Analysis of Yield Curve and Share Prices of AMP and Qantas

VerifiedAdded on 2023/06/05

|11

|1444

|217

AI Summary

This report analyzes the past performance and future prospects of AMP and Qantas shares based on yield curve and share prices analysis. It includes an analysis of the yield curve, monthly returns, beta, and CAPM model. The report also provides an overview of the companies and their current market conditions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Question 1

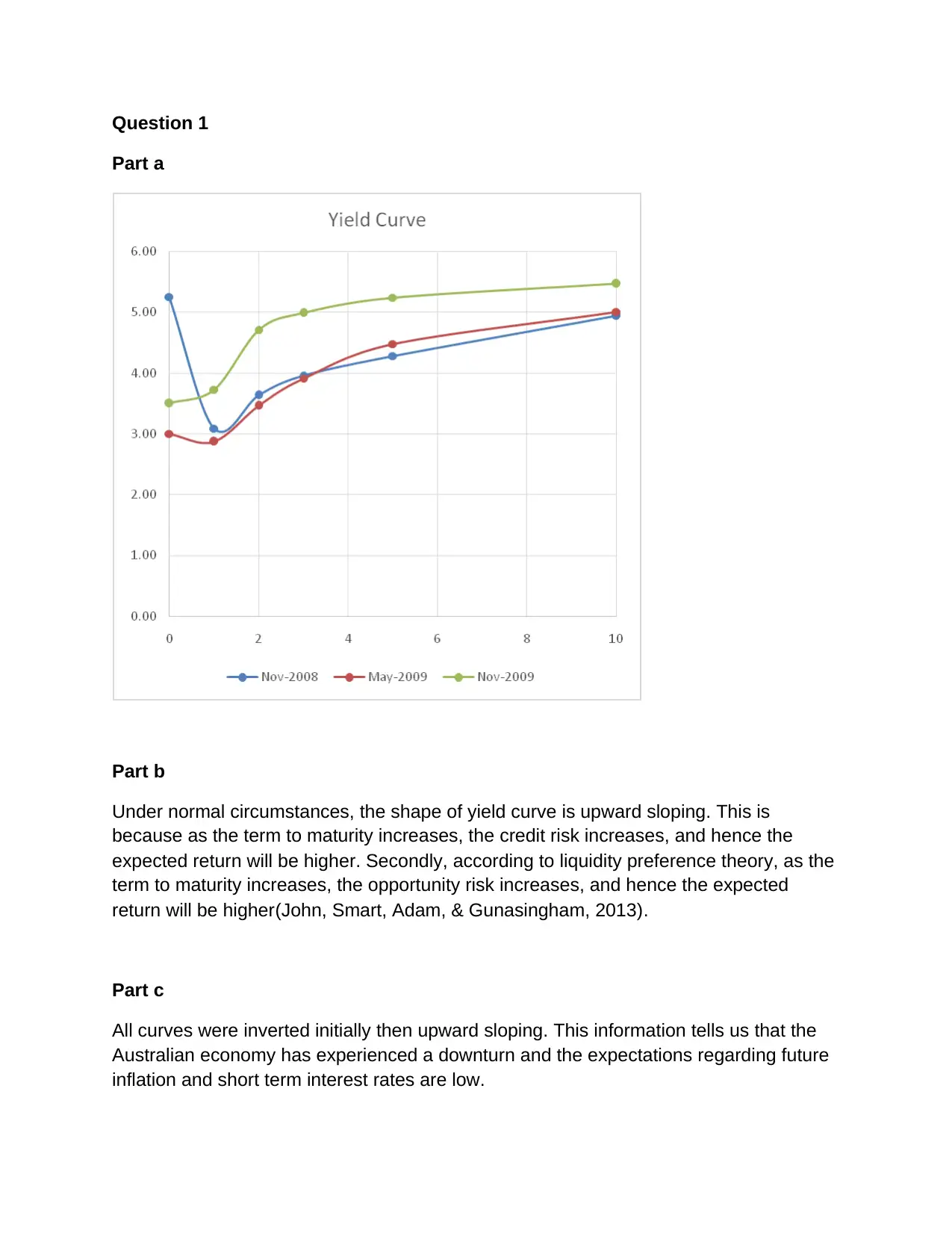

Part a

Part b

Under normal circumstances, the shape of yield curve is upward sloping. This is

because as the term to maturity increases, the credit risk increases, and hence the

expected return will be higher. Secondly, according to liquidity preference theory, as the

term to maturity increases, the opportunity risk increases, and hence the expected

return will be higher(John, Smart, Adam, & Gunasingham, 2013).

Part c

All curves were inverted initially then upward sloping. This information tells us that the

Australian economy has experienced a downturn and the expectations regarding future

inflation and short term interest rates are low.

Part a

Part b

Under normal circumstances, the shape of yield curve is upward sloping. This is

because as the term to maturity increases, the credit risk increases, and hence the

expected return will be higher. Secondly, according to liquidity preference theory, as the

term to maturity increases, the opportunity risk increases, and hence the expected

return will be higher(John, Smart, Adam, & Gunasingham, 2013).

Part c

All curves were inverted initially then upward sloping. This information tells us that the

Australian economy has experienced a downturn and the expectations regarding future

inflation and short term interest rates are low.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

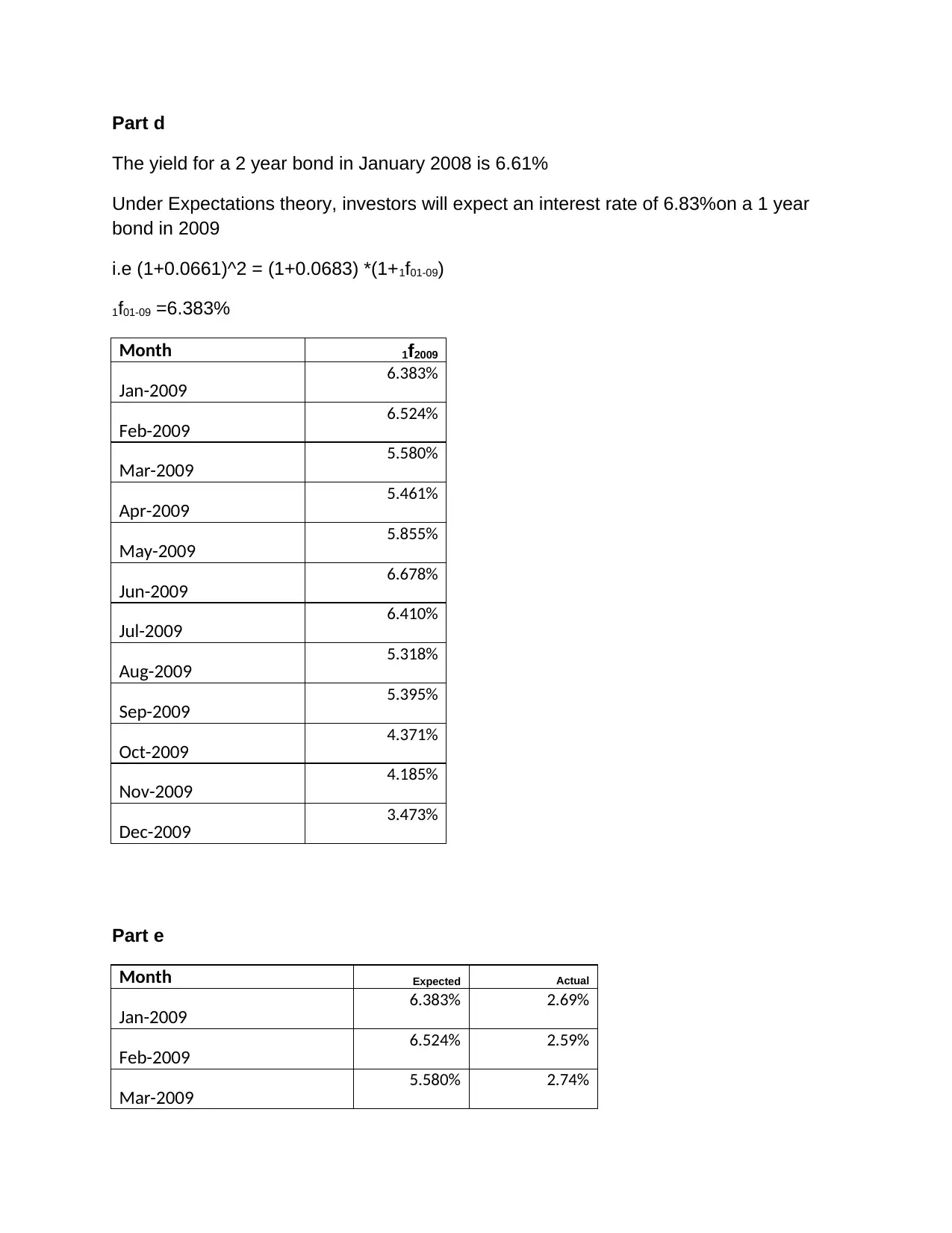

Part d

The yield for a 2 year bond in January 2008 is 6.61%

Under Expectations theory, investors will expect an interest rate of 6.83%on a 1 year

bond in 2009

i.e (1+0.0661)^2 = (1+0.0683) *(1+1f01-09)

1f01-09 =6.383%

Month 1f2009

Jan-2009 6.383%

Feb-2009 6.524%

Mar-2009 5.580%

Apr-2009 5.461%

May-2009 5.855%

Jun-2009 6.678%

Jul-2009 6.410%

Aug-2009 5.318%

Sep-2009 5.395%

Oct-2009 4.371%

Nov-2009 4.185%

Dec-2009 3.473%

Part e

Month Expected Actual

Jan-2009 6.383% 2.69%

Feb-2009 6.524% 2.59%

Mar-2009 5.580% 2.74%

The yield for a 2 year bond in January 2008 is 6.61%

Under Expectations theory, investors will expect an interest rate of 6.83%on a 1 year

bond in 2009

i.e (1+0.0661)^2 = (1+0.0683) *(1+1f01-09)

1f01-09 =6.383%

Month 1f2009

Jan-2009 6.383%

Feb-2009 6.524%

Mar-2009 5.580%

Apr-2009 5.461%

May-2009 5.855%

Jun-2009 6.678%

Jul-2009 6.410%

Aug-2009 5.318%

Sep-2009 5.395%

Oct-2009 4.371%

Nov-2009 4.185%

Dec-2009 3.473%

Part e

Month Expected Actual

Jan-2009 6.383% 2.69%

Feb-2009 6.524% 2.59%

Mar-2009 5.580% 2.74%

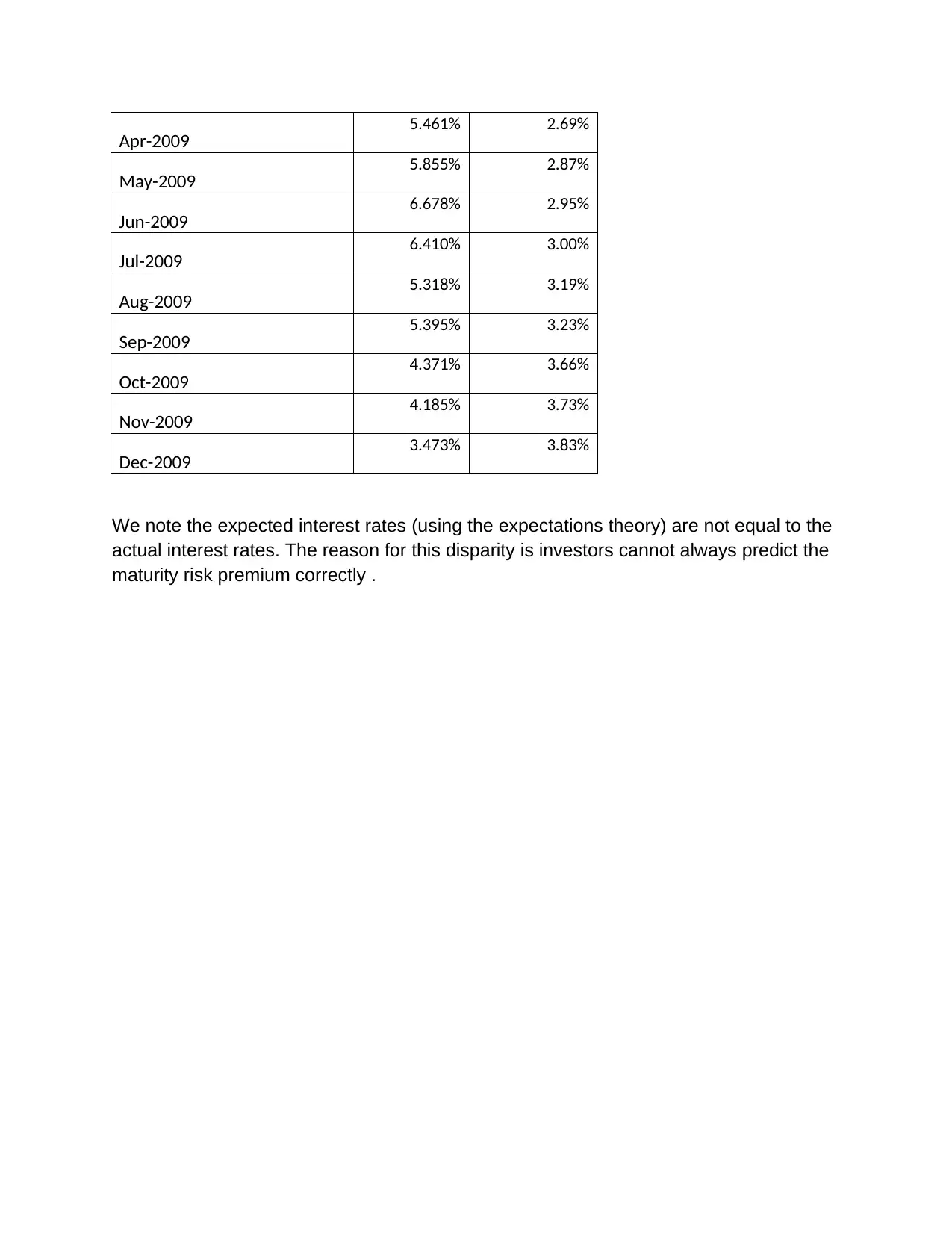

Apr-2009 5.461% 2.69%

May-2009 5.855% 2.87%

Jun-2009 6.678% 2.95%

Jul-2009 6.410% 3.00%

Aug-2009 5.318% 3.19%

Sep-2009 5.395% 3.23%

Oct-2009 4.371% 3.66%

Nov-2009 4.185% 3.73%

Dec-2009 3.473% 3.83%

We note the expected interest rates (using the expectations theory) are not equal to the

actual interest rates. The reason for this disparity is investors cannot always predict the

maturity risk premium correctly .

May-2009 5.855% 2.87%

Jun-2009 6.678% 2.95%

Jul-2009 6.410% 3.00%

Aug-2009 5.318% 3.19%

Sep-2009 5.395% 3.23%

Oct-2009 4.371% 3.66%

Nov-2009 4.185% 3.73%

Dec-2009 3.473% 3.83%

We note the expected interest rates (using the expectations theory) are not equal to the

actual interest rates. The reason for this disparity is investors cannot always predict the

maturity risk premium correctly .

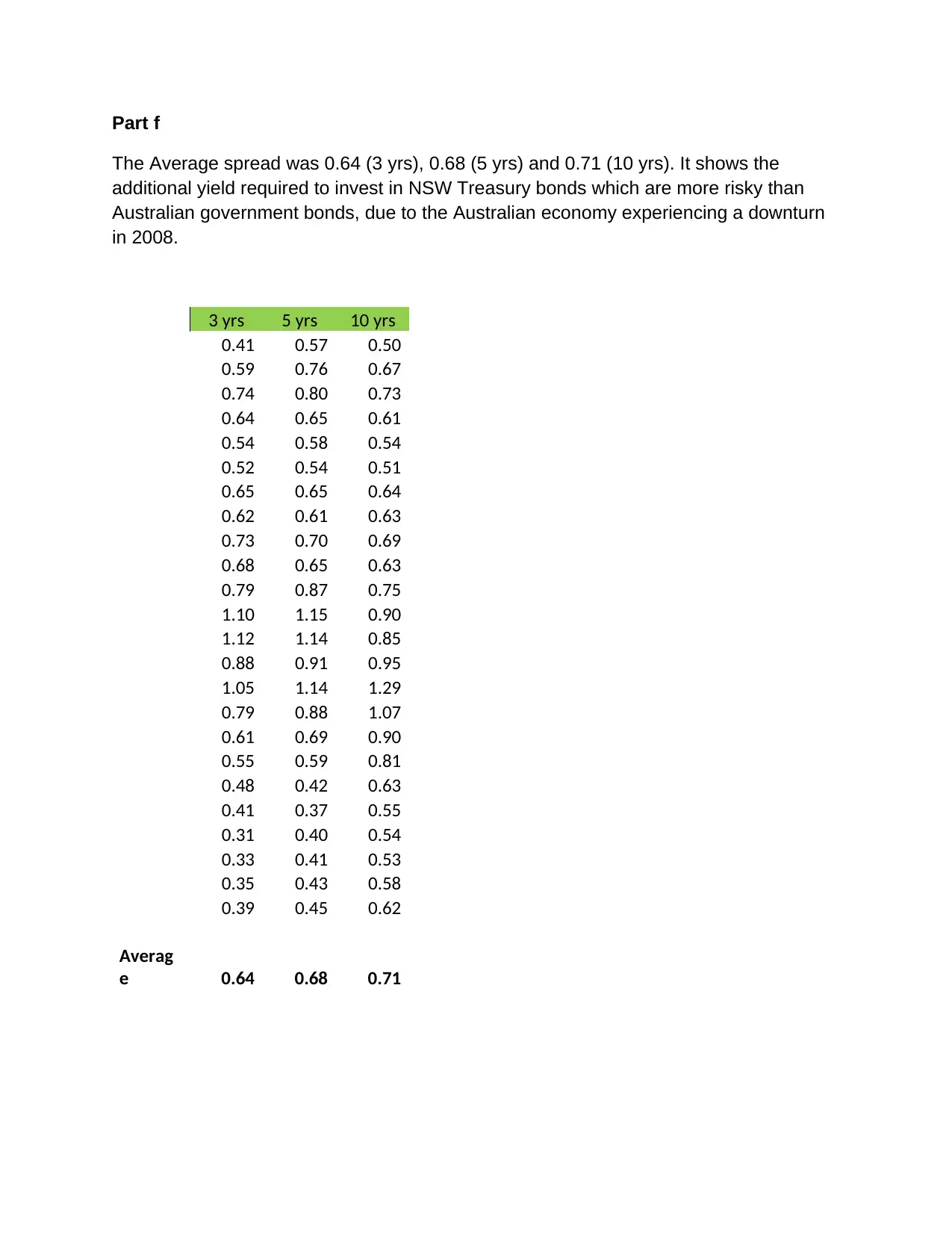

Part f

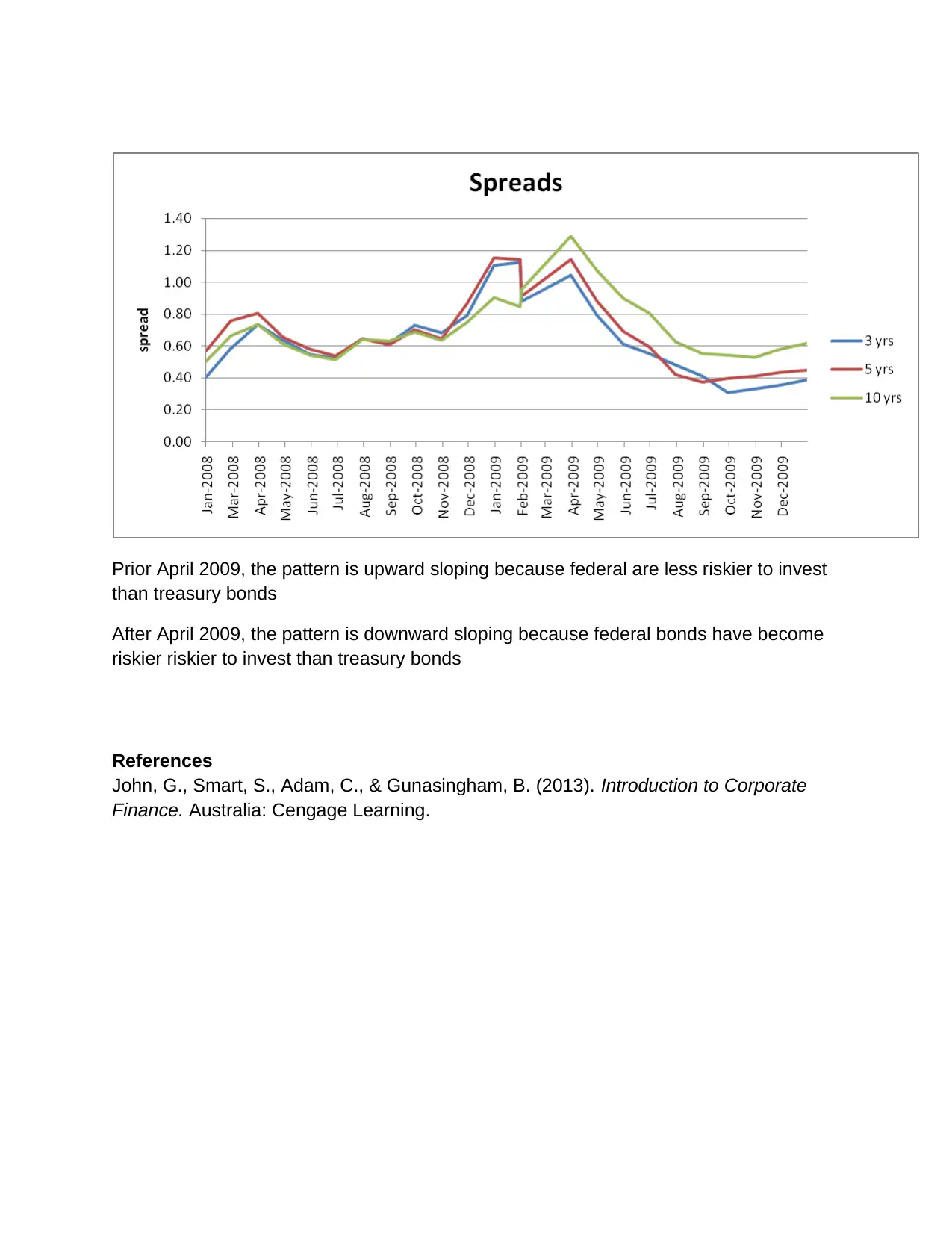

The Average spread was 0.64 (3 yrs), 0.68 (5 yrs) and 0.71 (10 yrs). It shows the

additional yield required to invest in NSW Treasury bonds which are more risky than

Australian government bonds, due to the Australian economy experiencing a downturn

in 2008.

3 yrs 5 yrs 10 yrs

0.41 0.57 0.50

0.59 0.76 0.67

0.74 0.80 0.73

0.64 0.65 0.61

0.54 0.58 0.54

0.52 0.54 0.51

0.65 0.65 0.64

0.62 0.61 0.63

0.73 0.70 0.69

0.68 0.65 0.63

0.79 0.87 0.75

1.10 1.15 0.90

1.12 1.14 0.85

0.88 0.91 0.95

1.05 1.14 1.29

0.79 0.88 1.07

0.61 0.69 0.90

0.55 0.59 0.81

0.48 0.42 0.63

0.41 0.37 0.55

0.31 0.40 0.54

0.33 0.41 0.53

0.35 0.43 0.58

0.39 0.45 0.62

Averag

e 0.64 0.68 0.71

The Average spread was 0.64 (3 yrs), 0.68 (5 yrs) and 0.71 (10 yrs). It shows the

additional yield required to invest in NSW Treasury bonds which are more risky than

Australian government bonds, due to the Australian economy experiencing a downturn

in 2008.

3 yrs 5 yrs 10 yrs

0.41 0.57 0.50

0.59 0.76 0.67

0.74 0.80 0.73

0.64 0.65 0.61

0.54 0.58 0.54

0.52 0.54 0.51

0.65 0.65 0.64

0.62 0.61 0.63

0.73 0.70 0.69

0.68 0.65 0.63

0.79 0.87 0.75

1.10 1.15 0.90

1.12 1.14 0.85

0.88 0.91 0.95

1.05 1.14 1.29

0.79 0.88 1.07

0.61 0.69 0.90

0.55 0.59 0.81

0.48 0.42 0.63

0.41 0.37 0.55

0.31 0.40 0.54

0.33 0.41 0.53

0.35 0.43 0.58

0.39 0.45 0.62

Averag

e 0.64 0.68 0.71

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Prior April 2009, the pattern is upward sloping because federal are less riskier to invest

than treasury bonds

After April 2009, the pattern is downward sloping because federal bonds have become

riskier riskier to invest than treasury bonds

References

John, G., Smart, S., Adam, C., & Gunasingham, B. (2013). Introduction to Corporate

Finance. Australia: Cengage Learning.

than treasury bonds

After April 2009, the pattern is downward sloping because federal bonds have become

riskier riskier to invest than treasury bonds

References

John, G., Smart, S., Adam, C., & Gunasingham, B. (2013). Introduction to Corporate

Finance. Australia: Cengage Learning.

Question 2

a)

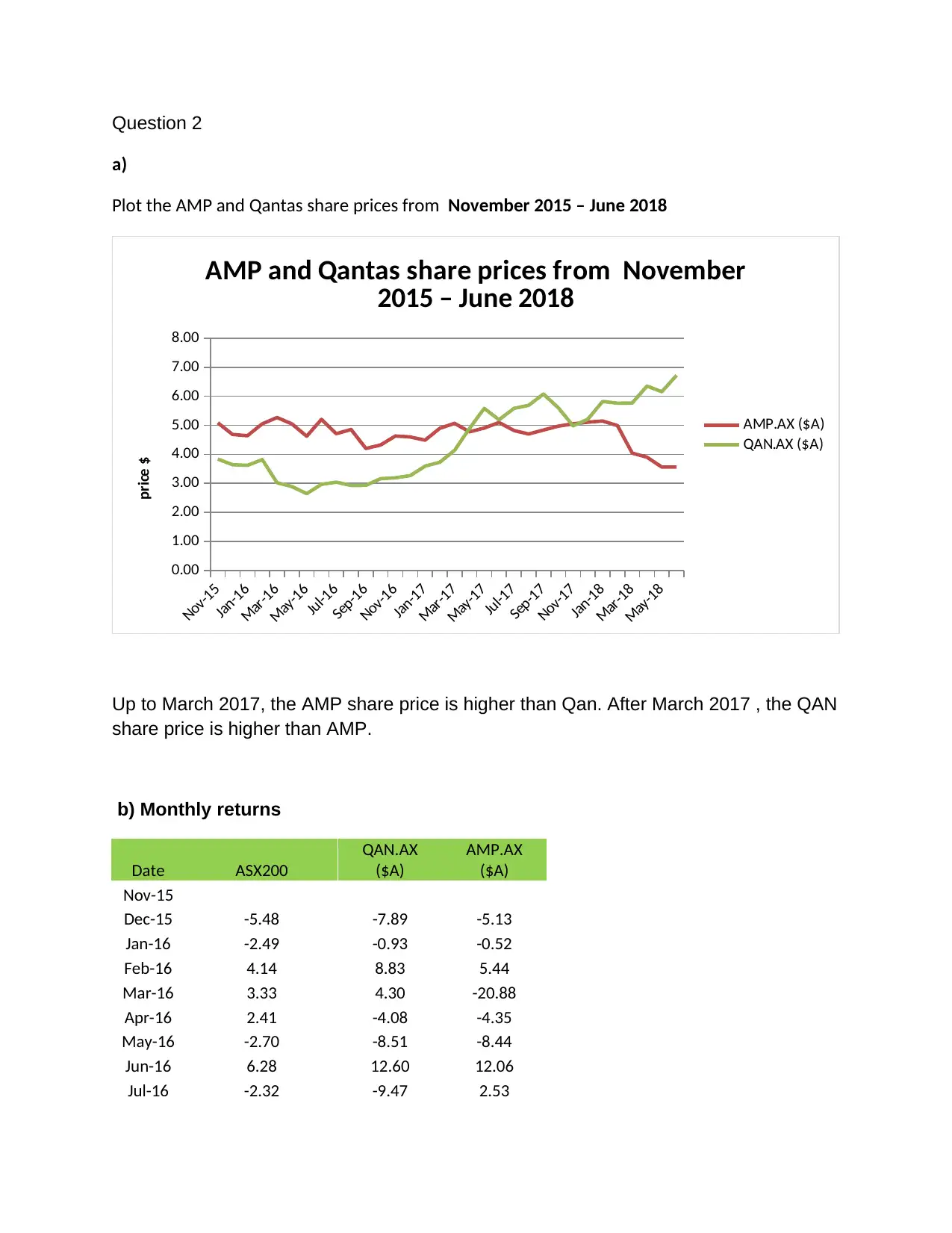

Plot the AMP and Qantas share prices from November 2015 – June 2018

Nov-15

Jan-16

Mar-16

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-17

Sep-17

Nov-17

Jan-18

Mar-18

May-18

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

AMP and Qantas share prices from November

2015 – June 2018

AMP.AX ($A)

QAN.AX ($A)

price $

Up to March 2017, the AMP share price is higher than Qan. After March 2017 , the QAN

share price is higher than AMP.

b) Monthly returns

Date ASX200

QAN.AX

($A)

AMP.AX

($A)

Nov-15

Dec-15 -5.48 -7.89 -5.13

Jan-16 -2.49 -0.93 -0.52

Feb-16 4.14 8.83 5.44

Mar-16 3.33 4.30 -20.88

Apr-16 2.41 -4.08 -4.35

May-16 -2.70 -8.51 -8.44

Jun-16 6.28 12.60 12.06

Jul-16 -2.32 -9.47 2.53

a)

Plot the AMP and Qantas share prices from November 2015 – June 2018

Nov-15

Jan-16

Mar-16

May-16

Jul-16

Sep-16

Nov-16

Jan-17

Mar-17

May-17

Jul-17

Sep-17

Nov-17

Jan-18

Mar-18

May-18

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

AMP and Qantas share prices from November

2015 – June 2018

AMP.AX ($A)

QAN.AX ($A)

price $

Up to March 2017, the AMP share price is higher than Qan. After March 2017 , the QAN

share price is higher than AMP.

b) Monthly returns

Date ASX200

QAN.AX

($A)

AMP.AX

($A)

Nov-15

Dec-15 -5.48 -7.89 -5.13

Jan-16 -2.49 -0.93 -0.52

Feb-16 4.14 8.83 5.44

Mar-16 3.33 4.30 -20.88

Apr-16 2.41 -4.08 -4.35

May-16 -2.70 -8.51 -8.44

Jun-16 6.28 12.60 12.06

Jul-16 -2.32 -9.47 2.53

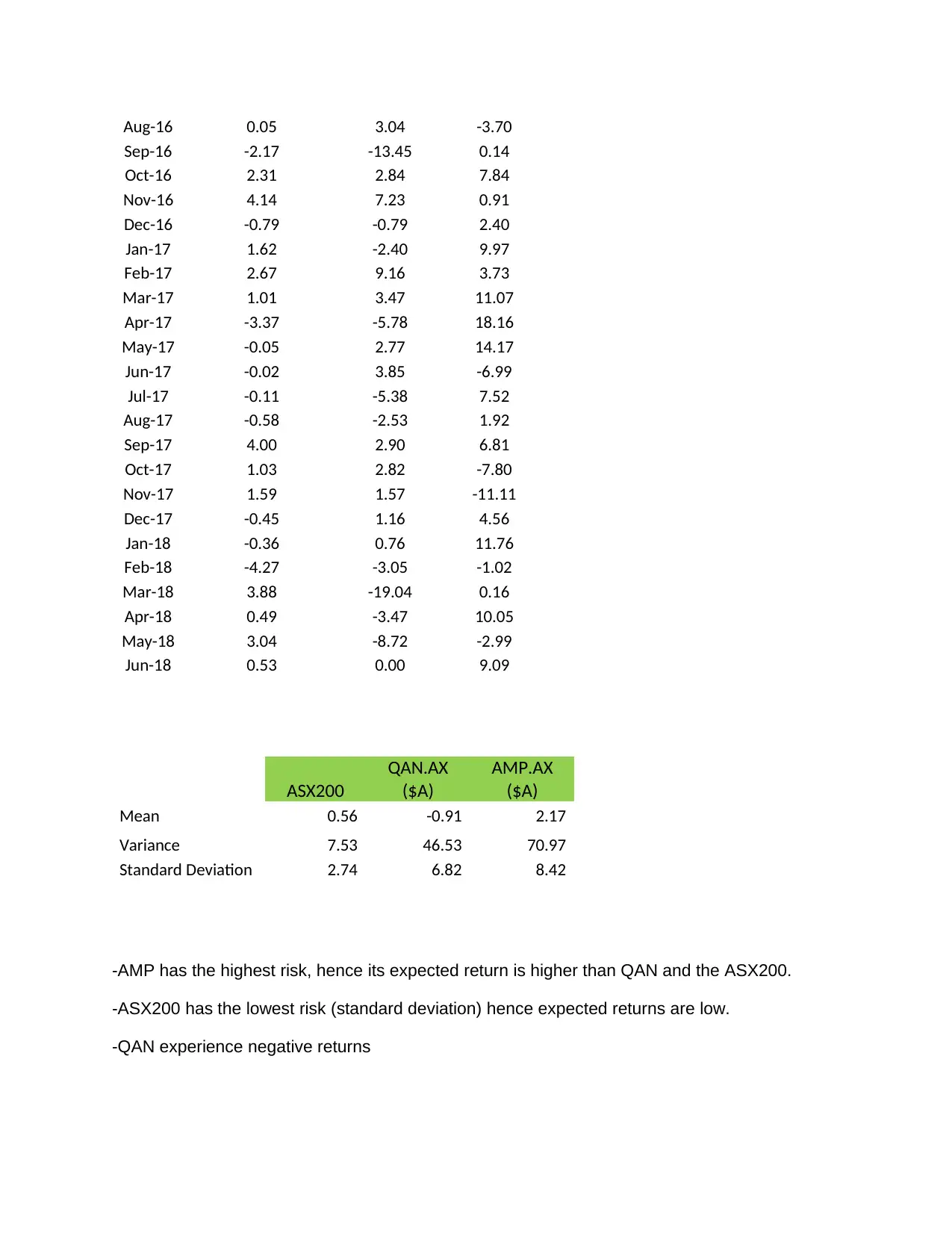

Aug-16 0.05 3.04 -3.70

Sep-16 -2.17 -13.45 0.14

Oct-16 2.31 2.84 7.84

Nov-16 4.14 7.23 0.91

Dec-16 -0.79 -0.79 2.40

Jan-17 1.62 -2.40 9.97

Feb-17 2.67 9.16 3.73

Mar-17 1.01 3.47 11.07

Apr-17 -3.37 -5.78 18.16

May-17 -0.05 2.77 14.17

Jun-17 -0.02 3.85 -6.99

Jul-17 -0.11 -5.38 7.52

Aug-17 -0.58 -2.53 1.92

Sep-17 4.00 2.90 6.81

Oct-17 1.03 2.82 -7.80

Nov-17 1.59 1.57 -11.11

Dec-17 -0.45 1.16 4.56

Jan-18 -0.36 0.76 11.76

Feb-18 -4.27 -3.05 -1.02

Mar-18 3.88 -19.04 0.16

Apr-18 0.49 -3.47 10.05

May-18 3.04 -8.72 -2.99

Jun-18 0.53 0.00 9.09

ASX200

QAN.AX

($A)

AMP.AX

($A)

Mean 0.56 -0.91 2.17

Variance 7.53 46.53 70.97

Standard Deviation 2.74 6.82 8.42

-AMP has the highest risk, hence its expected return is higher than QAN and the ASX200.

-ASX200 has the lowest risk (standard deviation) hence expected returns are low.

-QAN experience negative returns

Sep-16 -2.17 -13.45 0.14

Oct-16 2.31 2.84 7.84

Nov-16 4.14 7.23 0.91

Dec-16 -0.79 -0.79 2.40

Jan-17 1.62 -2.40 9.97

Feb-17 2.67 9.16 3.73

Mar-17 1.01 3.47 11.07

Apr-17 -3.37 -5.78 18.16

May-17 -0.05 2.77 14.17

Jun-17 -0.02 3.85 -6.99

Jul-17 -0.11 -5.38 7.52

Aug-17 -0.58 -2.53 1.92

Sep-17 4.00 2.90 6.81

Oct-17 1.03 2.82 -7.80

Nov-17 1.59 1.57 -11.11

Dec-17 -0.45 1.16 4.56

Jan-18 -0.36 0.76 11.76

Feb-18 -4.27 -3.05 -1.02

Mar-18 3.88 -19.04 0.16

Apr-18 0.49 -3.47 10.05

May-18 3.04 -8.72 -2.99

Jun-18 0.53 0.00 9.09

ASX200

QAN.AX

($A)

AMP.AX

($A)

Mean 0.56 -0.91 2.17

Variance 7.53 46.53 70.97

Standard Deviation 2.74 6.82 8.42

-AMP has the highest risk, hence its expected return is higher than QAN and the ASX200.

-ASX200 has the lowest risk (standard deviation) hence expected returns are low.

-QAN experience negative returns

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

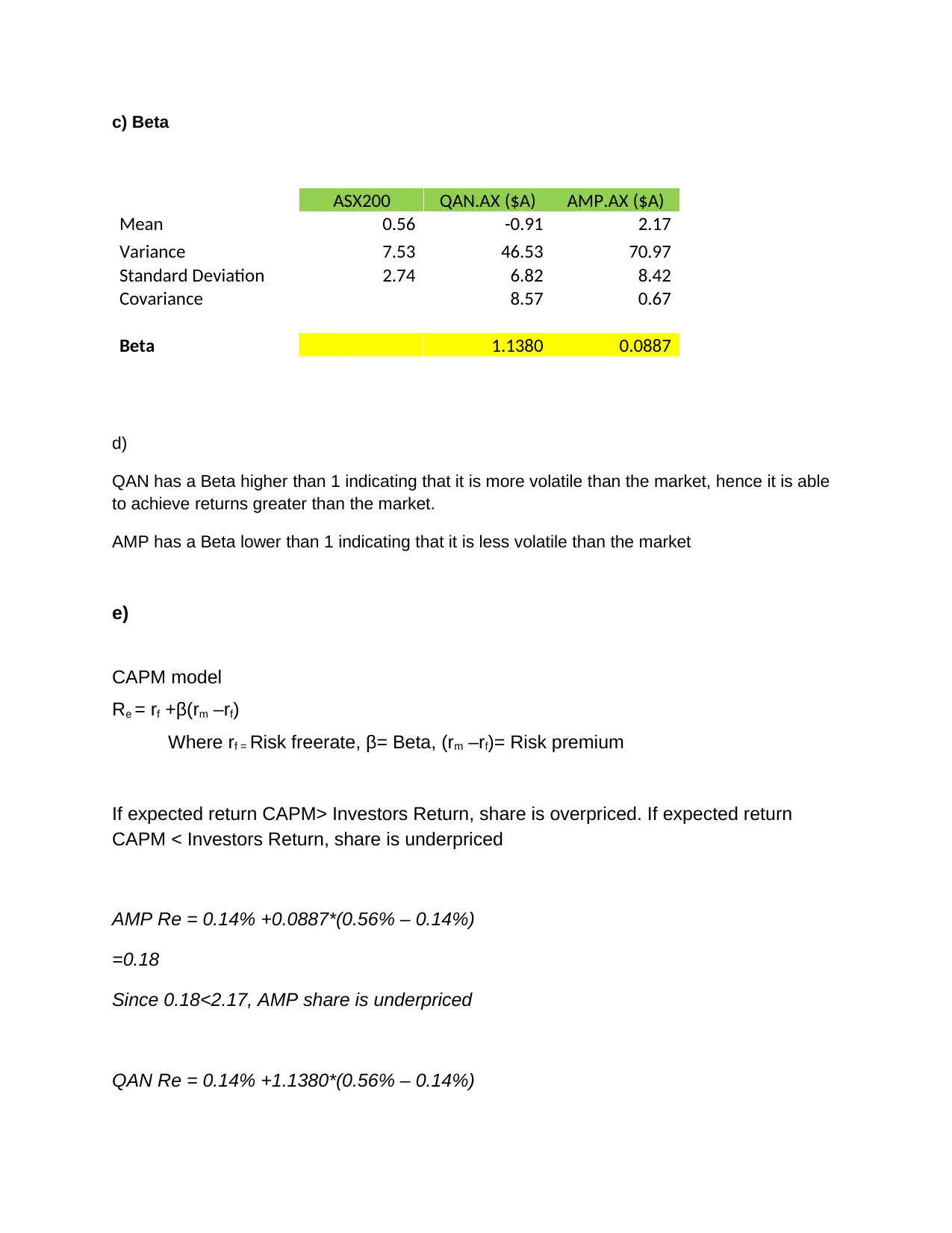

c) Beta

ASX200 QAN.AX ($A) AMP.AX ($A)

Mean 0.56 -0.91 2.17

Variance 7.53 46.53 70.97

Standard Deviation 2.74 6.82 8.42

Covariance 8.57 0.67

Beta 1.1380 0.0887

d)

QAN has a Beta higher than 1 indicating that it is more volatile than the market, hence it is able

to achieve returns greater than the market.

AMP has a Beta lower than 1 indicating that it is less volatile than the market

e)

CAPM model

Re = rf +β(rm –rf)

Where rf = Risk freerate, β= Beta, (rm –rf)= Risk premium

If expected return CAPM> Investors Return, share is overpriced. If expected return

CAPM < Investors Return, share is underpriced

AMP Re = 0.14% +0.0887*(0.56% – 0.14%)

=0.18

Since 0.18<2.17, AMP share is underpriced

QAN Re = 0.14% +1.1380*(0.56% – 0.14%)

ASX200 QAN.AX ($A) AMP.AX ($A)

Mean 0.56 -0.91 2.17

Variance 7.53 46.53 70.97

Standard Deviation 2.74 6.82 8.42

Covariance 8.57 0.67

Beta 1.1380 0.0887

d)

QAN has a Beta higher than 1 indicating that it is more volatile than the market, hence it is able

to achieve returns greater than the market.

AMP has a Beta lower than 1 indicating that it is less volatile than the market

e)

CAPM model

Re = rf +β(rm –rf)

Where rf = Risk freerate, β= Beta, (rm –rf)= Risk premium

If expected return CAPM> Investors Return, share is overpriced. If expected return

CAPM < Investors Return, share is underpriced

AMP Re = 0.14% +0.0887*(0.56% – 0.14%)

=0.18

Since 0.18<2.17, AMP share is underpriced

QAN Re = 0.14% +1.1380*(0.56% – 0.14%)

=0.62

Since 0.62 >-0.091, QAN share is overpriced

Since 0.62 >-0.091, QAN share is overpriced

F. Report

Introduction

The purpose of this report is to summarize the past performance and future prospects of AMP

and Qantas Shares.

AMP

AMP is a provider of life insurance, superannuation, pensions and other financial services in

Australia and New Zealand (AMP, 2018).

In the past, its share price has been falling. The main reason for the drop has been the effect of

movements in asset markets and investor confidence on AUM, earnings and sales. Furthermore,

the insurance industry has been faced with numerous challenges including: overcapacity,

underpricing and poor product design in the industry (The Australian, 2018).

However, it is expected that AMP’s insurance business will recover well due to a number of

changes to fix its claims management processes and stabilize lapse rates. Furthermore, AMP is

leveraged to the growth in wealth management, superannuation and retirement income supported

by an aging population and increased superannuation contributions (The Australian, 2018).

QANTAS

Qantas Airways Limited (QAN) operates its main business of transportation of passengers using

two complementary airline brands - Qantas and Jetstar. The Company also operates other

airlines, and businesses in specialist markets such as Q Catering (The Australian, 2018).

Despite increasing fuel costs, the company has managed to increase its share price. This has been

as a result of strong solid results from each of their business units which have been underpinned

by positive market conditions, timing, capacity discipline, and the airline’s ongoing

transformation (Mickleboro, 2018).

Introduction

The purpose of this report is to summarize the past performance and future prospects of AMP

and Qantas Shares.

AMP

AMP is a provider of life insurance, superannuation, pensions and other financial services in

Australia and New Zealand (AMP, 2018).

In the past, its share price has been falling. The main reason for the drop has been the effect of

movements in asset markets and investor confidence on AUM, earnings and sales. Furthermore,

the insurance industry has been faced with numerous challenges including: overcapacity,

underpricing and poor product design in the industry (The Australian, 2018).

However, it is expected that AMP’s insurance business will recover well due to a number of

changes to fix its claims management processes and stabilize lapse rates. Furthermore, AMP is

leveraged to the growth in wealth management, superannuation and retirement income supported

by an aging population and increased superannuation contributions (The Australian, 2018).

QANTAS

Qantas Airways Limited (QAN) operates its main business of transportation of passengers using

two complementary airline brands - Qantas and Jetstar. The Company also operates other

airlines, and businesses in specialist markets such as Q Catering (The Australian, 2018).

Despite increasing fuel costs, the company has managed to increase its share price. This has been

as a result of strong solid results from each of their business units which have been underpinned

by positive market conditions, timing, capacity discipline, and the airline’s ongoing

transformation (Mickleboro, 2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

AMP. (2018). About Us. Retrieved September 2018, from AMP: https://www.amp.com.au

John, G., Smart, S., Adam, C., & Gunasingham, B. (2013). Introduction to Corporate Finance. Australia:

Cengage Learning.

Mickleboro, J. (2018, May 2). Why Qantas Airways Limited Shares are taking off Today. Retrieved

September 2018, from The Motley fool: https://www.fool.com.au/2018/05/02/why-qantas-

airways-limited-shares-are-taking-off-today/

The Australian. (2018). QANTAS AIRWAYS LIMITED. Retrieved September 2018, from The Australian:

https://markets.theaustralian.com.au/shares/QAN/qantas-airways-limited

The Australian. (2018). The Australian. Retrieved September 2018, from AMP Limited Profile:

https://markets.theaustralian.com.au/shares/AMP/amp-limited

AMP. (2018). About Us. Retrieved September 2018, from AMP: https://www.amp.com.au

John, G., Smart, S., Adam, C., & Gunasingham, B. (2013). Introduction to Corporate Finance. Australia:

Cengage Learning.

Mickleboro, J. (2018, May 2). Why Qantas Airways Limited Shares are taking off Today. Retrieved

September 2018, from The Motley fool: https://www.fool.com.au/2018/05/02/why-qantas-

airways-limited-shares-are-taking-off-today/

The Australian. (2018). QANTAS AIRWAYS LIMITED. Retrieved September 2018, from The Australian:

https://markets.theaustralian.com.au/shares/QAN/qantas-airways-limited

The Australian. (2018). The Australian. Retrieved September 2018, from AMP Limited Profile:

https://markets.theaustralian.com.au/shares/AMP/amp-limited

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.