AAF0436 - Management Accounting: Costing, Pricing & Profitability

VerifiedAdded on 2023/06/18

|12

|3394

|217

Report

AI Summary

This report delves into various management accounting techniques relevant to BETA, an IT company. It discusses the usage, types, and limitations of standard costing, followed by a critical analysis of target costing and its differentiation from standard costing. The role of contribution techniques in decision-making is explained with examples, highlighting its application in setting selling prices, calculating break-even points, and examining margin of safety. Furthermore, the report analyzes how transfer pricing can be strategically used to improve a company's profitability position. The report concludes by summarizing the key aspects of each costing method and their importance in enhancing business performance.

Management Accounting and

Financial Planning AAF0436

Financial Planning AAF0436

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

I. Discussing usage of standard costing, its types and limitations..............................................3

II. Critically discussing Target costing and differentiating it from Standard Costing................5

III. Explaining role of contribution technique in decision-making with examples.....................6

IV. Analysing the ways in which transfer pricing can be used to improve profitability position

.....................................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

I. Discussing usage of standard costing, its types and limitations..............................................3

II. Critically discussing Target costing and differentiating it from Standard Costing................5

III. Explaining role of contribution technique in decision-making with examples.....................6

IV. Analysing the ways in which transfer pricing can be used to improve profitability position

.....................................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management Accounting is the procedure where different reports are prepared and

maintained which provides an assistance to managers in taking various decisions that are

important to business. The present report is based on BETA, a MNC that deals in IT business

and specializes in producing business solutions and online retail systems. Report will discuss

usage of standard costing along with its types and limitations.

Further, study will shed light on Target costing and differentiate it from standard costing.

In addition to this, it will also describe role of contribution techniques in decision-making

process and its application in BETA to improve business. Lastly, study will analyse transfer

pricing approaches that can be used to improve business condition and profitability.

I. Discussing usage of standard costing, its types and limitations

A standard costing is a method where costs are predetermined after careful evaluation

under stated conditions. It is a cost accounting technique which is majorly used by

manufacturing industries to identify costs and expenses such as direct labour, material and

overheads (Paul, 2020). These costs are just not the estimations but also the objectives to be

achieved within stipulated time period. After setting proper standards, achieving it becomes

rationally efficient and effective. Standards are determined by evaluating the industry standards

to improve labour effectiveness and controlling wastage in order to curb product cost.

Usage:

The main usage is to assist management by providing relevant information for day-to-day

operations.

BETA can use this technique which will help in establishing a solid basis for effectively

managing and controlling costs by providing a criterion to evaluate actual costs.

Standard costing helps in identifying variances, whether favourable or adverse, between

actual and estimated costs so that necessary actions can be taken to improve the present

business condition (Kristensen, 2021).

Another usage of it is to help in setting and preparing budgets which aids BETA in giving

vital information at the time of decision-making process.

It is also used to examine the level of performance and effectiveness of employees and

management.

Management Accounting is the procedure where different reports are prepared and

maintained which provides an assistance to managers in taking various decisions that are

important to business. The present report is based on BETA, a MNC that deals in IT business

and specializes in producing business solutions and online retail systems. Report will discuss

usage of standard costing along with its types and limitations.

Further, study will shed light on Target costing and differentiate it from standard costing.

In addition to this, it will also describe role of contribution techniques in decision-making

process and its application in BETA to improve business. Lastly, study will analyse transfer

pricing approaches that can be used to improve business condition and profitability.

I. Discussing usage of standard costing, its types and limitations

A standard costing is a method where costs are predetermined after careful evaluation

under stated conditions. It is a cost accounting technique which is majorly used by

manufacturing industries to identify costs and expenses such as direct labour, material and

overheads (Paul, 2020). These costs are just not the estimations but also the objectives to be

achieved within stipulated time period. After setting proper standards, achieving it becomes

rationally efficient and effective. Standards are determined by evaluating the industry standards

to improve labour effectiveness and controlling wastage in order to curb product cost.

Usage:

The main usage is to assist management by providing relevant information for day-to-day

operations.

BETA can use this technique which will help in establishing a solid basis for effectively

managing and controlling costs by providing a criterion to evaluate actual costs.

Standard costing helps in identifying variances, whether favourable or adverse, between

actual and estimated costs so that necessary actions can be taken to improve the present

business condition (Kristensen, 2021).

Another usage of it is to help in setting and preparing budgets which aids BETA in giving

vital information at the time of decision-making process.

It is also used to examine the level of performance and effectiveness of employees and

management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This type of costing is a control technique which uses feedback control cycle, it further

helps in reducing unwanted costs in future and leads to reduction in costs.

Valuation of inventory becomes easier which assists in reducing costing and improving

pricing of goods. Such technique enables BETA to adopt Management by Exception which can be

implemented at operational level.

Types of standards

Ideal standards

These standards are also known as perfection standards which are accepted on maximum

efficiency level and when there is no plan to stop the work or production. Such tight standards

cannot be obtained in real world due to uncertainty of market with so many fluctuations in price

levels. Ideal standard showcases that level of production that can be achieved if all the market

condition are perfect at all times. These standards are established by BETA on the assumptions

that there will be no breakdown of machinery and no work interruptions.

Basic Standards

Standards which are long-term standards and remain unaffected after computing it for the

first time are known as Basic standards. These estimations are rarely revised or upgraded to show

any changes in price or products. These standards are used by BETA for comparison of actual

costs with predetermined standards and are basically used as fixed base to measure any trends in

operations and performance.

Normal Standards

These are average standards that are attainable during a time period, usually long enough

to cover on business cycle. Here, standards are set on a normal capacity which shows normal

average output of BETA. Such standards are not updated until the business cycle has completed.

It often results in erroneous valuation of stock and leads to incorrect profit estimation.

Currently Attainable Standards

It is established to be applied for a short duration and is concerned with current

conditions. These standards are set after considering cost of normal spoilage, idle time and other

events that may affect normal business operations. Such standards are upgraded regularly to

examine the changes in price and methods.

helps in reducing unwanted costs in future and leads to reduction in costs.

Valuation of inventory becomes easier which assists in reducing costing and improving

pricing of goods. Such technique enables BETA to adopt Management by Exception which can be

implemented at operational level.

Types of standards

Ideal standards

These standards are also known as perfection standards which are accepted on maximum

efficiency level and when there is no plan to stop the work or production. Such tight standards

cannot be obtained in real world due to uncertainty of market with so many fluctuations in price

levels. Ideal standard showcases that level of production that can be achieved if all the market

condition are perfect at all times. These standards are established by BETA on the assumptions

that there will be no breakdown of machinery and no work interruptions.

Basic Standards

Standards which are long-term standards and remain unaffected after computing it for the

first time are known as Basic standards. These estimations are rarely revised or upgraded to show

any changes in price or products. These standards are used by BETA for comparison of actual

costs with predetermined standards and are basically used as fixed base to measure any trends in

operations and performance.

Normal Standards

These are average standards that are attainable during a time period, usually long enough

to cover on business cycle. Here, standards are set on a normal capacity which shows normal

average output of BETA. Such standards are not updated until the business cycle has completed.

It often results in erroneous valuation of stock and leads to incorrect profit estimation.

Currently Attainable Standards

It is established to be applied for a short duration and is concerned with current

conditions. These standards are set after considering cost of normal spoilage, idle time and other

events that may affect normal business operations. Such standards are upgraded regularly to

examine the changes in price and methods.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Limitations

Establishment of standard is a very difficult task which involves a lot of scientific

evaluation such as time study, motion study, etc. Along with this, it is costly due to which

small firms cannot operate on this system.

Such rigid estimations once set cannot be altered for a certain time period. It is not

applicable in industries which faces regular price fluctuations. Updating the standards is

also a tough job because of its costly nature.

Setting standards is much tedious job because a loose standard will not be effective and

high standard may increase frustration levels in workers of BETA.

For industries like BETA producing tailor-made products cannot apply standard costing

(Iliemena and Amedu, 2019). Also, in industries where production normally takes more

than an accounting period, standard costing becomes a tough task to apply.

Identification of controllable and uncontrollable factors is not possible in this type of

costing because a particular person or process cannot be identified and evaluated. Generally, managers oppose this type of costing because of less freedom attached to it

which also has bad psychological effects.

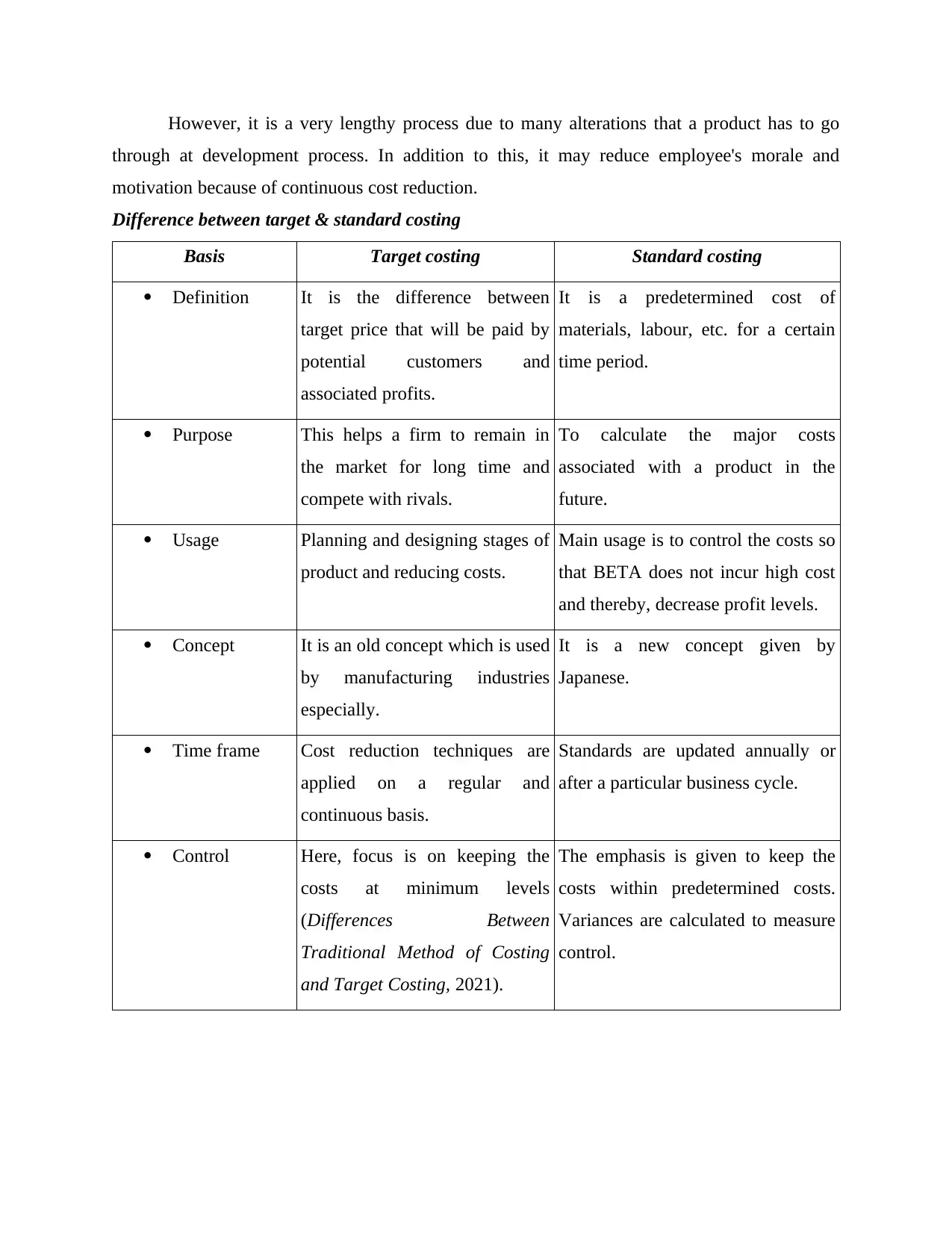

II. Critically discussing Target costing and differentiating it from Standard Costing

Target Costing

In Target Costing, BETA can plan in advance the price points, product costs and margins

that it wants to attain for a particular product. If the product cannot be produced at this planned

level then the complete product design is cancelled. It is a good tool in the hands of management

where a continuous evaluation is done right from design stage to its actual production stage.

This is beneficial that shows commitment levels of management and staff to identify

areas of improvements and innovations that will help in getting a competitive advantage over

rival firms (Gonçalves, Gaio, and Silva, 2018). In this type of costing, BETA can create a

product after examining the market which leads to full customer satisfaction. Here, new market

opportunities can be tapped by company and converted into products to reduce the production

costs. The formula for calculating target cost is as follows:

Target Costing = Selling Price – Profit Margin

Establishment of standard is a very difficult task which involves a lot of scientific

evaluation such as time study, motion study, etc. Along with this, it is costly due to which

small firms cannot operate on this system.

Such rigid estimations once set cannot be altered for a certain time period. It is not

applicable in industries which faces regular price fluctuations. Updating the standards is

also a tough job because of its costly nature.

Setting standards is much tedious job because a loose standard will not be effective and

high standard may increase frustration levels in workers of BETA.

For industries like BETA producing tailor-made products cannot apply standard costing

(Iliemena and Amedu, 2019). Also, in industries where production normally takes more

than an accounting period, standard costing becomes a tough task to apply.

Identification of controllable and uncontrollable factors is not possible in this type of

costing because a particular person or process cannot be identified and evaluated. Generally, managers oppose this type of costing because of less freedom attached to it

which also has bad psychological effects.

II. Critically discussing Target costing and differentiating it from Standard Costing

Target Costing

In Target Costing, BETA can plan in advance the price points, product costs and margins

that it wants to attain for a particular product. If the product cannot be produced at this planned

level then the complete product design is cancelled. It is a good tool in the hands of management

where a continuous evaluation is done right from design stage to its actual production stage.

This is beneficial that shows commitment levels of management and staff to identify

areas of improvements and innovations that will help in getting a competitive advantage over

rival firms (Gonçalves, Gaio, and Silva, 2018). In this type of costing, BETA can create a

product after examining the market which leads to full customer satisfaction. Here, new market

opportunities can be tapped by company and converted into products to reduce the production

costs. The formula for calculating target cost is as follows:

Target Costing = Selling Price – Profit Margin

However, it is a very lengthy process due to many alterations that a product has to go

through at development process. In addition to this, it may reduce employee's morale and

motivation because of continuous cost reduction.

Difference between target & standard costing

Basis Target costing Standard costing

Definition It is the difference between

target price that will be paid by

potential customers and

associated profits.

It is a predetermined cost of

materials, labour, etc. for a certain

time period.

Purpose This helps a firm to remain in

the market for long time and

compete with rivals.

To calculate the major costs

associated with a product in the

future.

Usage Planning and designing stages of

product and reducing costs.

Main usage is to control the costs so

that BETA does not incur high cost

and thereby, decrease profit levels.

Concept It is an old concept which is used

by manufacturing industries

especially.

It is a new concept given by

Japanese.

Time frame Cost reduction techniques are

applied on a regular and

continuous basis.

Standards are updated annually or

after a particular business cycle.

Control Here, focus is on keeping the

costs at minimum levels

(Differences Between

Traditional Method of Costing

and Target Costing, 2021).

The emphasis is given to keep the

costs within predetermined costs.

Variances are calculated to measure

control.

through at development process. In addition to this, it may reduce employee's morale and

motivation because of continuous cost reduction.

Difference between target & standard costing

Basis Target costing Standard costing

Definition It is the difference between

target price that will be paid by

potential customers and

associated profits.

It is a predetermined cost of

materials, labour, etc. for a certain

time period.

Purpose This helps a firm to remain in

the market for long time and

compete with rivals.

To calculate the major costs

associated with a product in the

future.

Usage Planning and designing stages of

product and reducing costs.

Main usage is to control the costs so

that BETA does not incur high cost

and thereby, decrease profit levels.

Concept It is an old concept which is used

by manufacturing industries

especially.

It is a new concept given by

Japanese.

Time frame Cost reduction techniques are

applied on a regular and

continuous basis.

Standards are updated annually or

after a particular business cycle.

Control Here, focus is on keeping the

costs at minimum levels

(Differences Between

Traditional Method of Costing

and Target Costing, 2021).

The emphasis is given to keep the

costs within predetermined costs.

Variances are calculated to measure

control.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

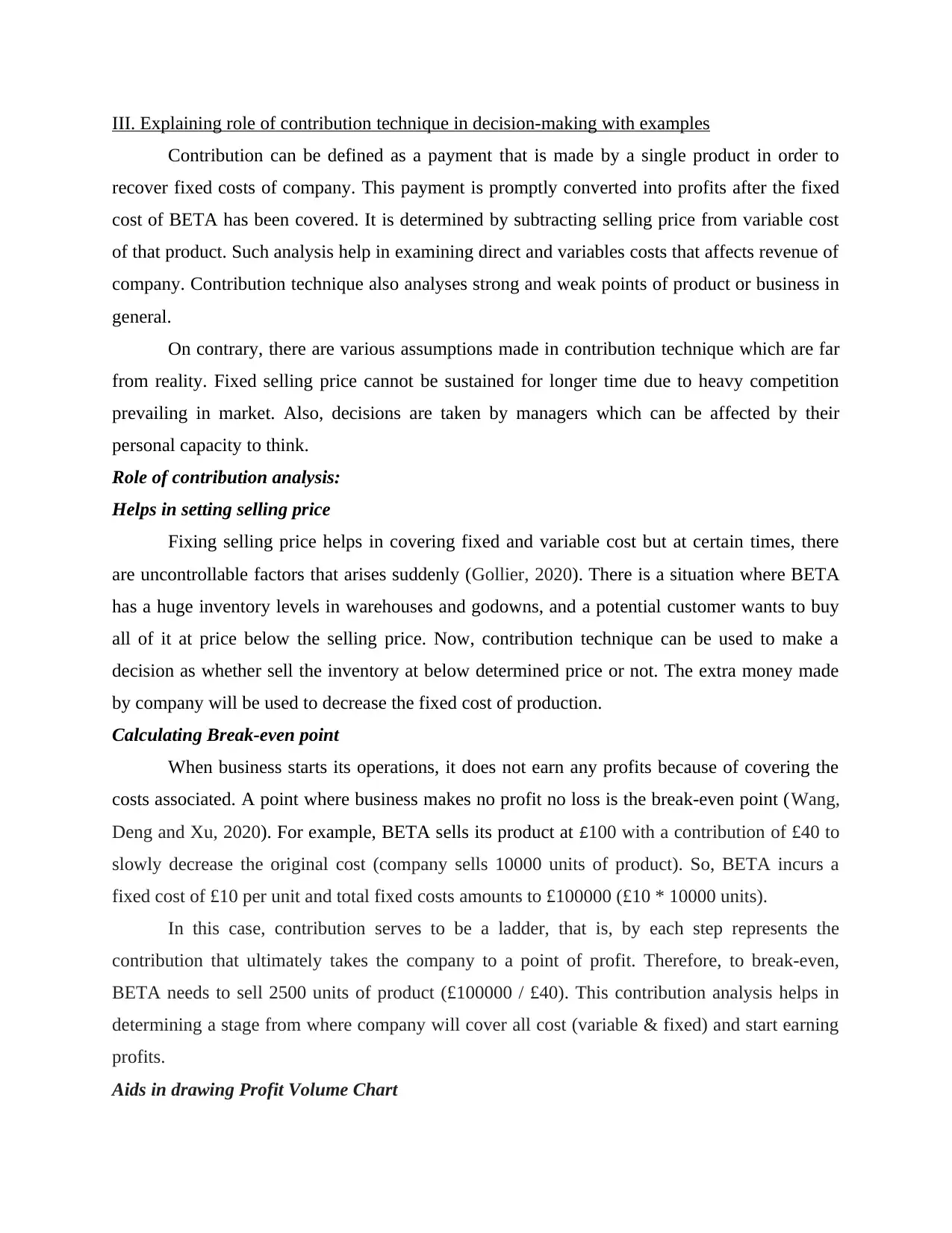

III. Explaining role of contribution technique in decision-making with examples

Contribution can be defined as a payment that is made by a single product in order to

recover fixed costs of company. This payment is promptly converted into profits after the fixed

cost of BETA has been covered. It is determined by subtracting selling price from variable cost

of that product. Such analysis help in examining direct and variables costs that affects revenue of

company. Contribution technique also analyses strong and weak points of product or business in

general.

On contrary, there are various assumptions made in contribution technique which are far

from reality. Fixed selling price cannot be sustained for longer time due to heavy competition

prevailing in market. Also, decisions are taken by managers which can be affected by their

personal capacity to think.

Role of contribution analysis:

Helps in setting selling price

Fixing selling price helps in covering fixed and variable cost but at certain times, there

are uncontrollable factors that arises suddenly (Gollier, 2020). There is a situation where BETA

has a huge inventory levels in warehouses and godowns, and a potential customer wants to buy

all of it at price below the selling price. Now, contribution technique can be used to make a

decision as whether sell the inventory at below determined price or not. The extra money made

by company will be used to decrease the fixed cost of production.

Calculating Break-even point

When business starts its operations, it does not earn any profits because of covering the

costs associated. A point where business makes no profit no loss is the break-even point (Wang,

Deng and Xu, 2020). For example, BETA sells its product at £100 with a contribution of £40 to

slowly decrease the original cost (company sells 10000 units of product). So, BETA incurs a

fixed cost of £10 per unit and total fixed costs amounts to £100000 (£10 * 10000 units).

In this case, contribution serves to be a ladder, that is, by each step represents the

contribution that ultimately takes the company to a point of profit. Therefore, to break-even,

BETA needs to sell 2500 units of product (£100000 / £40). This contribution analysis helps in

determining a stage from where company will cover all cost (variable & fixed) and start earning

profits.

Aids in drawing Profit Volume Chart

Contribution can be defined as a payment that is made by a single product in order to

recover fixed costs of company. This payment is promptly converted into profits after the fixed

cost of BETA has been covered. It is determined by subtracting selling price from variable cost

of that product. Such analysis help in examining direct and variables costs that affects revenue of

company. Contribution technique also analyses strong and weak points of product or business in

general.

On contrary, there are various assumptions made in contribution technique which are far

from reality. Fixed selling price cannot be sustained for longer time due to heavy competition

prevailing in market. Also, decisions are taken by managers which can be affected by their

personal capacity to think.

Role of contribution analysis:

Helps in setting selling price

Fixing selling price helps in covering fixed and variable cost but at certain times, there

are uncontrollable factors that arises suddenly (Gollier, 2020). There is a situation where BETA

has a huge inventory levels in warehouses and godowns, and a potential customer wants to buy

all of it at price below the selling price. Now, contribution technique can be used to make a

decision as whether sell the inventory at below determined price or not. The extra money made

by company will be used to decrease the fixed cost of production.

Calculating Break-even point

When business starts its operations, it does not earn any profits because of covering the

costs associated. A point where business makes no profit no loss is the break-even point (Wang,

Deng and Xu, 2020). For example, BETA sells its product at £100 with a contribution of £40 to

slowly decrease the original cost (company sells 10000 units of product). So, BETA incurs a

fixed cost of £10 per unit and total fixed costs amounts to £100000 (£10 * 10000 units).

In this case, contribution serves to be a ladder, that is, by each step represents the

contribution that ultimately takes the company to a point of profit. Therefore, to break-even,

BETA needs to sell 2500 units of product (£100000 / £40). This contribution analysis helps in

determining a stage from where company will cover all cost (variable & fixed) and start earning

profits.

Aids in drawing Profit Volume Chart

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

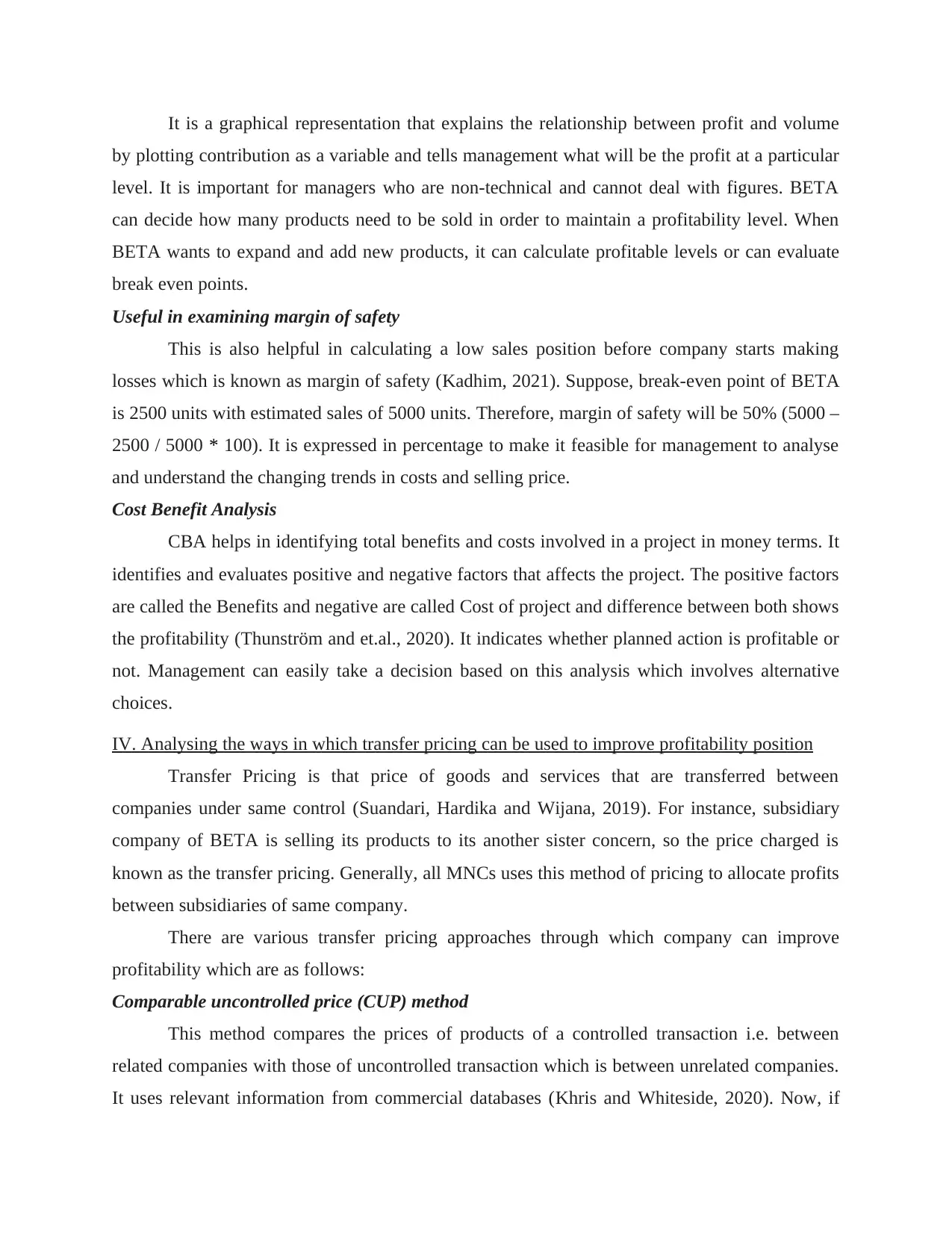

It is a graphical representation that explains the relationship between profit and volume

by plotting contribution as a variable and tells management what will be the profit at a particular

level. It is important for managers who are non-technical and cannot deal with figures. BETA

can decide how many products need to be sold in order to maintain a profitability level. When

BETA wants to expand and add new products, it can calculate profitable levels or can evaluate

break even points.

Useful in examining margin of safety

This is also helpful in calculating a low sales position before company starts making

losses which is known as margin of safety (Kadhim, 2021). Suppose, break-even point of BETA

is 2500 units with estimated sales of 5000 units. Therefore, margin of safety will be 50% (5000 –

2500 / 5000 * 100). It is expressed in percentage to make it feasible for management to analyse

and understand the changing trends in costs and selling price.

Cost Benefit Analysis

CBA helps in identifying total benefits and costs involved in a project in money terms. It

identifies and evaluates positive and negative factors that affects the project. The positive factors

are called the Benefits and negative are called Cost of project and difference between both shows

the profitability (Thunström and et.al., 2020). It indicates whether planned action is profitable or

not. Management can easily take a decision based on this analysis which involves alternative

choices.

IV. Analysing the ways in which transfer pricing can be used to improve profitability position

Transfer Pricing is that price of goods and services that are transferred between

companies under same control (Suandari, Hardika and Wijana, 2019). For instance, subsidiary

company of BETA is selling its products to its another sister concern, so the price charged is

known as the transfer pricing. Generally, all MNCs uses this method of pricing to allocate profits

between subsidiaries of same company.

There are various transfer pricing approaches through which company can improve

profitability which are as follows:

Comparable uncontrolled price (CUP) method

This method compares the prices of products of a controlled transaction i.e. between

related companies with those of uncontrolled transaction which is between unrelated companies.

It uses relevant information from commercial databases (Khris and Whiteside, 2020). Now, if

by plotting contribution as a variable and tells management what will be the profit at a particular

level. It is important for managers who are non-technical and cannot deal with figures. BETA

can decide how many products need to be sold in order to maintain a profitability level. When

BETA wants to expand and add new products, it can calculate profitable levels or can evaluate

break even points.

Useful in examining margin of safety

This is also helpful in calculating a low sales position before company starts making

losses which is known as margin of safety (Kadhim, 2021). Suppose, break-even point of BETA

is 2500 units with estimated sales of 5000 units. Therefore, margin of safety will be 50% (5000 –

2500 / 5000 * 100). It is expressed in percentage to make it feasible for management to analyse

and understand the changing trends in costs and selling price.

Cost Benefit Analysis

CBA helps in identifying total benefits and costs involved in a project in money terms. It

identifies and evaluates positive and negative factors that affects the project. The positive factors

are called the Benefits and negative are called Cost of project and difference between both shows

the profitability (Thunström and et.al., 2020). It indicates whether planned action is profitable or

not. Management can easily take a decision based on this analysis which involves alternative

choices.

IV. Analysing the ways in which transfer pricing can be used to improve profitability position

Transfer Pricing is that price of goods and services that are transferred between

companies under same control (Suandari, Hardika and Wijana, 2019). For instance, subsidiary

company of BETA is selling its products to its another sister concern, so the price charged is

known as the transfer pricing. Generally, all MNCs uses this method of pricing to allocate profits

between subsidiaries of same company.

There are various transfer pricing approaches through which company can improve

profitability which are as follows:

Comparable uncontrolled price (CUP) method

This method compares the prices of products of a controlled transaction i.e. between

related companies with those of uncontrolled transaction which is between unrelated companies.

It uses relevant information from commercial databases (Khris and Whiteside, 2020). Now, if

different prices are quoted in two transaction, it suggests that Arms's length principle cannot be

implemented. In such situations, OECD says that price between unrelated parties should not be

substituted for price for related parties.

BETA uses this method when a product is sold to its subsidiaries and a similar product is

sold by another company. The two transactions are comparable if situations are same. But if

there are differences, then BETA will determine whether this affected the price or not. However,

external and internal market may not match these criteria and commodity prices are highly

volatile.

Resale Price method

In this method, that price is taken at which associated company sells their product to

another third party. Gross margin is calculated by making comparisons of gross margin in

comparable transaction which is then deduced from resale price (Juranek Schindler and

Schjelderup, 2018). This method needs to assure that third party transactions can be compared

with controlled one. On contrary, it is only suitable for resellers and distributors and not for

manufacturers like BETA. Also, it is tough to meet requirement because of uniqueness of

transaction.

Cost-Plus-Percent Method

Here, transactions are compared between gross profit and cost of sales. It means cost of

transaction is calculated by supplying party and then adding a markup profit on products

delivered. Markup percentage can be the desirable level of profit earned by third party in

comparable party (Gjorgieva-Trajkovska and et.al., 2019). Suppose, BETA manufactures

product A and sells it to associated company in another country. From this transaction, BETA

earns a profit markup and does not include operating expenses in its cost. Another company

manufactures product similar to product A and sells it by including operating expenses in cost.

Therefore, profit markup by that company needs to be adjusted so that it can be compared with

BETA.

Transactional net margin method (TNMM)

TNM method assesses net profit by taking an “appropriate base” for example, sales or

fixed assets which results from controlled transactions. After this, net profit is determined from

comparable uncontrolled transaction taken from same base. It then, adjusts differences that do

not affect net profit in open market and finally adjusts profit by establishing Arm's length price

implemented. In such situations, OECD says that price between unrelated parties should not be

substituted for price for related parties.

BETA uses this method when a product is sold to its subsidiaries and a similar product is

sold by another company. The two transactions are comparable if situations are same. But if

there are differences, then BETA will determine whether this affected the price or not. However,

external and internal market may not match these criteria and commodity prices are highly

volatile.

Resale Price method

In this method, that price is taken at which associated company sells their product to

another third party. Gross margin is calculated by making comparisons of gross margin in

comparable transaction which is then deduced from resale price (Juranek Schindler and

Schjelderup, 2018). This method needs to assure that third party transactions can be compared

with controlled one. On contrary, it is only suitable for resellers and distributors and not for

manufacturers like BETA. Also, it is tough to meet requirement because of uniqueness of

transaction.

Cost-Plus-Percent Method

Here, transactions are compared between gross profit and cost of sales. It means cost of

transaction is calculated by supplying party and then adding a markup profit on products

delivered. Markup percentage can be the desirable level of profit earned by third party in

comparable party (Gjorgieva-Trajkovska and et.al., 2019). Suppose, BETA manufactures

product A and sells it to associated company in another country. From this transaction, BETA

earns a profit markup and does not include operating expenses in its cost. Another company

manufactures product similar to product A and sells it by including operating expenses in cost.

Therefore, profit markup by that company needs to be adjusted so that it can be compared with

BETA.

Transactional net margin method (TNMM)

TNM method assesses net profit by taking an “appropriate base” for example, sales or

fixed assets which results from controlled transactions. After this, net profit is determined from

comparable uncontrolled transaction taken from same base. It then, adjusts differences that do

not affect net profit in open market and finally adjusts profit by establishing Arm's length price

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Understanding TNMM In A Simple Way, 2021). It is commonly applied to industries like BETA

which provides business solutions, distributes finished goods or transfers semi-finished goods.

CONCLUSION

From the above report, it can be concluded that standard costing helps in setting

standards against which the actual performance can be evaluated and necessary actions can be

taken. However, it cannot be applied to companies where tailor-made goods are produced.

Further, it can also be said that target costing helps in examining the product continuously right

from design stage to its actual production. Report also examined that standard costing is an old

concept which is being used by companies from long time. In contrast to it, target costing is a

new method put to use by industries.

In addition to this, study also identified major role of contribution techniques in

evaluating break-even point, selling price, margin of safety, etc. Lastly, report mentioned the

importance of transfer pricing approaches through which business performance can be improved.

which provides business solutions, distributes finished goods or transfers semi-finished goods.

CONCLUSION

From the above report, it can be concluded that standard costing helps in setting

standards against which the actual performance can be evaluated and necessary actions can be

taken. However, it cannot be applied to companies where tailor-made goods are produced.

Further, it can also be said that target costing helps in examining the product continuously right

from design stage to its actual production. Report also examined that standard costing is an old

concept which is being used by companies from long time. In contrast to it, target costing is a

new method put to use by industries.

In addition to this, study also identified major role of contribution techniques in

evaluating break-even point, selling price, margin of safety, etc. Lastly, report mentioned the

importance of transfer pricing approaches through which business performance can be improved.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Gjorgieva-Trajkovska, O. and et.al., 2019. Transfer pricing–definition and methods. Knowledge

International Journal. 35(1). pp.167-173.

Gollier, C., 2020. Cost–benefit analysis of age‐specific deconfinement strategies. Journal of

Public Economic Theory. 22(6). pp.1746-1771.

Gonçalves, T., Gaio, C. and Silva, M., 2018. Target costing and innovation-exploratory

configurations: A comparison of fsQCA, multivariate regression, and variable cluster

analysis. Journal of Business Research. 89. pp.378-384.

Iliemena, R. O. and Amedu, J. M., 2019. Effect of standard costing on profitability of

manufacturing companies: study of Edo State Nigeria. Journal of Resources Development

and Management. 53(3). pp.28-34.

Juranek, S., Schindler, D. and Schjelderup, G., 2018. Transfer pricing regulation and taxation of

royalty payments. Journal of Public Economic Theory. 20(1). pp.67-84.

Kadhim, Z. R., 2021. Margin of Safety of Hiring Decision of Agricultural Machinery Services

by Rice Farmers in Alnajaf Al-Ashraf Province. IRAQI JOURNAL OF AGRICULTURAL

SCIENCES. 52(3). pp.756-762.

Khris, B. and Whiteside, M., 2020. Transfer Pricing: Purpose of Determination and Factors

Affecting Transfer Pricing Determination. Journal Dimensie Management and Public

Sector. 1(2). pp.27-34.

Kristensen, T. B., 2021. Enabling use of standard variable costing in lean production. Production

Planning & Control. 32(3). pp.169-184.

Paul, D. D., 2020. STANDARD COSTING AND ABC: A COEXISTENCE. Strategic Finance.

101(11). pp.32-39.

Suandari, N. K., Hardika, N. S. and Wijana, I. M., 2019. Analysis of Transfer Pricing Method

Determination in Transfer Pricing Documentation Practice at PT ABC Denpasar. Journal

of Applied Sciences in Accounting, Finance, and Tax. 2(1). pp.51-55.

Thunström, L. and et.al., 2020. The benefits and costs of using social distancing to flatten the

curve for COVID-19. Journal of Benefit-Cost Analysis. 11(2). pp.179-195.

Wang, Q., Deng, L. and Xu, G., 2020. Operational subsidy optimization in urban rail transit

under the break-even mode: considering two fare regimes. Computers & Industrial

Engineering. 149. p.106739.

Online

Differences Between Traditional Method of Costing and Target Costing. 2021. [Online].

Available through: <https://accountlearning.com/differences-traditional-method-costing-

target-costing/>

Understanding TNMM In A Simple Way. 2021. [Online]. Available through:

<https://taxguru.in/income-tax/understanding-tnmm-simple.html>

Books and Journals

Gjorgieva-Trajkovska, O. and et.al., 2019. Transfer pricing–definition and methods. Knowledge

International Journal. 35(1). pp.167-173.

Gollier, C., 2020. Cost–benefit analysis of age‐specific deconfinement strategies. Journal of

Public Economic Theory. 22(6). pp.1746-1771.

Gonçalves, T., Gaio, C. and Silva, M., 2018. Target costing and innovation-exploratory

configurations: A comparison of fsQCA, multivariate regression, and variable cluster

analysis. Journal of Business Research. 89. pp.378-384.

Iliemena, R. O. and Amedu, J. M., 2019. Effect of standard costing on profitability of

manufacturing companies: study of Edo State Nigeria. Journal of Resources Development

and Management. 53(3). pp.28-34.

Juranek, S., Schindler, D. and Schjelderup, G., 2018. Transfer pricing regulation and taxation of

royalty payments. Journal of Public Economic Theory. 20(1). pp.67-84.

Kadhim, Z. R., 2021. Margin of Safety of Hiring Decision of Agricultural Machinery Services

by Rice Farmers in Alnajaf Al-Ashraf Province. IRAQI JOURNAL OF AGRICULTURAL

SCIENCES. 52(3). pp.756-762.

Khris, B. and Whiteside, M., 2020. Transfer Pricing: Purpose of Determination and Factors

Affecting Transfer Pricing Determination. Journal Dimensie Management and Public

Sector. 1(2). pp.27-34.

Kristensen, T. B., 2021. Enabling use of standard variable costing in lean production. Production

Planning & Control. 32(3). pp.169-184.

Paul, D. D., 2020. STANDARD COSTING AND ABC: A COEXISTENCE. Strategic Finance.

101(11). pp.32-39.

Suandari, N. K., Hardika, N. S. and Wijana, I. M., 2019. Analysis of Transfer Pricing Method

Determination in Transfer Pricing Documentation Practice at PT ABC Denpasar. Journal

of Applied Sciences in Accounting, Finance, and Tax. 2(1). pp.51-55.

Thunström, L. and et.al., 2020. The benefits and costs of using social distancing to flatten the

curve for COVID-19. Journal of Benefit-Cost Analysis. 11(2). pp.179-195.

Wang, Q., Deng, L. and Xu, G., 2020. Operational subsidy optimization in urban rail transit

under the break-even mode: considering two fare regimes. Computers & Industrial

Engineering. 149. p.106739.

Online

Differences Between Traditional Method of Costing and Target Costing. 2021. [Online].

Available through: <https://accountlearning.com/differences-traditional-method-costing-

target-costing/>

Understanding TNMM In A Simple Way. 2021. [Online]. Available through:

<https://taxguru.in/income-tax/understanding-tnmm-simple.html>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.