Financial Analysis Report of Woolworths Group Limited

VerifiedAdded on 2023/06/07

|22

|3972

|70

AI Summary

This report is an independent analysis of the financial performance and position of Woolworths Group Limited for the five year period 2013 to 2017. It includes ratio analysis, profitability analysis, liquidity ratios, and overall industry analysis. The report compares the financial performance of Woolworths Group Limited with focus on the profitability indicators, liquidity, efficiency in operations, and financial structure. The report interprets the elements of the financial statement using ratio analysis through evaluation of critical elements in the statements that affect performance in one way or another.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL ANALYSIS

REPORT

WOOLWORTHS GROUP LIMITED.

REPORT

WOOLWORTHS GROUP LIMITED.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

This is an independent analysis of the financial performance and position of Woolworths Group

Limited for the five year period 2013 to 2017 as requested by the board of directors. It is a report

on the findings achieved after the analysis of the company’s financial statements including the

statement of financial position, Income statement and the cash flow statement. The study of the

various elements in the individual statements will gave insight on how well the company was

performing i.e. whether the company improved, dropped or stagnated in its performance in a

particular area as far as performance is concerned and the best explanation for any of the

performance pattern that might have been noted. The trend analysis had focus on 2017 the base

and most current year as this is the year that indicated the final trend from the review of the rest

of the period. Ratio analysis played a vital role in the analysis as it helped to specifically identify

relationship between various elements in the financial statements that projected the company’s

performance. The report further gives recommendations after evaluation of the various critical

performance indicators that helped correct deviations and also appraised elements that enhanced

performance.

This is an independent analysis of the financial performance and position of Woolworths Group

Limited for the five year period 2013 to 2017 as requested by the board of directors. It is a report

on the findings achieved after the analysis of the company’s financial statements including the

statement of financial position, Income statement and the cash flow statement. The study of the

various elements in the individual statements will gave insight on how well the company was

performing i.e. whether the company improved, dropped or stagnated in its performance in a

particular area as far as performance is concerned and the best explanation for any of the

performance pattern that might have been noted. The trend analysis had focus on 2017 the base

and most current year as this is the year that indicated the final trend from the review of the rest

of the period. Ratio analysis played a vital role in the analysis as it helped to specifically identify

relationship between various elements in the financial statements that projected the company’s

performance. The report further gives recommendations after evaluation of the various critical

performance indicators that helped correct deviations and also appraised elements that enhanced

performance.

Table of Contents

1. Introduction.............................................................................................................................................4

1.1 Authorization.....................................................................................................................................4

1.2 Limitations.........................................................................................................................................4

1.3 Report Objective and scope...............................................................................................................4

2. Company Profile......................................................................................................................................5

3. Ratio analysis..........................................................................................................................................6

3.1 Profitability analysis..........................................................................................................................6

3.1.1 Return on Assets..................................................................................................................6

3.1.2 Net Profit Margin........................................................................................................................7

3.1.3 Gross Profit Margin....................................................................................................................9

3.3 Efficiency Ratios.............................................................................................................................13

3.3.1 Inventory Turnover...................................................................................................................13

4. Overall Industry Analysis.....................................................................................................................17

Recommendations.....................................................................................................................................18

References.................................................................................................................................................19

1. Introduction.............................................................................................................................................4

1.1 Authorization.....................................................................................................................................4

1.2 Limitations.........................................................................................................................................4

1.3 Report Objective and scope...............................................................................................................4

2. Company Profile......................................................................................................................................5

3. Ratio analysis..........................................................................................................................................6

3.1 Profitability analysis..........................................................................................................................6

3.1.1 Return on Assets..................................................................................................................6

3.1.2 Net Profit Margin........................................................................................................................7

3.1.3 Gross Profit Margin....................................................................................................................9

3.3 Efficiency Ratios.............................................................................................................................13

3.3.1 Inventory Turnover...................................................................................................................13

4. Overall Industry Analysis.....................................................................................................................17

Recommendations.....................................................................................................................................18

References.................................................................................................................................................19

1. Introduction

1.1 Authorization

This report has been prepared as requested and authorized by the board of directors of

Woolworths Group Limited. The report is thus addressed to them for the corrective action to be

undertaken.

1.2 Limitations

This report specifically gives analysis from the study of the financial statements for the 5 year as

given in the company’s website.

1.3 Report Objective and scope

The report compares the financial performance of Woolworths Group Limited with focus on the;

Profitability indicators of the company.

The company’s Liquidity i.e. how well the company is set to repay its debt.

The company’s efficiency in its operations.

The company’s financial structure that determine its leverage level.

The report interprets the elements of the financial statement using ratio analysisthrough

evaluation of critical elements in the statements that affect performance in one way or another.

The financial statements include:

The income statement.

This financial statement is an important element as it shows how the revenue generated by

the company over the 5 year period as well as enlisting the expenses that was incurred and

ultimately states the profit that was made from operations.

Balance sheet.

This financial statement stated the assets (What the company owns) and the liabilities (What

the company owes others) as well as the shareholders stake or equity in the company. In brief

it indicates the company’s financing structure.

Cash flow statement.

This statement broke down the Company’s receipts (Money Received) and company’s

payments made over given period of time. It indicates important financing, operating and

investing activities incurred by a company for a given financial period.

Although evaluation of performance of a company for a number of periods is essential, the

findings make more sense if the results are compared by another company in the same industry

to determine whether it is operating profitably as far as the overall industry is concerned. The

reports will thus asses the competitors in the industry that the industry belongs to (the retailing

industry) and gives recommendations from the finding.

1.1 Authorization

This report has been prepared as requested and authorized by the board of directors of

Woolworths Group Limited. The report is thus addressed to them for the corrective action to be

undertaken.

1.2 Limitations

This report specifically gives analysis from the study of the financial statements for the 5 year as

given in the company’s website.

1.3 Report Objective and scope

The report compares the financial performance of Woolworths Group Limited with focus on the;

Profitability indicators of the company.

The company’s Liquidity i.e. how well the company is set to repay its debt.

The company’s efficiency in its operations.

The company’s financial structure that determine its leverage level.

The report interprets the elements of the financial statement using ratio analysisthrough

evaluation of critical elements in the statements that affect performance in one way or another.

The financial statements include:

The income statement.

This financial statement is an important element as it shows how the revenue generated by

the company over the 5 year period as well as enlisting the expenses that was incurred and

ultimately states the profit that was made from operations.

Balance sheet.

This financial statement stated the assets (What the company owns) and the liabilities (What

the company owes others) as well as the shareholders stake or equity in the company. In brief

it indicates the company’s financing structure.

Cash flow statement.

This statement broke down the Company’s receipts (Money Received) and company’s

payments made over given period of time. It indicates important financing, operating and

investing activities incurred by a company for a given financial period.

Although evaluation of performance of a company for a number of periods is essential, the

findings make more sense if the results are compared by another company in the same industry

to determine whether it is operating profitably as far as the overall industry is concerned. The

reports will thus asses the competitors in the industry that the industry belongs to (the retailing

industry) and gives recommendations from the finding.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2. Company Profile

Woolworths Group Limited formerly known as Woolworths Limited is an Australian Company

listed the Australian Securities Exchange and was founded in 1924. Woolworths Limited

operates retail stores and thus falls in the category of retailing industry.

It is the second largest company in Australia in terms of revenue and the second largest in New

Zealand. It operates more than 3200 stores in both New Zealand and Australia and is involved in

the following businesses:

Liquor stores such as BWS and Dan Murphy’s.

Supermarkets under numerous banners such as Food town, Thomas Dux and

Woolworths.

Sale of gasoline.

Runs consumer electronic shops under the brand names of Dick Smith and Tandy.

It runs 165 odd general merchandise that operates the name of Big W.

Operates nearly 300 hotels. Among others.

Woolworth’s group limited has Coles Supermarket, The distributors and ALDI Einkauf as some

of its top competitors.

Woolworths Group Limited complies with ASX corporate governance principles which help

them to achieve long term shareholder value.

It is governed by a board of directors which has a function to provide the strategic direction to be

followed in the achievement of company goals. The board has the following committees that

help them in carrying out there responsibility as well as gaining advice from them. This are:

The Audit, Risk and Compliance Committee.

The People Performance Committee.

The Sustainability committee.

The Nomination Committee.

These committees have specific set responsibility which they carry out and in the end contribute

to the overall success of the board.

Woolworths Group Limited formerly known as Woolworths Limited is an Australian Company

listed the Australian Securities Exchange and was founded in 1924. Woolworths Limited

operates retail stores and thus falls in the category of retailing industry.

It is the second largest company in Australia in terms of revenue and the second largest in New

Zealand. It operates more than 3200 stores in both New Zealand and Australia and is involved in

the following businesses:

Liquor stores such as BWS and Dan Murphy’s.

Supermarkets under numerous banners such as Food town, Thomas Dux and

Woolworths.

Sale of gasoline.

Runs consumer electronic shops under the brand names of Dick Smith and Tandy.

It runs 165 odd general merchandise that operates the name of Big W.

Operates nearly 300 hotels. Among others.

Woolworth’s group limited has Coles Supermarket, The distributors and ALDI Einkauf as some

of its top competitors.

Woolworths Group Limited complies with ASX corporate governance principles which help

them to achieve long term shareholder value.

It is governed by a board of directors which has a function to provide the strategic direction to be

followed in the achievement of company goals. The board has the following committees that

help them in carrying out there responsibility as well as gaining advice from them. This are:

The Audit, Risk and Compliance Committee.

The People Performance Committee.

The Sustainability committee.

The Nomination Committee.

These committees have specific set responsibility which they carry out and in the end contribute

to the overall success of the board.

3. Ratio analysis.

The financial statements were interpreted in the following classes of ratios.

3.1 Profitability analysis

Profitability analysis was done by the use of the following profitability ratios;

Return on assets (ROA)

Net profit margin

Gross profit margin

These ratios attempted to show how efficient the company has been in the utilization of the

resources at its disposal to generate income relative to the expenses incurred (Balogh 2017).

3.1.1 Return on Assets.

This indicated the profits generated from the assets the company had.

ROA= Net Profit

Average Assets.

Average assets = Current years assets value + Previous Years Assets

2

ROA Calculations

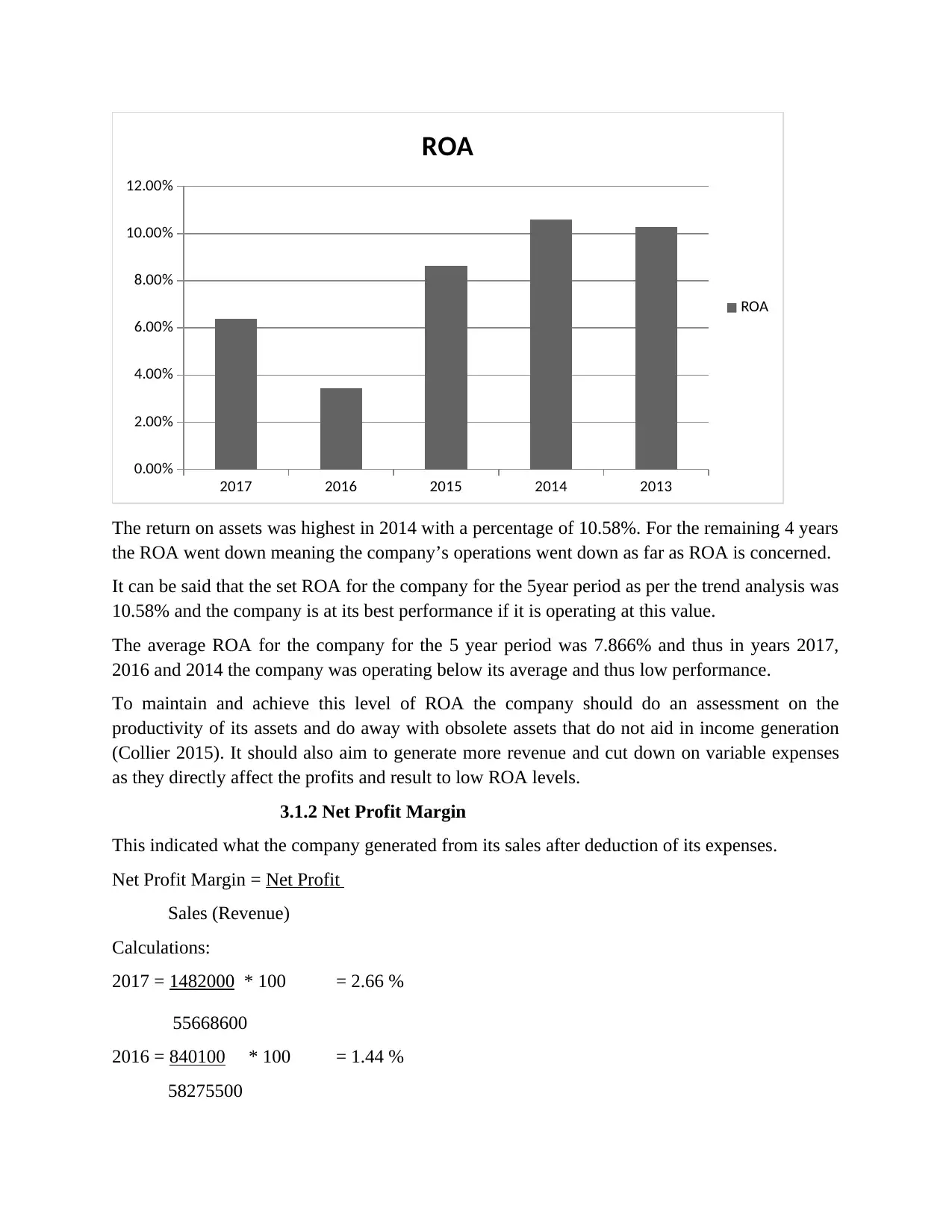

2017= 1482000* 100 = 6.39%

23209000

2016= 840100 * 100 = 3.44%

24419500

2015= 2137400 * 100 = 8.63%

24771000

2014 = 2458400 * 100 = 10.58%

23227700

2013 = 2254900 * 100 = 10.29%

21915650

The financial statements were interpreted in the following classes of ratios.

3.1 Profitability analysis

Profitability analysis was done by the use of the following profitability ratios;

Return on assets (ROA)

Net profit margin

Gross profit margin

These ratios attempted to show how efficient the company has been in the utilization of the

resources at its disposal to generate income relative to the expenses incurred (Balogh 2017).

3.1.1 Return on Assets.

This indicated the profits generated from the assets the company had.

ROA= Net Profit

Average Assets.

Average assets = Current years assets value + Previous Years Assets

2

ROA Calculations

2017= 1482000* 100 = 6.39%

23209000

2016= 840100 * 100 = 3.44%

24419500

2015= 2137400 * 100 = 8.63%

24771000

2014 = 2458400 * 100 = 10.58%

23227700

2013 = 2254900 * 100 = 10.29%

21915650

2017 2016 2015 2014 2013

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

ROA

ROA

The return on assets was highest in 2014 with a percentage of 10.58%. For the remaining 4 years

the ROA went down meaning the company’s operations went down as far as ROA is concerned.

It can be said that the set ROA for the company for the 5year period as per the trend analysis was

10.58% and the company is at its best performance if it is operating at this value.

The average ROA for the company for the 5 year period was 7.866% and thus in years 2017,

2016 and 2014 the company was operating below its average and thus low performance.

To maintain and achieve this level of ROA the company should do an assessment on the

productivity of its assets and do away with obsolete assets that do not aid in income generation

(Collier 2015). It should also aim to generate more revenue and cut down on variable expenses

as they directly affect the profits and result to low ROA levels.

3.1.2 Net Profit Margin

This indicated what the company generated from its sales after deduction of its expenses.

Net Profit Margin = Net Profit

Sales (Revenue)

Calculations:

2017 = 1482000 * 100 = 2.66 %

55668600

2016 = 840100 * 100 = 1.44 %

58275500

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

ROA

ROA

The return on assets was highest in 2014 with a percentage of 10.58%. For the remaining 4 years

the ROA went down meaning the company’s operations went down as far as ROA is concerned.

It can be said that the set ROA for the company for the 5year period as per the trend analysis was

10.58% and the company is at its best performance if it is operating at this value.

The average ROA for the company for the 5 year period was 7.866% and thus in years 2017,

2016 and 2014 the company was operating below its average and thus low performance.

To maintain and achieve this level of ROA the company should do an assessment on the

productivity of its assets and do away with obsolete assets that do not aid in income generation

(Collier 2015). It should also aim to generate more revenue and cut down on variable expenses

as they directly affect the profits and result to low ROA levels.

3.1.2 Net Profit Margin

This indicated what the company generated from its sales after deduction of its expenses.

Net Profit Margin = Net Profit

Sales (Revenue)

Calculations:

2017 = 1482000 * 100 = 2.66 %

55668600

2016 = 840100 * 100 = 1.44 %

58275500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

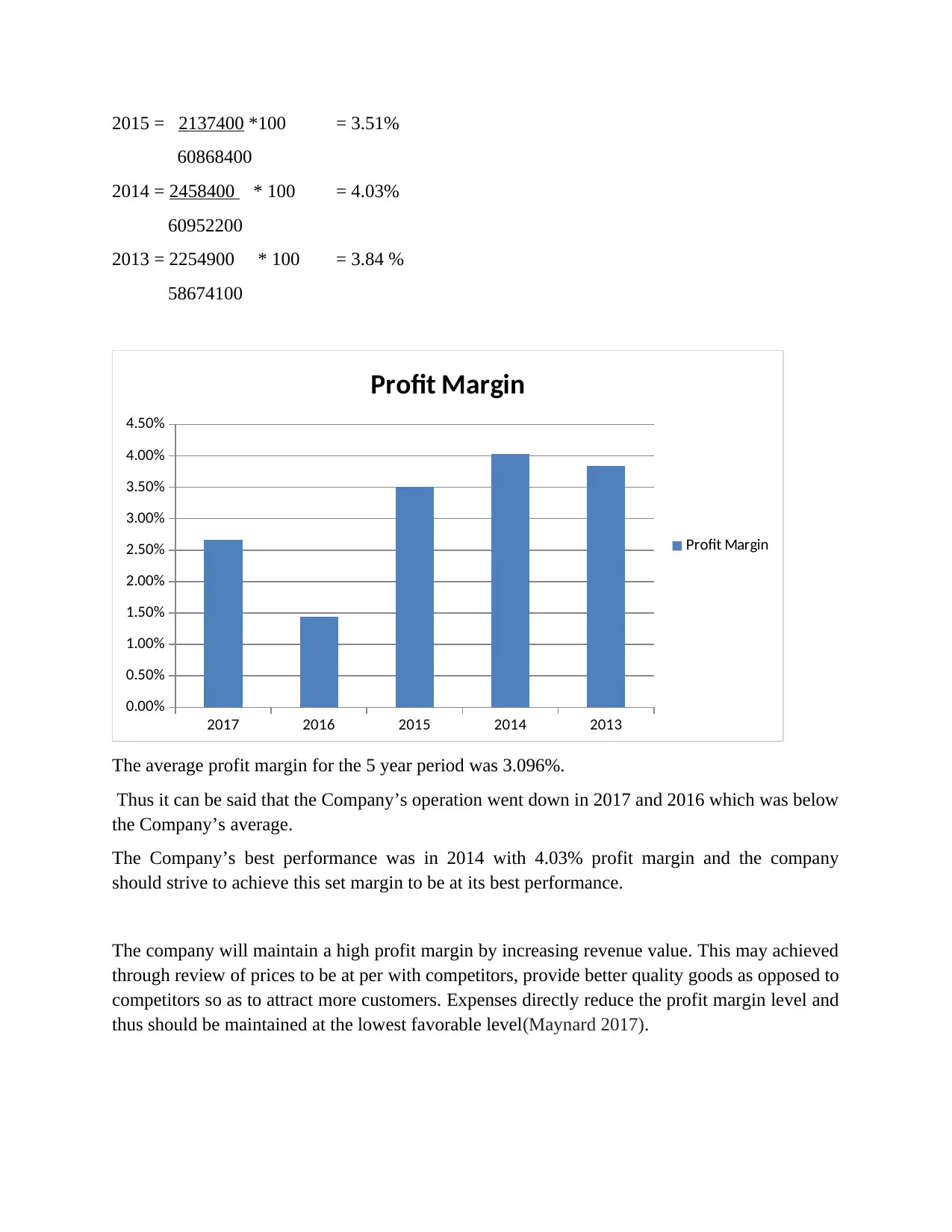

2015 = 2137400 *100 = 3.51%

60868400

2014 = 2458400 * 100 = 4.03%

60952200

2013 = 2254900 * 100 = 3.84 %

58674100

2017 2016 2015 2014 2013

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

Profit Margin

Profit Margin

The average profit margin for the 5 year period was 3.096%.

Thus it can be said that the Company’s operation went down in 2017 and 2016 which was below

the Company’s average.

The Company’s best performance was in 2014 with 4.03% profit margin and the company

should strive to achieve this set margin to be at its best performance.

The company will maintain a high profit margin by increasing revenue value. This may achieved

through review of prices to be at per with competitors, provide better quality goods as opposed to

competitors so as to attract more customers. Expenses directly reduce the profit margin level and

thus should be maintained at the lowest favorable level(Maynard 2017).

60868400

2014 = 2458400 * 100 = 4.03%

60952200

2013 = 2254900 * 100 = 3.84 %

58674100

2017 2016 2015 2014 2013

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

Profit Margin

Profit Margin

The average profit margin for the 5 year period was 3.096%.

Thus it can be said that the Company’s operation went down in 2017 and 2016 which was below

the Company’s average.

The Company’s best performance was in 2014 with 4.03% profit margin and the company

should strive to achieve this set margin to be at its best performance.

The company will maintain a high profit margin by increasing revenue value. This may achieved

through review of prices to be at per with competitors, provide better quality goods as opposed to

competitors so as to attract more customers. Expenses directly reduce the profit margin level and

thus should be maintained at the lowest favorable level(Maynard 2017).

3.1.3 Gross Profit Margin

This indicated the profit the company’s income margins after deduction of the cost of sales.

Gross Profit Margin = Net sales (Revenue) - Cost of Goods

Net Sales (Revenue)

Calculations

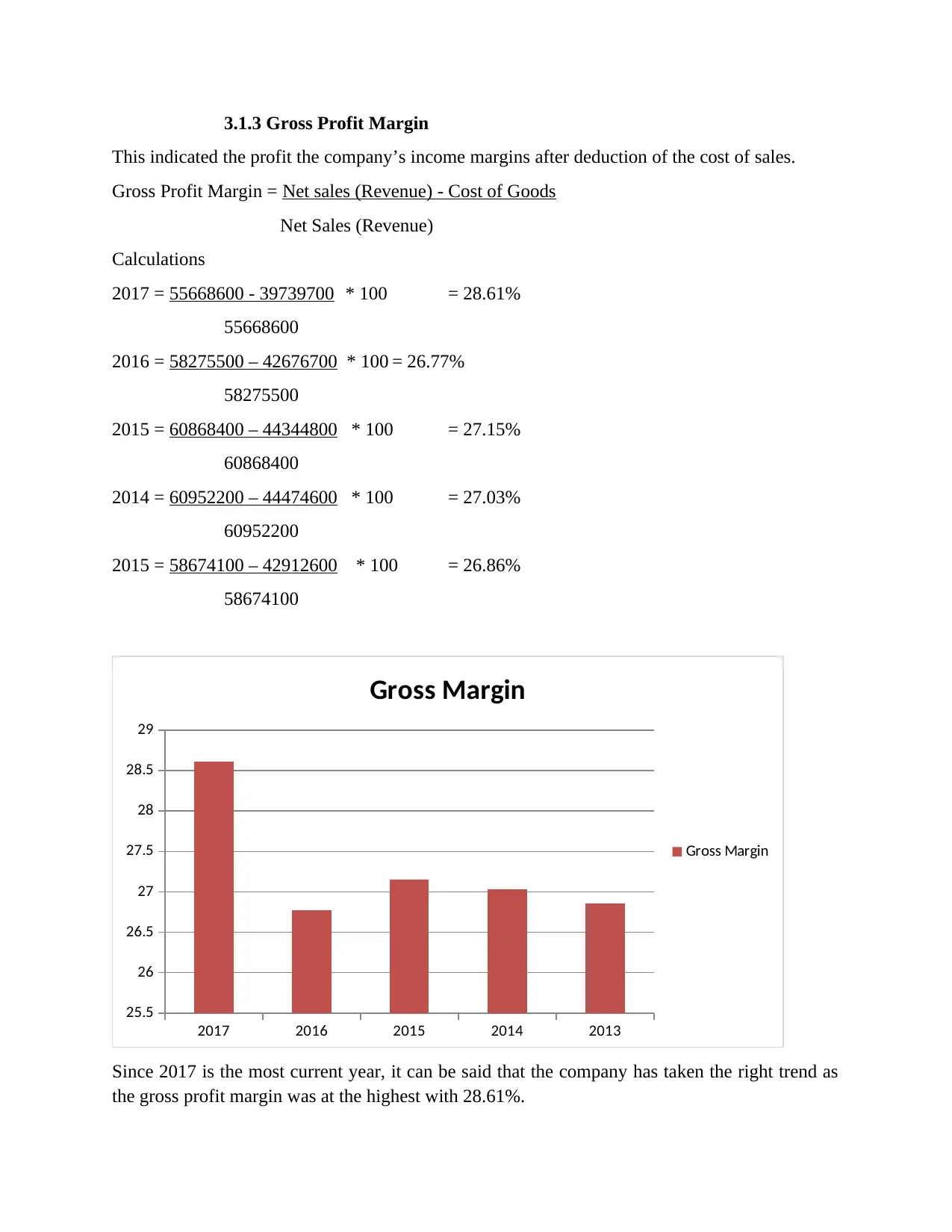

2017 = 55668600 - 39739700 * 100 = 28.61%

55668600

2016 = 58275500 – 42676700 * 100 = 26.77%

58275500

2015 = 60868400 – 44344800 * 100 = 27.15%

60868400

2014 = 60952200 – 44474600 * 100 = 27.03%

60952200

2015 = 58674100 – 42912600 * 100 = 26.86%

58674100

2017 2016 2015 2014 2013

25.5

26

26.5

27

27.5

28

28.5

29

Gross Margin

Gross Margin

Since 2017 is the most current year, it can be said that the company has taken the right trend as

the gross profit margin was at the highest with 28.61%.

This indicated the profit the company’s income margins after deduction of the cost of sales.

Gross Profit Margin = Net sales (Revenue) - Cost of Goods

Net Sales (Revenue)

Calculations

2017 = 55668600 - 39739700 * 100 = 28.61%

55668600

2016 = 58275500 – 42676700 * 100 = 26.77%

58275500

2015 = 60868400 – 44344800 * 100 = 27.15%

60868400

2014 = 60952200 – 44474600 * 100 = 27.03%

60952200

2015 = 58674100 – 42912600 * 100 = 26.86%

58674100

2017 2016 2015 2014 2013

25.5

26

26.5

27

27.5

28

28.5

29

Gross Margin

Gross Margin

Since 2017 is the most current year, it can be said that the company has taken the right trend as

the gross profit margin was at the highest with 28.61%.

The average profit margin for the five year period is 27.28%. The company thus operated below

its average in the years 2015 and 2014.

The company can maintain the set Gross margin through sourcing for cheaper but better quality

raw materials and labor as these components directly increase the cost of sales. It should also aim

to achieve high revenue values (Immorlica et al 2017).

3.2 Liquidity Ratios

These ratios indicated the ability of the company to repay both its short term debts using its

liquid assets (Michael & Albert 2015). Ratios used to analyze included:

Current Ratio

Quick Ratio

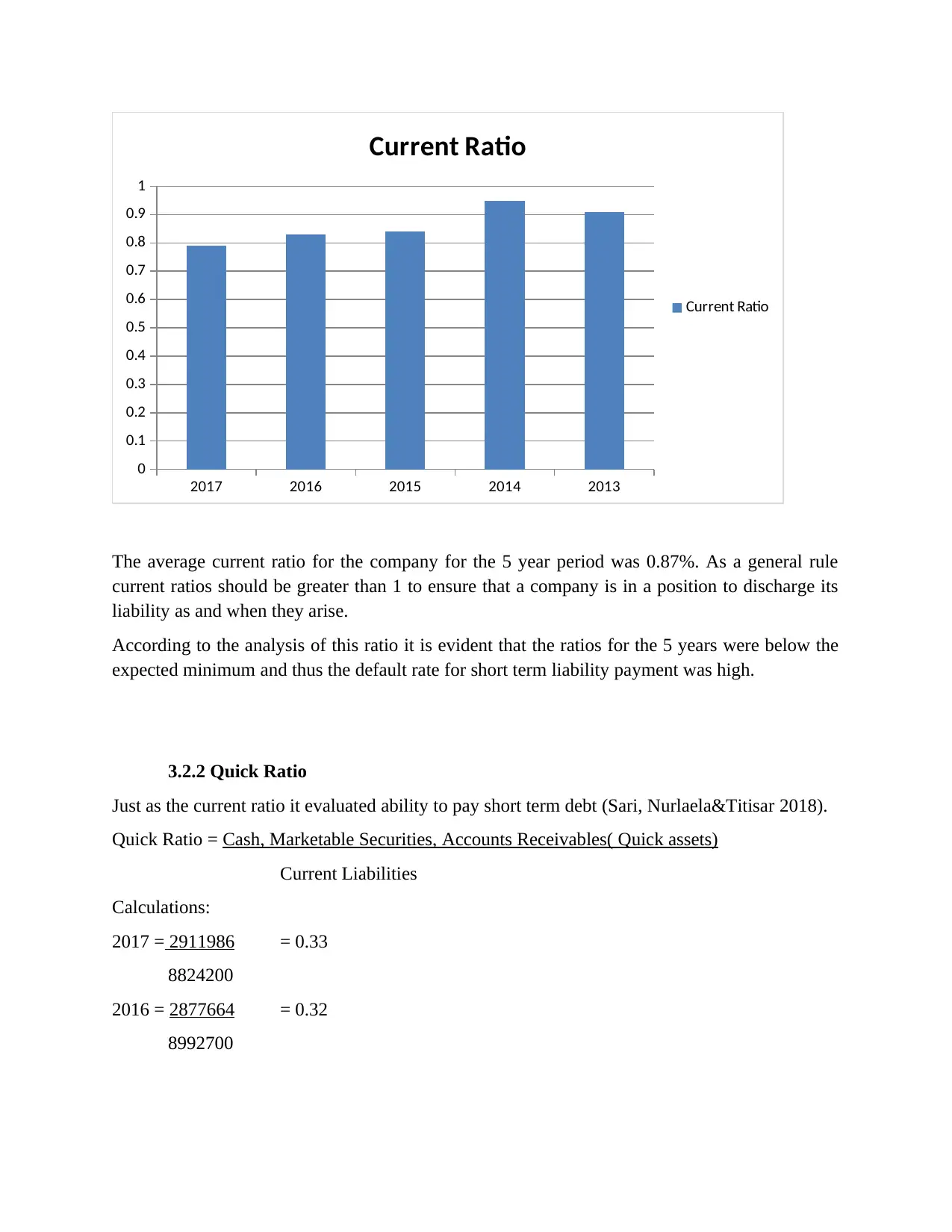

3.2.1 Current Ratio

This indicated the ability of Woolworths Group limited to repay its short term obligation

(Sekar& Saranya 2018).

Current Ratio = Current Assets

Current Liability

Calculations

2017 = 6994200 = 0.79

8824200

2016 = 7427000 = 0.83

8992700

2015 = 7660900 = 0.84

9168600

2014 = 7174800 = 0.95

7558200

2013= 6226100 = 0.91

6866000

its average in the years 2015 and 2014.

The company can maintain the set Gross margin through sourcing for cheaper but better quality

raw materials and labor as these components directly increase the cost of sales. It should also aim

to achieve high revenue values (Immorlica et al 2017).

3.2 Liquidity Ratios

These ratios indicated the ability of the company to repay both its short term debts using its

liquid assets (Michael & Albert 2015). Ratios used to analyze included:

Current Ratio

Quick Ratio

3.2.1 Current Ratio

This indicated the ability of Woolworths Group limited to repay its short term obligation

(Sekar& Saranya 2018).

Current Ratio = Current Assets

Current Liability

Calculations

2017 = 6994200 = 0.79

8824200

2016 = 7427000 = 0.83

8992700

2015 = 7660900 = 0.84

9168600

2014 = 7174800 = 0.95

7558200

2013= 6226100 = 0.91

6866000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2017 2016 2015 2014 2013

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Current Ratio

Current Ratio

The average current ratio for the company for the 5 year period was 0.87%. As a general rule

current ratios should be greater than 1 to ensure that a company is in a position to discharge its

liability as and when they arise.

According to the analysis of this ratio it is evident that the ratios for the 5 years were below the

expected minimum and thus the default rate for short term liability payment was high.

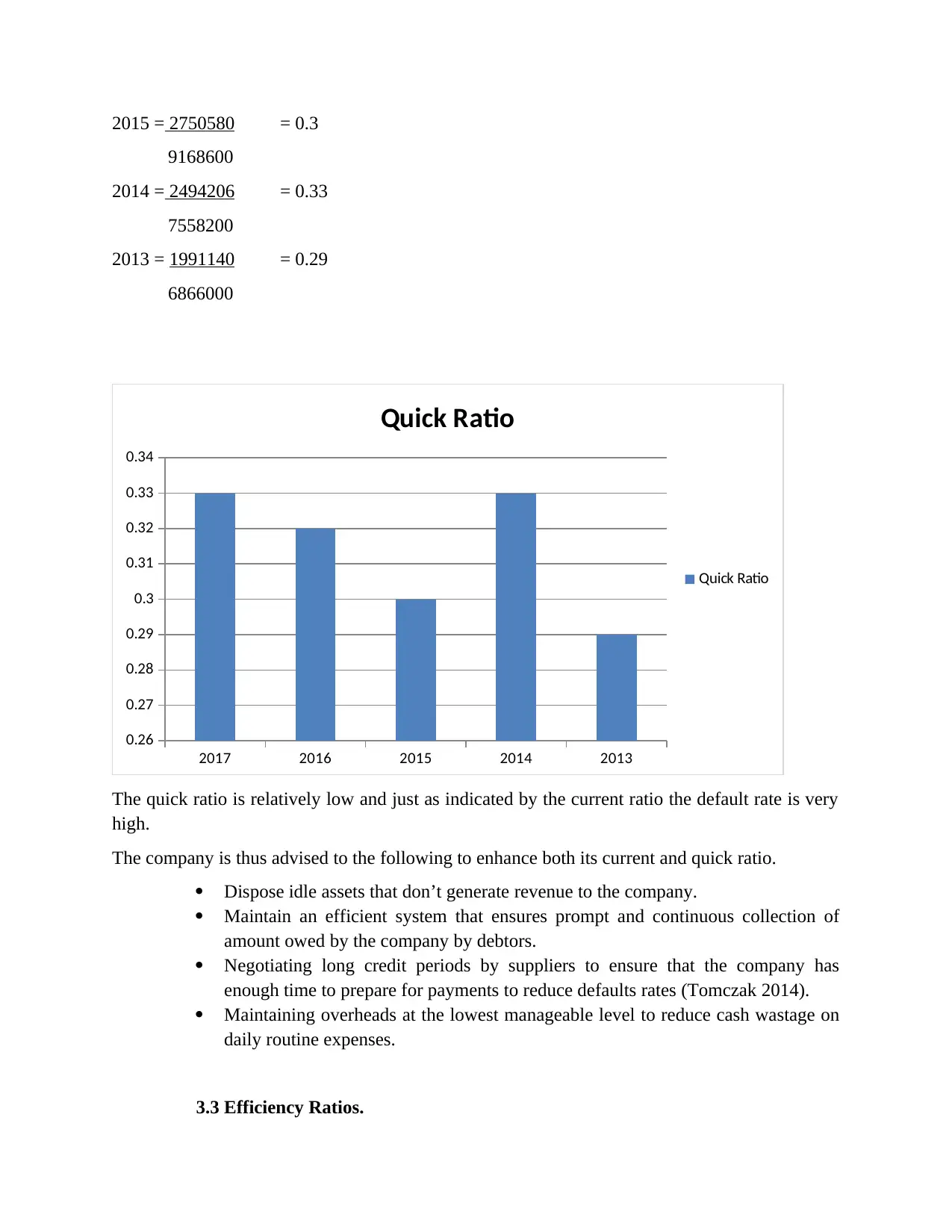

3.2.2 Quick Ratio

Just as the current ratio it evaluated ability to pay short term debt (Sari, Nurlaela&Titisar 2018).

Quick Ratio = Cash, Marketable Securities, Accounts Receivables( Quick assets)

Current Liabilities

Calculations:

2017 = 2911986 = 0.33

8824200

2016 = 2877664 = 0.32

8992700

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Current Ratio

Current Ratio

The average current ratio for the company for the 5 year period was 0.87%. As a general rule

current ratios should be greater than 1 to ensure that a company is in a position to discharge its

liability as and when they arise.

According to the analysis of this ratio it is evident that the ratios for the 5 years were below the

expected minimum and thus the default rate for short term liability payment was high.

3.2.2 Quick Ratio

Just as the current ratio it evaluated ability to pay short term debt (Sari, Nurlaela&Titisar 2018).

Quick Ratio = Cash, Marketable Securities, Accounts Receivables( Quick assets)

Current Liabilities

Calculations:

2017 = 2911986 = 0.33

8824200

2016 = 2877664 = 0.32

8992700

2015 = 2750580 = 0.3

9168600

2014 = 2494206 = 0.33

7558200

2013 = 1991140 = 0.29

6866000

2017 2016 2015 2014 2013

0.26

0.27

0.28

0.29

0.3

0.31

0.32

0.33

0.34

Quick Ratio

Quick Ratio

The quick ratio is relatively low and just as indicated by the current ratio the default rate is very

high.

The company is thus advised to the following to enhance both its current and quick ratio.

Dispose idle assets that don’t generate revenue to the company.

Maintain an efficient system that ensures prompt and continuous collection of

amount owed by the company by debtors.

Negotiating long credit periods by suppliers to ensure that the company has

enough time to prepare for payments to reduce defaults rates (Tomczak 2014).

Maintaining overheads at the lowest manageable level to reduce cash wastage on

daily routine expenses.

3.3 Efficiency Ratios.

9168600

2014 = 2494206 = 0.33

7558200

2013 = 1991140 = 0.29

6866000

2017 2016 2015 2014 2013

0.26

0.27

0.28

0.29

0.3

0.31

0.32

0.33

0.34

Quick Ratio

Quick Ratio

The quick ratio is relatively low and just as indicated by the current ratio the default rate is very

high.

The company is thus advised to the following to enhance both its current and quick ratio.

Dispose idle assets that don’t generate revenue to the company.

Maintain an efficient system that ensures prompt and continuous collection of

amount owed by the company by debtors.

Negotiating long credit periods by suppliers to ensure that the company has

enough time to prepare for payments to reduce defaults rates (Tomczak 2014).

Maintaining overheads at the lowest manageable level to reduce cash wastage on

daily routine expenses.

3.3 Efficiency Ratios.

These ratios indicated how well Woolworths Group Limited used its assets and managed its

liabilities (Santosuosso 2014).

The ratios analyzed under this category was the Inventory Turnover ratio.

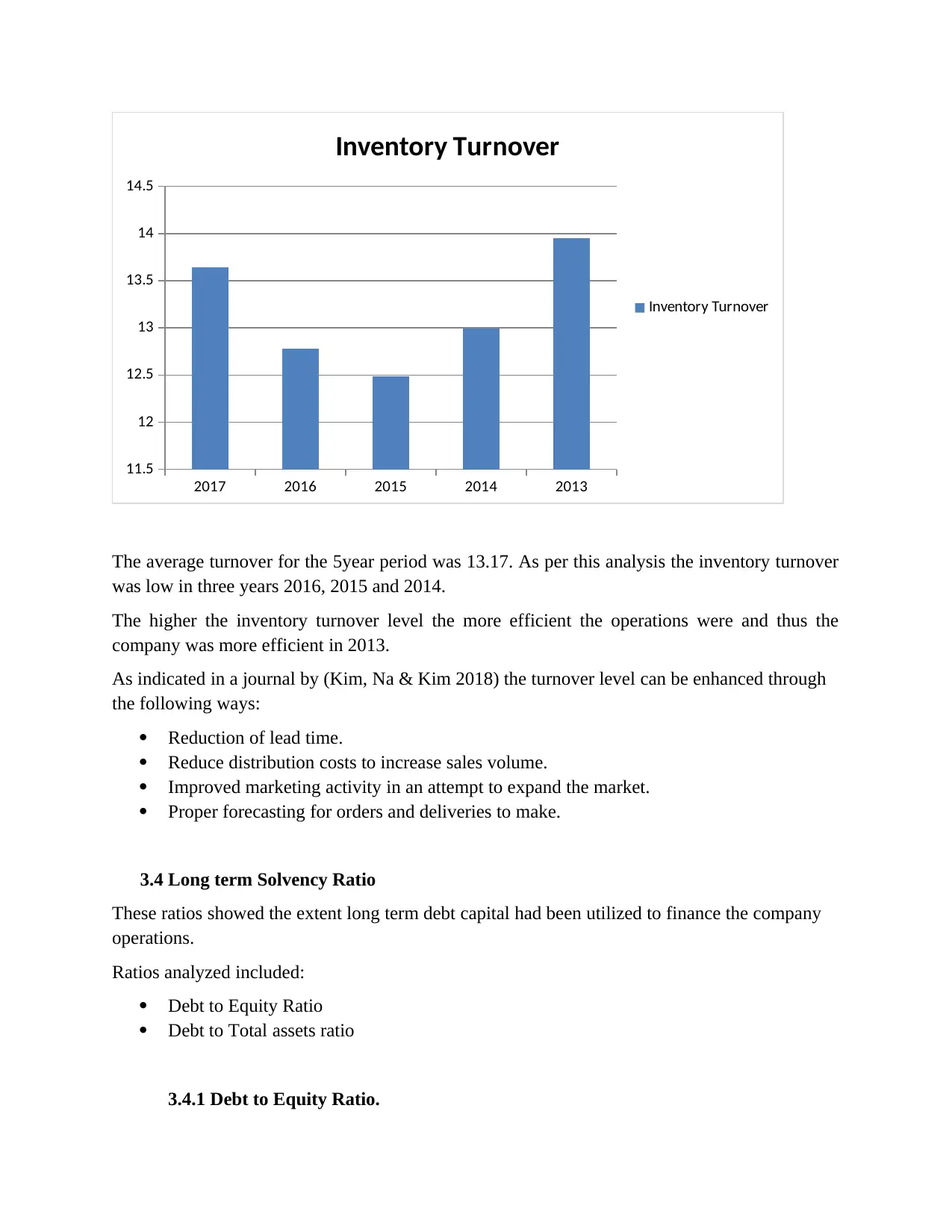

3.3.1 Inventory Turnover.

This indicated the number of times inventory was utilized or sold in the company.

Inventory Turnover = Net Sales

Average Inventory

Calculations:

2017 = 55668600 = 13.64 Times

4081276

2016 = 58275500 = 12.78 Times

4559898

2015 = 60868400 = 12.49 Times

4873371

2014 = 60952200 = 12.99 Times

4692241

2015 = 58674100 = 13.95 Times

4206029

liabilities (Santosuosso 2014).

The ratios analyzed under this category was the Inventory Turnover ratio.

3.3.1 Inventory Turnover.

This indicated the number of times inventory was utilized or sold in the company.

Inventory Turnover = Net Sales

Average Inventory

Calculations:

2017 = 55668600 = 13.64 Times

4081276

2016 = 58275500 = 12.78 Times

4559898

2015 = 60868400 = 12.49 Times

4873371

2014 = 60952200 = 12.99 Times

4692241

2015 = 58674100 = 13.95 Times

4206029

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 2016 2015 2014 2013

11.5

12

12.5

13

13.5

14

14.5

Inventory Turnover

Inventory Turnover

The average turnover for the 5year period was 13.17. As per this analysis the inventory turnover

was low in three years 2016, 2015 and 2014.

The higher the inventory turnover level the more efficient the operations were and thus the

company was more efficient in 2013.

As indicated in a journal by (Kim, Na & Kim 2018) the turnover level can be enhanced through

the following ways:

Reduction of lead time.

Reduce distribution costs to increase sales volume.

Improved marketing activity in an attempt to expand the market.

Proper forecasting for orders and deliveries to make.

3.4 Long term Solvency Ratio

These ratios showed the extent long term debt capital had been utilized to finance the company

operations.

Ratios analyzed included:

Debt to Equity Ratio

Debt to Total assets ratio

3.4.1 Debt to Equity Ratio.

11.5

12

12.5

13

13.5

14

14.5

Inventory Turnover

Inventory Turnover

The average turnover for the 5year period was 13.17. As per this analysis the inventory turnover

was low in three years 2016, 2015 and 2014.

The higher the inventory turnover level the more efficient the operations were and thus the

company was more efficient in 2013.

As indicated in a journal by (Kim, Na & Kim 2018) the turnover level can be enhanced through

the following ways:

Reduction of lead time.

Reduce distribution costs to increase sales volume.

Improved marketing activity in an attempt to expand the market.

Proper forecasting for orders and deliveries to make.

3.4 Long term Solvency Ratio

These ratios showed the extent long term debt capital had been utilized to finance the company

operations.

Ratios analyzed included:

Debt to Equity Ratio

Debt to Total assets ratio

3.4.1 Debt to Equity Ratio.

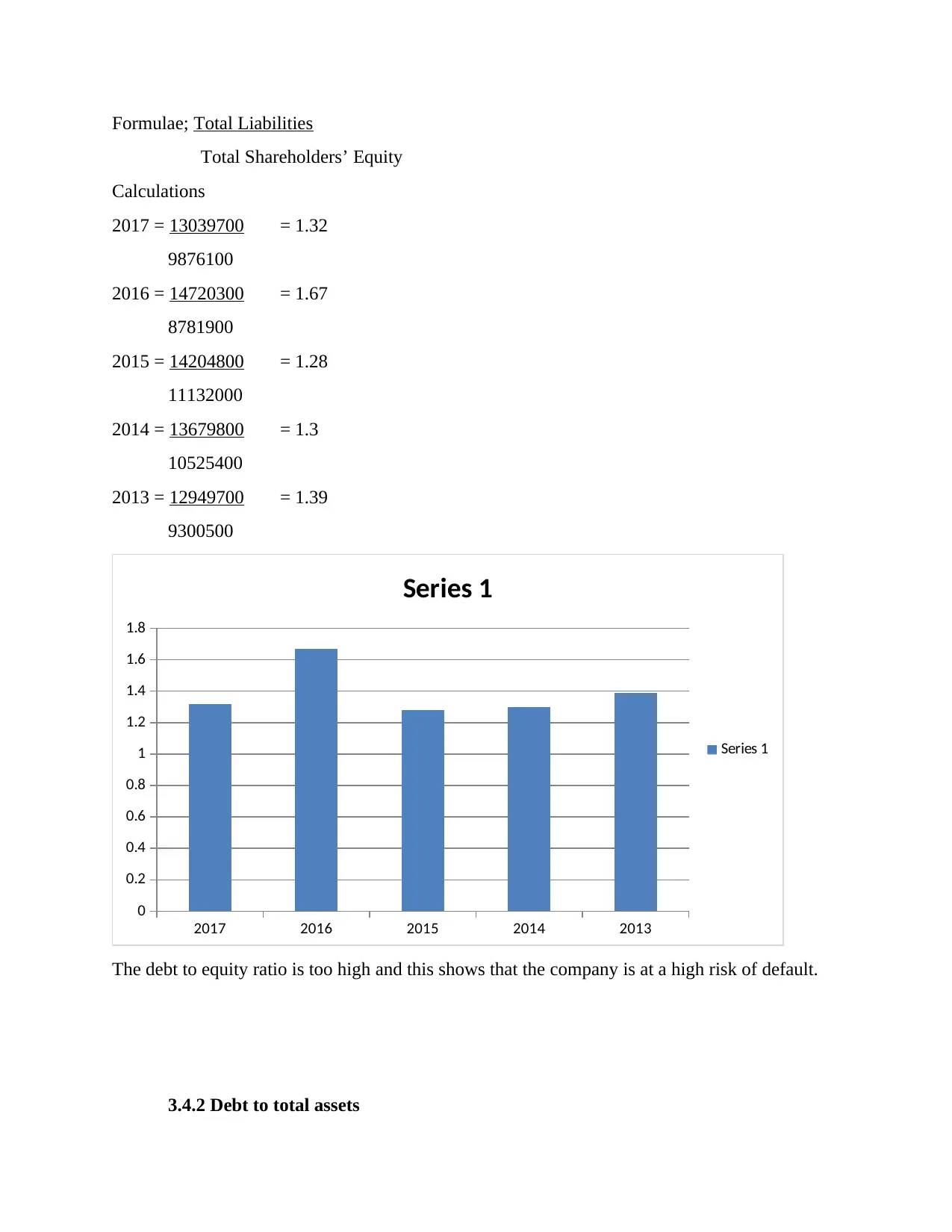

Formulae; Total Liabilities

Total Shareholders’ Equity

Calculations

2017 = 13039700 = 1.32

9876100

2016 = 14720300 = 1.67

8781900

2015 = 14204800 = 1.28

11132000

2014 = 13679800 = 1.3

10525400

2013 = 12949700 = 1.39

9300500

2017 2016 2015 2014 2013

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Series 1

Series 1

The debt to equity ratio is too high and this shows that the company is at a high risk of default.

3.4.2 Debt to total assets

Total Shareholders’ Equity

Calculations

2017 = 13039700 = 1.32

9876100

2016 = 14720300 = 1.67

8781900

2015 = 14204800 = 1.28

11132000

2014 = 13679800 = 1.3

10525400

2013 = 12949700 = 1.39

9300500

2017 2016 2015 2014 2013

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Series 1

Series 1

The debt to equity ratio is too high and this shows that the company is at a high risk of default.

3.4.2 Debt to total assets

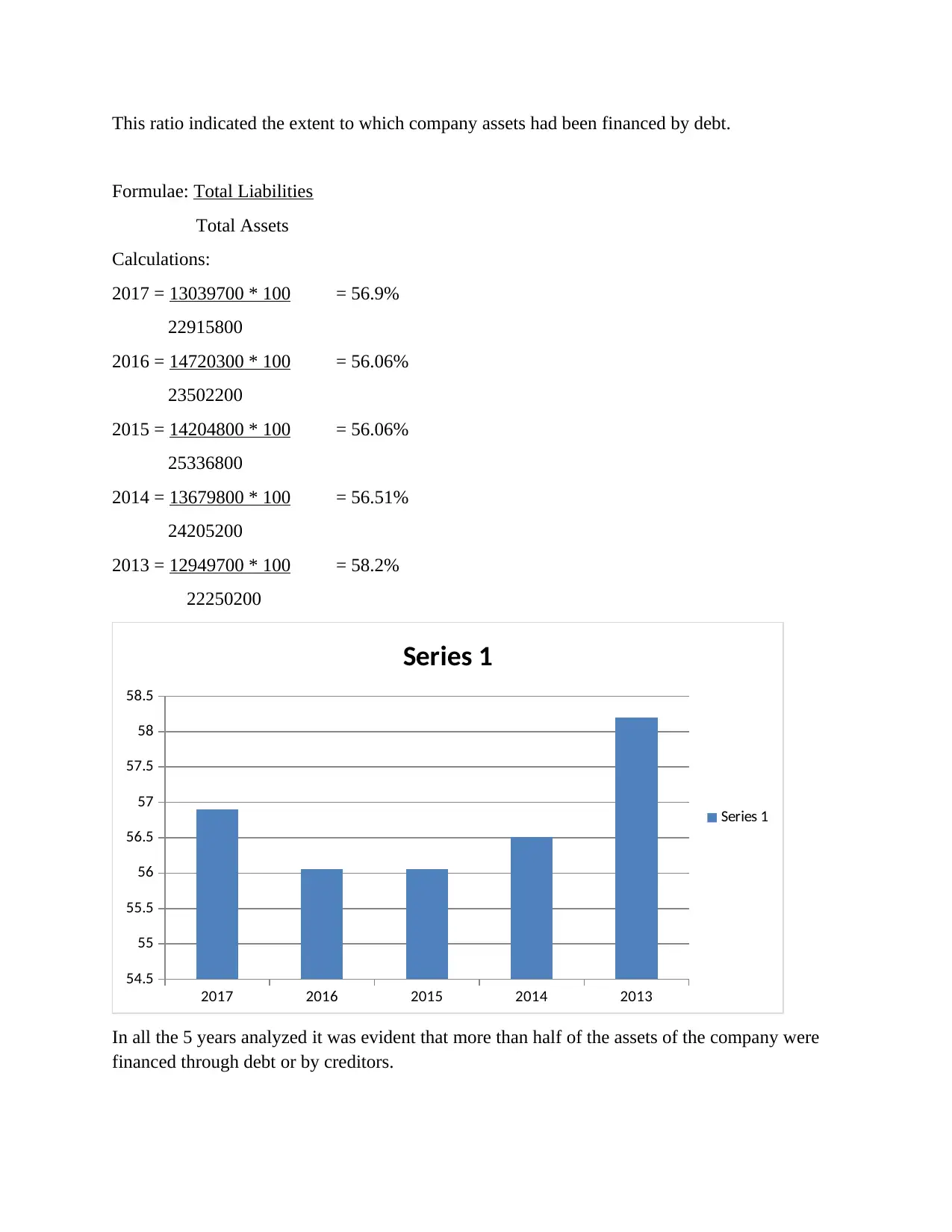

This ratio indicated the extent to which company assets had been financed by debt.

Formulae: Total Liabilities

Total Assets

Calculations:

2017 = 13039700 * 100 = 56.9%

22915800

2016 = 14720300 * 100 = 56.06%

23502200

2015 = 14204800 * 100 = 56.06%

25336800

2014 = 13679800 * 100 = 56.51%

24205200

2013 = 12949700 * 100 = 58.2%

22250200

2017 2016 2015 2014 2013

54.5

55

55.5

56

56.5

57

57.5

58

58.5

Series 1

Series 1

In all the 5 years analyzed it was evident that more than half of the assets of the company were

financed through debt or by creditors.

Formulae: Total Liabilities

Total Assets

Calculations:

2017 = 13039700 * 100 = 56.9%

22915800

2016 = 14720300 * 100 = 56.06%

23502200

2015 = 14204800 * 100 = 56.06%

25336800

2014 = 13679800 * 100 = 56.51%

24205200

2013 = 12949700 * 100 = 58.2%

22250200

2017 2016 2015 2014 2013

54.5

55

55.5

56

56.5

57

57.5

58

58.5

Series 1

Series 1

In all the 5 years analyzed it was evident that more than half of the assets of the company were

financed through debt or by creditors.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

This is very risky as any default by the company that may lead to repossession of the assets by

the company will greatly affect the company’s operations.

A company should ensure that it is in the position to solve both its long term and short term

obligations. As for the calculations above more debt than equity is used to run the company and

thus the company should try as much as it can to reduce the debt level by investing more on

equity financing.

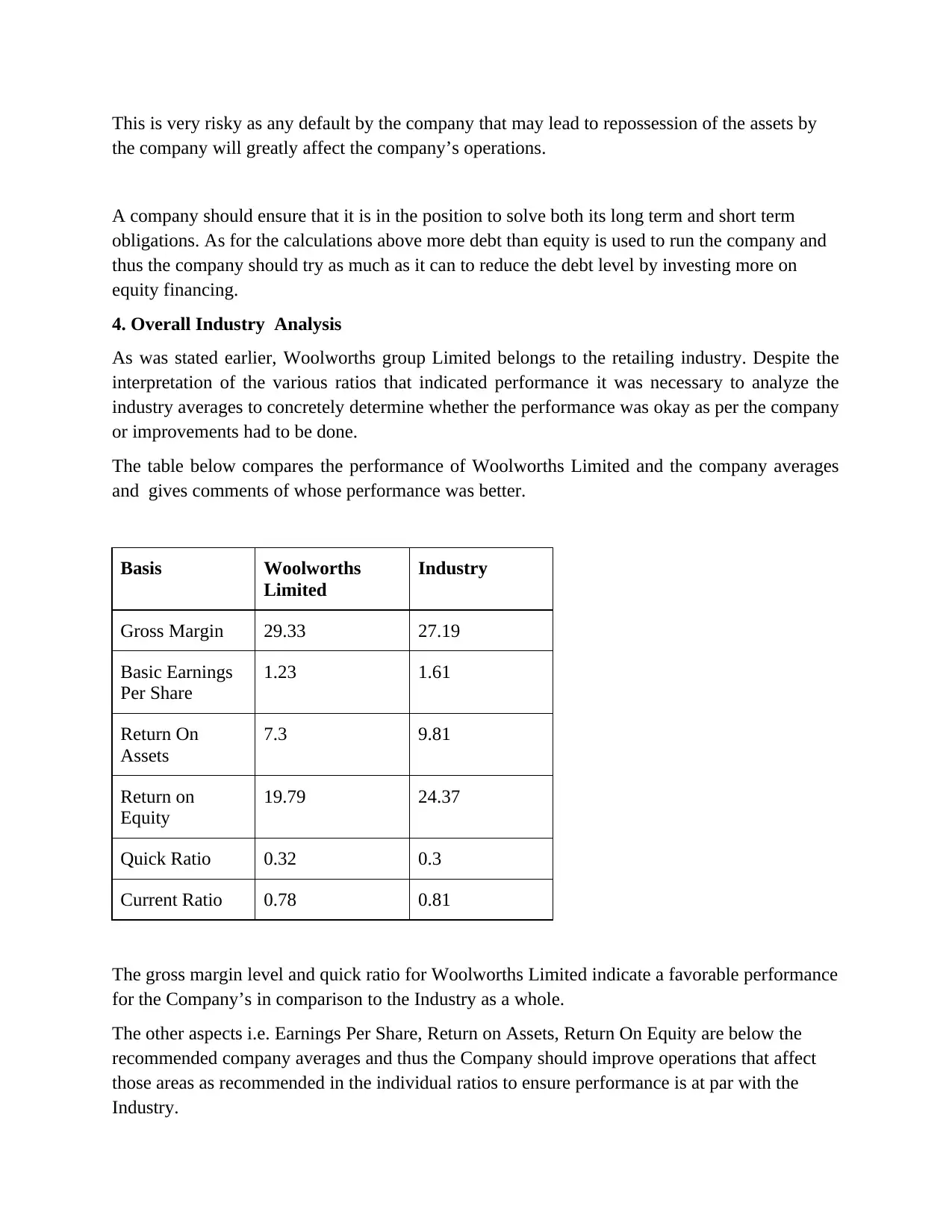

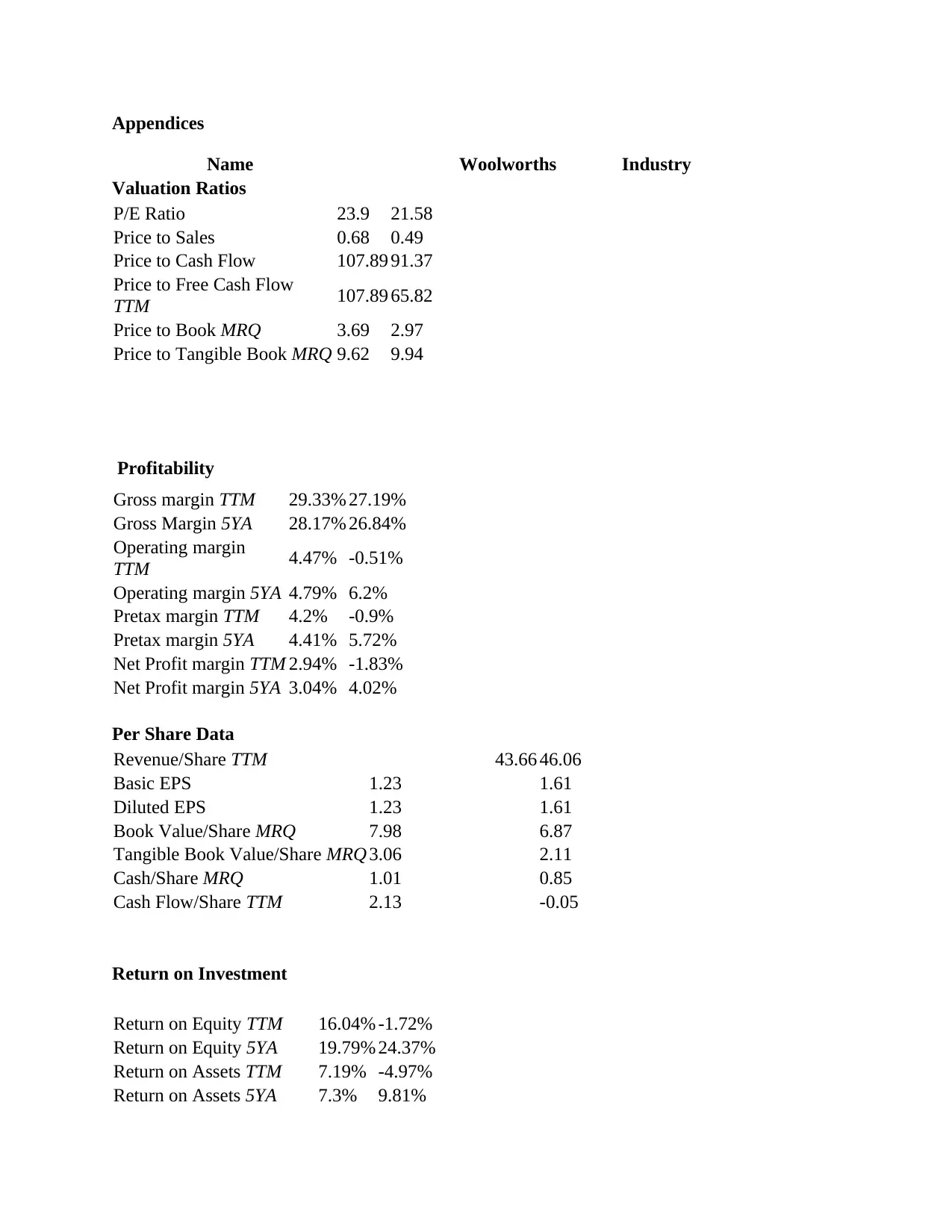

4. Overall Industry Analysis

As was stated earlier, Woolworths group Limited belongs to the retailing industry. Despite the

interpretation of the various ratios that indicated performance it was necessary to analyze the

industry averages to concretely determine whether the performance was okay as per the company

or improvements had to be done.

The table below compares the performance of Woolworths Limited and the company averages

and gives comments of whose performance was better.

Basis Woolworths

Limited

Industry

Gross Margin 29.33 27.19

Basic Earnings

Per Share

1.23 1.61

Return On

Assets

7.3 9.81

Return on

Equity

19.79 24.37

Quick Ratio 0.32 0.3

Current Ratio 0.78 0.81

The gross margin level and quick ratio for Woolworths Limited indicate a favorable performance

for the Company’s in comparison to the Industry as a whole.

The other aspects i.e. Earnings Per Share, Return on Assets, Return On Equity are below the

recommended company averages and thus the Company should improve operations that affect

those areas as recommended in the individual ratios to ensure performance is at par with the

Industry.

the company will greatly affect the company’s operations.

A company should ensure that it is in the position to solve both its long term and short term

obligations. As for the calculations above more debt than equity is used to run the company and

thus the company should try as much as it can to reduce the debt level by investing more on

equity financing.

4. Overall Industry Analysis

As was stated earlier, Woolworths group Limited belongs to the retailing industry. Despite the

interpretation of the various ratios that indicated performance it was necessary to analyze the

industry averages to concretely determine whether the performance was okay as per the company

or improvements had to be done.

The table below compares the performance of Woolworths Limited and the company averages

and gives comments of whose performance was better.

Basis Woolworths

Limited

Industry

Gross Margin 29.33 27.19

Basic Earnings

Per Share

1.23 1.61

Return On

Assets

7.3 9.81

Return on

Equity

19.79 24.37

Quick Ratio 0.32 0.3

Current Ratio 0.78 0.81

The gross margin level and quick ratio for Woolworths Limited indicate a favorable performance

for the Company’s in comparison to the Industry as a whole.

The other aspects i.e. Earnings Per Share, Return on Assets, Return On Equity are below the

recommended company averages and thus the Company should improve operations that affect

those areas as recommended in the individual ratios to ensure performance is at par with the

Industry.

Conclusion

It is thus concluded that several elements contribute to the overall performance of the company

and no element is less important. The company is thus advised to follow the recommendations

given after each analysis to ensure that deviations identified are corrected.

Recommendations

The company is advised to be carrying routine analysis on the financial status and performance

as well to ensure that deviations are identified andcorrected on time. The company should not

only do an assessment on its own but compare results with the industry finding to ensure that

their operations are not only profitable but are at par with the industry performance.

It is thus concluded that several elements contribute to the overall performance of the company

and no element is less important. The company is thus advised to follow the recommendations

given after each analysis to ensure that deviations identified are corrected.

Recommendations

The company is advised to be carrying routine analysis on the financial status and performance

as well to ensure that deviations are identified andcorrected on time. The company should not

only do an assessment on its own but compare results with the industry finding to ensure that

their operations are not only profitable but are at par with the industry performance.

References

Almeida, H., Fos, V. and Kronlund, M., 2016. The real effects of share repurchases. Journal of

Financial Economics, 119(1), pp.168-185.

Balogh, A. 2017.Financial Ratios for Accounting Research. SSRN Electronic Journal.

Bianconi, M. and Yoshino, J.A., 2017. Valuation of the worldwide commodities sector: The role

of market-to-book and return on equity. Studies in Economics and Finance, 34(4), pp.555-579.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Fernandez, P., 2017. Shareholder Value Creation: A Definition.

Gregory, A., Whittaker, J. and Yan, X., 2016.Corporate social performance, competitive

advantage, earnings persistence and firm value.Journal of Business Finance & Accounting, 43(1-

2), pp.3-30.

Immorlica, N., Lucier, B., Pountourakis, E. and Taggart, S., 2017, June.Repeated sales with

multiple strategic buyers.In Proceedings of the 2017 ACM Conference on Economics and

Computation (pp. 167-168).ACM.

Kim, B., Na, J. and Kim, S., 2018. Effects of target firm's inventory turnover on post-merger and

acquisition performance. International Journal of Applied Management Science, 10(3), pp.173-

191.

Mardani, M., Salehi, A.A., Langerodi, H.D., Pazoki, S., Golestani, R. and Alankesh, P.S., 2018.

Studying Relationship between Qualitative Features of Profit and Return on Common Equity (A

Data Mining on the Banks Accepted in Tehran Stock Exchange). Account and Financial

Management Journal, 3(01), pp.1259-1270.

Marsh, C. 2012. Financial management for non-financial managers. London: Kogan Page.

Maynard, J., 2017. Financial accounting, reporting, and analysis.Oxford University Press.

Michael, R. and Albert J, P. 2015. Financial Ratios for Executives How to Assess Company

Strength, Fix Problems, and Make Better Decisions.Apress.

Santosuosso, P. 2014. Do Efficiency Ratios Help Investors to Explore Firm Performances?

Evidence from Italian Listed Firms. International Business Research, 7(12).

Sari, R.K., Nurlaela, S. and Titisari, K.H., 2018, August.The Effect of Liquidity Ratio,

Profitability Ratio, Company Size, and Leverage on Bond Rating in Construction and Real

Estate Company.In PROCEEDING ICTESS (Internasional Conference on Technology,

Education and Social Sciences).

Almeida, H., Fos, V. and Kronlund, M., 2016. The real effects of share repurchases. Journal of

Financial Economics, 119(1), pp.168-185.

Balogh, A. 2017.Financial Ratios for Accounting Research. SSRN Electronic Journal.

Bianconi, M. and Yoshino, J.A., 2017. Valuation of the worldwide commodities sector: The role

of market-to-book and return on equity. Studies in Economics and Finance, 34(4), pp.555-579.

Collier, P.M., 2015. Accounting for managers: Interpreting accounting information for decision

making. John Wiley & Sons.

Fernandez, P., 2017. Shareholder Value Creation: A Definition.

Gregory, A., Whittaker, J. and Yan, X., 2016.Corporate social performance, competitive

advantage, earnings persistence and firm value.Journal of Business Finance & Accounting, 43(1-

2), pp.3-30.

Immorlica, N., Lucier, B., Pountourakis, E. and Taggart, S., 2017, June.Repeated sales with

multiple strategic buyers.In Proceedings of the 2017 ACM Conference on Economics and

Computation (pp. 167-168).ACM.

Kim, B., Na, J. and Kim, S., 2018. Effects of target firm's inventory turnover on post-merger and

acquisition performance. International Journal of Applied Management Science, 10(3), pp.173-

191.

Mardani, M., Salehi, A.A., Langerodi, H.D., Pazoki, S., Golestani, R. and Alankesh, P.S., 2018.

Studying Relationship between Qualitative Features of Profit and Return on Common Equity (A

Data Mining on the Banks Accepted in Tehran Stock Exchange). Account and Financial

Management Journal, 3(01), pp.1259-1270.

Marsh, C. 2012. Financial management for non-financial managers. London: Kogan Page.

Maynard, J., 2017. Financial accounting, reporting, and analysis.Oxford University Press.

Michael, R. and Albert J, P. 2015. Financial Ratios for Executives How to Assess Company

Strength, Fix Problems, and Make Better Decisions.Apress.

Santosuosso, P. 2014. Do Efficiency Ratios Help Investors to Explore Firm Performances?

Evidence from Italian Listed Firms. International Business Research, 7(12).

Sari, R.K., Nurlaela, S. and Titisari, K.H., 2018, August.The Effect of Liquidity Ratio,

Profitability Ratio, Company Size, and Leverage on Bond Rating in Construction and Real

Estate Company.In PROCEEDING ICTESS (Internasional Conference on Technology,

Education and Social Sciences).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sekar, D. and Saranya, M. 2018. A study on financial performance (Selected Liquidity Ratios &

Management performance ratios) of BAG Films and Media Ltd. International Journal of

Scientific Research and Management, 6(07).

Singh, S., Jain, P.K. and Yadav, S.S., 2018.Analysis of Practice Multiples-Empirical Evidence

from the Indian Stock Market.Research Bulletin, 44(1), pp.1-16.

Tomczak, S. 2014. Comparative analysis of liquidity ratios of bankrupt manufacturing

companies. Business and Economic Horizons, 10(3), pp.151-164.

Vedd, R., Lazarony, P. and Yassinski, N. 2014.Multivariables Determining Earnings per Share

within the U.S. Medical Laboratories & Research Industry. Archives of Business Research, 2(4),

pp.150-160.

Management performance ratios) of BAG Films and Media Ltd. International Journal of

Scientific Research and Management, 6(07).

Singh, S., Jain, P.K. and Yadav, S.S., 2018.Analysis of Practice Multiples-Empirical Evidence

from the Indian Stock Market.Research Bulletin, 44(1), pp.1-16.

Tomczak, S. 2014. Comparative analysis of liquidity ratios of bankrupt manufacturing

companies. Business and Economic Horizons, 10(3), pp.151-164.

Vedd, R., Lazarony, P. and Yassinski, N. 2014.Multivariables Determining Earnings per Share

within the U.S. Medical Laboratories & Research Industry. Archives of Business Research, 2(4),

pp.150-160.

Appendices

Name Woolworths Industry

Valuation Ratios

P/E Ratio 23.9 21.58

Price to Sales 0.68 0.49

Price to Cash Flow 107.89 91.37

Price to Free Cash Flow

TTM 107.89 65.82

Price to Book MRQ 3.69 2.97

Price to Tangible Book MRQ 9.62 9.94

Profitability

Gross margin TTM 29.33% 27.19%

Gross Margin 5YA 28.17% 26.84%

Operating margin

TTM 4.47% -0.51%

Operating margin 5YA 4.79% 6.2%

Pretax margin TTM 4.2% -0.9%

Pretax margin 5YA 4.41% 5.72%

Net Profit margin TTM 2.94% -1.83%

Net Profit margin 5YA 3.04% 4.02%

Per Share Data

Revenue/Share TTM 43.66 46.06

Basic EPS 1.23 1.61

Diluted EPS 1.23 1.61

Book Value/Share MRQ 7.98 6.87

Tangible Book Value/Share MRQ 3.06 2.11

Cash/Share MRQ 1.01 0.85

Cash Flow/Share TTM 2.13 -0.05

Return on Investment

Return on Equity TTM 16.04% -1.72%

Return on Equity 5YA 19.79% 24.37%

Return on Assets TTM 7.19% -4.97%

Return on Assets 5YA 7.3% 9.81%

Name Woolworths Industry

Valuation Ratios

P/E Ratio 23.9 21.58

Price to Sales 0.68 0.49

Price to Cash Flow 107.89 91.37

Price to Free Cash Flow

TTM 107.89 65.82

Price to Book MRQ 3.69 2.97

Price to Tangible Book MRQ 9.62 9.94

Profitability

Gross margin TTM 29.33% 27.19%

Gross Margin 5YA 28.17% 26.84%

Operating margin

TTM 4.47% -0.51%

Operating margin 5YA 4.79% 6.2%

Pretax margin TTM 4.2% -0.9%

Pretax margin 5YA 4.41% 5.72%

Net Profit margin TTM 2.94% -1.83%

Net Profit margin 5YA 3.04% 4.02%

Per Share Data

Revenue/Share TTM 43.66 46.06

Basic EPS 1.23 1.61

Diluted EPS 1.23 1.61

Book Value/Share MRQ 7.98 6.87

Tangible Book Value/Share MRQ 3.06 2.11

Cash/Share MRQ 1.01 0.85

Cash Flow/Share TTM 2.13 -0.05

Return on Investment

Return on Equity TTM 16.04% -1.72%

Return on Equity 5YA 19.79% 24.37%

Return on Assets TTM 7.19% -4.97%

Return on Assets 5YA 7.3% 9.81%

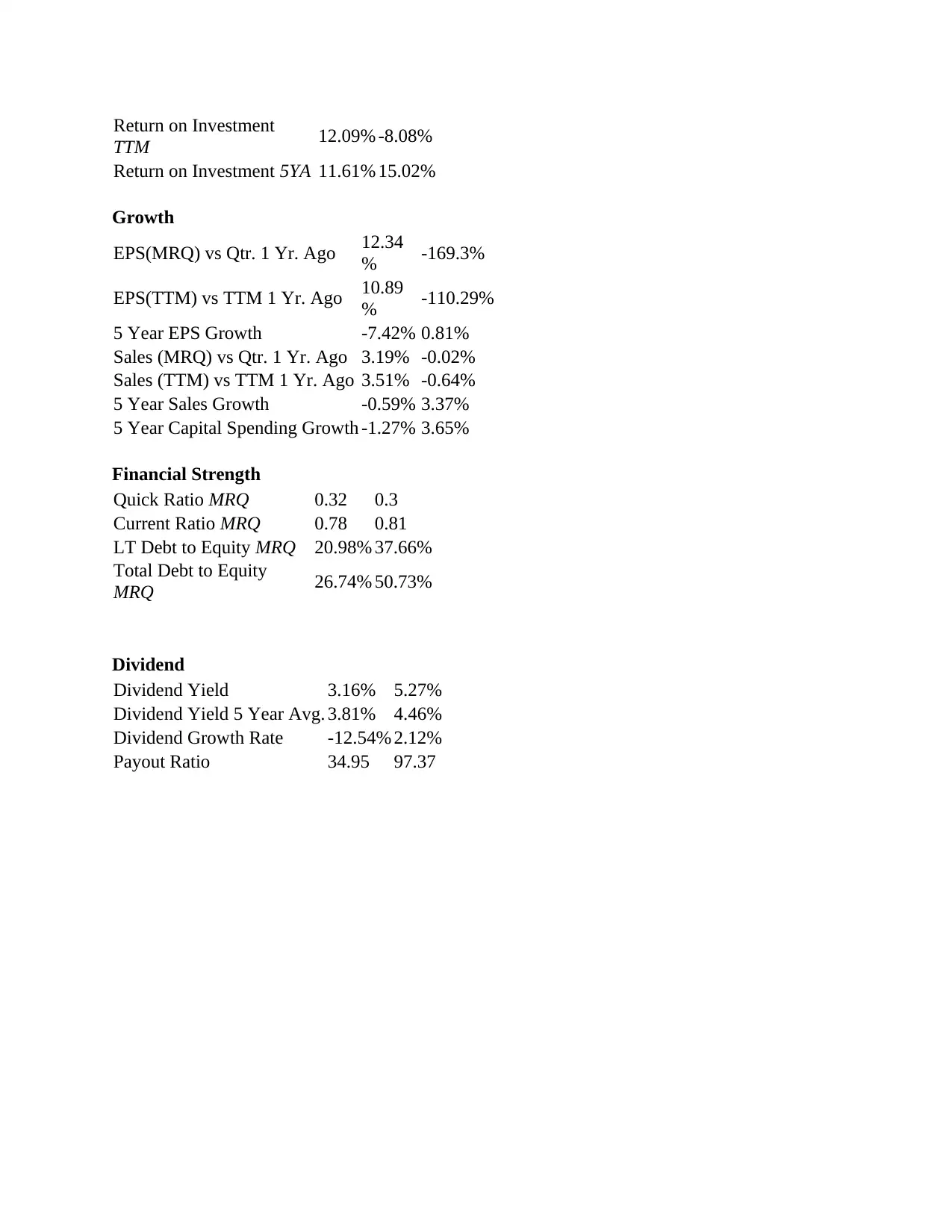

Return on Investment

TTM 12.09% -8.08%

Return on Investment 5YA 11.61% 15.02%

Growth

EPS(MRQ) vs Qtr. 1 Yr. Ago 12.34

% -169.3%

EPS(TTM) vs TTM 1 Yr. Ago 10.89

% -110.29%

5 Year EPS Growth -7.42% 0.81%

Sales (MRQ) vs Qtr. 1 Yr. Ago 3.19% -0.02%

Sales (TTM) vs TTM 1 Yr. Ago 3.51% -0.64%

5 Year Sales Growth -0.59% 3.37%

5 Year Capital Spending Growth -1.27% 3.65%

Financial Strength

Quick Ratio MRQ 0.32 0.3

Current Ratio MRQ 0.78 0.81

LT Debt to Equity MRQ 20.98% 37.66%

Total Debt to Equity

MRQ 26.74% 50.73%

Dividend

Dividend Yield 3.16% 5.27%

Dividend Yield 5 Year Avg. 3.81% 4.46%

Dividend Growth Rate -12.54% 2.12%

Payout Ratio 34.95 97.37

TTM 12.09% -8.08%

Return on Investment 5YA 11.61% 15.02%

Growth

EPS(MRQ) vs Qtr. 1 Yr. Ago 12.34

% -169.3%

EPS(TTM) vs TTM 1 Yr. Ago 10.89

% -110.29%

5 Year EPS Growth -7.42% 0.81%

Sales (MRQ) vs Qtr. 1 Yr. Ago 3.19% -0.02%

Sales (TTM) vs TTM 1 Yr. Ago 3.51% -0.64%

5 Year Sales Growth -0.59% 3.37%

5 Year Capital Spending Growth -1.27% 3.65%

Financial Strength

Quick Ratio MRQ 0.32 0.3

Current Ratio MRQ 0.78 0.81

LT Debt to Equity MRQ 20.98% 37.66%

Total Debt to Equity

MRQ 26.74% 50.73%

Dividend

Dividend Yield 3.16% 5.27%

Dividend Yield 5 Year Avg. 3.81% 4.46%

Dividend Growth Rate -12.54% 2.12%

Payout Ratio 34.95 97.37

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.