Company Accounting: AASB 112 and Financial Statements Analysis

VerifiedAdded on 2020/05/11

|14

|2993

|52

Report

AI Summary

This report examines the accounting standard AASB 112, focusing on deferred tax assets, liabilities, expense, and income. It evaluates the standard's accounting treatment and disclosures, particularly regarding temporary differences between accounting and taxable income. The report analyzes the financial statements of Woolworths Limited and Commonwealth Bank for 2015 and 2016, assessing the impact of deferred tax assets and liabilities, and conducting ratio analysis to understand the financial health of the companies. The analysis includes a critical evaluation of the standard, its disclosures, and the implications for financial statement users. The report aims to provide a clear understanding of how deferred tax impacts financial reporting and decision-making.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The accounting has the very important value in the functioning of the company operations. It is the only

accounting department which controls the operation of the company and helps in coordinating the efforts

of each function. The main aim of this report is to have an understanding of the deferred tax assets,

deferred tax liabilities, deferred tax expense and deferred tax income. While understanding the

aforementioned terms the reference has been made to the provisions of the Australian Accounting

standard number one hundred and twelve. The second major aim is to analyze the financial statements of

the two companies registered on Australian stock exchange. With these aims, the report has been

prepared.

EXECUTIVE SUMMARY........................................................................................................................................ 2

2

The accounting has the very important value in the functioning of the company operations. It is the only

accounting department which controls the operation of the company and helps in coordinating the efforts

of each function. The main aim of this report is to have an understanding of the deferred tax assets,

deferred tax liabilities, deferred tax expense and deferred tax income. While understanding the

aforementioned terms the reference has been made to the provisions of the Australian Accounting

standard number one hundred and twelve. The second major aim is to analyze the financial statements of

the two companies registered on Australian stock exchange. With these aims, the report has been

prepared.

EXECUTIVE SUMMARY........................................................................................................................................ 2

2

INTRODUCTION.................................................................................................................................................. 4

EVALUATION OF AASB 112.................................................................................................................................. 5

ACCOUNTING TREATMENT AND DISCLOSURES.................................................................................................... 6

ANALYSIS OF FINANCIAL STATEMENTS................................................................................................................ 8

IMPACT OF DTA AND DTLS......................................................................................................................................8

RATIO ANALYSIS.......................................................................................................................................................9

CONCLUSION.................................................................................................................................................... 10

REFERENCES...................................................................................................................................................... 11

APPENDIX......................................................................................................................................................... 12

3

EVALUATION OF AASB 112.................................................................................................................................. 5

ACCOUNTING TREATMENT AND DISCLOSURES.................................................................................................... 6

ANALYSIS OF FINANCIAL STATEMENTS................................................................................................................ 8

IMPACT OF DTA AND DTLS......................................................................................................................................8

RATIO ANALYSIS.......................................................................................................................................................9

CONCLUSION.................................................................................................................................................... 10

REFERENCES...................................................................................................................................................... 11

APPENDIX......................................................................................................................................................... 12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The title of the report is AASB 112 and analysis of financial statements. As the title suggests the

main aim of the report is to understand the concept of the deferred tax assets and deferred tax

liabilities. The purpose is to analyze the extent to which the disclosure relating to the Australian

accounting standard has prescribed and second purpose is to analyze how the users of the

financial statements finds the information relating to taxes as helpful and useful. After that the

financial statements of Woolworths Limited and Common Wealth Bank has been analyzed for

the year ending 2015 and 2016.

4

The title of the report is AASB 112 and analysis of financial statements. As the title suggests the

main aim of the report is to understand the concept of the deferred tax assets and deferred tax

liabilities. The purpose is to analyze the extent to which the disclosure relating to the Australian

accounting standard has prescribed and second purpose is to analyze how the users of the

financial statements finds the information relating to taxes as helpful and useful. After that the

financial statements of Woolworths Limited and Common Wealth Bank has been analyzed for

the year ending 2015 and 2016.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EVALUATION OF AASB 112

The standard has been criticized majorly on the premise that it has not followed the uniform

application of the accounting policies and procedures relating to the asset or liability. The critical

evaluation has been done in respect of the recognition and the measurement of the respective

asset or the liability. Before evaluating the aspect of the standards, it is vital to understand the

aim of the formation of standard. The main aim of this standard is to provide the means of

accounting treatment as to how the same shall be done for taxes. The tax in the accounting

standard has not only defined the current tax but has also provided for the tax aspect that can be

generated in the future or can have impact on the future (Ayers, 2008). In the beginning of the

standard it has been made clear that this accounting standard provides for the consequences on

tax both for current and upcoming of the:

- Offsetting of carrying amount that the assets or the liabilities will have respectively in the

future which are further shown in the annual report of the company showing the financial

health and

- Other transactions relating to the current reporting year and that is stated in the annual

report of the company (Deloitte, 2016).

The concept of deferred tax asset and deferred tax liability has been originated majorly from the

difference between the accounting income and taxable income. The accounting profit is

originated from the booking of the events of the company in the accounting books as per the

accounting standards of the company and the taxable profit is the profit which is basically

calculated for the purpose of calculating as to how much tax will be paid by the company for the

current year. It is calculated as per the provisions of the Income Tax laws of the country in which

the company is operating its functions and not as per the rules of accounting or the principles of

the respective accounting standards (Petree, 2005). In accordance with the Statement of

Accounting concepts number 109 on accounting for income tax read with accounting standard, it

is to compare the carrying amount of the asset or liability with the tax base of the respective asset

or the respective liability. Tax base is the amount which is directly related to the respective asset

or the respective liability for the income tax purposes. In case any difference arises then either

the asset or the liability is created and is recognized in the financial statements of the company.

5

The standard has been criticized majorly on the premise that it has not followed the uniform

application of the accounting policies and procedures relating to the asset or liability. The critical

evaluation has been done in respect of the recognition and the measurement of the respective

asset or the liability. Before evaluating the aspect of the standards, it is vital to understand the

aim of the formation of standard. The main aim of this standard is to provide the means of

accounting treatment as to how the same shall be done for taxes. The tax in the accounting

standard has not only defined the current tax but has also provided for the tax aspect that can be

generated in the future or can have impact on the future (Ayers, 2008). In the beginning of the

standard it has been made clear that this accounting standard provides for the consequences on

tax both for current and upcoming of the:

- Offsetting of carrying amount that the assets or the liabilities will have respectively in the

future which are further shown in the annual report of the company showing the financial

health and

- Other transactions relating to the current reporting year and that is stated in the annual

report of the company (Deloitte, 2016).

The concept of deferred tax asset and deferred tax liability has been originated majorly from the

difference between the accounting income and taxable income. The accounting profit is

originated from the booking of the events of the company in the accounting books as per the

accounting standards of the company and the taxable profit is the profit which is basically

calculated for the purpose of calculating as to how much tax will be paid by the company for the

current year. It is calculated as per the provisions of the Income Tax laws of the country in which

the company is operating its functions and not as per the rules of accounting or the principles of

the respective accounting standards (Petree, 2005). In accordance with the Statement of

Accounting concepts number 109 on accounting for income tax read with accounting standard, it

is to compare the carrying amount of the asset or liability with the tax base of the respective asset

or the respective liability. Tax base is the amount which is directly related to the respective asset

or the respective liability for the income tax purposes. In case any difference arises then either

the asset or the liability is created and is recognized in the financial statements of the company.

5

The creation of the deferred tax asset or the deferred tax liability has been criticized greatly

because of the major reason that the said creation does not connects in any manner with the

conceptual framework of presentation of the financial statements and also with the statement of

financial concepts. These two major criticisms are:

- Definition of the Asset – The accounting standard along with the statement of accounting

concepts have detailed that the asset shall be recognized in the books of accounts only it

is identifiable, measurable and most importantly is able to generate the economic benefits

for the company in future. It means the asset shall be embodied with the future economic

benefits. But in the case of the deferred tax asset, the company has no claim to receive

from someone and it will be reversed only if the company will have sufficient income

and the tax thereon can be adjusted from the deferred tax asset so created (Mackintosh,

2006).

- Definition of Liability – The liability is defined as the amount which is created as the

result of the event of the past and which will be settled in the future which entails the

outflow of the resources of the entity. Deferred tax liability does not carry any outflow of

the resources in cash or bank.

Although it has been critically analyzed by the users but it is necessary to account for the effect

that has been arisen from the temporary differences. Thus, the deferred tax asset or liability so

created is against the conceptual framework of accounting for reporting purpose and the

statement of accounting concepts and in some manner adds confusion to the users while taking

the decisions on the financial statements of the company.

ACCOUNTING TREATMENT AND DISCLOSURES

In actual, the current accounting treatment and disclosures hinders users. AASB 112 is the

Australian accounting standard issued by the Australian accounting standard board on income

taxes. It has been issued on the 15th of July of two thousand and four and has been made

applicable for the reporting periods starting from first of January two thousand and five only.

The standard has prescribed the accounting treatment of the differences generated in reconciling

the accounting profit and the taxable profit and thus provides the guidelines as to how the same

6

because of the major reason that the said creation does not connects in any manner with the

conceptual framework of presentation of the financial statements and also with the statement of

financial concepts. These two major criticisms are:

- Definition of the Asset – The accounting standard along with the statement of accounting

concepts have detailed that the asset shall be recognized in the books of accounts only it

is identifiable, measurable and most importantly is able to generate the economic benefits

for the company in future. It means the asset shall be embodied with the future economic

benefits. But in the case of the deferred tax asset, the company has no claim to receive

from someone and it will be reversed only if the company will have sufficient income

and the tax thereon can be adjusted from the deferred tax asset so created (Mackintosh,

2006).

- Definition of Liability – The liability is defined as the amount which is created as the

result of the event of the past and which will be settled in the future which entails the

outflow of the resources of the entity. Deferred tax liability does not carry any outflow of

the resources in cash or bank.

Although it has been critically analyzed by the users but it is necessary to account for the effect

that has been arisen from the temporary differences. Thus, the deferred tax asset or liability so

created is against the conceptual framework of accounting for reporting purpose and the

statement of accounting concepts and in some manner adds confusion to the users while taking

the decisions on the financial statements of the company.

ACCOUNTING TREATMENT AND DISCLOSURES

In actual, the current accounting treatment and disclosures hinders users. AASB 112 is the

Australian accounting standard issued by the Australian accounting standard board on income

taxes. It has been issued on the 15th of July of two thousand and four and has been made

applicable for the reporting periods starting from first of January two thousand and five only.

The standard has prescribed the accounting treatment of the differences generated in reconciling

the accounting profit and the taxable profit and thus provides the guidelines as to how the same

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shall be recognized in the financial statements of the company as the deferred tax liability,

deferred tax asset, deferred tax expense and the deferred tax income (Schipper, 2003).

Whenever any type of differences has been identified between the accounting profit and the

taxable profit then the corresponding deferred tax asset or the deferred tax liability is accounted

for in the books of accounts of the company. The differences so observed are regarded as the

temporary differences and are liable for getting reversed in the future. These temporary

differences are generally grouped under the two heads – one difference is that which is known as

the taxable difference and the other one is known as the deductible difference. In the first case of

the difference, deferred tax liability is created as the taxable difference will increase the liability

of the company to pay the tax in the future periods and in the second case of the difference,

deferred tax asset is created as the deductible difference and will result in the decrease of the tax

which will be paid in the future periods to come (Schrand, 2003). The accounting treatment of

these two differences is first done in the form of journal entry after doing the calculations. In the

first case deferred tax expense account is debited and the deferred tax liability account is

credited. In the second case the deferred tax asset account is debited and the deferred tax expense

account is credited.

After making the accounting entry the presentation of the same is done in the financial

statements of the company. The deferred tax expense either credited or debited is shown in the

statement of the profit and loss after the Current Tax Expense and the deferred tax liability or the

deferred tax asset so created is disclosed in the Statement of affairs on the liability and asset side

respectively. The paragraph number 79 to 81 of the accounting standard number 112 has

prescribed the disclosure requirements and given the exhaustive list of the requirements (AASB,

2015). Few of them have been mentioned below which are also relevant for the users of the

financial statements:

- A detailed explanation of the connection between the deferred tax asset or liability is

required to be given

- A detailed explanation of the changes in the rates applicable to the company for the

current financial year

- The amount of the temporary differences which has been identified while reconciling the

accounting profit and the taxable profit of the company (Skinner, 2008)

7

deferred tax asset, deferred tax expense and the deferred tax income (Schipper, 2003).

Whenever any type of differences has been identified between the accounting profit and the

taxable profit then the corresponding deferred tax asset or the deferred tax liability is accounted

for in the books of accounts of the company. The differences so observed are regarded as the

temporary differences and are liable for getting reversed in the future. These temporary

differences are generally grouped under the two heads – one difference is that which is known as

the taxable difference and the other one is known as the deductible difference. In the first case of

the difference, deferred tax liability is created as the taxable difference will increase the liability

of the company to pay the tax in the future periods and in the second case of the difference,

deferred tax asset is created as the deductible difference and will result in the decrease of the tax

which will be paid in the future periods to come (Schrand, 2003). The accounting treatment of

these two differences is first done in the form of journal entry after doing the calculations. In the

first case deferred tax expense account is debited and the deferred tax liability account is

credited. In the second case the deferred tax asset account is debited and the deferred tax expense

account is credited.

After making the accounting entry the presentation of the same is done in the financial

statements of the company. The deferred tax expense either credited or debited is shown in the

statement of the profit and loss after the Current Tax Expense and the deferred tax liability or the

deferred tax asset so created is disclosed in the Statement of affairs on the liability and asset side

respectively. The paragraph number 79 to 81 of the accounting standard number 112 has

prescribed the disclosure requirements and given the exhaustive list of the requirements (AASB,

2015). Few of them have been mentioned below which are also relevant for the users of the

financial statements:

- A detailed explanation of the connection between the deferred tax asset or liability is

required to be given

- A detailed explanation of the changes in the rates applicable to the company for the

current financial year

- The amount of the temporary differences which has been identified while reconciling the

accounting profit and the taxable profit of the company (Skinner, 2008)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- In reference to each of the temporary differences so identified, quantify the amount of the

deferred tax assets and the deferred tax liabilities which has been arrived by multiplying

the effective tax rate to the temporary differences

The aforementioned four disclosures gives the users of the financial statements as the insights as

to how the company is operating its functions and how the company has been able to reconcile

the accounting profit and the taxable profit and accordingly how the company has complied with

the provisions of the accounting standards of the company. But the users will not be able to

understand the actual tax expense of the current financial year in much better manner. It is

because all the companies whether it is manufacturing or service provider will find the effective

rate on its own and as per the Tax Transparency code of Australia, lower the effective tax rate

higher will be the chances of getting an scrutiny before Australian Taxation office (Pozen, 2007).

Thus, in this manner, the accounting treatment and the disclosure will not assist the users.

ANALYSIS OF FINANCIAL STATEMENTS

IMPACT OF DTA AND DTLS

Common Wealth Bank - The note number four of the annual report of the company has provided

the detail of Income Taxes. At first for the consecutive period of last three years, the current tax

expense has been calculated and accordingly applicable tax percentage is calculated and

identified.

Woolworths Limited - The note number fourteen of the annual report of the company has

provided detail of the Income Taxes. The income tax expense has been detailed with the

comparative amount for the reporting year ending 2016 and 2015.

In both the cases, the temporary differences has been detailed like provision for employee

benefits, lease financing, intangible assets, the investments made in associates, subsidiaries, joint

ventures and others (Company Official Website, 2016).

8

deferred tax assets and the deferred tax liabilities which has been arrived by multiplying

the effective tax rate to the temporary differences

The aforementioned four disclosures gives the users of the financial statements as the insights as

to how the company is operating its functions and how the company has been able to reconcile

the accounting profit and the taxable profit and accordingly how the company has complied with

the provisions of the accounting standards of the company. But the users will not be able to

understand the actual tax expense of the current financial year in much better manner. It is

because all the companies whether it is manufacturing or service provider will find the effective

rate on its own and as per the Tax Transparency code of Australia, lower the effective tax rate

higher will be the chances of getting an scrutiny before Australian Taxation office (Pozen, 2007).

Thus, in this manner, the accounting treatment and the disclosure will not assist the users.

ANALYSIS OF FINANCIAL STATEMENTS

IMPACT OF DTA AND DTLS

Common Wealth Bank - The note number four of the annual report of the company has provided

the detail of Income Taxes. At first for the consecutive period of last three years, the current tax

expense has been calculated and accordingly applicable tax percentage is calculated and

identified.

Woolworths Limited - The note number fourteen of the annual report of the company has

provided detail of the Income Taxes. The income tax expense has been detailed with the

comparative amount for the reporting year ending 2016 and 2015.

In both the cases, the temporary differences has been detailed like provision for employee

benefits, lease financing, intangible assets, the investments made in associates, subsidiaries, joint

ventures and others (Company Official Website, 2016).

8

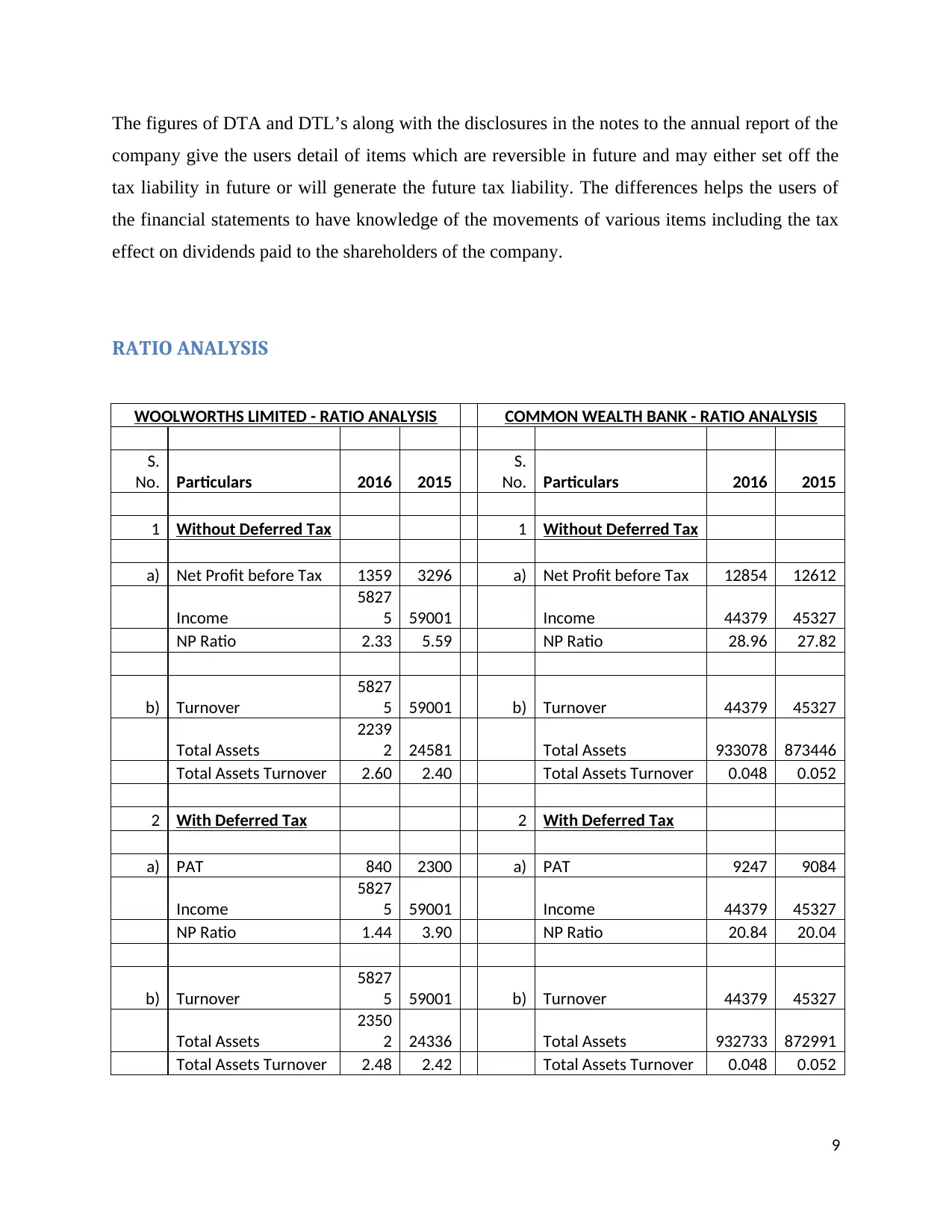

The figures of DTA and DTL’s along with the disclosures in the notes to the annual report of the

company give the users detail of items which are reversible in future and may either set off the

tax liability in future or will generate the future tax liability. The differences helps the users of

the financial statements to have knowledge of the movements of various items including the tax

effect on dividends paid to the shareholders of the company.

RATIO ANALYSIS

WOOLWORTHS LIMITED - RATIO ANALYSIS COMMON WEALTH BANK - RATIO ANALYSIS

S.

No. Particulars 2016 2015

S.

No. Particulars 2016 2015

1 Without Deferred Tax 1 Without Deferred Tax

a) Net Profit before Tax 1359 3296 a) Net Profit before Tax 12854 12612

Income

5827

5 59001 Income 44379 45327

NP Ratio 2.33 5.59 NP Ratio 28.96 27.82

b) Turnover

5827

5 59001 b) Turnover 44379 45327

Total Assets

2239

2 24581 Total Assets 933078 873446

Total Assets Turnover 2.60 2.40 Total Assets Turnover 0.048 0.052

2 With Deferred Tax 2 With Deferred Tax

a) PAT 840 2300 a) PAT 9247 9084

Income

5827

5 59001 Income 44379 45327

NP Ratio 1.44 3.90 NP Ratio 20.84 20.04

b) Turnover

5827

5 59001 b) Turnover 44379 45327

Total Assets

2350

2 24336 Total Assets 932733 872991

Total Assets Turnover 2.48 2.42 Total Assets Turnover 0.048 0.052

9

company give the users detail of items which are reversible in future and may either set off the

tax liability in future or will generate the future tax liability. The differences helps the users of

the financial statements to have knowledge of the movements of various items including the tax

effect on dividends paid to the shareholders of the company.

RATIO ANALYSIS

WOOLWORTHS LIMITED - RATIO ANALYSIS COMMON WEALTH BANK - RATIO ANALYSIS

S.

No. Particulars 2016 2015

S.

No. Particulars 2016 2015

1 Without Deferred Tax 1 Without Deferred Tax

a) Net Profit before Tax 1359 3296 a) Net Profit before Tax 12854 12612

Income

5827

5 59001 Income 44379 45327

NP Ratio 2.33 5.59 NP Ratio 28.96 27.82

b) Turnover

5827

5 59001 b) Turnover 44379 45327

Total Assets

2239

2 24581 Total Assets 933078 873446

Total Assets Turnover 2.60 2.40 Total Assets Turnover 0.048 0.052

2 With Deferred Tax 2 With Deferred Tax

a) PAT 840 2300 a) PAT 9247 9084

Income

5827

5 59001 Income 44379 45327

NP Ratio 1.44 3.90 NP Ratio 20.84 20.04

b) Turnover

5827

5 59001 b) Turnover 44379 45327

Total Assets

2350

2 24336 Total Assets 932733 872991

Total Assets Turnover 2.48 2.42 Total Assets Turnover 0.048 0.052

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above table has been made to understand as to how far the value of the deferred assets and

the deferred expense are valuable for users of the financial statements while taking the decision.

In the case of the Woolworths Limited, the net profit ratio of the company for both the financial

years has been reduced considerably which indicates that the amount of the deferred tax expense

plays the very important role in declaring the earning generated per share of the company. It is

calculated by proportioning the net profit available for the shareholders of the company by the

number of the stock outstanding at the end of the financial year. As the Earning per share

disclosed is decreased figure and hence the users of the financial statements is required to

consider the effect of the deferred tax expense (Phillips, 2004).

In the case of Common Wealth Bank, if rather checking the net profit ratio, the total assets

turnover is analyzed, it is observed that the company has been able to utilize the assets of the

company in the same manner as the company has made in the earlier years and there are no such

differences. In this manner, the deferred tax assets and liabilities does not have much relevance

in analyzing the financial positions of the company like in the ratios as – Net worth of the

company, net assets of the company.

Therefore, the relevance is very less for the users it is because the figure is very immaterial to

affect the decision of the stakeholders of the company.

CONCLUSION

Each and every company shall follow the correct accounting treatment and the correct financial

disclosures which are mentioned in the relevant accounting standards as prescribed by the

accounting standard board and other standard setting bodies, statement of accounting concepts

and conceptual framework of accounting and reporting. In the report, the Australian accounting

standard 112 on income taxes has been deeply analyzed with an understanding as to how the

accounting treatment is done for the transactions of the company relating to deferred tax asset or

the deferred tax liability. Also the disclosure requirements have been identified and analysed and

then the accounting standard has been critically evaluated as to how the deferred tax asset or

10

the deferred expense are valuable for users of the financial statements while taking the decision.

In the case of the Woolworths Limited, the net profit ratio of the company for both the financial

years has been reduced considerably which indicates that the amount of the deferred tax expense

plays the very important role in declaring the earning generated per share of the company. It is

calculated by proportioning the net profit available for the shareholders of the company by the

number of the stock outstanding at the end of the financial year. As the Earning per share

disclosed is decreased figure and hence the users of the financial statements is required to

consider the effect of the deferred tax expense (Phillips, 2004).

In the case of Common Wealth Bank, if rather checking the net profit ratio, the total assets

turnover is analyzed, it is observed that the company has been able to utilize the assets of the

company in the same manner as the company has made in the earlier years and there are no such

differences. In this manner, the deferred tax assets and liabilities does not have much relevance

in analyzing the financial positions of the company like in the ratios as – Net worth of the

company, net assets of the company.

Therefore, the relevance is very less for the users it is because the figure is very immaterial to

affect the decision of the stakeholders of the company.

CONCLUSION

Each and every company shall follow the correct accounting treatment and the correct financial

disclosures which are mentioned in the relevant accounting standards as prescribed by the

accounting standard board and other standard setting bodies, statement of accounting concepts

and conceptual framework of accounting and reporting. In the report, the Australian accounting

standard 112 on income taxes has been deeply analyzed with an understanding as to how the

accounting treatment is done for the transactions of the company relating to deferred tax asset or

the deferred tax liability. Also the disclosure requirements have been identified and analysed and

then the accounting standard has been critically evaluated as to how the deferred tax asset or

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

liability have helped the users of the financial statements of the company in understanding the

financial position and the financial performance of the company and whether it has been found

useful. For the purpose of the report, the financial statements of two companies have been

analysed for the year 2015 and 2016. These two companies are Woolworths Limited and

Common wealth Bank. In order to conclude the report, the accounting and disclosure of the taxes

shall be done in accordance with provisions of the accounting standards.

REFERENCES

AASB, (2015), “Income Taxes”, available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB112_08-15.pdf accessed on 15-10-2017

Ayers, B.C, (2008), “Deferred tax accounting under SFAS No. 109: An empirical investigation

of its incremental value-relevance relative to APB No. 11” Accounting Review, pp.195-212

Company Official Website, (2016), “Annual Report”, available at

https://www.commbank.com.au accessed on 15-10-2017

Company Official Website, (2016), “Annual Report”, available at

https://www.woolworthsgroup.com.au accessed on 15-10-2017

Deloitte,(2016), “IASB 16”, available at

https://www.iasplus.com/en/meeting-notes/iasb/2016/may/income-taxes accessed on 15-10-2017

Mackintosh, N.B. (2006). “Accounting-truth, lies, or "bullshit"? A philosophical investigation:

Commentary, the FASB and accounting for economic reality” Accounting and the Public Interest

6

11

financial position and the financial performance of the company and whether it has been found

useful. For the purpose of the report, the financial statements of two companies have been

analysed for the year 2015 and 2016. These two companies are Woolworths Limited and

Common wealth Bank. In order to conclude the report, the accounting and disclosure of the taxes

shall be done in accordance with provisions of the accounting standards.

REFERENCES

AASB, (2015), “Income Taxes”, available at

http://www.aasb.gov.au/admin/file/content105/c9/AASB112_08-15.pdf accessed on 15-10-2017

Ayers, B.C, (2008), “Deferred tax accounting under SFAS No. 109: An empirical investigation

of its incremental value-relevance relative to APB No. 11” Accounting Review, pp.195-212

Company Official Website, (2016), “Annual Report”, available at

https://www.commbank.com.au accessed on 15-10-2017

Company Official Website, (2016), “Annual Report”, available at

https://www.woolworthsgroup.com.au accessed on 15-10-2017

Deloitte,(2016), “IASB 16”, available at

https://www.iasplus.com/en/meeting-notes/iasb/2016/may/income-taxes accessed on 15-10-2017

Mackintosh, N.B. (2006). “Accounting-truth, lies, or "bullshit"? A philosophical investigation:

Commentary, the FASB and accounting for economic reality” Accounting and the Public Interest

6

11

Petree, T.R., (2005), “Evaluating deferred tax assets”. Journal of Accountancy, 179(3), p.71.

Phillips, J.D, (2004) “Decomposing changes in deferred tax assets and liabilities to isolate

earnings management activities”. Journal of the American Taxation Association, 26(s-1), pp.43-

66.

Pozen, R. (2007). “Discussion Paper for Consideration by the SEC Advisory Committee on

Improvements to Financial Reporting”. Security Exchange Commission.

Schipper, K. (2003). “Principles-based accounting standards”. Accounting Horizons, 17, 61-72

Schrand, C.M.,( 2003). “Earnings management using the valuation allowance for deferred tax

assets under SFAS No. 109”. Contemporary Accounting Research, 20(3), pp.579-611.

Skinner, D.J., (2008). “The rise of deferred tax assets in Japan: The role of deferred tax

accounting in the Japanese banking crisis”. Journal of Accounting and Economics, 46(2),

pp.218-239.

APPENDIX

Impact of DTA and DTLs

Common Wealth

12

Phillips, J.D, (2004) “Decomposing changes in deferred tax assets and liabilities to isolate

earnings management activities”. Journal of the American Taxation Association, 26(s-1), pp.43-

66.

Pozen, R. (2007). “Discussion Paper for Consideration by the SEC Advisory Committee on

Improvements to Financial Reporting”. Security Exchange Commission.

Schipper, K. (2003). “Principles-based accounting standards”. Accounting Horizons, 17, 61-72

Schrand, C.M.,( 2003). “Earnings management using the valuation allowance for deferred tax

assets under SFAS No. 109”. Contemporary Accounting Research, 20(3), pp.579-611.

Skinner, D.J., (2008). “The rise of deferred tax assets in Japan: The role of deferred tax

accounting in the Japanese banking crisis”. Journal of Accounting and Economics, 46(2),

pp.218-239.

APPENDIX

Impact of DTA and DTLs

Common Wealth

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.