Detailed Analysis of Impairment Loss Accounting Based on AASB 136

VerifiedAdded on 2019/10/30

|8

|1587

|198

Report

AI Summary

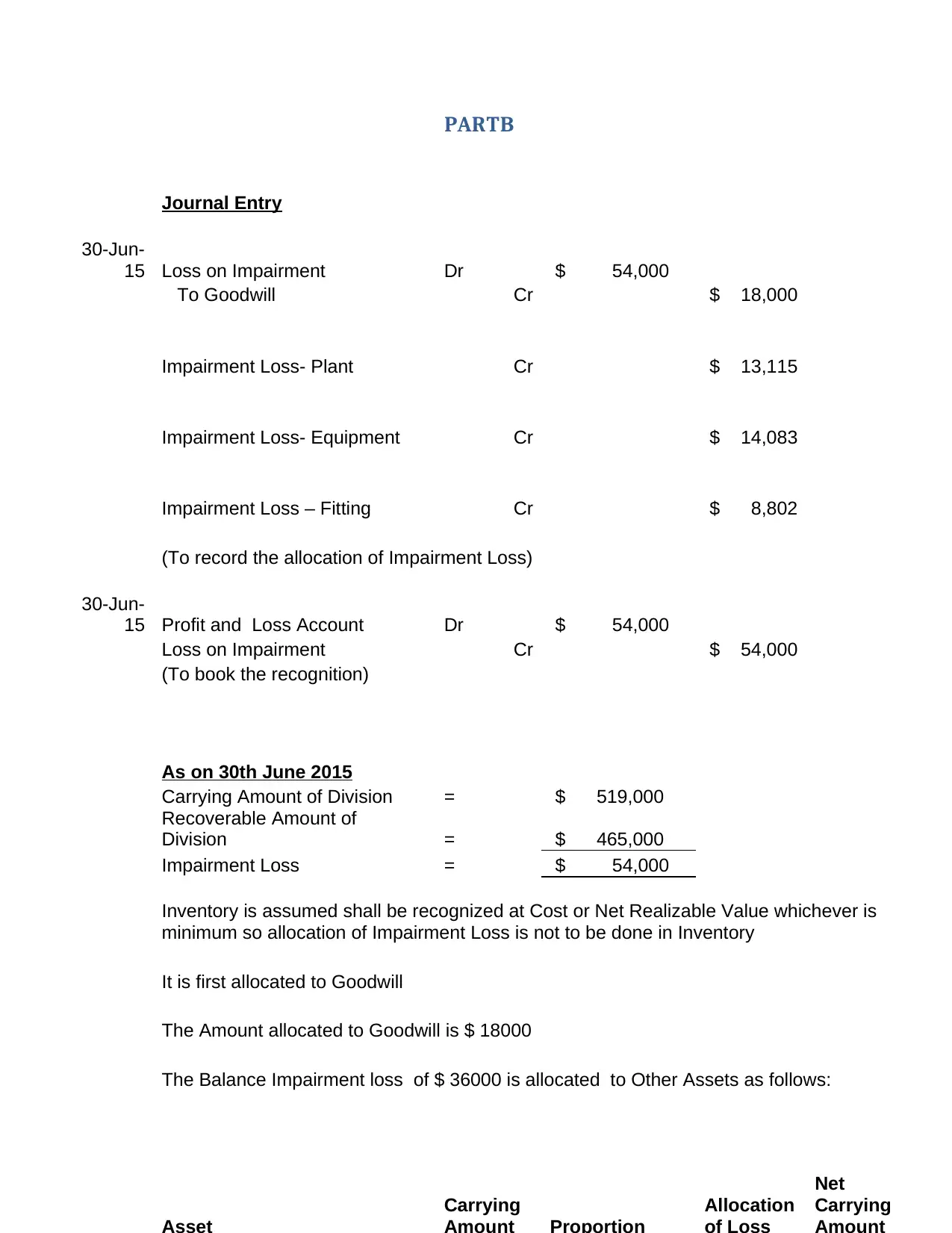

This report provides a comprehensive analysis of impairment loss accounting in accordance with AASB 136, the Australian Accounting Standard related to the impairment of assets. It defines key concepts such as carrying amount, recoverable amount, and fair value, explaining how to recognize and measure impairment losses for individual assets. The report outlines the procedures for calculating impairment loss, including the comparison of carrying amount with recoverable amount. It also covers the recognition of impairment loss in the profit and loss account and the adjustments required for revalued assets. Additionally, the report includes a practical example demonstrating the calculation of impairment loss and journal entries. The report also provides a detailed case study of a company's impairment loss allocation across different asset categories, including goodwill, plant, equipment, and fittings. It details the journal entries, and the allocation of impairment losses, and references relevant accounting standards and academic literature.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.