Financial Analysis: Working Capital Policy Report of Barclays PLC

VerifiedAdded on 2019/12/28

|7

|1134

|77

Report

AI Summary

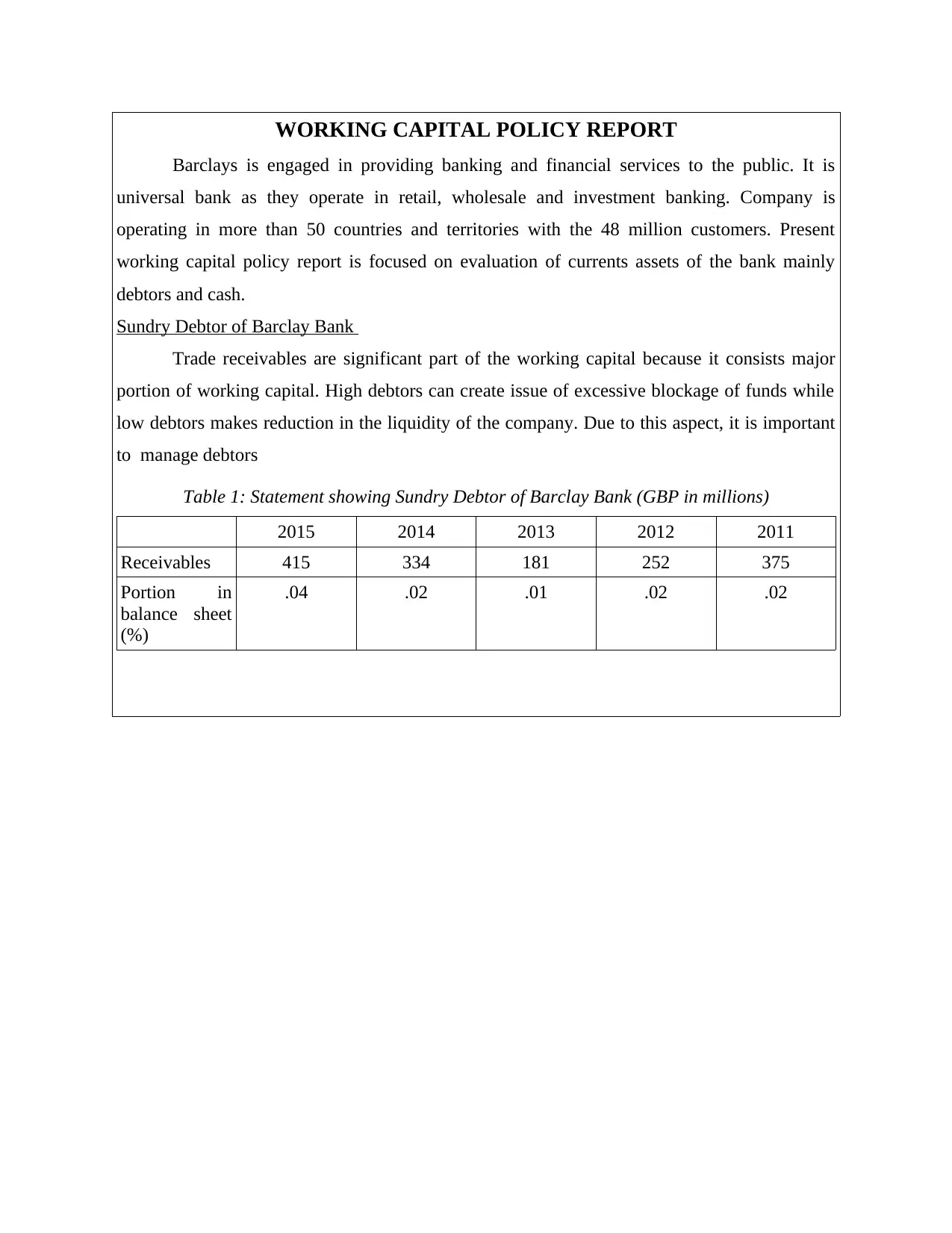

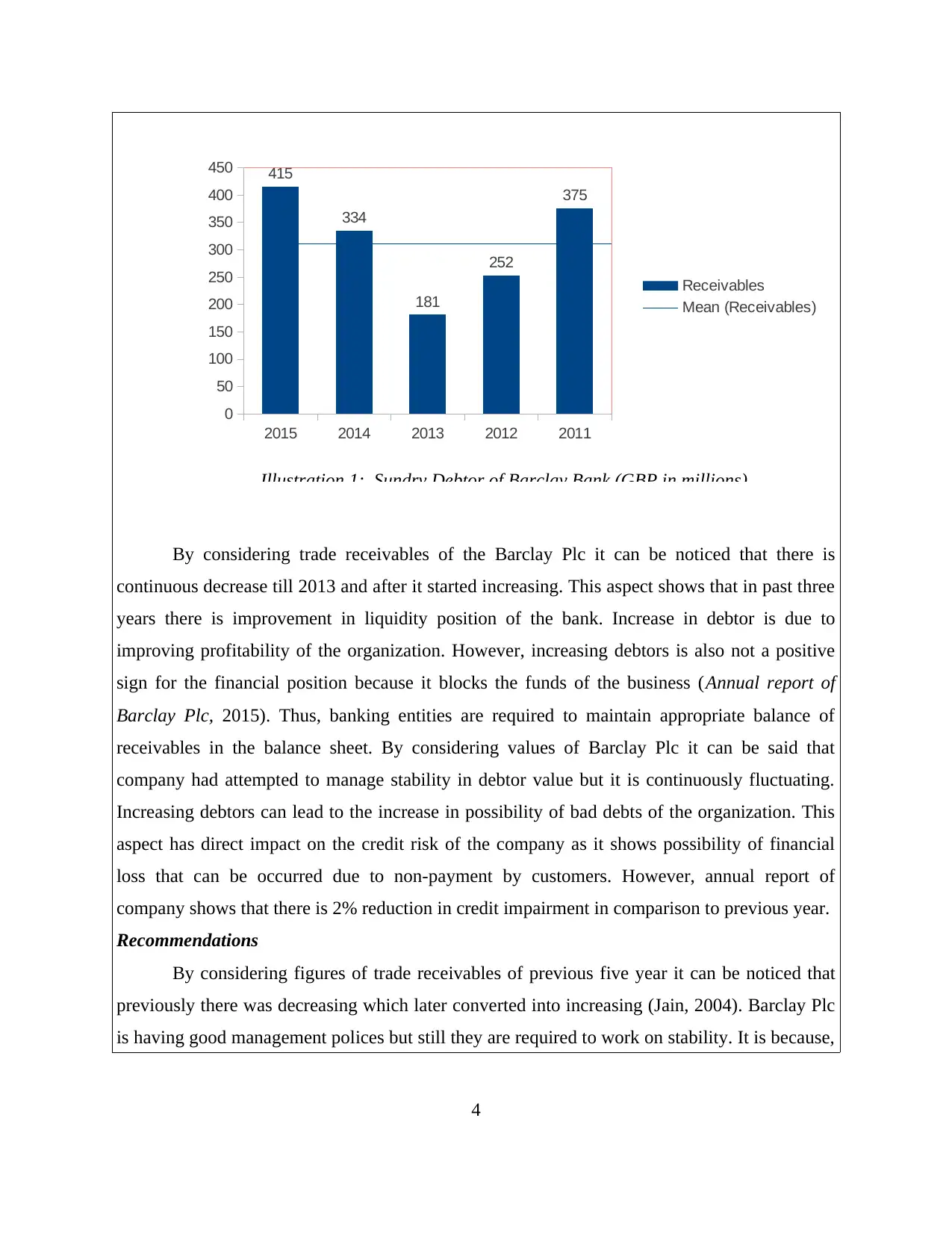

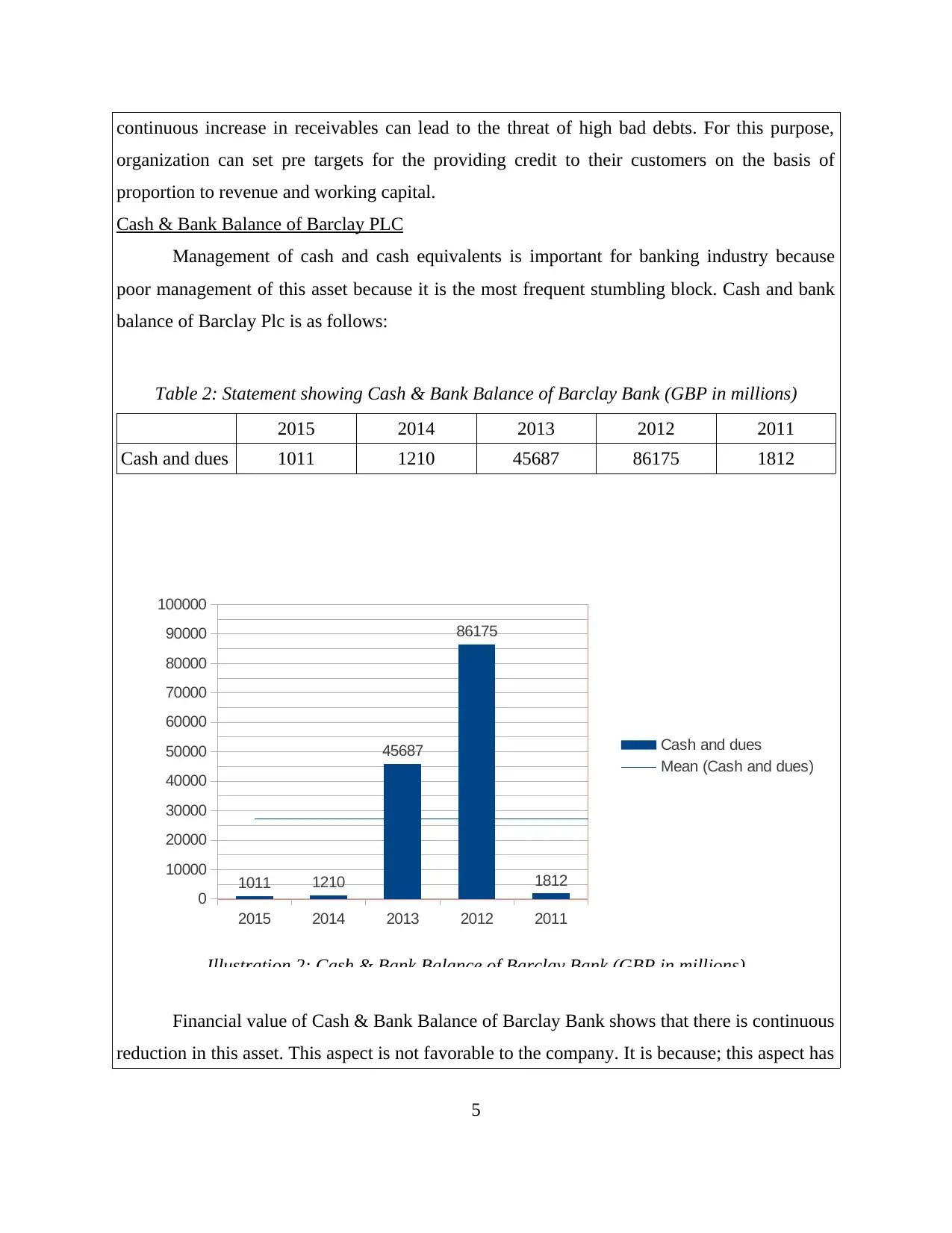

This report provides an analysis of Barclays Bank's working capital policy, focusing on the management of debtors (trade receivables) and cash & bank balances. The report examines the trends in receivables from 2011 to 2015, highlighting fluctuations and their implications on liquidity and credit risk. It also assesses the cash and bank balance trends, noting a continuous reduction and its potential adverse impacts on the company's quick ratio. The report provides recommendations for maintaining stability in financial values, balancing profitability with liquidity, and managing receivables to mitigate the risk of bad debts. The analysis is supported by data from Barclays' annual reports and other financial resources, offering insights into the bank's strategies and financial performance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.