AAMC Training - Loan Application Process Assessment - FNSFMB401

VerifiedAdded on 2022/08/15

|27

|9531

|12

Homework Assignment

AI Summary

This document presents a comprehensive assessment of the loan application process, designed for students in finance and mortgage broking courses. The assessment includes a detailed case study (with options for residential mortgages and plant & equipment/motor vehicle finance), requiring students to prepare a loan file from initial client contact through to application preparation and lodgment. Students are expected to demonstrate competency in communication, information gathering and analysis, planning, teamwork, problem-solving, and technology use. The case study involves a detailed fact find, client needs review, and the selection of appropriate loan products, while also considering relevant financial regulations and client risk protection. The assessment emphasizes practical application and requires the inclusion of supporting documentation, such as client details, employment information, and proposed property details. Students must also consider the impact of local regulations and stamp duty concessions. The assessment includes multiple tasks, including short answer questions, case studies, and workplace projects, and requires students to submit a cover sheet and skills sign-off forms. The document stresses the importance of original work, adherence to assessment guidelines, and proper referencing.

Loan Application Process

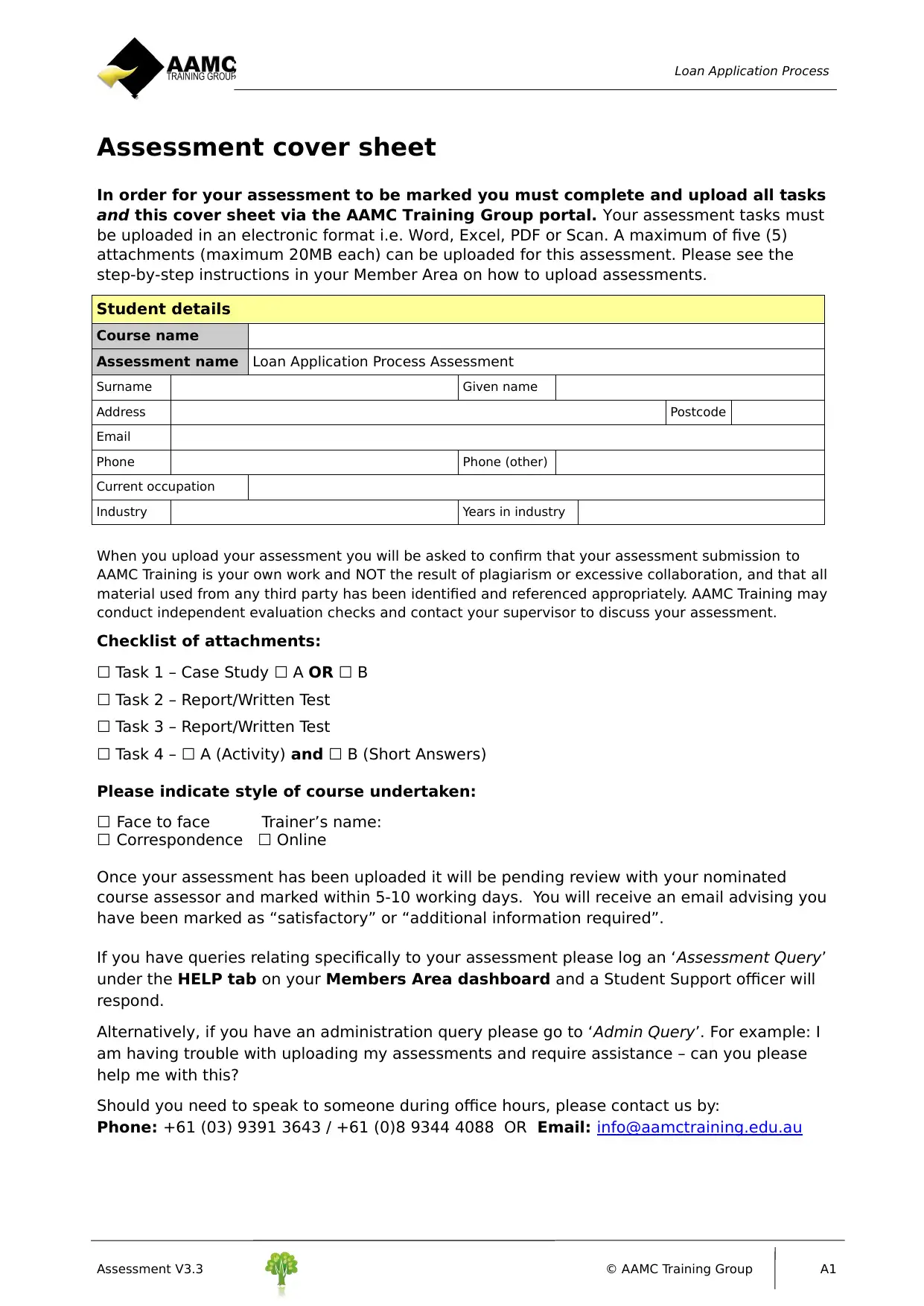

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. A maximum of five (5)

attachments (maximum 20MB each) can be uploaded for this assessment. Please see the

step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name

Assessment name Loan Application Process Assessment

Surname Given name

Address Postcode

Email

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment submission to

AAMC Training is your own work and NOT the result of plagiarism or excessive collaboration, and that all

material used from any third party has been identified and referenced appropriately. AAMC Training may

conduct independent evaluation checks and contact your supervisor to discuss your assessment.

Checklist of attachments:

☐ Task 1 – Case Study ☐ A OR ☐ B

☐ Task 2 – Report/Written Test

☐ Task 3 – Report/Written Test

☐ Task 4 – ☐ A (Activity) and ☐ B (Short Answers)

Please indicate style of course undertaken:

☐ Face to face Trainer’s name:

☐ Correspondence ☐ Online

Once your assessment has been uploaded it will be pending review with your nominated

course assessor and marked within 5-10 working days. You will receive an email advising you

have been marked as “satisfactory” or “additional information required”.

If you have queries relating specifically to your assessment please log an ‘Assessment Query’

under the HELP tab on your Members Area dashboard and a Student Support officer will

respond.

Alternatively, if you have an administration query please go to ‘Admin Query’. For example: I

am having trouble with uploading my assessments and require assistance – can you please

help me with this?

Should you need to speak to someone during office hours, please contact us by:

Phone: +61 (03) 9391 3643 / +61 (0)8 9344 4088 OR Email: info@aamctraining.edu.au

Assessment V3.3 © AAMC Training Group A1

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. A maximum of five (5)

attachments (maximum 20MB each) can be uploaded for this assessment. Please see the

step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name

Assessment name Loan Application Process Assessment

Surname Given name

Address Postcode

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment submission to

AAMC Training is your own work and NOT the result of plagiarism or excessive collaboration, and that all

material used from any third party has been identified and referenced appropriately. AAMC Training may

conduct independent evaluation checks and contact your supervisor to discuss your assessment.

Checklist of attachments:

☐ Task 1 – Case Study ☐ A OR ☐ B

☐ Task 2 – Report/Written Test

☐ Task 3 – Report/Written Test

☐ Task 4 – ☐ A (Activity) and ☐ B (Short Answers)

Please indicate style of course undertaken:

☐ Face to face Trainer’s name:

☐ Correspondence ☐ Online

Once your assessment has been uploaded it will be pending review with your nominated

course assessor and marked within 5-10 working days. You will receive an email advising you

have been marked as “satisfactory” or “additional information required”.

If you have queries relating specifically to your assessment please log an ‘Assessment Query’

under the HELP tab on your Members Area dashboard and a Student Support officer will

respond.

Alternatively, if you have an administration query please go to ‘Admin Query’. For example: I

am having trouble with uploading my assessments and require assistance – can you please

help me with this?

Should you need to speak to someone during office hours, please contact us by:

Phone: +61 (03) 9391 3643 / +61 (0)8 9344 4088 OR Email: info@aamctraining.edu.au

Assessment V3.3 © AAMC Training Group A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Loan Application Process

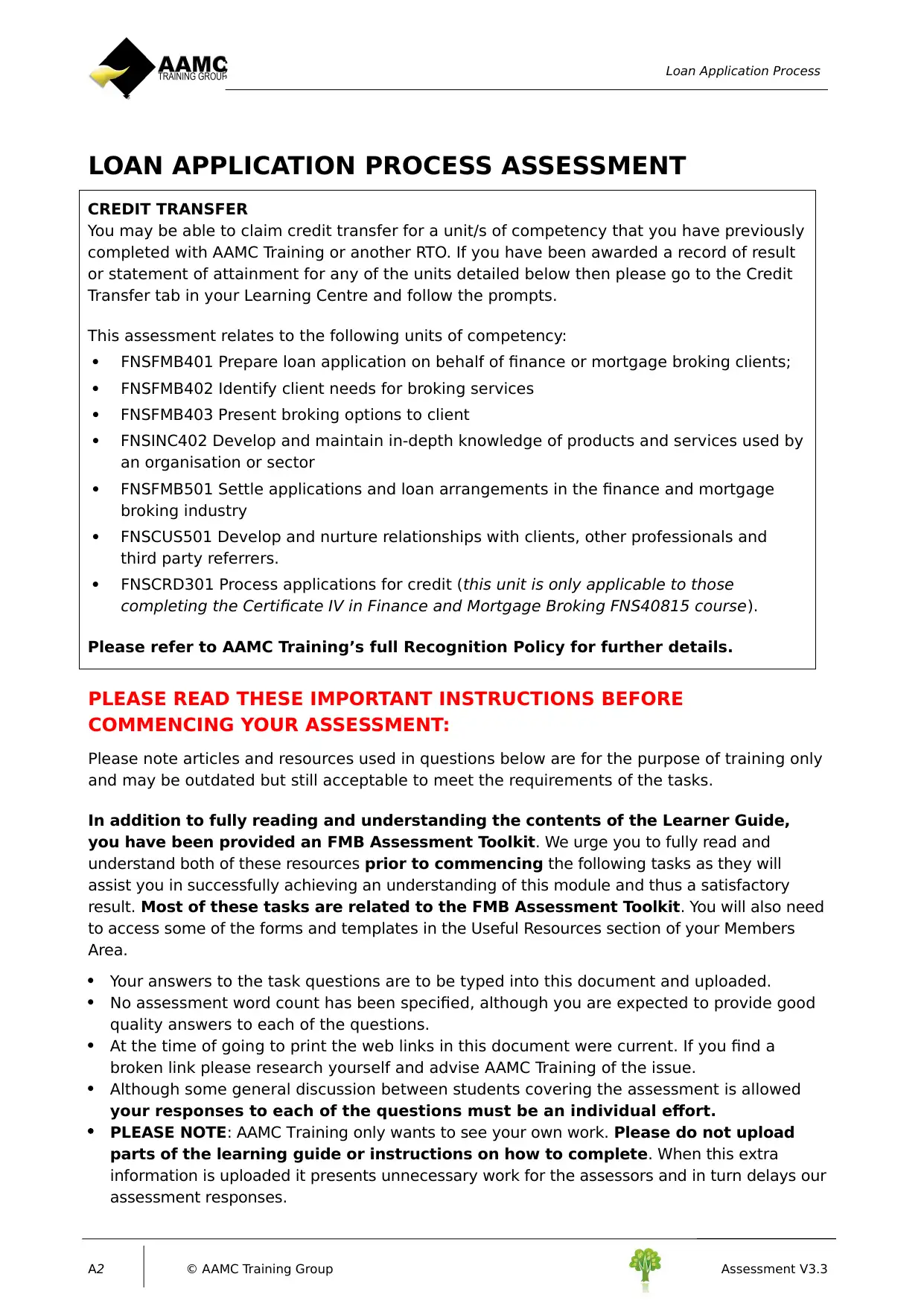

LOAN APPLICATION PROCESS ASSESSMENT

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result

or statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

FNSFMB401 Prepare loan application on behalf of finance or mortgage broking clients;

FNSFMB402 Identify client needs for broking services

FNSFMB403 Present broking options to client

FNSINC402 Develop and maintain in-depth knowledge of products and services used by

an organisation or sector

FNSFMB501 Settle applications and loan arrangements in the finance and mortgage

broking industry

FNSCUS501 Develop and nurture relationships with clients, other professionals and

third party referrers.

FNSCRD301 Process applications for credit (this unit is only applicable to those

completing the Certificate IV in Finance and Mortgage Broking FNS40815 course).

Please refer to AAMC Training’s full Recognition Policy for further details.

PLEASE READ THESE IMPORTANT INSTRUCTIONS BEFORE

COMMENCING YOUR ASSESSMENT:

Please note articles and resources used in questions below are for the purpose of training only

and may be outdated but still acceptable to meet the requirements of the tasks.

In addition to fully reading and understanding the contents of the Learner Guide,

you have been provided an FMB Assessment Toolkit. We urge you to fully read and

understand both of these resources prior to commencing the following tasks as they will

assist you in successfully achieving an understanding of this module and thus a satisfactory

result. Most of these tasks are related to the FMB Assessment Toolkit. You will also need

to access some of the forms and templates in the Useful Resources section of your Members

Area.

Your answers to the task questions are to be typed into this document and uploaded.

No assessment word count has been specified, although you are expected to provide good

quality answers to each of the questions.

At the time of going to print the web links in this document were current. If you find a

broken link please research yourself and advise AAMC Training of the issue.

Although some general discussion between students covering the assessment is allowed

your responses to each of the questions must be an individual effort.

PLEASE NOTE: AAMC Training only wants to see your own work. Please do not upload

parts of the learning guide or instructions on how to complete. When this extra

information is uploaded it presents unnecessary work for the assessors and in turn delays our

assessment responses.

A2 © AAMC Training Group Assessment V3.3

LOAN APPLICATION PROCESS ASSESSMENT

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result

or statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

FNSFMB401 Prepare loan application on behalf of finance or mortgage broking clients;

FNSFMB402 Identify client needs for broking services

FNSFMB403 Present broking options to client

FNSINC402 Develop and maintain in-depth knowledge of products and services used by

an organisation or sector

FNSFMB501 Settle applications and loan arrangements in the finance and mortgage

broking industry

FNSCUS501 Develop and nurture relationships with clients, other professionals and

third party referrers.

FNSCRD301 Process applications for credit (this unit is only applicable to those

completing the Certificate IV in Finance and Mortgage Broking FNS40815 course).

Please refer to AAMC Training’s full Recognition Policy for further details.

PLEASE READ THESE IMPORTANT INSTRUCTIONS BEFORE

COMMENCING YOUR ASSESSMENT:

Please note articles and resources used in questions below are for the purpose of training only

and may be outdated but still acceptable to meet the requirements of the tasks.

In addition to fully reading and understanding the contents of the Learner Guide,

you have been provided an FMB Assessment Toolkit. We urge you to fully read and

understand both of these resources prior to commencing the following tasks as they will

assist you in successfully achieving an understanding of this module and thus a satisfactory

result. Most of these tasks are related to the FMB Assessment Toolkit. You will also need

to access some of the forms and templates in the Useful Resources section of your Members

Area.

Your answers to the task questions are to be typed into this document and uploaded.

No assessment word count has been specified, although you are expected to provide good

quality answers to each of the questions.

At the time of going to print the web links in this document were current. If you find a

broken link please research yourself and advise AAMC Training of the issue.

Although some general discussion between students covering the assessment is allowed

your responses to each of the questions must be an individual effort.

PLEASE NOTE: AAMC Training only wants to see your own work. Please do not upload

parts of the learning guide or instructions on how to complete. When this extra

information is uploaded it presents unnecessary work for the assessors and in turn delays our

assessment responses.

A2 © AAMC Training Group Assessment V3.3

Loan Application Process

Task 1: You will notice that there are two options of Case Study within this assessment – the

first (A) is more specifically for Mortgage Brokers, the second (B) for brokers in the Plant &

Equipment and Motor Vehicle field. Please complete only the stream relevant to you

and indicate this on the assessment cover sheet.

Either the Mortgage Finance or Motor Vehicle Equipment Checklist must be submitted with the

fully completed assessment. This must encompass all documents from initial contact with the

clients through to settlement of the loan. Documents must be submitted in a suitable logical

order as listed on the checklists and consist of all relevant NCCP documents.

The documentation required should be consistent for all submissions, however student

submissions will vary in regards to outcomes based on the interpretation of the data and

“client” responses during the interview process.

As you are aware, our learning centre allows for 5 uploads per assessment (max 20MB per

file). As there are many attachments required for this assessment, you may wish to embed

documents as a way of minimising document uploads. Please see instructions on how to do

this if you are not familiar with this practice.

Assessment V3.3 © AAMC Training Group A3

Task 1: You will notice that there are two options of Case Study within this assessment – the

first (A) is more specifically for Mortgage Brokers, the second (B) for brokers in the Plant &

Equipment and Motor Vehicle field. Please complete only the stream relevant to you

and indicate this on the assessment cover sheet.

Either the Mortgage Finance or Motor Vehicle Equipment Checklist must be submitted with the

fully completed assessment. This must encompass all documents from initial contact with the

clients through to settlement of the loan. Documents must be submitted in a suitable logical

order as listed on the checklists and consist of all relevant NCCP documents.

The documentation required should be consistent for all submissions, however student

submissions will vary in regards to outcomes based on the interpretation of the data and

“client” responses during the interview process.

As you are aware, our learning centre allows for 5 uploads per assessment (max 20MB per

file). As there are many attachments required for this assessment, you may wish to embed

documents as a way of minimising document uploads. Please see instructions on how to do

this if you are not familiar with this practice.

Assessment V3.3 © AAMC Training Group A3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Loan Application Process

Task 1: Case Study – Loan application preparation

You will notice that there are two options of Case Study within this assessment –

the first (A) is more specifically for Mortgage Brokers, the second (B) for brokers in

the Plant & Equipment and Motor Vehicle field. Please complete only the stream

relevant to you and indicate this on the assessment cover sheet.

Choosing one of the case studies presented below, prepare a loan file from contact with the

clients to preparing the loan application for lodgement with the client’s lender of choice.

In completing this task, you need to demonstrate to your assessor that you are competent in

the following areas and able to:

communicate ideas and information

collect, analyse and organise information

plan and organise activities

work with others in a team

use mathematical ideas and techniques

solve problems by providing solutions

use technology.

To do this you will need to compile a report (Client Needs Review/Fact Find) indicating your

thoughts and processes on different aspects of your application. These may include, but are

not limited to:

the choice of loan product for your client and the information about the loan product that

you presented to them. Where you located the product information. Remember there is no

right/wrong answer to this area, it is always subjective.

the use of technology to compare the product/fees, find information on the products etc.

how you would work in a team situation with your co-workers, lenders, real estate agents,

mentor etc.

In areas where you do not have copies of actual supporting documentation, insert a page with the

name of the document you would include e.g. copy of driver’s licence for the client.

There are a number of templates in the Member’s Area under ‘Useful Resources’ that you

could use in your submission.

Remember there is no right or wrong answer as each client you see presents a new challenge

and if you can provide solutions for those challenges you will be well regarded and successful

in this industry.

Because this course is taken nationally, we ask that you localise addresses and

places of employment so that you can have familiarity with the assessment.

You will have to take into account any necessary adjustment of stamp duty

concessions for first home buyers. This will have to be considered when discussing

and setting out the fees and costs with your clients. You will have to contact your

Office of State Revenue to determine the correct amount of benefits to which your

clients are entitled.

A4 © AAMC Training Group Assessment V3.3

Task 1: Case Study – Loan application preparation

You will notice that there are two options of Case Study within this assessment –

the first (A) is more specifically for Mortgage Brokers, the second (B) for brokers in

the Plant & Equipment and Motor Vehicle field. Please complete only the stream

relevant to you and indicate this on the assessment cover sheet.

Choosing one of the case studies presented below, prepare a loan file from contact with the

clients to preparing the loan application for lodgement with the client’s lender of choice.

In completing this task, you need to demonstrate to your assessor that you are competent in

the following areas and able to:

communicate ideas and information

collect, analyse and organise information

plan and organise activities

work with others in a team

use mathematical ideas and techniques

solve problems by providing solutions

use technology.

To do this you will need to compile a report (Client Needs Review/Fact Find) indicating your

thoughts and processes on different aspects of your application. These may include, but are

not limited to:

the choice of loan product for your client and the information about the loan product that

you presented to them. Where you located the product information. Remember there is no

right/wrong answer to this area, it is always subjective.

the use of technology to compare the product/fees, find information on the products etc.

how you would work in a team situation with your co-workers, lenders, real estate agents,

mentor etc.

In areas where you do not have copies of actual supporting documentation, insert a page with the

name of the document you would include e.g. copy of driver’s licence for the client.

There are a number of templates in the Member’s Area under ‘Useful Resources’ that you

could use in your submission.

Remember there is no right or wrong answer as each client you see presents a new challenge

and if you can provide solutions for those challenges you will be well regarded and successful

in this industry.

Because this course is taken nationally, we ask that you localise addresses and

places of employment so that you can have familiarity with the assessment.

You will have to take into account any necessary adjustment of stamp duty

concessions for first home buyers. This will have to be considered when discussing

and setting out the fees and costs with your clients. You will have to contact your

Office of State Revenue to determine the correct amount of benefits to which your

clients are entitled.

A4 © AAMC Training Group Assessment V3.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Loan Application Process

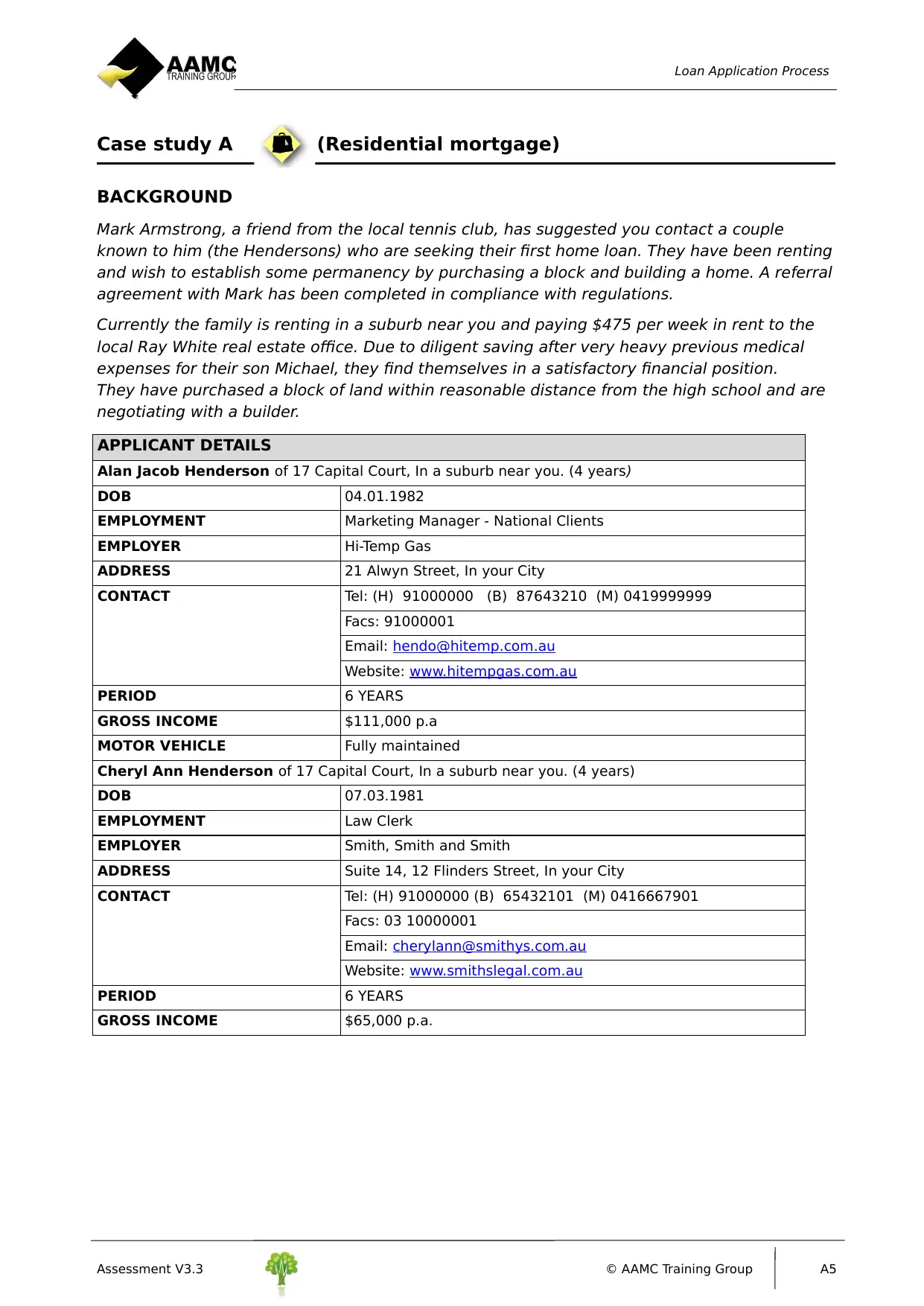

Case study A (Residential mortgage)

BACKGROUND

Mark Armstrong, a friend from the local tennis club, has suggested you contact a couple

known to him (the Hendersons) who are seeking their first home loan. They have been renting

and wish to establish some permanency by purchasing a block and building a home. A referral

agreement with Mark has been completed in compliance with regulations.

Currently the family is renting in a suburb near you and paying $475 per week in rent to the

local Ray White real estate office. Due to diligent saving after very heavy previous medical

expenses for their son Michael, they find themselves in a satisfactory financial position.

They have purchased a block of land within reasonable distance from the high school and are

negotiating with a builder.

APPLICANT DETAILS

Alan Jacob Henderson of 17 Capital Court, In a suburb near you. (4 years)

DOB 04.01.1982

EMPLOYMENT Marketing Manager - National Clients

EMPLOYER Hi-Temp Gas

ADDRESS 21 Alwyn Street, In your City

CONTACT Tel: (H) 91000000 (B) 87643210 (M) 0419999999

Facs: 91000001

Email: hendo@hitemp.com.au

Website: www.hitempgas.com.au

PERIOD 6 YEARS

GROSS INCOME $111,000 p.a

MOTOR VEHICLE Fully maintained

Cheryl Ann Henderson of 17 Capital Court, In a suburb near you. (4 years)

DOB 07.03.1981

EMPLOYMENT Law Clerk

EMPLOYER Smith, Smith and Smith

ADDRESS Suite 14, 12 Flinders Street, In your City

CONTACT Tel: (H) 91000000 (B) 65432101 (M) 0416667901

Facs: 03 10000001

Email: cherylann@smithys.com.au

Website: www.smithslegal.com.au

PERIOD 6 YEARS

GROSS INCOME $65,000 p.a.

Assessment V3.3 © AAMC Training Group A5

Case study A (Residential mortgage)

BACKGROUND

Mark Armstrong, a friend from the local tennis club, has suggested you contact a couple

known to him (the Hendersons) who are seeking their first home loan. They have been renting

and wish to establish some permanency by purchasing a block and building a home. A referral

agreement with Mark has been completed in compliance with regulations.

Currently the family is renting in a suburb near you and paying $475 per week in rent to the

local Ray White real estate office. Due to diligent saving after very heavy previous medical

expenses for their son Michael, they find themselves in a satisfactory financial position.

They have purchased a block of land within reasonable distance from the high school and are

negotiating with a builder.

APPLICANT DETAILS

Alan Jacob Henderson of 17 Capital Court, In a suburb near you. (4 years)

DOB 04.01.1982

EMPLOYMENT Marketing Manager - National Clients

EMPLOYER Hi-Temp Gas

ADDRESS 21 Alwyn Street, In your City

CONTACT Tel: (H) 91000000 (B) 87643210 (M) 0419999999

Facs: 91000001

Email: hendo@hitemp.com.au

Website: www.hitempgas.com.au

PERIOD 6 YEARS

GROSS INCOME $111,000 p.a

MOTOR VEHICLE Fully maintained

Cheryl Ann Henderson of 17 Capital Court, In a suburb near you. (4 years)

DOB 07.03.1981

EMPLOYMENT Law Clerk

EMPLOYER Smith, Smith and Smith

ADDRESS Suite 14, 12 Flinders Street, In your City

CONTACT Tel: (H) 91000000 (B) 65432101 (M) 0416667901

Facs: 03 10000001

Email: cherylann@smithys.com.au

Website: www.smithslegal.com.au

PERIOD 6 YEARS

GROSS INCOME $65,000 p.a.

Assessment V3.3 © AAMC Training Group A5

Loan Application Process

OTHER DETAILS

DEPENDENTS Jennifer Ann Henderson DOB 07.03.2004

Michael Alan Henderson DOB 07.03.2004

NEAREST RELATIVE NOT

LIVING WITH APPLICANT

John Joseph Henderson (Brother)

108 Budburst Ave, In a suburb near you

0410000000

BANK DETAILS NAB – BSB: 001 002 A/c Number: 1234567

REAL ESTATE AGENT Flying High Estate Agents

4 Birdsnest Avenue, In a suburb near you.

CONTACT: Hugh Talon

Tel: 10000700 Facs: 10000080

Email: hught@gmail.com

BULDER Homes Plus More (Master Builders)

38 Archdeacon Street West, In a suburb near you.

CONTACT: Grace Love

Tel: 40000000 Facs: 40000003

Email: grace@hpm.com.au

CONVEYANCING FIRM Lightning Settlements

Suite 3, 4 Business Ave, In a suburb near you.

CONTACT: Louise Stratton

Tel: 10004000 Facs: 10005000

Email: lulu@lightningsetts.com.au

PROPOSED ADDRESS Lot 47 Eaglehawk Circle, In a suburb near you.

LAND DESCRIPTION Lot 47 on Plan of Subdivision 731680Z

PARENT TITLE Volume 11580 Folio 996

Created by instrument PS725680G 04.04.2018

VENDOR Inspired Developments Pty Ltd

Suite 114/ 100 Bridge Road, In a suburb near you.

Tel: 50000001 Facs: 50000002

Email: Info @inspired.com.au

SETTLEMENT DATE 14/00/20XX

When completing your Fact Find/ Client Needs review please remember the Duty of Care.

One of the most important questions you should ask is about Risk Protection. Have the clients

considered the ramifications of financial hardship caused by illness, accident or death?

The Q & A component of the CNR covers this adequately. You are made aware their contents

are insured but they have no insurance policies covering life, trauma and income protection.

This is where you ask what cover they consider is enough in view of the financial

commitments they are now planning? Will Cheryl have to visit Centrelink if an unforeseen

event happens to Alan and vice versa? Should they have to change their lifestyle? Not if the

Broker carries out all the requirements to provide the clients’ needs.

A6 © AAMC Training Group Assessment V3.3

OTHER DETAILS

DEPENDENTS Jennifer Ann Henderson DOB 07.03.2004

Michael Alan Henderson DOB 07.03.2004

NEAREST RELATIVE NOT

LIVING WITH APPLICANT

John Joseph Henderson (Brother)

108 Budburst Ave, In a suburb near you

0410000000

BANK DETAILS NAB – BSB: 001 002 A/c Number: 1234567

REAL ESTATE AGENT Flying High Estate Agents

4 Birdsnest Avenue, In a suburb near you.

CONTACT: Hugh Talon

Tel: 10000700 Facs: 10000080

Email: hught@gmail.com

BULDER Homes Plus More (Master Builders)

38 Archdeacon Street West, In a suburb near you.

CONTACT: Grace Love

Tel: 40000000 Facs: 40000003

Email: grace@hpm.com.au

CONVEYANCING FIRM Lightning Settlements

Suite 3, 4 Business Ave, In a suburb near you.

CONTACT: Louise Stratton

Tel: 10004000 Facs: 10005000

Email: lulu@lightningsetts.com.au

PROPOSED ADDRESS Lot 47 Eaglehawk Circle, In a suburb near you.

LAND DESCRIPTION Lot 47 on Plan of Subdivision 731680Z

PARENT TITLE Volume 11580 Folio 996

Created by instrument PS725680G 04.04.2018

VENDOR Inspired Developments Pty Ltd

Suite 114/ 100 Bridge Road, In a suburb near you.

Tel: 50000001 Facs: 50000002

Email: Info @inspired.com.au

SETTLEMENT DATE 14/00/20XX

When completing your Fact Find/ Client Needs review please remember the Duty of Care.

One of the most important questions you should ask is about Risk Protection. Have the clients

considered the ramifications of financial hardship caused by illness, accident or death?

The Q & A component of the CNR covers this adequately. You are made aware their contents

are insured but they have no insurance policies covering life, trauma and income protection.

This is where you ask what cover they consider is enough in view of the financial

commitments they are now planning? Will Cheryl have to visit Centrelink if an unforeseen

event happens to Alan and vice versa? Should they have to change their lifestyle? Not if the

Broker carries out all the requirements to provide the clients’ needs.

A6 © AAMC Training Group Assessment V3.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Loan Application Process

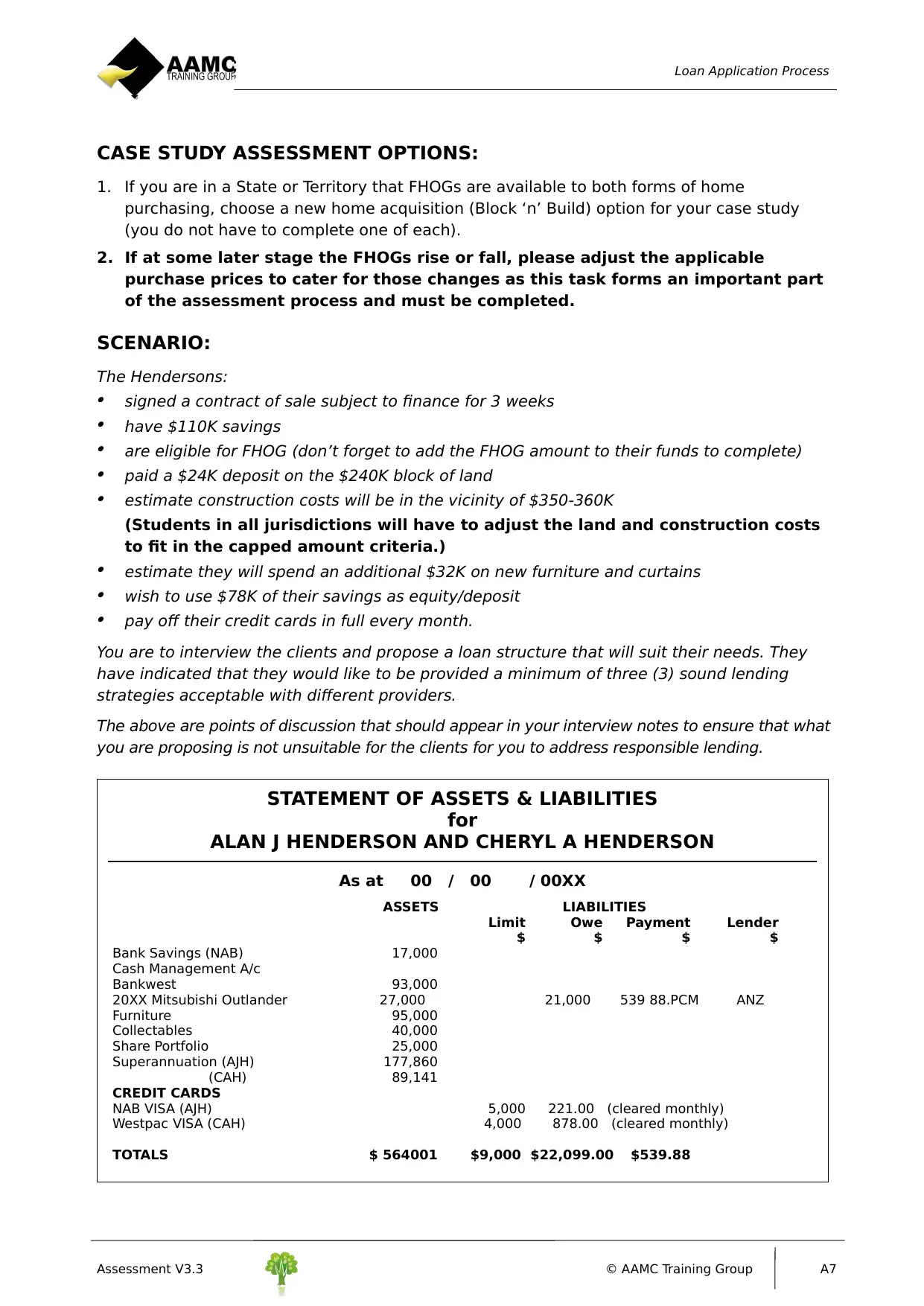

CASE STUDY ASSESSMENT OPTIONS:

1. If you are in a State or Territory that FHOGs are available to both forms of home

purchasing, choose a new home acquisition (Block ‘n’ Build) option for your case study

(you do not have to complete one of each).

2. If at some later stage the FHOGs rise or fall, please adjust the applicable

purchase prices to cater for those changes as this task forms an important part

of the assessment process and must be completed.

SCENARIO:

The Hendersons: signed a contract of sale subject to finance for 3 weeks have $110K savings are eligible for FHOG (don’t forget to add the FHOG amount to their funds to complete) paid a $24K deposit on the $240K block of land estimate construction costs will be in the vicinity of $350-360K

(Students in all jurisdictions will have to adjust the land and construction costs

to fit in the capped amount criteria.) estimate they will spend an additional $32K on new furniture and curtains wish to use $78K of their savings as equity/deposit pay off their credit cards in full every month.

You are to interview the clients and propose a loan structure that will suit their needs. They

have indicated that they would like to be provided a minimum of three (3) sound lending

strategies acceptable with different providers.

The above are points of discussion that should appear in your interview notes to ensure that what

you are proposing is not unsuitable for the clients for you to address responsible lending.

Assessment V3.3 © AAMC Training Group A7

STATEMENT OF ASSETS & LIABILITIES

for

ALAN J HENDERSON AND CHERYL A HENDERSON

As at 00 / 00 / 00XX

ASSETS LIABILITIES

Limit Owe Payment Lender

$ $ $ $

Bank Savings (NAB) 17,000

Cash Management A/c

Bankwest 93,000

20XX Mitsubishi Outlander 27,000 21,000 539 88.PCM ANZ

Furniture 95,000

Collectables 40,000

Share Portfolio 25,000

Superannuation (AJH) 177,860

(CAH) 89,141

CREDIT CARDS

NAB VISA (AJH) 5,000 221.00 (cleared monthly)

Westpac VISA (CAH) 4,000 878.00 (cleared monthly)

TOTALS $ 564001 $9,000 $22,099.00 $539.88

CASE STUDY ASSESSMENT OPTIONS:

1. If you are in a State or Territory that FHOGs are available to both forms of home

purchasing, choose a new home acquisition (Block ‘n’ Build) option for your case study

(you do not have to complete one of each).

2. If at some later stage the FHOGs rise or fall, please adjust the applicable

purchase prices to cater for those changes as this task forms an important part

of the assessment process and must be completed.

SCENARIO:

The Hendersons: signed a contract of sale subject to finance for 3 weeks have $110K savings are eligible for FHOG (don’t forget to add the FHOG amount to their funds to complete) paid a $24K deposit on the $240K block of land estimate construction costs will be in the vicinity of $350-360K

(Students in all jurisdictions will have to adjust the land and construction costs

to fit in the capped amount criteria.) estimate they will spend an additional $32K on new furniture and curtains wish to use $78K of their savings as equity/deposit pay off their credit cards in full every month.

You are to interview the clients and propose a loan structure that will suit their needs. They

have indicated that they would like to be provided a minimum of three (3) sound lending

strategies acceptable with different providers.

The above are points of discussion that should appear in your interview notes to ensure that what

you are proposing is not unsuitable for the clients for you to address responsible lending.

Assessment V3.3 © AAMC Training Group A7

STATEMENT OF ASSETS & LIABILITIES

for

ALAN J HENDERSON AND CHERYL A HENDERSON

As at 00 / 00 / 00XX

ASSETS LIABILITIES

Limit Owe Payment Lender

$ $ $ $

Bank Savings (NAB) 17,000

Cash Management A/c

Bankwest 93,000

20XX Mitsubishi Outlander 27,000 21,000 539 88.PCM ANZ

Furniture 95,000

Collectables 40,000

Share Portfolio 25,000

Superannuation (AJH) 177,860

(CAH) 89,141

CREDIT CARDS

NAB VISA (AJH) 5,000 221.00 (cleared monthly)

Westpac VISA (CAH) 4,000 878.00 (cleared monthly)

TOTALS $ 564001 $9,000 $22,099.00 $539.88

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Loan Application Process

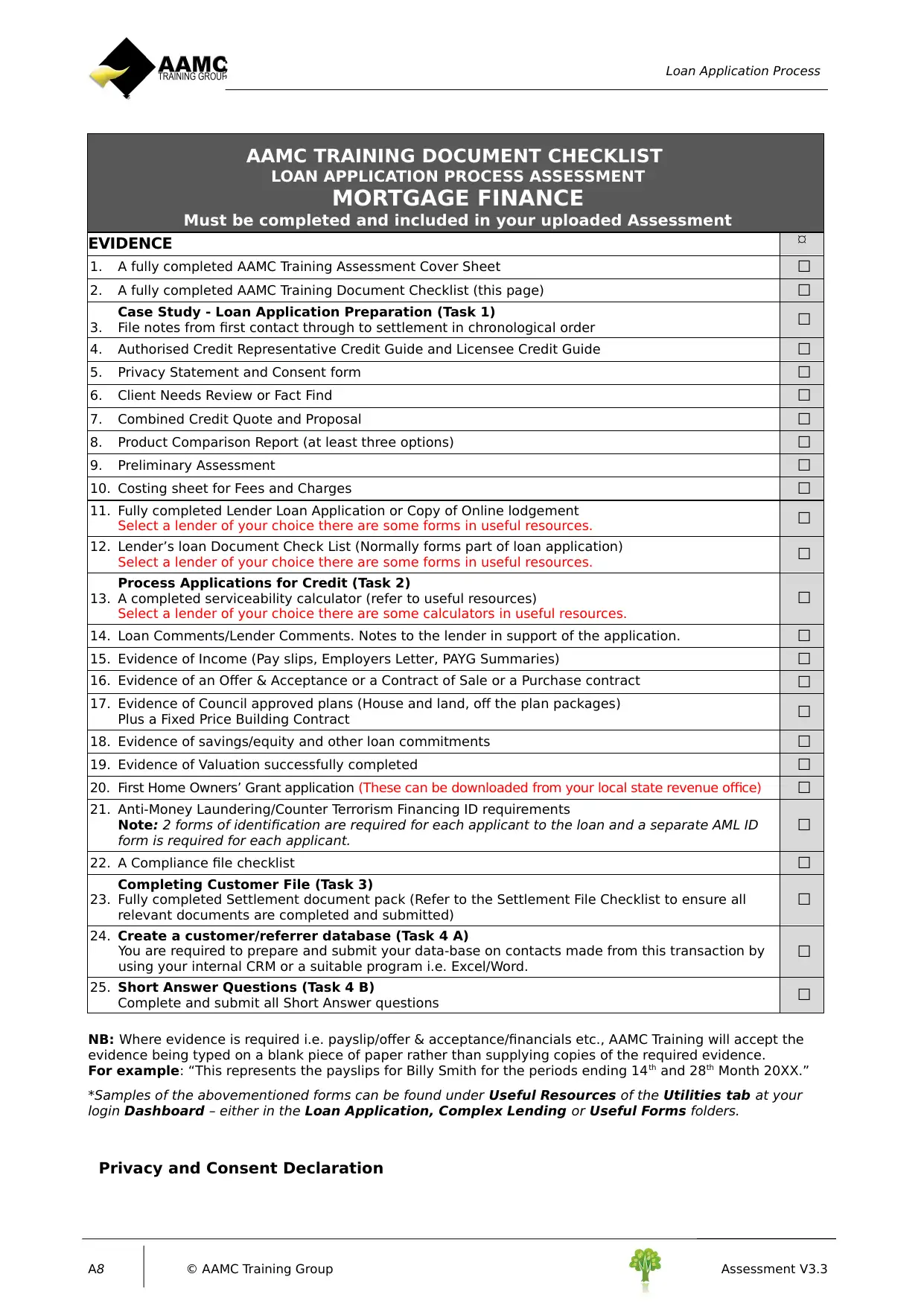

AAMC TRAINING DOCUMENT CHECKLIST

LOAN APPLICATION PROCESS ASSESSMENT

MORTGAGE FINANCE

Must be completed and included in your uploaded Assessment

EVIDENCE

1. A fully completed AAMC Training Assessment Cover Sheet ☐

2. A fully completed AAMC Training Document Checklist (this page) ☐

Case Study - Loan Application Preparation (Task 1)

3. File notes from first contact through to settlement in chronological order ☐

4. Authorised Credit Representative Credit Guide and Licensee Credit Guide ☐

5. Privacy Statement and Consent form ☐

6. Client Needs Review or Fact Find ☐

7. Combined Credit Quote and Proposal ☐

8. Product Comparison Report (at least three options) ☐

9. Preliminary Assessment ☐

10. Costing sheet for Fees and Charges ☐

11. Fully completed Lender Loan Application or Copy of Online lodgement

Select a lender of your choice there are some forms in useful resources. ☐

12. Lender’s loan Document Check List (Normally forms part of loan application)

Select a lender of your choice there are some forms in useful resources. ☐

Process Applications for Credit (Task 2)

13. A completed serviceability calculator (refer to useful resources)

Select a lender of your choice there are some calculators in useful resources.

☐

14. Loan Comments/Lender Comments. Notes to the lender in support of the application. ☐

15. Evidence of Income (Pay slips, Employers Letter, PAYG Summaries) ☐

16. Evidence of an Offer & Acceptance or a Contract of Sale or a Purchase contract ☐

17. Evidence of Council approved plans (House and land, off the plan packages)

Plus a Fixed Price Building Contract ☐

18. Evidence of savings/equity and other loan commitments ☐

19. Evidence of Valuation successfully completed ☐

20. First Home Owners’ Grant application (These can be downloaded from your local state revenue office) ☐

21. Anti-Money Laundering/Counter Terrorism Financing ID requirements

Note: 2 forms of identification are required for each applicant to the loan and a separate AML ID

form is required for each applicant.

☐

22. A Compliance file checklist ☐

Completing Customer File (Task 3)

23. Fully completed Settlement document pack (Refer to the Settlement File Checklist to ensure all

relevant documents are completed and submitted)

☐

24. Create a customer/referrer database (Task 4 A)

You are required to prepare and submit your data-base on contacts made from this transaction by

using your internal CRM or a suitable program i.e. Excel/Word.

☐

25. Short Answer Questions (Task 4 B)

Complete and submit all Short Answer questions ☐

NB: Where evidence is required i.e. payslip/offer & acceptance/financials etc., AAMC Training will accept the

evidence being typed on a blank piece of paper rather than supplying copies of the required evidence.

For example: “This represents the payslips for Billy Smith for the periods ending 14th and 28th Month 20XX.”

*Samples of the abovementioned forms can be found under Useful Resources of the Utilities tab at your

login Dashboard – either in the Loan Application, Complex Lending or Useful Forms folders.

Privacy and Consent Declaration

A8 © AAMC Training Group Assessment V3.3

AAMC TRAINING DOCUMENT CHECKLIST

LOAN APPLICATION PROCESS ASSESSMENT

MORTGAGE FINANCE

Must be completed and included in your uploaded Assessment

EVIDENCE

1. A fully completed AAMC Training Assessment Cover Sheet ☐

2. A fully completed AAMC Training Document Checklist (this page) ☐

Case Study - Loan Application Preparation (Task 1)

3. File notes from first contact through to settlement in chronological order ☐

4. Authorised Credit Representative Credit Guide and Licensee Credit Guide ☐

5. Privacy Statement and Consent form ☐

6. Client Needs Review or Fact Find ☐

7. Combined Credit Quote and Proposal ☐

8. Product Comparison Report (at least three options) ☐

9. Preliminary Assessment ☐

10. Costing sheet for Fees and Charges ☐

11. Fully completed Lender Loan Application or Copy of Online lodgement

Select a lender of your choice there are some forms in useful resources. ☐

12. Lender’s loan Document Check List (Normally forms part of loan application)

Select a lender of your choice there are some forms in useful resources. ☐

Process Applications for Credit (Task 2)

13. A completed serviceability calculator (refer to useful resources)

Select a lender of your choice there are some calculators in useful resources.

☐

14. Loan Comments/Lender Comments. Notes to the lender in support of the application. ☐

15. Evidence of Income (Pay slips, Employers Letter, PAYG Summaries) ☐

16. Evidence of an Offer & Acceptance or a Contract of Sale or a Purchase contract ☐

17. Evidence of Council approved plans (House and land, off the plan packages)

Plus a Fixed Price Building Contract ☐

18. Evidence of savings/equity and other loan commitments ☐

19. Evidence of Valuation successfully completed ☐

20. First Home Owners’ Grant application (These can be downloaded from your local state revenue office) ☐

21. Anti-Money Laundering/Counter Terrorism Financing ID requirements

Note: 2 forms of identification are required for each applicant to the loan and a separate AML ID

form is required for each applicant.

☐

22. A Compliance file checklist ☐

Completing Customer File (Task 3)

23. Fully completed Settlement document pack (Refer to the Settlement File Checklist to ensure all

relevant documents are completed and submitted)

☐

24. Create a customer/referrer database (Task 4 A)

You are required to prepare and submit your data-base on contacts made from this transaction by

using your internal CRM or a suitable program i.e. Excel/Word.

☐

25. Short Answer Questions (Task 4 B)

Complete and submit all Short Answer questions ☐

NB: Where evidence is required i.e. payslip/offer & acceptance/financials etc., AAMC Training will accept the

evidence being typed on a blank piece of paper rather than supplying copies of the required evidence.

For example: “This represents the payslips for Billy Smith for the periods ending 14th and 28th Month 20XX.”

*Samples of the abovementioned forms can be found under Useful Resources of the Utilities tab at your

login Dashboard – either in the Loan Application, Complex Lending or Useful Forms folders.

Privacy and Consent Declaration

A8 © AAMC Training Group Assessment V3.3

Loan Application Process

It can be ensured that while preparation of your lending plan proper adherence is placed both

on legal and your personal and we are confident of the quality and accuracy of our advice,

there are certain factors outside our control that can have an impact on lending option. These

factors include:

the completeness and accuracy of the information you have supplied;

the accuracy of the information received from other financial institutions;

any legislation introduced after the preparation of your SOA;

different results to the estimates used to illustrate the future performance of the

investments in your SOA (please note, these estimates are not intended as forecasts);

whether you hold the investments for the length of time recommended;

the economic environment in Australia and internationally; and

Changes to your personal circumstances.

These, and other factors, are constantly changing. Neither I, nor Mentor Financial Planning

Pty Ltd, accept responsibility for any change in circumstances that affects the strategies

covered in your Statement of Advice.

As outlined in the Financial Services Guide (FSG) provided to you on the business do not

guarantee risk free exposure of the loan. Please note carefully that although historical

investment performance information may be provided, this is not necessarily an accurate

guide to future performance.

The report explains that the client have various loan taking options that can be advised in

respect of achieving the goals of the clients and also to reduce the risk for long term benefit of

the client.

Client Needs Review

As far as I can understand the situation, you have purchased a block of land on which you

would be building a house for yourselves and therefore you require loan advices for ensuring

that the risks can be kept at a minimum and a proper LVR is maintained. As per the personal

details provided Alan you work for a law firm and you have a gross salsry of $ 111,000 while

Cheryl you also have a income of $ 65,000. In my understanding you both have two childrens

and both are dependents. Now, as per the details sheet provided by you both, a ssavings of $

110,000 has been accumulated by you.

As per my belief, this is your first home which is being build and the current place

where you are staying is a rented placed. This means that you are applicable to claim FHOG

scheme which allows you deduxtions and the same is a scheme offered by the government.

You need my help to secure a borrowimg options which can manage the servicibility and the

risk factor in equal proportions. As per your request you want three sources as an option for

borrowing loans.

The assessment of the risk profile determines that the client are balanced investor as the

investment objective is to maintain stable returns over the medium term, whereby security of

Assessment V3.3 © AAMC Training Group A9

It can be ensured that while preparation of your lending plan proper adherence is placed both

on legal and your personal and we are confident of the quality and accuracy of our advice,

there are certain factors outside our control that can have an impact on lending option. These

factors include:

the completeness and accuracy of the information you have supplied;

the accuracy of the information received from other financial institutions;

any legislation introduced after the preparation of your SOA;

different results to the estimates used to illustrate the future performance of the

investments in your SOA (please note, these estimates are not intended as forecasts);

whether you hold the investments for the length of time recommended;

the economic environment in Australia and internationally; and

Changes to your personal circumstances.

These, and other factors, are constantly changing. Neither I, nor Mentor Financial Planning

Pty Ltd, accept responsibility for any change in circumstances that affects the strategies

covered in your Statement of Advice.

As outlined in the Financial Services Guide (FSG) provided to you on the business do not

guarantee risk free exposure of the loan. Please note carefully that although historical

investment performance information may be provided, this is not necessarily an accurate

guide to future performance.

The report explains that the client have various loan taking options that can be advised in

respect of achieving the goals of the clients and also to reduce the risk for long term benefit of

the client.

Client Needs Review

As far as I can understand the situation, you have purchased a block of land on which you

would be building a house for yourselves and therefore you require loan advices for ensuring

that the risks can be kept at a minimum and a proper LVR is maintained. As per the personal

details provided Alan you work for a law firm and you have a gross salsry of $ 111,000 while

Cheryl you also have a income of $ 65,000. In my understanding you both have two childrens

and both are dependents. Now, as per the details sheet provided by you both, a ssavings of $

110,000 has been accumulated by you.

As per my belief, this is your first home which is being build and the current place

where you are staying is a rented placed. This means that you are applicable to claim FHOG

scheme which allows you deduxtions and the same is a scheme offered by the government.

You need my help to secure a borrowimg options which can manage the servicibility and the

risk factor in equal proportions. As per your request you want three sources as an option for

borrowing loans.

The assessment of the risk profile determines that the client are balanced investor as the

investment objective is to maintain stable returns over the medium term, whereby security of

Assessment V3.3 © AAMC Training Group A9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Loan Application Process

capital is of major importance. You will tend to seek higher returns where possible from

investments providing high security of capital and low investment risk.

Credit Proposal

On the basis of the information which is provided to me, I would be suggesting the loan from

ANZ bank which provides one of the best home loan options in the country. As pr my

computations, you require $ 508,000 more for meeting the sales and construction

requirements of the business and also the interior decorations. The amount of loan which you

require is high and therefore it is anticipated that the LVR would also be high.

Alternative Options

The alternative homes loans which xan be considered by you both for meeting the financing

requirements of UHome loans which operates in australlia is quite combatible with the FHOG

scheme. The second alternative which I can present before you is a loan from CBA which is

quite a safe and brilliant option. Howeever, in my opinion the home loan of $ 508,000 should

be taken from ANZ bank due to the effectiveness of the product.

Case study B (Asset Finance Motor Vehicles)

John and Samantha Brown have decided to upgrade their main vehicle and will give their 1995

Mitsubishi to their son. The Holden ute will still be used by John to travel to work.

They are seeking to fund the full purchase of a Holden Captiva Active 7 seater and have

provided an invoice from the dealer. The new vehicle is required to do a lot of country travel

and tow a caravan as they intend to take a number of trips.

Mr and Mrs Brown have full time employment and been working for the same companies for

over 5 years since moving from interstate.

Mrs Brown is the bookkeeper for FSR Consulting Pty Ltd and is responsible for all invoicing

and reporting. Mr Brown works fulltime for Build It Right Carpentry Pty Ltd as a carpenter.

They have also completed a personal statement of position which is enclosed with the

documents.

Other information provided: Intend to keep the vehicle for at least 5 years Wish to keep repayments as low as possible Happy to consider a Residual which would be reflective of the value of the vehicle at end

of loan Fixed Rates and flexibility important with the loan being sought Have asked for advice on Insurance for the vehicle. Have own superannuation funds but not averse to having them reviewed Both clients are unsure of what personal insurances they have but have made an

estimate of coverage

A10 © AAMC Training Group Assessment V3.3

capital is of major importance. You will tend to seek higher returns where possible from

investments providing high security of capital and low investment risk.

Credit Proposal

On the basis of the information which is provided to me, I would be suggesting the loan from

ANZ bank which provides one of the best home loan options in the country. As pr my

computations, you require $ 508,000 more for meeting the sales and construction

requirements of the business and also the interior decorations. The amount of loan which you

require is high and therefore it is anticipated that the LVR would also be high.

Alternative Options

The alternative homes loans which xan be considered by you both for meeting the financing

requirements of UHome loans which operates in australlia is quite combatible with the FHOG

scheme. The second alternative which I can present before you is a loan from CBA which is

quite a safe and brilliant option. Howeever, in my opinion the home loan of $ 508,000 should

be taken from ANZ bank due to the effectiveness of the product.

Case study B (Asset Finance Motor Vehicles)

John and Samantha Brown have decided to upgrade their main vehicle and will give their 1995

Mitsubishi to their son. The Holden ute will still be used by John to travel to work.

They are seeking to fund the full purchase of a Holden Captiva Active 7 seater and have

provided an invoice from the dealer. The new vehicle is required to do a lot of country travel

and tow a caravan as they intend to take a number of trips.

Mr and Mrs Brown have full time employment and been working for the same companies for

over 5 years since moving from interstate.

Mrs Brown is the bookkeeper for FSR Consulting Pty Ltd and is responsible for all invoicing

and reporting. Mr Brown works fulltime for Build It Right Carpentry Pty Ltd as a carpenter.

They have also completed a personal statement of position which is enclosed with the

documents.

Other information provided: Intend to keep the vehicle for at least 5 years Wish to keep repayments as low as possible Happy to consider a Residual which would be reflective of the value of the vehicle at end

of loan Fixed Rates and flexibility important with the loan being sought Have asked for advice on Insurance for the vehicle. Have own superannuation funds but not averse to having them reviewed Both clients are unsure of what personal insurances they have but have made an

estimate of coverage

A10 © AAMC Training Group Assessment V3.3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Loan Application Process

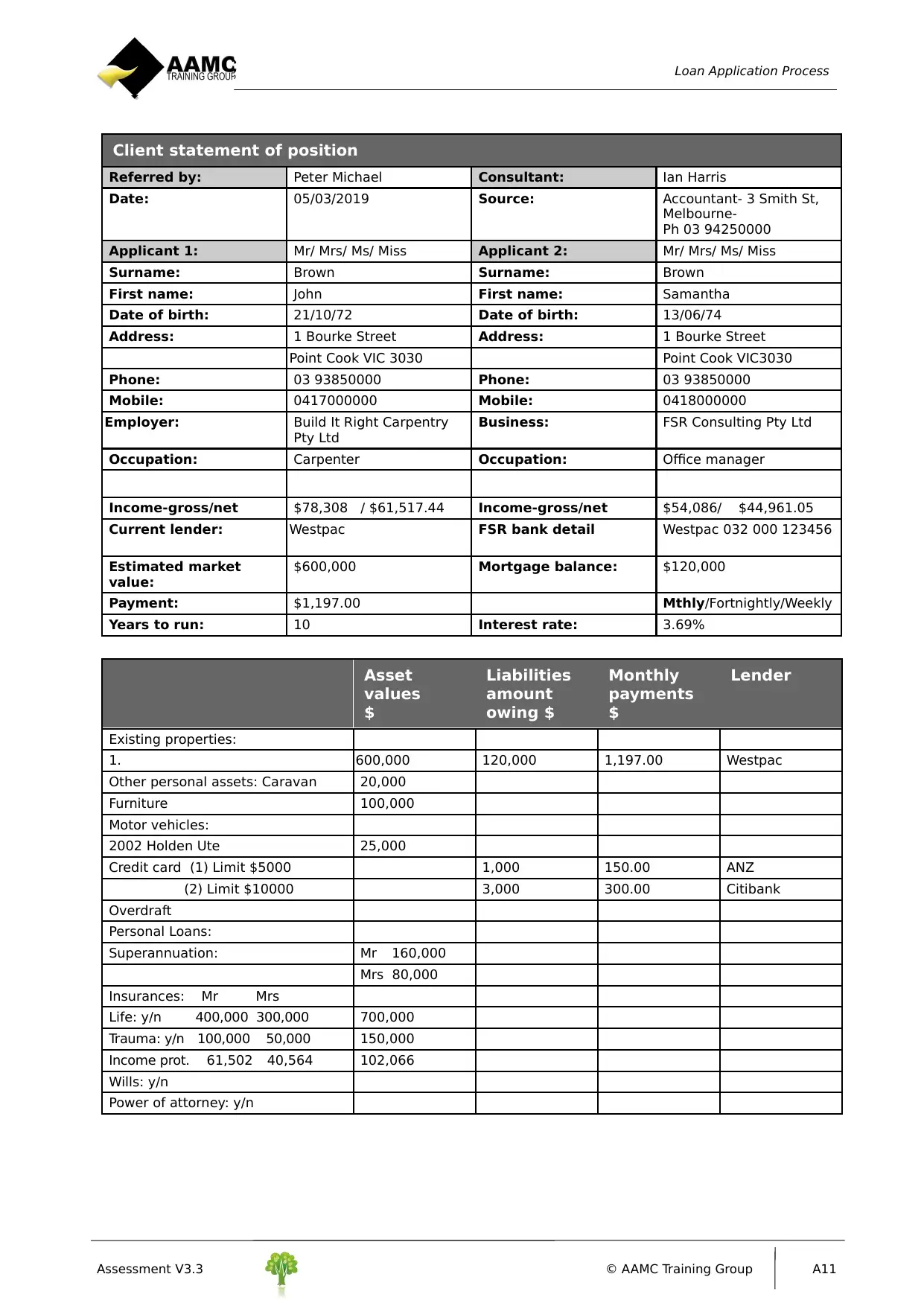

Client statement of position

Referred by: Peter Michael Consultant: Ian Harris

Date: 05/03/2019 Source: Accountant- 3 Smith St,

Melbourne-

Ph 03 94250000

Applicant 1: Mr/ Mrs/ Ms/ Miss Applicant 2: Mr/ Mrs/ Ms/ Miss

Surname: Brown Surname: Brown

First name: John First name: Samantha

Date of birth: 21/10/72 Date of birth: 13/06/74

Address: 1 Bourke Street Address: 1 Bourke Street

Point Cook VIC 3030 Point Cook VIC3030

Phone: 03 93850000 Phone: 03 93850000

Mobile: 0417000000 Mobile: 0418000000

Employer: Build It Right Carpentry

Pty Ltd

Business: FSR Consulting Pty Ltd

Occupation: Carpenter Occupation: Office manager

Income-gross/net $78,308 / $61,517.44 Income-gross/net $54,086/ $44,961.05

Current lender: Westpac FSR bank detail Westpac 032 000 123456

Estimated market

value:

$600,000 Mortgage balance: $120,000

Payment: $1,197.00 Mthly/Fortnightly/Weekly

Years to run: 10 Interest rate: 3.69%

Asset

values

$

Liabilities

amount

owing $

Monthly

payments

$

Lender

Existing properties:

1. 600,000 120,000 1,197.00 Westpac

Other personal assets: Caravan 20,000

Furniture 100,000

Motor vehicles:

2002 Holden Ute 25,000

Credit card (1) Limit $5000 1,000 150.00 ANZ

(2) Limit $10000 3,000 300.00 Citibank

Overdraft

Personal Loans:

Superannuation: Mr 160,000

Mrs 80,000

Insurances: Mr Mrs

Life: y/n 400,000 300,000 700,000

Trauma: y/n 100,000 50,000 150,000

Income prot. 61,502 40,564 102,066

Wills: y/n

Power of attorney: y/n

Assessment V3.3 © AAMC Training Group A11

Client statement of position

Referred by: Peter Michael Consultant: Ian Harris

Date: 05/03/2019 Source: Accountant- 3 Smith St,

Melbourne-

Ph 03 94250000

Applicant 1: Mr/ Mrs/ Ms/ Miss Applicant 2: Mr/ Mrs/ Ms/ Miss

Surname: Brown Surname: Brown

First name: John First name: Samantha

Date of birth: 21/10/72 Date of birth: 13/06/74

Address: 1 Bourke Street Address: 1 Bourke Street

Point Cook VIC 3030 Point Cook VIC3030

Phone: 03 93850000 Phone: 03 93850000

Mobile: 0417000000 Mobile: 0418000000

Employer: Build It Right Carpentry

Pty Ltd

Business: FSR Consulting Pty Ltd

Occupation: Carpenter Occupation: Office manager

Income-gross/net $78,308 / $61,517.44 Income-gross/net $54,086/ $44,961.05

Current lender: Westpac FSR bank detail Westpac 032 000 123456

Estimated market

value:

$600,000 Mortgage balance: $120,000

Payment: $1,197.00 Mthly/Fortnightly/Weekly

Years to run: 10 Interest rate: 3.69%

Asset

values

$

Liabilities

amount

owing $

Monthly

payments

$

Lender

Existing properties:

1. 600,000 120,000 1,197.00 Westpac

Other personal assets: Caravan 20,000

Furniture 100,000

Motor vehicles:

2002 Holden Ute 25,000

Credit card (1) Limit $5000 1,000 150.00 ANZ

(2) Limit $10000 3,000 300.00 Citibank

Overdraft

Personal Loans:

Superannuation: Mr 160,000

Mrs 80,000

Insurances: Mr Mrs

Life: y/n 400,000 300,000 700,000

Trauma: y/n 100,000 50,000 150,000

Income prot. 61,502 40,564 102,066

Wills: y/n

Power of attorney: y/n

Assessment V3.3 © AAMC Training Group A11

Loan Application Process

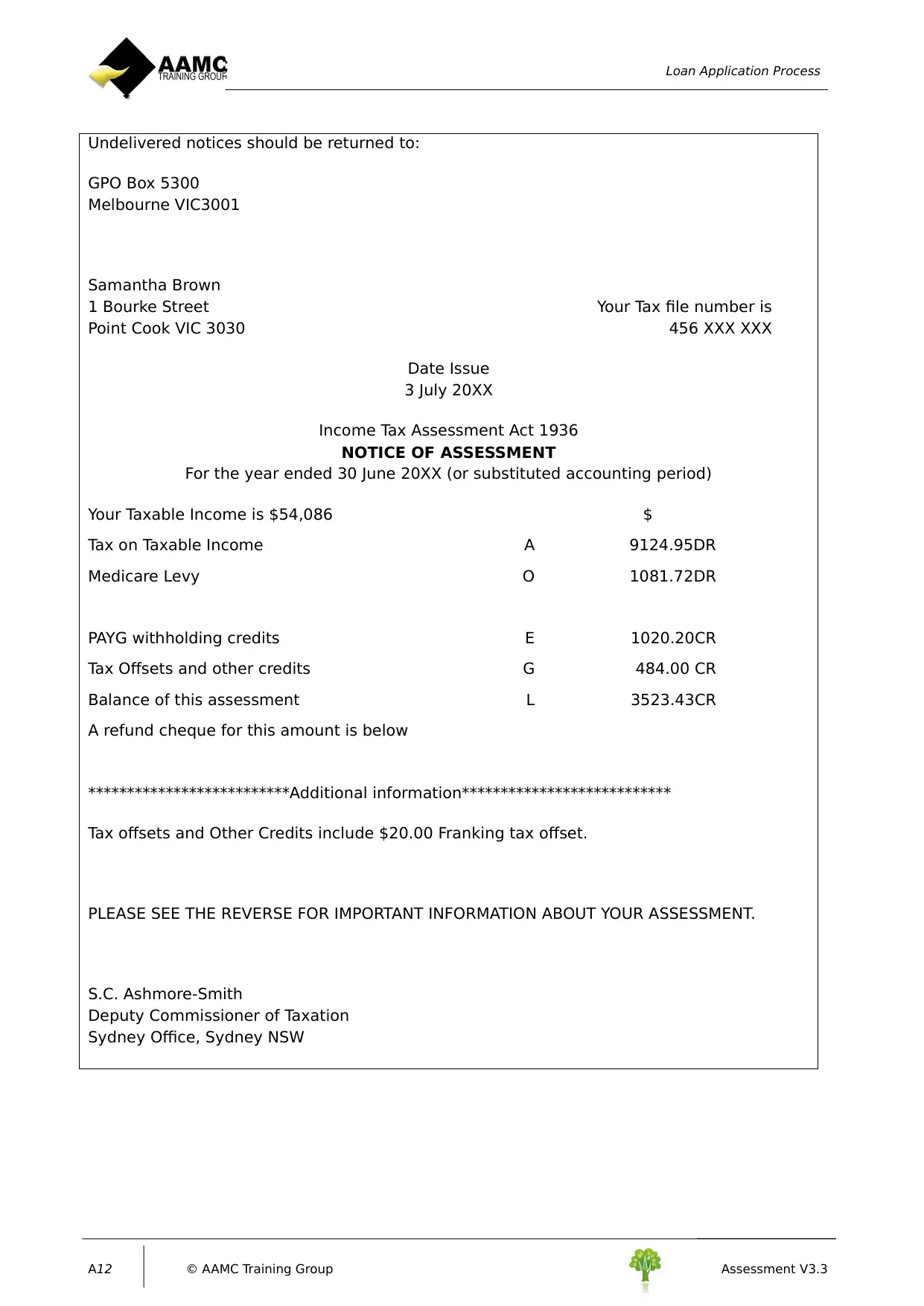

Undelivered notices should be returned to:

GPO Box 5300

Melbourne VIC3001

Samantha Brown

1 Bourke Street Your Tax file number is

Point Cook VIC 3030 456 XXX XXX

Date Issue

3 July 20XX

Income Tax Assessment Act 1936

NOTICE OF ASSESSMENT

For the year ended 30 June 20XX (or substituted accounting period)

Your Taxable Income is $54,086 $

Tax on Taxable Income A 9124.95DR

Medicare Levy O 1081.72DR

PAYG withholding credits E 1020.20CR

Tax Offsets and other credits G 484.00 CR

Balance of this assessment L 3523.43CR

A refund cheque for this amount is below

**************************Additional information***************************

Tax offsets and Other Credits include $20.00 Franking tax offset.

PLEASE SEE THE REVERSE FOR IMPORTANT INFORMATION ABOUT YOUR ASSESSMENT.

S.C. Ashmore-Smith

Deputy Commissioner of Taxation

Sydney Office, Sydney NSW

A12 © AAMC Training Group Assessment V3.3

Undelivered notices should be returned to:

GPO Box 5300

Melbourne VIC3001

Samantha Brown

1 Bourke Street Your Tax file number is

Point Cook VIC 3030 456 XXX XXX

Date Issue

3 July 20XX

Income Tax Assessment Act 1936

NOTICE OF ASSESSMENT

For the year ended 30 June 20XX (or substituted accounting period)

Your Taxable Income is $54,086 $

Tax on Taxable Income A 9124.95DR

Medicare Levy O 1081.72DR

PAYG withholding credits E 1020.20CR

Tax Offsets and other credits G 484.00 CR

Balance of this assessment L 3523.43CR

A refund cheque for this amount is below

**************************Additional information***************************

Tax offsets and Other Credits include $20.00 Franking tax offset.

PLEASE SEE THE REVERSE FOR IMPORTANT INFORMATION ABOUT YOUR ASSESSMENT.

S.C. Ashmore-Smith

Deputy Commissioner of Taxation

Sydney Office, Sydney NSW

A12 © AAMC Training Group Assessment V3.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.