolworths

Limited 2015).

The auditor must

call for written

confirmations from

external parties to

confirm the assets

kept as a security, if

that is so the case.

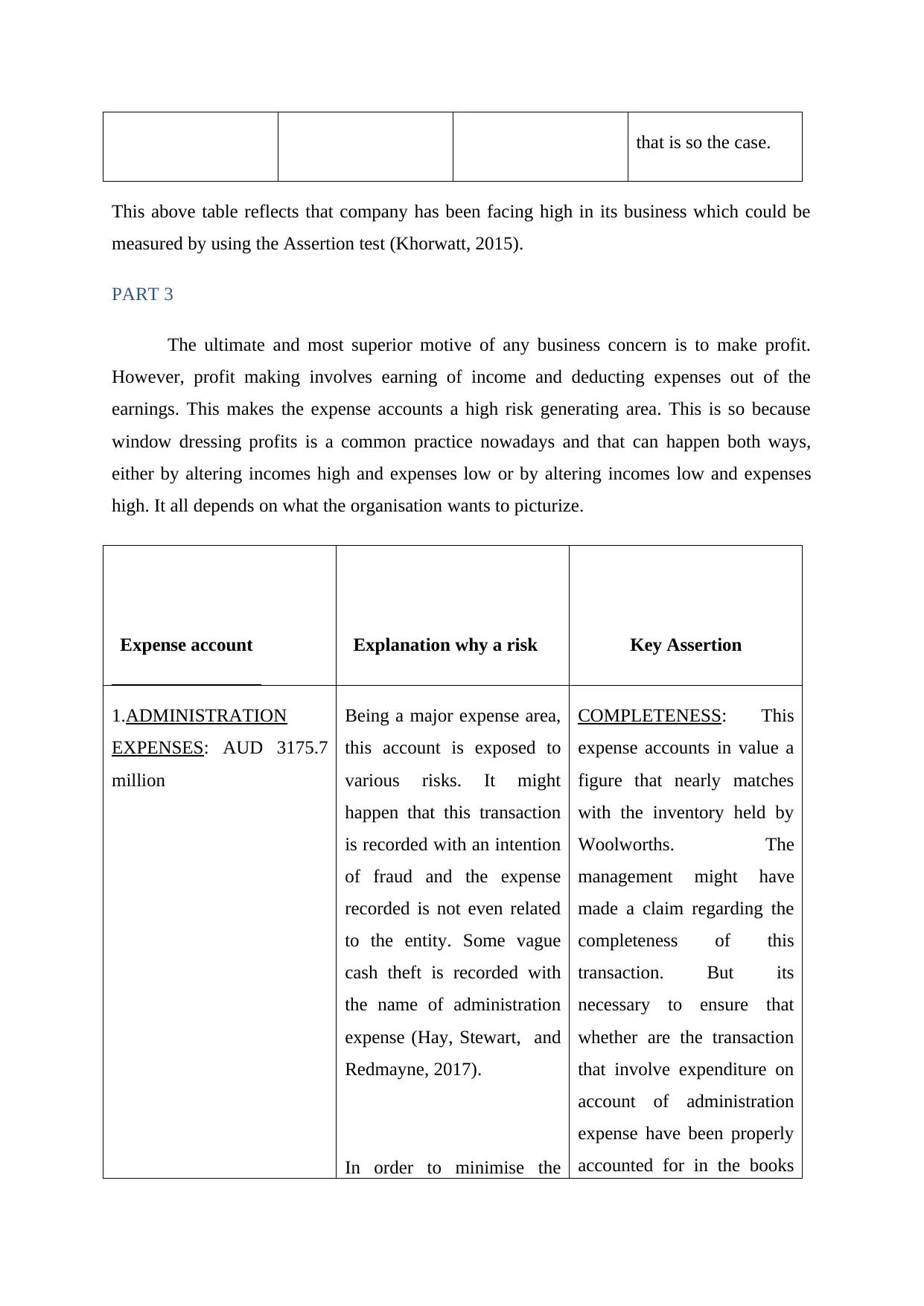

This above table reflects that company has been facing high in its business which could be

measured by using the Assertion test (Khorwatt, 2015).

PART 3

The ultimate and most superior motive of any business concern is to make profit.

However, profit making involves earning of income and deducting expenses out of the

earnings. This makes the expense accounts a high risk generating area. This is so because

window dressing profits is a common practice nowadays and that can happen both ways,

either by altering incomes high and expenses low or by altering incomes low and expenses

high. It all depends on what the organisation wants to picturize.

Expense account Explanation why a risk Key Assertion

1.ADMINISTRATION

EXPENSES: AUD 3175.7

million

Being a major expense area,

this account is exposed to

various risks. It might

happen that this transaction

is recorded with an intention

of fraud and the expense

recorded is not even related

to the entity. Some vague

cash theft is recorded with

the name of administration

expense (Hay, Stewart, and

Redmayne, 2017).

In order to minimise the

COMPLETENESS: This

expense accounts in value a

figure that nearly matches

with the inventory held by

Woolworths. The

management might have

made a claim regarding the

completeness of this

transaction. But its

necessary to ensure that

whether are the transaction

that involve expenditure on

account of administration

expense have been properly

accounted for in the books

This above table reflects that company has been facing high in its business which could be

measured by using the Assertion test (Khorwatt, 2015).

PART 3

The ultimate and most superior motive of any business concern is to make profit.

However, profit making involves earning of income and deducting expenses out of the

earnings. This makes the expense accounts a high risk generating area. This is so because

window dressing profits is a common practice nowadays and that can happen both ways,

either by altering incomes high and expenses low or by altering incomes low and expenses

high. It all depends on what the organisation wants to picturize.

Expense account Explanation why a risk Key Assertion

1.ADMINISTRATION

EXPENSES: AUD 3175.7

million

Being a major expense area,

this account is exposed to

various risks. It might

happen that this transaction

is recorded with an intention

of fraud and the expense

recorded is not even related

to the entity. Some vague

cash theft is recorded with

the name of administration

expense (Hay, Stewart, and

Redmayne, 2017).

In order to minimise the

COMPLETENESS: This

expense accounts in value a

figure that nearly matches

with the inventory held by

Woolworths. The

management might have

made a claim regarding the

completeness of this

transaction. But its

necessary to ensure that

whether are the transaction

that involve expenditure on

account of administration

expense have been properly

accounted for in the books

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profits with a view to

eliminate taxes, there are

chances of not recording all

the payments done for

administration expenses. A

few transactions might have

been eliminated.

Some human error is also

bound to have taken place,

as its impossible to protect.

High possibilities exist of

recording inaccurate

amounts, i.e. the transactions

might have been recorded

completely, but the amount

might not be accurate

(Deloitte, 2018).

There might exist the case of

overlapping financial years

and due to which some

transactions relating to

administration expense

might have been exposed to

the risk of being recognised

in a period other than the

accounting period of its

accrual (Auditing and

Assurance Standards Board

of accounts of Woolworths

and the tax effect have also

been considered for the

same (Grant Thornton

2017).

One thing that is required to

be kept in mind is keeping

the awareness while

checking for this claim that

the transaction recorded

does relate to Woolworths

only and is a valid

transaction. There is no

forgery in same (Financial

Times 2017).

eliminate taxes, there are

chances of not recording all

the payments done for

administration expenses. A

few transactions might have

been eliminated.

Some human error is also

bound to have taken place,

as its impossible to protect.

High possibilities exist of

recording inaccurate

amounts, i.e. the transactions

might have been recorded

completely, but the amount

might not be accurate

(Deloitte, 2018).

There might exist the case of

overlapping financial years

and due to which some

transactions relating to

administration expense

might have been exposed to

the risk of being recognised

in a period other than the

accounting period of its

accrual (Auditing and

Assurance Standards Board

of accounts of Woolworths

and the tax effect have also

been considered for the

same (Grant Thornton

2017).

One thing that is required to

be kept in mind is keeping

the awareness while

checking for this claim that

the transaction recorded

does relate to Woolworths

only and is a valid

transaction. There is no

forgery in same (Financial

Times 2017).

2015).

References

Auditing and Assurance Standards Board 2015. Auditing Standard ASA 570 Going Concern

[ONLINE] retrieved from

http://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [

Deloitte 2018. Deloitte Touche Tohmatsu LLC [ONLINE] retrieved from

https://www2.deloitte.com/jp/en/pages/about-deloitte/articles/audit/audit.html

Financial Times 2017. Equities [ONLINE] retrieved from

https://markets.ft.com/data/equities/tearsheet/forecasts?s=WOW:ASX

Grant Thornton 2017. IFRS Viewpoint. [ONLINE] retrieved from

https://www.grantthornton.global/globalassets/1.-member-firms/global/insights/

article-pdfs/2017/IFRS-Viewpoint-7-going-concern.pdf

Hay, D. Stewart, J. and Redmayne, N, B. (2017). The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian

Accounting Review. 27(4).

Khorwatt, E., (2015) .Assessment of Business Risk and Control Risk in the Libyan Context.

Open Journal of Accounting.4.

Kristensen, R. H. (2015). Judgment in an auditor’s materiality assessments. Danish Journal

of Management & Business. 2.

The Institute of Chartered Accountants in England and Wales 2013. Audit and Assurance

Advanced Stage Technical Integration Level. [ONLINE] Available from

https://www.icaew.com/~/media/corporate/files/qualifications%20and

%20programmes/learning%20partners/learning%20materials/ti%20audit

%20assurance%2020142015%20inspection%20copy.ashx

Vîlsănoiua, & Buzenche (Matei),S. (2014). Determining Audit Materiality in the banking

industry- a knowledge based approach. Procedia Economics and Finance.15.

Woolworths Group (2016). Financial Report 2016. [ONLINE] Available from

https://wow2016ar.qreports.com.au/xresources/pdf/wow16ar-financial-report.pdf /

Woolworths Group Limited 2018 Portfolio Businesses [ONLINE] Available from

https://www.woolworthsgroup.com.au/page/about-us/our-brands/portfolio-businesses/

[Accessed 22nd May, 2018].

Woolworths Limited (2015). Annual Report 2015. [ONLINE] retrieved from

https://www.woolworthsgroup.com.au/icms_docs/182381_Annual_Report_2015.pdf

Auditing and Assurance Standards Board 2015. Auditing Standard ASA 570 Going Concern

[ONLINE] retrieved from

http://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [

Deloitte 2018. Deloitte Touche Tohmatsu LLC [ONLINE] retrieved from

https://www2.deloitte.com/jp/en/pages/about-deloitte/articles/audit/audit.html

Financial Times 2017. Equities [ONLINE] retrieved from

https://markets.ft.com/data/equities/tearsheet/forecasts?s=WOW:ASX

Grant Thornton 2017. IFRS Viewpoint. [ONLINE] retrieved from

https://www.grantthornton.global/globalassets/1.-member-firms/global/insights/

article-pdfs/2017/IFRS-Viewpoint-7-going-concern.pdf

Hay, D. Stewart, J. and Redmayne, N, B. (2017). The Role of Auditing in Corporate

Governance in Australia and New Zealand: A Research Synthesis. Australian

Accounting Review. 27(4).

Khorwatt, E., (2015) .Assessment of Business Risk and Control Risk in the Libyan Context.

Open Journal of Accounting.4.

Kristensen, R. H. (2015). Judgment in an auditor’s materiality assessments. Danish Journal

of Management & Business. 2.

The Institute of Chartered Accountants in England and Wales 2013. Audit and Assurance

Advanced Stage Technical Integration Level. [ONLINE] Available from

https://www.icaew.com/~/media/corporate/files/qualifications%20and

%20programmes/learning%20partners/learning%20materials/ti%20audit

%20assurance%2020142015%20inspection%20copy.ashx

Vîlsănoiua, & Buzenche (Matei),S. (2014). Determining Audit Materiality in the banking

industry- a knowledge based approach. Procedia Economics and Finance.15.

Woolworths Group (2016). Financial Report 2016. [ONLINE] Available from

https://wow2016ar.qreports.com.au/xresources/pdf/wow16ar-financial-report.pdf /

Woolworths Group Limited 2018 Portfolio Businesses [ONLINE] Available from

https://www.woolworthsgroup.com.au/page/about-us/our-brands/portfolio-businesses/

[Accessed 22nd May, 2018].

Woolworths Limited (2015). Annual Report 2015. [ONLINE] retrieved from

https://www.woolworthsgroup.com.au/icms_docs/182381_Annual_Report_2015.pdf

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.