Zoopla PLC: A Comprehensive Corporate Finance Analysis Report

VerifiedAdded on 2023/06/03

|19

|3000

|242

Report

AI Summary

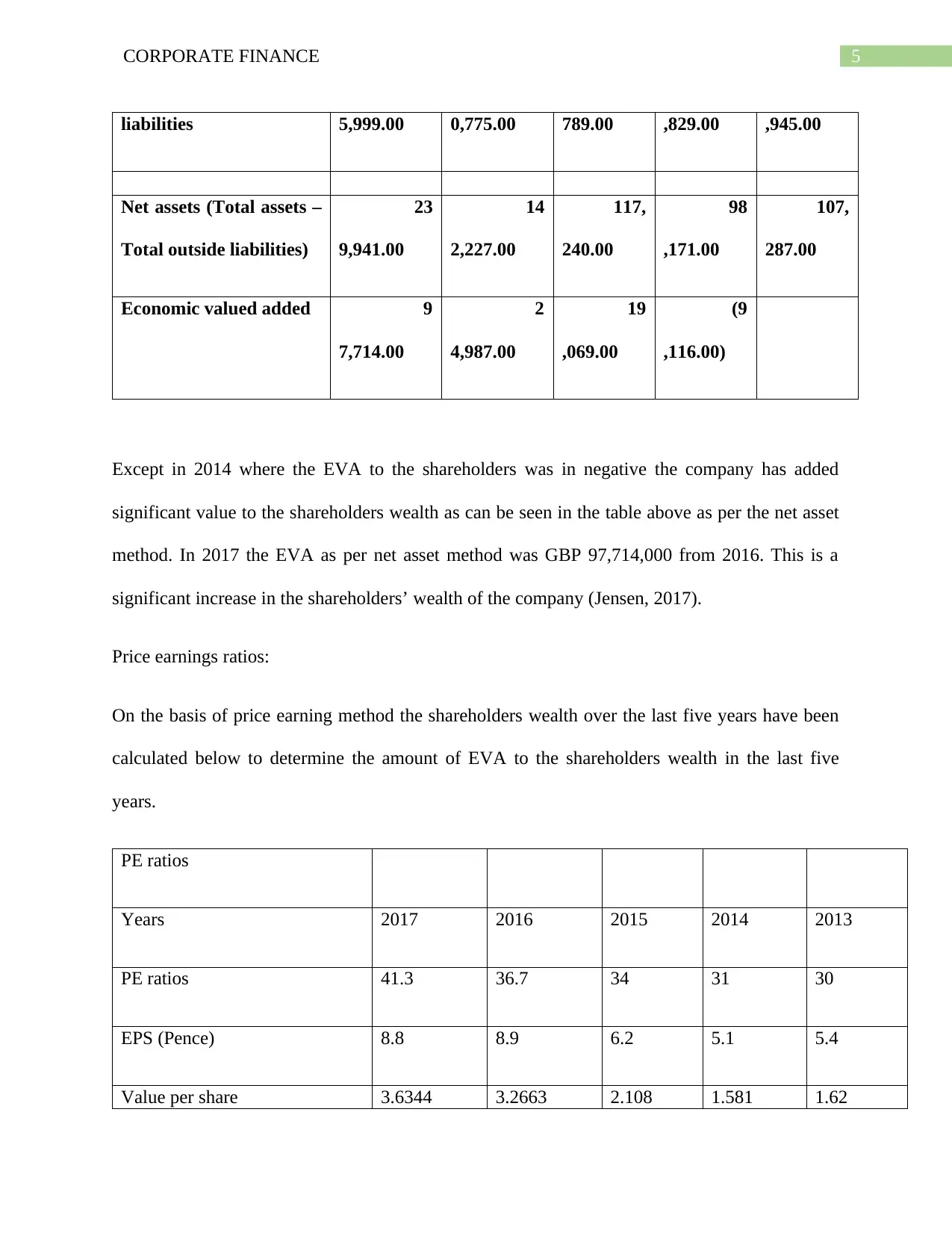

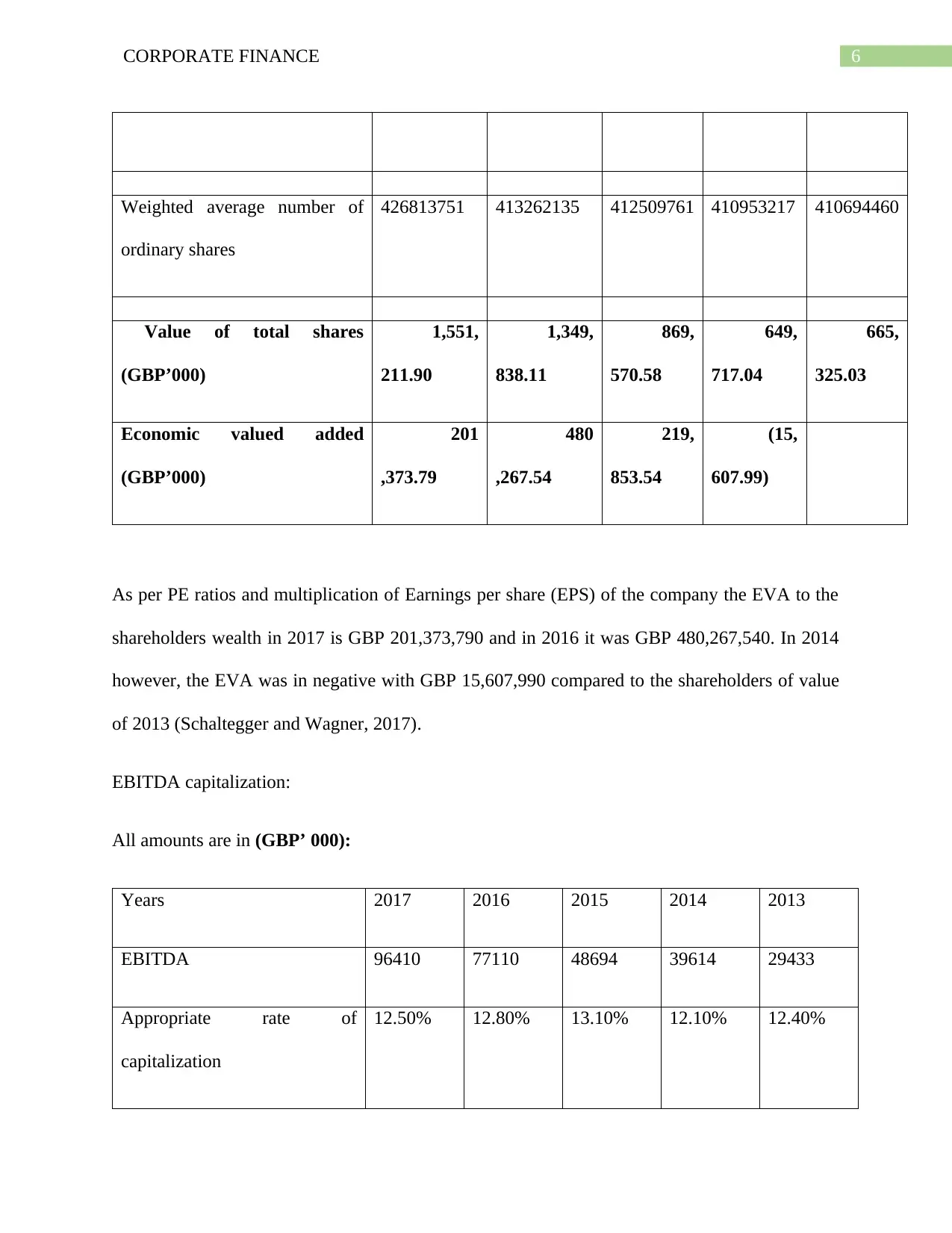

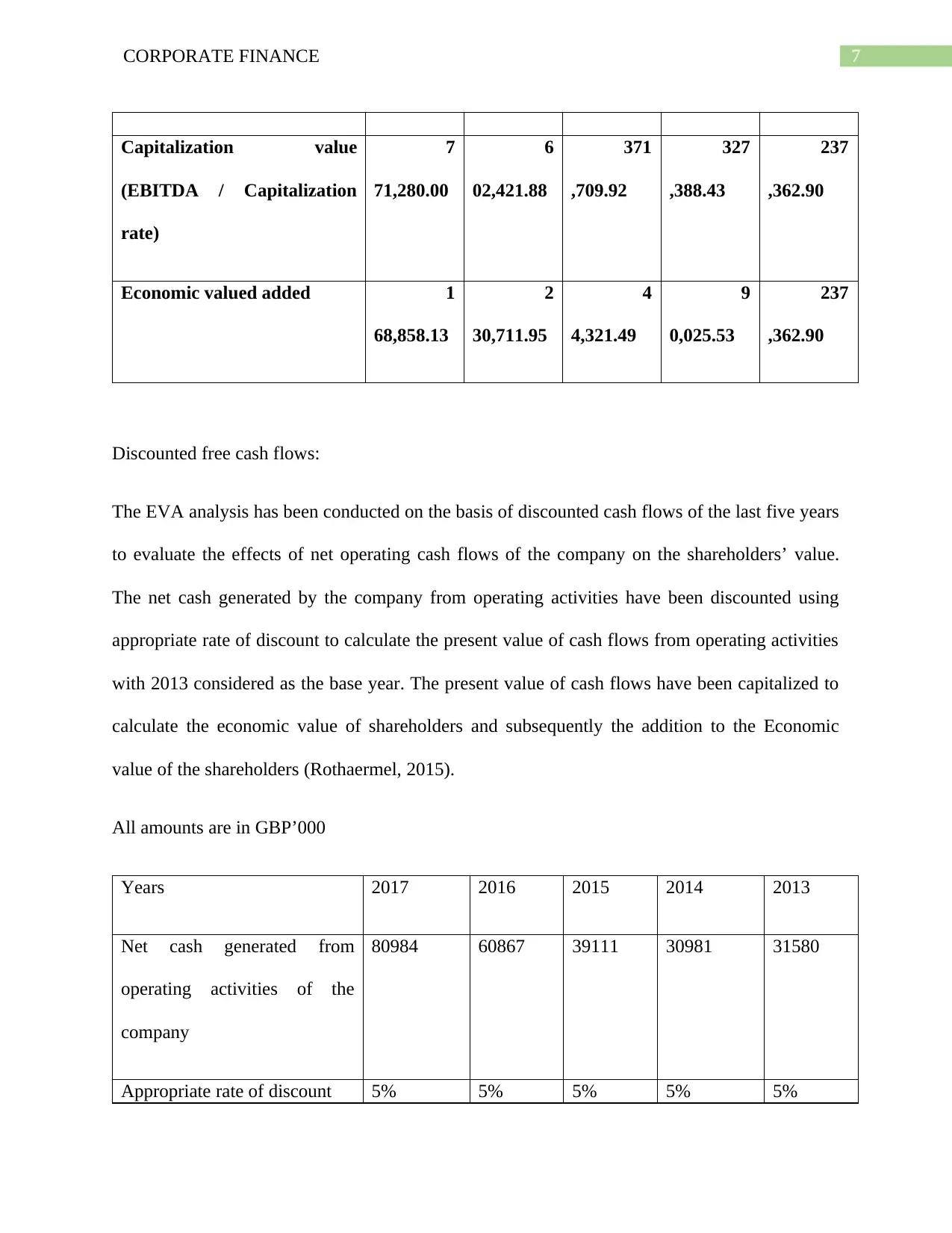

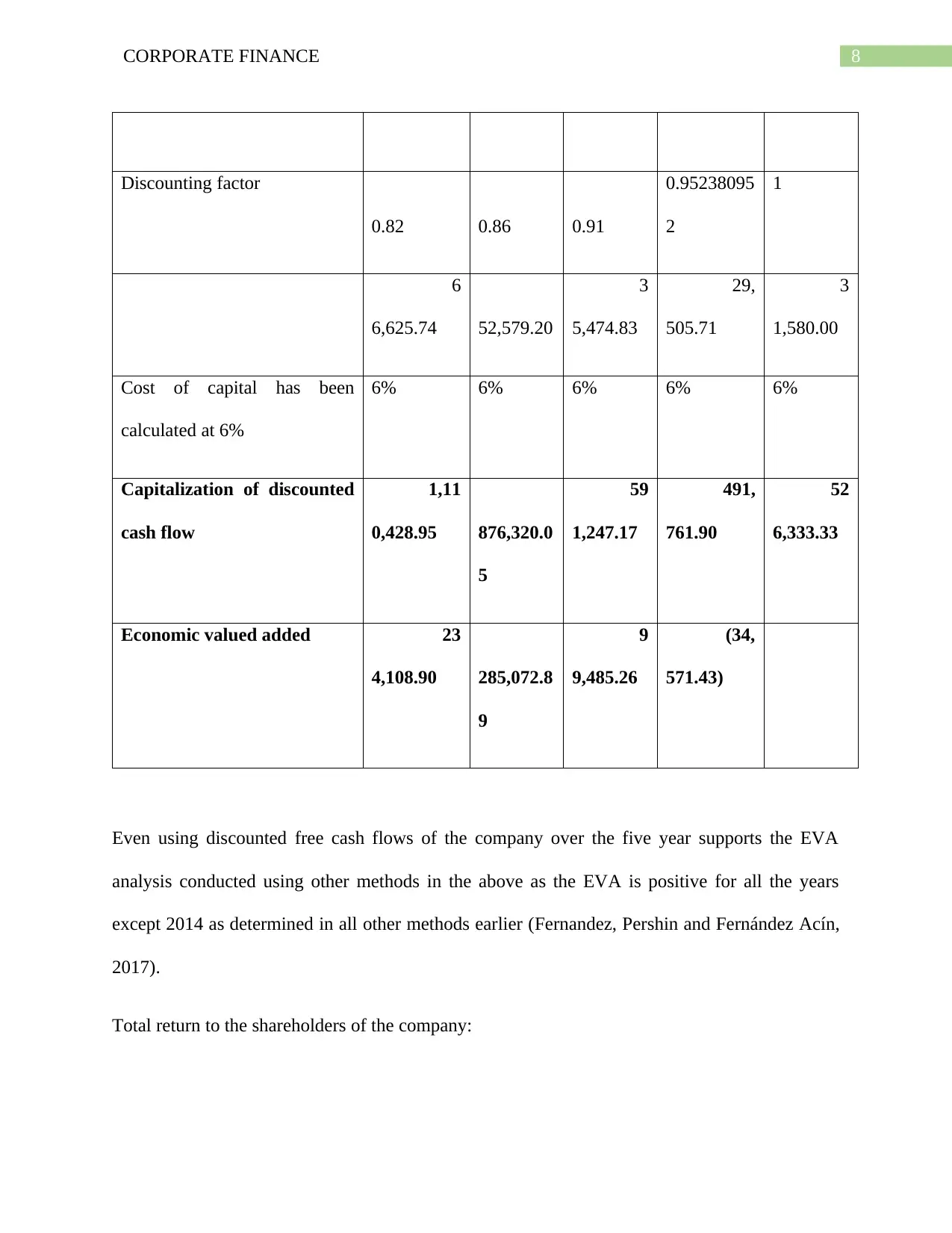

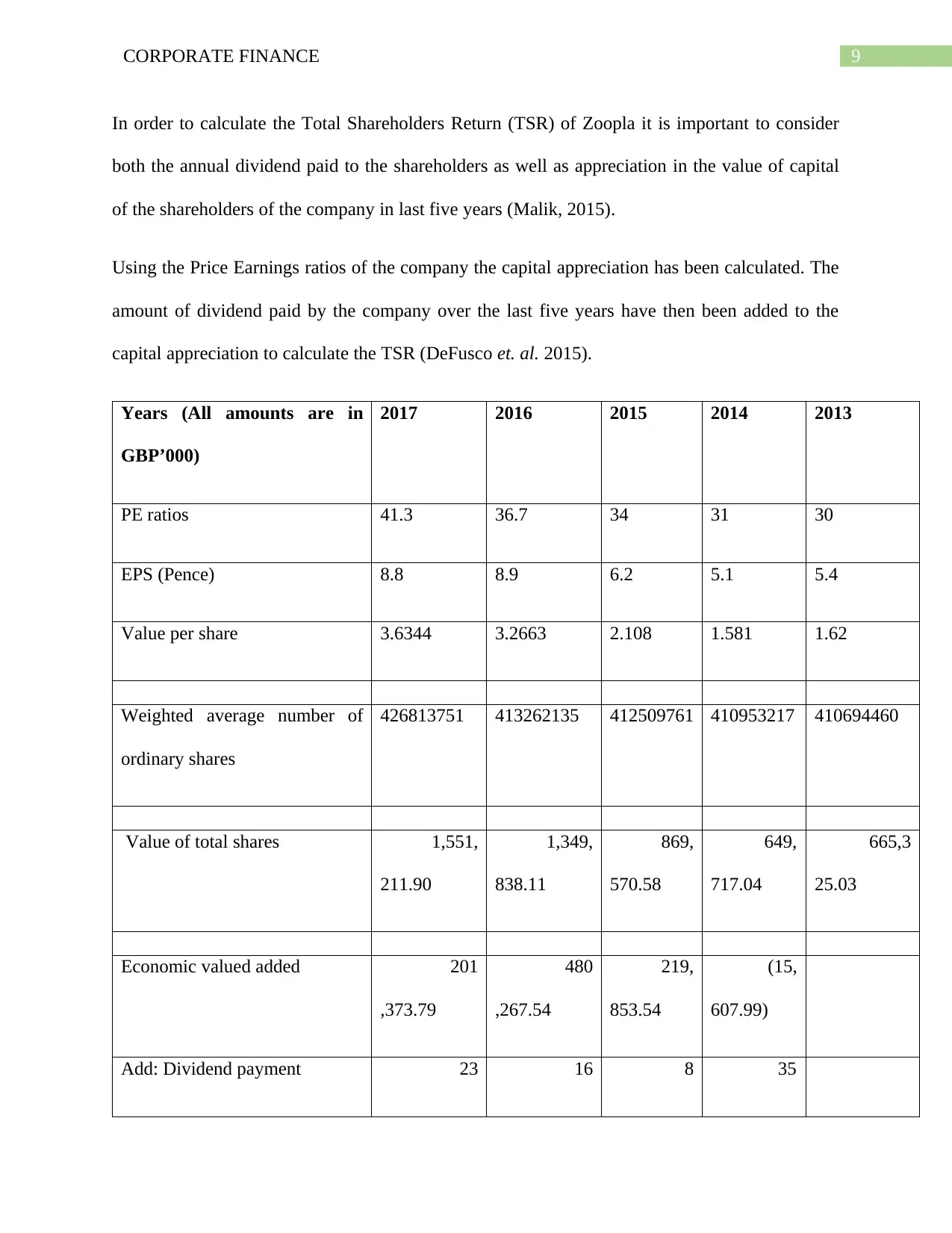

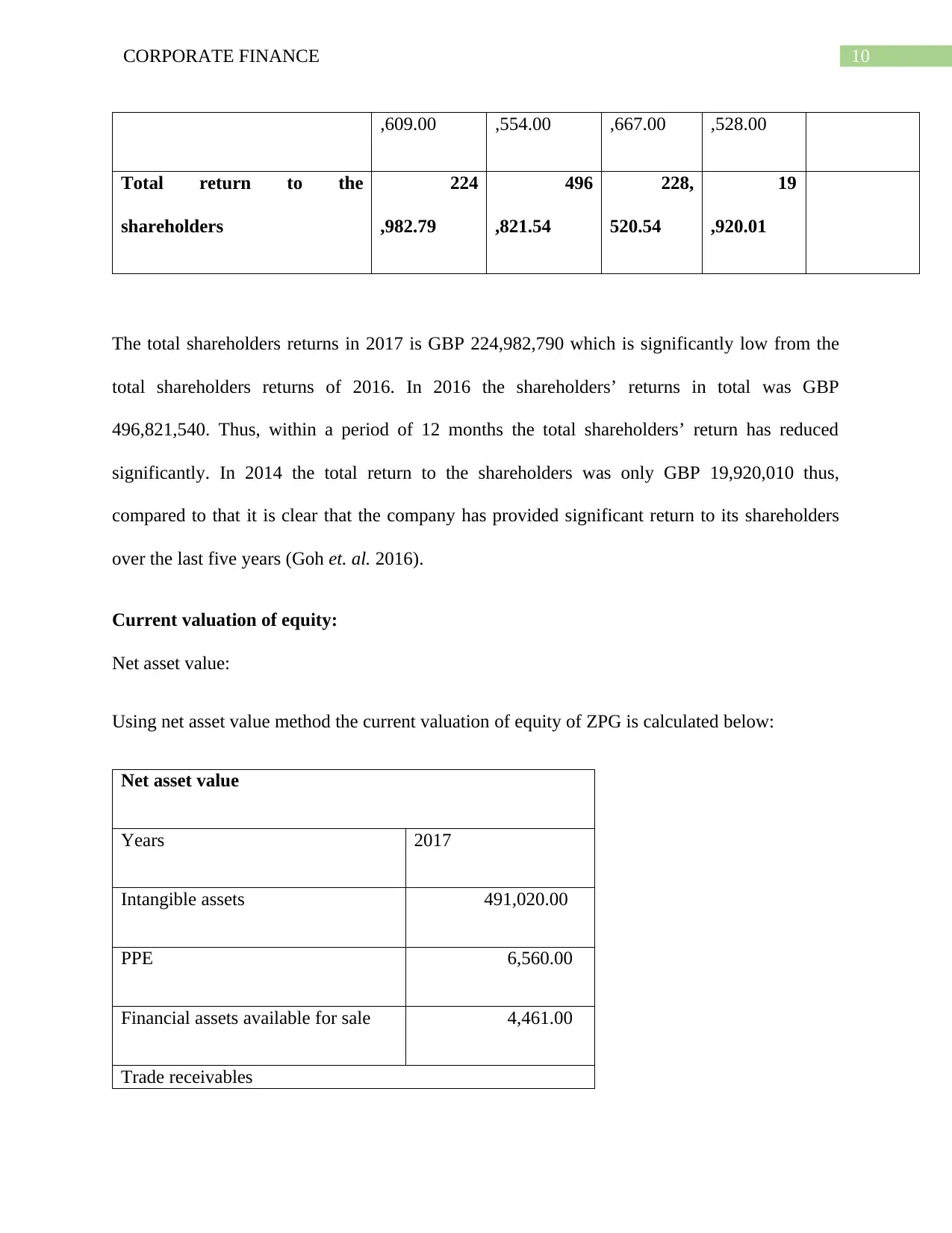

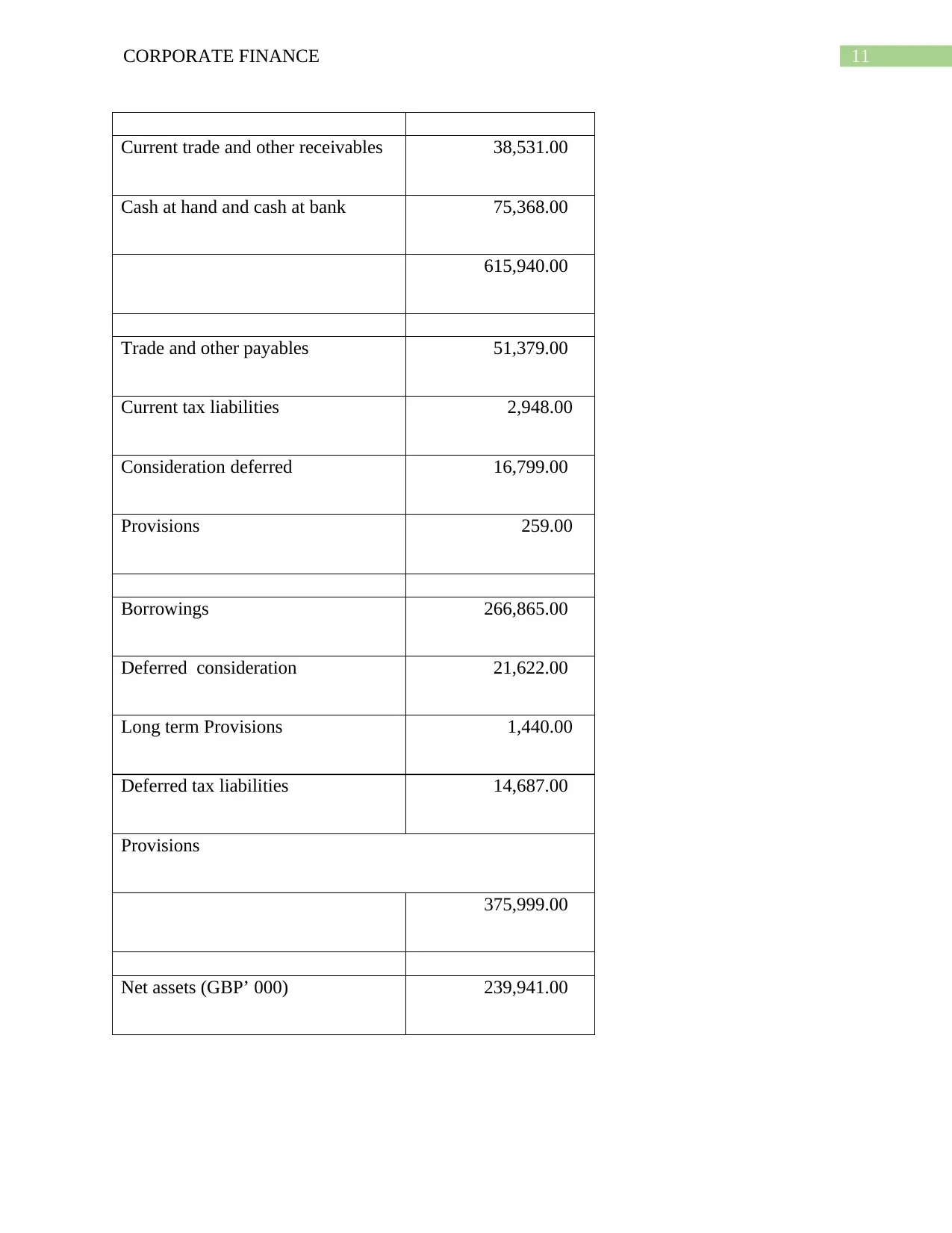

This report provides a comprehensive financial analysis of Zoopla Property Group PLC (ZPG) over the past five years, focusing on its success in delivering value to shareholders. It includes an Economic Value Added (EVA) analysis using net asset valuation, price-earnings ratios, EBITDA capitalization, and discounted free cash flows, assessing the company's ability to generate returns above its cost of capital. The report also analyzes the Total Shareholder Return (TSR), considering both dividend payments and capital appreciation. Furthermore, the document undertakes a current valuation of ZPG's equity using net asset value, comparable ratios (P/E, P/B, EV/EBITDA), and discounted free cash flow methods, providing a multifaceted perspective on the company's financial health and shareholder value creation.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.