ACC701 - Financial Statement Analysis Case Study: Woolworths Ltd

VerifiedAdded on 2023/06/04

|20

|4444

|175

Case Study

AI Summary

This report presents a financial statement analysis of Woolworths Limited to assess its investment viability. It includes a company background, a detailed ratio analysis covering profitability, asset efficiency, liquidity, solvency, and stock market performance, and a trend analysis of sales and net profit. The ratio analysis examines key metrics such as return on capital employed, gross profit margin, operating profit margin, trade payable turnover days, receivable turnover days, inventory turnover days, current ratio, quick ratio, gearing ratio, interest coverage ratio, and earnings per share. The trend analysis studies the sales and net profit of the business to measure the changes into overall performance in last 3 years. The report aims to provide insights for investors to make informed decisions about investing in Woolworths.

Running Head: Accounting for managers

1

Project Report: Accounting for managers

1

Project Report: Accounting for managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers

2

Executive summary:

The study on the final financial statement of the business is one of the easiest methods

to evaluate the overall performance of a business. The report focuses on the case study of

Woolworths limited. The report has been conducted to identify the investment position of the

company. In order to evaluate the investment position of the company, the ratio analysis

study has been done and it has been measured that the performance of the company is quite

impressive. The investment into the company is better option for the investors to get higher

return.

2

Executive summary:

The study on the final financial statement of the business is one of the easiest methods

to evaluate the overall performance of a business. The report focuses on the case study of

Woolworths limited. The report has been conducted to identify the investment position of the

company. In order to evaluate the investment position of the company, the ratio analysis

study has been done and it has been measured that the performance of the company is quite

impressive. The investment into the company is better option for the investors to get higher

return.

Accounting for managers

3

Contents

Introduction.......................................................................................................................4

Company background.......................................................................................................4

Analysis and discussion....................................................................................................4

Trend analysis...............................................................................................................8

Conclusion......................................................................................................................10

Recommendation............................................................................................................10

References.......................................................................................................................12

Appendix.........................................................................................................................13

3

Contents

Introduction.......................................................................................................................4

Company background.......................................................................................................4

Analysis and discussion....................................................................................................4

Trend analysis...............................................................................................................8

Conclusion......................................................................................................................10

Recommendation............................................................................................................10

References.......................................................................................................................12

Appendix.........................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for managers

4

Introduction:

Evaluation on the final financial statement and the annual report of an organization is

one of the major parts while making the decision about the investment in that particular

company. The final statement and other relevant information in the annual report of the

company makes it easier for the investors and the analyst to collect the information for the

purpose of making the decision about the investment in that company. The strategic direction,

director’s report, operating environment, financial items, stock price, strategically changes etc

are the few figures and information which makes a base for the investors and the analyst.

This information leads to the analyst and the potential investors of the business to reach over

the conclusion (Moyer, McGuigan, Rao and Kretlow, 2011).

In the report, the case study of Woolworths limited has been studied in order to

identify the investment position of the company and identify that whether the investment into

the company would be enough profitable for the investors or not. Various tools and

techniques of analysis have been applied on the annual report and financial statement of the

company to reach over the conclusion.

Company background:

Woolworths group limited is a retailing company which is based in the Australian

market mainly. The company offers various segment to its customers such as Australian food,

liquor, petrol, hotels services, supermarket services etc. the different segment of the company

is operated by the different subsidiaries of the company in order to meet the financial and non

financial objectives of the business such as to improve the turnover, profitability position and

the market base of the company (Reuters, 2018). The total market capital of the business is

36,116 million on the basis of the annual report (2017) of the company. Company has

diversified its market in the New Zealand and Indian market recently.

Analysis and discussion:

The analysis has been done on the annual report and the financial statement of

Woolworths limited to measure the investment position of the company in the market. Firstly,

the study of ratio analysis has been done on the company to identify the various financial

level of the business such as liquidity financial level, profitability financial level, solvency

4

Introduction:

Evaluation on the final financial statement and the annual report of an organization is

one of the major parts while making the decision about the investment in that particular

company. The final statement and other relevant information in the annual report of the

company makes it easier for the investors and the analyst to collect the information for the

purpose of making the decision about the investment in that company. The strategic direction,

director’s report, operating environment, financial items, stock price, strategically changes etc

are the few figures and information which makes a base for the investors and the analyst.

This information leads to the analyst and the potential investors of the business to reach over

the conclusion (Moyer, McGuigan, Rao and Kretlow, 2011).

In the report, the case study of Woolworths limited has been studied in order to

identify the investment position of the company and identify that whether the investment into

the company would be enough profitable for the investors or not. Various tools and

techniques of analysis have been applied on the annual report and financial statement of the

company to reach over the conclusion.

Company background:

Woolworths group limited is a retailing company which is based in the Australian

market mainly. The company offers various segment to its customers such as Australian food,

liquor, petrol, hotels services, supermarket services etc. the different segment of the company

is operated by the different subsidiaries of the company in order to meet the financial and non

financial objectives of the business such as to improve the turnover, profitability position and

the market base of the company (Reuters, 2018). The total market capital of the business is

36,116 million on the basis of the annual report (2017) of the company. Company has

diversified its market in the New Zealand and Indian market recently.

Analysis and discussion:

The analysis has been done on the annual report and the financial statement of

Woolworths limited to measure the investment position of the company in the market. Firstly,

the study of ratio analysis has been done on the company to identify the various financial

level of the business such as liquidity financial level, profitability financial level, solvency

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers

5

financial level, and efficiency financial level and market ratios of the business (Baker and

English, 2011). The analysis on the ratios of the company is as follows:

Profitability ratios:

Profitability ratios are calculated by the analyst and the investors to measure the entire

capabilities of an entity to generate and make profits on the basis of the total equity funds,

available resources, total turnover and many others basis. The profitability ratio analysis

process makes it easier for the analyst and the investors to identify that how much profit

could be generated by the business and how much return could be got by the investors from

the company (Ahrendsen and Katchova, 2012). In case of Woolworths limited, return on

capital employed (ROCE), operating profit margin and gross profit margin of the business

has been calculated to identify the profit making level and capabilities of the business. The

calculations of profitability ratios analysis are as follows:

Return on capital employed:

Return on capital employed is a profitability identifying ratio which is used to

measure the total profit generated against the capital employed of the business (Brigham and

Ehrhardt, 2013). The ROCE of Woolworths limited has been lowered to 30.04% from

35.11% in 2013 which depicts improved and competitive position of the business.

Gross profit margin:

Gross profit margin is a profitability ratio which is used to identify the difference

among the total turnover and the cost of sales of the business. The gross profit margin level of

Woolworths limited has been improved by 28.6% in 2017 from 26.9% in 2013 which depicts

improved and competitive position of the business and a great management of profit level

(Annual report, 2017).

Operating profit margin:

Operating profit margin is a profitability identifying ratio which calculated the total

expenses deduction from the total sales amount of the business. The operating profit margin

of Woolworths limited has been reduced by from 5.48% to 3.83% in 2017 which depicts

lower position of the business.

5

financial level, and efficiency financial level and market ratios of the business (Baker and

English, 2011). The analysis on the ratios of the company is as follows:

Profitability ratios:

Profitability ratios are calculated by the analyst and the investors to measure the entire

capabilities of an entity to generate and make profits on the basis of the total equity funds,

available resources, total turnover and many others basis. The profitability ratio analysis

process makes it easier for the analyst and the investors to identify that how much profit

could be generated by the business and how much return could be got by the investors from

the company (Ahrendsen and Katchova, 2012). In case of Woolworths limited, return on

capital employed (ROCE), operating profit margin and gross profit margin of the business

has been calculated to identify the profit making level and capabilities of the business. The

calculations of profitability ratios analysis are as follows:

Return on capital employed:

Return on capital employed is a profitability identifying ratio which is used to

measure the total profit generated against the capital employed of the business (Brigham and

Ehrhardt, 2013). The ROCE of Woolworths limited has been lowered to 30.04% from

35.11% in 2013 which depicts improved and competitive position of the business.

Gross profit margin:

Gross profit margin is a profitability ratio which is used to identify the difference

among the total turnover and the cost of sales of the business. The gross profit margin level of

Woolworths limited has been improved by 28.6% in 2017 from 26.9% in 2013 which depicts

improved and competitive position of the business and a great management of profit level

(Annual report, 2017).

Operating profit margin:

Operating profit margin is a profitability identifying ratio which calculated the total

expenses deduction from the total sales amount of the business. The operating profit margin

of Woolworths limited has been reduced by from 5.48% to 3.83% in 2017 which depicts

lower position of the business.

Accounting for managers

6

The overall profitability analysis of the company explains that the company is trying

to manage the profitability level and it would lead to the better earnings to the investors of the

company.

Asset efficiency ratios:

Asset efficiency ratios are calculated by the analyst and the investors to measure the

efficiency level of an entity in order to manage their daily operations of the business and the

cash conversion cycle of the business through maintain the better cash position in the

business for daily operations and the activities. The efficiency ratio analysis process makes it

easier for the analyst to identify that how much cash is needed for the business to run the

activities (Madura, 2011). In case of Woolworths limited, trade payment turnover days,

receivable turnover days and inventory turnover days of the business has been calculated to

identify the cash conversion cycle and efficiency level of the business. The calculations of

asset efficiency ratios analysis are as follows:

Trade payable payment turnover:

Trade payable turnover days brief the efficiency position of the company in order to

manage the cash position and the credit policies of the business. The payment payable

turnover days of Woolworths limited has been improved to 46.55 days (annual report, 2017).

It explains better efficiency position of the company.

Receivable turnover:

Receivable turnover days brief the efficiency position of the company in order to

manage the total days in which the debtors would pay the credit amount. The receivable

turnover days of Woolworths limited has been changed from 35.77 days to 37.48 in last 5

years (yahoo finance, 2018). It explains that the debtors turnover days have been improved.

Inventory turnover:

Lastly, the inventory turnover days brief the total days in which the inventory of the

company would be ordered and replaced the old inventory of the business. The inventory

turnover days of Woolworths limited is higher and explains that more cash is required for the

business.

The overall efficiency analysis of the company explains that the efficient level of the

business is enough competitive.

6

The overall profitability analysis of the company explains that the company is trying

to manage the profitability level and it would lead to the better earnings to the investors of the

company.

Asset efficiency ratios:

Asset efficiency ratios are calculated by the analyst and the investors to measure the

efficiency level of an entity in order to manage their daily operations of the business and the

cash conversion cycle of the business through maintain the better cash position in the

business for daily operations and the activities. The efficiency ratio analysis process makes it

easier for the analyst to identify that how much cash is needed for the business to run the

activities (Madura, 2011). In case of Woolworths limited, trade payment turnover days,

receivable turnover days and inventory turnover days of the business has been calculated to

identify the cash conversion cycle and efficiency level of the business. The calculations of

asset efficiency ratios analysis are as follows:

Trade payable payment turnover:

Trade payable turnover days brief the efficiency position of the company in order to

manage the cash position and the credit policies of the business. The payment payable

turnover days of Woolworths limited has been improved to 46.55 days (annual report, 2017).

It explains better efficiency position of the company.

Receivable turnover:

Receivable turnover days brief the efficiency position of the company in order to

manage the total days in which the debtors would pay the credit amount. The receivable

turnover days of Woolworths limited has been changed from 35.77 days to 37.48 in last 5

years (yahoo finance, 2018). It explains that the debtors turnover days have been improved.

Inventory turnover:

Lastly, the inventory turnover days brief the total days in which the inventory of the

company would be ordered and replaced the old inventory of the business. The inventory

turnover days of Woolworths limited is higher and explains that more cash is required for the

business.

The overall efficiency analysis of the company explains that the efficient level of the

business is enough competitive.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for managers

7

Liquidity ratios:

Liquidity ratios are calculated by the analyst and the investors to measure the

capabilities of an entity to manage the enough funds from their daily activities to pay the

current debt of the business. The liquidity ratio analysis process makes it easier for the

analyst and the investors to identify the associated liquidity risk of the business as it measures

that whether the business is able to pay the entire debt at a single time through its current and

quick assets to the debt holders of the business. It calculates the short term solvency position

of the business (Koller, Goedhart and Wessels, 2010). In case of Woolworths limited, current

ratio and acid test ratio of the business has been calculated to identify the solvency position of

the business in short term. The calculations of liquidity ratios analysis are as follows:

Current ratio:

Current ratio is a liquidity ratio which is used to identify that whether the business is

able to replay the current debt against the current funds available to the company (Higgins,

2012). The current ratio of Woolworths limited has been reduced by 0.79 from 0.91 times in

2018. It explains higher liquidity risk of the business.

Quick ratio:

Further, the quick ratio is a liquidity ratio which is used to identify that whether the

business is able to replay the current debt against the quick funds which can be transferred

quickly into cash, available to the company. The quick ratio of Woolworths limited has been

almost similar in last 5 years (Annual report, 2017).

On the basis of the overall evaluation, it has been found that the liquidity risk of the

business has been higher in 2017.

Solvency ratios:

Solvency ratios are calculated by the analyst and the investors to measure the entire

capabilities of an entity to meet the long term obligations of the business on the basis of the

available assets and equity fund of the business. The solvency ratio analysis process makes it

easier for the analyst and the investors to identify the financial risk level through measuring

the debt level, equity level and assets level of the business (Hogarth and Makridakis, 2011).

In case of Woolworths limited, gearing ratio and interest coverage ratio of the business has

7

Liquidity ratios:

Liquidity ratios are calculated by the analyst and the investors to measure the

capabilities of an entity to manage the enough funds from their daily activities to pay the

current debt of the business. The liquidity ratio analysis process makes it easier for the

analyst and the investors to identify the associated liquidity risk of the business as it measures

that whether the business is able to pay the entire debt at a single time through its current and

quick assets to the debt holders of the business. It calculates the short term solvency position

of the business (Koller, Goedhart and Wessels, 2010). In case of Woolworths limited, current

ratio and acid test ratio of the business has been calculated to identify the solvency position of

the business in short term. The calculations of liquidity ratios analysis are as follows:

Current ratio:

Current ratio is a liquidity ratio which is used to identify that whether the business is

able to replay the current debt against the current funds available to the company (Higgins,

2012). The current ratio of Woolworths limited has been reduced by 0.79 from 0.91 times in

2018. It explains higher liquidity risk of the business.

Quick ratio:

Further, the quick ratio is a liquidity ratio which is used to identify that whether the

business is able to replay the current debt against the quick funds which can be transferred

quickly into cash, available to the company. The quick ratio of Woolworths limited has been

almost similar in last 5 years (Annual report, 2017).

On the basis of the overall evaluation, it has been found that the liquidity risk of the

business has been higher in 2017.

Solvency ratios:

Solvency ratios are calculated by the analyst and the investors to measure the entire

capabilities of an entity to meet the long term obligations of the business on the basis of the

available assets and equity fund of the business. The solvency ratio analysis process makes it

easier for the analyst and the investors to identify the financial risk level through measuring

the debt level, equity level and assets level of the business (Hogarth and Makridakis, 2011).

In case of Woolworths limited, gearing ratio and interest coverage ratio of the business has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers

8

been calculated to identify the long term obligation management capabilities of the business.

The calculations of solvency ratios analysis are as follows:

Gearing ratio:

Gearing ratio is a long term solvency ratio defines the total long term liabilities

against the capital employed (total assets – current liabilities) of the business. The gearing

ratio of Woolworths limited has been reduced from 2013 to 2017 to 64.33%. It explains that

the level of long term liabilities and gearing position has been improved by the business.

Interest coverage ratio:

Further, the interest coverage ratio is a long term solvency ratio defines the EBIT

level against the finance cost of the business to measure that whether the business would be

able to pay the debt cost (Gibson, 2011). The interest coverage ratio of Woolworths limited

has been improved and explains the better position of the company.

It explains that the long term solvency position has been maintained by the company a

great level.

Stock market ratios:

Stock market performance ratios are calculated by the analyst and the investors to

measure the market position of the business on the basis of their earnings, dividend and the

stock price of the business. The stock market ratio analysis process makes it easier for the

analyst and the investors to identify the market position and attractiveness of the company

among the investors (Gibson, 2011). In case of Woolworths limited, earnings per share and

dividend coverage ratio of the business has been calculated to identify the market

attractiveness of the business. The calculations of stock market ratios analysis are as follows:

Earnings per share:

Earnings per share define total earnings which have been generated by the company

for each of the shareholders. The level of EPS has been improved and brief better investment

and marketing level of the business.

Dividend coverage ratio:

Dividend coverage ratio defines total time in which the dividend amount could be

paid the shareholders against the net profit of the business (Annual report, 2017). The level of

8

been calculated to identify the long term obligation management capabilities of the business.

The calculations of solvency ratios analysis are as follows:

Gearing ratio:

Gearing ratio is a long term solvency ratio defines the total long term liabilities

against the capital employed (total assets – current liabilities) of the business. The gearing

ratio of Woolworths limited has been reduced from 2013 to 2017 to 64.33%. It explains that

the level of long term liabilities and gearing position has been improved by the business.

Interest coverage ratio:

Further, the interest coverage ratio is a long term solvency ratio defines the EBIT

level against the finance cost of the business to measure that whether the business would be

able to pay the debt cost (Gibson, 2011). The interest coverage ratio of Woolworths limited

has been improved and explains the better position of the company.

It explains that the long term solvency position has been maintained by the company a

great level.

Stock market ratios:

Stock market performance ratios are calculated by the analyst and the investors to

measure the market position of the business on the basis of their earnings, dividend and the

stock price of the business. The stock market ratio analysis process makes it easier for the

analyst and the investors to identify the market position and attractiveness of the company

among the investors (Gibson, 2011). In case of Woolworths limited, earnings per share and

dividend coverage ratio of the business has been calculated to identify the market

attractiveness of the business. The calculations of stock market ratios analysis are as follows:

Earnings per share:

Earnings per share define total earnings which have been generated by the company

for each of the shareholders. The level of EPS has been improved and brief better investment

and marketing level of the business.

Dividend coverage ratio:

Dividend coverage ratio defines total time in which the dividend amount could be

paid the shareholders against the net profit of the business (Annual report, 2017). The level of

Accounting for managers

9

dividend coverage ratio has been improved and brief better investment and marketing level of

the business.

On the basis of the market ratio of the business, it has been found that the position has

been improved by the business to attract more customers towards the business.

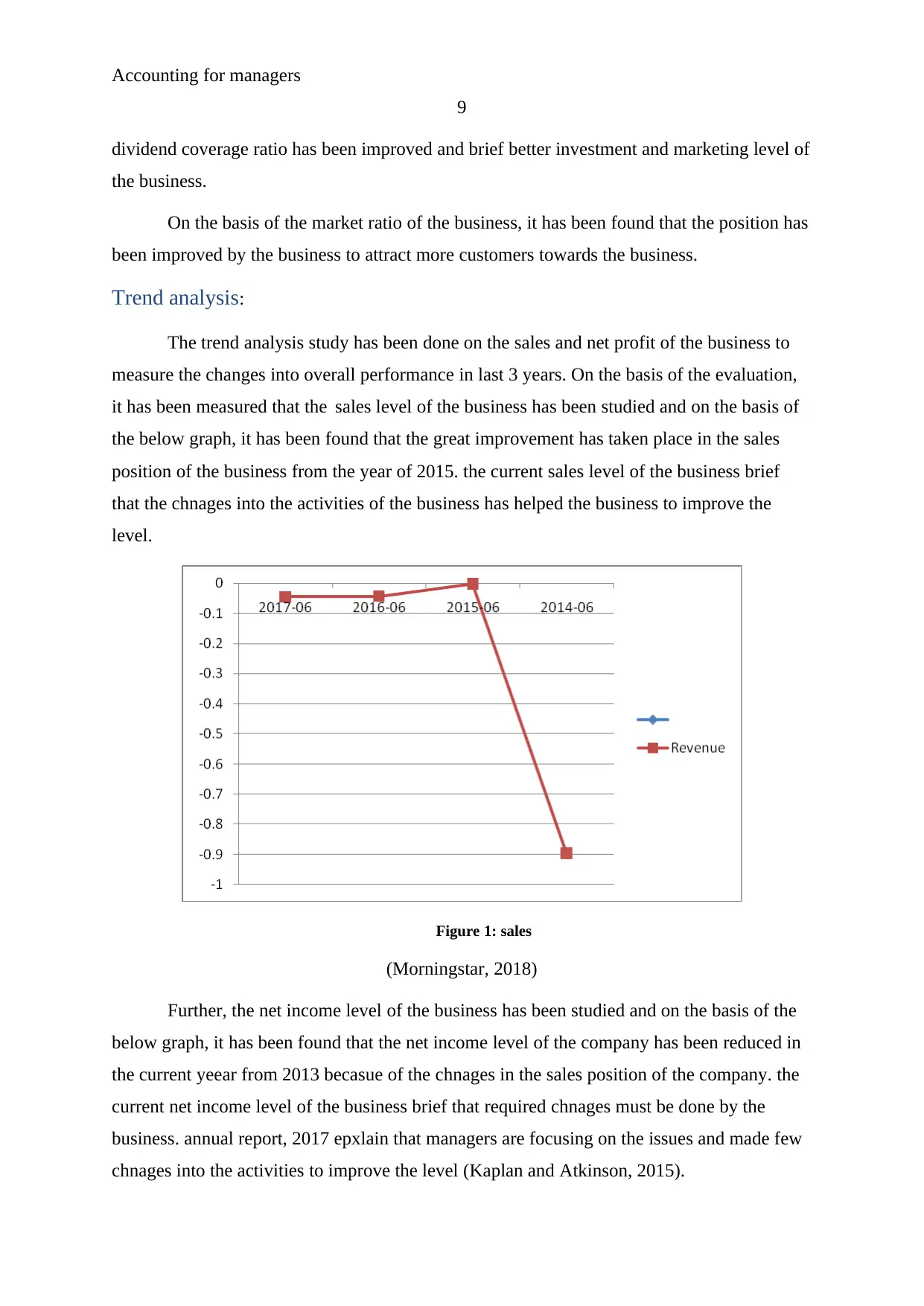

Trend analysis:

The trend analysis study has been done on the sales and net profit of the business to

measure the changes into overall performance in last 3 years. On the basis of the evaluation,

it has been measured that the sales level of the business has been studied and on the basis of

the below graph, it has been found that the great improvement has taken place in the sales

position of the business from the year of 2015. the current sales level of the business brief

that the chnages into the activities of the business has helped the business to improve the

level.

Figure 1: sales

(Morningstar, 2018)

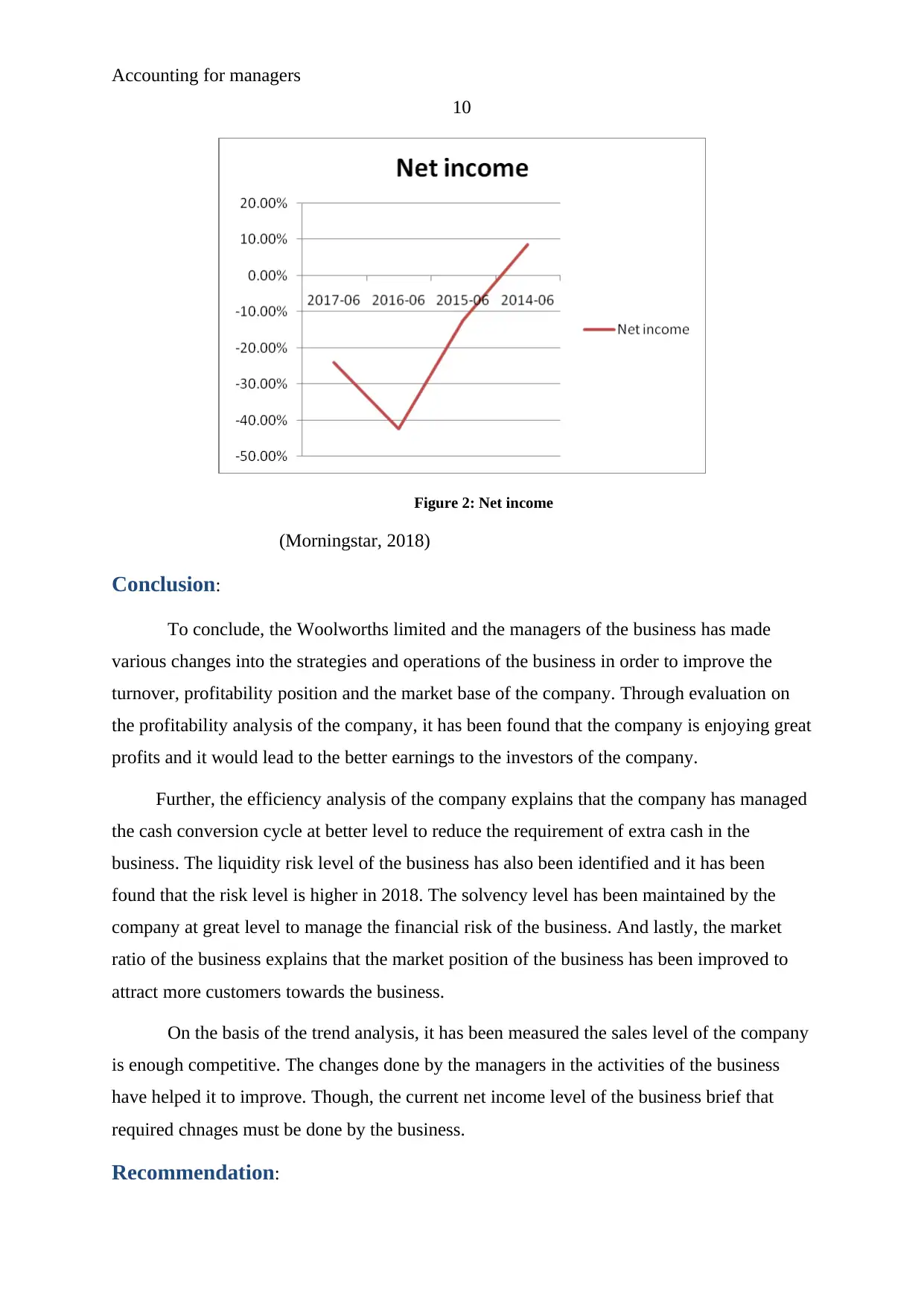

Further, the net income level of the business has been studied and on the basis of the

below graph, it has been found that the net income level of the company has been reduced in

the current yeear from 2013 becasue of the chnages in the sales position of the company. the

current net income level of the business brief that required chnages must be done by the

business. annual report, 2017 epxlain that managers are focusing on the issues and made few

chnages into the activities to improve the level (Kaplan and Atkinson, 2015).

9

dividend coverage ratio has been improved and brief better investment and marketing level of

the business.

On the basis of the market ratio of the business, it has been found that the position has

been improved by the business to attract more customers towards the business.

Trend analysis:

The trend analysis study has been done on the sales and net profit of the business to

measure the changes into overall performance in last 3 years. On the basis of the evaluation,

it has been measured that the sales level of the business has been studied and on the basis of

the below graph, it has been found that the great improvement has taken place in the sales

position of the business from the year of 2015. the current sales level of the business brief

that the chnages into the activities of the business has helped the business to improve the

level.

Figure 1: sales

(Morningstar, 2018)

Further, the net income level of the business has been studied and on the basis of the

below graph, it has been found that the net income level of the company has been reduced in

the current yeear from 2013 becasue of the chnages in the sales position of the company. the

current net income level of the business brief that required chnages must be done by the

business. annual report, 2017 epxlain that managers are focusing on the issues and made few

chnages into the activities to improve the level (Kaplan and Atkinson, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for managers

10

Figure 2: Net income

(Morningstar, 2018)

Conclusion:

To conclude, the Woolworths limited and the managers of the business has made

various changes into the strategies and operations of the business in order to improve the

turnover, profitability position and the market base of the company. Through evaluation on

the profitability analysis of the company, it has been found that the company is enjoying great

profits and it would lead to the better earnings to the investors of the company.

Further, the efficiency analysis of the company explains that the company has managed

the cash conversion cycle at better level to reduce the requirement of extra cash in the

business. The liquidity risk level of the business has also been identified and it has been

found that the risk level is higher in 2018. The solvency level has been maintained by the

company at great level to manage the financial risk of the business. And lastly, the market

ratio of the business explains that the market position of the business has been improved to

attract more customers towards the business.

On the basis of the trend analysis, it has been measured the sales level of the company

is enough competitive. The changes done by the managers in the activities of the business

have helped it to improve. Though, the current net income level of the business brief that

required chnages must be done by the business.

Recommendation:

10

Figure 2: Net income

(Morningstar, 2018)

Conclusion:

To conclude, the Woolworths limited and the managers of the business has made

various changes into the strategies and operations of the business in order to improve the

turnover, profitability position and the market base of the company. Through evaluation on

the profitability analysis of the company, it has been found that the company is enjoying great

profits and it would lead to the better earnings to the investors of the company.

Further, the efficiency analysis of the company explains that the company has managed

the cash conversion cycle at better level to reduce the requirement of extra cash in the

business. The liquidity risk level of the business has also been identified and it has been

found that the risk level is higher in 2018. The solvency level has been maintained by the

company at great level to manage the financial risk of the business. And lastly, the market

ratio of the business explains that the market position of the business has been improved to

attract more customers towards the business.

On the basis of the trend analysis, it has been measured the sales level of the company

is enough competitive. The changes done by the managers in the activities of the business

have helped it to improve. Though, the current net income level of the business brief that

required chnages must be done by the business.

Recommendation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers

11

Through conducting the study on the financial ratios of the business, it has been found

that the company is required to focus on its operating expenses which have impacted on the

profitability ratio a lot. The director’s message has also depicted that few required changes

would be done by the business. The liquidity position must also be improved by the business

in order to manage the liquidity risk of the business. Further, the business is also

recommended to evaluate the turnover days and efficiency position to manage and lower the

cash conversion cycle of the business. The annual report (2017) of Woolworths limited has

described that the company has maintained proper strategies to manage the liquidity risk of

the business.

The proper strategies have been described by the business in the financial risk

management heading to describe the shareholders and other stakeholders of the business. So

that the attractiveness level of the business could be improved and it could offer a better base

to the investors of the company. annual report, 2017 epxlains that managers are focusing on

the issues and made few chnages into the activities to improve the net income level. On the

basis of the overall evaluation, it has been found that the investment into the stock of

Woolworths limited is better option for the business.

11

Through conducting the study on the financial ratios of the business, it has been found

that the company is required to focus on its operating expenses which have impacted on the

profitability ratio a lot. The director’s message has also depicted that few required changes

would be done by the business. The liquidity position must also be improved by the business

in order to manage the liquidity risk of the business. Further, the business is also

recommended to evaluate the turnover days and efficiency position to manage and lower the

cash conversion cycle of the business. The annual report (2017) of Woolworths limited has

described that the company has maintained proper strategies to manage the liquidity risk of

the business.

The proper strategies have been described by the business in the financial risk

management heading to describe the shareholders and other stakeholders of the business. So

that the attractiveness level of the business could be improved and it could offer a better base

to the investors of the company. annual report, 2017 epxlains that managers are focusing on

the issues and made few chnages into the activities to improve the net income level. On the

basis of the overall evaluation, it has been found that the investment into the stock of

Woolworths limited is better option for the business.

Accounting for managers

12

References:

Ahrendsen, B. L., & Katchova, A. L. 2012. Financial ratio analysis using ARMS

data. Agricultural Finance Review, 72(2), p.p. 262-272.

Annual report, 2017. Woolworths Limited. (Online). Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2017.pdf (accessed

20/09/2018).

Baker, H. K., & English, P. 2011. Capital budgeting valuation: Financial analysis for today's

investment projects (Vol. 13). John Wiley & Sons.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Gibson, C.H., 2011. Financial reporting and analysis. South-Western Cengage Learning.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hogarth, R.M. and Makridakis, S., 2011. Forecasting and planning: An

evaluation. Management science, 27(2), pp.115-138.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Koller, T., Goedhart, M. and Wessels, D., 2010. Valuation: measuring and managing the

value of companies (Vol. 499). john Wiley and sons.

Madura, J., 2011. International financial management. Cengage Learning.

Morningstar. 2018. Woolworths Limited. (Online). Available at:

http://financials.morningstar.com/cash-flow/cf.html?t=WOW®ion=aus&culture=en-US

(accessed 20/09/2018).

Moyer, R. C., McGuigan, J., Rao, R., & Kretlow, W. 2011. Contemporary financial

management. Nelson Education.

Reuters. 2018. Woolworths Limited. (Online). Available at:,

https://www.reuters.com/finance/stocks/company-profile/WOW.AX (accessed 20/09/2018).

Yahoo Finance, 2018. Woolworths Limited. (Online). Available at:

https://au.finance.yahoo.com/quote/WOW.AX/ (accessed 20/09/2018).

12

References:

Ahrendsen, B. L., & Katchova, A. L. 2012. Financial ratio analysis using ARMS

data. Agricultural Finance Review, 72(2), p.p. 262-272.

Annual report, 2017. Woolworths Limited. (Online). Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2017.pdf (accessed

20/09/2018).

Baker, H. K., & English, P. 2011. Capital budgeting valuation: Financial analysis for today's

investment projects (Vol. 13). John Wiley & Sons.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Gibson, C.H., 2011. Financial reporting and analysis. South-Western Cengage Learning.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Hogarth, R.M. and Makridakis, S., 2011. Forecasting and planning: An

evaluation. Management science, 27(2), pp.115-138.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Koller, T., Goedhart, M. and Wessels, D., 2010. Valuation: measuring and managing the

value of companies (Vol. 499). john Wiley and sons.

Madura, J., 2011. International financial management. Cengage Learning.

Morningstar. 2018. Woolworths Limited. (Online). Available at:

http://financials.morningstar.com/cash-flow/cf.html?t=WOW®ion=aus&culture=en-US

(accessed 20/09/2018).

Moyer, R. C., McGuigan, J., Rao, R., & Kretlow, W. 2011. Contemporary financial

management. Nelson Education.

Reuters. 2018. Woolworths Limited. (Online). Available at:,

https://www.reuters.com/finance/stocks/company-profile/WOW.AX (accessed 20/09/2018).

Yahoo Finance, 2018. Woolworths Limited. (Online). Available at:

https://au.finance.yahoo.com/quote/WOW.AX/ (accessed 20/09/2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.