6004LBSAF Taxation: Income Tax, NICs, and Self-Employment Analysis

VerifiedAdded on 2023/06/12

|17

|3204

|207

Report

AI Summary

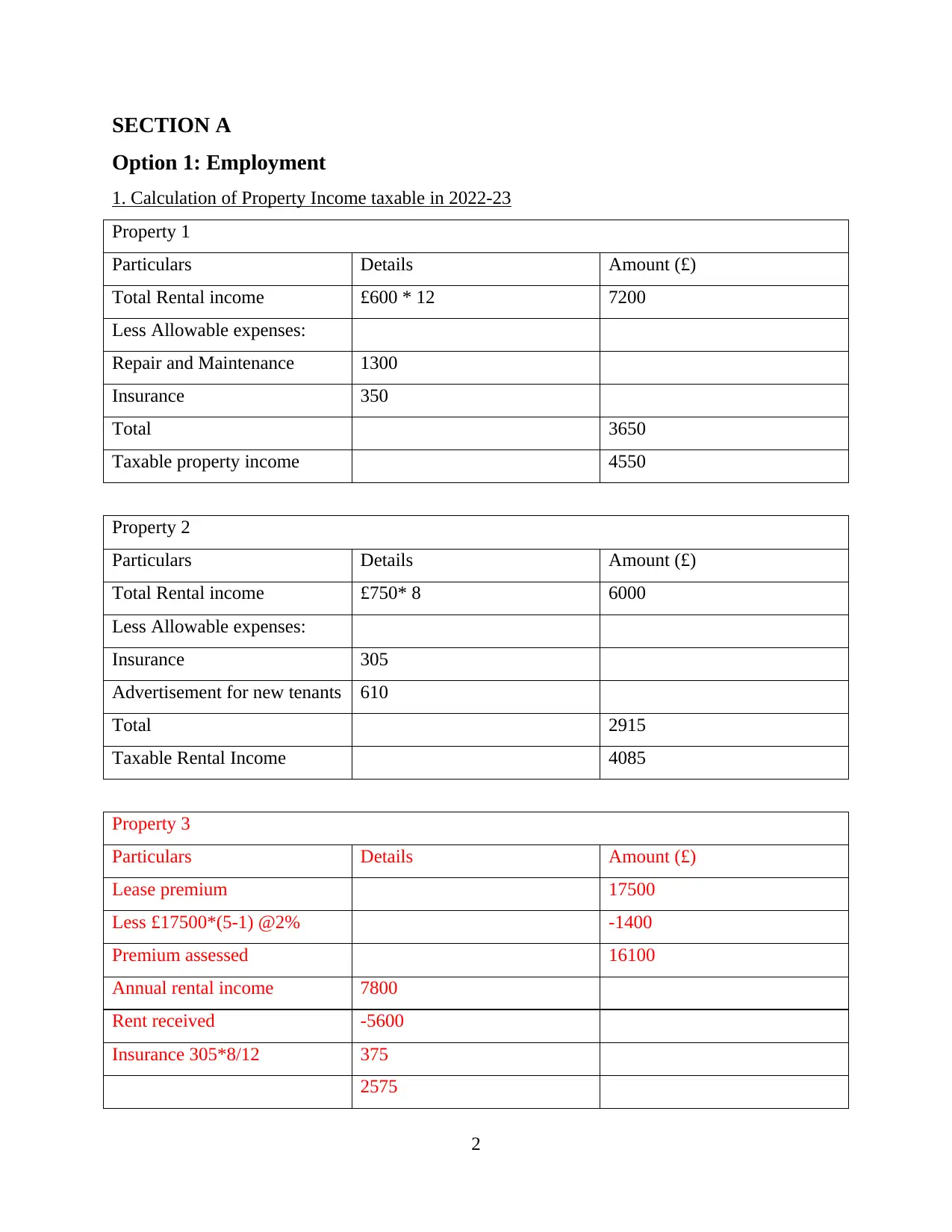

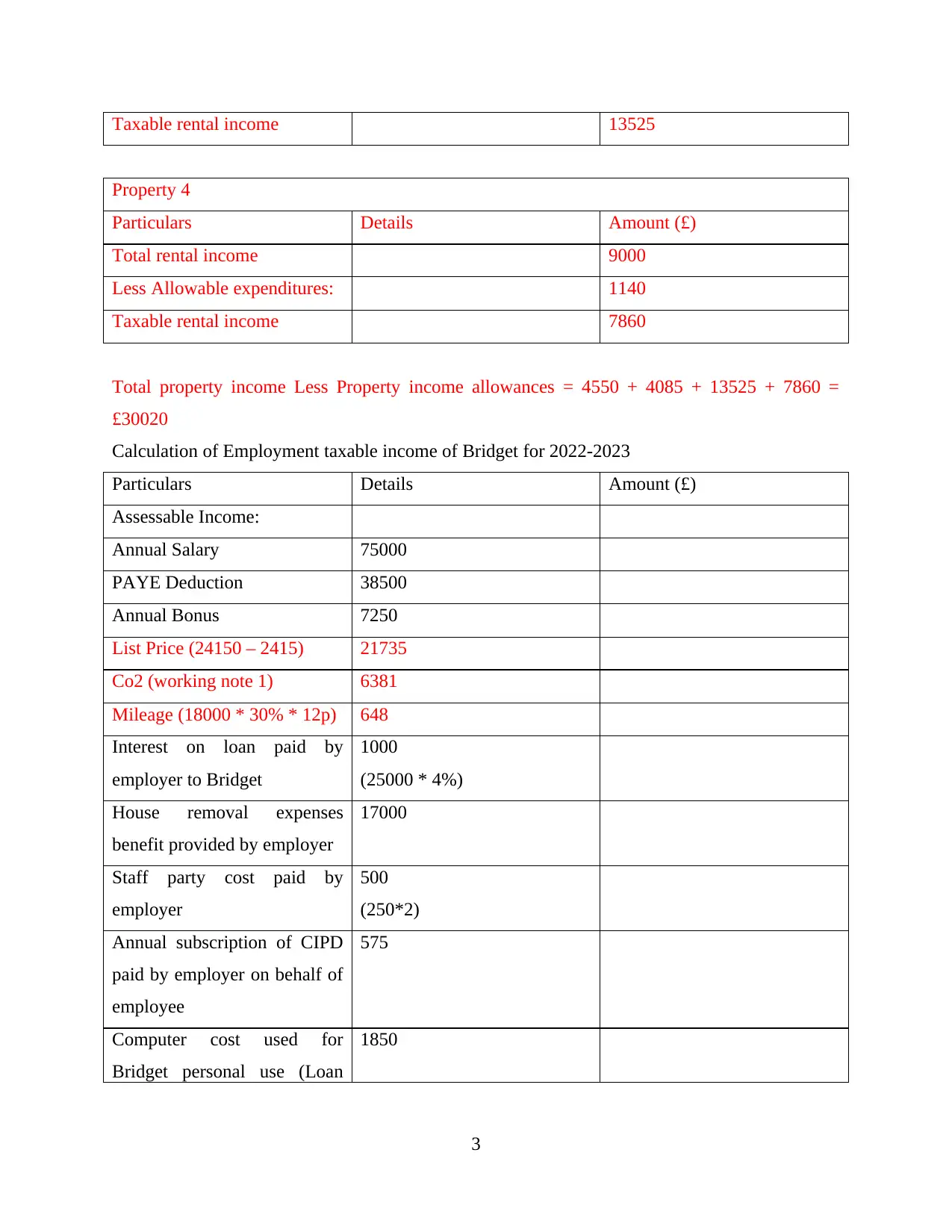

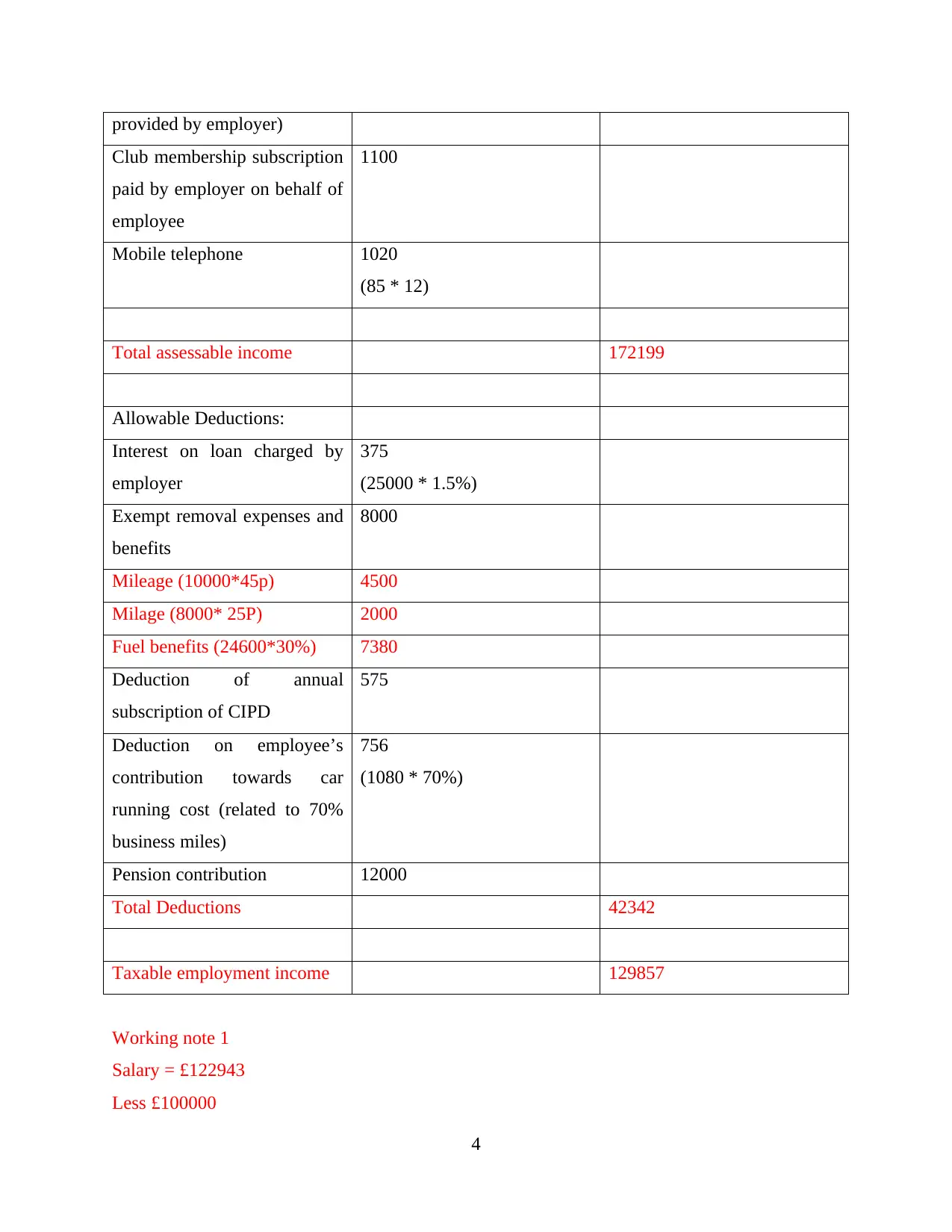

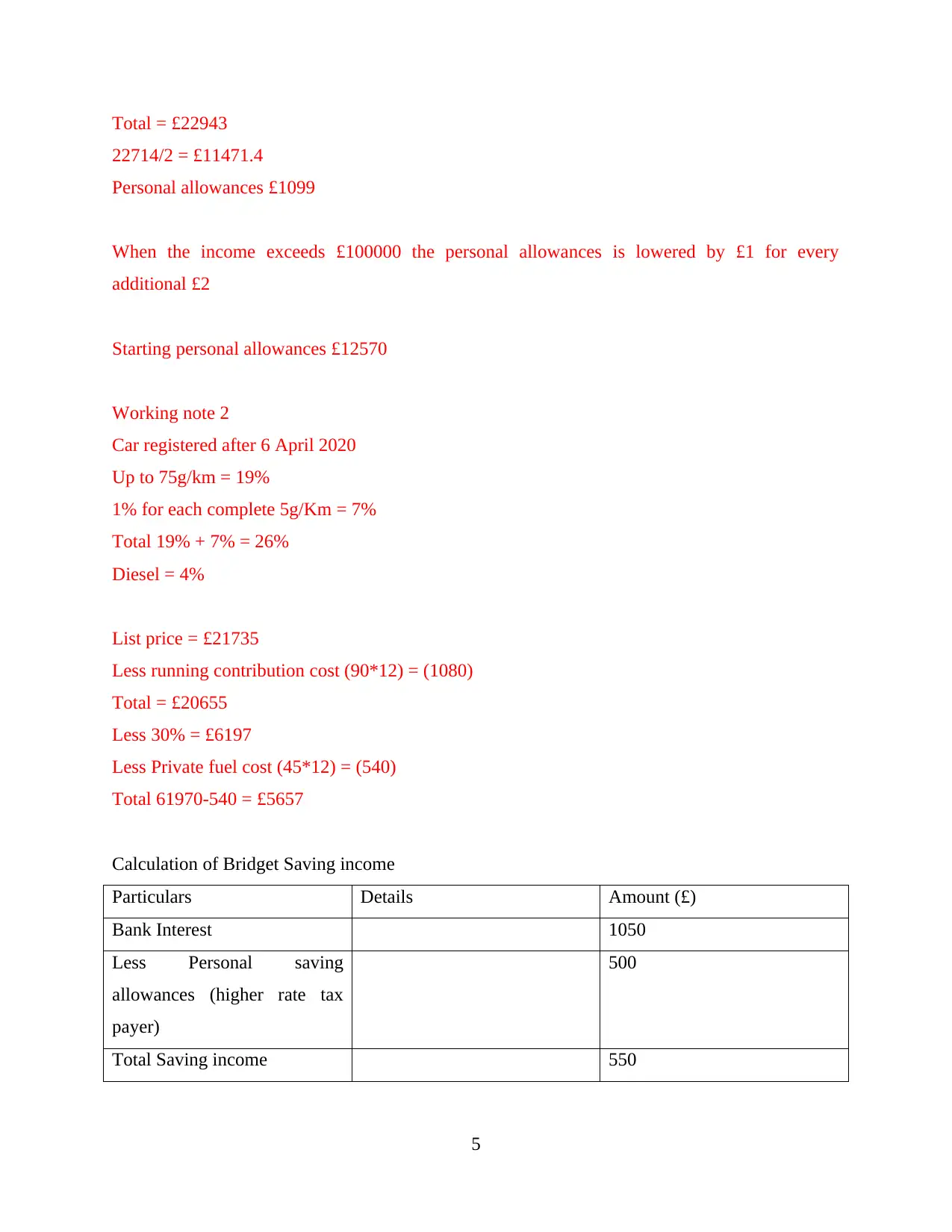

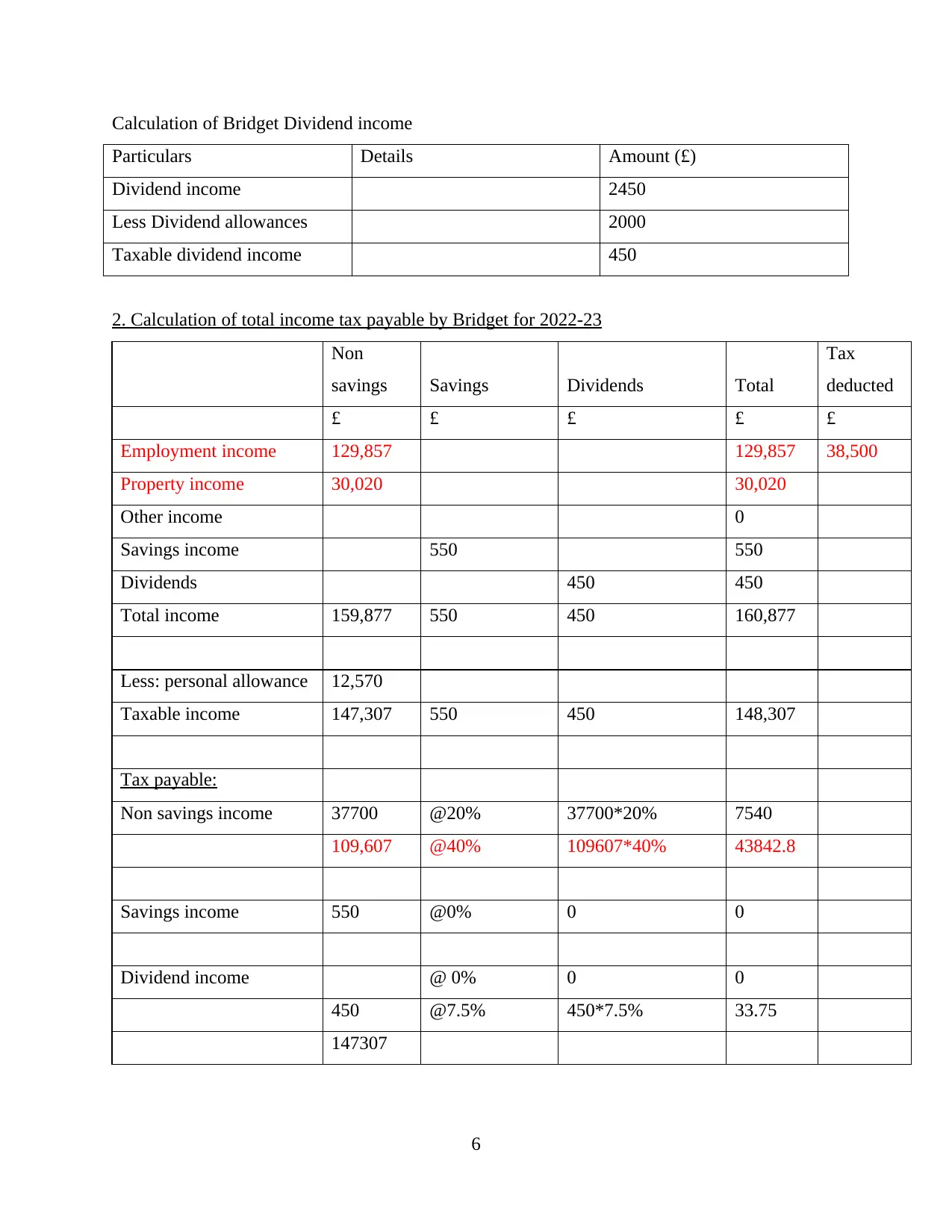

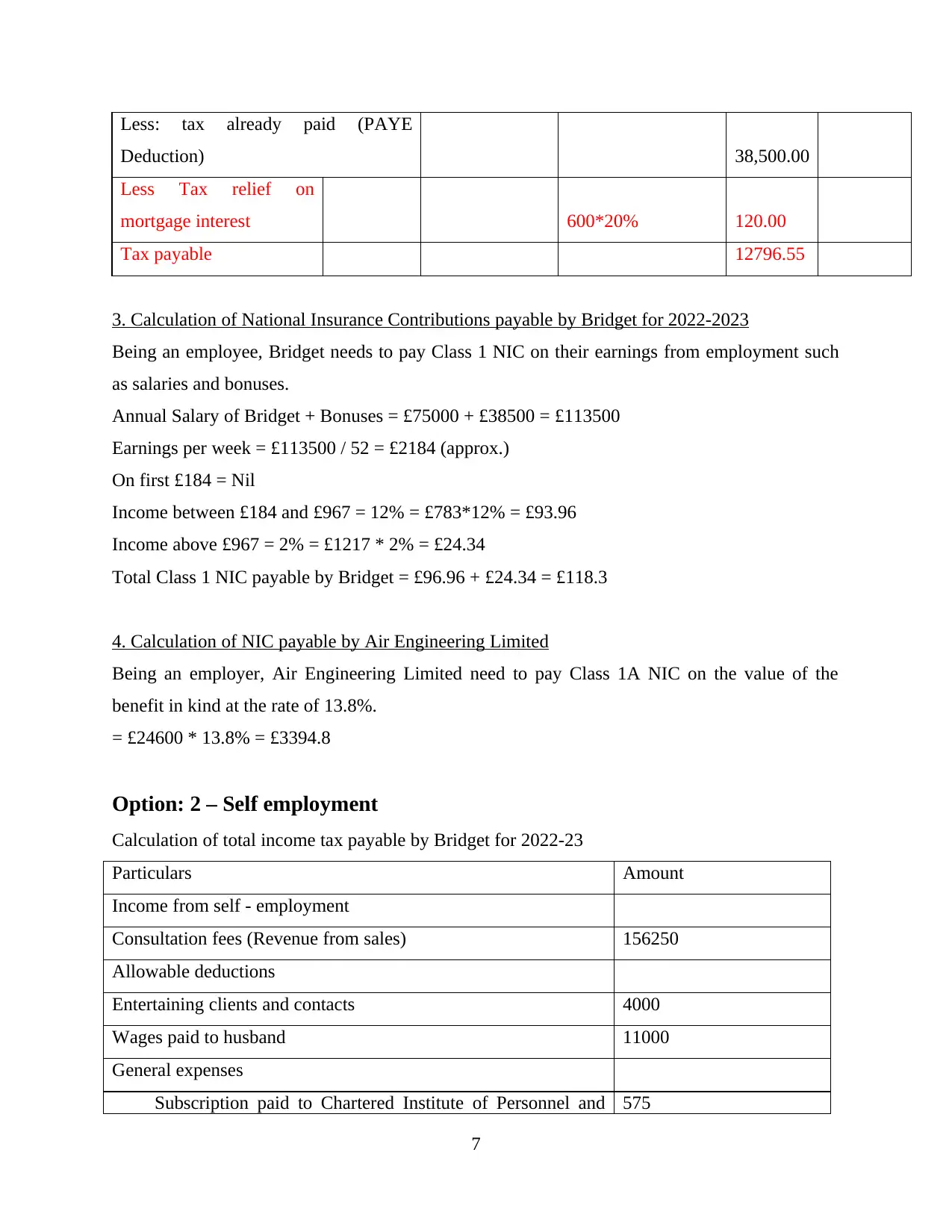

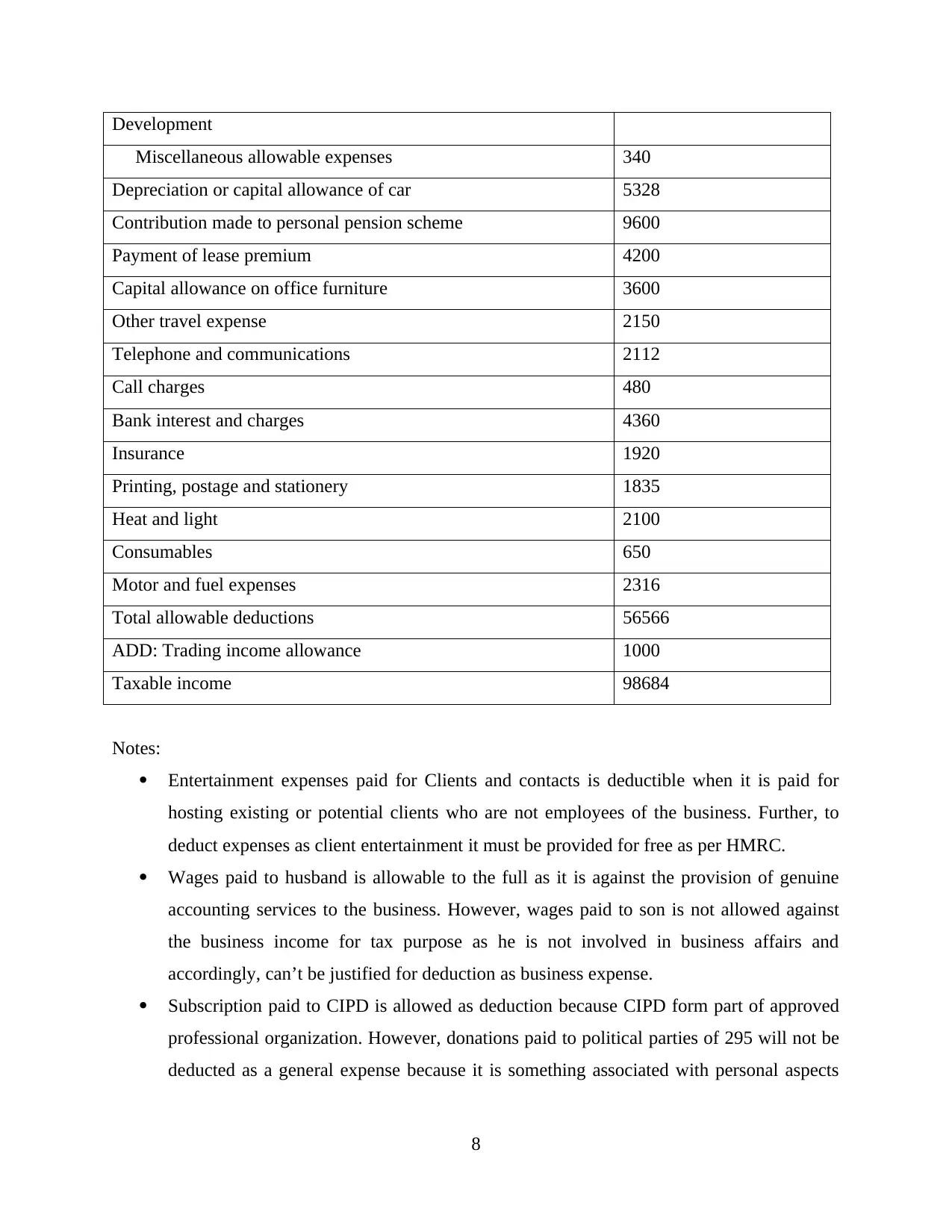

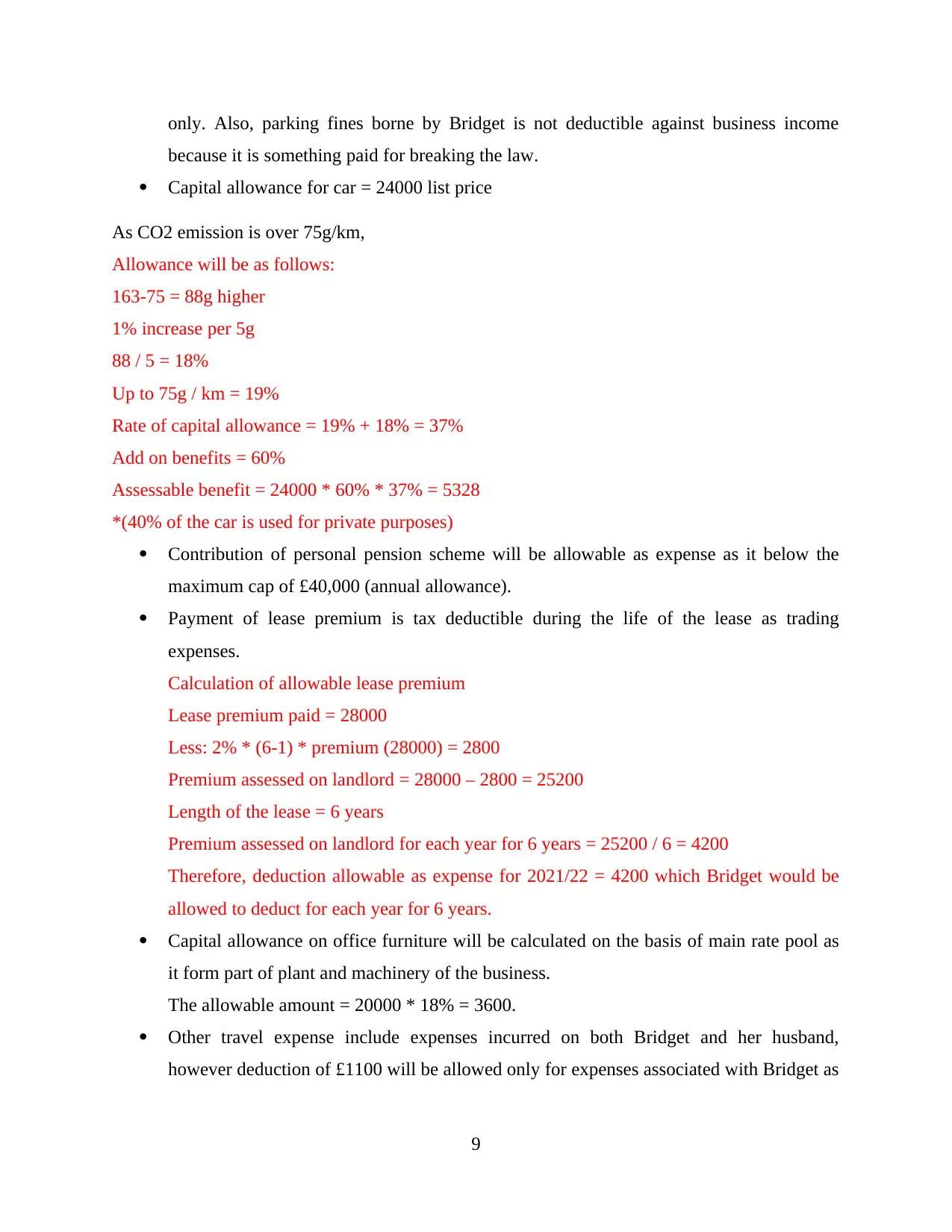

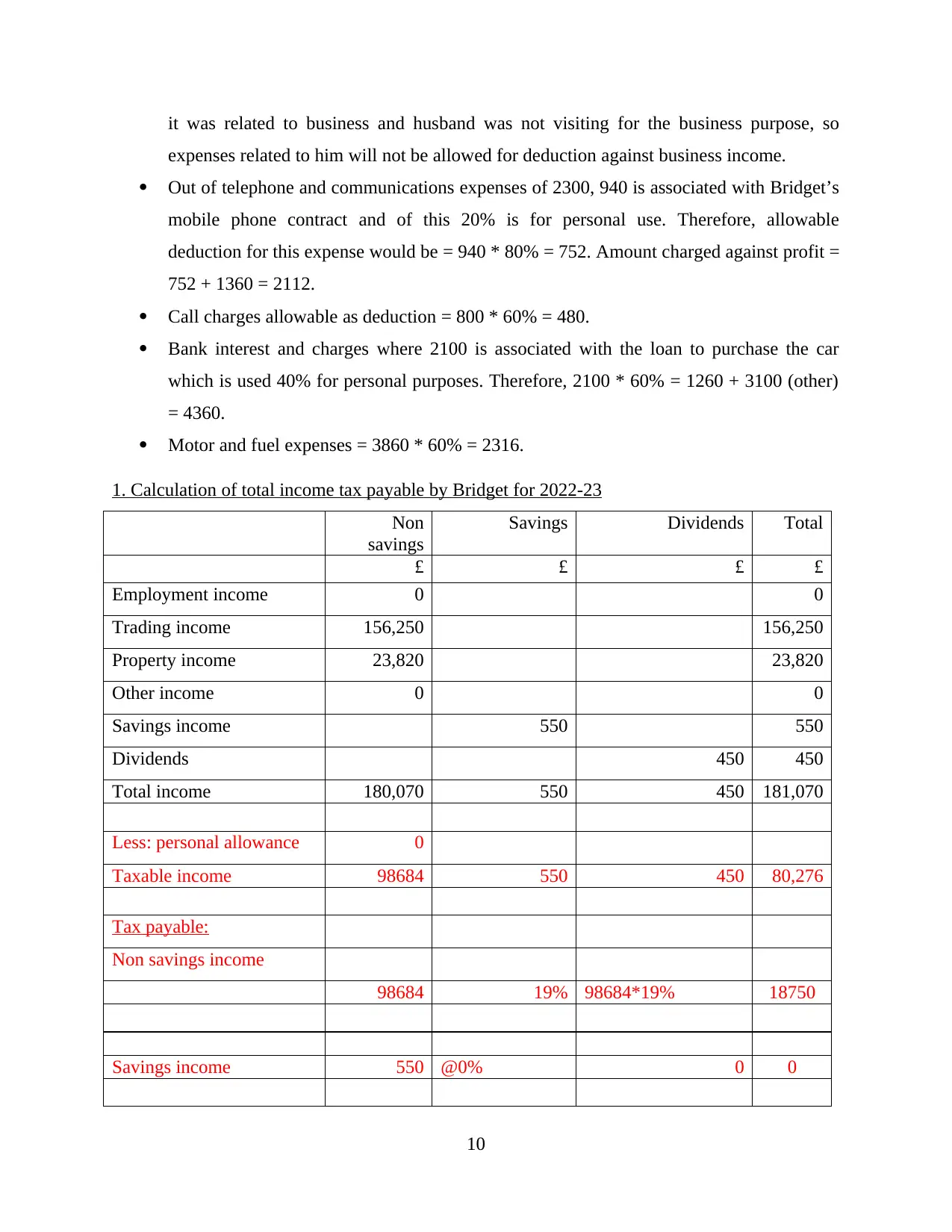

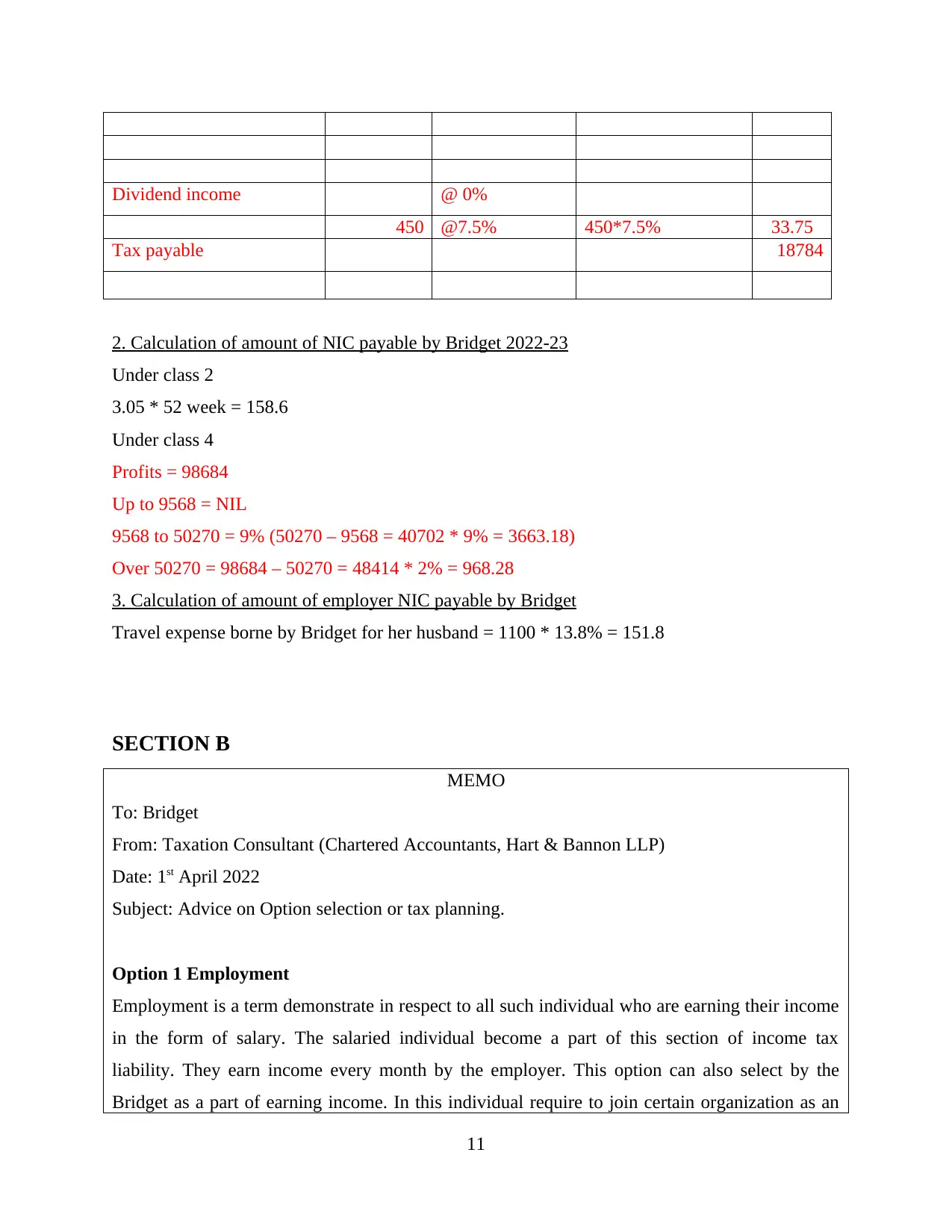

This report provides a detailed analysis of Bridget's tax liabilities under two different scenarios: employment and self-employment, in accordance with the UK's taxation laws. The employment scenario includes calculations of property income, taxable employment income, savings income, and dividend income, followed by the computation of total income tax and National Insurance Contributions (NICs) payable by both Bridget and her employer, Air Engineering Limited. The self-employment scenario covers the calculation of income from self-employment, allowable deductions, and taxable income, along with the computation of income tax and NICs. It also includes a memo offering advice on option selection or tax planning, suggesting that employment is more advantageous due to lower tax liability compared to self-employment. Desklib offers a range of solved assignments and past papers for students.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.