Management Accounting Report: 4com PLC Financial Performance

VerifiedAdded on 2020/06/06

|17

|5299

|311

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within 4com PLC. It begins with an introduction to management accounting, highlighting its role in making businesses sustainable and compatible, and emphasizes the use of management reports for financial and cost-related information. The report then explores various management accounting systems, including inventory management, price optimization, job costing, and cost accounting systems (including job costing, process costing, standard costing). It also details the essentials of management accounting, such as decision-making, planning, and efficiency enhancement, along with the importance of producing profit/loss or income statements. The report includes details of the 4com PLC’s financial reporting through various reports, such as budget reports, variance analysis reports, performance reports, job costing reports, and inventory control reports, discussing their significance. Challenges in management reporting are also considered. Overall, the report provides insights into how management accounting supports financial stability, performance evaluation, and strategic decision-making within 4com PLC.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

P1............................................................................................................................................1

P2............................................................................................................................................3

M1: ........................................................................................................................................5

D1:..........................................................................................................................................5

P3............................................................................................................................................5

M2: ........................................................................................................................................1

D2: .........................................................................................................................................1

P4............................................................................................................................................1

P5............................................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

P1............................................................................................................................................1

P2............................................................................................................................................3

M1: ........................................................................................................................................5

D1:..........................................................................................................................................5

P3............................................................................................................................................5

M2: ........................................................................................................................................1

D2: .........................................................................................................................................1

P4............................................................................................................................................1

P5............................................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

Management accounting is the broad managerial aspect which is needed to be prepared

by the management of the company in order to, make the business sustainable and compatible.

This assist the firm to make the business prosperous and developed (Baldvinsdottir, Mitchell and

Nørreklit, 2010). With the help of management report, anyone can know about the financial and

other cost related information about the company. Normally, financial statement of Next plc is

used for the individuals' who are directly or indirectly concerned with the operations of the

company. But, management accounting system is used by the cited firm's internal management

for effective management. Management accounting is used by the management. Management

accounting comprises of cash details, sales revenue generated, debtors, creditors, stock, raw

material and additional covers trends charts.

In management report, information of 4com company is provided and planning tools of

management are discussed in details for stabilization of financial position of the cited firm.

Management accounting also helps the firm to solve the financial problems so that the firm could

easily obtain its objectives.

PART A

P1

This is totally related to making reports which is concerned to the internal management.

This is the process of determining, assessing and recording and summarizing information (Bodie,

2013). To frame the decisions, there is a strong requirement of the 4com company to know the

management accounting reports so that the resources can be efficiently utilized. This system

helps in managing entire cost of the cited company and enhancing productivity and revenues of

the firm. It additionally controls day to day affairs of the cited firm. Management accounting

assist in making the business grow. There are so many kinds of management accounting systems. Inventory management system: This system is implemented for monitoring of inventory

or stock items. Under this management system, whole inventory of a company can be

managed and this would lead to provide a smooth functioning of the firm. With the help

of this system, 4com can use its raw material in an optimum manner. This will also assist

in monitoring the flow of inventory from the manufacturer to the retailers.

1

Management accounting is the broad managerial aspect which is needed to be prepared

by the management of the company in order to, make the business sustainable and compatible.

This assist the firm to make the business prosperous and developed (Baldvinsdottir, Mitchell and

Nørreklit, 2010). With the help of management report, anyone can know about the financial and

other cost related information about the company. Normally, financial statement of Next plc is

used for the individuals' who are directly or indirectly concerned with the operations of the

company. But, management accounting system is used by the cited firm's internal management

for effective management. Management accounting is used by the management. Management

accounting comprises of cash details, sales revenue generated, debtors, creditors, stock, raw

material and additional covers trends charts.

In management report, information of 4com company is provided and planning tools of

management are discussed in details for stabilization of financial position of the cited firm.

Management accounting also helps the firm to solve the financial problems so that the firm could

easily obtain its objectives.

PART A

P1

This is totally related to making reports which is concerned to the internal management.

This is the process of determining, assessing and recording and summarizing information (Bodie,

2013). To frame the decisions, there is a strong requirement of the 4com company to know the

management accounting reports so that the resources can be efficiently utilized. This system

helps in managing entire cost of the cited company and enhancing productivity and revenues of

the firm. It additionally controls day to day affairs of the cited firm. Management accounting

assist in making the business grow. There are so many kinds of management accounting systems. Inventory management system: This system is implemented for monitoring of inventory

or stock items. Under this management system, whole inventory of a company can be

managed and this would lead to provide a smooth functioning of the firm. With the help

of this system, 4com can use its raw material in an optimum manner. This will also assist

in monitoring the flow of inventory from the manufacturer to the retailers.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price optimization system: Under this system, the price of the company is determined

after considering total cost which are covered while producing goods. Prices are needed

to be decided in such a manner that could lead to produce higher profits and that could

also be affordable by the consumers. Under this, an analysis is framed to identify about

the responses from consumers on various prices of the products. The main objective of

this concept is to reach at price which is most favourable to the cited organisation. Job costing: This costing method is used for examining cost covered in any specified job

which is being performed in certain production process of certain special products. Job

costing is used to determine the cost involved in any particular work specified by

customers. This method of costing is used by such organisations where every job is

particularly different and being done with specifications given by clients.

Cost accounting system: This is being used by a company to ascertain total cost incurred

in different activities for producing goods of organisation. This analysis is being used for

profitability analysis of an organisation and it helps in controlling cost of company. After

analysing cost of all the activities it can be evaluated that which items of cost are vital

and which are of no use and increasing cost unnecessarily. Cost accounting system is

utilised in ascertaining value of raw material, work in progress and final product. This all

information collected by using this system are utilised in preparing financial accounts of

a company (Burritt, and et. al, 2011). Cost accounting system is further divided into 2

parts. These are job costing and process costing. Process costing is being used in such

organisations where manufacturing of a product is done by different processes.

Standard costing: It is based on estimations which is related with operational activities,

thus people can develop items effectively under the normal circumstances. Along with

this, it can be utilized on the basis of target and additionally can be created with

assistance of historical information. It is always different from actual price, at each and

every circumstances will be linked with unpredictable elements. There are two methods

of this costing, such as LIFO and FIFO.

Types of standard costing:

Ideal standards:Cost settled those depend on perfect conditions. It is illustrative for long

haul objectives with greatest effectiveness.

2

after considering total cost which are covered while producing goods. Prices are needed

to be decided in such a manner that could lead to produce higher profits and that could

also be affordable by the consumers. Under this, an analysis is framed to identify about

the responses from consumers on various prices of the products. The main objective of

this concept is to reach at price which is most favourable to the cited organisation. Job costing: This costing method is used for examining cost covered in any specified job

which is being performed in certain production process of certain special products. Job

costing is used to determine the cost involved in any particular work specified by

customers. This method of costing is used by such organisations where every job is

particularly different and being done with specifications given by clients.

Cost accounting system: This is being used by a company to ascertain total cost incurred

in different activities for producing goods of organisation. This analysis is being used for

profitability analysis of an organisation and it helps in controlling cost of company. After

analysing cost of all the activities it can be evaluated that which items of cost are vital

and which are of no use and increasing cost unnecessarily. Cost accounting system is

utilised in ascertaining value of raw material, work in progress and final product. This all

information collected by using this system are utilised in preparing financial accounts of

a company (Burritt, and et. al, 2011). Cost accounting system is further divided into 2

parts. These are job costing and process costing. Process costing is being used in such

organisations where manufacturing of a product is done by different processes.

Standard costing: It is based on estimations which is related with operational activities,

thus people can develop items effectively under the normal circumstances. Along with

this, it can be utilized on the basis of target and additionally can be created with

assistance of historical information. It is always different from actual price, at each and

every circumstances will be linked with unpredictable elements. There are two methods

of this costing, such as LIFO and FIFO.

Types of standard costing:

Ideal standards:Cost settled those depend on perfect conditions. It is illustrative for long

haul objectives with greatest effectiveness.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Attainable standards:It is connected with organization condition that what can be

achieved through the current conditions.

Current standards: These are here and now in nature and for the most part utilized for

control reason. It is for the most part related with that state which business is by and by

working or binds to accomplish.

Advantages:

Standard are set keeping in mind the end goal to gave standard against which real

expenses are identified with find out real execution.

It helps to break down differences that are help to a person out wastefulness and moved

those people those are responsible for antagonistic fluctuations.

Disadvantages:

If there should be an occurrence of little concern it can not be pertinent on the grounds

that it require high level of aptitudes.

Types of variances:

Direct material variance: It is the connection among real cost of material at real units

and standard cost of material of standard units. It is total of material cost and material

amount.

Labour variance: It is connected with the cost of work. It is contrasts among standard

costing of work for the real human activity and the genuine cost caused on work.

Overhead variances: This is the variance which is related to the indirect costs that are

linked with production of the company.

Sales variance: This is the sales variance that are related to the actual sales and standard

sales.

Following are some of essentials of management accounting systems:

Decision making: Decisions are made by upper level or strategic level management for

welfare of the whole company. Internal management use these information systems in

taking decisions regarding business activities. These decisions are made to control costs

of organisation and control extra expenses involved in manufacturing process. Make or

buy decisions are also made by using these systems.

Planning: Effective and appropriate strategies and plans are made by company after

considering these information tools. These strategies are regarding monitoring costs and

3

achieved through the current conditions.

Current standards: These are here and now in nature and for the most part utilized for

control reason. It is for the most part related with that state which business is by and by

working or binds to accomplish.

Advantages:

Standard are set keeping in mind the end goal to gave standard against which real

expenses are identified with find out real execution.

It helps to break down differences that are help to a person out wastefulness and moved

those people those are responsible for antagonistic fluctuations.

Disadvantages:

If there should be an occurrence of little concern it can not be pertinent on the grounds

that it require high level of aptitudes.

Types of variances:

Direct material variance: It is the connection among real cost of material at real units

and standard cost of material of standard units. It is total of material cost and material

amount.

Labour variance: It is connected with the cost of work. It is contrasts among standard

costing of work for the real human activity and the genuine cost caused on work.

Overhead variances: This is the variance which is related to the indirect costs that are

linked with production of the company.

Sales variance: This is the sales variance that are related to the actual sales and standard

sales.

Following are some of essentials of management accounting systems:

Decision making: Decisions are made by upper level or strategic level management for

welfare of the whole company. Internal management use these information systems in

taking decisions regarding business activities. These decisions are made to control costs

of organisation and control extra expenses involved in manufacturing process. Make or

buy decisions are also made by using these systems.

Planning: Effective and appropriate strategies and plans are made by company after

considering these information tools. These strategies are regarding monitoring costs and

3

maximising revenues of enterprise. These are used for achieving long term goals of

company.

Increment in Efficiency: These information systems are used by company to control and

monitor routine activities and enhancing efficiency of the firm. After determining the

cost, efficient decisions are formulated in relation to the managing costs and enhancing

productivity of the organisation and attaining firms’ goals of optimizing revenues and

satisfying consumers. These accounting systems renders information to managers that

reflects financial stability of the cited firm.

P2

Mostly organizations require the management accountant to produce profit/loss or

income statement. One of company is 4com PLC which hold a small business. Accounting

reports shows all kind of information data related to business (Garrison, and et. al, 2010). These

reports are made by 4com PLC company’s accountant or internal management system. A

monthly management account's report not only show income statement but also reveal many

kinds of other information. 4Com PLC company's Reports can be generated monthly, quarterly

or yearly. 4Com PLC Company's revenue can be seen by account manager. These reports consist

different kind of data, reports and figures of organization which help to growth 4com PLC

company's business.

These reports of 4com PLC company also help the manager to see company's

performance and making affective strategies for organization. These can help in controlling cost

and achieving goals as well. Budget reports, variance analysis report, performance reports, job

costing reports, inventory control reports are reports which analyse 4com PLC company's

performance. This work is done by 4com PLC company's manager. following details are in brief:

-

Budget report: - Budget reports are prepared by 4com PLC company's manager to see

actual performance of company. Manager compares actual performance of 4com PLC

company to the expected target achieved by 4com PLC. Employees achieve incentives

through budget report which is managed by managers of 4com PLC. This help the

manager to see the performance of 4com PLC company and controlling cost. 4com PLC

Company's maximising profit is another target of company's manager.

4

company.

Increment in Efficiency: These information systems are used by company to control and

monitor routine activities and enhancing efficiency of the firm. After determining the

cost, efficient decisions are formulated in relation to the managing costs and enhancing

productivity of the organisation and attaining firms’ goals of optimizing revenues and

satisfying consumers. These accounting systems renders information to managers that

reflects financial stability of the cited firm.

P2

Mostly organizations require the management accountant to produce profit/loss or

income statement. One of company is 4com PLC which hold a small business. Accounting

reports shows all kind of information data related to business (Garrison, and et. al, 2010). These

reports are made by 4com PLC company’s accountant or internal management system. A

monthly management account's report not only show income statement but also reveal many

kinds of other information. 4Com PLC company's Reports can be generated monthly, quarterly

or yearly. 4Com PLC Company's revenue can be seen by account manager. These reports consist

different kind of data, reports and figures of organization which help to growth 4com PLC

company's business.

These reports of 4com PLC company also help the manager to see company's

performance and making affective strategies for organization. These can help in controlling cost

and achieving goals as well. Budget reports, variance analysis report, performance reports, job

costing reports, inventory control reports are reports which analyse 4com PLC company's

performance. This work is done by 4com PLC company's manager. following details are in brief:

-

Budget report: - Budget reports are prepared by 4com PLC company's manager to see

actual performance of company. Manager compares actual performance of 4com PLC

company to the expected target achieved by 4com PLC. Employees achieve incentives

through budget report which is managed by managers of 4com PLC. This help the

manager to see the performance of 4com PLC company and controlling cost. 4com PLC

Company's maximising profit is another target of company's manager.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Variance Analysis Report: - This Is different from budget report for 4com PLC.

Company's manager analyse and compare actual sales and budgeted sales of the company

by this report Company's manager compares expected data with actual data and evaluates

it through statistical tools, in this analytical report. It helps in finding fluctuation of

company's growth and reasons for the same so as to remove them. There are many type

of variances like sales mix, sales price variance etc.

Performance report: - This report is based on 4com PLC company's performance. These

measures operation and then performance of company. Generally, government body

prepares 4com PLC company's performance reports.

Job costing report: - 4com PLC company's manager prepare these reports. 4Com PLC

Company's manager controls cost involvement in a particular job in this report. These

reports show cost allocation to every work. Many strategies and plan works to minimise

cost and maximise profits. These reports are used to make strategies to minimise cost of

distributing the products.

Inventory Control Report: - These reports control stock position of 4com PLC

company. These reports show that how much stock has been sold and how much is

available for 4com PLC company. There are several methods like LIFO, FIFO etc,

methods of stock managements. Management of inventory is considered in this report. So

this very useful report. LIFO, FIFO methods follows Last In First Out and First in First

Out policy respectively. These are best policies are for 4com PLC company.

Financial strategies should be known for 4com PLC's manager. A balance sheet

is a picture of company's asset at a single point oftime (Herzig and et. al, 2012). The growth of

company can be mentioned in balance sheet or in management report. Every company has

different way to work in market. Strategies are also different. Account management reporting

work save more time and keep manage to all the things like budget of company cost, need of

employees, market strategies etc.

There are many challenges during management reporting. Reports can be complex, time

consuming etc. Manual nature of such kind of report is another problem of 4com PLC company.

5

Company's manager analyse and compare actual sales and budgeted sales of the company

by this report Company's manager compares expected data with actual data and evaluates

it through statistical tools, in this analytical report. It helps in finding fluctuation of

company's growth and reasons for the same so as to remove them. There are many type

of variances like sales mix, sales price variance etc.

Performance report: - This report is based on 4com PLC company's performance. These

measures operation and then performance of company. Generally, government body

prepares 4com PLC company's performance reports.

Job costing report: - 4com PLC company's manager prepare these reports. 4Com PLC

Company's manager controls cost involvement in a particular job in this report. These

reports show cost allocation to every work. Many strategies and plan works to minimise

cost and maximise profits. These reports are used to make strategies to minimise cost of

distributing the products.

Inventory Control Report: - These reports control stock position of 4com PLC

company. These reports show that how much stock has been sold and how much is

available for 4com PLC company. There are several methods like LIFO, FIFO etc,

methods of stock managements. Management of inventory is considered in this report. So

this very useful report. LIFO, FIFO methods follows Last In First Out and First in First

Out policy respectively. These are best policies are for 4com PLC company.

Financial strategies should be known for 4com PLC's manager. A balance sheet

is a picture of company's asset at a single point oftime (Herzig and et. al, 2012). The growth of

company can be mentioned in balance sheet or in management report. Every company has

different way to work in market. Strategies are also different. Account management reporting

work save more time and keep manage to all the things like budget of company cost, need of

employees, market strategies etc.

There are many challenges during management reporting. Reports can be complex, time

consuming etc. Manual nature of such kind of report is another problem of 4com PLC company.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M1:

According to the above mentioned accounting system which is more appropriate for the

company to manage and control their business operations. The advantages of this system would

help the cited company's to increase its productive and efficiency.

D1:

From the above accounting systems used by the company in order to maintain its

financial reporting and transaction. The overall financial stability and performance of the

company is depend upon the accounting system they are using in their businesses.

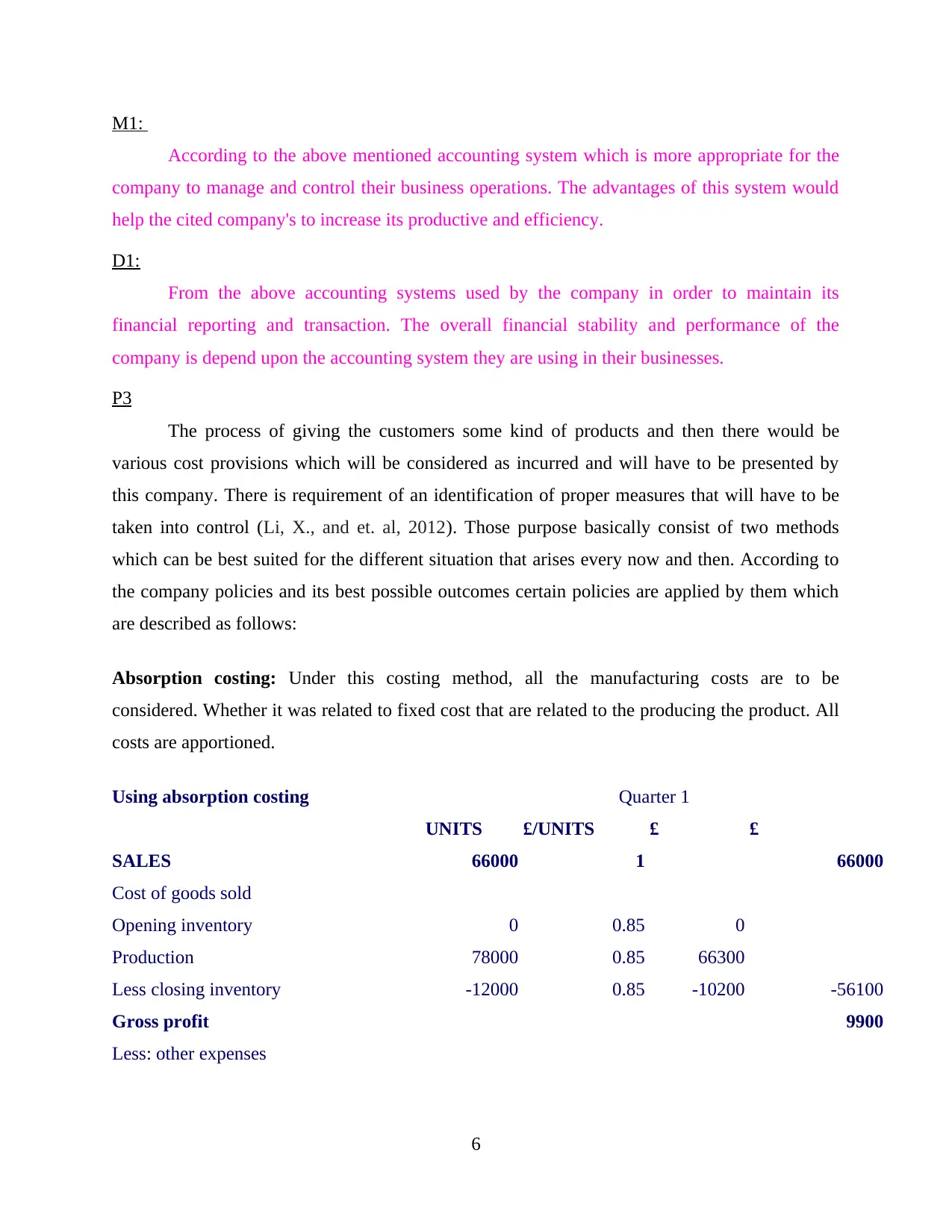

P3

The process of giving the customers some kind of products and then there would be

various cost provisions which will be considered as incurred and will have to be presented by

this company. There is requirement of an identification of proper measures that will have to be

taken into control (Li, X., and et. al, 2012). Those purpose basically consist of two methods

which can be best suited for the different situation that arises every now and then. According to

the company policies and its best possible outcomes certain policies are applied by them which

are described as follows:

Absorption costing: Under this costing method, all the manufacturing costs are to be

considered. Whether it was related to fixed cost that are related to the producing the product. All

costs are apportioned.

Using absorption costing Quarter 1

UNITS £/UNITS £ £

SALES 66000 1 66000

Cost of goods sold

Opening inventory 0 0.85 0

Production 78000 0.85 66300

Less closing inventory -12000 0.85 -10200 -56100

Gross profit 9900

Less: other expenses

6

According to the above mentioned accounting system which is more appropriate for the

company to manage and control their business operations. The advantages of this system would

help the cited company's to increase its productive and efficiency.

D1:

From the above accounting systems used by the company in order to maintain its

financial reporting and transaction. The overall financial stability and performance of the

company is depend upon the accounting system they are using in their businesses.

P3

The process of giving the customers some kind of products and then there would be

various cost provisions which will be considered as incurred and will have to be presented by

this company. There is requirement of an identification of proper measures that will have to be

taken into control (Li, X., and et. al, 2012). Those purpose basically consist of two methods

which can be best suited for the different situation that arises every now and then. According to

the company policies and its best possible outcomes certain policies are applied by them which

are described as follows:

Absorption costing: Under this costing method, all the manufacturing costs are to be

considered. Whether it was related to fixed cost that are related to the producing the product. All

costs are apportioned.

Using absorption costing Quarter 1

UNITS £/UNITS £ £

SALES 66000 1 66000

Cost of goods sold

Opening inventory 0 0.85 0

Production 78000 0.85 66300

Less closing inventory -12000 0.85 -10200 -56100

Gross profit 9900

Less: other expenses

6

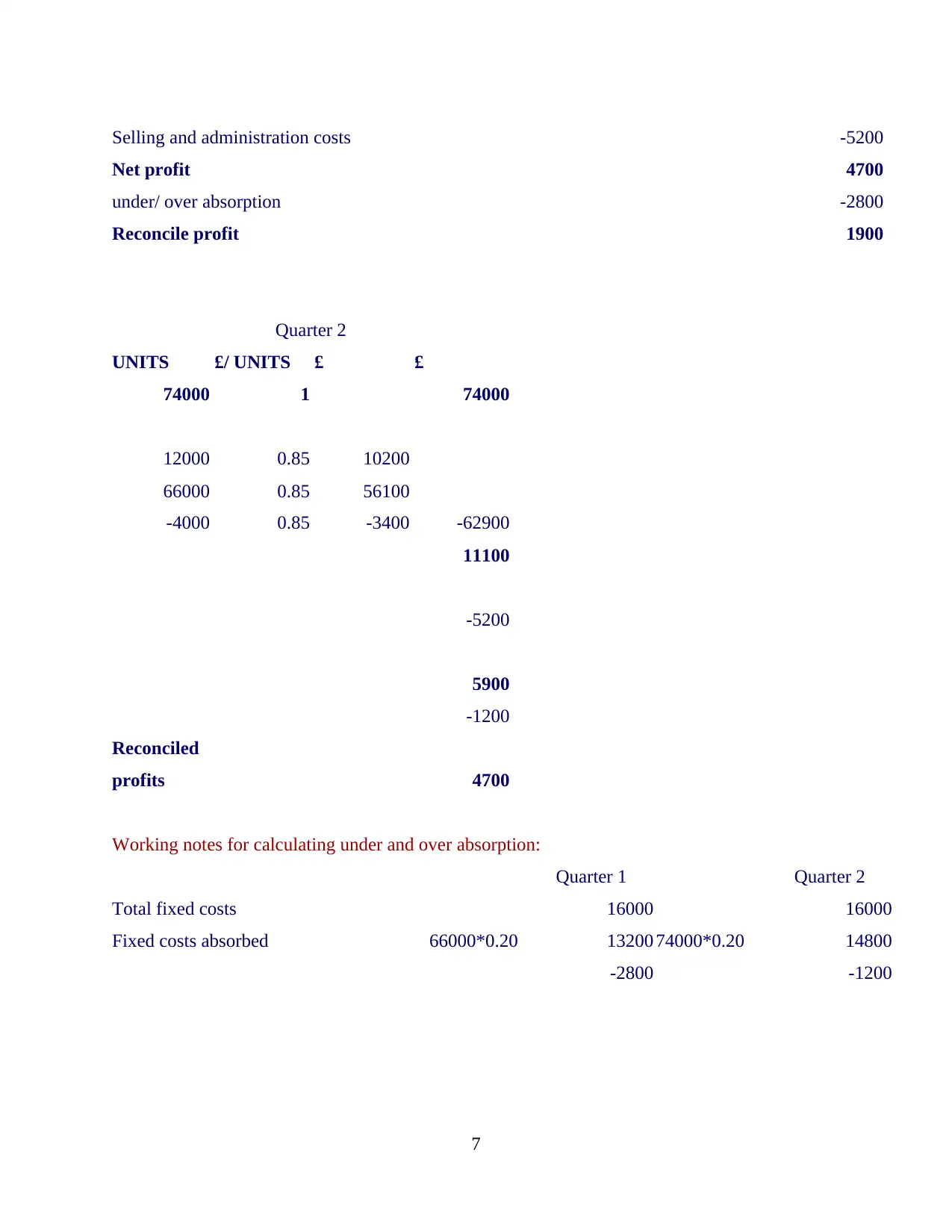

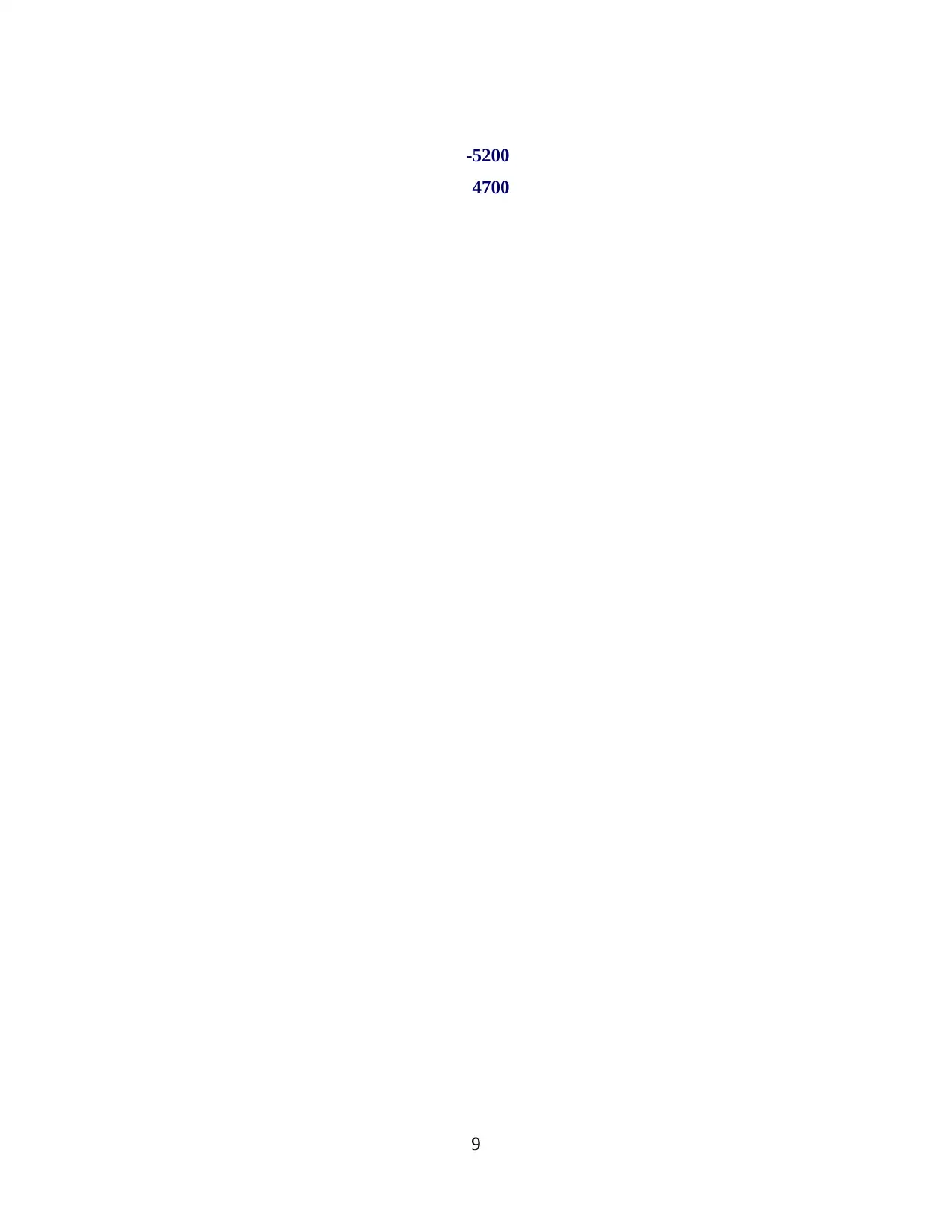

Selling and administration costs -5200

Net profit 4700

under/ over absorption -2800

Reconcile profit 1900

Quarter 2

UNITS £/ UNITS £ £

74000 1 74000

12000 0.85 10200

66000 0.85 56100

-4000 0.85 -3400 -62900

11100

-5200

5900

-1200

Reconciled

profits 4700

Working notes for calculating under and over absorption:

Quarter 1 Quarter 2

Total fixed costs 16000 16000

Fixed costs absorbed 66000*0.20 13200 74000*0.20 14800

-2800 -1200

7

Net profit 4700

under/ over absorption -2800

Reconcile profit 1900

Quarter 2

UNITS £/ UNITS £ £

74000 1 74000

12000 0.85 10200

66000 0.85 56100

-4000 0.85 -3400 -62900

11100

-5200

5900

-1200

Reconciled

profits 4700

Working notes for calculating under and over absorption:

Quarter 1 Quarter 2

Total fixed costs 16000 16000

Fixed costs absorbed 66000*0.20 13200 74000*0.20 14800

-2800 -1200

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

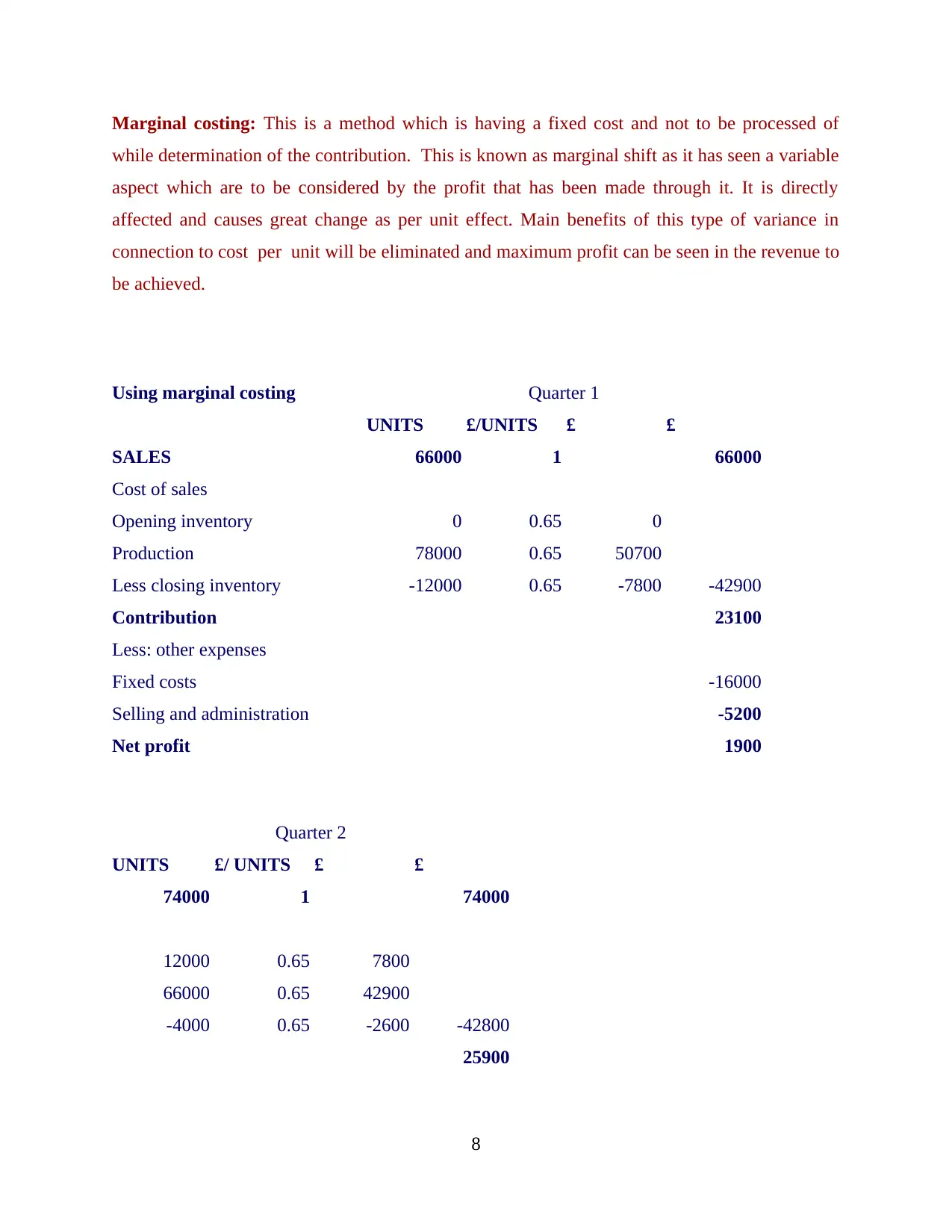

Marginal costing: This is a method which is having a fixed cost and not to be processed of

while determination of the contribution. This is known as marginal shift as it has seen a variable

aspect which are to be considered by the profit that has been made through it. It is directly

affected and causes great change as per unit effect. Main benefits of this type of variance in

connection to cost per unit will be eliminated and maximum profit can be seen in the revenue to

be achieved.

Using marginal costing Quarter 1

UNITS £/UNITS £ £

SALES 66000 1 66000

Cost of sales

Opening inventory 0 0.65 0

Production 78000 0.65 50700

Less closing inventory -12000 0.65 -7800 -42900

Contribution 23100

Less: other expenses

Fixed costs -16000

Selling and administration -5200

Net profit 1900

Quarter 2

UNITS £/ UNITS £ £

74000 1 74000

12000 0.65 7800

66000 0.65 42900

-4000 0.65 -2600 -42800

25900

8

while determination of the contribution. This is known as marginal shift as it has seen a variable

aspect which are to be considered by the profit that has been made through it. It is directly

affected and causes great change as per unit effect. Main benefits of this type of variance in

connection to cost per unit will be eliminated and maximum profit can be seen in the revenue to

be achieved.

Using marginal costing Quarter 1

UNITS £/UNITS £ £

SALES 66000 1 66000

Cost of sales

Opening inventory 0 0.65 0

Production 78000 0.65 50700

Less closing inventory -12000 0.65 -7800 -42900

Contribution 23100

Less: other expenses

Fixed costs -16000

Selling and administration -5200

Net profit 1900

Quarter 2

UNITS £/ UNITS £ £

74000 1 74000

12000 0.65 7800

66000 0.65 42900

-4000 0.65 -2600 -42800

25900

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

-5200

4700

9

4700

9

M2:

There are various range of accounting system can a company do have which they can

apply it in their business operations. Such as inventory management system and job costing

systems are more effective in evaluating the performance of the businesses.

D2:

As it was mentioned under the above scenario that company do have the option of both

absorption and marginal costing which can be use to evaluated the profitability of the company.

The one which provide more relevant results should be selected.

P4

Budgetary control is simply used to monitor and control costs of company and operations

also for any particular accounting year (Lukka and Modell, 2011). This procedure is undertaken

by an organisation to decide their goals and targets, after that various plans and strategies are

made to enhance performance of company and get actual results same as budgeted data.

Functions and operations are performed by a company in such manner that decided results can be

attained. This technique is used by internal management of any company so that wanted results

can be got and then actual data is compared with budgeted data and variances are found. After

that company takes reasonable steps to remove these differences. Following are some purposes

and objectives of budgetary control:Its main objective is to make coordination between all

resources available so the internal management which can utilise them properly.

To maintain standard in such manner that is required for all control systems.

Maintaining the costs and control as well as minimise them.

Provide guidelines and right path to manage all functions and operations of organisation.

Advantages:

Increased Efficiency: This technique of budgetary control is useful in increasing

efficiency of employees in any organisation. It is possible because it provides a path to all the

workers that what is to be done and how it is to be done. If efficiency will be increased then it

will automatically generate high profits for organisation.

There are various range of accounting system can a company do have which they can

apply it in their business operations. Such as inventory management system and job costing

systems are more effective in evaluating the performance of the businesses.

D2:

As it was mentioned under the above scenario that company do have the option of both

absorption and marginal costing which can be use to evaluated the profitability of the company.

The one which provide more relevant results should be selected.

P4

Budgetary control is simply used to monitor and control costs of company and operations

also for any particular accounting year (Lukka and Modell, 2011). This procedure is undertaken

by an organisation to decide their goals and targets, after that various plans and strategies are

made to enhance performance of company and get actual results same as budgeted data.

Functions and operations are performed by a company in such manner that decided results can be

attained. This technique is used by internal management of any company so that wanted results

can be got and then actual data is compared with budgeted data and variances are found. After

that company takes reasonable steps to remove these differences. Following are some purposes

and objectives of budgetary control:Its main objective is to make coordination between all

resources available so the internal management which can utilise them properly.

To maintain standard in such manner that is required for all control systems.

Maintaining the costs and control as well as minimise them.

Provide guidelines and right path to manage all functions and operations of organisation.

Advantages:

Increased Efficiency: This technique of budgetary control is useful in increasing

efficiency of employees in any organisation. It is possible because it provides a path to all the

workers that what is to be done and how it is to be done. If efficiency will be increased then it

will automatically generate high profits for organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.