Business Finance: Working Capital Management and Capital Budgeting

VerifiedAdded on 2021/04/19

|16

|3690

|161

Report

AI Summary

This report provides a comprehensive analysis of working capital management and capital budgeting techniques in business finance. It begins with an executive summary outlining the key concepts discussed, including the difference between profit and cash flow, the impact of working capital on...

RUNNING HEAD: BUSINESS FINANCE

Working capital management and capital budgeting

Working capital management and capital budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE 1

Executive summary

The reports include a concise knowledge related to the management of cash, working capital and

importance of capital budgeting techniques along with the examples. The first part of the report

deals with difference between profit and cash flow as well as states the reason for having

shortage of cash in the business. It also explains the terms like working capital, payables, and

also the effect of changes in working capital on the cash flow.

The second part of the reports concerns with the introduction of capital budgeting, its purpose

and process. It also shows the merit and demerits of investment appraisal methods and their use

with the help of examples. Overall analysis of cash management and capital budgeting

techniques is done followed by the conclusion and recommendation.

Executive summary

The reports include a concise knowledge related to the management of cash, working capital and

importance of capital budgeting techniques along with the examples. The first part of the report

deals with difference between profit and cash flow as well as states the reason for having

shortage of cash in the business. It also explains the terms like working capital, payables, and

also the effect of changes in working capital on the cash flow.

The second part of the reports concerns with the introduction of capital budgeting, its purpose

and process. It also shows the merit and demerits of investment appraisal methods and their use

with the help of examples. Overall analysis of cash management and capital budgeting

techniques is done followed by the conclusion and recommendation.

BUSINESS FINANCE 2

Contents

Part 1...........................................................................................................................................................3

Requirement A........................................................................................................................................3

Requirement B.........................................................................................................................................4

Requirement C.........................................................................................................................................5

Part 2...........................................................................................................................................................6

Requirement A........................................................................................................................................6

Requirement B.........................................................................................................................................9

Requirement C.......................................................................................................................................12

Conclusion.................................................................................................................................................12

References.................................................................................................................................................14

Contents

Part 1...........................................................................................................................................................3

Requirement A........................................................................................................................................3

Requirement B.........................................................................................................................................4

Requirement C.........................................................................................................................................5

Part 2...........................................................................................................................................................6

Requirement A........................................................................................................................................6

Requirement B.........................................................................................................................................9

Requirement C.......................................................................................................................................12

Conclusion.................................................................................................................................................12

References.................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE 3

Part 1

Requirement A

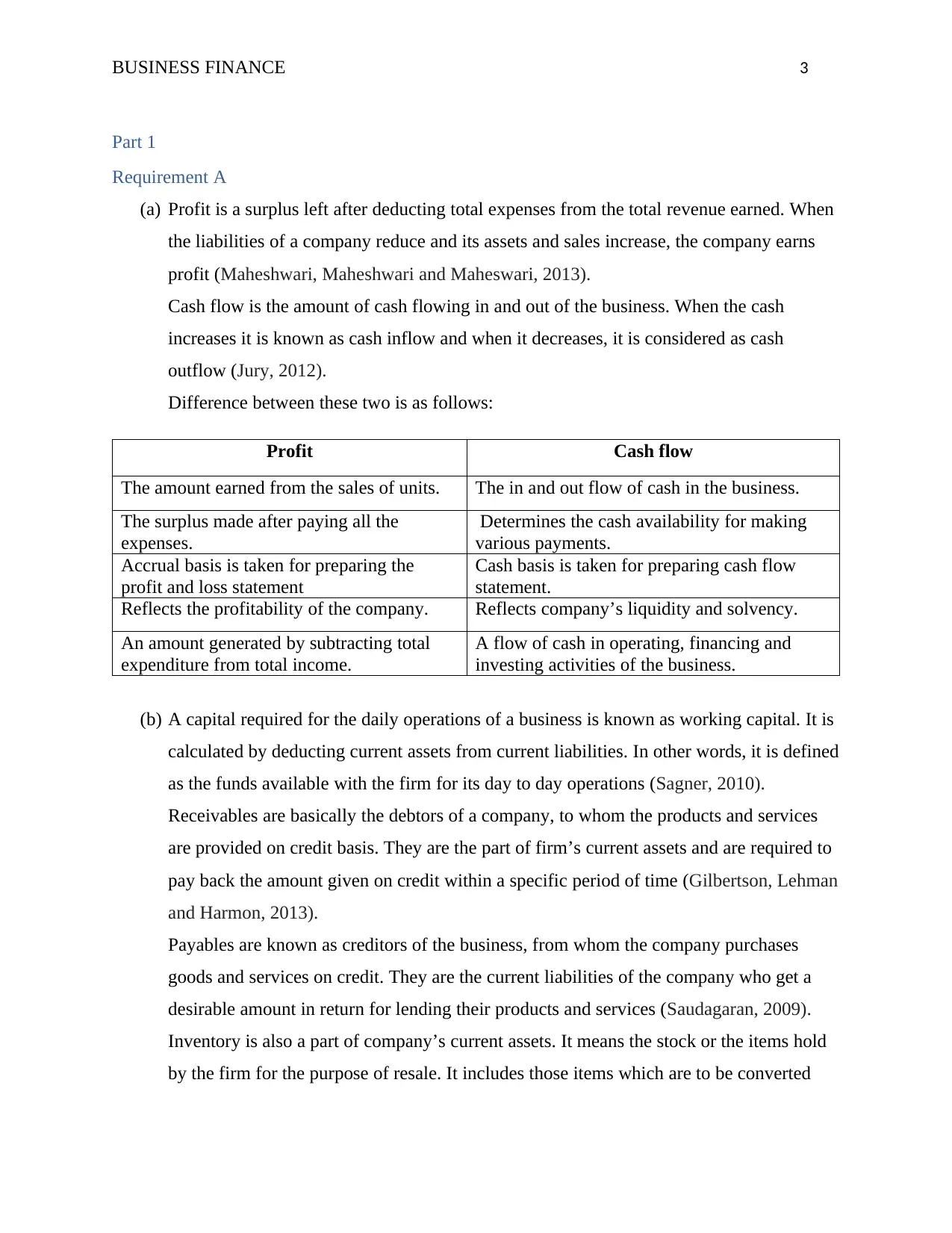

(a) Profit is a surplus left after deducting total expenses from the total revenue earned. When

the liabilities of a company reduce and its assets and sales increase, the company earns

profit (Maheshwari, Maheshwari and Maheswari, 2013).

Cash flow is the amount of cash flowing in and out of the business. When the cash

increases it is known as cash inflow and when it decreases, it is considered as cash

outflow (Jury, 2012).

Difference between these two is as follows:

Profit Cash flow

The amount earned from the sales of units. The in and out flow of cash in the business.

The surplus made after paying all the

expenses.

Determines the cash availability for making

various payments.

Accrual basis is taken for preparing the

profit and loss statement

Cash basis is taken for preparing cash flow

statement.

Reflects the profitability of the company. Reflects company’s liquidity and solvency.

An amount generated by subtracting total

expenditure from total income.

A flow of cash in operating, financing and

investing activities of the business.

(b) A capital required for the daily operations of a business is known as working capital. It is

calculated by deducting current assets from current liabilities. In other words, it is defined

as the funds available with the firm for its day to day operations (Sagner, 2010).

Receivables are basically the debtors of a company, to whom the products and services

are provided on credit basis. They are the part of firm’s current assets and are required to

pay back the amount given on credit within a specific period of time (Gilbertson, Lehman

and Harmon, 2013).

Payables are known as creditors of the business, from whom the company purchases

goods and services on credit. They are the current liabilities of the company who get a

desirable amount in return for lending their products and services (Saudagaran, 2009).

Inventory is also a part of company’s current assets. It means the stock or the items hold

by the firm for the purpose of resale. It includes those items which are to be converted

Part 1

Requirement A

(a) Profit is a surplus left after deducting total expenses from the total revenue earned. When

the liabilities of a company reduce and its assets and sales increase, the company earns

profit (Maheshwari, Maheshwari and Maheswari, 2013).

Cash flow is the amount of cash flowing in and out of the business. When the cash

increases it is known as cash inflow and when it decreases, it is considered as cash

outflow (Jury, 2012).

Difference between these two is as follows:

Profit Cash flow

The amount earned from the sales of units. The in and out flow of cash in the business.

The surplus made after paying all the

expenses.

Determines the cash availability for making

various payments.

Accrual basis is taken for preparing the

profit and loss statement

Cash basis is taken for preparing cash flow

statement.

Reflects the profitability of the company. Reflects company’s liquidity and solvency.

An amount generated by subtracting total

expenditure from total income.

A flow of cash in operating, financing and

investing activities of the business.

(b) A capital required for the daily operations of a business is known as working capital. It is

calculated by deducting current assets from current liabilities. In other words, it is defined

as the funds available with the firm for its day to day operations (Sagner, 2010).

Receivables are basically the debtors of a company, to whom the products and services

are provided on credit basis. They are the part of firm’s current assets and are required to

pay back the amount given on credit within a specific period of time (Gilbertson, Lehman

and Harmon, 2013).

Payables are known as creditors of the business, from whom the company purchases

goods and services on credit. They are the current liabilities of the company who get a

desirable amount in return for lending their products and services (Saudagaran, 2009).

Inventory is also a part of company’s current assets. It means the stock or the items hold

by the firm for the purpose of resale. It includes those items which are to be converted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE 4

into cash within one year. The inventory mainly comprises of raw materials, work in

progress and finished goods (Muller, 2011).

The cash flow of the firm is directly affected by the changes in working capital. Increase in

capital implies that the current assets have risen through investing the resources, which

ultimately reduces the cash flow in the business. On the other hand, decrease in the capital means

current liabilities have raised which reflects that there is an inflow of cash in the business.

Therefore, it can be said that working capital does affect the cash flow of the company and it is

very necessary to analyze the changes in working capital while making the cash flow statement

(Faulkender, et al., 2012).

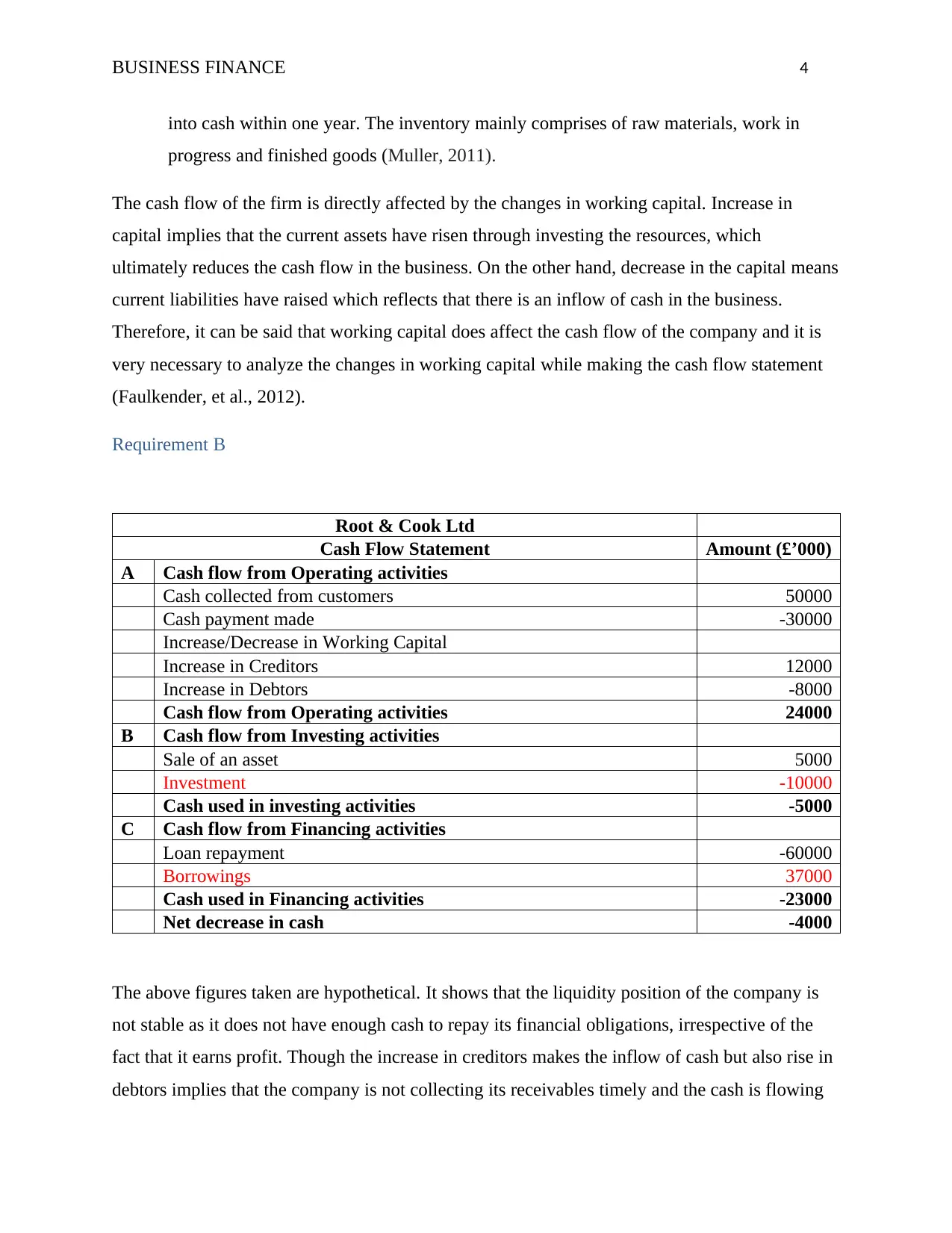

Requirement B

Root & Cook Ltd

Cash Flow Statement Amount (£’000)

A Cash flow from Operating activities

Cash collected from customers 50000

Cash payment made -30000

Increase/Decrease in Working Capital

Increase in Creditors 12000

Increase in Debtors -8000

Cash flow from Operating activities 24000

B Cash flow from Investing activities

Sale of an asset 5000

Investment -10000

Cash used in investing activities -5000

C Cash flow from Financing activities

Loan repayment -60000

Borrowings 37000

Cash used in Financing activities -23000

Net decrease in cash -4000

The above figures taken are hypothetical. It shows that the liquidity position of the company is

not stable as it does not have enough cash to repay its financial obligations, irrespective of the

fact that it earns profit. Though the increase in creditors makes the inflow of cash but also rise in

debtors implies that the company is not collecting its receivables timely and the cash is flowing

into cash within one year. The inventory mainly comprises of raw materials, work in

progress and finished goods (Muller, 2011).

The cash flow of the firm is directly affected by the changes in working capital. Increase in

capital implies that the current assets have risen through investing the resources, which

ultimately reduces the cash flow in the business. On the other hand, decrease in the capital means

current liabilities have raised which reflects that there is an inflow of cash in the business.

Therefore, it can be said that working capital does affect the cash flow of the company and it is

very necessary to analyze the changes in working capital while making the cash flow statement

(Faulkender, et al., 2012).

Requirement B

Root & Cook Ltd

Cash Flow Statement Amount (£’000)

A Cash flow from Operating activities

Cash collected from customers 50000

Cash payment made -30000

Increase/Decrease in Working Capital

Increase in Creditors 12000

Increase in Debtors -8000

Cash flow from Operating activities 24000

B Cash flow from Investing activities

Sale of an asset 5000

Investment -10000

Cash used in investing activities -5000

C Cash flow from Financing activities

Loan repayment -60000

Borrowings 37000

Cash used in Financing activities -23000

Net decrease in cash -4000

The above figures taken are hypothetical. It shows that the liquidity position of the company is

not stable as it does not have enough cash to repay its financial obligations, irrespective of the

fact that it earns profit. Though the increase in creditors makes the inflow of cash but also rise in

debtors implies that the company is not collecting its receivables timely and the cash is flowing

BUSINESS FINANCE 5

out of the business. In order to manage its financial condition, company needs to raise cash from

investing and financing activities also. The amount generated from sales revenue is not enough

for setting off the debts of the business. Because of the dispute between RCL and BricoFrance,

the payment of the consignment worth £20 million, is on hold which restricts the flow of cash in

the business. So it is not necessary that if a company is making profits, it is highly stable in terms

of liquidity. It is required for the business to derive cash from the activities other than operating

(Tracy and Tracy, 2011).

Requirement C

By managing the working capital, RCL can improve its cash flow. A proper management of the

capital will have a positive impact on the movement of cash in the business (Aktas, Croci and

Petmezas, 2015). Certain steps can be taken form improving the cash flow statement:

Enhancing receivables collection: The position of RCL’s cash flow shows that the

company’s debtors and suppliers are not properly managed. There is an increase in the

accounts receivables and the collection is not done timely. So, it is necessary for the

company to lay more emphasis on improving its debt collection, so that more cash will be

available for paying other debts.

Categorization of suppliers, customers and inventory: Proper segmentation of the

suppliers should be done according to their relations with the company that is regular

ones or the one from whom company purchases on frequent basis. Divide the customers

as per the probability of the payments made by them and segregate the inventory as raw

materials and finished good. This is very important because sometimes most of the

money is tied up in the form of inventory which not appropriate as per the requirement of

the customer. So, segmentation of these three items is necessary.

Forecasting: One of the main step, a company can take is to look after the past and

current position of the cash flow, and then forecast about its future situation. The business

should perform a good forecast and must take suitable decisions regarding its cash flow.

This will help the company to get aware about the future inflow and outflow of cash.

Managing the risk: A proper and authentic process of risk management should be

followed by the company, for the purpose of dealing with uncertainties and

contingencies. The process applied, should be on the basis of role of working capital.

out of the business. In order to manage its financial condition, company needs to raise cash from

investing and financing activities also. The amount generated from sales revenue is not enough

for setting off the debts of the business. Because of the dispute between RCL and BricoFrance,

the payment of the consignment worth £20 million, is on hold which restricts the flow of cash in

the business. So it is not necessary that if a company is making profits, it is highly stable in terms

of liquidity. It is required for the business to derive cash from the activities other than operating

(Tracy and Tracy, 2011).

Requirement C

By managing the working capital, RCL can improve its cash flow. A proper management of the

capital will have a positive impact on the movement of cash in the business (Aktas, Croci and

Petmezas, 2015). Certain steps can be taken form improving the cash flow statement:

Enhancing receivables collection: The position of RCL’s cash flow shows that the

company’s debtors and suppliers are not properly managed. There is an increase in the

accounts receivables and the collection is not done timely. So, it is necessary for the

company to lay more emphasis on improving its debt collection, so that more cash will be

available for paying other debts.

Categorization of suppliers, customers and inventory: Proper segmentation of the

suppliers should be done according to their relations with the company that is regular

ones or the one from whom company purchases on frequent basis. Divide the customers

as per the probability of the payments made by them and segregate the inventory as raw

materials and finished good. This is very important because sometimes most of the

money is tied up in the form of inventory which not appropriate as per the requirement of

the customer. So, segmentation of these three items is necessary.

Forecasting: One of the main step, a company can take is to look after the past and

current position of the cash flow, and then forecast about its future situation. The business

should perform a good forecast and must take suitable decisions regarding its cash flow.

This will help the company to get aware about the future inflow and outflow of cash.

Managing the risk: A proper and authentic process of risk management should be

followed by the company, for the purpose of dealing with uncertainties and

contingencies. The process applied, should be on the basis of role of working capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE 6

Priority of workers: providing an understanding about the cash flow to all the

employees can also help in improving the position of cash in a business. The targets set

for workers should motivate them, as the efficient and effective performance of the staff

will automatically result in increase in the cash position (Damodaran, 2010).

Part 2

Requirement A

(a) Capital budgeting:

It is a process followed by the management of a company, for choosing a better investment

proposal. It is used as a tool by the companies for the purpose of increasing its profits.

Evaluating an investment proposal is one of the challenging task for the management, as it deals

with the allocation of funds to the most appropriate and profitable projects (Morris and Daley,

2017). The managers use capital budgeting tools and techniques for checking the viability,

feasibility and profitability of an investment proposal. It includes calculation of the profit which

can be generated from each project, estimating the present values of the cash inflow, determining

the time taken by the project in recovering the initial cash outlay and assessment of risk and

other factors. The techniques used are NPV, IRR, pay back method and ARR. These are also

known as investment appraisal methods (Bose, 2011).

Purpose

Certain objective of the company can be achieved by using capital budgeting techniques. The

purpose of doing it is as follows:

To determine the capital expenditure which is most profitable.

Selecting a specific project or proposal.

To examine that replace of any existing fixed asset will generate more returns or not.

Determining the amount of funds required for financing the capital expenditure.

Finding out the sources of funds and,

Choosing the best investment proposal or option among the alternatives.

Apart from the above objectives, it is very important for the business to take correct and proper

decisions regarding the investment, so as to derive more profits in the long run. For this purpose,

Priority of workers: providing an understanding about the cash flow to all the

employees can also help in improving the position of cash in a business. The targets set

for workers should motivate them, as the efficient and effective performance of the staff

will automatically result in increase in the cash position (Damodaran, 2010).

Part 2

Requirement A

(a) Capital budgeting:

It is a process followed by the management of a company, for choosing a better investment

proposal. It is used as a tool by the companies for the purpose of increasing its profits.

Evaluating an investment proposal is one of the challenging task for the management, as it deals

with the allocation of funds to the most appropriate and profitable projects (Morris and Daley,

2017). The managers use capital budgeting tools and techniques for checking the viability,

feasibility and profitability of an investment proposal. It includes calculation of the profit which

can be generated from each project, estimating the present values of the cash inflow, determining

the time taken by the project in recovering the initial cash outlay and assessment of risk and

other factors. The techniques used are NPV, IRR, pay back method and ARR. These are also

known as investment appraisal methods (Bose, 2011).

Purpose

Certain objective of the company can be achieved by using capital budgeting techniques. The

purpose of doing it is as follows:

To determine the capital expenditure which is most profitable.

Selecting a specific project or proposal.

To examine that replace of any existing fixed asset will generate more returns or not.

Determining the amount of funds required for financing the capital expenditure.

Finding out the sources of funds and,

Choosing the best investment proposal or option among the alternatives.

Apart from the above objectives, it is very important for the business to take correct and proper

decisions regarding the investment, so as to derive more profits in the long run. For this purpose,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE 7

appropriate capital budgeting techniques should be used, as the decision made will affect the

overall profitability of the company (Baker and English, 2011).

Process

A process generally include the steps related to identification, estimation, selection, analysis,

review and implementation of a proposal. The process of capital budgeting is very flexible

because of the changes taking place in the business environment. These changes can affect the

project and also the investment made in it (Abor, 2016). The stages involved are:

Identifying the proposal: This is the first stage, in which a preliminary screening of all

the available alternatives is done. The task of identification is performed by the

management, followed by further evaluation and screening.

Cash flow estimates: This stage is concerned with the preparation of capital budget for

the selected projects. It shows the estimates made regarding the amount required for

investment.

Project approval: after preparing the budgets, the projects are been sent for the approval

to the authorized people. Generally, the proposals, which include small expenditure get

approved quickly, whereas the one which involves huge expenditure has to go through

the process of authorization and approval.

Evaluating the cash flows: In this stage, evaluation of incremental cash flow is done to

know about their capacity to generate profits and give proper results.

Implementation: It is not the final step, but is performed after completing all the above

stages. It deals with the implementation of the selected project, on which the work is need

to done.

Tracking of the project: This is after implementation stage, in which management team

track the implemented projects and prepare the reports regarding the expenses incurred

and revenue made.

Post completion audit: The audit involves the comparison of actual cash flow with the

budgeted one and a timely review of the project is done to check the feasibility of the

proposal. It also determines, how well a company manages its cash flow.

appropriate capital budgeting techniques should be used, as the decision made will affect the

overall profitability of the company (Baker and English, 2011).

Process

A process generally include the steps related to identification, estimation, selection, analysis,

review and implementation of a proposal. The process of capital budgeting is very flexible

because of the changes taking place in the business environment. These changes can affect the

project and also the investment made in it (Abor, 2016). The stages involved are:

Identifying the proposal: This is the first stage, in which a preliminary screening of all

the available alternatives is done. The task of identification is performed by the

management, followed by further evaluation and screening.

Cash flow estimates: This stage is concerned with the preparation of capital budget for

the selected projects. It shows the estimates made regarding the amount required for

investment.

Project approval: after preparing the budgets, the projects are been sent for the approval

to the authorized people. Generally, the proposals, which include small expenditure get

approved quickly, whereas the one which involves huge expenditure has to go through

the process of authorization and approval.

Evaluating the cash flows: In this stage, evaluation of incremental cash flow is done to

know about their capacity to generate profits and give proper results.

Implementation: It is not the final step, but is performed after completing all the above

stages. It deals with the implementation of the selected project, on which the work is need

to done.

Tracking of the project: This is after implementation stage, in which management team

track the implemented projects and prepare the reports regarding the expenses incurred

and revenue made.

Post completion audit: The audit involves the comparison of actual cash flow with the

budgeted one and a timely review of the project is done to check the feasibility of the

proposal. It also determines, how well a company manages its cash flow.

BUSINESS FINANCE 8

(b) Investment Appraisal methods

In order to check the financial viability of each and every investment proposal, certain methods

are used by the company. These methods are Net Present value, Payback period, Internal Rate of

return and Average rate of return (Gotze, Northcott and Schuster, 2016).

NPV: It is basically a difference between the PV of cash inflow and PV of cash outflow. The

purpose of calculating NPV is to check the profitability of a project. If NPV is positive, accept

the proposal and if it is negative, reject the same. When NPV is equal to zero, then the company

can accept or reject the project (Weygandt, Kimmel and Kieso, 2009).

Payback Period: In simpler terms, it is the amount of time taken by a project to recover the

initial cash outflow. Usually, projects having short payback period are considered to be more

desirable than the ones, which takes longer time to recoup the initial investment (Periasamy,

2009).

IRR: It is that discounting rate where PV of cash inflow is equal to the PV of cash outflow. The

proposal which has high IRR is more suitable for the purpose of investment (Brealey, et al.,

2012).

Advantage and disadvantages

Methods Advantages Disadvantages

Payback

period

Simple method.

Helps in evaluating the

projects quickly.

Does not takes into account,

time value of money.

Priority is given to liquidity,

rather than profitability.

Net Present

Value.

Increase the value of business.

Measures risk and

profitability of the proposal.

Suitable discount rate cannot

be easily determined.

Not appropriate for the

projects having unequal

investments.

Internal Rate

of Return.

Calculates true profitability.

It is not required to determine

the cost of capital in advance.

Repetitive calculations.

Assumption made may prove

to be wrong.

(Shim, Siegel and Shim, 2011).

(b) Investment Appraisal methods

In order to check the financial viability of each and every investment proposal, certain methods

are used by the company. These methods are Net Present value, Payback period, Internal Rate of

return and Average rate of return (Gotze, Northcott and Schuster, 2016).

NPV: It is basically a difference between the PV of cash inflow and PV of cash outflow. The

purpose of calculating NPV is to check the profitability of a project. If NPV is positive, accept

the proposal and if it is negative, reject the same. When NPV is equal to zero, then the company

can accept or reject the project (Weygandt, Kimmel and Kieso, 2009).

Payback Period: In simpler terms, it is the amount of time taken by a project to recover the

initial cash outflow. Usually, projects having short payback period are considered to be more

desirable than the ones, which takes longer time to recoup the initial investment (Periasamy,

2009).

IRR: It is that discounting rate where PV of cash inflow is equal to the PV of cash outflow. The

proposal which has high IRR is more suitable for the purpose of investment (Brealey, et al.,

2012).

Advantage and disadvantages

Methods Advantages Disadvantages

Payback

period

Simple method.

Helps in evaluating the

projects quickly.

Does not takes into account,

time value of money.

Priority is given to liquidity,

rather than profitability.

Net Present

Value.

Increase the value of business.

Measures risk and

profitability of the proposal.

Suitable discount rate cannot

be easily determined.

Not appropriate for the

projects having unequal

investments.

Internal Rate

of Return.

Calculates true profitability.

It is not required to determine

the cost of capital in advance.

Repetitive calculations.

Assumption made may prove

to be wrong.

(Shim, Siegel and Shim, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE 9

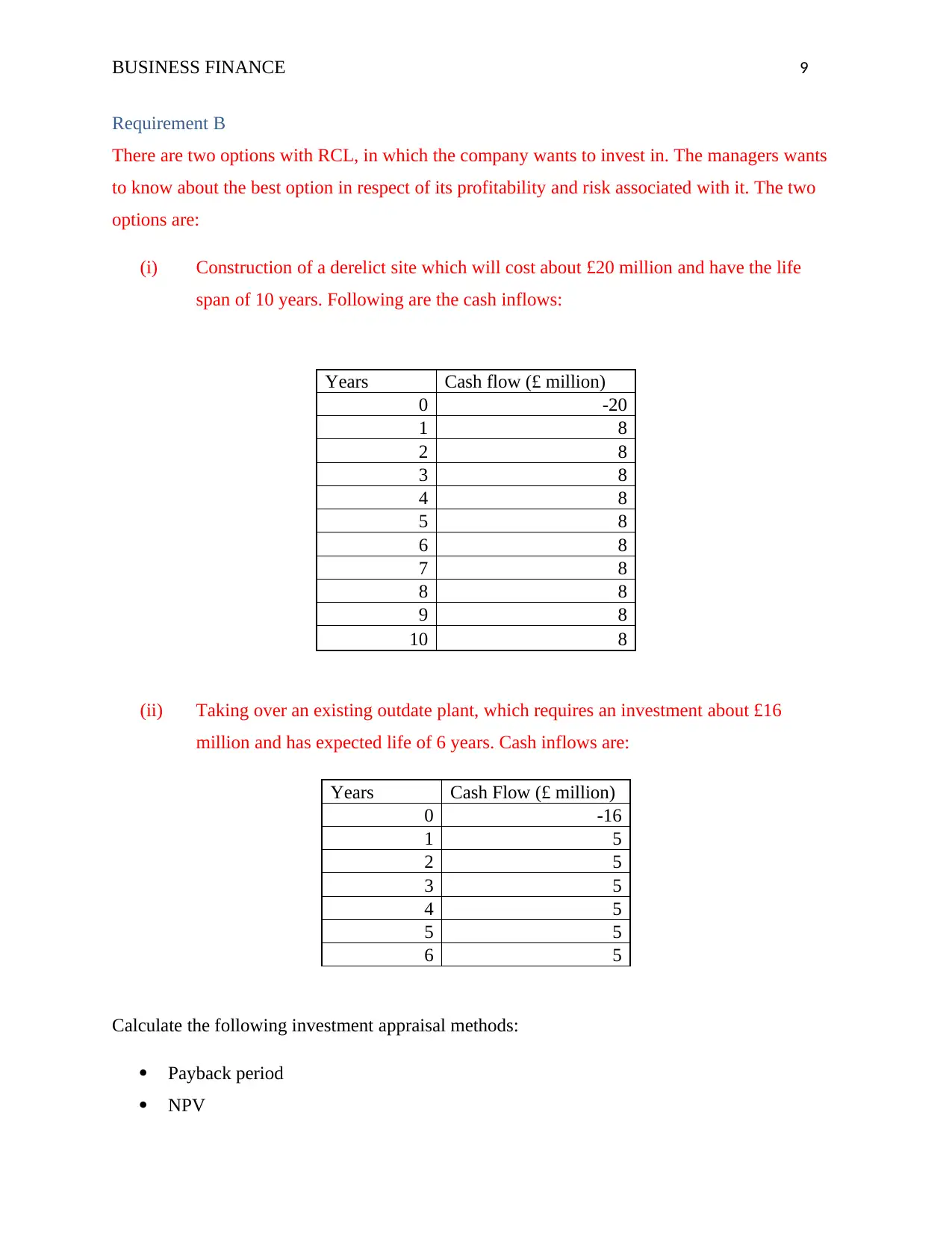

Requirement B

There are two options with RCL, in which the company wants to invest in. The managers wants

to know about the best option in respect of its profitability and risk associated with it. The two

options are:

(i) Construction of a derelict site which will cost about £20 million and have the life

span of 10 years. Following are the cash inflows:

Years Cash flow (£ million)

0 -20

1 8

2 8

3 8

4 8

5 8

6 8

7 8

8 8

9 8

10 8

(ii) Taking over an existing outdate plant, which requires an investment about £16

million and has expected life of 6 years. Cash inflows are:

Years Cash Flow (£ million)

0 -16

1 5

2 5

3 5

4 5

5 5

6 5

Calculate the following investment appraisal methods:

Payback period

NPV

Requirement B

There are two options with RCL, in which the company wants to invest in. The managers wants

to know about the best option in respect of its profitability and risk associated with it. The two

options are:

(i) Construction of a derelict site which will cost about £20 million and have the life

span of 10 years. Following are the cash inflows:

Years Cash flow (£ million)

0 -20

1 8

2 8

3 8

4 8

5 8

6 8

7 8

8 8

9 8

10 8

(ii) Taking over an existing outdate plant, which requires an investment about £16

million and has expected life of 6 years. Cash inflows are:

Years Cash Flow (£ million)

0 -16

1 5

2 5

3 5

4 5

5 5

6 5

Calculate the following investment appraisal methods:

Payback period

NPV

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE 10

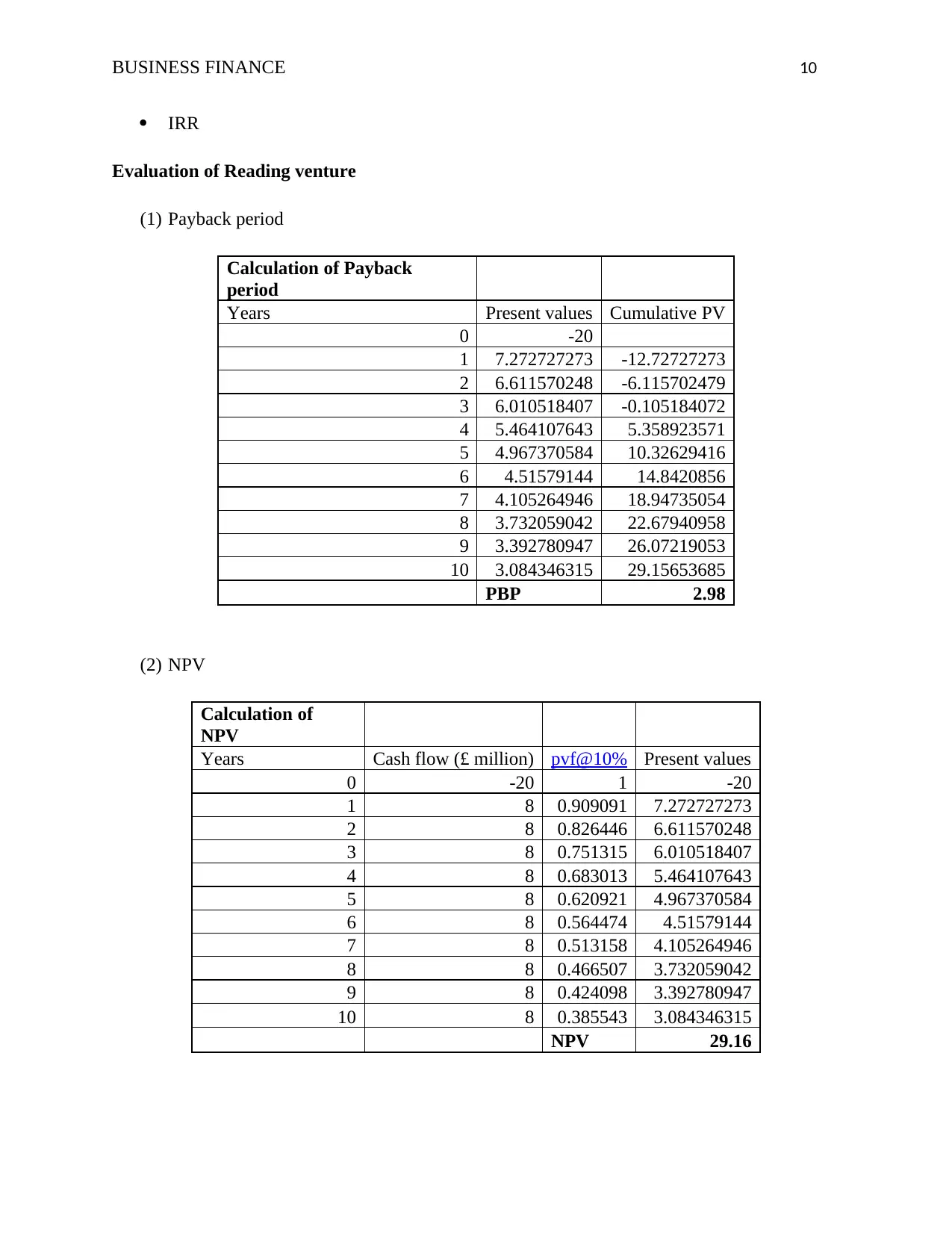

IRR

Evaluation of Reading venture

(1) Payback period

Calculation of Payback

period

Years Present values Cumulative PV

0 -20

1 7.272727273 -12.72727273

2 6.611570248 -6.115702479

3 6.010518407 -0.105184072

4 5.464107643 5.358923571

5 4.967370584 10.32629416

6 4.51579144 14.8420856

7 4.105264946 18.94735054

8 3.732059042 22.67940958

9 3.392780947 26.07219053

10 3.084346315 29.15653685

PBP 2.98

(2) NPV

Calculation of

NPV

Years Cash flow (£ million) pvf@10% Present values

0 -20 1 -20

1 8 0.909091 7.272727273

2 8 0.826446 6.611570248

3 8 0.751315 6.010518407

4 8 0.683013 5.464107643

5 8 0.620921 4.967370584

6 8 0.564474 4.51579144

7 8 0.513158 4.105264946

8 8 0.466507 3.732059042

9 8 0.424098 3.392780947

10 8 0.385543 3.084346315

NPV 29.16

IRR

Evaluation of Reading venture

(1) Payback period

Calculation of Payback

period

Years Present values Cumulative PV

0 -20

1 7.272727273 -12.72727273

2 6.611570248 -6.115702479

3 6.010518407 -0.105184072

4 5.464107643 5.358923571

5 4.967370584 10.32629416

6 4.51579144 14.8420856

7 4.105264946 18.94735054

8 3.732059042 22.67940958

9 3.392780947 26.07219053

10 3.084346315 29.15653685

PBP 2.98

(2) NPV

Calculation of

NPV

Years Cash flow (£ million) pvf@10% Present values

0 -20 1 -20

1 8 0.909091 7.272727273

2 8 0.826446 6.611570248

3 8 0.751315 6.010518407

4 8 0.683013 5.464107643

5 8 0.620921 4.967370584

6 8 0.564474 4.51579144

7 8 0.513158 4.105264946

8 8 0.466507 3.732059042

9 8 0.424098 3.392780947

10 8 0.385543 3.084346315

NPV 29.16

BUSINESS FINANCE 11

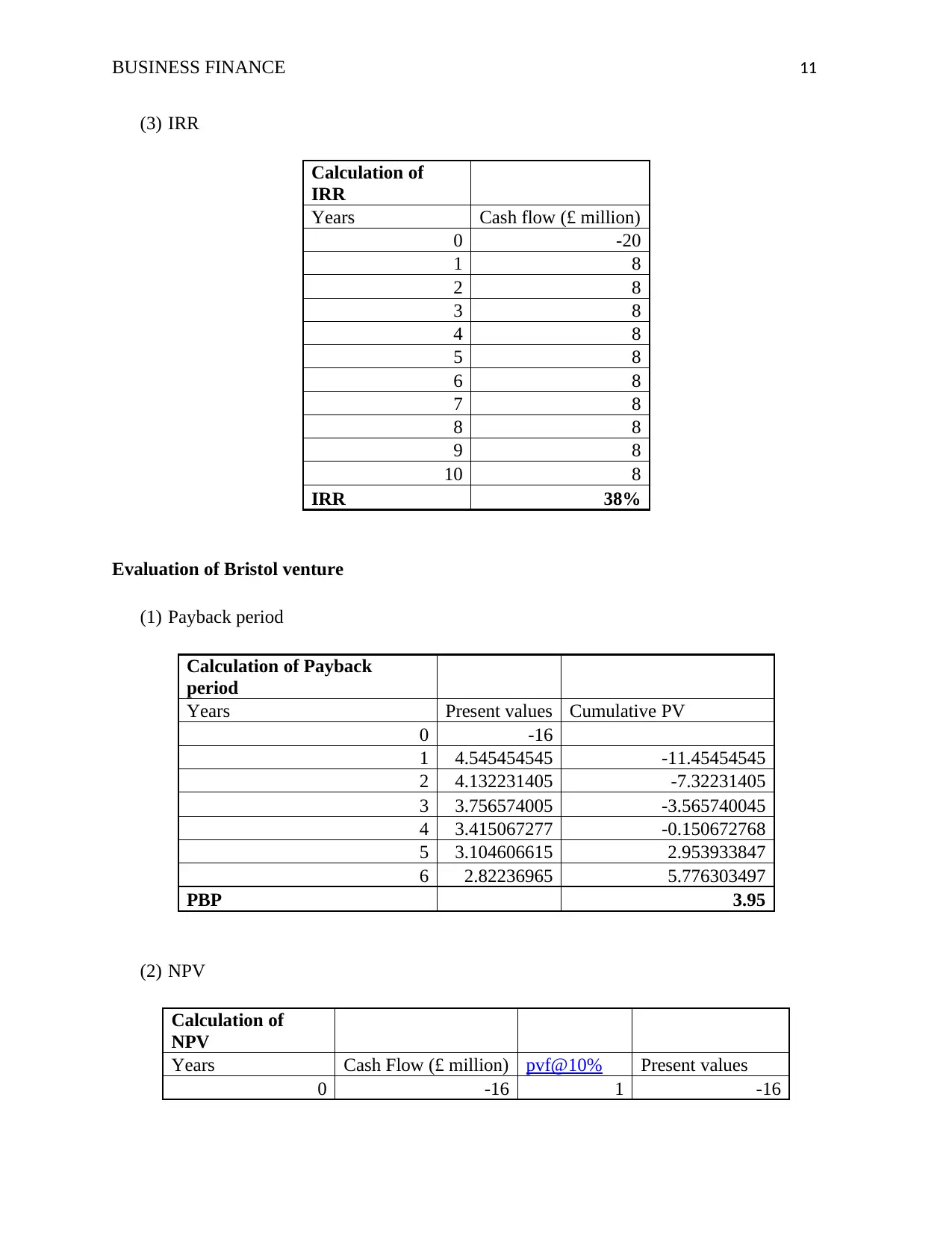

(3) IRR

Calculation of

IRR

Years Cash flow (£ million)

0 -20

1 8

2 8

3 8

4 8

5 8

6 8

7 8

8 8

9 8

10 8

IRR 38%

Evaluation of Bristol venture

(1) Payback period

Calculation of Payback

period

Years Present values Cumulative PV

0 -16

1 4.545454545 -11.45454545

2 4.132231405 -7.32231405

3 3.756574005 -3.565740045

4 3.415067277 -0.150672768

5 3.104606615 2.953933847

6 2.82236965 5.776303497

PBP 3.95

(2) NPV

Calculation of

NPV

Years Cash Flow (£ million) pvf@10% Present values

0 -16 1 -16

(3) IRR

Calculation of

IRR

Years Cash flow (£ million)

0 -20

1 8

2 8

3 8

4 8

5 8

6 8

7 8

8 8

9 8

10 8

IRR 38%

Evaluation of Bristol venture

(1) Payback period

Calculation of Payback

period

Years Present values Cumulative PV

0 -16

1 4.545454545 -11.45454545

2 4.132231405 -7.32231405

3 3.756574005 -3.565740045

4 3.415067277 -0.150672768

5 3.104606615 2.953933847

6 2.82236965 5.776303497

PBP 3.95

(2) NPV

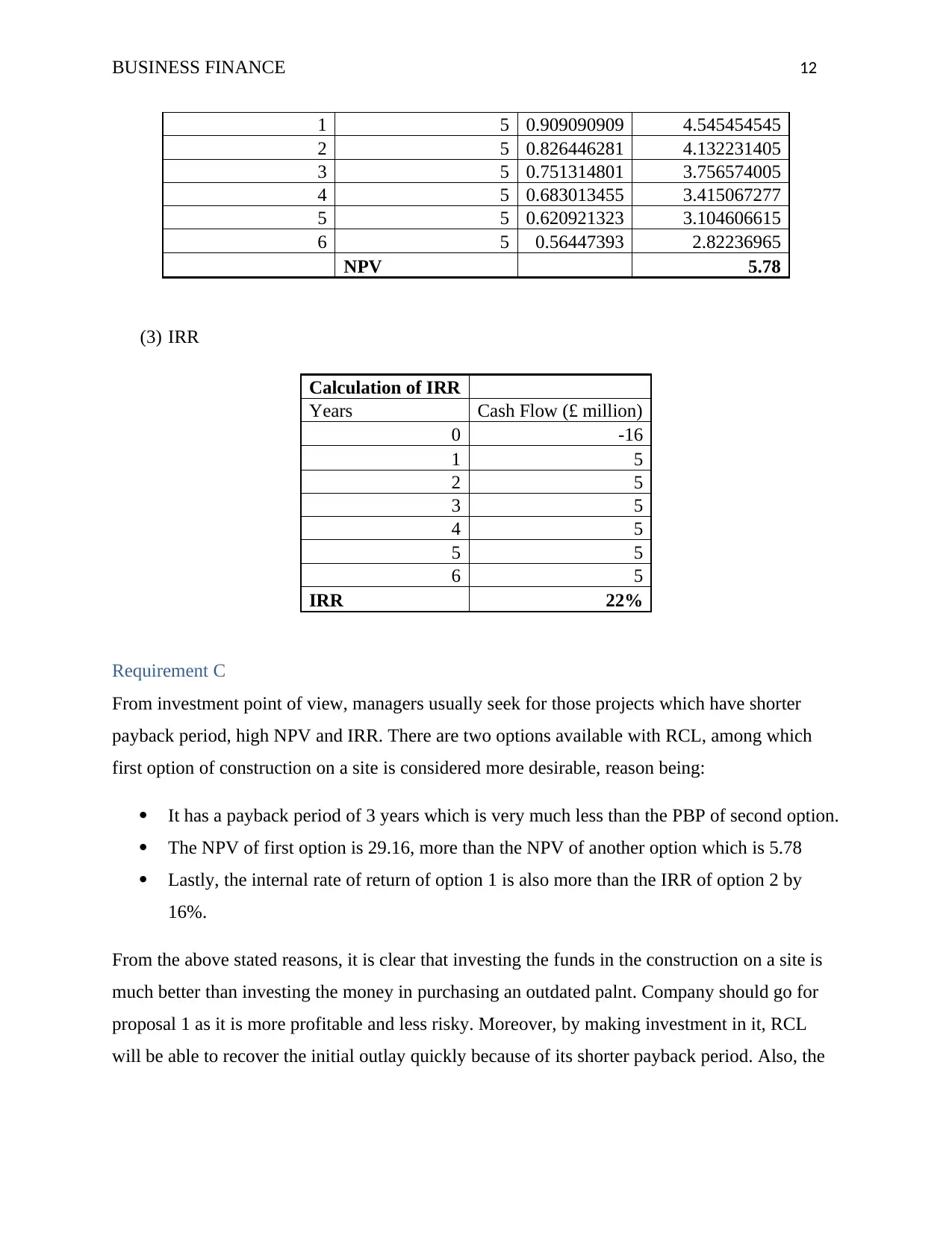

Calculation of

NPV

Years Cash Flow (£ million) pvf@10% Present values

0 -16 1 -16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE 12

1 5 0.909090909 4.545454545

2 5 0.826446281 4.132231405

3 5 0.751314801 3.756574005

4 5 0.683013455 3.415067277

5 5 0.620921323 3.104606615

6 5 0.56447393 2.82236965

NPV 5.78

(3) IRR

Calculation of IRR

Years Cash Flow (£ million)

0 -16

1 5

2 5

3 5

4 5

5 5

6 5

IRR 22%

Requirement C

From investment point of view, managers usually seek for those projects which have shorter

payback period, high NPV and IRR. There are two options available with RCL, among which

first option of construction on a site is considered more desirable, reason being:

It has a payback period of 3 years which is very much less than the PBP of second option.

The NPV of first option is 29.16, more than the NPV of another option which is 5.78

Lastly, the internal rate of return of option 1 is also more than the IRR of option 2 by

16%.

From the above stated reasons, it is clear that investing the funds in the construction on a site is

much better than investing the money in purchasing an outdated palnt. Company should go for

proposal 1 as it is more profitable and less risky. Moreover, by making investment in it, RCL

will be able to recover the initial outlay quickly because of its shorter payback period. Also, the

1 5 0.909090909 4.545454545

2 5 0.826446281 4.132231405

3 5 0.751314801 3.756574005

4 5 0.683013455 3.415067277

5 5 0.620921323 3.104606615

6 5 0.56447393 2.82236965

NPV 5.78

(3) IRR

Calculation of IRR

Years Cash Flow (£ million)

0 -16

1 5

2 5

3 5

4 5

5 5

6 5

IRR 22%

Requirement C

From investment point of view, managers usually seek for those projects which have shorter

payback period, high NPV and IRR. There are two options available with RCL, among which

first option of construction on a site is considered more desirable, reason being:

It has a payback period of 3 years which is very much less than the PBP of second option.

The NPV of first option is 29.16, more than the NPV of another option which is 5.78

Lastly, the internal rate of return of option 1 is also more than the IRR of option 2 by

16%.

From the above stated reasons, it is clear that investing the funds in the construction on a site is

much better than investing the money in purchasing an outdated palnt. Company should go for

proposal 1 as it is more profitable and less risky. Moreover, by making investment in it, RCL

will be able to recover the initial outlay quickly because of its shorter payback period. Also, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE 13

project will be generates profits in future because of higher NPV and IRR. Hence, RCL should

opt for first option as it more suitable (Atrill and McLaney, 2009).

Conclusion

From the above report, it can be concluded that, managing the cash and working capital is very

important for the company to have an effective and efficient growth in future. Also, proper

investment appraisal methods should be used while making investment decision as it can affect

company’s profitability in long run.

project will be generates profits in future because of higher NPV and IRR. Hence, RCL should

opt for first option as it more suitable (Atrill and McLaney, 2009).

Conclusion

From the above report, it can be concluded that, managing the cash and working capital is very

important for the company to have an effective and efficient growth in future. Also, proper

investment appraisal methods should be used while making investment decision as it can affect

company’s profitability in long run.

BUSINESS FINANCE 14

References

Abor, J.Y., (2016). Entrepreneurial Finance for MSMEs: A Managerial Approach for

Developing Markets. Switzerland: Springer.

Aktas, N., Croci, E. and Petmezas, D., (2015). Is working capital management value-

enhancing? Evidence from firm performance and investments. Journal of Corporate

Finance, 30, pp.98-113.

Atrill, P. and McLaney, E., (2009). Management accounting for decision makers. 4th ed.

England: Pearson Education.

Baker, H.K. and English, P., (2011). Capital budgeting valuation: Financial analysis for

today's investment projects (Vol. 13). New Jersey: John Wiley & Sons.

Bose, D.C., (2011). Fundamentals of Financial management. 6th ed. New Delhi: McGraw Hill

Pvt. Ltd.

Brealey, R.A., Myers, S.C., Allen, F. and Mohanty, P., (2012). Principles of corporate finance.

10th ed. New Delhi:Tata McGraw-Hill Education.

Damodaran, A., (2010). Applied corporate finance. 3rd ed. USA: John Wiley & Sons.

Faulkender, M., Flannery, M.J., Hankins, K.W. and Smith, J.M., (2012). Cash flows and

leverage adjustments. Journal of Financial Economics, 103(3), pp.632-646.

Gilbertson, C., Lehman, M.W. and Harmon-Gentene, D., (2013). Fundamentals of

Accounting: Course 1. 10th ed. USA: Cengage Learning.

Gotze, U., Northcott, D. and Schuster, P., (2016). INVESTMENT APPRAISAL. 2nd ed. London:

SPRINGER-VERLAG BERLIN AN.

References

Abor, J.Y., (2016). Entrepreneurial Finance for MSMEs: A Managerial Approach for

Developing Markets. Switzerland: Springer.

Aktas, N., Croci, E. and Petmezas, D., (2015). Is working capital management value-

enhancing? Evidence from firm performance and investments. Journal of Corporate

Finance, 30, pp.98-113.

Atrill, P. and McLaney, E., (2009). Management accounting for decision makers. 4th ed.

England: Pearson Education.

Baker, H.K. and English, P., (2011). Capital budgeting valuation: Financial analysis for

today's investment projects (Vol. 13). New Jersey: John Wiley & Sons.

Bose, D.C., (2011). Fundamentals of Financial management. 6th ed. New Delhi: McGraw Hill

Pvt. Ltd.

Brealey, R.A., Myers, S.C., Allen, F. and Mohanty, P., (2012). Principles of corporate finance.

10th ed. New Delhi:Tata McGraw-Hill Education.

Damodaran, A., (2010). Applied corporate finance. 3rd ed. USA: John Wiley & Sons.

Faulkender, M., Flannery, M.J., Hankins, K.W. and Smith, J.M., (2012). Cash flows and

leverage adjustments. Journal of Financial Economics, 103(3), pp.632-646.

Gilbertson, C., Lehman, M.W. and Harmon-Gentene, D., (2013). Fundamentals of

Accounting: Course 1. 10th ed. USA: Cengage Learning.

Gotze, U., Northcott, D. and Schuster, P., (2016). INVESTMENT APPRAISAL. 2nd ed. London:

SPRINGER-VERLAG BERLIN AN.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE 15

Jury, T., (2012). Cash flow analysis and forecasting: the definitive guide to understanding and

using published cash flow data (Vol. 653). USA: John Wiley & Sons.

Maheshwari, S.N., Maheshwari, S.K. and Maheswari, S.K., (2013). An Introduction to

Accountancy. 11th ed. India: Vikas Publishing House.

Morris, J.R. and Daley, J.P., (2017). Introduction to financial models for management and

planning. 2nd ed. Florida: CRC press.

Muller, M., (2011). Essentials of inventory management. 2nd ed. New York: AMACOM.

Periasamy, P. (2009). Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd

Sagner, J., (2010). Essentials of working capital management (Vol. 55). New Jersey: John

Wiley & Sons.

Saudagaran, S.M., (2009). International accounting: A user perspective. Chicago: CCH.

Shim, J.K., Siegel, J.G. and Shim, A.I., (2011). Budgeting basics and beyond 4th ed. New

Jersey: John Wiley & Sons.

Tracy, T. and Tracy, J.A., (2011). Cash flow for dummies. New Jersey: John Wiley & Sons.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., (2009). Managerial accounting: tools for

business decision making. 5th ed. USA: John Wiley & Sons.

Jury, T., (2012). Cash flow analysis and forecasting: the definitive guide to understanding and

using published cash flow data (Vol. 653). USA: John Wiley & Sons.

Maheshwari, S.N., Maheshwari, S.K. and Maheswari, S.K., (2013). An Introduction to

Accountancy. 11th ed. India: Vikas Publishing House.

Morris, J.R. and Daley, J.P., (2017). Introduction to financial models for management and

planning. 2nd ed. Florida: CRC press.

Muller, M., (2011). Essentials of inventory management. 2nd ed. New York: AMACOM.

Periasamy, P. (2009). Financial Management. 2nd ed. New Delhi: Tata McGraw-Hill

Education Pvt. Ltd

Sagner, J., (2010). Essentials of working capital management (Vol. 55). New Jersey: John

Wiley & Sons.

Saudagaran, S.M., (2009). International accounting: A user perspective. Chicago: CCH.

Shim, J.K., Siegel, J.G. and Shim, A.I., (2011). Budgeting basics and beyond 4th ed. New

Jersey: John Wiley & Sons.

Tracy, T. and Tracy, J.A., (2011). Cash flow for dummies. New Jersey: John Wiley & Sons.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., (2009). Managerial accounting: tools for

business decision making. 5th ed. USA: John Wiley & Sons.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.