7702AFE Accounting & Reporting: Detailed Financial Statement Analysis

VerifiedAdded on 2023/06/10

|10

|1872

|283

Report

AI Summary

This report provides a comprehensive financial statement analysis, focusing on the accounting and reporting aspects of Vulcan Energy Resources Ltd and A2 Milk. It includes a ratio analysis, trend analysis, and synthesis of income statements, balance sheets, and cash flow statements. The analysis identifies key differences in net profit and cash flow, reasons for performance decline, and the reliability of cash flow statements versus income statements for strategic decision-making. The report also reflects on the learning experience, emphasizing data analysis, time management, and the application of financial evaluation techniques.

7702AFE Accounting and

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART A..........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................3

4...................................................................................................................................................3

PART B FINANCIAL STATEMENT ANALYSIS ......................................................................4

1) ratio analysis...........................................................................................................................4

2. Trend analysis.........................................................................................................................6

C) Synthesis-income statement, balance sheet and cash flows statement..................................8

Part D Profit or cash flows..........................................................................................................8

Part E...........................................................................................................................................9

REFERENCES..............................................................................................................................10

PART A..........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................3

4...................................................................................................................................................3

PART B FINANCIAL STATEMENT ANALYSIS ......................................................................4

1) ratio analysis...........................................................................................................................4

2. Trend analysis.........................................................................................................................6

C) Synthesis-income statement, balance sheet and cash flows statement..................................8

Part D Profit or cash flows..........................................................................................................8

Part E...........................................................................................................................................9

REFERENCES..............................................................................................................................10

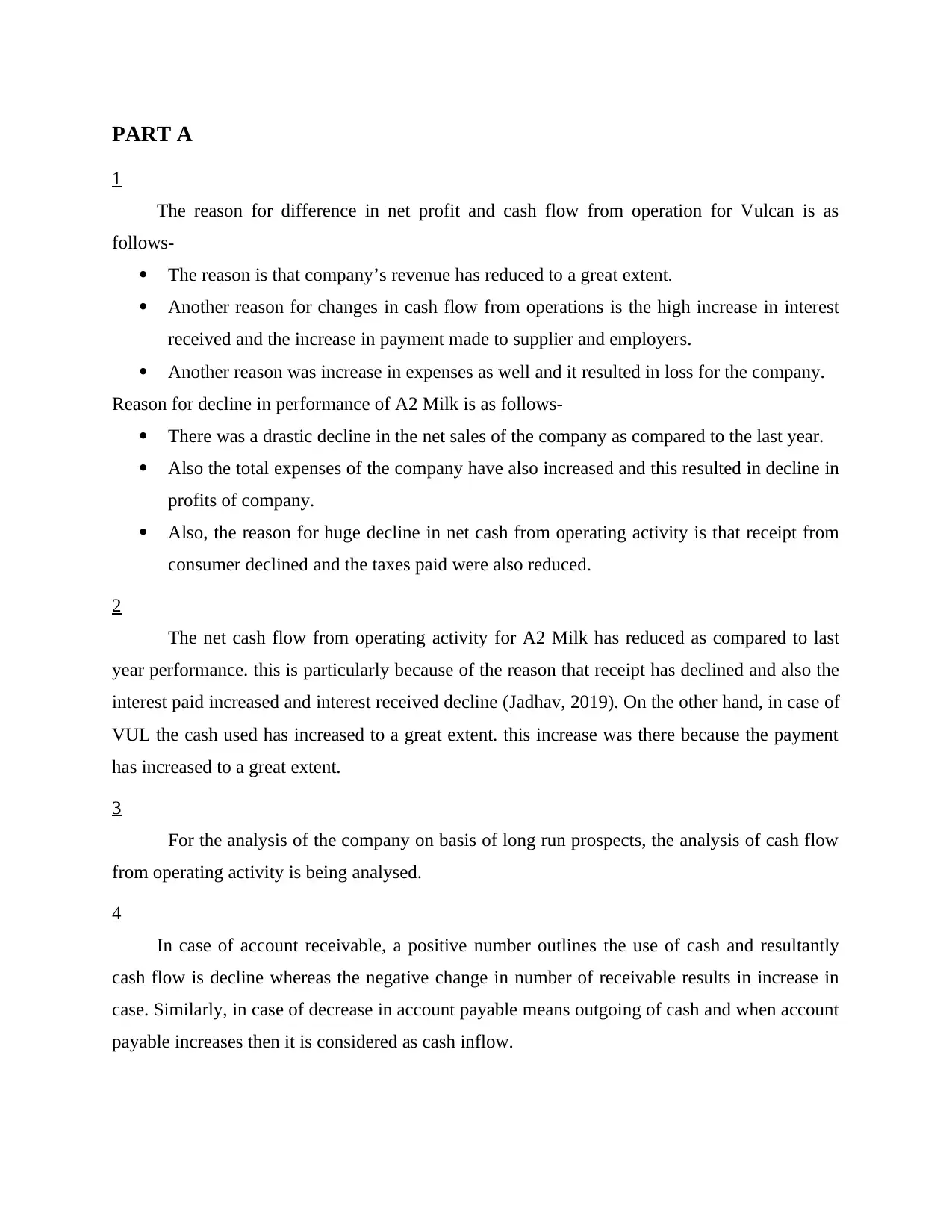

PART A

1

The reason for difference in net profit and cash flow from operation for Vulcan is as

follows-

The reason is that company’s revenue has reduced to a great extent.

Another reason for changes in cash flow from operations is the high increase in interest

received and the increase in payment made to supplier and employers.

Another reason was increase in expenses as well and it resulted in loss for the company.

Reason for decline in performance of A2 Milk is as follows-

There was a drastic decline in the net sales of the company as compared to the last year.

Also the total expenses of the company have also increased and this resulted in decline in

profits of company.

Also, the reason for huge decline in net cash from operating activity is that receipt from

consumer declined and the taxes paid were also reduced.

2

The net cash flow from operating activity for A2 Milk has reduced as compared to last

year performance. this is particularly because of the reason that receipt has declined and also the

interest paid increased and interest received decline (Jadhav, 2019). On the other hand, in case of

VUL the cash used has increased to a great extent. this increase was there because the payment

has increased to a great extent.

3

For the analysis of the company on basis of long run prospects, the analysis of cash flow

from operating activity is being analysed.

4

In case of account receivable, a positive number outlines the use of cash and resultantly

cash flow is decline whereas the negative change in number of receivable results in increase in

case. Similarly, in case of decrease in account payable means outgoing of cash and when account

payable increases then it is considered as cash inflow.

1

The reason for difference in net profit and cash flow from operation for Vulcan is as

follows-

The reason is that company’s revenue has reduced to a great extent.

Another reason for changes in cash flow from operations is the high increase in interest

received and the increase in payment made to supplier and employers.

Another reason was increase in expenses as well and it resulted in loss for the company.

Reason for decline in performance of A2 Milk is as follows-

There was a drastic decline in the net sales of the company as compared to the last year.

Also the total expenses of the company have also increased and this resulted in decline in

profits of company.

Also, the reason for huge decline in net cash from operating activity is that receipt from

consumer declined and the taxes paid were also reduced.

2

The net cash flow from operating activity for A2 Milk has reduced as compared to last

year performance. this is particularly because of the reason that receipt has declined and also the

interest paid increased and interest received decline (Jadhav, 2019). On the other hand, in case of

VUL the cash used has increased to a great extent. this increase was there because the payment

has increased to a great extent.

3

For the analysis of the company on basis of long run prospects, the analysis of cash flow

from operating activity is being analysed.

4

In case of account receivable, a positive number outlines the use of cash and resultantly

cash flow is decline whereas the negative change in number of receivable results in increase in

case. Similarly, in case of decrease in account payable means outgoing of cash and when account

payable increases then it is considered as cash inflow.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

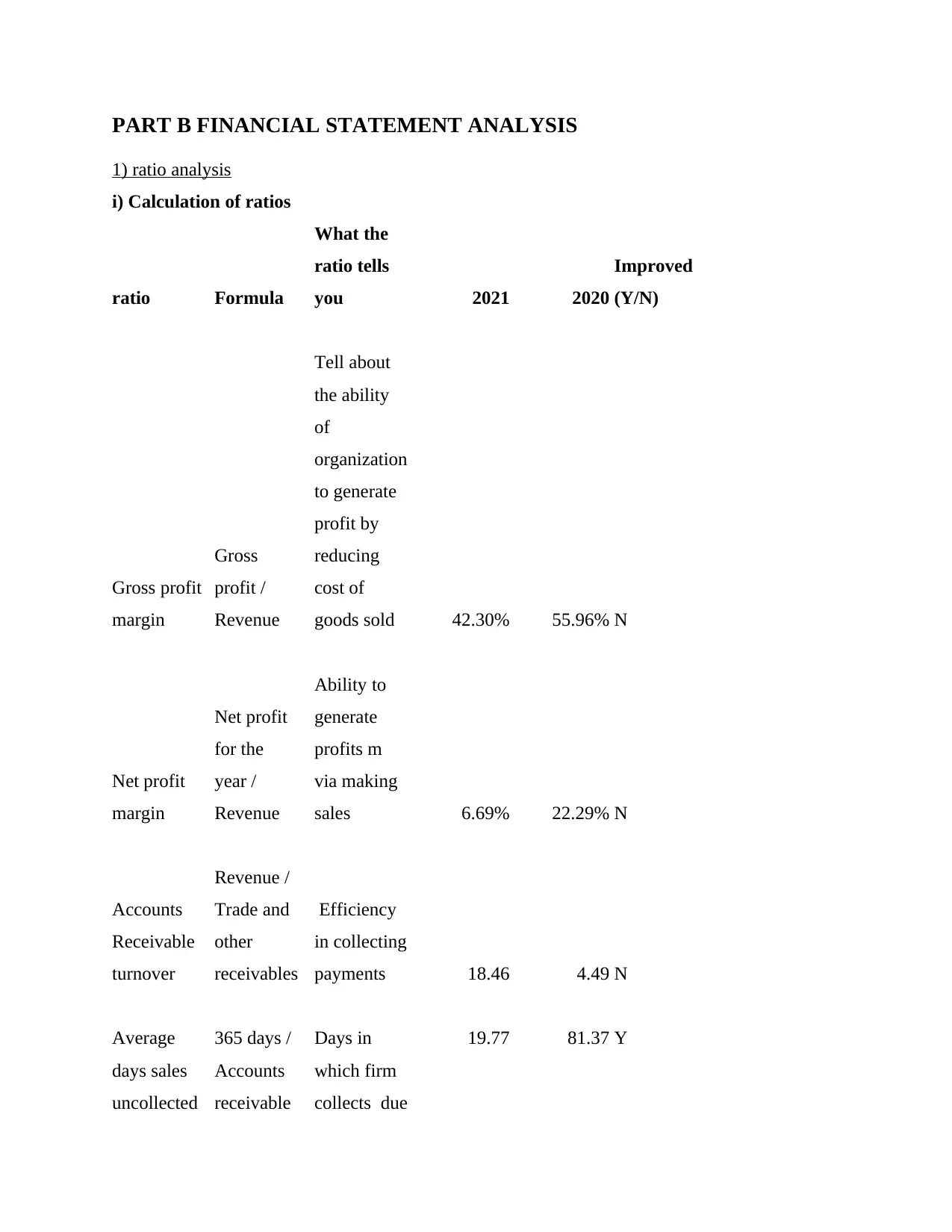

PART B FINANCIAL STATEMENT ANALYSIS

1) ratio analysis

i) Calculation of ratios

ratio Formula

What the

ratio tells

you 2021 2020

Improved

(Y/N)

Gross profit

margin

Gross

profit /

Revenue

Tell about

the ability

of

organization

to generate

profit by

reducing

cost of

goods sold 42.30% 55.96% N

Net profit

margin

Net profit

for the

year /

Revenue

Ability to

generate

profits m

via making

sales 6.69% 22.29% N

Accounts

Receivable

turnover

Revenue /

Trade and

other

receivables

Efficiency

in collecting

payments 18.46 4.49 N

Average

days sales

uncollected

365 days /

Accounts

receivable

Days in

which firm

collects due

19.77 81.37 Y

1) ratio analysis

i) Calculation of ratios

ratio Formula

What the

ratio tells

you 2021 2020

Improved

(Y/N)

Gross profit

margin

Gross

profit /

Revenue

Tell about

the ability

of

organization

to generate

profit by

reducing

cost of

goods sold 42.30% 55.96% N

Net profit

margin

Net profit

for the

year /

Revenue

Ability to

generate

profits m

via making

sales 6.69% 22.29% N

Accounts

Receivable

turnover

Revenue /

Trade and

other

receivables

Efficiency

in collecting

payments 18.46 4.49 N

Average

days sales

uncollected

365 days /

Accounts

receivable

Days in

which firm

collects due

19.77 81.37 Y

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

turnover payments

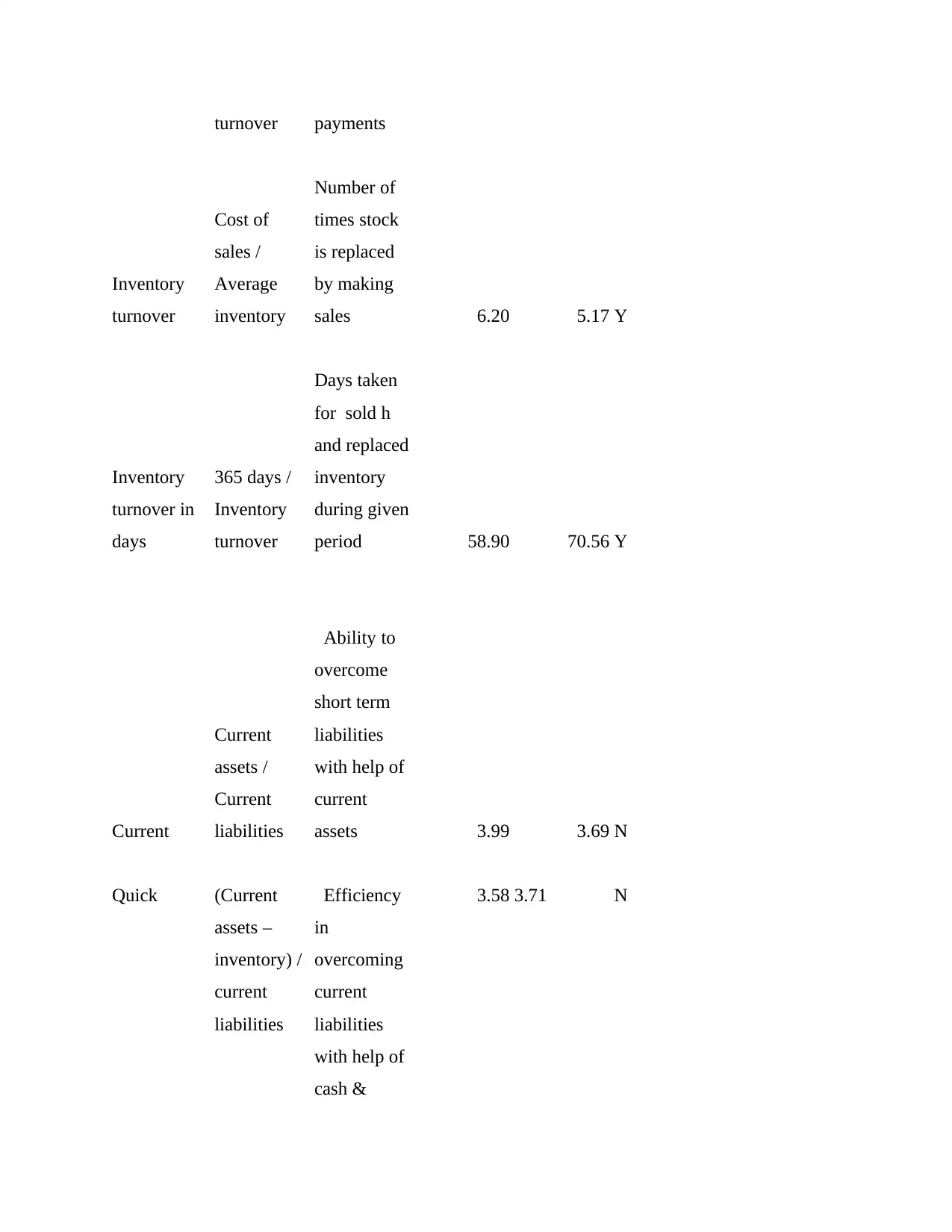

Inventory

turnover

Cost of

sales /

Average

inventory

Number of

times stock

is replaced

by making

sales 6.20 5.17 Y

Inventory

turnover in

days

365 days /

Inventory

turnover

Days taken

for sold h

and replaced

inventory

during given

period 58.90 70.56 Y

Current

Current

assets /

Current

liabilities

Ability to

overcome

short term

liabilities

with help of

current

assets 3.99 3.69 N

Quick (Current

assets –

inventory) /

current

liabilities

Efficiency

in

overcoming

current

liabilities

with help of

cash &

3.58 3.71 N

Inventory

turnover

Cost of

sales /

Average

inventory

Number of

times stock

is replaced

by making

sales 6.20 5.17 Y

Inventory

turnover in

days

365 days /

Inventory

turnover

Days taken

for sold h

and replaced

inventory

during given

period 58.90 70.56 Y

Current

Current

assets /

Current

liabilities

Ability to

overcome

short term

liabilities

with help of

current

assets 3.99 3.69 N

Quick (Current

assets –

inventory) /

current

liabilities

Efficiency

in

overcoming

current

liabilities

with help of

cash &

3.58 3.71 N

equivalent

assets

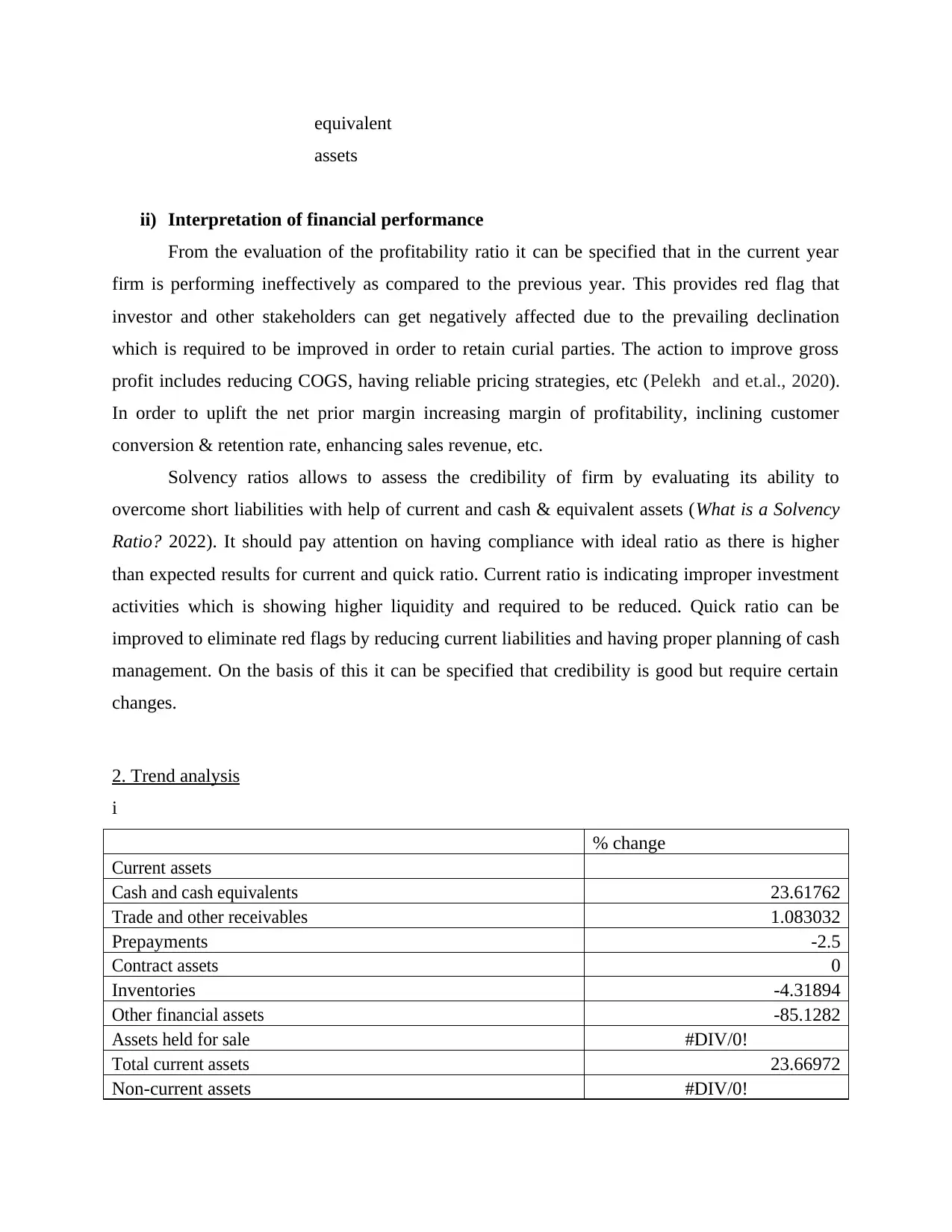

ii) Interpretation of financial performance

From the evaluation of the profitability ratio it can be specified that in the current year

firm is performing ineffectively as compared to the previous year. This provides red flag that

investor and other stakeholders can get negatively affected due to the prevailing declination

which is required to be improved in order to retain curial parties. The action to improve gross

profit includes reducing COGS, having reliable pricing strategies, etc (Pelekh and et.al., 2020).

In order to uplift the net prior margin increasing margin of profitability, inclining customer

conversion & retention rate, enhancing sales revenue, etc.

Solvency ratios allows to assess the credibility of firm by evaluating its ability to

overcome short liabilities with help of current and cash & equivalent assets (What is a Solvency

Ratio? 2022). It should pay attention on having compliance with ideal ratio as there is higher

than expected results for current and quick ratio. Current ratio is indicating improper investment

activities which is showing higher liquidity and required to be reduced. Quick ratio can be

improved to eliminate red flags by reducing current liabilities and having proper planning of cash

management. On the basis of this it can be specified that credibility is good but require certain

changes.

2. Trend analysis

i

% change

Current assets

Cash and cash equivalents 23.61762

Trade and other receivables 1.083032

Prepayments -2.5

Contract assets 0

Inventories -4.31894

Other financial assets -85.1282

Assets held for sale #DIV/0!

Total current assets 23.66972

Non-current assets #DIV/0!

assets

ii) Interpretation of financial performance

From the evaluation of the profitability ratio it can be specified that in the current year

firm is performing ineffectively as compared to the previous year. This provides red flag that

investor and other stakeholders can get negatively affected due to the prevailing declination

which is required to be improved in order to retain curial parties. The action to improve gross

profit includes reducing COGS, having reliable pricing strategies, etc (Pelekh and et.al., 2020).

In order to uplift the net prior margin increasing margin of profitability, inclining customer

conversion & retention rate, enhancing sales revenue, etc.

Solvency ratios allows to assess the credibility of firm by evaluating its ability to

overcome short liabilities with help of current and cash & equivalent assets (What is a Solvency

Ratio? 2022). It should pay attention on having compliance with ideal ratio as there is higher

than expected results for current and quick ratio. Current ratio is indicating improper investment

activities which is showing higher liquidity and required to be reduced. Quick ratio can be

improved to eliminate red flags by reducing current liabilities and having proper planning of cash

management. On the basis of this it can be specified that credibility is good but require certain

changes.

2. Trend analysis

i

% change

Current assets

Cash and cash equivalents 23.61762

Trade and other receivables 1.083032

Prepayments -2.5

Contract assets 0

Inventories -4.31894

Other financial assets -85.1282

Assets held for sale #DIV/0!

Total current assets 23.66972

Non-current assets #DIV/0!

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

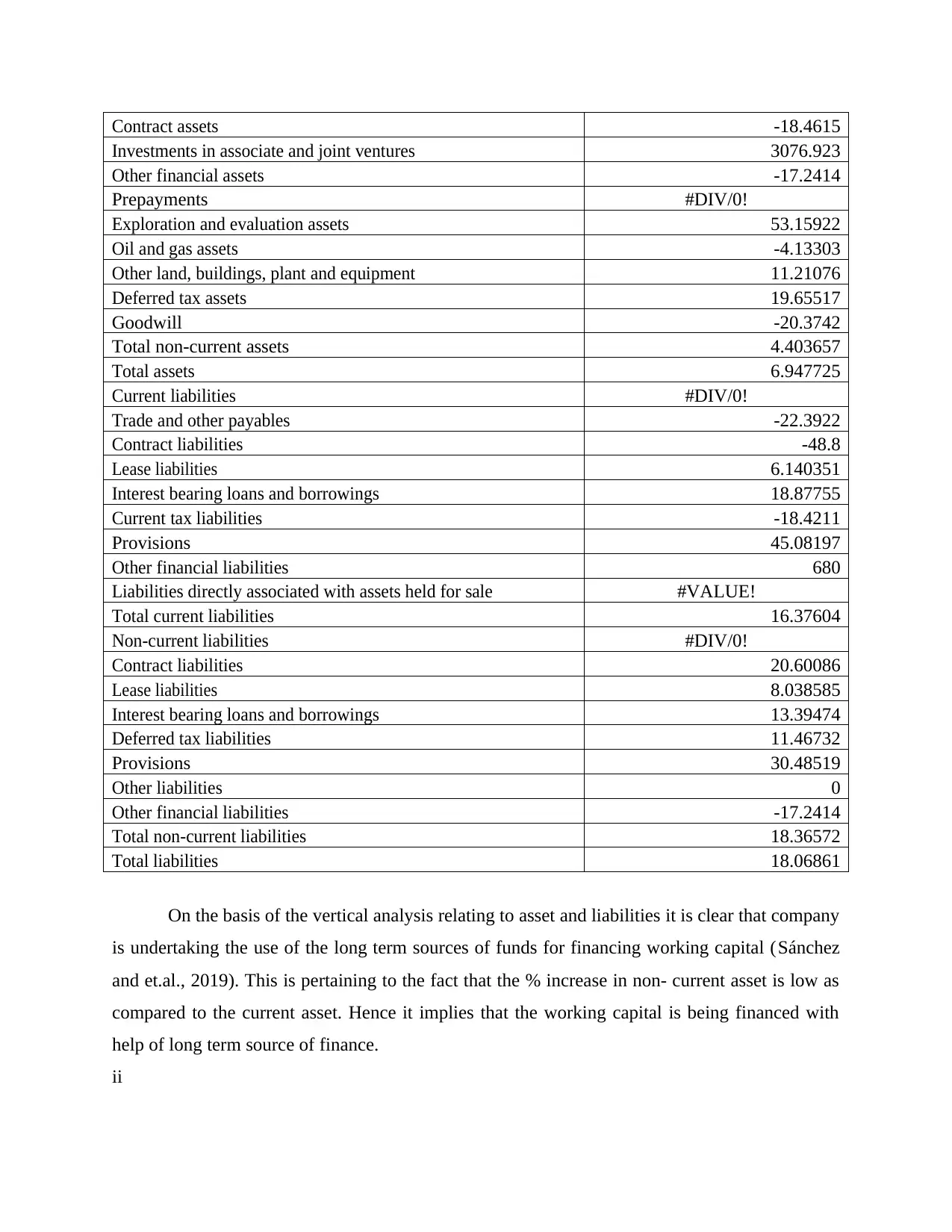

Contract assets -18.4615

Investments in associate and joint ventures 3076.923

Other financial assets -17.2414

Prepayments #DIV/0!

Exploration and evaluation assets 53.15922

Oil and gas assets -4.13303

Other land, buildings, plant and equipment 11.21076

Deferred tax assets 19.65517

Goodwill -20.3742

Total non-current assets 4.403657

Total assets 6.947725

Current liabilities #DIV/0!

Trade and other payables -22.3922

Contract liabilities -48.8

Lease liabilities 6.140351

Interest bearing loans and borrowings 18.87755

Current tax liabilities -18.4211

Provisions 45.08197

Other financial liabilities 680

Liabilities directly associated with assets held for sale #VALUE!

Total current liabilities 16.37604

Non-current liabilities #DIV/0!

Contract liabilities 20.60086

Lease liabilities 8.038585

Interest bearing loans and borrowings 13.39474

Deferred tax liabilities 11.46732

Provisions 30.48519

Other liabilities 0

Other financial liabilities -17.2414

Total non-current liabilities 18.36572

Total liabilities 18.06861

On the basis of the vertical analysis relating to asset and liabilities it is clear that company

is undertaking the use of the long term sources of funds for financing working capital (Sánchez

and et.al., 2019). This is pertaining to the fact that the % increase in non- current asset is low as

compared to the current asset. Hence it implies that the working capital is being financed with

help of long term source of finance.

ii

Investments in associate and joint ventures 3076.923

Other financial assets -17.2414

Prepayments #DIV/0!

Exploration and evaluation assets 53.15922

Oil and gas assets -4.13303

Other land, buildings, plant and equipment 11.21076

Deferred tax assets 19.65517

Goodwill -20.3742

Total non-current assets 4.403657

Total assets 6.947725

Current liabilities #DIV/0!

Trade and other payables -22.3922

Contract liabilities -48.8

Lease liabilities 6.140351

Interest bearing loans and borrowings 18.87755

Current tax liabilities -18.4211

Provisions 45.08197

Other financial liabilities 680

Liabilities directly associated with assets held for sale #VALUE!

Total current liabilities 16.37604

Non-current liabilities #DIV/0!

Contract liabilities 20.60086

Lease liabilities 8.038585

Interest bearing loans and borrowings 13.39474

Deferred tax liabilities 11.46732

Provisions 30.48519

Other liabilities 0

Other financial liabilities -17.2414

Total non-current liabilities 18.36572

Total liabilities 18.06861

On the basis of the vertical analysis relating to asset and liabilities it is clear that company

is undertaking the use of the long term sources of funds for financing working capital (Sánchez

and et.al., 2019). This is pertaining to the fact that the % increase in non- current asset is low as

compared to the current asset. Hence it implies that the working capital is being financed with

help of long term source of finance.

ii

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

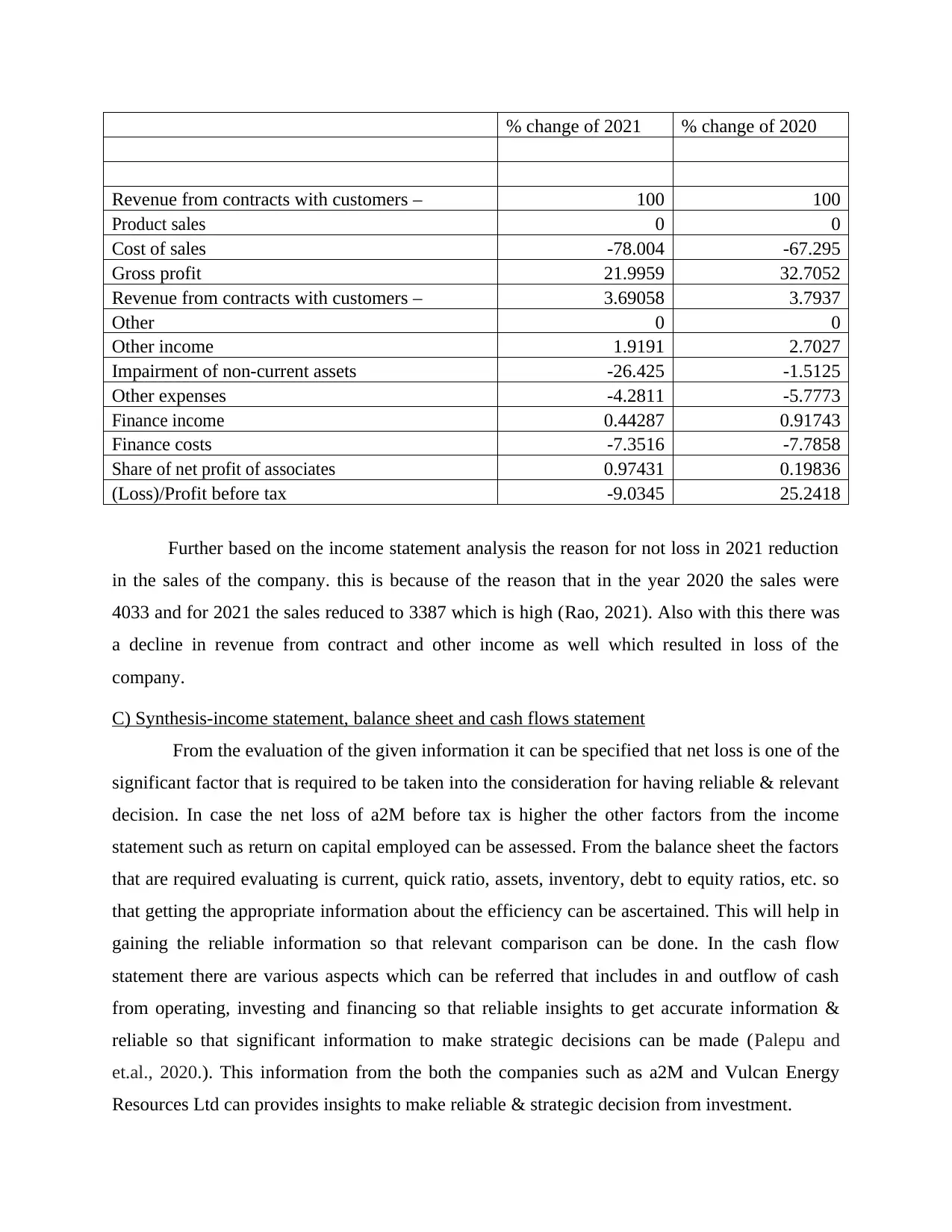

% change of 2021 % change of 2020

Revenue from contracts with customers – 100 100

Product sales 0 0

Cost of sales -78.004 -67.295

Gross profit 21.9959 32.7052

Revenue from contracts with customers – 3.69058 3.7937

Other 0 0

Other income 1.9191 2.7027

Impairment of non-current assets -26.425 -1.5125

Other expenses -4.2811 -5.7773

Finance income 0.44287 0.91743

Finance costs -7.3516 -7.7858

Share of net profit of associates 0.97431 0.19836

(Loss)/Profit before tax -9.0345 25.2418

Further based on the income statement analysis the reason for not loss in 2021 reduction

in the sales of the company. this is because of the reason that in the year 2020 the sales were

4033 and for 2021 the sales reduced to 3387 which is high (Rao, 2021). Also with this there was

a decline in revenue from contract and other income as well which resulted in loss of the

company.

C) Synthesis-income statement, balance sheet and cash flows statement

From the evaluation of the given information it can be specified that net loss is one of the

significant factor that is required to be taken into the consideration for having reliable & relevant

decision. In case the net loss of a2M before tax is higher the other factors from the income

statement such as return on capital employed can be assessed. From the balance sheet the factors

that are required evaluating is current, quick ratio, assets, inventory, debt to equity ratios, etc. so

that getting the appropriate information about the efficiency can be ascertained. This will help in

gaining the reliable information so that relevant comparison can be done. In the cash flow

statement there are various aspects which can be referred that includes in and outflow of cash

from operating, investing and financing so that reliable insights to get accurate information &

reliable so that significant information to make strategic decisions can be made (Palepu and

et.al., 2020.). This information from the both the companies such as a2M and Vulcan Energy

Resources Ltd can provides insights to make reliable & strategic decision from investment.

Revenue from contracts with customers – 100 100

Product sales 0 0

Cost of sales -78.004 -67.295

Gross profit 21.9959 32.7052

Revenue from contracts with customers – 3.69058 3.7937

Other 0 0

Other income 1.9191 2.7027

Impairment of non-current assets -26.425 -1.5125

Other expenses -4.2811 -5.7773

Finance income 0.44287 0.91743

Finance costs -7.3516 -7.7858

Share of net profit of associates 0.97431 0.19836

(Loss)/Profit before tax -9.0345 25.2418

Further based on the income statement analysis the reason for not loss in 2021 reduction

in the sales of the company. this is because of the reason that in the year 2020 the sales were

4033 and for 2021 the sales reduced to 3387 which is high (Rao, 2021). Also with this there was

a decline in revenue from contract and other income as well which resulted in loss of the

company.

C) Synthesis-income statement, balance sheet and cash flows statement

From the evaluation of the given information it can be specified that net loss is one of the

significant factor that is required to be taken into the consideration for having reliable & relevant

decision. In case the net loss of a2M before tax is higher the other factors from the income

statement such as return on capital employed can be assessed. From the balance sheet the factors

that are required evaluating is current, quick ratio, assets, inventory, debt to equity ratios, etc. so

that getting the appropriate information about the efficiency can be ascertained. This will help in

gaining the reliable information so that relevant comparison can be done. In the cash flow

statement there are various aspects which can be referred that includes in and outflow of cash

from operating, investing and financing so that reliable insights to get accurate information &

reliable so that significant information to make strategic decisions can be made (Palepu and

et.al., 2020.). This information from the both the companies such as a2M and Vulcan Energy

Resources Ltd can provides insights to make reliable & strategic decision from investment.

Part D Profit or cash flows

From the assessment it can be specified that the cash flow statements is highly reliable

in order to get the appropriate information so that strategic decision can be formulated (Easton

and et.al., 2018). This statement as compared to the income pay attention on reflecting the

changes prevailing in the cash inflows and outflows that provides the reliable insights from the

realistic perspective. This tends to offer higher realistic insights for decision-making. On the

other side, income statement is related with gaining the information about the profitability which

has nothing to do with cash so taking into consideration as compared to cash flow might not

offer the relevant information to investors to make decisions.

Part E

From the evaluation of the obtained information it can be specified that there are different

kinds of the learning that has been developed in me. This learning comprises having data

analysis by computing the figures, significant concentration on each detail in turn reliable

information to get make strategic decision. Time management via ensuring the completion of

project through meeting deadlines. The insights about the various technique of evaluating

financial of firm such as ratio & technical to obtain relevant information for decision-making

procedure. This learning is helpful in effective insights through data analysts, etc so that

investment & long term decision can be made,

From the assessment it can be specified that the cash flow statements is highly reliable

in order to get the appropriate information so that strategic decision can be formulated (Easton

and et.al., 2018). This statement as compared to the income pay attention on reflecting the

changes prevailing in the cash inflows and outflows that provides the reliable insights from the

realistic perspective. This tends to offer higher realistic insights for decision-making. On the

other side, income statement is related with gaining the information about the profitability which

has nothing to do with cash so taking into consideration as compared to cash flow might not

offer the relevant information to investors to make decisions.

Part E

From the evaluation of the obtained information it can be specified that there are different

kinds of the learning that has been developed in me. This learning comprises having data

analysis by computing the figures, significant concentration on each detail in turn reliable

information to get make strategic decision. Time management via ensuring the completion of

project through meeting deadlines. The insights about the various technique of evaluating

financial of firm such as ratio & technical to obtain relevant information for decision-making

procedure. This learning is helpful in effective insights through data analysts, etc so that

investment & long term decision can be made,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Easton, P.D. And et.al., 2018. Financial statement analysis & valuation. Boston, MA:

Cambridge Business Publishers.

Jadhav, M. S. V., 2019. Cash Flow Statement Analysis. Think India Journal. 22(4). pp.8418-

8427.

Palepu, K.G. and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Pelekh, U and et.al., 2020. Financial statements as a management tool. Management Science

Letters. 10(1). pp.197-208.

Rao, P. M., 2021. Financial statement analysis and reporting. PHI Learning Pvt. Ltd..

Sánchez, M. N. and et.al., 2019. Experimental validation of a numerical model of a ventilated

façade with horizontal and vertical open joints. Energies. 13(1). p.146.

Online

What is a Solvency Ratio? 2022. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/finance/solvency-ratio/>

Books and Journals

Easton, P.D. And et.al., 2018. Financial statement analysis & valuation. Boston, MA:

Cambridge Business Publishers.

Jadhav, M. S. V., 2019. Cash Flow Statement Analysis. Think India Journal. 22(4). pp.8418-

8427.

Palepu, K.G. and et.al., 2020. Business analysis and valuation: Using financial statements.

Cengage AU.

Pelekh, U and et.al., 2020. Financial statements as a management tool. Management Science

Letters. 10(1). pp.197-208.

Rao, P. M., 2021. Financial statement analysis and reporting. PHI Learning Pvt. Ltd..

Sánchez, M. N. and et.al., 2019. Experimental validation of a numerical model of a ventilated

façade with horizontal and vertical open joints. Energies. 13(1). p.146.

Online

What is a Solvency Ratio? 2022. [Online]. Available through:

<https://corporatefinanceinstitute.com/resources/knowledge/finance/solvency-ratio/>

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.