Financial Analysis of Woolworths (ACC00724) - 2013-2017 Report

VerifiedAdded on 2023/06/10

|16

|3238

|339

Report

AI Summary

This report presents a comprehensive financial analysis of Woolworths, examining its performance from 2013 to 2017. The analysis begins with a horizontal analysis of the income statement, evaluating changes in revenue, expenses, and net income over the five-year period. The report then calculates and interprets various financial ratios, including return on assets, return on equity, operating profit margin, gross profit margin, inventory turnover, settlement period for debtors, current ratio, quick ratio, debt-to-assets ratio, interest cover ratio, assets turnover, earnings per share, price-earnings ratio, and dividend yield. The discussion covers profitability, efficiency, liquidity, financial gearing, and investment ratios, providing insights into Woolworths' financial health and performance trends. The report also includes a detailed calculation of each ratio, along with the formula used to derive the results.

Running head: ACCOUNTING FOR MANAGERS

Accounting for Managers

Name of the Student:

Name of the University:

Authors Note:

Accounting for Managers

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGERS

1

Table of Contents

C. Preparing Horizontal analysis of the Income Statement for Five years:...............................2

D. Calculating financial ratios of Woolworths from 2013 to 2017:..........................................3

E. Commenting on the profitability, efficiency, liquidity, financial gearing and investment

ratios of Woolworths from 2013 to 2017:..................................................................................9

Reference and Bibliography:....................................................................................................14

1

Table of Contents

C. Preparing Horizontal analysis of the Income Statement for Five years:...............................2

D. Calculating financial ratios of Woolworths from 2013 to 2017:..........................................3

E. Commenting on the profitability, efficiency, liquidity, financial gearing and investment

ratios of Woolworths from 2013 to 2017:..................................................................................9

Reference and Bibliography:....................................................................................................14

ACCOUNTING FOR MANAGERS

2

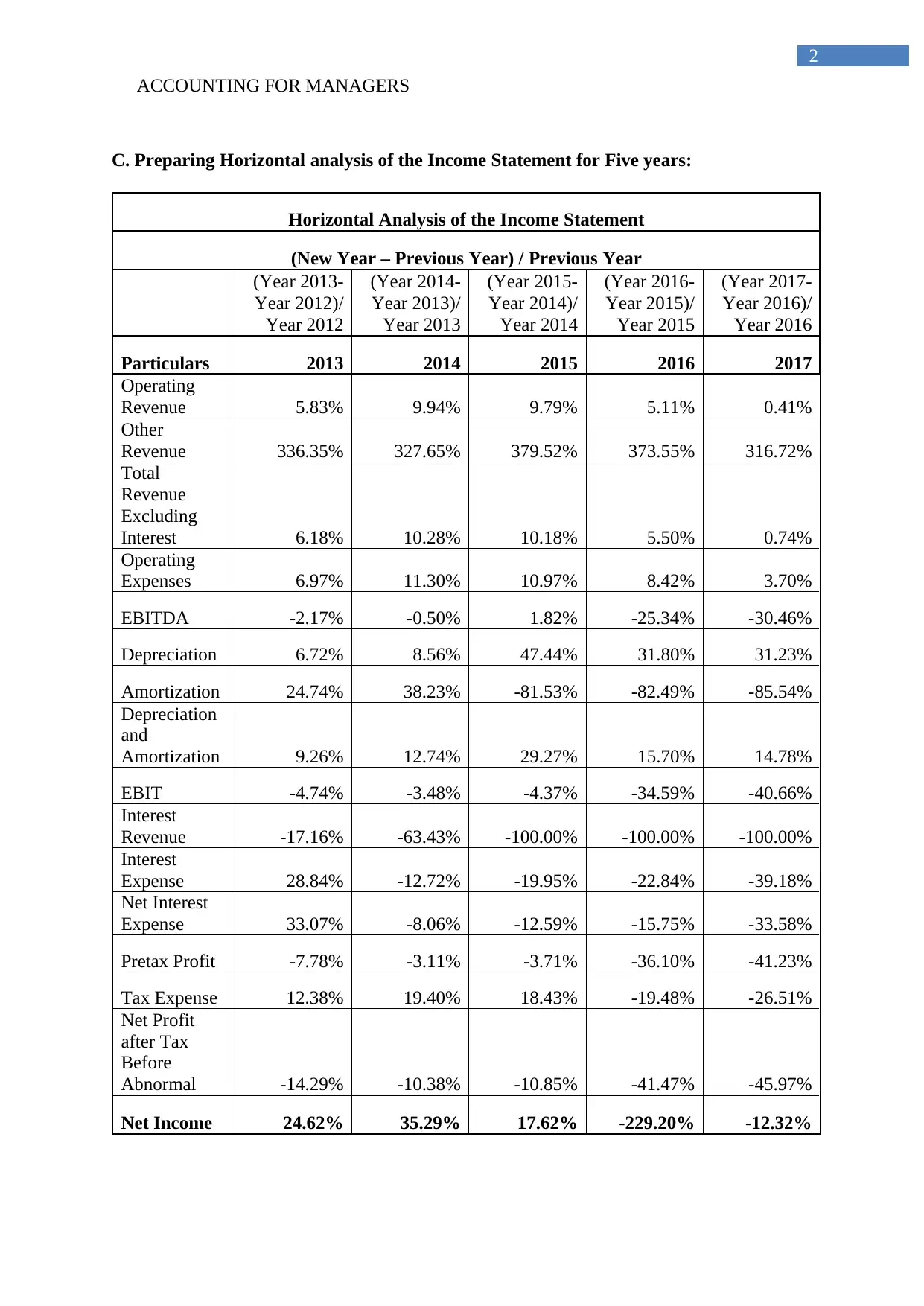

C. Preparing Horizontal analysis of the Income Statement for Five years:

Horizontal Analysis of the Income Statement

(New Year – Previous Year) / Previous Year

(Year 2013-

Year 2012)/

Year 2012

(Year 2014-

Year 2013)/

Year 2013

(Year 2015-

Year 2014)/

Year 2014

(Year 2016-

Year 2015)/

Year 2015

(Year 2017-

Year 2016)/

Year 2016

Particulars 2013 2014 2015 2016 2017

Operating

Revenue 5.83% 9.94% 9.79% 5.11% 0.41%

Other

Revenue 336.35% 327.65% 379.52% 373.55% 316.72%

Total

Revenue

Excluding

Interest 6.18% 10.28% 10.18% 5.50% 0.74%

Operating

Expenses 6.97% 11.30% 10.97% 8.42% 3.70%

EBITDA -2.17% -0.50% 1.82% -25.34% -30.46%

Depreciation 6.72% 8.56% 47.44% 31.80% 31.23%

Amortization 24.74% 38.23% -81.53% -82.49% -85.54%

Depreciation

and

Amortization 9.26% 12.74% 29.27% 15.70% 14.78%

EBIT -4.74% -3.48% -4.37% -34.59% -40.66%

Interest

Revenue -17.16% -63.43% -100.00% -100.00% -100.00%

Interest

Expense 28.84% -12.72% -19.95% -22.84% -39.18%

Net Interest

Expense 33.07% -8.06% -12.59% -15.75% -33.58%

Pretax Profit -7.78% -3.11% -3.71% -36.10% -41.23%

Tax Expense 12.38% 19.40% 18.43% -19.48% -26.51%

Net Profit

after Tax

Before

Abnormal -14.29% -10.38% -10.85% -41.47% -45.97%

Net Income 24.62% 35.29% 17.62% -229.20% -12.32%

2

C. Preparing Horizontal analysis of the Income Statement for Five years:

Horizontal Analysis of the Income Statement

(New Year – Previous Year) / Previous Year

(Year 2013-

Year 2012)/

Year 2012

(Year 2014-

Year 2013)/

Year 2013

(Year 2015-

Year 2014)/

Year 2014

(Year 2016-

Year 2015)/

Year 2015

(Year 2017-

Year 2016)/

Year 2016

Particulars 2013 2014 2015 2016 2017

Operating

Revenue 5.83% 9.94% 9.79% 5.11% 0.41%

Other

Revenue 336.35% 327.65% 379.52% 373.55% 316.72%

Total

Revenue

Excluding

Interest 6.18% 10.28% 10.18% 5.50% 0.74%

Operating

Expenses 6.97% 11.30% 10.97% 8.42% 3.70%

EBITDA -2.17% -0.50% 1.82% -25.34% -30.46%

Depreciation 6.72% 8.56% 47.44% 31.80% 31.23%

Amortization 24.74% 38.23% -81.53% -82.49% -85.54%

Depreciation

and

Amortization 9.26% 12.74% 29.27% 15.70% 14.78%

EBIT -4.74% -3.48% -4.37% -34.59% -40.66%

Interest

Revenue -17.16% -63.43% -100.00% -100.00% -100.00%

Interest

Expense 28.84% -12.72% -19.95% -22.84% -39.18%

Net Interest

Expense 33.07% -8.06% -12.59% -15.75% -33.58%

Pretax Profit -7.78% -3.11% -3.71% -36.10% -41.23%

Tax Expense 12.38% 19.40% 18.43% -19.48% -26.51%

Net Profit

after Tax

Before

Abnormal -14.29% -10.38% -10.85% -41.47% -45.97%

Net Income 24.62% 35.29% 17.62% -229.20% -12.32%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR MANAGERS

3

The above table mainly represents the overall horizontal analysis of Woolworths

Income statement from 2013 to 2017. In addition, base year for the evaluation of horizontal

analysis is taken as 2012, which helps in understanding the progress made by Woolworths

over the period of five years. From the evaluation it is understood that total revenue of the

company has declined, which has forced the company to reduce its net income. Moreover, the

continuous decline in expenses is witnessed for the organisation, which only indicates the

measure is taken by the company in curbing the declining revenues. Hence, from the

evaluation it is seen that the progress of Woolworths has declined immensely from the level

of 24.62% in net income during 2013 to -12.32% in 2017. This mainly portrays the low

financial capability of the company is maintaining the level of income and generating high

rate of profits from operations. In this context, Saleh (2016) stated that investors with the help

of horizontal analysis is able to identify the level of income, which a company could obtain

over the period of time by conducting relevant actions. On the other hand, Berg and

Bjarnegard (2016) criticises that due to the unethical actions of the organisation in

manipulating their annual report, the projections made by the investors become invalid.

The management of Woolworths need to comply with the changing trend and

amendment their operations to increase revenue and generate adequate income to support its

expenses. The continuation of losses incurred during 2016 needs to be stopped by the

management of Woolworths for smoothly conducing their operations.

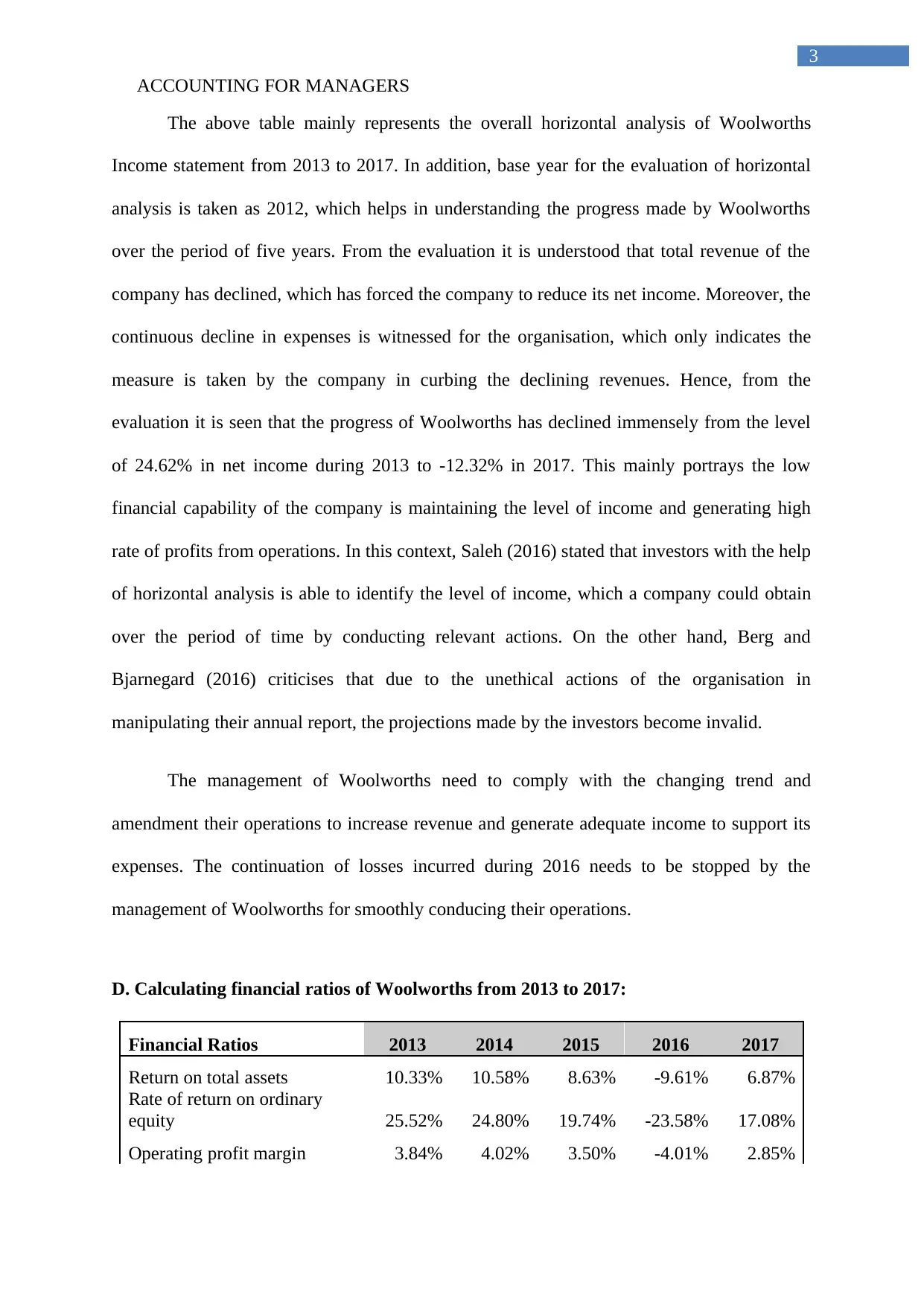

D. Calculating financial ratios of Woolworths from 2013 to 2017:

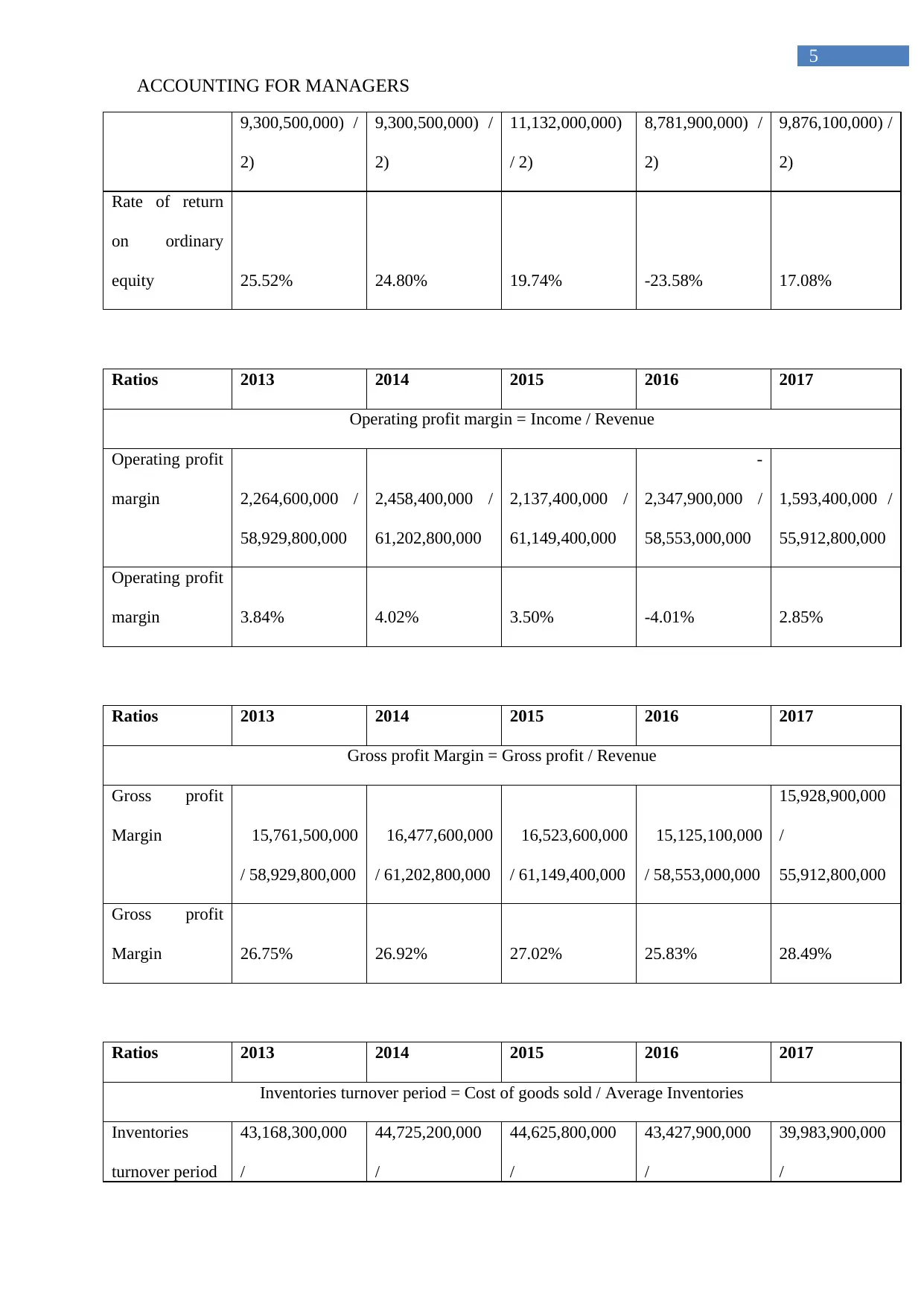

Financial Ratios 2013 2014 2015 2016 2017

Return on total assets 10.33% 10.58% 8.63% -9.61% 6.87%

Rate of return on ordinary

equity 25.52% 24.80% 19.74% -23.58% 17.08%

Operating profit margin 3.84% 4.02% 3.50% -4.01% 2.85%

3

The above table mainly represents the overall horizontal analysis of Woolworths

Income statement from 2013 to 2017. In addition, base year for the evaluation of horizontal

analysis is taken as 2012, which helps in understanding the progress made by Woolworths

over the period of five years. From the evaluation it is understood that total revenue of the

company has declined, which has forced the company to reduce its net income. Moreover, the

continuous decline in expenses is witnessed for the organisation, which only indicates the

measure is taken by the company in curbing the declining revenues. Hence, from the

evaluation it is seen that the progress of Woolworths has declined immensely from the level

of 24.62% in net income during 2013 to -12.32% in 2017. This mainly portrays the low

financial capability of the company is maintaining the level of income and generating high

rate of profits from operations. In this context, Saleh (2016) stated that investors with the help

of horizontal analysis is able to identify the level of income, which a company could obtain

over the period of time by conducting relevant actions. On the other hand, Berg and

Bjarnegard (2016) criticises that due to the unethical actions of the organisation in

manipulating their annual report, the projections made by the investors become invalid.

The management of Woolworths need to comply with the changing trend and

amendment their operations to increase revenue and generate adequate income to support its

expenses. The continuation of losses incurred during 2016 needs to be stopped by the

management of Woolworths for smoothly conducing their operations.

D. Calculating financial ratios of Woolworths from 2013 to 2017:

Financial Ratios 2013 2014 2015 2016 2017

Return on total assets 10.33% 10.58% 8.63% -9.61% 6.87%

Rate of return on ordinary

equity 25.52% 24.80% 19.74% -23.58% 17.08%

Operating profit margin 3.84% 4.02% 3.50% -4.01% 2.85%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGERS

4

Gross profit Margin 26.75% 26.92% 27.02% 25.83% 28.49%

Inventories turnover period 11 10 9 9 9

Settlement period for debtors 4 4 3 3 3

Current ratio 0.91 0.95 0.84 0.83 0.79

Quick ratio 0.29 0.33 0.30 0.32 0.33

Debt to assets ratio 58.20% 56.52% 56.06% 62.63% 56.90%

Interest cover ratio 9.1 13.6 14.7 10.4 12.0

Assets turnover 2.69 2.63 2.47 2.40 2.41

Earnings per share (cents) 180.72 194.61 169.43 -96.56 118.92

Price-earnings ratio

1815.48

%

1832.38

%

1616.62

%

-

2129.19

%

2132.49

%

Dividend yield 4.05% 3.84% 5.07% 3.75% 3.31%

Ratios 2013 2014 2015 2016 2017

Return on total assets = Income / Average Assets

Return on total

assets

2,264,600,000 /

((21,581,100,000

+

22,250,200,000)

/ 2)

2,458,400,000 /

((24,205,200,000

+

22,250,200,000)

/ 2)

2,137,400,000 /

((24,205,200,000

+

25,336,800,000)

/ 2)

-2,347,900,000 /

((23,502,200,000

+

25,336,800,000)

/ 2)

1,593,400,000 /

((23,502,200,000

+

22,915,800,000)

/ 2)

Return on total

assets 10.33% 10.58% 8.63% -9.61% 6.87%

Ratios 2013 2014 2015 2016 2017

Rate of return on ordinary equity = Income / Average Equity

Rate of return

on ordinary

equity

2,264,600,000 /

((8,446,300,000

+

2,458,400,000 /

((10,525,400,000

+

2,137,400,000 /

((10,525,400,000

+

-2,347,900,000 /

((11,132,000,00

0 +

1,593,400,000 /

((8,781,900,000

+

4

Gross profit Margin 26.75% 26.92% 27.02% 25.83% 28.49%

Inventories turnover period 11 10 9 9 9

Settlement period for debtors 4 4 3 3 3

Current ratio 0.91 0.95 0.84 0.83 0.79

Quick ratio 0.29 0.33 0.30 0.32 0.33

Debt to assets ratio 58.20% 56.52% 56.06% 62.63% 56.90%

Interest cover ratio 9.1 13.6 14.7 10.4 12.0

Assets turnover 2.69 2.63 2.47 2.40 2.41

Earnings per share (cents) 180.72 194.61 169.43 -96.56 118.92

Price-earnings ratio

1815.48

%

1832.38

%

1616.62

%

-

2129.19

%

2132.49

%

Dividend yield 4.05% 3.84% 5.07% 3.75% 3.31%

Ratios 2013 2014 2015 2016 2017

Return on total assets = Income / Average Assets

Return on total

assets

2,264,600,000 /

((21,581,100,000

+

22,250,200,000)

/ 2)

2,458,400,000 /

((24,205,200,000

+

22,250,200,000)

/ 2)

2,137,400,000 /

((24,205,200,000

+

25,336,800,000)

/ 2)

-2,347,900,000 /

((23,502,200,000

+

25,336,800,000)

/ 2)

1,593,400,000 /

((23,502,200,000

+

22,915,800,000)

/ 2)

Return on total

assets 10.33% 10.58% 8.63% -9.61% 6.87%

Ratios 2013 2014 2015 2016 2017

Rate of return on ordinary equity = Income / Average Equity

Rate of return

on ordinary

equity

2,264,600,000 /

((8,446,300,000

+

2,458,400,000 /

((10,525,400,000

+

2,137,400,000 /

((10,525,400,000

+

-2,347,900,000 /

((11,132,000,00

0 +

1,593,400,000 /

((8,781,900,000

+

ACCOUNTING FOR MANAGERS

5

9,300,500,000) /

2)

9,300,500,000) /

2)

11,132,000,000)

/ 2)

8,781,900,000) /

2)

9,876,100,000) /

2)

Rate of return

on ordinary

equity 25.52% 24.80% 19.74% -23.58% 17.08%

Ratios 2013 2014 2015 2016 2017

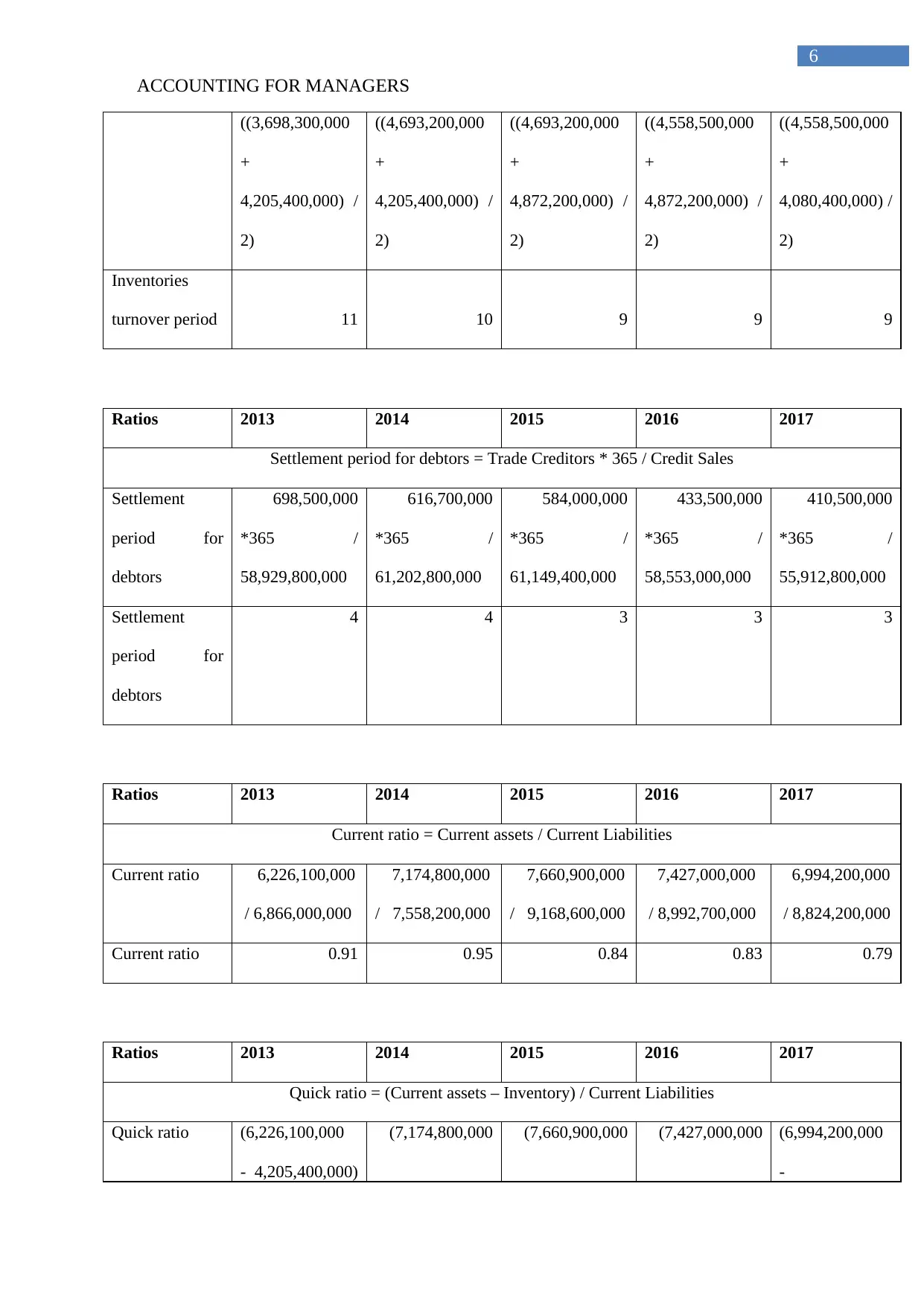

Operating profit margin = Income / Revenue

Operating profit

margin 2,264,600,000 /

58,929,800,000

2,458,400,000 /

61,202,800,000

2,137,400,000 /

61,149,400,000

-

2,347,900,000 /

58,553,000,000

1,593,400,000 /

55,912,800,000

Operating profit

margin 3.84% 4.02% 3.50% -4.01% 2.85%

Ratios 2013 2014 2015 2016 2017

Gross profit Margin = Gross profit / Revenue

Gross profit

Margin 15,761,500,000

/ 58,929,800,000

16,477,600,000

/ 61,202,800,000

16,523,600,000

/ 61,149,400,000

15,125,100,000

/ 58,553,000,000

15,928,900,000

/

55,912,800,000

Gross profit

Margin 26.75% 26.92% 27.02% 25.83% 28.49%

Ratios 2013 2014 2015 2016 2017

Inventories turnover period = Cost of goods sold / Average Inventories

Inventories

turnover period

43,168,300,000

/

44,725,200,000

/

44,625,800,000

/

43,427,900,000

/

39,983,900,000

/

5

9,300,500,000) /

2)

9,300,500,000) /

2)

11,132,000,000)

/ 2)

8,781,900,000) /

2)

9,876,100,000) /

2)

Rate of return

on ordinary

equity 25.52% 24.80% 19.74% -23.58% 17.08%

Ratios 2013 2014 2015 2016 2017

Operating profit margin = Income / Revenue

Operating profit

margin 2,264,600,000 /

58,929,800,000

2,458,400,000 /

61,202,800,000

2,137,400,000 /

61,149,400,000

-

2,347,900,000 /

58,553,000,000

1,593,400,000 /

55,912,800,000

Operating profit

margin 3.84% 4.02% 3.50% -4.01% 2.85%

Ratios 2013 2014 2015 2016 2017

Gross profit Margin = Gross profit / Revenue

Gross profit

Margin 15,761,500,000

/ 58,929,800,000

16,477,600,000

/ 61,202,800,000

16,523,600,000

/ 61,149,400,000

15,125,100,000

/ 58,553,000,000

15,928,900,000

/

55,912,800,000

Gross profit

Margin 26.75% 26.92% 27.02% 25.83% 28.49%

Ratios 2013 2014 2015 2016 2017

Inventories turnover period = Cost of goods sold / Average Inventories

Inventories

turnover period

43,168,300,000

/

44,725,200,000

/

44,625,800,000

/

43,427,900,000

/

39,983,900,000

/

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR MANAGERS

6

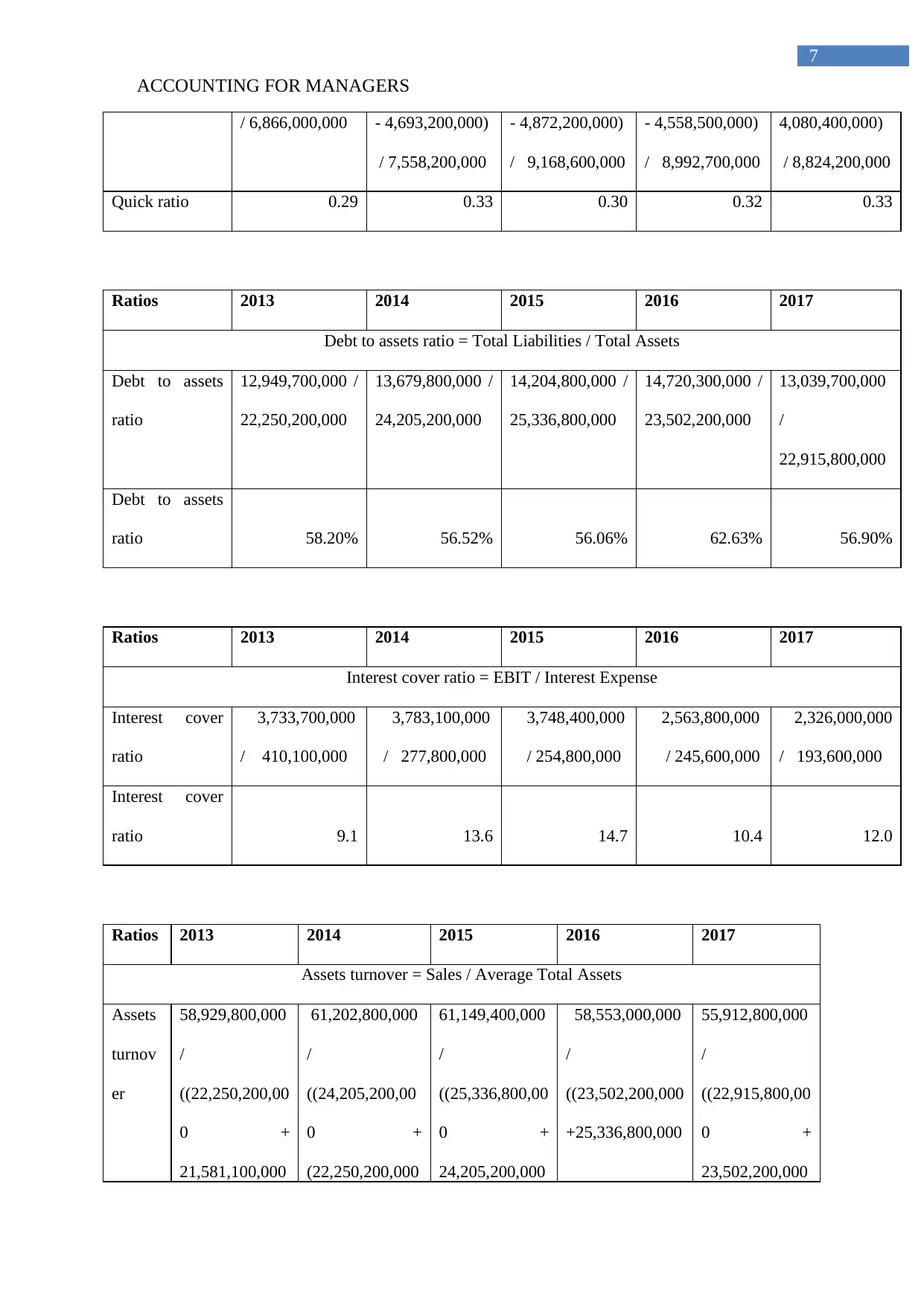

((3,698,300,000

+

4,205,400,000) /

2)

((4,693,200,000

+

4,205,400,000) /

2)

((4,693,200,000

+

4,872,200,000) /

2)

((4,558,500,000

+

4,872,200,000) /

2)

((4,558,500,000

+

4,080,400,000) /

2)

Inventories

turnover period 11 10 9 9 9

Ratios 2013 2014 2015 2016 2017

Settlement period for debtors = Trade Creditors * 365 / Credit Sales

Settlement

period for

debtors

698,500,000

*365 /

58,929,800,000

616,700,000

*365 /

61,202,800,000

584,000,000

*365 /

61,149,400,000

433,500,000

*365 /

58,553,000,000

410,500,000

*365 /

55,912,800,000

Settlement

period for

debtors

4 4 3 3 3

Ratios 2013 2014 2015 2016 2017

Current ratio = Current assets / Current Liabilities

Current ratio 6,226,100,000

/ 6,866,000,000

7,174,800,000

/ 7,558,200,000

7,660,900,000

/ 9,168,600,000

7,427,000,000

/ 8,992,700,000

6,994,200,000

/ 8,824,200,000

Current ratio 0.91 0.95 0.84 0.83 0.79

Ratios 2013 2014 2015 2016 2017

Quick ratio = (Current assets – Inventory) / Current Liabilities

Quick ratio (6,226,100,000

- 4,205,400,000)

(7,174,800,000 (7,660,900,000 (7,427,000,000 (6,994,200,000

-

6

((3,698,300,000

+

4,205,400,000) /

2)

((4,693,200,000

+

4,205,400,000) /

2)

((4,693,200,000

+

4,872,200,000) /

2)

((4,558,500,000

+

4,872,200,000) /

2)

((4,558,500,000

+

4,080,400,000) /

2)

Inventories

turnover period 11 10 9 9 9

Ratios 2013 2014 2015 2016 2017

Settlement period for debtors = Trade Creditors * 365 / Credit Sales

Settlement

period for

debtors

698,500,000

*365 /

58,929,800,000

616,700,000

*365 /

61,202,800,000

584,000,000

*365 /

61,149,400,000

433,500,000

*365 /

58,553,000,000

410,500,000

*365 /

55,912,800,000

Settlement

period for

debtors

4 4 3 3 3

Ratios 2013 2014 2015 2016 2017

Current ratio = Current assets / Current Liabilities

Current ratio 6,226,100,000

/ 6,866,000,000

7,174,800,000

/ 7,558,200,000

7,660,900,000

/ 9,168,600,000

7,427,000,000

/ 8,992,700,000

6,994,200,000

/ 8,824,200,000

Current ratio 0.91 0.95 0.84 0.83 0.79

Ratios 2013 2014 2015 2016 2017

Quick ratio = (Current assets – Inventory) / Current Liabilities

Quick ratio (6,226,100,000

- 4,205,400,000)

(7,174,800,000 (7,660,900,000 (7,427,000,000 (6,994,200,000

-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGERS

7

/ 6,866,000,000 - 4,693,200,000)

/ 7,558,200,000

- 4,872,200,000)

/ 9,168,600,000

- 4,558,500,000)

/ 8,992,700,000

4,080,400,000)

/ 8,824,200,000

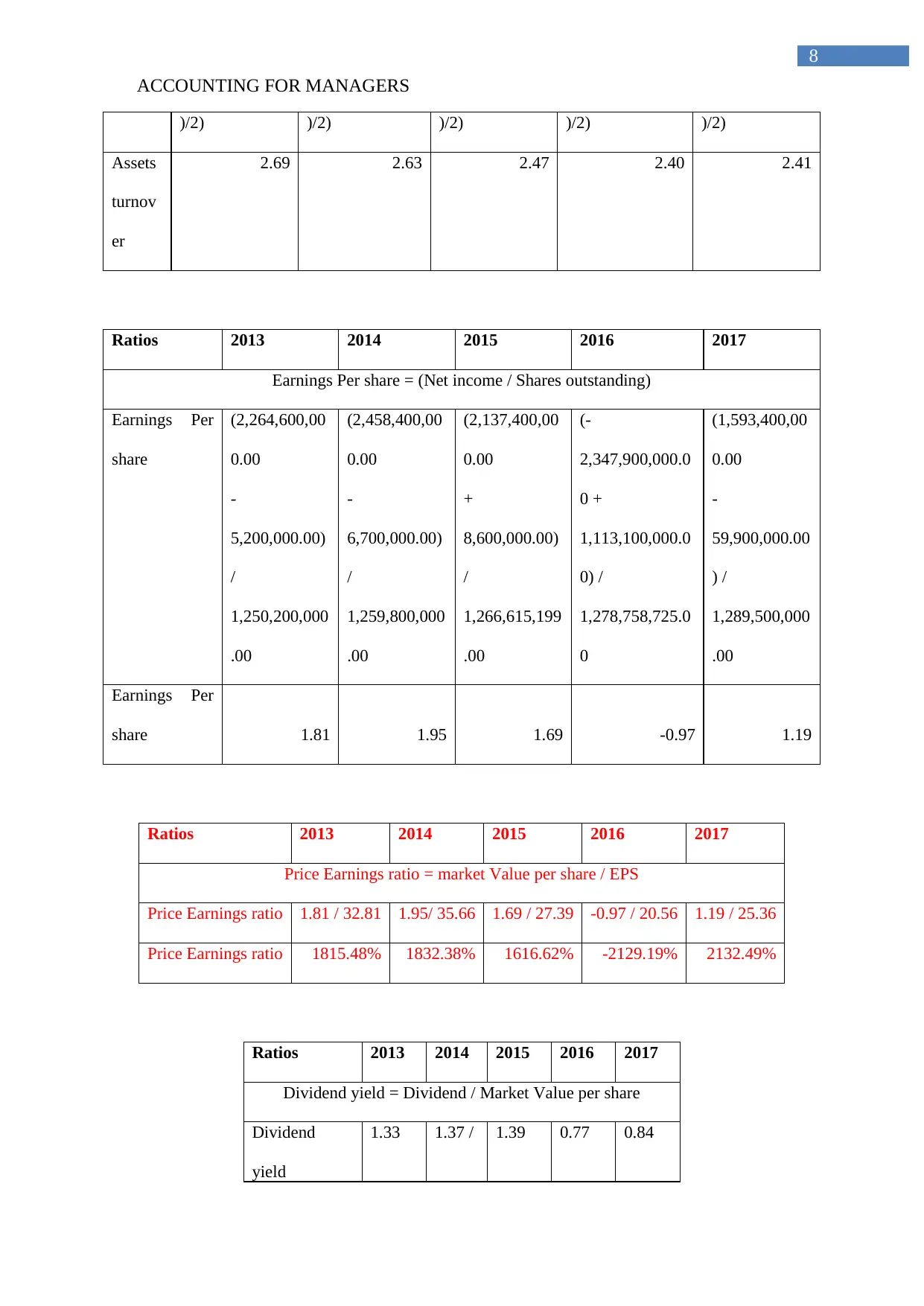

Quick ratio 0.29 0.33 0.30 0.32 0.33

Ratios 2013 2014 2015 2016 2017

Debt to assets ratio = Total Liabilities / Total Assets

Debt to assets

ratio

12,949,700,000 /

22,250,200,000

13,679,800,000 /

24,205,200,000

14,204,800,000 /

25,336,800,000

14,720,300,000 /

23,502,200,000

13,039,700,000

/

22,915,800,000

Debt to assets

ratio 58.20% 56.52% 56.06% 62.63% 56.90%

Ratios 2013 2014 2015 2016 2017

Interest cover ratio = EBIT / Interest Expense

Interest cover

ratio

3,733,700,000

/ 410,100,000

3,783,100,000

/ 277,800,000

3,748,400,000

/ 254,800,000

2,563,800,000

/ 245,600,000

2,326,000,000

/ 193,600,000

Interest cover

ratio 9.1 13.6 14.7 10.4 12.0

Ratios 2013 2014 2015 2016 2017

Assets turnover = Sales / Average Total Assets

Assets

turnov

er

58,929,800,000

/

((22,250,200,00

0 +

21,581,100,000

61,202,800,000

/

((24,205,200,00

0 +

(22,250,200,000

61,149,400,000

/

((25,336,800,00

0 +

24,205,200,000

58,553,000,000

/

((23,502,200,000

+25,336,800,000

55,912,800,000

/

((22,915,800,00

0 +

23,502,200,000

7

/ 6,866,000,000 - 4,693,200,000)

/ 7,558,200,000

- 4,872,200,000)

/ 9,168,600,000

- 4,558,500,000)

/ 8,992,700,000

4,080,400,000)

/ 8,824,200,000

Quick ratio 0.29 0.33 0.30 0.32 0.33

Ratios 2013 2014 2015 2016 2017

Debt to assets ratio = Total Liabilities / Total Assets

Debt to assets

ratio

12,949,700,000 /

22,250,200,000

13,679,800,000 /

24,205,200,000

14,204,800,000 /

25,336,800,000

14,720,300,000 /

23,502,200,000

13,039,700,000

/

22,915,800,000

Debt to assets

ratio 58.20% 56.52% 56.06% 62.63% 56.90%

Ratios 2013 2014 2015 2016 2017

Interest cover ratio = EBIT / Interest Expense

Interest cover

ratio

3,733,700,000

/ 410,100,000

3,783,100,000

/ 277,800,000

3,748,400,000

/ 254,800,000

2,563,800,000

/ 245,600,000

2,326,000,000

/ 193,600,000

Interest cover

ratio 9.1 13.6 14.7 10.4 12.0

Ratios 2013 2014 2015 2016 2017

Assets turnover = Sales / Average Total Assets

Assets

turnov

er

58,929,800,000

/

((22,250,200,00

0 +

21,581,100,000

61,202,800,000

/

((24,205,200,00

0 +

(22,250,200,000

61,149,400,000

/

((25,336,800,00

0 +

24,205,200,000

58,553,000,000

/

((23,502,200,000

+25,336,800,000

55,912,800,000

/

((22,915,800,00

0 +

23,502,200,000

ACCOUNTING FOR MANAGERS

8

)/2) )/2) )/2) )/2) )/2)

Assets

turnov

er

2.69 2.63 2.47 2.40 2.41

Ratios 2013 2014 2015 2016 2017

Earnings Per share = (Net income / Shares outstanding)

Earnings Per

share

(2,264,600,00

0.00

-

5,200,000.00)

/

1,250,200,000

.00

(2,458,400,00

0.00

-

6,700,000.00)

/

1,259,800,000

.00

(2,137,400,00

0.00

+

8,600,000.00)

/

1,266,615,199

.00

(-

2,347,900,000.0

0 +

1,113,100,000.0

0) /

1,278,758,725.0

0

(1,593,400,00

0.00

-

59,900,000.00

) /

1,289,500,000

.00

Earnings Per

share 1.81 1.95 1.69 -0.97 1.19

Ratios 2013 2014 2015 2016 2017

Price Earnings ratio = market Value per share / EPS

Price Earnings ratio 1.81 / 32.81 1.95/ 35.66 1.69 / 27.39 -0.97 / 20.56 1.19 / 25.36

Price Earnings ratio 1815.48% 1832.38% 1616.62% -2129.19% 2132.49%

Ratios 2013 2014 2015 2016 2017

Dividend yield = Dividend / Market Value per share

Dividend

yield

1.33 1.37 / 1.39 0.77 0.84

8

)/2) )/2) )/2) )/2) )/2)

Assets

turnov

er

2.69 2.63 2.47 2.40 2.41

Ratios 2013 2014 2015 2016 2017

Earnings Per share = (Net income / Shares outstanding)

Earnings Per

share

(2,264,600,00

0.00

-

5,200,000.00)

/

1,250,200,000

.00

(2,458,400,00

0.00

-

6,700,000.00)

/

1,259,800,000

.00

(2,137,400,00

0.00

+

8,600,000.00)

/

1,266,615,199

.00

(-

2,347,900,000.0

0 +

1,113,100,000.0

0) /

1,278,758,725.0

0

(1,593,400,00

0.00

-

59,900,000.00

) /

1,289,500,000

.00

Earnings Per

share 1.81 1.95 1.69 -0.97 1.19

Ratios 2013 2014 2015 2016 2017

Price Earnings ratio = market Value per share / EPS

Price Earnings ratio 1.81 / 32.81 1.95/ 35.66 1.69 / 27.39 -0.97 / 20.56 1.19 / 25.36

Price Earnings ratio 1815.48% 1832.38% 1616.62% -2129.19% 2132.49%

Ratios 2013 2014 2015 2016 2017

Dividend yield = Dividend / Market Value per share

Dividend

yield

1.33 1.37 / 1.39 0.77 0.84

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING FOR MANAGERS

9

/ 32.81 35.66 /

27.39

/ 20.56 / 25.36

Dividend

yield 4.05% 3.84% 5.07% 3.75% 3.31%

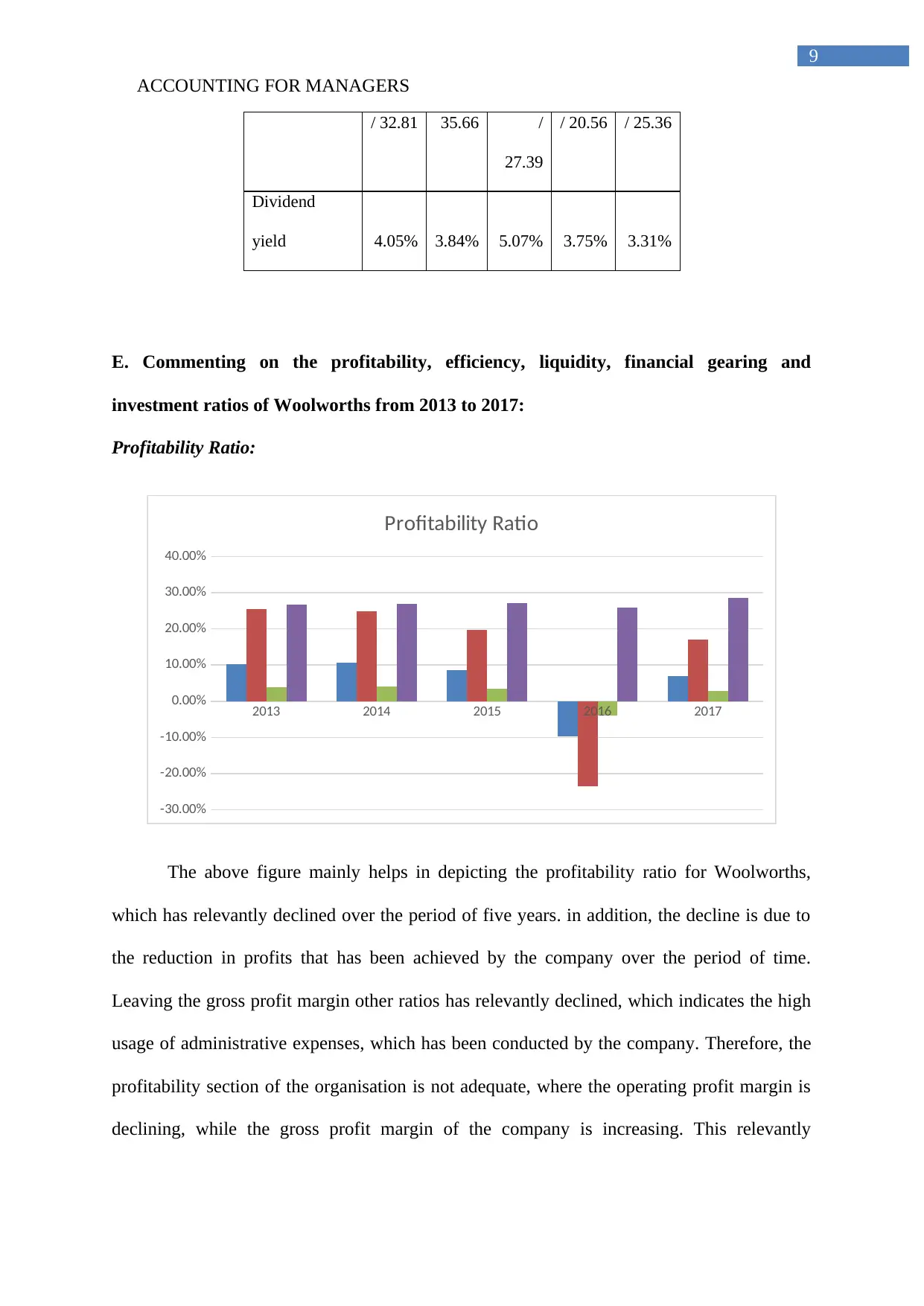

E. Commenting on the profitability, efficiency, liquidity, financial gearing and

investment ratios of Woolworths from 2013 to 2017:

Profitability Ratio:

2013 2014 2015 2016 2017

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

Profitability Ratio

The above figure mainly helps in depicting the profitability ratio for Woolworths,

which has relevantly declined over the period of five years. in addition, the decline is due to

the reduction in profits that has been achieved by the company over the period of time.

Leaving the gross profit margin other ratios has relevantly declined, which indicates the high

usage of administrative expenses, which has been conducted by the company. Therefore, the

profitability section of the organisation is not adequate, where the operating profit margin is

declining, while the gross profit margin of the company is increasing. This relevantly

9

/ 32.81 35.66 /

27.39

/ 20.56 / 25.36

Dividend

yield 4.05% 3.84% 5.07% 3.75% 3.31%

E. Commenting on the profitability, efficiency, liquidity, financial gearing and

investment ratios of Woolworths from 2013 to 2017:

Profitability Ratio:

2013 2014 2015 2016 2017

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

Profitability Ratio

The above figure mainly helps in depicting the profitability ratio for Woolworths,

which has relevantly declined over the period of five years. in addition, the decline is due to

the reduction in profits that has been achieved by the company over the period of time.

Leaving the gross profit margin other ratios has relevantly declined, which indicates the high

usage of administrative expenses, which has been conducted by the company. Therefore, the

profitability section of the organisation is not adequate, where the operating profit margin is

declining, while the gross profit margin of the company is increasing. This relevantly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR MANAGERS

10

indicates that the company is controlling its expenses in cost of sales, while increasing its

spending in administrative expenses (Soares and Pina 2017).

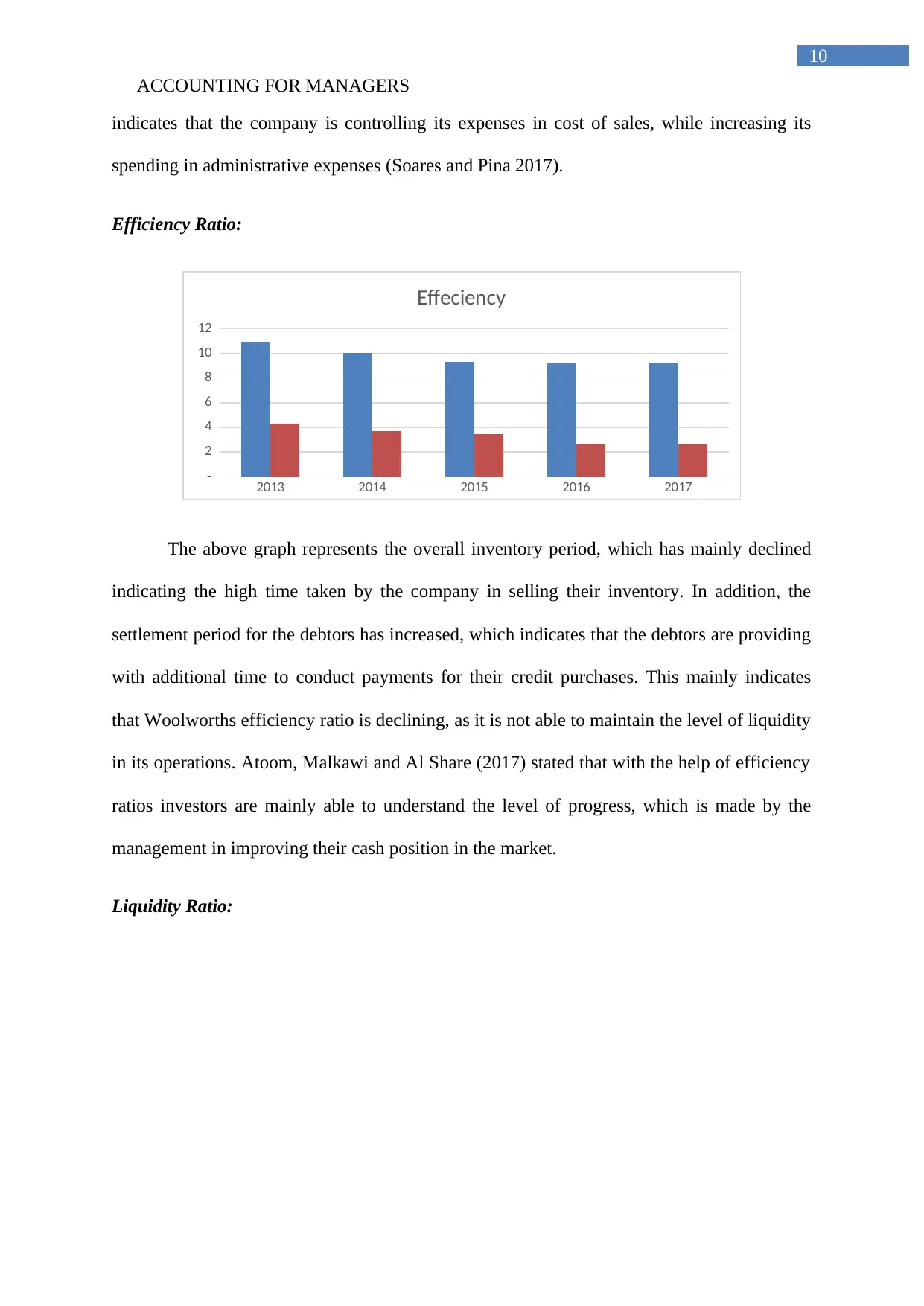

Efficiency Ratio:

2013 2014 2015 2016 2017

-

2

4

6

8

10

12

Effeciency

The above graph represents the overall inventory period, which has mainly declined

indicating the high time taken by the company in selling their inventory. In addition, the

settlement period for the debtors has increased, which indicates that the debtors are providing

with additional time to conduct payments for their credit purchases. This mainly indicates

that Woolworths efficiency ratio is declining, as it is not able to maintain the level of liquidity

in its operations. Atoom, Malkawi and Al Share (2017) stated that with the help of efficiency

ratios investors are mainly able to understand the level of progress, which is made by the

management in improving their cash position in the market.

Liquidity Ratio:

10

indicates that the company is controlling its expenses in cost of sales, while increasing its

spending in administrative expenses (Soares and Pina 2017).

Efficiency Ratio:

2013 2014 2015 2016 2017

-

2

4

6

8

10

12

Effeciency

The above graph represents the overall inventory period, which has mainly declined

indicating the high time taken by the company in selling their inventory. In addition, the

settlement period for the debtors has increased, which indicates that the debtors are providing

with additional time to conduct payments for their credit purchases. This mainly indicates

that Woolworths efficiency ratio is declining, as it is not able to maintain the level of liquidity

in its operations. Atoom, Malkawi and Al Share (2017) stated that with the help of efficiency

ratios investors are mainly able to understand the level of progress, which is made by the

management in improving their cash position in the market.

Liquidity Ratio:

ACCOUNTING FOR MANAGERS

11

2013 2014 2015 2016 2017

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Liquidity Ratio

The above figure helps in understanding the level of liquidity ratio of Woolworths

from 2013 to 2017. In addition, the liquidity ratios such as current and quick ratio mainly

indicates the current financial ability of Woolworths in conducting its operations after paying

for all its short-term obligations. from the evaluation it is detected that both current and quick

ratio of the organisation is not at desired levels, where the company is not accumulating

adequate current assets to compliments its current liability during adverse time (Rey and

Santelli 2017). The current ratios of the company have declined from 0.91 to 0.79 in five

years, where it needs to be at the level of 2. Furthermore, the quick ratio of the company has

improved over the period of five years, where the values has increased from 0.29 to 0.33,

while the values is lower than the standard 1, which needs to be maintained by the

organisation.

Financial Gearing:

11

2013 2014 2015 2016 2017

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Liquidity Ratio

The above figure helps in understanding the level of liquidity ratio of Woolworths

from 2013 to 2017. In addition, the liquidity ratios such as current and quick ratio mainly

indicates the current financial ability of Woolworths in conducting its operations after paying

for all its short-term obligations. from the evaluation it is detected that both current and quick

ratio of the organisation is not at desired levels, where the company is not accumulating

adequate current assets to compliments its current liability during adverse time (Rey and

Santelli 2017). The current ratios of the company have declined from 0.91 to 0.79 in five

years, where it needs to be at the level of 2. Furthermore, the quick ratio of the company has

improved over the period of five years, where the values has increased from 0.29 to 0.33,

while the values is lower than the standard 1, which needs to be maintained by the

organisation.

Financial Gearing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.