AAMC Training: Risk Management Assessment in Finance and Mortgage

VerifiedAdded on 2023/06/11

|9

|2852

|285

Report

AI Summary

This risk management assessment covers various aspects of risk within the finance and mortgage industry, including written activities, project-based risk identification, case studies, and a comprehensive report. It addresses credit risk, fraud risk, operational risk, and interest rate risk, providing preventative and corrective actions. The assessment references the Australian Standard AS/NZS ISO 31000:2009, emphasizing the importance of understanding and managing uncertainty in financial objectives. It includes risk registers and analysis of loan applications to determine associated risks, offering a thorough evaluation of risk management principles and their practical application in the finance sector. This document is shared by a student on Desklib, a platform offering study tools and resources.

Risk ManagementAssessment

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. A maximum of five (5)

attachments (maximum 20MB each) can be uploaded for this assessment. Please see the

step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name

Assessment name Risk Management Assessment

Surname Given name

Address Postcode

Email

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment

submissionto AAMC Training is your own work and NOT the result of plagiarism or excessive

collaboration, and that all material used from any third party has been identified and

referenced appropriately. AAMC Training may conduct independent evaluation checks and

contact your supervisor to discuss your assessment.

Checklist of attachments:

☐Task 1 – Written activities

☐Task 2 – Project

☐Task 3 – Case study 1

☐Task 4 – Report

☐Task 5 – Case Study 2

Please indicate style of course undertaken:

☐Face to face Trainer’s name:

☐Correspondence ☐Online

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Please contact our head office if you need assistance with your assessment:

Office: +61 8 9344 4088 Fax: +61 8 9344 4188 Email:info@aamctraining.edu.au

Assessment V2.2 © AAMC Training Group A1

Assessment cover sheet

In order for your assessment to be marked you must complete and upload all tasks

and this cover sheet via the AAMC Training Group portal. Your assessment tasks must

be uploaded in an electronic format i.e. Word, Excel, PDF or Scan. A maximum of five (5)

attachments (maximum 20MB each) can be uploaded for this assessment. Please see the

step-by-step instructions in your Member Area on how to upload assessments.

Student details

Course name

Assessment name Risk Management Assessment

Surname Given name

Address Postcode

Phone Phone (other)

Current occupation

Industry Years in industry

When you upload your assessment you will be asked to confirm that your assessment

submissionto AAMC Training is your own work and NOT the result of plagiarism or excessive

collaboration, and that all material used from any third party has been identified and

referenced appropriately. AAMC Training may conduct independent evaluation checks and

contact your supervisor to discuss your assessment.

Checklist of attachments:

☐Task 1 – Written activities

☐Task 2 – Project

☐Task 3 – Case study 1

☐Task 4 – Report

☐Task 5 – Case Study 2

Please indicate style of course undertaken:

☐Face to face Trainer’s name:

☐Correspondence ☐Online

Once your assessment has been successfully uploaded it will be pending review with your

nominated course assessor. Your assessor will mark your assessment and you will receive an

email advising you if you have been assessed as satisfactory. If you are marked as not yet

satisfactory you will be contacted and asked to provide additional information or re-visit the

assessment and re-upload your amended case study or written tasks.

Please contact our head office if you need assistance with your assessment:

Office: +61 8 9344 4088 Fax: +61 8 9344 4188 Email:info@aamctraining.edu.au

Assessment V2.2 © AAMC Training Group A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk ManagementAssessment

RISK MANAGEMENTASSESSMENT TASKS

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result or

statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

BSBRSK401 Identify risk and apply risk management processes

FNSRSK502 Assess risk

Please refer to AAMC Training’s full Recognition Policy for further details.

IMPORTANT INSTRUCTIONS

Your answers to each of the tasks are to be typed into this document or supplied

electronically and uploaded.

No assessment word count has been specified although you are expected to provide good

quality answers to each of the questions.

Although some general discussion between students covering the assessment is allowed

your responses to each of the questions must be an individual effort.

PLEASE NOTE: AAMC Training only wants to see your own work. Please do not upload

parts of the learning guide or instructions on how to complete. When this extra information

is uploaded it presents unnecessary work for the assessors and in turn delays our

assessment responses.

Task 1 – Written activities

1. Name the two categories of risk.

1 Pure risk – it is the chances of loss owing to peril or accident

2 Speculative risk – it is the chances of gain as well as chances of loss

2. Pure risk or speculative risk—which one can usually be mitigated by transferring the risk

to another party i.e. insurance company?

Among pure risk and speculative risk, pure risk can be mitigated through transferring of

the risk to another party that is the insurance company. Speculative risk generalle

involves the risk in stock market investment or gambling and therefore cannot be insured

under the tradtional market of insurance.

3. What are the four steps in the risk management process?

1. Idtifying potential risk and assessing the impact

2. Examining various courses of available action and developing the implementation plan

A2 © AAMC Training Group Assessment V2.2

RISK MANAGEMENTASSESSMENT TASKS

CREDIT TRANSFER

You may be able to claim credit transfer for a unit/s of competency that you have previously

completed with AAMC Training or another RTO. If you have been awarded a record of result or

statement of attainment for any of the units detailed below then please go to the Credit

Transfer tab in your Learning Centre and follow the prompts.

This assessment relates to the following units of competency:

BSBRSK401 Identify risk and apply risk management processes

FNSRSK502 Assess risk

Please refer to AAMC Training’s full Recognition Policy for further details.

IMPORTANT INSTRUCTIONS

Your answers to each of the tasks are to be typed into this document or supplied

electronically and uploaded.

No assessment word count has been specified although you are expected to provide good

quality answers to each of the questions.

Although some general discussion between students covering the assessment is allowed

your responses to each of the questions must be an individual effort.

PLEASE NOTE: AAMC Training only wants to see your own work. Please do not upload

parts of the learning guide or instructions on how to complete. When this extra information

is uploaded it presents unnecessary work for the assessors and in turn delays our

assessment responses.

Task 1 – Written activities

1. Name the two categories of risk.

1 Pure risk – it is the chances of loss owing to peril or accident

2 Speculative risk – it is the chances of gain as well as chances of loss

2. Pure risk or speculative risk—which one can usually be mitigated by transferring the risk

to another party i.e. insurance company?

Among pure risk and speculative risk, pure risk can be mitigated through transferring of

the risk to another party that is the insurance company. Speculative risk generalle

involves the risk in stock market investment or gambling and therefore cannot be insured

under the tradtional market of insurance.

3. What are the four steps in the risk management process?

1. Idtifying potential risk and assessing the impact

2. Examining various courses of available action and developing the implementation plan

A2 © AAMC Training Group Assessment V2.2

Risk ManagementAssessment

3. Implementing the plan

4. Evaluating and reviewing the plan

4. In assessing credit risk from a single borrower, a lender must consider what three issues?

1. Recovery rate – in case of default, what percentage of exposures projected to b

erecovered through proceedings of bankruptcy or through any other settlement form

2. Credit exposure – in case of default the amount of outstanding obligation, if the default

takes place

3. Probability of default – likelihood that counterparty will default in payment of obligation

over the time period of obligation or over the specific time period like year. If

calculated on the horizon of 1 year time it will be called as expected frequency of

default.

5. The seven Cs analysis frame work is the most common of all expert systems. It involves

examining the borrower using the seven key principles in lending; list them.

1. Character

2. Capacity

3. Capital

4. Conditions

5. Collateral

6. Cause

7. Common sense

6. What are the more common types of security?

Personal real estate, personal vehicles, business property, home equity, valuable items

like collectibles or jewellery, equipment, assets and paper investment

7. What does the PARSER analysis method consider?

PARSER is the expert system used for credit analysis in Australia. Like 5 Cs PARSER

system is used to analyse the following –

Borrower’s personal character

Requirement of amount and purpose

Capacity of repayment

Security

Expedience or thye opportunities for future profits

Return from loan

Assessment V2.2 © AAMC Training Group A3

3. Implementing the plan

4. Evaluating and reviewing the plan

4. In assessing credit risk from a single borrower, a lender must consider what three issues?

1. Recovery rate – in case of default, what percentage of exposures projected to b

erecovered through proceedings of bankruptcy or through any other settlement form

2. Credit exposure – in case of default the amount of outstanding obligation, if the default

takes place

3. Probability of default – likelihood that counterparty will default in payment of obligation

over the time period of obligation or over the specific time period like year. If

calculated on the horizon of 1 year time it will be called as expected frequency of

default.

5. The seven Cs analysis frame work is the most common of all expert systems. It involves

examining the borrower using the seven key principles in lending; list them.

1. Character

2. Capacity

3. Capital

4. Conditions

5. Collateral

6. Cause

7. Common sense

6. What are the more common types of security?

Personal real estate, personal vehicles, business property, home equity, valuable items

like collectibles or jewellery, equipment, assets and paper investment

7. What does the PARSER analysis method consider?

PARSER is the expert system used for credit analysis in Australia. Like 5 Cs PARSER

system is used to analyse the following –

Borrower’s personal character

Requirement of amount and purpose

Capacity of repayment

Security

Expedience or thye opportunities for future profits

Return from loan

Assessment V2.2 © AAMC Training Group A3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk ManagementAssessment

Task 2 – Project

a. Using the table below, make a list (minimum of two in each category) on what you

perceive to be risks for each of the key risk areas for Finance/Mortgage Industry

representatives AND list who would be the internal and external stakeholders in the risk

identification process.

Financial &

Economic

Stakeholder/ s Manage Safety

& Health

Stakeholder/s

Internal External Internal External

Credit risk Management,

staff

member,

policy

makers

Suppliers,

vendors, local

community

Environmental hazard Staff member,

Management,

board

members

Vendors,

local

community

Liquidity risk Management Customers,

clients,

regulatory

bodies

Risk of fire Management,

Board

members,

staff

members

Local

community,

customers,

cleints

Regulatory/Legal Stakeholder/ s Professionalism

and Reputation

Stakeholder/s

Internal External Internal External

Administration of permits

and licensing

Board of

directors,

management

,

Clients,

shareholders

Unconscionable conduct Management

, Board

members,

staff

members

Vendors,

local

community

Control of the hazardous

substance

Board of

directors,

policy makers

Shareholders,

suppliers

Unethical and illegal

competitive practices

Staff

member,

Management

, board

members

Local

community,

customers,

cleints

Sales documentation Stakeholder/s

Internal External

Delayed settlement Management,

Board

members

Customers,

clients

Poorly completed applications for loan Board

members,

policy makers

Clients,

customers

A4 © AAMC Training Group Assessment V2.2

Task 2 – Project

a. Using the table below, make a list (minimum of two in each category) on what you

perceive to be risks for each of the key risk areas for Finance/Mortgage Industry

representatives AND list who would be the internal and external stakeholders in the risk

identification process.

Financial &

Economic

Stakeholder/ s Manage Safety

& Health

Stakeholder/s

Internal External Internal External

Credit risk Management,

staff

member,

policy

makers

Suppliers,

vendors, local

community

Environmental hazard Staff member,

Management,

board

members

Vendors,

local

community

Liquidity risk Management Customers,

clients,

regulatory

bodies

Risk of fire Management,

Board

members,

staff

members

Local

community,

customers,

cleints

Regulatory/Legal Stakeholder/ s Professionalism

and Reputation

Stakeholder/s

Internal External Internal External

Administration of permits

and licensing

Board of

directors,

management

,

Clients,

shareholders

Unconscionable conduct Management

, Board

members,

staff

members

Vendors,

local

community

Control of the hazardous

substance

Board of

directors,

policy makers

Shareholders,

suppliers

Unethical and illegal

competitive practices

Staff

member,

Management

, board

members

Local

community,

customers,

cleints

Sales documentation Stakeholder/s

Internal External

Delayed settlement Management,

Board

members

Customers,

clients

Poorly completed applications for loan Board

members,

policy makers

Clients,

customers

A4 © AAMC Training Group Assessment V2.2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk ManagementAssessment

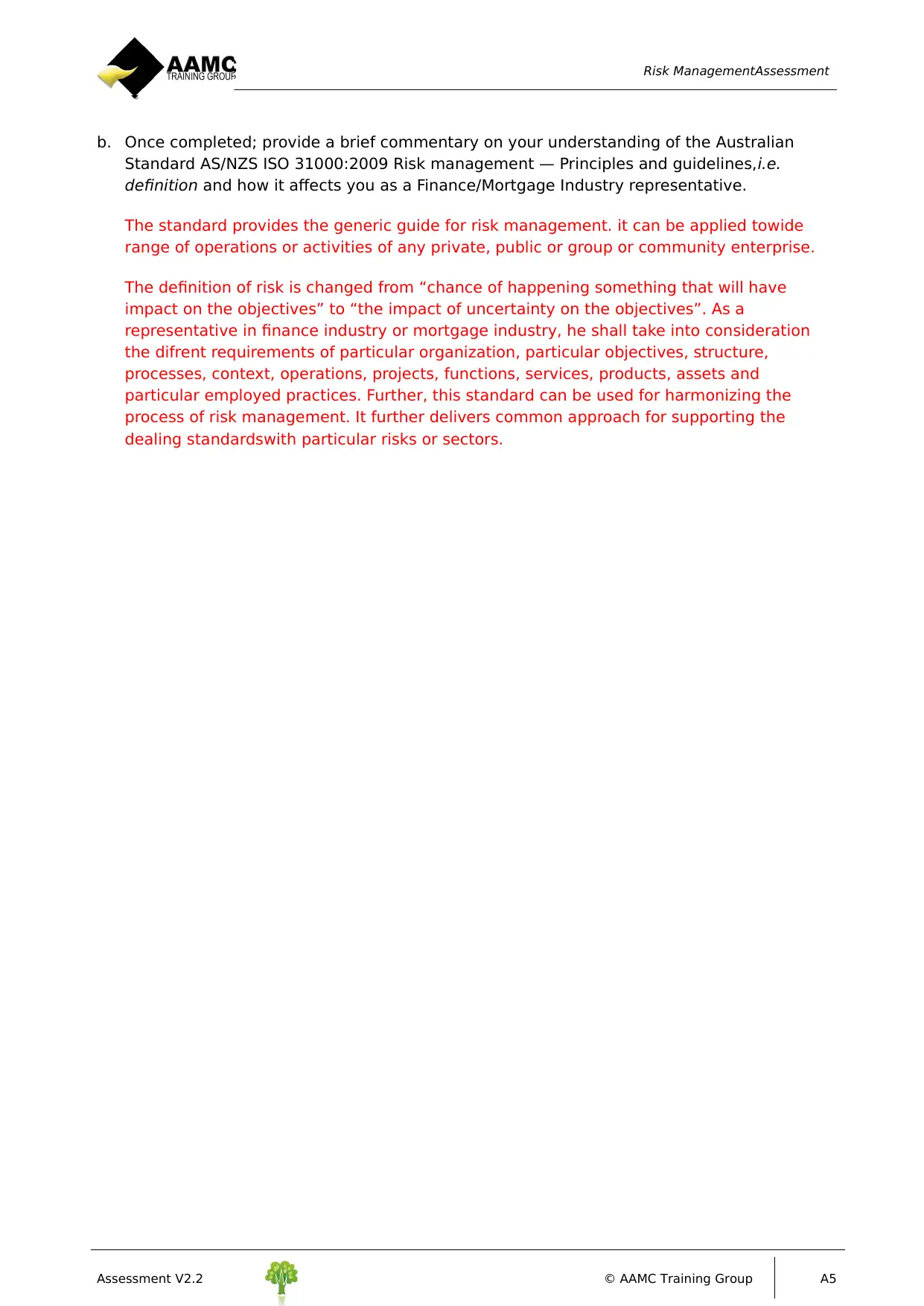

b. Once completed; provide a brief commentary on your understanding of the Australian

Standard AS/NZS ISO 31000:2009 Risk management — Principles and guidelines,i.e.

definition and how it affects you as a Finance/Mortgage Industry representative.

The standard provides the generic guide for risk management. it can be applied towide

range of operations or activities of any private, public or group or community enterprise.

The definition of risk is changed from “chance of happening something that will have

impact on the objectives” to “the impact of uncertainty on the objectives”. As a

representative in finance industry or mortgage industry, he shall take into consideration

the difrent requirements of particular organization, particular objectives, structure,

processes, context, operations, projects, functions, services, products, assets and

particular employed practices. Further, this standard can be used for harmonizing the

process of risk management. It further delivers common approach for supporting the

dealing standardswith particular risks or sectors.

Assessment V2.2 © AAMC Training Group A5

b. Once completed; provide a brief commentary on your understanding of the Australian

Standard AS/NZS ISO 31000:2009 Risk management — Principles and guidelines,i.e.

definition and how it affects you as a Finance/Mortgage Industry representative.

The standard provides the generic guide for risk management. it can be applied towide

range of operations or activities of any private, public or group or community enterprise.

The definition of risk is changed from “chance of happening something that will have

impact on the objectives” to “the impact of uncertainty on the objectives”. As a

representative in finance industry or mortgage industry, he shall take into consideration

the difrent requirements of particular organization, particular objectives, structure,

processes, context, operations, projects, functions, services, products, assets and

particular employed practices. Further, this standard can be used for harmonizing the

process of risk management. It further delivers common approach for supporting the

dealing standardswith particular risks or sectors.

Assessment V2.2 © AAMC Training Group A5

Risk ManagementAssessment

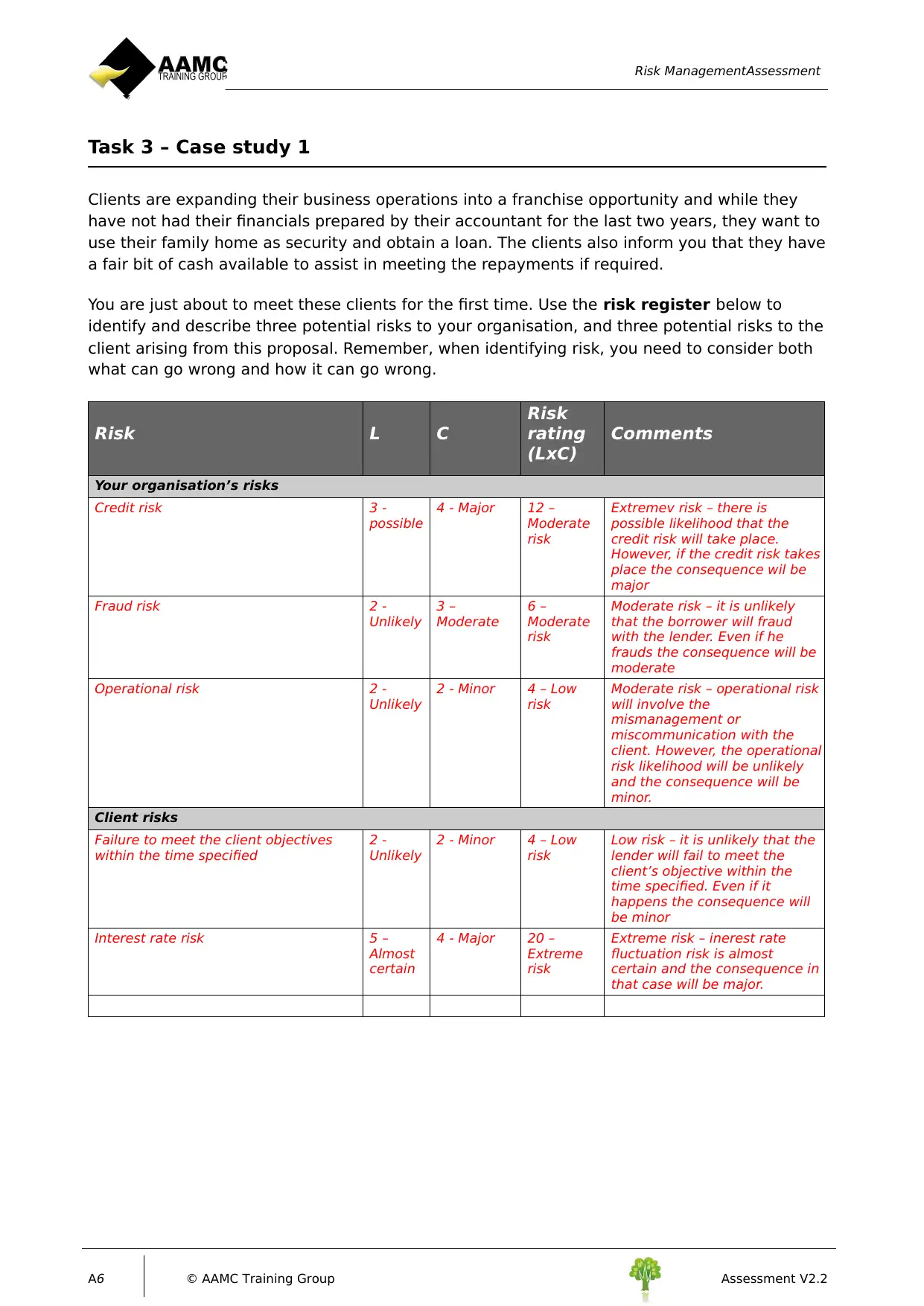

Task 3 – Case study 1

Clients are expanding their business operations into a franchise opportunity and while they

have not had their financials prepared by their accountant for the last two years, they want to

use their family home as security and obtain a loan. The clients also inform you that they have

a fair bit of cash available to assist in meeting the repayments if required.

You are just about to meet these clients for the first time. Use the risk register below to

identify and describe three potential risks to your organisation, and three potential risks to the

client arising from this proposal. Remember, when identifying risk, you need to consider both

what can go wrong and how it can go wrong.

Risk L C

Risk

rating

(LxC)

Comments

Your organisation’s risks

Credit risk 3 -

possible

4 - Major 12 –

Moderate

risk

Extremev risk – there is

possible likelihood that the

credit risk will take place.

However, if the credit risk takes

place the consequence wil be

major

Fraud risk 2 -

Unlikely

3 –

Moderate

6 –

Moderate

risk

Moderate risk – it is unlikely

that the borrower will fraud

with the lender. Even if he

frauds the consequence will be

moderate

Operational risk 2 -

Unlikely

2 - Minor 4 – Low

risk

Moderate risk – operational risk

will involve the

mismanagement or

miscommunication with the

client. However, the operational

risk likelihood will be unlikely

and the consequence will be

minor.

Client risks

Failure to meet the client objectives

within the time specified

2 -

Unlikely

2 - Minor 4 – Low

risk

Low risk – it is unlikely that the

lender will fail to meet the

client’s objective within the

time specified. Even if it

happens the consequence will

be minor

Interest rate risk 5 –

Almost

certain

4 - Major 20 –

Extreme

risk

Extreme risk – inerest rate

fluctuation risk is almost

certain and the consequence in

that case will be major.

A6 © AAMC Training Group Assessment V2.2

Task 3 – Case study 1

Clients are expanding their business operations into a franchise opportunity and while they

have not had their financials prepared by their accountant for the last two years, they want to

use their family home as security and obtain a loan. The clients also inform you that they have

a fair bit of cash available to assist in meeting the repayments if required.

You are just about to meet these clients for the first time. Use the risk register below to

identify and describe three potential risks to your organisation, and three potential risks to the

client arising from this proposal. Remember, when identifying risk, you need to consider both

what can go wrong and how it can go wrong.

Risk L C

Risk

rating

(LxC)

Comments

Your organisation’s risks

Credit risk 3 -

possible

4 - Major 12 –

Moderate

risk

Extremev risk – there is

possible likelihood that the

credit risk will take place.

However, if the credit risk takes

place the consequence wil be

major

Fraud risk 2 -

Unlikely

3 –

Moderate

6 –

Moderate

risk

Moderate risk – it is unlikely

that the borrower will fraud

with the lender. Even if he

frauds the consequence will be

moderate

Operational risk 2 -

Unlikely

2 - Minor 4 – Low

risk

Moderate risk – operational risk

will involve the

mismanagement or

miscommunication with the

client. However, the operational

risk likelihood will be unlikely

and the consequence will be

minor.

Client risks

Failure to meet the client objectives

within the time specified

2 -

Unlikely

2 - Minor 4 – Low

risk

Low risk – it is unlikely that the

lender will fail to meet the

client’s objective within the

time specified. Even if it

happens the consequence will

be minor

Interest rate risk 5 –

Almost

certain

4 - Major 20 –

Extreme

risk

Extreme risk – inerest rate

fluctuation risk is almost

certain and the consequence in

that case will be major.

A6 © AAMC Training Group Assessment V2.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk ManagementAssessment

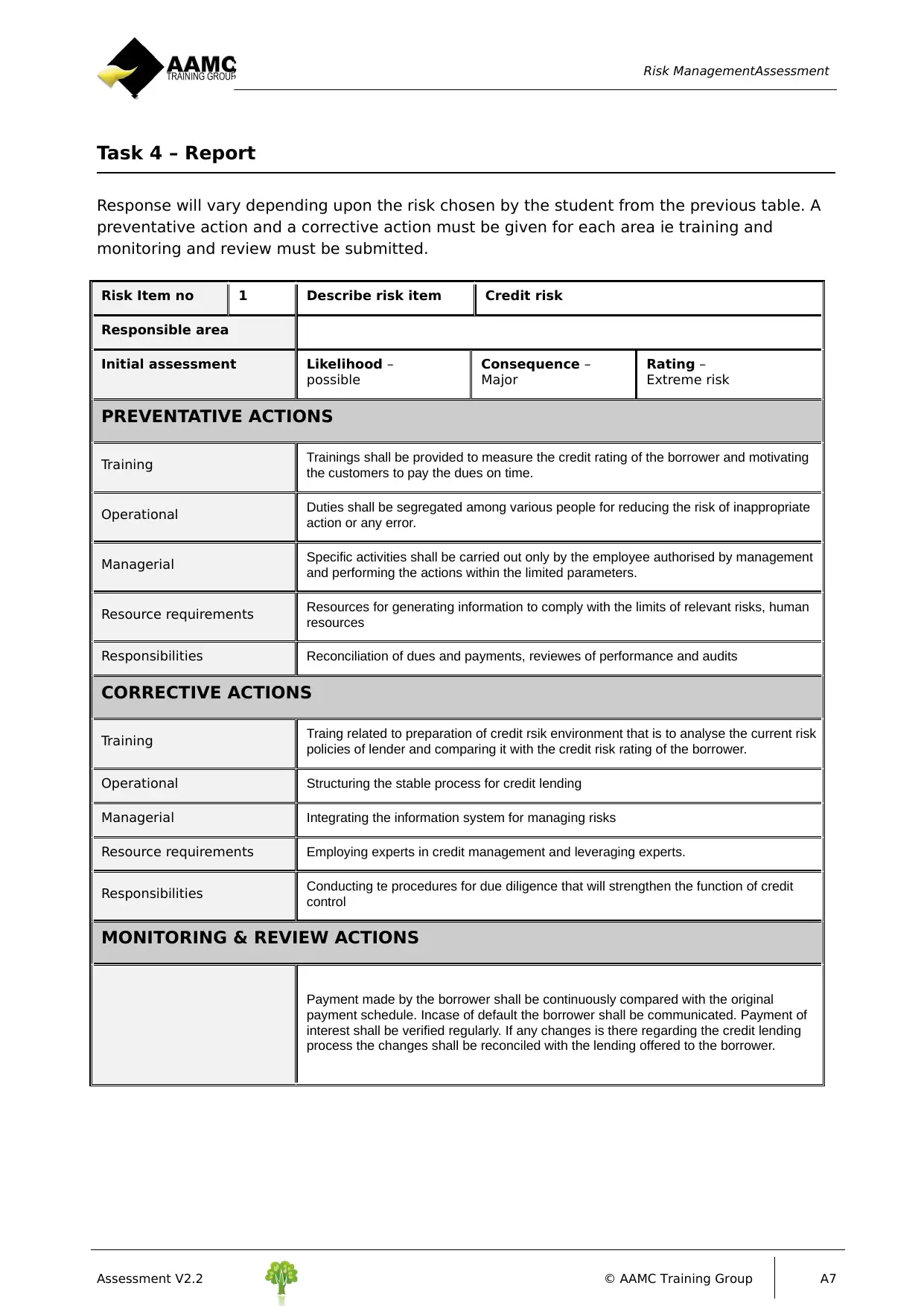

Task 4 – Report

Response will vary depending upon the risk chosen by the student from the previous table. A

preventative action and a corrective action must be given for each area ie training and

monitoring and review must be submitted.

Risk Item no 1 Describe risk item Credit risk

Responsible area

Initial assessment Likelihood –

possible

Consequence –

Major

Rating –

Extreme risk

PREVENTATIVE ACTIONS

Training Trainings shall be provided to measure the credit rating of the borrower and motivating

the customers to pay the dues on time.

Operational Duties shall be segregated among various people for reducing the risk of inappropriate

action or any error.

Managerial Specific activities shall be carried out only by the employee authorised by management

and performing the actions within the limited parameters.

Resource requirements Resources for generating information to comply with the limits of relevant risks, human

resources

Responsibilities Reconciliation of dues and payments, reviewes of performance and audits

CORRECTIVE ACTIONS

Training Traing related to preparation of credit rsik environment that is to analyse the current risk

policies of lender and comparing it with the credit risk rating of the borrower.

Operational Structuring the stable process for credit lending

Managerial Integrating the information system for managing risks

Resource requirements Employing experts in credit management and leveraging experts.

Responsibilities Conducting te procedures for due diligence that will strengthen the function of credit

control

MONITORING & REVIEW ACTIONS

Payment made by the borrower shall be continuously compared with the original

payment schedule. Incase of default the borrower shall be communicated. Payment of

interest shall be verified regularly. If any changes is there regarding the credit lending

process the changes shall be reconciled with the lending offered to the borrower.

Assessment V2.2 © AAMC Training Group A7

Task 4 – Report

Response will vary depending upon the risk chosen by the student from the previous table. A

preventative action and a corrective action must be given for each area ie training and

monitoring and review must be submitted.

Risk Item no 1 Describe risk item Credit risk

Responsible area

Initial assessment Likelihood –

possible

Consequence –

Major

Rating –

Extreme risk

PREVENTATIVE ACTIONS

Training Trainings shall be provided to measure the credit rating of the borrower and motivating

the customers to pay the dues on time.

Operational Duties shall be segregated among various people for reducing the risk of inappropriate

action or any error.

Managerial Specific activities shall be carried out only by the employee authorised by management

and performing the actions within the limited parameters.

Resource requirements Resources for generating information to comply with the limits of relevant risks, human

resources

Responsibilities Reconciliation of dues and payments, reviewes of performance and audits

CORRECTIVE ACTIONS

Training Traing related to preparation of credit rsik environment that is to analyse the current risk

policies of lender and comparing it with the credit risk rating of the borrower.

Operational Structuring the stable process for credit lending

Managerial Integrating the information system for managing risks

Resource requirements Employing experts in credit management and leveraging experts.

Responsibilities Conducting te procedures for due diligence that will strengthen the function of credit

control

MONITORING & REVIEW ACTIONS

Payment made by the borrower shall be continuously compared with the original

payment schedule. Incase of default the borrower shall be communicated. Payment of

interest shall be verified regularly. If any changes is there regarding the credit lending

process the changes shall be reconciled with the lending offered to the borrower.

Assessment V2.2 © AAMC Training Group A7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk ManagementAssessment

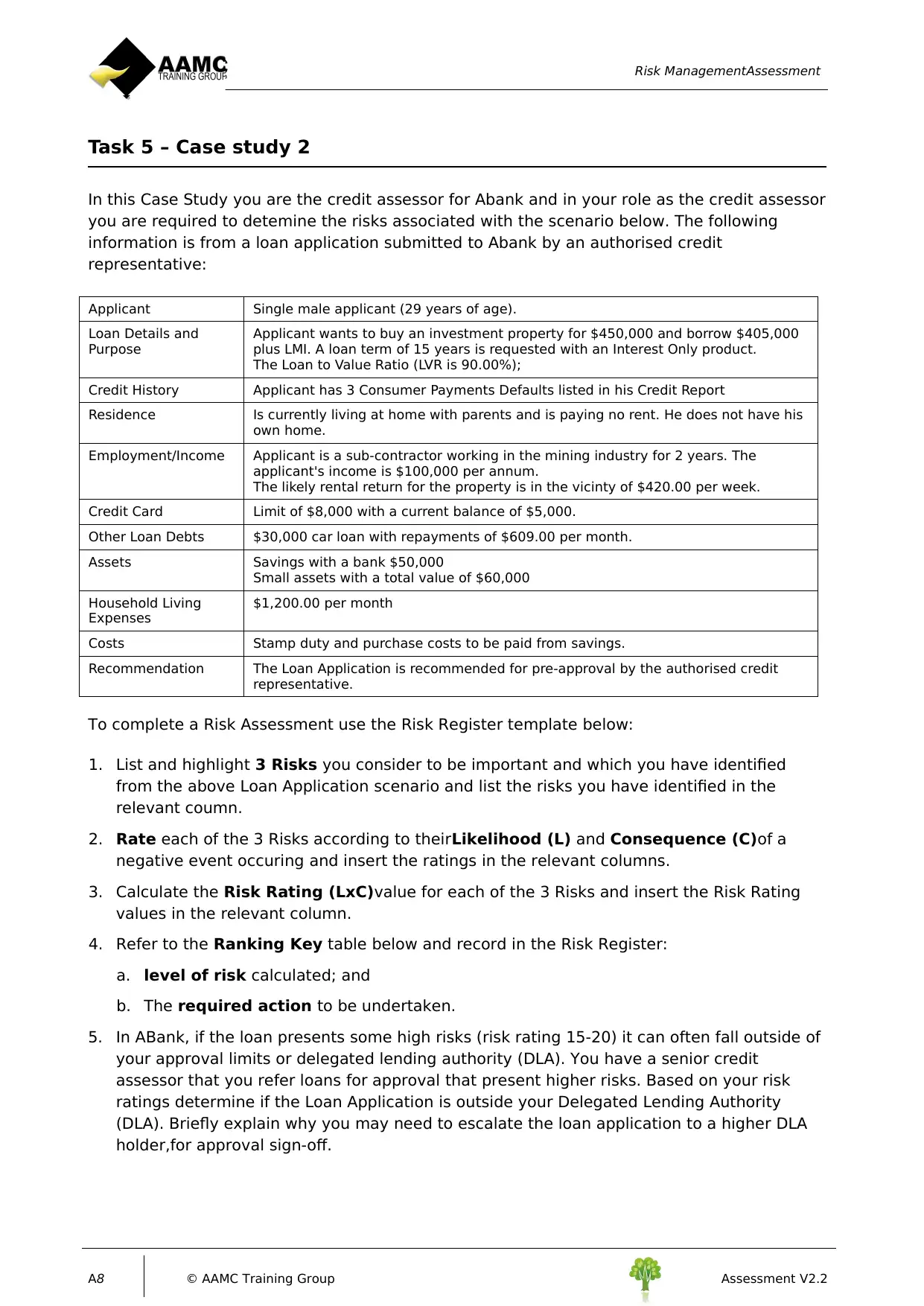

Task 5 – Case study 2

In this Case Study you are the credit assessor for Abank and in your role as the credit assessor

you are required to detemine the risks associated with the scenario below. The following

information is from a loan application submitted to Abank by an authorised credit

representative:

Applicant Single male applicant (29 years of age).

Loan Details and

Purpose

Applicant wants to buy an investment property for $450,000 and borrow $405,000

plus LMI. A loan term of 15 years is requested with an Interest Only product.

The Loan to Value Ratio (LVR is 90.00%);

Credit History Applicant has 3 Consumer Payments Defaults listed in his Credit Report

Residence Is currently living at home with parents and is paying no rent. He does not have his

own home.

Employment/Income Applicant is a sub-contractor working in the mining industry for 2 years. The

applicant's income is $100,000 per annum.

The likely rental return for the property is in the vicinty of $420.00 per week.

Credit Card Limit of $8,000 with a current balance of $5,000.

Other Loan Debts $30,000 car loan with repayments of $609.00 per month.

Assets Savings with a bank $50,000

Small assets with a total value of $60,000

Household Living

Expenses

$1,200.00 per month

Costs Stamp duty and purchase costs to be paid from savings.

Recommendation The Loan Application is recommended for pre-approval by the authorised credit

representative.

To complete a Risk Assessment use the Risk Register template below:

1. List and highlight 3 Risks you consider to be important and which you have identified

from the above Loan Application scenario and list the risks you have identified in the

relevant coumn.

2. Rate each of the 3 Risks according to theirLikelihood (L) and Consequence (C)of a

negative event occuring and insert the ratings in the relevant columns.

3. Calculate the Risk Rating (LxC)value for each of the 3 Risks and insert the Risk Rating

values in the relevant column.

4. Refer to the Ranking Key table below and record in the Risk Register:

a. level of risk calculated; and

b. The required action to be undertaken.

5. In ABank, if the loan presents some high risks (risk rating 15-20) it can often fall outside of

your approval limits or delegated lending authority (DLA). You have a senior credit

assessor that you refer loans for approval that present higher risks. Based on your risk

ratings determine if the Loan Application is outside your Delegated Lending Authority

(DLA). Briefly explain why you may need to escalate the loan application to a higher DLA

holder,for approval sign-off.

A8 © AAMC Training Group Assessment V2.2

Task 5 – Case study 2

In this Case Study you are the credit assessor for Abank and in your role as the credit assessor

you are required to detemine the risks associated with the scenario below. The following

information is from a loan application submitted to Abank by an authorised credit

representative:

Applicant Single male applicant (29 years of age).

Loan Details and

Purpose

Applicant wants to buy an investment property for $450,000 and borrow $405,000

plus LMI. A loan term of 15 years is requested with an Interest Only product.

The Loan to Value Ratio (LVR is 90.00%);

Credit History Applicant has 3 Consumer Payments Defaults listed in his Credit Report

Residence Is currently living at home with parents and is paying no rent. He does not have his

own home.

Employment/Income Applicant is a sub-contractor working in the mining industry for 2 years. The

applicant's income is $100,000 per annum.

The likely rental return for the property is in the vicinty of $420.00 per week.

Credit Card Limit of $8,000 with a current balance of $5,000.

Other Loan Debts $30,000 car loan with repayments of $609.00 per month.

Assets Savings with a bank $50,000

Small assets with a total value of $60,000

Household Living

Expenses

$1,200.00 per month

Costs Stamp duty and purchase costs to be paid from savings.

Recommendation The Loan Application is recommended for pre-approval by the authorised credit

representative.

To complete a Risk Assessment use the Risk Register template below:

1. List and highlight 3 Risks you consider to be important and which you have identified

from the above Loan Application scenario and list the risks you have identified in the

relevant coumn.

2. Rate each of the 3 Risks according to theirLikelihood (L) and Consequence (C)of a

negative event occuring and insert the ratings in the relevant columns.

3. Calculate the Risk Rating (LxC)value for each of the 3 Risks and insert the Risk Rating

values in the relevant column.

4. Refer to the Ranking Key table below and record in the Risk Register:

a. level of risk calculated; and

b. The required action to be undertaken.

5. In ABank, if the loan presents some high risks (risk rating 15-20) it can often fall outside of

your approval limits or delegated lending authority (DLA). You have a senior credit

assessor that you refer loans for approval that present higher risks. Based on your risk

ratings determine if the Loan Application is outside your Delegated Lending Authority

(DLA). Briefly explain why you may need to escalate the loan application to a higher DLA

holder,for approval sign-off.

A8 © AAMC Training Group Assessment V2.2

Risk ManagementAssessment

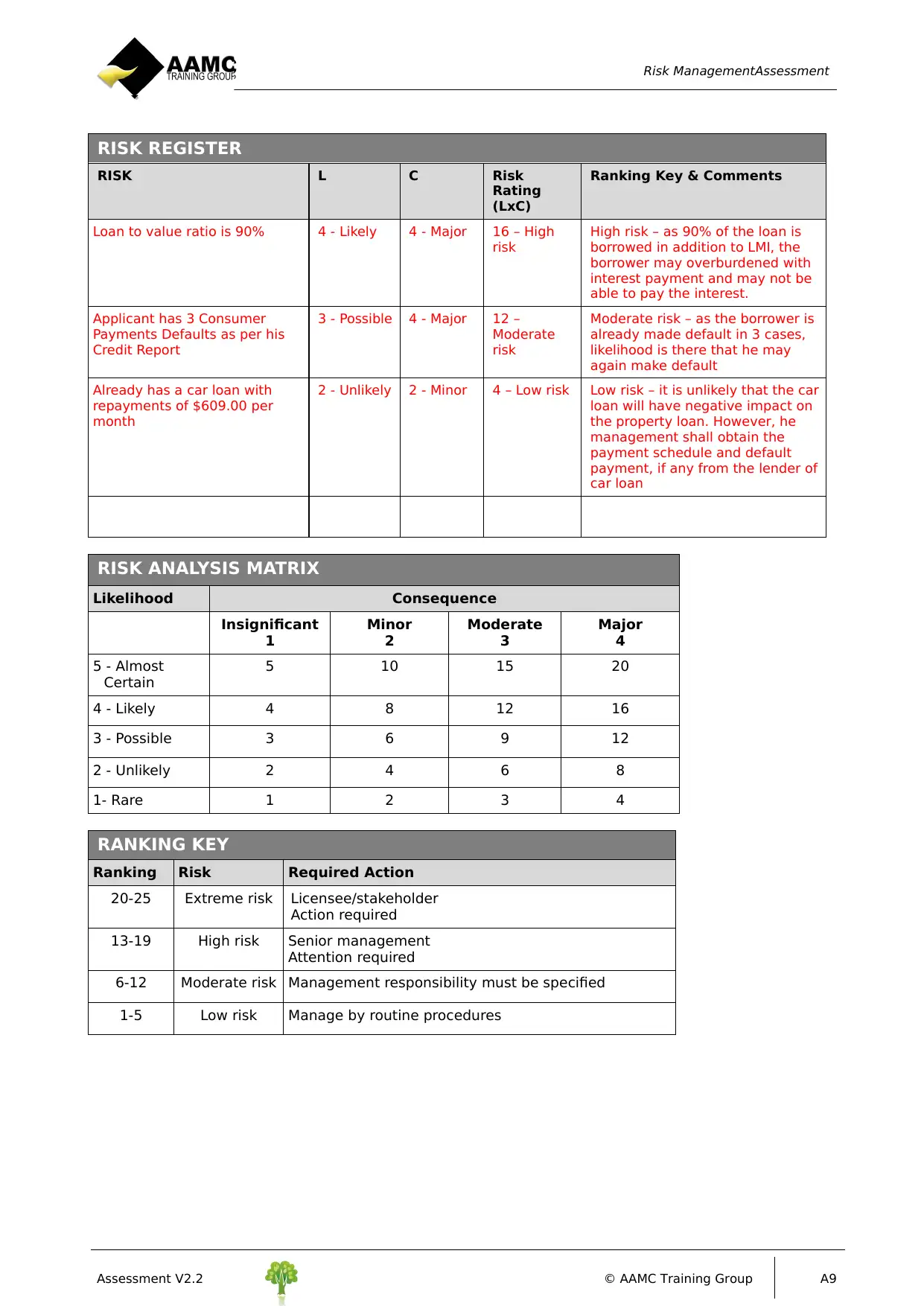

RISK REGISTER

RISK L C Risk

Rating

(LxC)

Ranking Key & Comments

Loan to value ratio is 90% 4 - Likely 4 - Major 16 – High

risk

High risk – as 90% of the loan is

borrowed in addition to LMI, the

borrower may overburdened with

interest payment and may not be

able to pay the interest.

Applicant has 3 Consumer

Payments Defaults as per his

Credit Report

3 - Possible 4 - Major 12 –

Moderate

risk

Moderate risk – as the borrower is

already made default in 3 cases,

likelihood is there that he may

again make default

Already has a car loan with

repayments of $609.00 per

month

2 - Unlikely 2 - Minor 4 – Low risk Low risk – it is unlikely that the car

loan will have negative impact on

the property loan. However, he

management shall obtain the

payment schedule and default

payment, if any from the lender of

car loan

RISK ANALYSIS MATRIX

Likelihood Consequence

Insignificant

1

Minor

2

Moderate

3

Major

4

5 - Almost

Certain

5 10 15 20

4 - Likely 4 8 12 16

3 - Possible 3 6 9 12

2 - Unlikely 2 4 6 8

1- Rare 1 2 3 4

RANKING KEY

Ranking Risk Required Action

20-25 Extreme risk Licensee/stakeholder

Action required

13-19 High risk Senior management

Attention required

6-12 Moderate risk Management responsibility must be specified

1-5 Low risk Manage by routine procedures

Assessment V2.2 © AAMC Training Group A9

RISK REGISTER

RISK L C Risk

Rating

(LxC)

Ranking Key & Comments

Loan to value ratio is 90% 4 - Likely 4 - Major 16 – High

risk

High risk – as 90% of the loan is

borrowed in addition to LMI, the

borrower may overburdened with

interest payment and may not be

able to pay the interest.

Applicant has 3 Consumer

Payments Defaults as per his

Credit Report

3 - Possible 4 - Major 12 –

Moderate

risk

Moderate risk – as the borrower is

already made default in 3 cases,

likelihood is there that he may

again make default

Already has a car loan with

repayments of $609.00 per

month

2 - Unlikely 2 - Minor 4 – Low risk Low risk – it is unlikely that the car

loan will have negative impact on

the property loan. However, he

management shall obtain the

payment schedule and default

payment, if any from the lender of

car loan

RISK ANALYSIS MATRIX

Likelihood Consequence

Insignificant

1

Minor

2

Moderate

3

Major

4

5 - Almost

Certain

5 10 15 20

4 - Likely 4 8 12 16

3 - Possible 3 6 9 12

2 - Unlikely 2 4 6 8

1- Rare 1 2 3 4

RANKING KEY

Ranking Risk Required Action

20-25 Extreme risk Licensee/stakeholder

Action required

13-19 High risk Senior management

Attention required

6-12 Moderate risk Management responsibility must be specified

1-5 Low risk Manage by routine procedures

Assessment V2.2 © AAMC Training Group A9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.