Exploring Depreciation Methods and Their Impact on Financial Reporting

VerifiedAdded on 2020/05/28

|10

|3125

|89

Essay

AI Summary

The essay delves into the strategic application of various depreciation techniques within corporate financial management, focusing on their effects on profit reporting and asset valuation over time. By analyzing different depreciation methods such as straight-line and accelerated depreciation, it highlights how these choices can significantly impact a company's financial statements and future economic benefits from assets. The discussion includes an exploration of ethical considerations when altering depreciation methods for financial advantage, using a case study to illustrate the potential implications on profit margins and asset valuation.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Executive Summary:

It is explained that governance and ethics is concerned about mortality and it is not

imposed on anyone. In contrast, it is considered that the ethics is highly efficient as the

confidence of the users might get boosted with maintaining the necessary level and quality of

work. Certain vital concerns associated with accounting of plant, property and equipment are

within the asset realization, the ascertainment of the carrying amounts along with advancements

within depreciation along with impairment losses that is realised along with the same.

Executive Summary:

It is explained that governance and ethics is concerned about mortality and it is not

imposed on anyone. In contrast, it is considered that the ethics is highly efficient as the

confidence of the users might get boosted with maintaining the necessary level and quality of

work. Certain vital concerns associated with accounting of plant, property and equipment are

within the asset realization, the ascertainment of the carrying amounts along with advancements

within depreciation along with impairment losses that is realised along with the same.

2FINANCIAL ACCOUNTING

Table of Contents

1. Introduction:................................................................................................................................3

2. Governance and Ethics:...............................................................................................................3

3. Role of Accountants in Depreciation Method Change................................................................4

4. Stakeholders.................................................................................................................................5

5. AASB 116 Standard Effect..........................................................................................................6

6. Conclusion:..................................................................................................................................7

References:......................................................................................................................................9

Table of Contents

1. Introduction:................................................................................................................................3

2. Governance and Ethics:...............................................................................................................3

3. Role of Accountants in Depreciation Method Change................................................................4

4. Stakeholders.................................................................................................................................5

5. AASB 116 Standard Effect..........................................................................................................6

6. Conclusion:..................................................................................................................................7

References:......................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

1. Introduction:

This case study has been prepared regarding a company that is “Sunshine Ltd” in which

the General Manager named Kam Sunshine considered approaching Maria Mars which is the

accountant of the company. The objective was to ensure certain advancements within the

company’s incoming profit discretely. This has increased certain dilemma for the accountant for

the reason that she is focussed on her contract renewal in the company. Other than being aware

of the fact that certain actions remain unethical, Maria has altered the depreciation method from

applying straight line method to using the sum-of-years digits technique (Bazley et al. 2013). For

this reason, the stakeholders has recognised that in this case study is focussed on shareholders,

governments, communities, partners, suppliers, consumers, accountant, general manager and the

creditors. Certain ethical concerns recognised by Maria in altering the depreciation methods that

is explained in accordance with the requirements of the company along with AASB 116 effect.

2. Governance and Ethics:

It is explained that governance and ethics is concerned about mortality and it is not

imposed on anyone. In contrast, ethics is considered to be highly efficient as the confidence of

the users might get boosted with maintaining the necessary level and quality of work. Certain

concerns associated with ethics of Sunshine Ltd are explained below:

Objectivity Violation- General Manager of Sunshine Ltd is observed to misbehave with

the company’s senior management for certain personal gain and the accountant has also

supported the person in attaining such objective. The company has employed several

depreciation techniques on the fixed assets in order to indicate the devaluation effect

along with depreciation method. This might indicate a situation within which the future

advantages associated with assets are anticipated to be caused. Maria has altered the

method of depreciation that has resulted in certain difference within the timing of the

overall depreciation (Aasb.gov.au. 2017). This has resulted on the decisions of the

shareholders to get impacted from the real decisions by certain anticipations regarding

error. The accountant was held responsible to indicate accounting information in a better

manner and the changes within financial reports should be reported. This is deemed to be

against the working ethics of the accountant that has interrupted the necessary objectivity

principle.

Integrity and Transparency Defect- the Company’s shareholders are deemed to have

the responsibility to realise about the profitability associated with its investments. Relied

on such variation associated with their investment profitability, they have the right to

make sure that the shares are kept within the company. For addressing the needs of the

shareholders within Sunshine Limited, Kam Sunshine has explained the fact that altering

the deprecation method for developing an illusion of constant high profit. This indicates

absence of integrity and transparency on the behalf of Sunshine Ltd in order to signify

proper information to the financial statement users (Beatty and Liao 2014).

1. Introduction:

This case study has been prepared regarding a company that is “Sunshine Ltd” in which

the General Manager named Kam Sunshine considered approaching Maria Mars which is the

accountant of the company. The objective was to ensure certain advancements within the

company’s incoming profit discretely. This has increased certain dilemma for the accountant for

the reason that she is focussed on her contract renewal in the company. Other than being aware

of the fact that certain actions remain unethical, Maria has altered the depreciation method from

applying straight line method to using the sum-of-years digits technique (Bazley et al. 2013). For

this reason, the stakeholders has recognised that in this case study is focussed on shareholders,

governments, communities, partners, suppliers, consumers, accountant, general manager and the

creditors. Certain ethical concerns recognised by Maria in altering the depreciation methods that

is explained in accordance with the requirements of the company along with AASB 116 effect.

2. Governance and Ethics:

It is explained that governance and ethics is concerned about mortality and it is not

imposed on anyone. In contrast, ethics is considered to be highly efficient as the confidence of

the users might get boosted with maintaining the necessary level and quality of work. Certain

concerns associated with ethics of Sunshine Ltd are explained below:

Objectivity Violation- General Manager of Sunshine Ltd is observed to misbehave with

the company’s senior management for certain personal gain and the accountant has also

supported the person in attaining such objective. The company has employed several

depreciation techniques on the fixed assets in order to indicate the devaluation effect

along with depreciation method. This might indicate a situation within which the future

advantages associated with assets are anticipated to be caused. Maria has altered the

method of depreciation that has resulted in certain difference within the timing of the

overall depreciation (Aasb.gov.au. 2017). This has resulted on the decisions of the

shareholders to get impacted from the real decisions by certain anticipations regarding

error. The accountant was held responsible to indicate accounting information in a better

manner and the changes within financial reports should be reported. This is deemed to be

against the working ethics of the accountant that has interrupted the necessary objectivity

principle.

Integrity and Transparency Defect- the Company’s shareholders are deemed to have

the responsibility to realise about the profitability associated with its investments. Relied

on such variation associated with their investment profitability, they have the right to

make sure that the shares are kept within the company. For addressing the needs of the

shareholders within Sunshine Limited, Kam Sunshine has explained the fact that altering

the deprecation method for developing an illusion of constant high profit. This indicates

absence of integrity and transparency on the behalf of Sunshine Ltd in order to signify

proper information to the financial statement users (Beatty and Liao 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

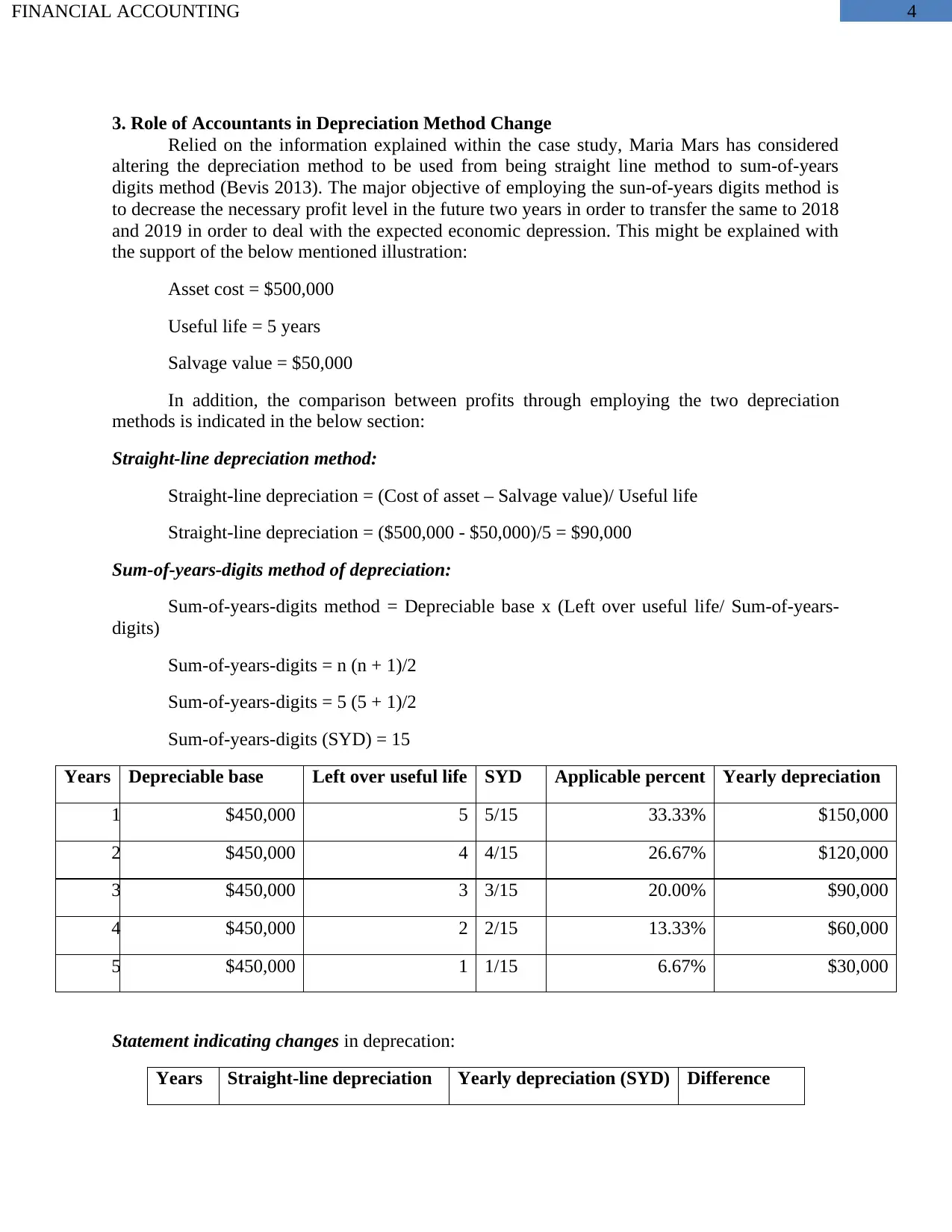

3. Role of Accountants in Depreciation Method Change

Relied on the information explained within the case study, Maria Mars has considered

altering the depreciation method to be used from being straight line method to sum-of-years

digits method (Bevis 2013). The major objective of employing the sun-of-years digits method is

to decrease the necessary profit level in the future two years in order to transfer the same to 2018

and 2019 in order to deal with the expected economic depression. This might be explained with

the support of the below mentioned illustration:

Asset cost = $500,000

Useful life = 5 years

Salvage value = $50,000

In addition, the comparison between profits through employing the two depreciation

methods is indicated in the below section:

Straight-line depreciation method:

Straight-line depreciation = (Cost of asset – Salvage value)/ Useful life

Straight-line depreciation = ($500,000 - $50,000)/5 = $90,000

Sum-of-years-digits method of depreciation:

Sum-of-years-digits method = Depreciable base x (Left over useful life/ Sum-of-years-

digits)

Sum-of-years-digits = n (n + 1)/2

Sum-of-years-digits = 5 (5 + 1)/2

Sum-of-years-digits (SYD) = 15

Years Depreciable base Left over useful life SYD Applicable percent Yearly depreciation

1 $450,000 5 5/15 33.33% $150,000

2 $450,000 4 4/15 26.67% $120,000

3 $450,000 3 3/15 20.00% $90,000

4 $450,000 2 2/15 13.33% $60,000

5 $450,000 1 1/15 6.67% $30,000

Statement indicating changes in deprecation:

Years Straight-line depreciation Yearly depreciation (SYD) Difference

3. Role of Accountants in Depreciation Method Change

Relied on the information explained within the case study, Maria Mars has considered

altering the depreciation method to be used from being straight line method to sum-of-years

digits method (Bevis 2013). The major objective of employing the sun-of-years digits method is

to decrease the necessary profit level in the future two years in order to transfer the same to 2018

and 2019 in order to deal with the expected economic depression. This might be explained with

the support of the below mentioned illustration:

Asset cost = $500,000

Useful life = 5 years

Salvage value = $50,000

In addition, the comparison between profits through employing the two depreciation

methods is indicated in the below section:

Straight-line depreciation method:

Straight-line depreciation = (Cost of asset – Salvage value)/ Useful life

Straight-line depreciation = ($500,000 - $50,000)/5 = $90,000

Sum-of-years-digits method of depreciation:

Sum-of-years-digits method = Depreciable base x (Left over useful life/ Sum-of-years-

digits)

Sum-of-years-digits = n (n + 1)/2

Sum-of-years-digits = 5 (5 + 1)/2

Sum-of-years-digits (SYD) = 15

Years Depreciable base Left over useful life SYD Applicable percent Yearly depreciation

1 $450,000 5 5/15 33.33% $150,000

2 $450,000 4 4/15 26.67% $120,000

3 $450,000 3 3/15 20.00% $90,000

4 $450,000 2 2/15 13.33% $60,000

5 $450,000 1 1/15 6.67% $30,000

Statement indicating changes in deprecation:

Years Straight-line depreciation Yearly depreciation (SYD) Difference

5FINANCIAL ACCOUNTING

1 $90,000 $150,000 ($60,000)

2 $90,000 $120,000 ($30,000)

3 $90,000 $90,000 Nil

4 $90,000 $60,000 $30,000

5 $90,000 $30,000 $60,000

After altering the depreciation method, the necessary depreciation amount can increase in

the initial years. Moreover, it might result in decline in the future years. This might facilitate in

maintaining the profits to be constant over the future years because of the decrease on the

depreciation charges with the passage of years (Callen 2015). Therefore, Maria Mars has a major

role in altering the depreciation method from straight line method to sum-of-years digits

technique in addressing the objectives of Kam Sunshine that is the general manager of the

company.

4. Stakeholders

It is gathered from the Sunshine Ltd case study that a stakeholder is an individual,

company or a group that has interest or concern in other companies. In this case study, the major

shareholders those are recognised are explained under:

Government and Communities- Communities and the government are considered as

eternal shareholders for they are linked closely with Sunshine Ltd (Christensen, Cottrell

and Baker 2013). As companies has their operation within the community, their conducts

has an impact beyond consumers. The company experience taxes and in certain cases it is

the informal expectations of the residents to have business operation in an ethical manner

and sustain environmental sustainability. Moreover, the communities anticipate the

companies to be linked with events along with domestic charitable giving. The

government entities take certain decisions that might have an impact on Sunshine Limited

Company’s operations (Crawley and Wahlen 2014). For this reason, it is deemed to be

considerable for the business managers of the company in sustaining strong link with the

domestic officials for anticipating regulatory changes or community development

impacting the company’s operations.

Consumers- The consumers are observed as vital external shareholders and these are

required to be considered. In the retailer’s case, the consumers are deemed to be

customers. For this reason, retaining, drawing and generating loyalty from the major

consumers make sure of extended term financial progress of the company (Dutta and

Patatoukas 2016). Considering the business-to-business companies, the business

companies are the consumers those acquire goods for commercial purposes. The trade

resellers are associated in direct selling from retailers or wholesalers and in certain

scenario end consumers must be considered to be an aspect of the stakeholders. In a

scenario where the consumers do not acquire the manufactured goods for instance, the

distribution channel failure is inevitable.

1 $90,000 $150,000 ($60,000)

2 $90,000 $120,000 ($30,000)

3 $90,000 $90,000 Nil

4 $90,000 $60,000 $30,000

5 $90,000 $30,000 $60,000

After altering the depreciation method, the necessary depreciation amount can increase in

the initial years. Moreover, it might result in decline in the future years. This might facilitate in

maintaining the profits to be constant over the future years because of the decrease on the

depreciation charges with the passage of years (Callen 2015). Therefore, Maria Mars has a major

role in altering the depreciation method from straight line method to sum-of-years digits

technique in addressing the objectives of Kam Sunshine that is the general manager of the

company.

4. Stakeholders

It is gathered from the Sunshine Ltd case study that a stakeholder is an individual,

company or a group that has interest or concern in other companies. In this case study, the major

shareholders those are recognised are explained under:

Government and Communities- Communities and the government are considered as

eternal shareholders for they are linked closely with Sunshine Ltd (Christensen, Cottrell

and Baker 2013). As companies has their operation within the community, their conducts

has an impact beyond consumers. The company experience taxes and in certain cases it is

the informal expectations of the residents to have business operation in an ethical manner

and sustain environmental sustainability. Moreover, the communities anticipate the

companies to be linked with events along with domestic charitable giving. The

government entities take certain decisions that might have an impact on Sunshine Limited

Company’s operations (Crawley and Wahlen 2014). For this reason, it is deemed to be

considerable for the business managers of the company in sustaining strong link with the

domestic officials for anticipating regulatory changes or community development

impacting the company’s operations.

Consumers- The consumers are observed as vital external shareholders and these are

required to be considered. In the retailer’s case, the consumers are deemed to be

customers. For this reason, retaining, drawing and generating loyalty from the major

consumers make sure of extended term financial progress of the company (Dutta and

Patatoukas 2016). Considering the business-to-business companies, the business

companies are the consumers those acquire goods for commercial purposes. The trade

resellers are associated in direct selling from retailers or wholesalers and in certain

scenario end consumers must be considered to be an aspect of the stakeholders. In a

scenario where the consumers do not acquire the manufactured goods for instance, the

distribution channel failure is inevitable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

Suppliers and Partners- The business partners and suppliers are observed as major

shareholders within the recent competitive environment (Henderson et al. 2015). The

companies generally tend to maintain loyal relationship with the suppliers and the

associates. This might support Sunshine Ltd in maintaining common goals, shared vision

and strategies. The buyers and the trade sellers might efficiently collaborate in offering

maximum value to the end consumers that is beneficial to the partners. Moreover, the

trade partners are anticipated to have its operation in an ethical way for avoiding

hampering consumer reputation of the company related with Sunshine Ltd.

Accountant- As per the Sunshine Ltd case study, Maria Mars the accountant that

supported in developing the financial statements along with altering the profit from the

tear 2016 to 2017 along with 2018 to 2019.

Creditors- It is explained that the companies often employ lenders in order to fund their

purchases, business ventures, asset purchases as well as the supply purchases (Weil,

Schipper and Francis 2013). The banks are involved in offering loans for vital purchases

that includes new building. The suppliers can offer product inventory on account that is

paid by the company at some other time in future. The current creditors of Sunshine Ltd

might anticipate that the payment deadlines are addressed regularly along with

accordingly. In such scenario, the company might be able to enhance relationships with

its creditors that might increase the profitability of attaining effective funding in

upcoming years.

Shareholders- The individuals those invest in Sunshine Ltd for attaining advantages

through attaining a share of the business profit is recognised as the vital shareholders of

the company (May 2013).

General Manager- In alignment with the given case study, Kam Sunshine is recognised

to be Sunshine Ltd Company’s general manager. The individual is likely to undertake

certain decisions for enhancing total organizational performance (Van Mourik 2014).

5. AASB 116 Standard Effect

After the end of the period 30th June, 2015, Kam Sunshine has manipulated Maria Mars

in recognising a manner for decreasing the profits in the future two years that initiates from 2016

and continues. Hence, this might offer regular profits over the future two years in order to

address the interests of the shareholders. The accountant has altered the depreciation method fro

being the straight line method to sum-of-digits technique (Narayanaswamy 2014). Moreover,

Maria Mars has not disclosed any alterations made within the financial statements of the

company. AASB 116 that is an Australian Accounting Standards Board associated with plant,

property and equipment is a complied standard that is applicable to the annual reporting periods

that initiated on or after 1st July, 2009. This standard has an objective to stipulate the accounting

treatment associated with property, plant and equipment for providing necessary information to

the financial statement users in accordance with the company’s investment on certain assets

along with required advancements in that investment. Certain vital concerns associated with

accounting of plant, property and equipment are within the asset realization, the ascertainment of

the carrying amounts along with advancements within depreciation along with impairment losses

that is realised along with the same (McLaney and Atrill 2014).

Suppliers and Partners- The business partners and suppliers are observed as major

shareholders within the recent competitive environment (Henderson et al. 2015). The

companies generally tend to maintain loyal relationship with the suppliers and the

associates. This might support Sunshine Ltd in maintaining common goals, shared vision

and strategies. The buyers and the trade sellers might efficiently collaborate in offering

maximum value to the end consumers that is beneficial to the partners. Moreover, the

trade partners are anticipated to have its operation in an ethical way for avoiding

hampering consumer reputation of the company related with Sunshine Ltd.

Accountant- As per the Sunshine Ltd case study, Maria Mars the accountant that

supported in developing the financial statements along with altering the profit from the

tear 2016 to 2017 along with 2018 to 2019.

Creditors- It is explained that the companies often employ lenders in order to fund their

purchases, business ventures, asset purchases as well as the supply purchases (Weil,

Schipper and Francis 2013). The banks are involved in offering loans for vital purchases

that includes new building. The suppliers can offer product inventory on account that is

paid by the company at some other time in future. The current creditors of Sunshine Ltd

might anticipate that the payment deadlines are addressed regularly along with

accordingly. In such scenario, the company might be able to enhance relationships with

its creditors that might increase the profitability of attaining effective funding in

upcoming years.

Shareholders- The individuals those invest in Sunshine Ltd for attaining advantages

through attaining a share of the business profit is recognised as the vital shareholders of

the company (May 2013).

General Manager- In alignment with the given case study, Kam Sunshine is recognised

to be Sunshine Ltd Company’s general manager. The individual is likely to undertake

certain decisions for enhancing total organizational performance (Van Mourik 2014).

5. AASB 116 Standard Effect

After the end of the period 30th June, 2015, Kam Sunshine has manipulated Maria Mars

in recognising a manner for decreasing the profits in the future two years that initiates from 2016

and continues. Hence, this might offer regular profits over the future two years in order to

address the interests of the shareholders. The accountant has altered the depreciation method fro

being the straight line method to sum-of-digits technique (Narayanaswamy 2014). Moreover,

Maria Mars has not disclosed any alterations made within the financial statements of the

company. AASB 116 that is an Australian Accounting Standards Board associated with plant,

property and equipment is a complied standard that is applicable to the annual reporting periods

that initiated on or after 1st July, 2009. This standard has an objective to stipulate the accounting

treatment associated with property, plant and equipment for providing necessary information to

the financial statement users in accordance with the company’s investment on certain assets

along with required advancements in that investment. Certain vital concerns associated with

accounting of plant, property and equipment are within the asset realization, the ascertainment of

the carrying amounts along with advancements within depreciation along with impairment losses

that is realised along with the same (McLaney and Atrill 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

Within this case study, Maria Mars has advanced the method of depreciation from the

straight line method to the sum-of-years digits method. Such concept associated with

depreciation technique is segmenting the cost of tangible asset aver useful life of any good. It is

also gathered that the business firms are getting highly associated within depreciating fixed or

the non-current assets for attaining purposes of accounting and tax reasons. Accounting aspects

is deemed to have an effect on the prepared net income statement of the company and tax based

factors is observed to have an effect on the balance sheet statement of the company. Majorly,

certain cost is apportioned in the depreciation expense form in time duration where the asset is

anticipated to be used. The business companies realise their expenses for tax financial reporting

and tax factors (May 2013). The techniques of computing depreciation along with the years over

which certain assets are depreciated might diverge among the type of assets in the similar

business along with difference in tax purposes. The accounting standards along with laws can

specify the same as it varies in several countries. The techniques of calculating depreciation

expense are numerous that includes straight line method, decreasing balance along with sum-of-

years-digits methods. Certain emergence of depreciation expense is present at the time the assets

are utilised within the service.

It is also gathered that the sum-of-years-digits method serves as an accelerated process

for calculating the asset depreciation. The formula that is employed in calculating the value of

depreciation under this process is explained under:

SYD depreciation = Depreciable base x (Left over useful life/ Sum-of-years-digits

method)

This technique is developed in order to signify the consumption pattern of an important

asset. Moreover, it is also employed in the absence of any particular pattern in the process

where the asset must be used over the future years (May 2013). The straight line

depreciation technique charges uniform costs over the non-current assets useful life. Such

depreciation method is efficient within which the economic realisation from an asset is

deemed to be realised in a better manner over their useful lives.

Depreciation per year = (Cost – Residual value)/ Useful life

Sunshine Ltd is a huge departmental store along with having a group of members that

undertakes decisions developed on rules at the time of the company’s emergence. For this

reason, Kam Sunshine has not followed the organizational policy through undertaking

certain personal decisions that has direct effect on the company’s financial statement. In

addition, from the case study it is observed that certain advancements those were made in

the company is focussed in taking the final decision that is required to e disclosed to all

the stakeholders related with the company (May 2013). For this reason, it might be

elucidated that the conducts of Maria Mars was not in accordance with AASB 116.

6. Conclusion:

The objective was to ensure certain advancements within the company’s incoming profit

discretely. This has increased certain dilemma for the accountant for the reason that she is

focussed on her contract renewal in the company. From the above discussion, it could be stated

that the company has employed several depreciation techniques on the fixed assets in order to

Within this case study, Maria Mars has advanced the method of depreciation from the

straight line method to the sum-of-years digits method. Such concept associated with

depreciation technique is segmenting the cost of tangible asset aver useful life of any good. It is

also gathered that the business firms are getting highly associated within depreciating fixed or

the non-current assets for attaining purposes of accounting and tax reasons. Accounting aspects

is deemed to have an effect on the prepared net income statement of the company and tax based

factors is observed to have an effect on the balance sheet statement of the company. Majorly,

certain cost is apportioned in the depreciation expense form in time duration where the asset is

anticipated to be used. The business companies realise their expenses for tax financial reporting

and tax factors (May 2013). The techniques of computing depreciation along with the years over

which certain assets are depreciated might diverge among the type of assets in the similar

business along with difference in tax purposes. The accounting standards along with laws can

specify the same as it varies in several countries. The techniques of calculating depreciation

expense are numerous that includes straight line method, decreasing balance along with sum-of-

years-digits methods. Certain emergence of depreciation expense is present at the time the assets

are utilised within the service.

It is also gathered that the sum-of-years-digits method serves as an accelerated process

for calculating the asset depreciation. The formula that is employed in calculating the value of

depreciation under this process is explained under:

SYD depreciation = Depreciable base x (Left over useful life/ Sum-of-years-digits

method)

This technique is developed in order to signify the consumption pattern of an important

asset. Moreover, it is also employed in the absence of any particular pattern in the process

where the asset must be used over the future years (May 2013). The straight line

depreciation technique charges uniform costs over the non-current assets useful life. Such

depreciation method is efficient within which the economic realisation from an asset is

deemed to be realised in a better manner over their useful lives.

Depreciation per year = (Cost – Residual value)/ Useful life

Sunshine Ltd is a huge departmental store along with having a group of members that

undertakes decisions developed on rules at the time of the company’s emergence. For this

reason, Kam Sunshine has not followed the organizational policy through undertaking

certain personal decisions that has direct effect on the company’s financial statement. In

addition, from the case study it is observed that certain advancements those were made in

the company is focussed in taking the final decision that is required to e disclosed to all

the stakeholders related with the company (May 2013). For this reason, it might be

elucidated that the conducts of Maria Mars was not in accordance with AASB 116.

6. Conclusion:

The objective was to ensure certain advancements within the company’s incoming profit

discretely. This has increased certain dilemma for the accountant for the reason that she is

focussed on her contract renewal in the company. From the above discussion, it could be stated

that the company has employed several depreciation techniques on the fixed assets in order to

8FINANCIAL ACCOUNTING

indicate the devaluation effect along with depreciation method. This might indicate a situation

within which the future advantages associated with assets are anticipated to be caused. Maria has

altered the method of depreciation that has resulted in certain difference within the timing of the

overall depreciation.

indicate the devaluation effect along with depreciation method. This might indicate a situation

within which the future advantages associated with assets are anticipated to be caused. Maria has

altered the method of depreciation that has resulted in certain difference within the timing of the

overall depreciation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ACCOUNTING

References:

Aasb.gov.au., 2017. [online] Available at:

<http://www.aasb.gov.au/admin/file/content102/c3/AASB116_07-04_ERDRjun10_07-09.pdf>

[Accessed 24 Apr. 2017].

Bazley, M., Hancock, P., Fisher, C., Lovell, A., Berk, J., DeMarzo, P., Berk, J. and DeMarzo, P.,

2013. Financial Accounting: An Integrated. Thomson Pty Ltd, South Melbourne.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2), pp.339-383.

Bevis, H.W., 2013. Corporate Financial Accounting in a Competitive Economy (RLE

Accounting). Routledge.

Callen, J.L., 2015. A selective critical review of financial accounting research. Critical

Perspectives on Accounting, 26, pp.157-167.

Christensen, T., Cottrell, D. and Baker, R., 2013. Advanced Financial Accounting (No. 2013).

McGraw-Hill.

Crawley, M. and Wahlen, J., 2014. Analytics in empirical/archival financial accounting

research. Business Horizons, 57(5), pp.583-593.

Dutta, S. and Patatoukas, P.N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting) (Vol. 29). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C. and Maxfield, J.,

2014. Financial accounting.

May, G.O., 2013. Financial accounting. Read Books Ltd.

McLaney, E.J. and Atrill, P., 2014. Accounting and Finance: An Introduction. Pearson.

Narayanaswamy, R., 2014. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

Van Mourik, C., 2014. Fundamental issues in financial accounting and reporting theory.

Routledge.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

References:

Aasb.gov.au., 2017. [online] Available at:

<http://www.aasb.gov.au/admin/file/content102/c3/AASB116_07-04_ERDRjun10_07-09.pdf>

[Accessed 24 Apr. 2017].

Bazley, M., Hancock, P., Fisher, C., Lovell, A., Berk, J., DeMarzo, P., Berk, J. and DeMarzo, P.,

2013. Financial Accounting: An Integrated. Thomson Pty Ltd, South Melbourne.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2), pp.339-383.

Bevis, H.W., 2013. Corporate Financial Accounting in a Competitive Economy (RLE

Accounting). Routledge.

Callen, J.L., 2015. A selective critical review of financial accounting research. Critical

Perspectives on Accounting, 26, pp.157-167.

Christensen, T., Cottrell, D. and Baker, R., 2013. Advanced Financial Accounting (No. 2013).

McGraw-Hill.

Crawley, M. and Wahlen, J., 2014. Analytics in empirical/archival financial accounting

research. Business Horizons, 57(5), pp.583-593.

Dutta, S. and Patatoukas, P.N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting) (Vol. 29). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hoggett, J., Edwards, L., Medlin, J., Chalmers, K., Hellmann, A., Beattie, C. and Maxfield, J.,

2014. Financial accounting.

May, G.O., 2013. Financial accounting. Read Books Ltd.

McLaney, E.J. and Atrill, P., 2014. Accounting and Finance: An Introduction. Pearson.

Narayanaswamy, R., 2014. Financial accounting: a managerial perspective. PHI Learning Pvt.

Ltd.

Van Mourik, C., 2014. Fundamental issues in financial accounting and reporting theory.

Routledge.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.