Mortgage Broking Project: Finance Case Studies CIVMB_AS_v5A2

VerifiedAdded on 2023/01/07

|69

|19259

|1

Project

AI Summary

This written project, part of the Certificate IV in Finance and Mortgage Broking (CIVMB_AS_v5A2), presents a comprehensive analysis of mortgage broking practices through multiple case studies. It covers key aspects of the finance industry, including gathering and documenting client information, assessing client situations, exploring borrowing options, conducting reasonable inquiries, and understanding first home owner grants and home buyer assistance schemes. The project also delves into professional networks, loan settlement processes, interest rates, and establishing clients' financial knowledge. Furthermore, it addresses responsible lending obligations, self-employed considerations, advising on strategies, the impact of credit history, dispute resolution, effective file access, financial services legislation, and industry codes of practice. The project requires designing documents, applying principles of professional practice, and maintaining in-depth knowledge of financial products and services. The project is structured into multiple sections, each focusing on a different case study and a series of short-answer questions. The project aims to demonstrate competence in processing credit applications, preparing loan applications, identifying client needs, presenting broking options, complying with financial services legislation, applying principles of professional practice, developing in-depth knowledge of products and services, designing business documents, delivering and monitoring services, addressing customer needs, prospecting for new clients, and settling applications and loan arrangements.

Written Project

Certificate IV in Finance and Mortgage

Broking(CIVMB_AS_v5A2)

Student identification(student to complete)

Please complete the fields shaded grey.

Student number

Written projectoverall result (assessor to complete)

First submission Not yet demonstrated

Resubmission (if applicable) Not applicable

CIVMB_AS_v5A2

Certificate IV in Finance and Mortgage

Broking(CIVMB_AS_v5A2)

Student identification(student to complete)

Please complete the fields shaded grey.

Student number

Written projectoverall result (assessor to complete)

First submission Not yet demonstrated

Resubmission (if applicable) Not applicable

CIVMB_AS_v5A2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Result summary(assessor to complete)

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if required)

Task 1 — Key terms, gathering and documenting client information Not yet demonstrated Not applicable

Task 2 — Assessing the clients’ situation Not yet demonstrated Not applicable

Task 3 — Borrowing options Not yet demonstrated Not applicable

Task 4 — Reasonable enquiries Not yet demonstrated Not applicable

Task 5 — First Home Owners Grant and home buyer assistance schemes Not yet demonstrated Not applicable

Task 6 — Professional network and loan settlement process Not yet demonstrated Not applicable

Task 7 — Interest rates Not yet demonstrated Not applicable

Section 2: Case study 2 — Richard and Pauline Jackson

Task 8 — Establishing level of financial knowledge Not yet demonstrated Not applicable

Task 9 — Responsible lending obligations Not yet demonstrated Not applicable

Task 10 — Self-employed special considerations Not yet demonstrated Not applicable

Task 11 — Advising on strategies Not yet demonstrated Not applicable

Task 12 — Impact of credit history Not yet demonstrated Not applicable

Task 13 — Dispute resolution Not yet demonstrated Not applicable

Task 14 — Effective access to files Not yet demonstrated Not applicable

Section 3: Case study 3 — Mary Jane Smith

Task 15 — Prepare and check a loan application Not yet demonstrated Not applicable

Section 4: Working in financial services

Task 16 — Financial services legislation and industry codes of practice Not yet demonstrated Not applicable

Task 17 — Design a document Not yet demonstrated Not applicable

Task 18 — Applying principles of professional practice to work in the financial

services industry Not yet demonstrated Not applicable

Task 19 — Develop and maintain in-depth knowledge of products and

services used by an organisation Not yet demonstrated Not applicable

Please note:To pass this written project, you will need to be assessed as DEMONSTRATED in either your

first submission or your resubmission in all tasksabove.

Task feedback

Please refer to the assessor’s detailed feedback found at the end of each task so that you know what to do

for any tasks you need to resubmit.

Page 2 of 69

Section 1: Case study 1 — Philip and Jennifer Brown First submission Resubmission (if required)

Task 1 — Key terms, gathering and documenting client information Not yet demonstrated Not applicable

Task 2 — Assessing the clients’ situation Not yet demonstrated Not applicable

Task 3 — Borrowing options Not yet demonstrated Not applicable

Task 4 — Reasonable enquiries Not yet demonstrated Not applicable

Task 5 — First Home Owners Grant and home buyer assistance schemes Not yet demonstrated Not applicable

Task 6 — Professional network and loan settlement process Not yet demonstrated Not applicable

Task 7 — Interest rates Not yet demonstrated Not applicable

Section 2: Case study 2 — Richard and Pauline Jackson

Task 8 — Establishing level of financial knowledge Not yet demonstrated Not applicable

Task 9 — Responsible lending obligations Not yet demonstrated Not applicable

Task 10 — Self-employed special considerations Not yet demonstrated Not applicable

Task 11 — Advising on strategies Not yet demonstrated Not applicable

Task 12 — Impact of credit history Not yet demonstrated Not applicable

Task 13 — Dispute resolution Not yet demonstrated Not applicable

Task 14 — Effective access to files Not yet demonstrated Not applicable

Section 3: Case study 3 — Mary Jane Smith

Task 15 — Prepare and check a loan application Not yet demonstrated Not applicable

Section 4: Working in financial services

Task 16 — Financial services legislation and industry codes of practice Not yet demonstrated Not applicable

Task 17 — Design a document Not yet demonstrated Not applicable

Task 18 — Applying principles of professional practice to work in the financial

services industry Not yet demonstrated Not applicable

Task 19 — Develop and maintain in-depth knowledge of products and

services used by an organisation Not yet demonstrated Not applicable

Please note:To pass this written project, you will need to be assessed as DEMONSTRATED in either your

first submission or your resubmission in all tasksabove.

Task feedback

Please refer to the assessor’s detailed feedback found at the end of each task so that you know what to do

for any tasks you need to resubmit.

Page 2 of 69

Before you begin

Read everything in this document before you start your written projectforCertificate IV in Finance and

Mortgage Broking (CIVMB_ASMG_v5A2).

About this document

This document is the written project— half of the overall Written and Oral Project.

This document includes the following parts:

• Instructions for completing and submitting this project

• Section 1: Case study 1 — Philip and Jennifer Brown

A case study with a series of short-answer questions:

– Task 1 — Key terms, gathering and documenting client information

– Task 2 — Assessing the clients’ situation

– Task 3 — Borrowing options

– Task 4 — Reasonable enquiries

– Task 5 — First Home Owners Grant and home buyer assistance schemes

– Task 6 —Professional network and loan settlement process

– Task 7 — Interest rates

• Section 2: Case study 2 — Richard and Pauline Jackson

A case study and a series of short-answer questions:

– Task 8 — Establishing level of financial knowledge

– Task 9 — Responsible lending obligations

– Task 10 — Self-employed special considerations

– Task 11 — Advising on strategies

– Task 12 — Impact of credit history

– Task 13 — Dispute resolution

– Task 14 — Effective access to files

• Section 3: Case study 3 — Mary Jane Smith

A case study and a series of short-answer questions:

– Task 15 — Prepare and check a loan application

• Section 4:Working in financial services

– Task 16 — Financial services legislation and industry codes of practice

– Task 17 — Design a document

– Task 18 — Applying principles of professional practice to work in the financial services industry

– Task 19 — Develop and maintain in depth knowledge of products and services used by an

organisation

• Appendix 1:Key terms

• Appendix 2: Client information collection tool/Fact finder

• Appendix 3:Loan application.

Page 3 of 69

Read everything in this document before you start your written projectforCertificate IV in Finance and

Mortgage Broking (CIVMB_ASMG_v5A2).

About this document

This document is the written project— half of the overall Written and Oral Project.

This document includes the following parts:

• Instructions for completing and submitting this project

• Section 1: Case study 1 — Philip and Jennifer Brown

A case study with a series of short-answer questions:

– Task 1 — Key terms, gathering and documenting client information

– Task 2 — Assessing the clients’ situation

– Task 3 — Borrowing options

– Task 4 — Reasonable enquiries

– Task 5 — First Home Owners Grant and home buyer assistance schemes

– Task 6 —Professional network and loan settlement process

– Task 7 — Interest rates

• Section 2: Case study 2 — Richard and Pauline Jackson

A case study and a series of short-answer questions:

– Task 8 — Establishing level of financial knowledge

– Task 9 — Responsible lending obligations

– Task 10 — Self-employed special considerations

– Task 11 — Advising on strategies

– Task 12 — Impact of credit history

– Task 13 — Dispute resolution

– Task 14 — Effective access to files

• Section 3: Case study 3 — Mary Jane Smith

A case study and a series of short-answer questions:

– Task 15 — Prepare and check a loan application

• Section 4:Working in financial services

– Task 16 — Financial services legislation and industry codes of practice

– Task 17 — Design a document

– Task 18 — Applying principles of professional practice to work in the financial services industry

– Task 19 — Develop and maintain in depth knowledge of products and services used by an

organisation

• Appendix 1:Key terms

• Appendix 2: Client information collection tool/Fact finder

• Appendix 3:Loan application.

Page 3 of 69

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the written project within your enrolment period. Your study plan is in the KapLearn Certificate IV in

Finance and Mortgage Broking (CIVMBv5) subject room.

Instructions for completing and submitting the

written project

Completing the written project

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these projects.

• Name your file as follows: Studentnumber_SubjectCode_Project_versionnumber_Submissionnumber

(e.g. 12345678_CIVMB_AS_v5A2_Submission1).

• Include your student ID on the first page of the project.

Before you submit your work, please do a spell check and proofread your work to ensure that everything

is clear and unambiguous.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the ‘Client information collection tool’in Appendix 2, assumptions are permitted,

although they must not be in conflict with the information provided in the Case study.

Throughout the project you will also be required to research additional information from other

organisations in the finance industry to find the right products or services to meet your client’s

requirements or to calculate any service fees that may be applicable.

Page 4 of 69

We recommend that you use the study plan for this subject to help you manage your time to complete

the written project within your enrolment period. Your study plan is in the KapLearn Certificate IV in

Finance and Mortgage Broking (CIVMBv5) subject room.

Instructions for completing and submitting the

written project

Completing the written project

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these projects.

• Name your file as follows: Studentnumber_SubjectCode_Project_versionnumber_Submissionnumber

(e.g. 12345678_CIVMB_AS_v5A2_Submission1).

• Include your student ID on the first page of the project.

Before you submit your work, please do a spell check and proofread your work to ensure that everything

is clear and unambiguous.

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

When completing the ‘Client information collection tool’in Appendix 2, assumptions are permitted,

although they must not be in conflict with the information provided in the Case study.

Throughout the project you will also be required to research additional information from other

organisations in the finance industry to find the right products or services to meet your client’s

requirements or to calculate any service fees that may be applicable.

Page 4 of 69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Submitting the writtenproject

Only Microsoft Office compatible written projects submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed project as a PDF.

The written project must be completed before submitting it to Kaplan Professional Education.

Incomplete written projects will be returned to you unmarked. The written project must be submitted

together with the oral project. If you do not submit both completed projects at the one time it will be

returned to you unmarked.

The maximum file size is 20MB for the written and oral project. Once you submit your written project for

marking you will be unable to make any further changes to it.

Once you submit your written project for marking you will be unable to make any further changes to it.

You are able to submit bothprojects earlier than the deadline if you are confident you have completed all

parts and have prepared a quality submission.

Please refer to the Project submission/resubmission videos in the Assessment section of KapLearn under

your ‘Project Enrolment’ for details on how to submit/resubmit your written project.

Your Written Project and Oral Project must be submitted together on or before your due date. Please

check KapLearn for the due date.

The written project marking process

You have 26 weeks from the date of your enrolment in this subject to submit your completed project.

If you reach the end of your initial enrolment period and have been deemed ‘Not yet demonstrated’ in one

or more assessment items, then an additional four (4) weeks will be granted, provided you attempted all

assessment tasks during the initial enrolment period.

Your assessor will mark your written and oral project and return it to you in the Certificate IV in Finance and

Mortgage Broking (CIVMBv5) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written project. Failure to do so will mean that your project will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completedwritten and oral project.

How your written project is graded

Project tasks are used to determine your ‘competence’ in demonstrating the required knowledge and/or

skills for each subject. As a result, you will be graded as either Demonstrated or Not yet demonstrated.

Page 5 of 69

Only Microsoft Office compatible written projects submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed project as a PDF.

The written project must be completed before submitting it to Kaplan Professional Education.

Incomplete written projects will be returned to you unmarked. The written project must be submitted

together with the oral project. If you do not submit both completed projects at the one time it will be

returned to you unmarked.

The maximum file size is 20MB for the written and oral project. Once you submit your written project for

marking you will be unable to make any further changes to it.

Once you submit your written project for marking you will be unable to make any further changes to it.

You are able to submit bothprojects earlier than the deadline if you are confident you have completed all

parts and have prepared a quality submission.

Please refer to the Project submission/resubmission videos in the Assessment section of KapLearn under

your ‘Project Enrolment’ for details on how to submit/resubmit your written project.

Your Written Project and Oral Project must be submitted together on or before your due date. Please

check KapLearn for the due date.

The written project marking process

You have 26 weeks from the date of your enrolment in this subject to submit your completed project.

If you reach the end of your initial enrolment period and have been deemed ‘Not yet demonstrated’ in one

or more assessment items, then an additional four (4) weeks will be granted, provided you attempted all

assessment tasks during the initial enrolment period.

Your assessor will mark your written and oral project and return it to you in the Certificate IV in Finance and

Mortgage Broking (CIVMBv5) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written project. Failure to do so will mean that your project will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completedwritten and oral project.

How your written project is graded

Project tasks are used to determine your ‘competence’ in demonstrating the required knowledge and/or

skills for each subject. As a result, you will be graded as either Demonstrated or Not yet demonstrated.

Page 5 of 69

Your assessor will follow the below process when marking your project:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed to be demonstrated in all assessment items in order to be awarded the units

of competency in this subject, including:

• all of the exam questions

• the written and oral project.

‘Not yet demonstrated’and resubmissions

Should sections of your project be marked as ‘not yet demonstrated’you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet demonstrated’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your project, so your second assessor can see the instructions that were originally

provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written project is your opportunity to demonstrate your competency against these units:

FNSCRD301 Process applications for credit

FNSFMB401 Prepare a loan application on behalf of finance or mortgage broking clients

FNSFMB402 Identify client needs for broking services

FNSFMB403 Present broking options to client

FNSFMK505 Comply with financial services legislation and industry codes of practice

FNSINC401 Apply principles of professional practice to work in the financial services industry

FNSINC402 Develop and maintain in-depth knowledge of products and services used by an organisation or sector

BSBITU306 Design and produce business documents

BSBCUS301 Deliver and monitor a services to customers

BSBCUS402 Address customer needs

FNSSAM403 Prospect for new clients

FNSFMB501 Settle applications and loan arrangements in the finance and mortgage broking industry

Note that the written and oral project is one of two assessments required to meet the requirements of the

units of competency.

We are here to help

If you have any questions about this written project you can post your query at the ‘Ask your Tutor’ forum

in your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 69

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed to be demonstrated in all assessment items in order to be awarded the units

of competency in this subject, including:

• all of the exam questions

• the written and oral project.

‘Not yet demonstrated’and resubmissions

Should sections of your project be marked as ‘not yet demonstrated’you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet demonstrated’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your project, so your second assessor can see the instructions that were originally

provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written project is your opportunity to demonstrate your competency against these units:

FNSCRD301 Process applications for credit

FNSFMB401 Prepare a loan application on behalf of finance or mortgage broking clients

FNSFMB402 Identify client needs for broking services

FNSFMB403 Present broking options to client

FNSFMK505 Comply with financial services legislation and industry codes of practice

FNSINC401 Apply principles of professional practice to work in the financial services industry

FNSINC402 Develop and maintain in-depth knowledge of products and services used by an organisation or sector

BSBITU306 Design and produce business documents

BSBCUS301 Deliver and monitor a services to customers

BSBCUS402 Address customer needs

FNSSAM403 Prospect for new clients

FNSFMB501 Settle applications and loan arrangements in the finance and mortgage broking industry

Note that the written and oral project is one of two assessments required to meet the requirements of the

units of competency.

We are here to help

If you have any questions about this written project you can post your query at the ‘Ask your Tutor’ forum

in your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 6 of 69

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 1: Case study 1 — Philip and Jennifer Brown

Background

Philip and Jennifer Brown are a young couple about to buy their first home. They have been married for

five years and during that time have rented an apartment while saving for their own home.

Following a personal referral from Glenn Brown, Philip’s brother you have already had a first meeting with

Philip and Jennifer to discuss their objectives and needs. They admitted they have little time to do much

research of lenders, have limited knowledge of the loan products available and have approached you to

guide them through the process as they are confused.

During (and subsequent) to your first meeting, Philip and Jennifer have provided the basic information

documents — pay slips, tax returns, bank statements, property details for review/verification. You have

now undertaken your preliminary assessment and need to discuss and present to them the proposal

covering the options and your recommendations. It is important to get the proposal moving quickly,

as the agent has indicated other parties are interested in the property.

They have been looking at properties for the past three months and have found a 10 year old established

apartment that has really caught their eye, although they have some concern over the kitchen which

requires some minor renovations.

They have not paid a deposit at this stage, but the Real Estate Agent has provided some guidance on

additional fees and charges.

Following is a summary of the details of the property they wish to purchase, the couple’s financial and

employment details, and the loan features they require.

The property

Address Unit 1, 92 Seaside Lane Edgartown (Your state)

Purchase price $490,000

Description 2 bedroom, 2 bathroom Strata Title apartment

Agent details Stephanie Jones

Phone 8123 1113

Mobile 0412 880 088

The couple

Current address Unit 12, 22 Wentworth Lane, Highville, (Your state)

Philip and Jennifer have lived there since March 2012

Home phone 9123 2121

Page 7 of 69

Background

Philip and Jennifer Brown are a young couple about to buy their first home. They have been married for

five years and during that time have rented an apartment while saving for their own home.

Following a personal referral from Glenn Brown, Philip’s brother you have already had a first meeting with

Philip and Jennifer to discuss their objectives and needs. They admitted they have little time to do much

research of lenders, have limited knowledge of the loan products available and have approached you to

guide them through the process as they are confused.

During (and subsequent) to your first meeting, Philip and Jennifer have provided the basic information

documents — pay slips, tax returns, bank statements, property details for review/verification. You have

now undertaken your preliminary assessment and need to discuss and present to them the proposal

covering the options and your recommendations. It is important to get the proposal moving quickly,

as the agent has indicated other parties are interested in the property.

They have been looking at properties for the past three months and have found a 10 year old established

apartment that has really caught their eye, although they have some concern over the kitchen which

requires some minor renovations.

They have not paid a deposit at this stage, but the Real Estate Agent has provided some guidance on

additional fees and charges.

Following is a summary of the details of the property they wish to purchase, the couple’s financial and

employment details, and the loan features they require.

The property

Address Unit 1, 92 Seaside Lane Edgartown (Your state)

Purchase price $490,000

Description 2 bedroom, 2 bathroom Strata Title apartment

Agent details Stephanie Jones

Phone 8123 1113

Mobile 0412 880 088

The couple

Current address Unit 12, 22 Wentworth Lane, Highville, (Your state)

Philip and Jennifer have lived there since March 2012

Home phone 9123 2121

Page 7 of 69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

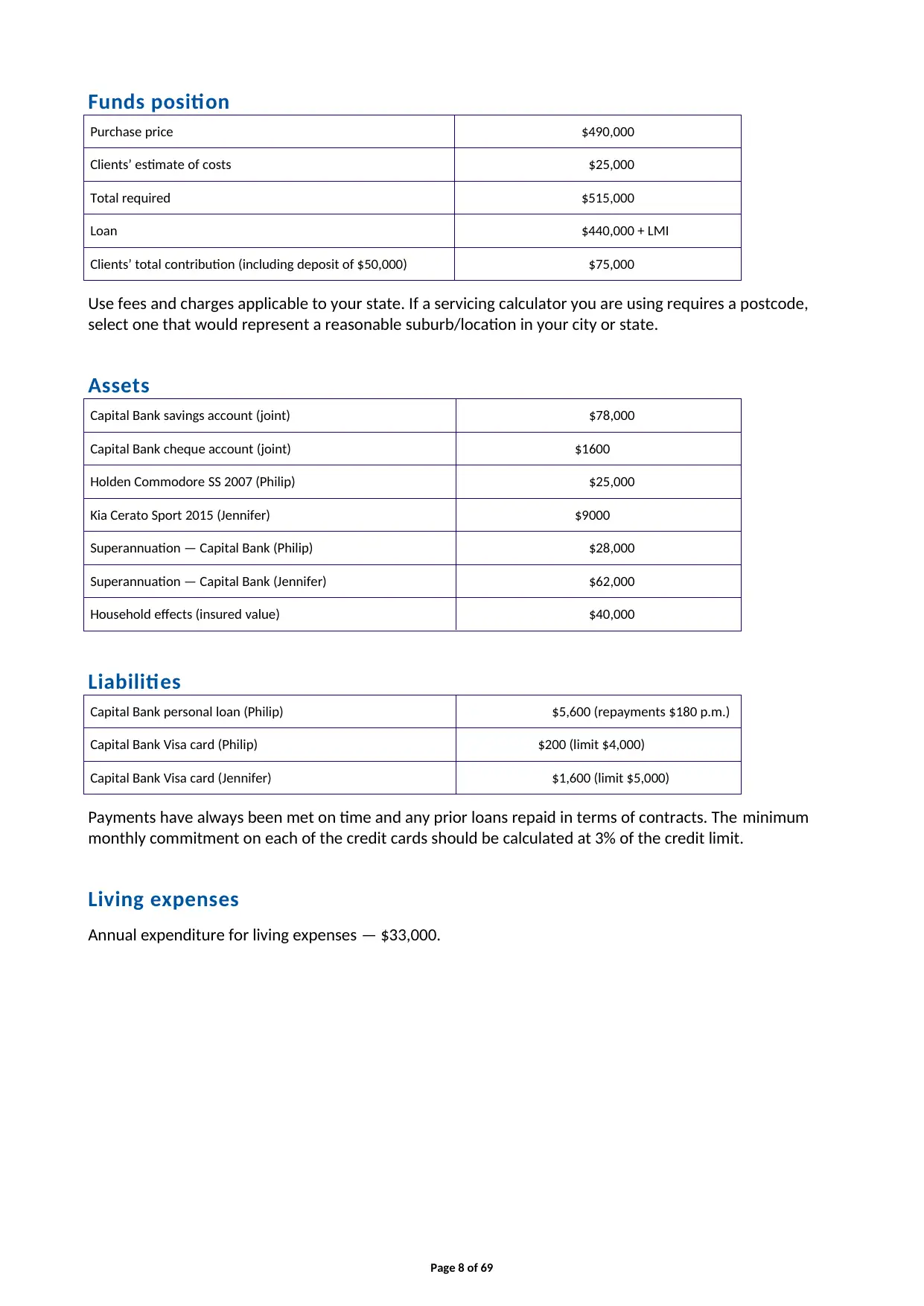

Funds position

Purchase price $490,000

Clients’ estimate of costs $25,000

Total required $515,000

Loan $440,000 + LMI

Clients’ total contribution (including deposit of $50,000) $75,000

Use fees and charges applicable to your state. If a servicing calculator you are using requires a postcode,

select one that would represent a reasonable suburb/location in your city or state.

Assets

Capital Bank savings account (joint) $78,000

Capital Bank cheque account (joint) $1600

Holden Commodore SS 2007 (Philip) $25,000

Kia Cerato Sport 2015 (Jennifer) $9000

Superannuation — Capital Bank (Philip) $28,000

Superannuation — Capital Bank (Jennifer) $62,000

Household effects (insured value) $40,000

Liabilities

Capital Bank personal loan (Philip) $5,600 (repayments $180 p.m.)

Capital Bank Visa card (Philip) $200 (limit $4,000)

Capital Bank Visa card (Jennifer) $1,600 (limit $5,000)

Payments have always been met on time and any prior loans repaid in terms of contracts. The minimum

monthly commitment on each of the credit cards should be calculated at 3% of the credit limit.

Living expenses

Annual expenditure for living expenses — $33,000.

Page 8 of 69

Purchase price $490,000

Clients’ estimate of costs $25,000

Total required $515,000

Loan $440,000 + LMI

Clients’ total contribution (including deposit of $50,000) $75,000

Use fees and charges applicable to your state. If a servicing calculator you are using requires a postcode,

select one that would represent a reasonable suburb/location in your city or state.

Assets

Capital Bank savings account (joint) $78,000

Capital Bank cheque account (joint) $1600

Holden Commodore SS 2007 (Philip) $25,000

Kia Cerato Sport 2015 (Jennifer) $9000

Superannuation — Capital Bank (Philip) $28,000

Superannuation — Capital Bank (Jennifer) $62,000

Household effects (insured value) $40,000

Liabilities

Capital Bank personal loan (Philip) $5,600 (repayments $180 p.m.)

Capital Bank Visa card (Philip) $200 (limit $4,000)

Capital Bank Visa card (Jennifer) $1,600 (limit $5,000)

Payments have always been met on time and any prior loans repaid in terms of contracts. The minimum

monthly commitment on each of the credit cards should be calculated at 3% of the credit limit.

Living expenses

Annual expenditure for living expenses — $33,000.

Page 8 of 69

Employment and income

Philip (date of birth 21/2/87)

Position Team Leader (full time)

Employer ACE Limited 101 City Rd, Westside (Your state)

Phone 9800 1111

Income (gross) $58,000 p.a. monthly gross income: $4,833

Employer contact Dwayne Johnson, HR Manager

Length of service Since October 2005

Driver’s licence 8855KL

Email philipb@ace.com.au

Jennifer (date of birth 8/10/88)

Position Accountant (full time)

Employer Tech city 804 High Street, City East (Your state)

Phone 9910 2033

Income (gross) $95,000 p.a. monthly gross income: $7,917

Employer contact Bruce Wayne, HR Manager

Length of service Since March 2006

Driver’s licence 17016C

Email jbrown@techcity.com.au

Solicitor’s details

Jones and Co

22 High Street, City East (Your state)

Phone: 82811382

Email: jonesandco.net.au

The solicitor has quoted a fee of $1,500 for the conveyance.

Page 9 of 69

Philip (date of birth 21/2/87)

Position Team Leader (full time)

Employer ACE Limited 101 City Rd, Westside (Your state)

Phone 9800 1111

Income (gross) $58,000 p.a. monthly gross income: $4,833

Employer contact Dwayne Johnson, HR Manager

Length of service Since October 2005

Driver’s licence 8855KL

Email philipb@ace.com.au

Jennifer (date of birth 8/10/88)

Position Accountant (full time)

Employer Tech city 804 High Street, City East (Your state)

Phone 9910 2033

Income (gross) $95,000 p.a. monthly gross income: $7,917

Employer contact Bruce Wayne, HR Manager

Length of service Since March 2006

Driver’s licence 17016C

Email jbrown@techcity.com.au

Solicitor’s details

Jones and Co

22 High Street, City East (Your state)

Phone: 82811382

Email: jonesandco.net.au

The solicitor has quoted a fee of $1,500 for the conveyance.

Page 9 of 69

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The loan requirements

• 30 year term

• premium option home loan features

• variable interest rate (for this case use 4.5%p.a.)

• LMI to be capitalised

• proposed settlement date — six weeks from exchange of contracts

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• funds access via card.

Note: Loan application fee is waived under Special Offer.

Other information

• They have advised that the Real Estate Agents have indicated they need to make a formal offer within

the next 10 days, however they are reluctant to do so until they obtain an approval.

• Jennifer has asked if there are any professional package benefits available because she is an accountant.

However, she did confirm she has not maintained her continuing professional development.

• Jennifer previously owned and lived in an apartment with her two older sisters when they attended

university but they sold this before she married — they did not make a lot from sale.

• Family plans are five years away.

• They do have plans to take a major overseas trip before family comes along.

• Philip is hoping for a promotion within the next 12 months upon possible retirement of a long-term

employee where he works.

They have also expressed a concern about the possibility of interest rates increasing.

Page 10 of 69

• 30 year term

• premium option home loan features

• variable interest rate (for this case use 4.5%p.a.)

• LMI to be capitalised

• proposed settlement date — six weeks from exchange of contracts

• ability to make additional payments from time to time without penalty

• fortnightly repayment option

• redraw facility

• funds access via card.

Note: Loan application fee is waived under Special Offer.

Other information

• They have advised that the Real Estate Agents have indicated they need to make a formal offer within

the next 10 days, however they are reluctant to do so until they obtain an approval.

• Jennifer has asked if there are any professional package benefits available because she is an accountant.

However, she did confirm she has not maintained her continuing professional development.

• Jennifer previously owned and lived in an apartment with her two older sisters when they attended

university but they sold this before she married — they did not make a lot from sale.

• Family plans are five years away.

• They do have plans to take a major overseas trip before family comes along.

• Philip is hoping for a promotion within the next 12 months upon possible retirement of a long-term

employee where he works.

They have also expressed a concern about the possibility of interest rates increasing.

Page 10 of 69

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Project tasks (student to complete)

Task 1 —Key terms,gathering and documenting client information

1. Complete the ‘Key terms’ (located at the end of the written project inAppendix 1).

2. Using the information provided in Case study 1, complete the ‘Client information collection

tool’(located at the end of the written project in Appendix 2).

3. You will also need to complete the Genworth Serviceability Calculator to assess the security,

debt service and borrowing capacity for Jennifer and Phillip Brown. To do this, follow these steps:

(a) Use the details in Case study 1.

(b) Read the Genworth Calculator Supplementary Material Guide available in the Kaplearn

CIVMBv5 subject room.

(c) Process the loan application using the Genworth Serviceability Calculator accessible here:

<https://www.genworth.com.au/lenders/lmi-tools/serviceability-calculator>.

(d) Once you have processed it, download a copy of the PDF and save it to your desktop.

Note:You will need to upload a copy of this pdf with your written and oral project submission. This will

assist your assessor with providing feedback on your written and oral project submission.

Note: Any assumptions you make should be listed and should not be in conflict with the case study

information already provided.

Assessor feedback for Task 1 — Key terms, gathering and documenting client information

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 11 of 69

Task 1 —Key terms,gathering and documenting client information

1. Complete the ‘Key terms’ (located at the end of the written project inAppendix 1).

2. Using the information provided in Case study 1, complete the ‘Client information collection

tool’(located at the end of the written project in Appendix 2).

3. You will also need to complete the Genworth Serviceability Calculator to assess the security,

debt service and borrowing capacity for Jennifer and Phillip Brown. To do this, follow these steps:

(a) Use the details in Case study 1.

(b) Read the Genworth Calculator Supplementary Material Guide available in the Kaplearn

CIVMBv5 subject room.

(c) Process the loan application using the Genworth Serviceability Calculator accessible here:

<https://www.genworth.com.au/lenders/lmi-tools/serviceability-calculator>.

(d) Once you have processed it, download a copy of the PDF and save it to your desktop.

Note:You will need to upload a copy of this pdf with your written and oral project submission. This will

assist your assessor with providing feedback on your written and oral project submission.

Note: Any assumptions you make should be listed and should not be in conflict with the case study

information already provided.

Assessor feedback for Task 1 — Key terms, gathering and documenting client information

(Insert Feedback)

Question(s) that need to be resubmitted (if required) (List question numbers)

First submission Not yet demonstrated

Resubmission (if required) Not applicable

Page 11 of 69

Task 2 — Assessing the clients’ situation

1. Based on the information provided in the case study and any other online tools used, you now need

to assess the clients’ loan application paying particular attention that you have met legislative

requirements, followed industry codes of practice and met lender credit policy.

Comment on issues such as:

• does it appear to meet legislative requirements (e.g. NCCP)

• maximum borrowing capacity of client

• capacity to meet deposit and total cash contribution for the loan required

• repayment requirements based on the loan required

• what the security will be and if it is appropriate

• do Jennifer and Phillip require Lenders Mortgage Insurance (LMI), and if so, how much will it cost and

what are the options to pay the fee

• what loan amount would you recommend, and why

• likelihood that the clients will be able to meet all their financial obligations

• do Jennifer and Philip qualify for concessions on any of the fees and charges

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Note:The assessment of the clients’ needs is a critical prelude to you completing Part 4 of the

Oral project requirement for this course.

Student response to Task 2: Question 1

Answer here

Meeting Legislative requirements

Yes the clients have the requirements of NCCP as well as consumer credit code regulations. Couple has

good credit score which could be identified from the records of couple maintained with the bank they have

not made in default in the repayments of loan and credit card payments. The compliance requirement

regarding the consumer credit has been by the lender Capital banks. The complete details about the clients,

employment, contact details, property to be purchased and the broker has been provided. The application

have met all the legislative requirements before processing the loan further.

Maximum borrowing capacity of client

Maximum borrowing capacity of the clients is measured using borrowing power calculator that

assesses the earning capacity of the clients, dependants, existing and proposed loan and term of maturity.

As per the current earning capacity and proposed loan they could borrow up to $1,474,000. The borrowing

capacity of the clients is very high where the loan borrowed is less. Clients will pass the requirement for

passing the loan application based on borrowing capacity and credit score of the couple jointly

Capacity to meet deposit and total cash contribution for the loan required

Philip and Jennifer have been saving from many years and living in rented premised for purchasing

own home. They have cash saving in the savings account with capital bank. Also the total cash contribution

of $ 75000 could be met from that savings only. They are also having balance in superannuation account

which could also be used in case of need. They have surplus funds for meeting the deposits and cash

contributions for the loan.

Repayment requirements based on the loan required

Clients have applied for the home loan for purchasing new House. The loan amount applied is

$440,000. The clients want repayment over loan on fortnight basis so that they are not burdened with

single monthly payments for loan. The clients are also desirous of redraw facility so that they could make

additional payment for setting off the loan as soon as possible. The loan applied from the bank could

Page 12 of 69

1. Based on the information provided in the case study and any other online tools used, you now need

to assess the clients’ loan application paying particular attention that you have met legislative

requirements, followed industry codes of practice and met lender credit policy.

Comment on issues such as:

• does it appear to meet legislative requirements (e.g. NCCP)

• maximum borrowing capacity of client

• capacity to meet deposit and total cash contribution for the loan required

• repayment requirements based on the loan required

• what the security will be and if it is appropriate

• do Jennifer and Phillip require Lenders Mortgage Insurance (LMI), and if so, how much will it cost and

what are the options to pay the fee

• what loan amount would you recommend, and why

• likelihood that the clients will be able to meet all their financial obligations

• do Jennifer and Philip qualify for concessions on any of the fees and charges

• any other issues that may impact, now or in the future, on the clients’ ability to meet their

obligations, including any possible risks.

Provide data to support your comments and conclusions. (750 words)

Note:The assessment of the clients’ needs is a critical prelude to you completing Part 4 of the

Oral project requirement for this course.

Student response to Task 2: Question 1

Answer here

Meeting Legislative requirements

Yes the clients have the requirements of NCCP as well as consumer credit code regulations. Couple has

good credit score which could be identified from the records of couple maintained with the bank they have

not made in default in the repayments of loan and credit card payments. The compliance requirement

regarding the consumer credit has been by the lender Capital banks. The complete details about the clients,

employment, contact details, property to be purchased and the broker has been provided. The application

have met all the legislative requirements before processing the loan further.

Maximum borrowing capacity of client

Maximum borrowing capacity of the clients is measured using borrowing power calculator that

assesses the earning capacity of the clients, dependants, existing and proposed loan and term of maturity.

As per the current earning capacity and proposed loan they could borrow up to $1,474,000. The borrowing

capacity of the clients is very high where the loan borrowed is less. Clients will pass the requirement for

passing the loan application based on borrowing capacity and credit score of the couple jointly

Capacity to meet deposit and total cash contribution for the loan required

Philip and Jennifer have been saving from many years and living in rented premised for purchasing

own home. They have cash saving in the savings account with capital bank. Also the total cash contribution

of $ 75000 could be met from that savings only. They are also having balance in superannuation account

which could also be used in case of need. They have surplus funds for meeting the deposits and cash

contributions for the loan.

Repayment requirements based on the loan required

Clients have applied for the home loan for purchasing new House. The loan amount applied is

$440,000. The clients want repayment over loan on fortnight basis so that they are not burdened with

single monthly payments for loan. The clients are also desirous of redraw facility so that they could make

additional payment for setting off the loan as soon as possible. The loan applied from the bank could

Page 12 of 69

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 69

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.