External Reporting Analysis: AASB 101 and Dom Ltd Financial Statements

VerifiedAdded on 2020/03/28

|8

|1057

|254

Report

AI Summary

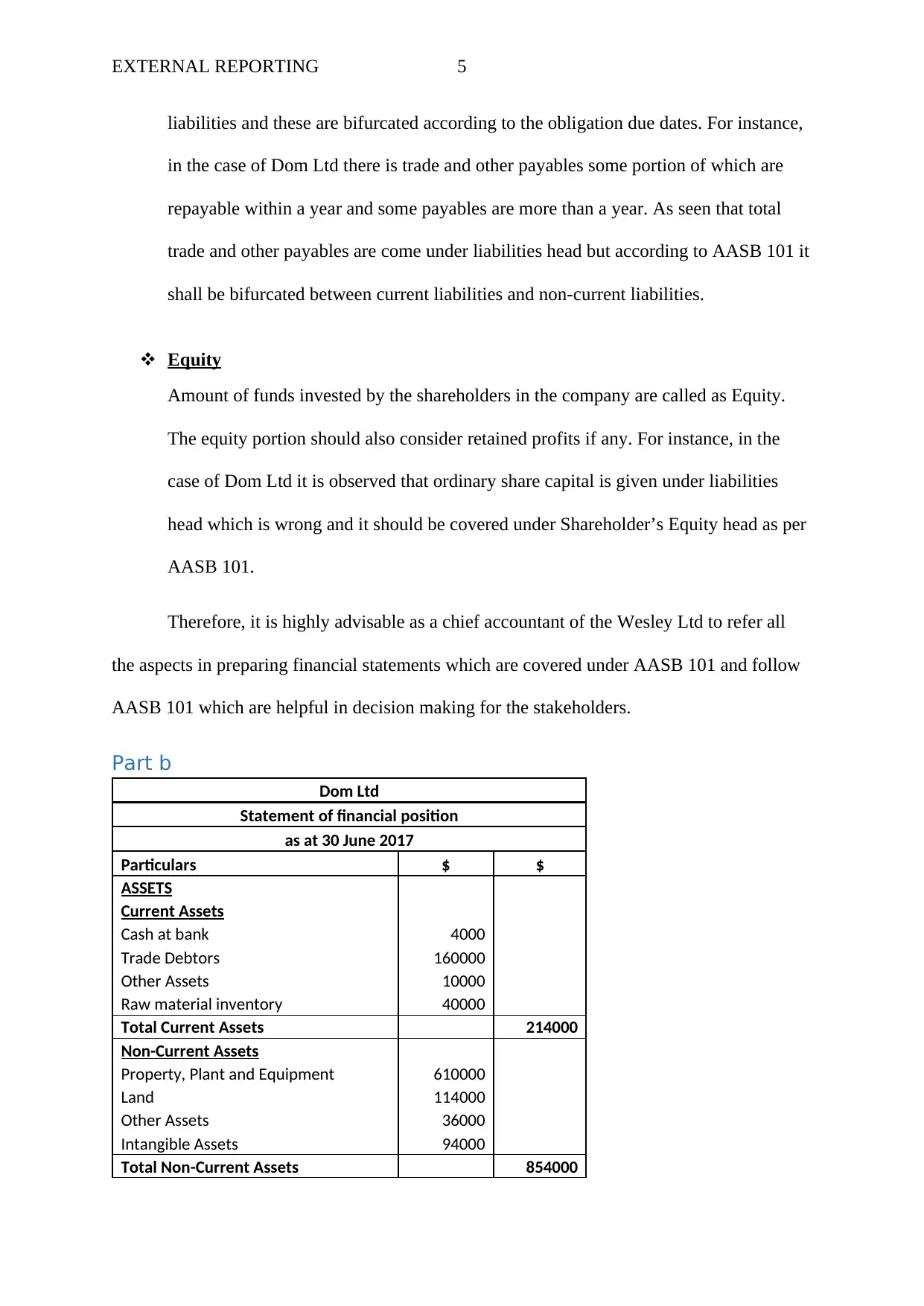

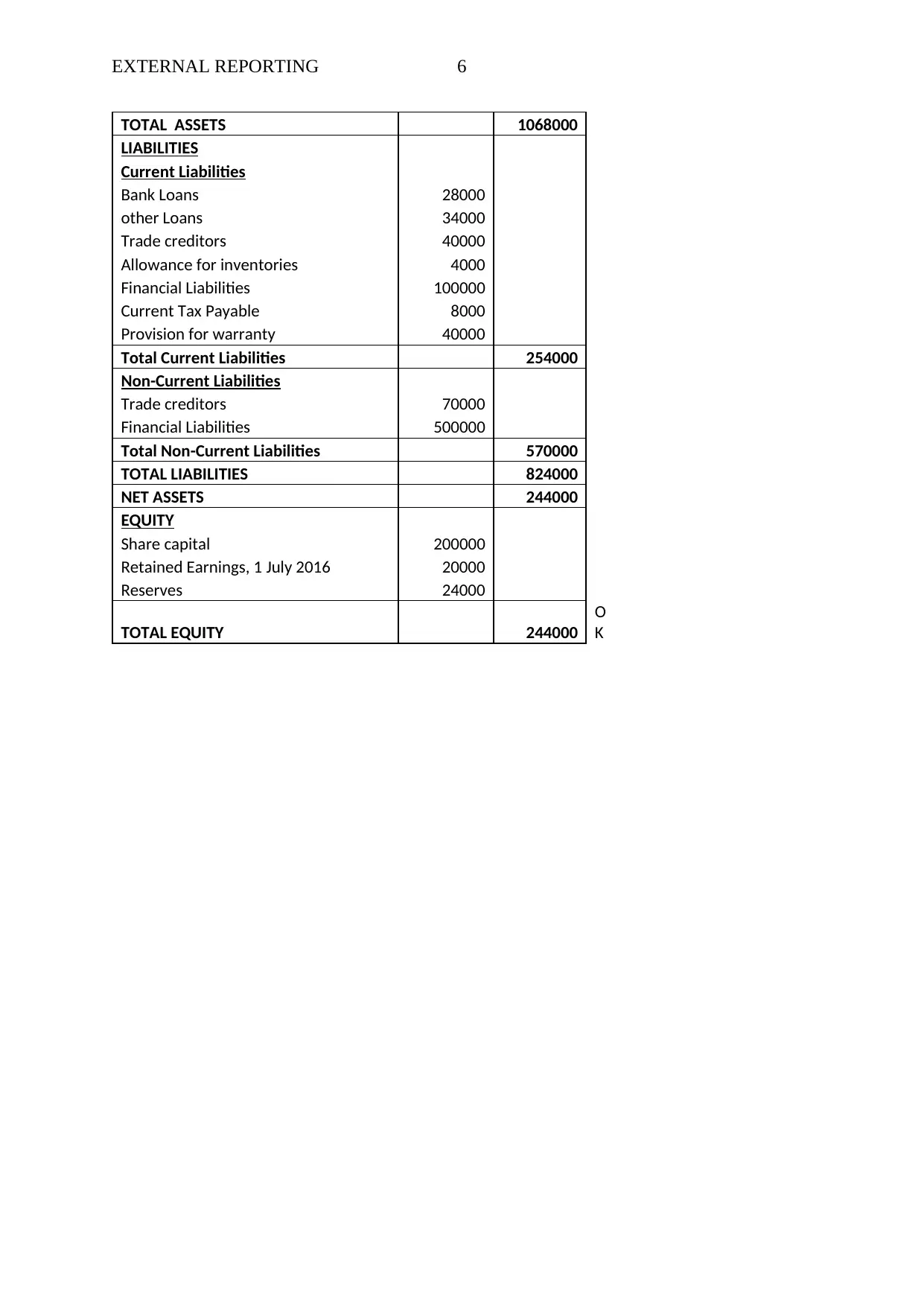

This report provides a comprehensive analysis of the external reporting practices of Dom Ltd, focusing on its financial statements as of June 30, 2017. The report, prepared for Jennifer by the Chief Accountant of Wesley Ltd, identifies key issues in the presentation of the statement of financial position, specifically concerning compliance with Australian Accounting Standard AASB 101. The analysis highlights the importance of presenting a true and fair view of the company's financial stability to stakeholders by correctly classifying assets, liabilities, and equity. The report critiques the existing financial statement, pointing out the lack of proper line item segregation and sub-headings, and provides recommendations for improvement, such as separating current and non-current assets and liabilities according to AASB 101 guidelines. The report also includes a revised statement of financial position for Dom Ltd, demonstrating the correct classification of assets, liabilities, and equity, and emphasizes the importance of following AASB 101 to facilitate informed decision-making by stakeholders. The report concludes with a reference to AASB 101 (2015) for further guidance.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.