Enhanced Auditor Reporting: A Case Study of Woolworths Group

VerifiedAdded on 2023/06/05

|12

|3027

|98

AI Summary

This audit assignment highlights the significance of enhanced auditor reporting with Woolworths Group as a case study. It covers requirements for independence, provisions of non-audit services, auditors remuneration analysis, performed matters of audit, key matters of audit, responsibilities of directors and management, responsibilities of auditors, subsequent events, and more.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Audit Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

By student name

Professor

University

Date: 20th Sep 2018.

Executive Summary

1 | Page

By student name

Professor

University

Date: 20th Sep 2018.

Executive Summary

1 | Page

2

The objective of the assignment is to highlight the significance and crucial nature of enhanced auditor

reporting. As an illustration, Woolworths Group has been taken for the better understanding of the

concept. Upon analysing the annual report, it seems that the audit has done a good study on the

enhanced reporting front. From the viewpoint of the shareholders, sufficient information has been

provided necessary for a good understanding. It seems to me that no information that could be material

has been omitted.

Contents

Introduction.................................................................................................................................................4

2 | Page

The objective of the assignment is to highlight the significance and crucial nature of enhanced auditor

reporting. As an illustration, Woolworths Group has been taken for the better understanding of the

concept. Upon analysing the annual report, it seems that the audit has done a good study on the

enhanced reporting front. From the viewpoint of the shareholders, sufficient information has been

provided necessary for a good understanding. It seems to me that no information that could be material

has been omitted.

Contents

Introduction.................................................................................................................................................4

2 | Page

3

Requirements for Independence …………………………………………………………………………………………………..……….4

Provisions of non-audit services ……………………………………………………………………………………………………..…….4

Auditors remuneration Analysis ………………..………………………………………………………………………………………….4

Performed matters of audit and the Key matters of Audit..........................................................................5

Carrying value of Plant, Property and Equipment of Big W .......................................................................5

Provisioning of Inventory.............................................................................................................................5

Aspects of Accounting related to rebates....................................................................................................6

Information Technology Systems................................................................................................................6

Audit Committee.........................................................................................................................................5

Audit Opinion..............................................................................................................................................6

Responsibilities of the Directors and Management.....................................................................................6

Responsibilities of the Auditors...................................................................................................................6

Subsequent events that are material in nature...........................................................................................7

Assessment of material information...........................................................................................................7

Potential misreported or under-reported information...............................................................................7

Follow up questions.....................................................................................................................................8

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

3 | Page

Requirements for Independence …………………………………………………………………………………………………..……….4

Provisions of non-audit services ……………………………………………………………………………………………………..…….4

Auditors remuneration Analysis ………………..………………………………………………………………………………………….4

Performed matters of audit and the Key matters of Audit..........................................................................5

Carrying value of Plant, Property and Equipment of Big W .......................................................................5

Provisioning of Inventory.............................................................................................................................5

Aspects of Accounting related to rebates....................................................................................................6

Information Technology Systems................................................................................................................6

Audit Committee.........................................................................................................................................5

Audit Opinion..............................................................................................................................................6

Responsibilities of the Directors and Management.....................................................................................6

Responsibilities of the Auditors...................................................................................................................6

Subsequent events that are material in nature...........................................................................................7

Assessment of material information...........................................................................................................7

Potential misreported or under-reported information...............................................................................7

Follow up questions.....................................................................................................................................8

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

3 | Page

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

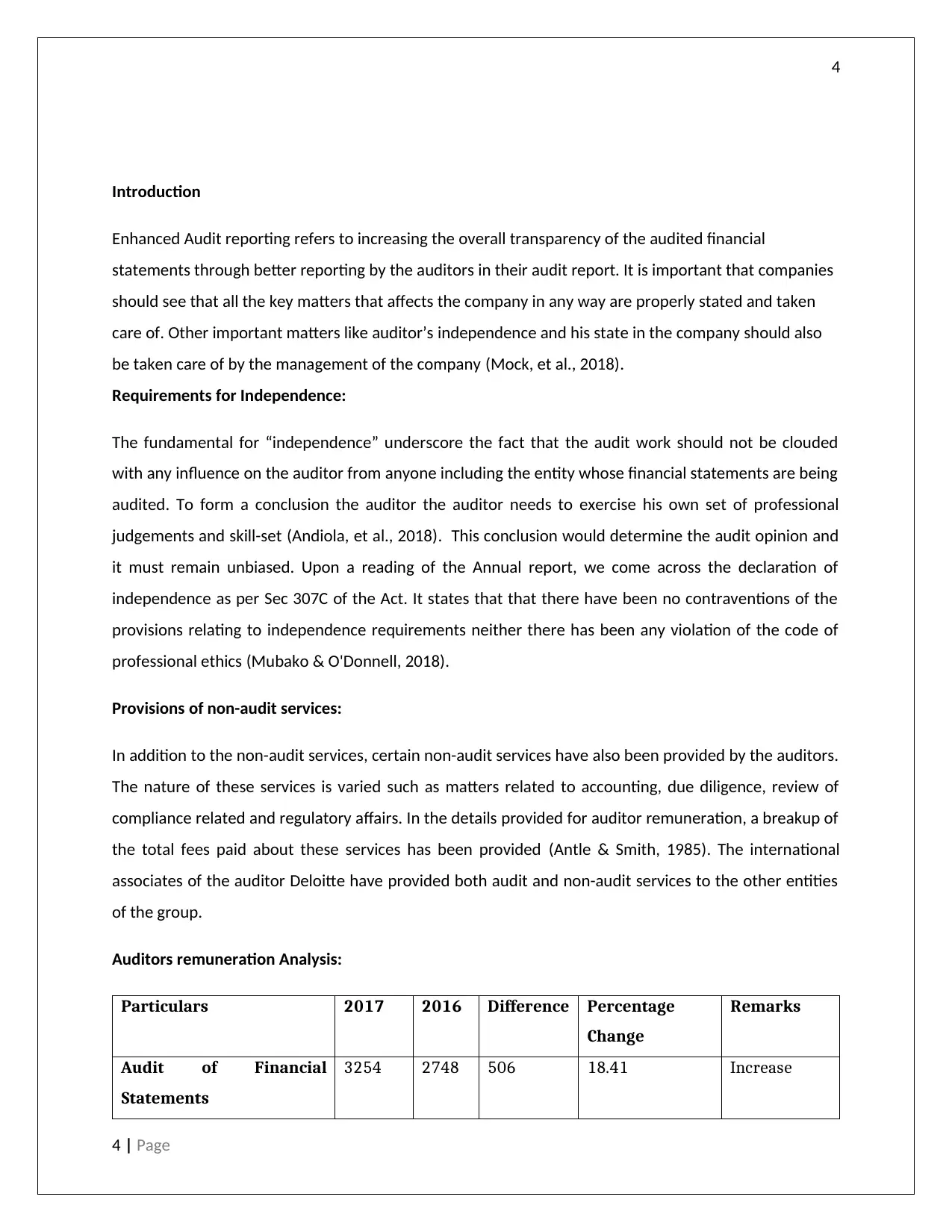

Introduction

Enhanced Audit reporting refers to increasing the overall transparency of the audited financial

statements through better reporting by the auditors in their audit report. It is important that companies

should see that all the key matters that affects the company in any way are properly stated and taken

care of. Other important matters like auditor’s independence and his state in the company should also

be taken care of by the management of the company (Mock, et al., 2018).

Requirements for Independence:

The fundamental for “independence” underscore the fact that the audit work should not be clouded

with any influence on the auditor from anyone including the entity whose financial statements are being

audited. To form a conclusion the auditor the auditor needs to exercise his own set of professional

judgements and skill-set (Andiola, et al., 2018). This conclusion would determine the audit opinion and

it must remain unbiased. Upon a reading of the Annual report, we come across the declaration of

independence as per Sec 307C of the Act. It states that that there have been no contraventions of the

provisions relating to independence requirements neither there has been any violation of the code of

professional ethics (Mubako & O'Donnell, 2018).

Provisions of non-audit services:

In addition to the non-audit services, certain non-audit services have also been provided by the auditors.

The nature of these services is varied such as matters related to accounting, due diligence, review of

compliance related and regulatory affairs. In the details provided for auditor remuneration, a breakup of

the total fees paid about these services has been provided (Antle & Smith, 1985). The international

associates of the auditor Deloitte have provided both audit and non-audit services to the other entities

of the group.

Auditors remuneration Analysis:

Particulars 2017 2016 Difference Percentage

Change

Remarks

Audit of Financial

Statements

3254 2748 506 18.41 Increase

4 | Page

Introduction

Enhanced Audit reporting refers to increasing the overall transparency of the audited financial

statements through better reporting by the auditors in their audit report. It is important that companies

should see that all the key matters that affects the company in any way are properly stated and taken

care of. Other important matters like auditor’s independence and his state in the company should also

be taken care of by the management of the company (Mock, et al., 2018).

Requirements for Independence:

The fundamental for “independence” underscore the fact that the audit work should not be clouded

with any influence on the auditor from anyone including the entity whose financial statements are being

audited. To form a conclusion the auditor the auditor needs to exercise his own set of professional

judgements and skill-set (Andiola, et al., 2018). This conclusion would determine the audit opinion and

it must remain unbiased. Upon a reading of the Annual report, we come across the declaration of

independence as per Sec 307C of the Act. It states that that there have been no contraventions of the

provisions relating to independence requirements neither there has been any violation of the code of

professional ethics (Mubako & O'Donnell, 2018).

Provisions of non-audit services:

In addition to the non-audit services, certain non-audit services have also been provided by the auditors.

The nature of these services is varied such as matters related to accounting, due diligence, review of

compliance related and regulatory affairs. In the details provided for auditor remuneration, a breakup of

the total fees paid about these services has been provided (Antle & Smith, 1985). The international

associates of the auditor Deloitte have provided both audit and non-audit services to the other entities

of the group.

Auditors remuneration Analysis:

Particulars 2017 2016 Difference Percentage

Change

Remarks

Audit of Financial

Statements

3254 2748 506 18.41 Increase

4 | Page

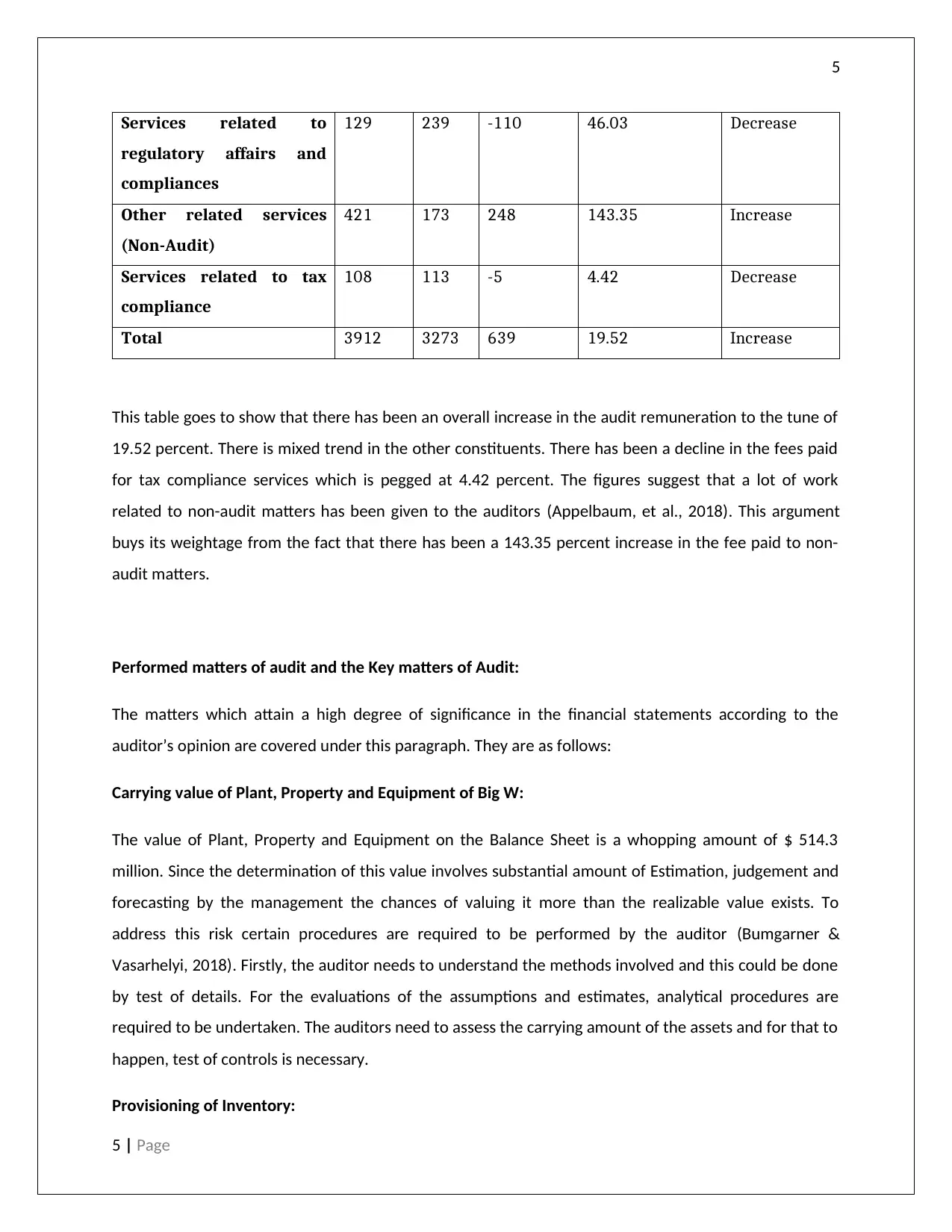

5

Services related to

regulatory affairs and

compliances

129 239 -110 46.03 Decrease

Other related services

(Non-Audit)

421 173 248 143.35 Increase

Services related to tax

compliance

108 113 -5 4.42 Decrease

Total 3912 3273 639 19.52 Increase

This table goes to show that there has been an overall increase in the audit remuneration to the tune of

19.52 percent. There is mixed trend in the other constituents. There has been a decline in the fees paid

for tax compliance services which is pegged at 4.42 percent. The figures suggest that a lot of work

related to non-audit matters has been given to the auditors (Appelbaum, et al., 2018). This argument

buys its weightage from the fact that there has been a 143.35 percent increase in the fee paid to non-

audit matters.

Performed matters of audit and the Key matters of Audit:

The matters which attain a high degree of significance in the financial statements according to the

auditor’s opinion are covered under this paragraph. They are as follows:

Carrying value of Plant, Property and Equipment of Big W:

The value of Plant, Property and Equipment on the Balance Sheet is a whopping amount of $ 514.3

million. Since the determination of this value involves substantial amount of Estimation, judgement and

forecasting by the management the chances of valuing it more than the realizable value exists. To

address this risk certain procedures are required to be performed by the auditor (Bumgarner &

Vasarhelyi, 2018). Firstly, the auditor needs to understand the methods involved and this could be done

by test of details. For the evaluations of the assumptions and estimates, analytical procedures are

required to be undertaken. The auditors need to assess the carrying amount of the assets and for that to

happen, test of controls is necessary.

Provisioning of Inventory:

5 | Page

Services related to

regulatory affairs and

compliances

129 239 -110 46.03 Decrease

Other related services

(Non-Audit)

421 173 248 143.35 Increase

Services related to tax

compliance

108 113 -5 4.42 Decrease

Total 3912 3273 639 19.52 Increase

This table goes to show that there has been an overall increase in the audit remuneration to the tune of

19.52 percent. There is mixed trend in the other constituents. There has been a decline in the fees paid

for tax compliance services which is pegged at 4.42 percent. The figures suggest that a lot of work

related to non-audit matters has been given to the auditors (Appelbaum, et al., 2018). This argument

buys its weightage from the fact that there has been a 143.35 percent increase in the fee paid to non-

audit matters.

Performed matters of audit and the Key matters of Audit:

The matters which attain a high degree of significance in the financial statements according to the

auditor’s opinion are covered under this paragraph. They are as follows:

Carrying value of Plant, Property and Equipment of Big W:

The value of Plant, Property and Equipment on the Balance Sheet is a whopping amount of $ 514.3

million. Since the determination of this value involves substantial amount of Estimation, judgement and

forecasting by the management the chances of valuing it more than the realizable value exists. To

address this risk certain procedures are required to be performed by the auditor (Bumgarner &

Vasarhelyi, 2018). Firstly, the auditor needs to understand the methods involved and this could be done

by test of details. For the evaluations of the assumptions and estimates, analytical procedures are

required to be undertaken. The auditors need to assess the carrying amount of the assets and for that to

happen, test of controls is necessary.

Provisioning of Inventory:

5 | Page

6

The accounting policy followed by the company states that the inventory of the company would be

valued at the cost price or net recoverable value, whichever is lower. The total inventories of the group

amounted to $ 4,080.4 million. For dealing with different factors like obsolescence, trends, it was

important to evaluate the process adopted for this and hence test of controls was required. For value

testing, certain items were selected on a sample basis as well

Aspects of Accounting related to rebates:

The suppliers of the group offer certain discounts and rebates often as the group has a big size and thus

procures in large quantities. The company has a practice which involves lowering he costs of the

products with amount of rebate or discount received. However, the timing of recognizing these

incentives is a tricky. Since this area is a key matter for the auditor, hence the requirement of control

testing and performing analytical procedures are very much required, as test of controls is the best tool

for determining the robustness of the controls (Kim, et al., 2017).

Information Technology Systems:

The IT systems in place are critical to the business operations. The systems are integrated to one

another. Assessing the degree of effectiveness and the efficiency of the IT systems are of paramount

importance. Collecting required information for the audit of the same was done using enquiry as a tool.

This enabled the auditor to obtain an understanding of the entity’s degree of reliance on its IT systems

about day to day activities. The IT tools testing involves two forms of testing one being substantive tests

of details and the other being controls testing (Kim, et al., 2017).

Audit Committee:

The group complies with the statutory guidelines regarding audit committee. The committee has five

members and is headed by its Chairman Michael Elmer. Hundred percent of the members on the

committee are non-executive directors.

The major issues covered in the charter are as under:

Objectives of the committee: One primary objective of the board is to provide advice and

guidance on working within the governance frame work of the entity. The audit committee also

has a role to play in managing the risks and providing recommendations for an effective and

6 | Page

The accounting policy followed by the company states that the inventory of the company would be

valued at the cost price or net recoverable value, whichever is lower. The total inventories of the group

amounted to $ 4,080.4 million. For dealing with different factors like obsolescence, trends, it was

important to evaluate the process adopted for this and hence test of controls was required. For value

testing, certain items were selected on a sample basis as well

Aspects of Accounting related to rebates:

The suppliers of the group offer certain discounts and rebates often as the group has a big size and thus

procures in large quantities. The company has a practice which involves lowering he costs of the

products with amount of rebate or discount received. However, the timing of recognizing these

incentives is a tricky. Since this area is a key matter for the auditor, hence the requirement of control

testing and performing analytical procedures are very much required, as test of controls is the best tool

for determining the robustness of the controls (Kim, et al., 2017).

Information Technology Systems:

The IT systems in place are critical to the business operations. The systems are integrated to one

another. Assessing the degree of effectiveness and the efficiency of the IT systems are of paramount

importance. Collecting required information for the audit of the same was done using enquiry as a tool.

This enabled the auditor to obtain an understanding of the entity’s degree of reliance on its IT systems

about day to day activities. The IT tools testing involves two forms of testing one being substantive tests

of details and the other being controls testing (Kim, et al., 2017).

Audit Committee:

The group complies with the statutory guidelines regarding audit committee. The committee has five

members and is headed by its Chairman Michael Elmer. Hundred percent of the members on the

committee are non-executive directors.

The major issues covered in the charter are as under:

Objectives of the committee: One primary objective of the board is to provide advice and

guidance on working within the governance frame work of the entity. The audit committee also

has a role to play in managing the risks and providing recommendations for an effective and

6 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

efficient system of internal control. Various other areas are also covered under the ambit of the

committee such as recommendation related to the compliance framework, oversight of the

audit functions of the entity (Both internal and external), adherence to the accounting policies

and monitoring of the financial reporting framework.

Authoritative powers of the committee: The audit committee can act within the purview of the

charter. The committee has the power to discuss organization specific to the internal as well as

external auditors. There is no requirement of a presence of any other member of the

management when the discussions happen. No restrictions can be imposed on the committee

relating to access over records of the company the and senior management. When the need

arises, the committee is entitled to take technical help from an external agency or person who

has some level of expertise in concern (Kangarluie & Aalizadeh, 2017).

Composition of the committee: The formation of the committee takes place by a minimum of

three directors. There are restrictions on the quantum of non-independent directors in this

regard. The charter requires that most of the members on the committee must be independent

directors. All the members should some possess some level of financial literacy meaning that the

must understand how to read and analyze a set of financial statements. The members should

have some idea about business processes and dynamics of competitive corporate environment.

Chairman of the committee should be an independent director who will be appointed by the

board of directors from amongst the members of the audit committee. A member can be

appointed or re-appointed as per the discretion of the board. A person who is an executive

director cannot be made a member of the board. The secretary to the committee will be the

company secretary. For ensuring the right balance of experience and skill-set, the composition

of the committee will be subjected to process of annual review.

Responsibilities of the committee:

a) Providing recommendations to the board on the appointment and selection of statutory

auditors.

b) Evaluations of the policies of the company and recommendations on enhancing and

strengthening of the governance framework and providing an oversight mechanism for it.

c) Review the work of the internal audit function and discuss the issues to resolve and plug the

loopholes. They also need to assess the performance of the statutory auditors, deal with the

observations made in the audit report and re-negotiate their re-appointment based on the

assessment (Garon, 2018).

7 | Page

efficient system of internal control. Various other areas are also covered under the ambit of the

committee such as recommendation related to the compliance framework, oversight of the

audit functions of the entity (Both internal and external), adherence to the accounting policies

and monitoring of the financial reporting framework.

Authoritative powers of the committee: The audit committee can act within the purview of the

charter. The committee has the power to discuss organization specific to the internal as well as

external auditors. There is no requirement of a presence of any other member of the

management when the discussions happen. No restrictions can be imposed on the committee

relating to access over records of the company the and senior management. When the need

arises, the committee is entitled to take technical help from an external agency or person who

has some level of expertise in concern (Kangarluie & Aalizadeh, 2017).

Composition of the committee: The formation of the committee takes place by a minimum of

three directors. There are restrictions on the quantum of non-independent directors in this

regard. The charter requires that most of the members on the committee must be independent

directors. All the members should some possess some level of financial literacy meaning that the

must understand how to read and analyze a set of financial statements. The members should

have some idea about business processes and dynamics of competitive corporate environment.

Chairman of the committee should be an independent director who will be appointed by the

board of directors from amongst the members of the audit committee. A member can be

appointed or re-appointed as per the discretion of the board. A person who is an executive

director cannot be made a member of the board. The secretary to the committee will be the

company secretary. For ensuring the right balance of experience and skill-set, the composition

of the committee will be subjected to process of annual review.

Responsibilities of the committee:

a) Providing recommendations to the board on the appointment and selection of statutory

auditors.

b) Evaluations of the policies of the company and recommendations on enhancing and

strengthening of the governance framework and providing an oversight mechanism for it.

c) Review the work of the internal audit function and discuss the issues to resolve and plug the

loopholes. They also need to assess the performance of the statutory auditors, deal with the

observations made in the audit report and re-negotiate their re-appointment based on the

assessment (Garon, 2018).

7 | Page

8

Audit Opinion:

The audit opinion states that the preparation of the financial statements have been made as per

the financial reporting framework and it complies to the Australian accounting standards as well

as the Corporation regulation 2001. The statements present a true and fair view of the of the

group.

Responsibilities of the Directors and Management:

Directors and management are responsible for preparation of the financial statements in

compliance with statutes prevalent such as the accounting standards and the Corporations Act

2001 such that the report gives a true and fair picture of the. In doing this it is their duty to

ensure that any material misstatement does not exist in the financials and that necessary and

appropriate internal controls are in place and are operating effectively and efficiently for the

preparations of the statements. They must keep in consideration the corporation’s ability to

continue to exist as a going concern while preparing the financial statements (Lessambo, 2018).

Responsibilities of the Auditor:

It is the responsibility of the auditor to provide an opinion on the financial statements. He must

provide a reasonable assurance that the financial statements do not contain any material miss-

statement whether because an error or fraud and that the assurance is based on the sufficient

appropriate audit evidence obtained during the year (Fukukawa & Mock, 2011). The report is

addressed to the equity shareholders of the company. The thing to be kept in mind in here is

that reasonable assurance can never be construed as a guarantee, it is simply an opinion that

has come out from professional judgement.

Subsequent events that are material in nature:

The company made an exit from one of its business verticals namely Home Improvement and

thus the following events related to it have taken place:

A share sale agreement was entered into by the company with Home consortium in

which an agreement was made for sale of 66.7% shares of Hydrox. The agreement

included acquisition of 20 of the master’s leasehold sites, 40 trading sites and 21

8 | Page

Audit Opinion:

The audit opinion states that the preparation of the financial statements have been made as per

the financial reporting framework and it complies to the Australian accounting standards as well

as the Corporation regulation 2001. The statements present a true and fair view of the of the

group.

Responsibilities of the Directors and Management:

Directors and management are responsible for preparation of the financial statements in

compliance with statutes prevalent such as the accounting standards and the Corporations Act

2001 such that the report gives a true and fair picture of the. In doing this it is their duty to

ensure that any material misstatement does not exist in the financials and that necessary and

appropriate internal controls are in place and are operating effectively and efficiently for the

preparations of the statements. They must keep in consideration the corporation’s ability to

continue to exist as a going concern while preparing the financial statements (Lessambo, 2018).

Responsibilities of the Auditor:

It is the responsibility of the auditor to provide an opinion on the financial statements. He must

provide a reasonable assurance that the financial statements do not contain any material miss-

statement whether because an error or fraud and that the assurance is based on the sufficient

appropriate audit evidence obtained during the year (Fukukawa & Mock, 2011). The report is

addressed to the equity shareholders of the company. The thing to be kept in mind in here is

that reasonable assurance can never be construed as a guarantee, it is simply an opinion that

has come out from professional judgement.

Subsequent events that are material in nature:

The company made an exit from one of its business verticals namely Home Improvement and

thus the following events related to it have taken place:

A share sale agreement was entered into by the company with Home consortium in

which an agreement was made for sale of 66.7% shares of Hydrox. The agreement

included acquisition of 20 of the master’s leasehold sites, 40 trading sites and 21

8 | Page

9

freehold development sites. There was an obligation for Woolworth for taking

responsibilities of liabilities of 11 master leases and acquisition of 3 master freehold

sites.

In a trust where Home consortium was a beneficiary, shares of Hydrox pertaining to

Lowe were sold to that trust.

The mammoth capital losses which occurred after the date of balance sheet were the outcome of sale

decision of Hydrox. Upon completion of transaction with Home consortium, the capital losses are

estimated to be pegged at $1.8 billion. Deferred tax asset has not been recognized because the group

estimates sufficient future capital gains against which such losses could be utilized.

Assessment of material information reporting by auditor from the perspective of a third-party

stakeholder who has interests:

As third party I believe the information is effective particularly on key matters. The segment wise

information gives a good picture on the performance of each of the segments. It is easier to understand

and analyze as to which is the best performing segment on various fronts of profitability and sales. The

segregation of financial risk management into various categories also helped in making decisions (Bailey,

et al., 2017).

Potential misreported or under-reported information which has not been communicated in an

effective manner:

The carrying value of plant, property and equipment involved estimates and forecast to be made. Those

required some more detailed explanation. Disclosure relating to inventory provision would also have

been beneficial.

Follow-up questions for the auditor at the AGM:

Did any whistleblowing matters took place? If yes, how did the investigation take place and

was the results that came out of it?

Was any deficiency noticed in internal control and whether they were discussed with the

appropriate people? Reasons for not considering deficiencies, if any, material/

9 | Page

freehold development sites. There was an obligation for Woolworth for taking

responsibilities of liabilities of 11 master leases and acquisition of 3 master freehold

sites.

In a trust where Home consortium was a beneficiary, shares of Hydrox pertaining to

Lowe were sold to that trust.

The mammoth capital losses which occurred after the date of balance sheet were the outcome of sale

decision of Hydrox. Upon completion of transaction with Home consortium, the capital losses are

estimated to be pegged at $1.8 billion. Deferred tax asset has not been recognized because the group

estimates sufficient future capital gains against which such losses could be utilized.

Assessment of material information reporting by auditor from the perspective of a third-party

stakeholder who has interests:

As third party I believe the information is effective particularly on key matters. The segment wise

information gives a good picture on the performance of each of the segments. It is easier to understand

and analyze as to which is the best performing segment on various fronts of profitability and sales. The

segregation of financial risk management into various categories also helped in making decisions (Bailey,

et al., 2017).

Potential misreported or under-reported information which has not been communicated in an

effective manner:

The carrying value of plant, property and equipment involved estimates and forecast to be made. Those

required some more detailed explanation. Disclosure relating to inventory provision would also have

been beneficial.

Follow-up questions for the auditor at the AGM:

Did any whistleblowing matters took place? If yes, how did the investigation take place and

was the results that came out of it?

Was any deficiency noticed in internal control and whether they were discussed with the

appropriate people? Reasons for not considering deficiencies, if any, material/

9 | Page

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

Conclusion:

The enhanced requirements related to reporting have been taken care of by the auditors and they have

acted within the framework and discharged their duties and responsibilities in accordance with the act

and standards in place. The users of the financial statements are better informed through the report.

10 | Page

Conclusion:

The enhanced requirements related to reporting have been taken care of by the auditors and they have

acted within the framework and discharged their duties and responsibilities in accordance with the act

and standards in place. The users of the financial statements are better informed through the report.

10 | Page

11

References

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit Documentation,

and Closing Review Notes in the Audit of Accounts Receivable. Issues in Accounting Education, 33(2), pp.

43-55.

Antle, R. & Smith, A., 1985. Measuring Executive Compensation: Methods and an Application. Journal of

Accounting Research , 23(1), pp. 296-325.

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics.. Journal of Accounting

Literature, 40(1), pp. 83-101.

Bailey, C., Collins, D. & Abbott, L., 2017. The Impact of Enterprise Risk Management on the Audit

Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of Practice & Theory, 37(3), pp.

25-46.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Garon, J., 2018. Ownership of University Intellectual Property. Cardozo Arts & Ent. LJ, 36(1), p. 635.

Kangarluie, S. & Aalizadeh, A., 2017. 'The expectation gap in auditing. Accounting, 3(1), pp. 19-22.

Kim, M., Schmidgall, R. & Damitio, J., 2017. Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of Hospitality &

Tourism Administration, , 18(1), pp. 23-40.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Mock, T. J., Ragothaman, S. C. & Srivastava, R. P., 2018. Using Evidential Reasoning Technology to

Enhance the Audit Quality Assurance Inspection Process. Journal of Emerging Technologies in

Accounting, 15(1), pp. 29-43.

Mubako, G. & O'Donnell, E., 2018. Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), pp. 55-64.

11 | Page

References

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit Documentation,

and Closing Review Notes in the Audit of Accounts Receivable. Issues in Accounting Education, 33(2), pp.

43-55.

Antle, R. & Smith, A., 1985. Measuring Executive Compensation: Methods and an Application. Journal of

Accounting Research , 23(1), pp. 296-325.

Appelbaum, D., Kogan, A. & Vasarhelyi, M., 2018. Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics.. Journal of Accounting

Literature, 40(1), pp. 83-101.

Bailey, C., Collins, D. & Abbott, L., 2017. The Impact of Enterprise Risk Management on the Audit

Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of Practice & Theory, 37(3), pp.

25-46.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Garon, J., 2018. Ownership of University Intellectual Property. Cardozo Arts & Ent. LJ, 36(1), p. 635.

Kangarluie, S. & Aalizadeh, A., 2017. 'The expectation gap in auditing. Accounting, 3(1), pp. 19-22.

Kim, M., Schmidgall, R. & Damitio, J., 2017. Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of Hospitality &

Tourism Administration, , 18(1), pp. 23-40.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Mock, T. J., Ragothaman, S. C. & Srivastava, R. P., 2018. Using Evidential Reasoning Technology to

Enhance the Audit Quality Assurance Inspection Process. Journal of Emerging Technologies in

Accounting, 15(1), pp. 29-43.

Mubako, G. & O'Donnell, E., 2018. Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), pp. 55-64.

11 | Page

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.