3102AFE Auditing: Top Fashion Warehouse Client Analysis 2018

VerifiedAdded on 2023/04/21

|10

|2103

|296

Case Study

AI Summary

This auditing case study analyzes Top Fashion Warehouse's financial performance and identifies key risks. It includes a ratio analysis covering profitability, efficiency, liquidity, and solvency, highlighting fluctuations in inventory and cash balances. The study identifies cash, inventory, property, plant, and equipment, and intangible assets as high-risk accounts, detailing the potential misstatements and omissions. Key assertions related to these accounts are discussed, emphasizing the need for auditor scrutiny. The document is available on Desklib, a platform offering study tools and resources for students.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note

Auditing

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Ratios Analysis............................................................................................................................2

Key Inherent Risks of the business..............................................................................................5

Four Accounts which are at Risk.................................................................................................6

Key Assertions.............................................................................................................................7

Conclusion.......................................................................................................................................8

Reference.........................................................................................................................................9

AUDITING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Ratios Analysis............................................................................................................................2

Key Inherent Risks of the business..............................................................................................5

Four Accounts which are at Risk.................................................................................................6

Key Assertions.............................................................................................................................7

Conclusion.......................................................................................................................................8

Reference.........................................................................................................................................9

2

AUDITING

Introduction

The main purpose of this assessment is to analyse the business environment of Top

Fashion Warehouse which is engaged in the business of manufacturing and designing designer

clothing for the customers. The assessment aims to identify key risk matter of the business and

also identify inherent risks from the analysis of the financial statement of the business. The

assessment would be including calculation of key financial ratios which would help in

determining the performance of the business (Coetzee & Lubbe, 2014). In addition to this, key

accounts are to be recognised which are at risk and how the same affect the financial statement

of the business. The assessment would also include key assertions of the risks which is faced by

the business.

Discussion

Ratios Analysis

The main purpose of ratios which are computed is to analyse the financial performance of

the business and also identify significant risks which are faced by the business in certain areas.

The different ratios which are to be computed cover different area of performance of the business

and the same are show below:

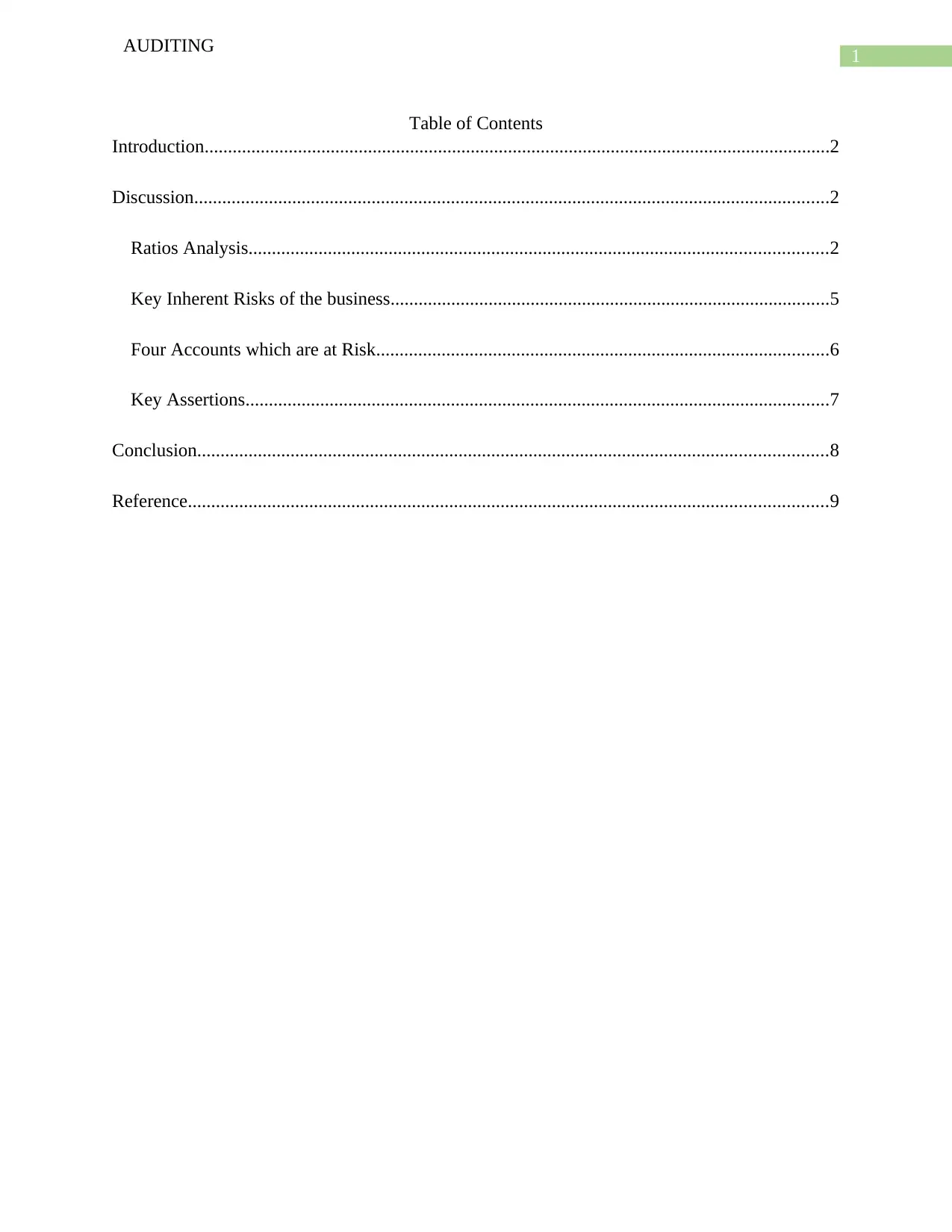

Figure 1: (Image showing Profitability Ratios of the Business)

AUDITING

Introduction

The main purpose of this assessment is to analyse the business environment of Top

Fashion Warehouse which is engaged in the business of manufacturing and designing designer

clothing for the customers. The assessment aims to identify key risk matter of the business and

also identify inherent risks from the analysis of the financial statement of the business. The

assessment would be including calculation of key financial ratios which would help in

determining the performance of the business (Coetzee & Lubbe, 2014). In addition to this, key

accounts are to be recognised which are at risk and how the same affect the financial statement

of the business. The assessment would also include key assertions of the risks which is faced by

the business.

Discussion

Ratios Analysis

The main purpose of ratios which are computed is to analyse the financial performance of

the business and also identify significant risks which are faced by the business in certain areas.

The different ratios which are to be computed cover different area of performance of the business

and the same are show below:

Figure 1: (Image showing Profitability Ratios of the Business)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

Source: (Created by the Author)

The profitability ratio of the business which is shown above comprises of gross profit

margin and net profit margin of the business. The gross profit margin of the business has

increased significantly and the same is shown to be 26.72% for the year 2018. This shows that

the management has made improvement in the operational structure of the business (Bratten et

al., 2013). The net profit margin of the business is shown to have increased significantly as well

in comparison to previous year analysis. The increase in the net profit is mainly due to the

increase in the total revenue which is generated by the business.

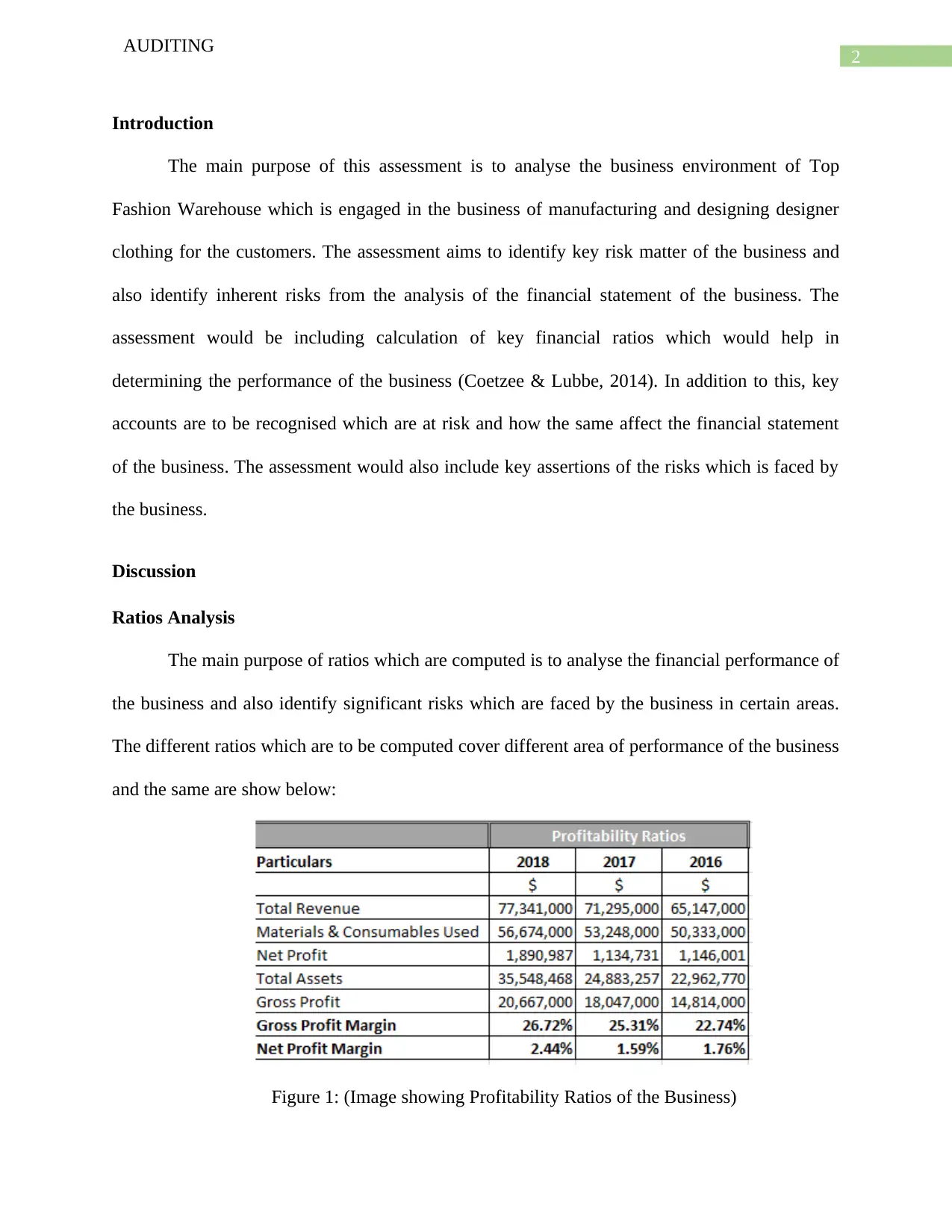

Figure 2: (Image showing Efficiency Ratios of the Business)

Source: (Created by the Author)

The above figure shows efficiency ratio of the business and the same is demonstrated by

inventory turnover ratio and receivable turnover ratio. The inventory turnover ratio has decreased

which is not a good sign for the business and the same is the case with the receivable turnover

ratio of the business (Delen, Kuzey & Uyar 2013). This shows that there is a fall in the efficiency

of the business in terms of both debtors and inventory management.

AUDITING

Source: (Created by the Author)

The profitability ratio of the business which is shown above comprises of gross profit

margin and net profit margin of the business. The gross profit margin of the business has

increased significantly and the same is shown to be 26.72% for the year 2018. This shows that

the management has made improvement in the operational structure of the business (Bratten et

al., 2013). The net profit margin of the business is shown to have increased significantly as well

in comparison to previous year analysis. The increase in the net profit is mainly due to the

increase in the total revenue which is generated by the business.

Figure 2: (Image showing Efficiency Ratios of the Business)

Source: (Created by the Author)

The above figure shows efficiency ratio of the business and the same is demonstrated by

inventory turnover ratio and receivable turnover ratio. The inventory turnover ratio has decreased

which is not a good sign for the business and the same is the case with the receivable turnover

ratio of the business (Delen, Kuzey & Uyar 2013). This shows that there is a fall in the efficiency

of the business in terms of both debtors and inventory management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

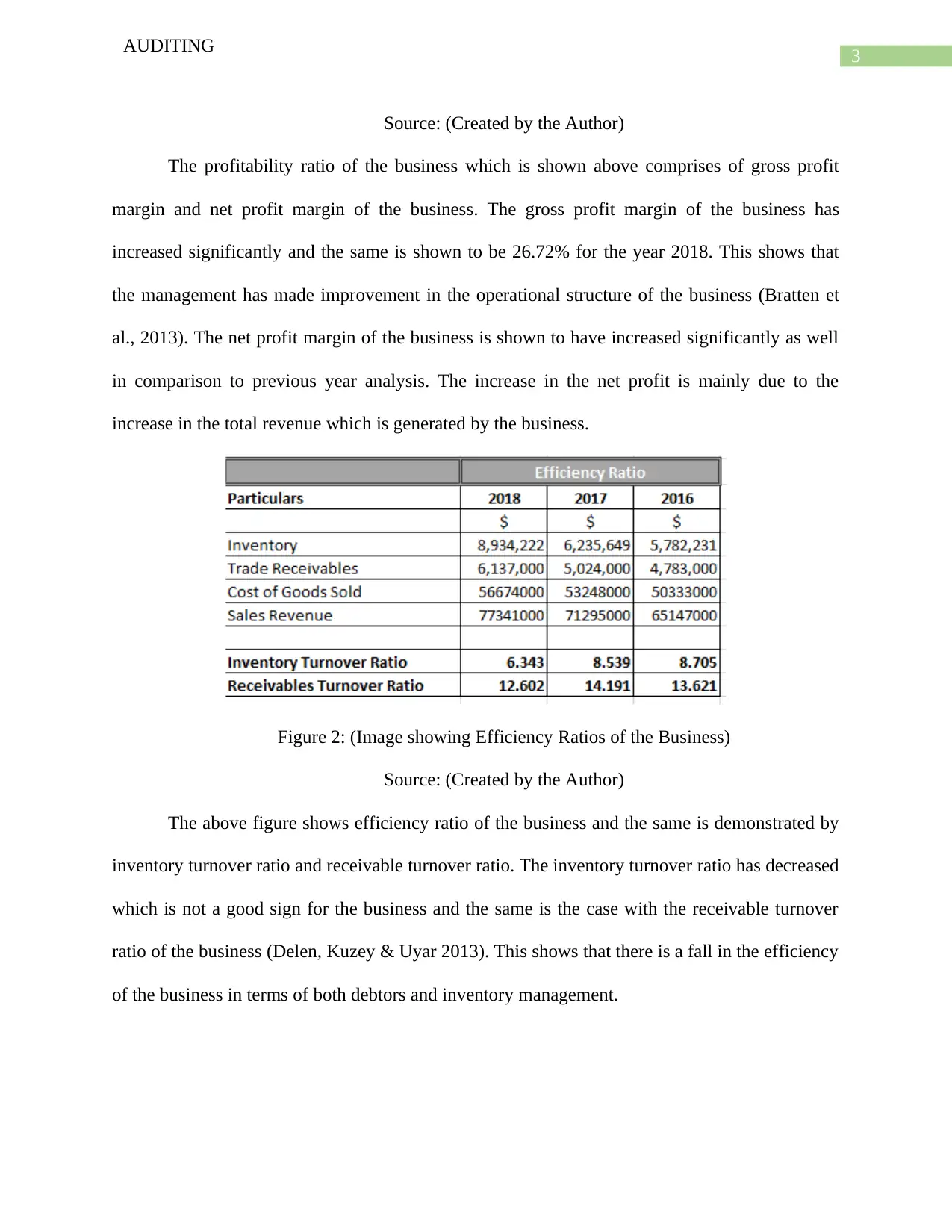

Figure 3: (Image showing Liquidity Ratios of the Business)

Source: (Created by the Author)

The above table shows liquidity ratio which comprises of current ratio and quick ratio of

the business. These ratios are considered to be financial indicators for overall success of the

business. The current ratio of the business has improved slightly while there is a fall in the quick

ratio of the business. The current ratio of the business is shown to be 1.354 for the business and

this shows that the business is maintaining the level of liquidity of the business.

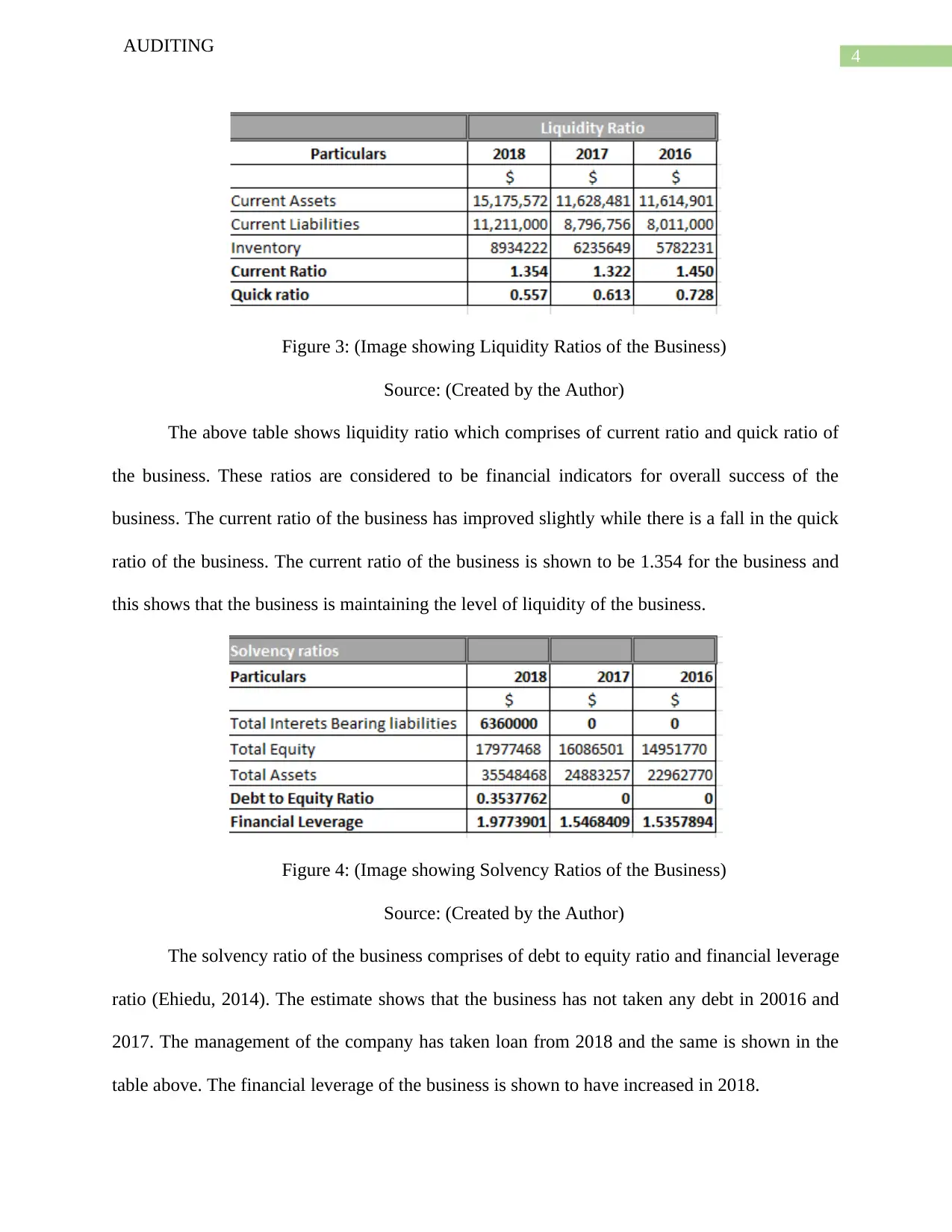

Figure 4: (Image showing Solvency Ratios of the Business)

Source: (Created by the Author)

The solvency ratio of the business comprises of debt to equity ratio and financial leverage

ratio (Ehiedu, 2014). The estimate shows that the business has not taken any debt in 20016 and

2017. The management of the company has taken loan from 2018 and the same is shown in the

table above. The financial leverage of the business is shown to have increased in 2018.

AUDITING

Figure 3: (Image showing Liquidity Ratios of the Business)

Source: (Created by the Author)

The above table shows liquidity ratio which comprises of current ratio and quick ratio of

the business. These ratios are considered to be financial indicators for overall success of the

business. The current ratio of the business has improved slightly while there is a fall in the quick

ratio of the business. The current ratio of the business is shown to be 1.354 for the business and

this shows that the business is maintaining the level of liquidity of the business.

Figure 4: (Image showing Solvency Ratios of the Business)

Source: (Created by the Author)

The solvency ratio of the business comprises of debt to equity ratio and financial leverage

ratio (Ehiedu, 2014). The estimate shows that the business has not taken any debt in 20016 and

2017. The management of the company has taken loan from 2018 and the same is shown in the

table above. The financial leverage of the business is shown to have increased in 2018.

5

AUDITING

Key Inherent Risks of the business

The business of Top Fashion Warehouse is engaged in the business of manufacturing

fashions products for the customers and also meet the fashion requirements of the business. The

business also faces certain risks in operations of the business. Inherent risks of the business are

categorised as the risks which arises from omission and material misstatement of the business.

The inherent risks can be recognised from the process of audit.

In the case of Top Fashion Warehouse, the financial statement shows that there has been

significant fluctuations in the balance of inventory and cash of the business. There has been

significant increase in the value of inventory as shown in the balance sheet of the company. The

inventory of the business is unique and therefore an increase in the same with such a magnitude

indicate certain inherent risks that there might be material misstatement in the reporting process

for the same (Hadjimichael & Hegland, 2016). The inventory balance is shown to be $ 8,934,222

which is significantly more than the previous year figures. The auditor needs to ensure that the

valuation of inventory is appropriately done without any discrepancies so that the business can

ensure full disclosures of the same (Jha and Chen 2014). Another account which shows a

significant decrease in 20018 is cash account of the business. The cash balance of the business

has decreased on a consistent basis and the value for the same in 2018 is shown to be $ 424,350.

The cash account shows significant decline and therefore, there might be certain inherent risks

that there might be some omission or misstatement in the reporting process.

Four Accounts which are at Risk

The financial statement of Top Fashion Warehouse and analysis of key financial ratios

are considered for the purpose of identifying the accounts which are at risks. The accounts which

are recognised as being risky are listed below in details:

AUDITING

Key Inherent Risks of the business

The business of Top Fashion Warehouse is engaged in the business of manufacturing

fashions products for the customers and also meet the fashion requirements of the business. The

business also faces certain risks in operations of the business. Inherent risks of the business are

categorised as the risks which arises from omission and material misstatement of the business.

The inherent risks can be recognised from the process of audit.

In the case of Top Fashion Warehouse, the financial statement shows that there has been

significant fluctuations in the balance of inventory and cash of the business. There has been

significant increase in the value of inventory as shown in the balance sheet of the company. The

inventory of the business is unique and therefore an increase in the same with such a magnitude

indicate certain inherent risks that there might be material misstatement in the reporting process

for the same (Hadjimichael & Hegland, 2016). The inventory balance is shown to be $ 8,934,222

which is significantly more than the previous year figures. The auditor needs to ensure that the

valuation of inventory is appropriately done without any discrepancies so that the business can

ensure full disclosures of the same (Jha and Chen 2014). Another account which shows a

significant decrease in 20018 is cash account of the business. The cash balance of the business

has decreased on a consistent basis and the value for the same in 2018 is shown to be $ 424,350.

The cash account shows significant decline and therefore, there might be certain inherent risks

that there might be some omission or misstatement in the reporting process.

Four Accounts which are at Risk

The financial statement of Top Fashion Warehouse and analysis of key financial ratios

are considered for the purpose of identifying the accounts which are at risks. The accounts which

are recognised as being risky are listed below in details:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

Cash Account: The cash account of the business shows that there has been significant

decrease in the cash balance of the business. The fall in cash balance suggest that the

management has undertaken some project which the auditor needs to ensure. There might be

a significant risk that there might be a misstatement in the annual reports. The auditor of the

business needs to check the cash balance as the liquidity of the business is falling.

Inventory: Another account which is identified to be at risk is inventory account of the

business. The inventory is general circumstances is most open to risks of misstatement and

omission. The auditor needs to appropriately value the same in order to ensure that the value

which is shown in the financial statement are appropriate in nature (Ho & Kang, 2013). The

value of the inventory has shown a tremendous increase in comparison to previous year and

the auditor needs to ensure that the balances which is shown for the inventory are genuine in

nature.

Property, Plant and Equipment: The value for property, plant and equipment is shown to be

$ 17,589,254 in 2018 and the amount is shown to have significantly increased in comparison

to previous year analysis. The auditor needs to check whether the balances which is shown in

the balance are appropriate in nature and also whether appropriate amount of depreciation is

charged by the business.

Intangible Assets: The intangible assets of the business are shown in the balance sheet of the

business. The auditor of the business needs to check whether the valuation of the intangible

assets is shown appropriately in the balance sheet. As per 2018 estimates, the intangible

assets of the business are shown to be nil which suggest that the management has sold off the

intangible assets of the business.

AUDITING

Cash Account: The cash account of the business shows that there has been significant

decrease in the cash balance of the business. The fall in cash balance suggest that the

management has undertaken some project which the auditor needs to ensure. There might be

a significant risk that there might be a misstatement in the annual reports. The auditor of the

business needs to check the cash balance as the liquidity of the business is falling.

Inventory: Another account which is identified to be at risk is inventory account of the

business. The inventory is general circumstances is most open to risks of misstatement and

omission. The auditor needs to appropriately value the same in order to ensure that the value

which is shown in the financial statement are appropriate in nature (Ho & Kang, 2013). The

value of the inventory has shown a tremendous increase in comparison to previous year and

the auditor needs to ensure that the balances which is shown for the inventory are genuine in

nature.

Property, Plant and Equipment: The value for property, plant and equipment is shown to be

$ 17,589,254 in 2018 and the amount is shown to have significantly increased in comparison

to previous year analysis. The auditor needs to check whether the balances which is shown in

the balance are appropriate in nature and also whether appropriate amount of depreciation is

charged by the business.

Intangible Assets: The intangible assets of the business are shown in the balance sheet of the

business. The auditor of the business needs to check whether the valuation of the intangible

assets is shown appropriately in the balance sheet. As per 2018 estimates, the intangible

assets of the business are shown to be nil which suggest that the management has sold off the

intangible assets of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

Key Assertions

The key assertions which can be provided from the analysis of the risks for the accounts

are cash, plant and machinery, intangibles assets and inventory. The cash balance of the business

is shown to have declined in comparison to previous year’s analysis and this shows that there is a

fall in the liquidity of the business while the analysis of the current ratio show that the liquidity

has improved slightly (Islam, 2014). The auditor needs to assess the cash management process of

the business as there is scope for misappropriation of cash and apply appropriate vouching

practices in the business.

The value of property, plant and equipment needs to assessed by the auditor whether the

same are showing genuine results or not. The value of property, plant and equipment is shown to

have increased which suggest that the management of the company has made purchases and the

auditor needs to check whether the same are actual or not.

In case of inventory, the balances have shown a tremendous rise which can suggest that

the management of the company is planning to enhance the scale of operations of the business.

However, there is a risk that the balance of inventory might be misrepresented in the balance

sheet. The auditor needs to verify with the store ledgers and in case the need arises switch to

physical taking of the stock to ensure that the value for the same is appropriately represented.’

The intangible assets of the business are shown to be nil in 2018 which signifies that the

management has sold off whatever intangible assets which the company owned. The auditor

needs to check whether the same is true or not. The auditor can use the assistance of an expert to

ensure that the intangible assets are appropriately valued.

AUDITING

Key Assertions

The key assertions which can be provided from the analysis of the risks for the accounts

are cash, plant and machinery, intangibles assets and inventory. The cash balance of the business

is shown to have declined in comparison to previous year’s analysis and this shows that there is a

fall in the liquidity of the business while the analysis of the current ratio show that the liquidity

has improved slightly (Islam, 2014). The auditor needs to assess the cash management process of

the business as there is scope for misappropriation of cash and apply appropriate vouching

practices in the business.

The value of property, plant and equipment needs to assessed by the auditor whether the

same are showing genuine results or not. The value of property, plant and equipment is shown to

have increased which suggest that the management of the company has made purchases and the

auditor needs to check whether the same are actual or not.

In case of inventory, the balances have shown a tremendous rise which can suggest that

the management of the company is planning to enhance the scale of operations of the business.

However, there is a risk that the balance of inventory might be misrepresented in the balance

sheet. The auditor needs to verify with the store ledgers and in case the need arises switch to

physical taking of the stock to ensure that the value for the same is appropriately represented.’

The intangible assets of the business are shown to be nil in 2018 which signifies that the

management has sold off whatever intangible assets which the company owned. The auditor

needs to check whether the same is true or not. The auditor can use the assistance of an expert to

ensure that the intangible assets are appropriately valued.

8

AUDITING

Conclusion

The above discussion effectively identifies the key risks which are associated with the

financial statement of Top Fashion Warehouse. The major risks which is identified in the

financial statements are cash, plant and machinery, intangible assets and inventory. The

assessment also shows computation and analysis of key financial ratios of the business. The

ratios are computed to analyse the performance of the business and also identify the areas where

the business might be facing significant risks.

AUDITING

Conclusion

The above discussion effectively identifies the key risks which are associated with the

financial statement of Top Fashion Warehouse. The major risks which is identified in the

financial statements are cash, plant and machinery, intangible assets and inventory. The

assessment also shows computation and analysis of key financial ratios of the business. The

ratios are computed to analyse the performance of the business and also identify the areas where

the business might be facing significant risks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

Reference

Bratten, B., Gaynor, L.M., McDaniel, L., Montague, N.R. & Sierra, G.E., (2013). The audit of

fair values and other estimates: The effects of underlying environmental, task, and

auditor-specific factors. Auditing: A Journal of Practice & Theory, 32(sp1), pp.7-44.

Coetzee, P. & Lubbe, D. (2014). Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Delen, D., Kuzey, C. and Uyar, A., (2013). Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Ehiedu, V. C. (2014). The impact of liquidity on profitability of some selected companies: the

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), 81-90.

Hadjimichael, M. & Hegland, T.J., (2016). Really sustainable? Inherent risks of eco-labeling in

fisheries. Fisheries research, 174, pp.129-135.

Ho, J.L. and Kang, F., (2013). Auditor choice and audit fees in family firms: Evidence from the

S&P 1500. Auditing: A Journal of Practice & Theory, 32(4), pp.71-93.

Islam, M. A. (2014). An analysis of the financial performance of national bank limited using

financial ratio. Journal of Behavioural Economics, Finance, Entrepreneurship,

Accounting and Transport, 2(5), 121-129.

Jha, A. & Chen, Y., (2014). Audit fees and social capital. The Accounting Review, 90(2), pp.611-

639.

AUDITING

Reference

Bratten, B., Gaynor, L.M., McDaniel, L., Montague, N.R. & Sierra, G.E., (2013). The audit of

fair values and other estimates: The effects of underlying environmental, task, and

auditor-specific factors. Auditing: A Journal of Practice & Theory, 32(sp1), pp.7-44.

Coetzee, P. & Lubbe, D. (2014). Improving the efficiency and effectiveness of risk‐based

internal audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Delen, D., Kuzey, C. and Uyar, A., (2013). Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Ehiedu, V. C. (2014). The impact of liquidity on profitability of some selected companies: the

financial statement analysis (FSA) approach. Research Journal of Finance and

Accounting, 5(5), 81-90.

Hadjimichael, M. & Hegland, T.J., (2016). Really sustainable? Inherent risks of eco-labeling in

fisheries. Fisheries research, 174, pp.129-135.

Ho, J.L. and Kang, F., (2013). Auditor choice and audit fees in family firms: Evidence from the

S&P 1500. Auditing: A Journal of Practice & Theory, 32(4), pp.71-93.

Islam, M. A. (2014). An analysis of the financial performance of national bank limited using

financial ratio. Journal of Behavioural Economics, Finance, Entrepreneurship,

Accounting and Transport, 2(5), 121-129.

Jha, A. & Chen, Y., (2014). Audit fees and social capital. The Accounting Review, 90(2), pp.611-

639.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.