AASB 136 Impairment, Financial Ratio Analysis & Cash Flows

VerifiedAdded on 2023/06/13

|11

|2078

|128

Report

AI Summary

This assignment includes a letter to the CFO regarding AASB 136 and CGUs, financial ratio analysis for 2016 and 2017, a report summarizing Woolworths Limited's financial performance, an analysis of liquidity ratios, and a discussion on translating foreign currency financial statements. The assignment also presents a statement of cash flow for Flash in the Pan Ltd. for the year ended 30th June, 2019, including detailed workings for cash collected from sales, payments to suppliers, proceeds from the sale of assets, and payment of taxes. Desklib provides a range of solved assignments and study resources for students.

Solution-1

To,

The Chief Financial Officer,

The Wentnor Dairy Company Ltd.

Dear Sir,

Subject: Advice on application of AASB 136 to the company’s various activities

This letter is in reference to the application of AASB 136, “Impairment of assets” on the company’s

various activities. Let’s start with the definition of cash generating units.

A cash generating unit (or CGU) is a smallest identifiable group of assets, which generates cash inflows

and these cash inflows are largely independent from the cash inflows generated by other assets or other

cash generating units.

Para 66 of AASB 136, states that the impairment testing should be conducted on a single asset basis, but

if the recoverable amount for a single asset cannot be determined for the reason because the cash inflows

of that asset cannot be separately identified or are not independent from the cash inflows of other assets or

its value in use cannot be determined then the impairment testing should be conducted on a cash

generating units basis.

So, considering above, the impairment testing is conduct on a CGU basis, because the cash inflows

involved in the individual assets cannot be reliably estimated or calculated.

Further, for identifying the CGUs of the company, the following factors should be considered.

(a) Whether there is an identifiable group of assets whose cash flows are largely independent from

the cash flows of other assets

(b) Whether an active market exists for the assets being produced by above group of assets

irrespective of the fact that whether the produced products are used internally or externally.

Further, para 70 of AASB 136, states that (Aasb.gov.au, 2018)

“If an active market exists for the output produced by an asset or group of assets, that asset or group of

assets shall be identified as a cash-generating unit, even if some or all of the output is used internally.”

So, considering the above factors we can conclude that the milk production section is a separate CGU

since, the milk produce by the CGU can be sold externally means an active market exists for it and

further, the CGU’s cash inflows are independent of the cash inflows of other factories.

Hope it helps and have clarified the issues.

Thanks,

To,

The Chief Financial Officer,

The Wentnor Dairy Company Ltd.

Dear Sir,

Subject: Advice on application of AASB 136 to the company’s various activities

This letter is in reference to the application of AASB 136, “Impairment of assets” on the company’s

various activities. Let’s start with the definition of cash generating units.

A cash generating unit (or CGU) is a smallest identifiable group of assets, which generates cash inflows

and these cash inflows are largely independent from the cash inflows generated by other assets or other

cash generating units.

Para 66 of AASB 136, states that the impairment testing should be conducted on a single asset basis, but

if the recoverable amount for a single asset cannot be determined for the reason because the cash inflows

of that asset cannot be separately identified or are not independent from the cash inflows of other assets or

its value in use cannot be determined then the impairment testing should be conducted on a cash

generating units basis.

So, considering above, the impairment testing is conduct on a CGU basis, because the cash inflows

involved in the individual assets cannot be reliably estimated or calculated.

Further, for identifying the CGUs of the company, the following factors should be considered.

(a) Whether there is an identifiable group of assets whose cash flows are largely independent from

the cash flows of other assets

(b) Whether an active market exists for the assets being produced by above group of assets

irrespective of the fact that whether the produced products are used internally or externally.

Further, para 70 of AASB 136, states that (Aasb.gov.au, 2018)

“If an active market exists for the output produced by an asset or group of assets, that asset or group of

assets shall be identified as a cash-generating unit, even if some or all of the output is used internally.”

So, considering the above factors we can conclude that the milk production section is a separate CGU

since, the milk produce by the CGU can be sold externally means an active market exists for it and

further, the CGU’s cash inflows are independent of the cash inflows of other factories.

Hope it helps and have clarified the issues.

Thanks,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With Regards,

XYZ

XYZ

Solution-2

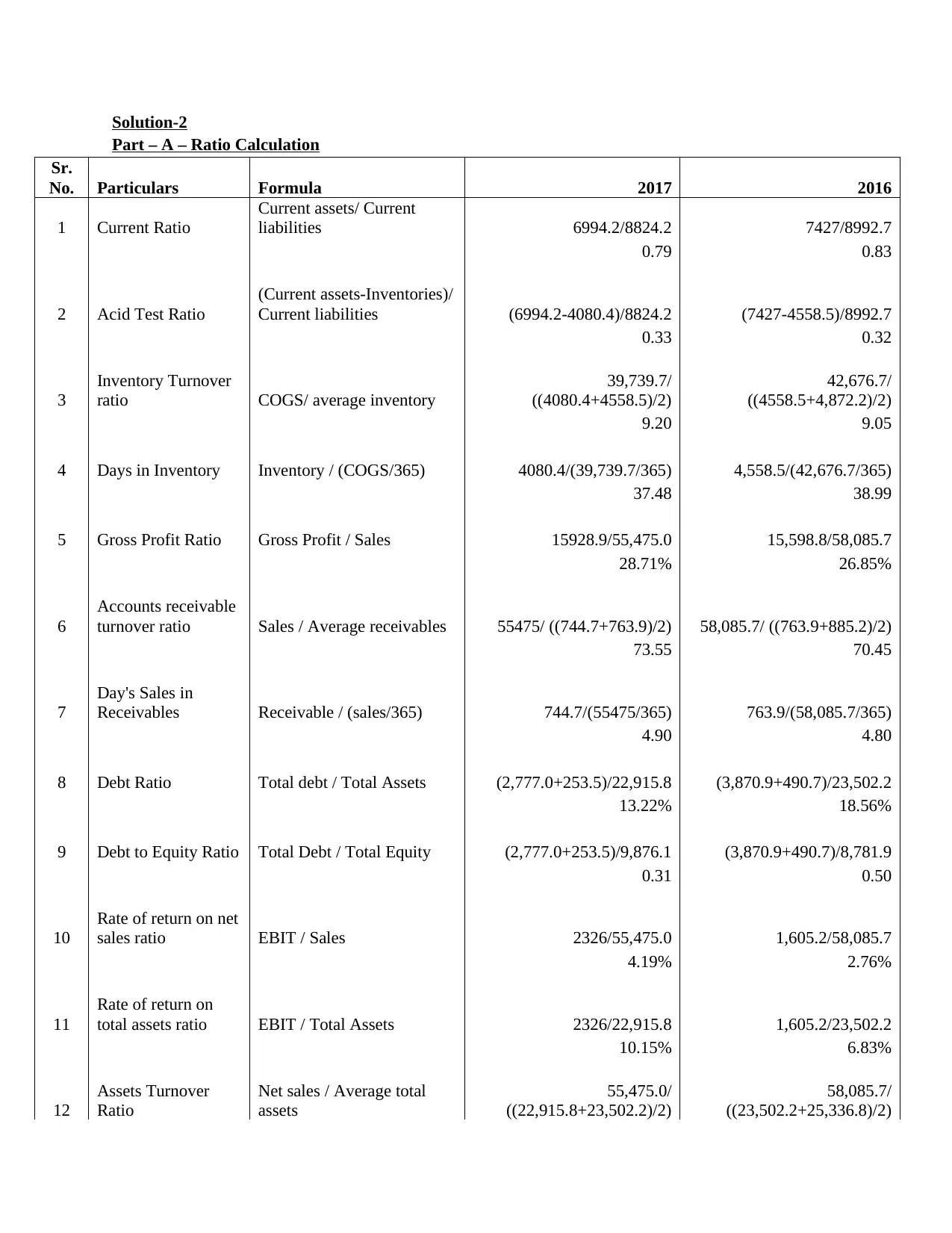

Part – A – Ratio Calculation

Sr.

No. Particulars Formula 2017 2016

1 Current Ratio

Current assets/ Current

liabilities 6994.2/8824.2 7427/8992.7

0.79 0.83

2 Acid Test Ratio

(Current assets-Inventories)/

Current liabilities (6994.2-4080.4)/8824.2 (7427-4558.5)/8992.7

0.33 0.32

3

Inventory Turnover

ratio COGS/ average inventory

39,739.7/

((4080.4+4558.5)/2)

42,676.7/

((4558.5+4,872.2)/2)

9.20 9.05

4 Days in Inventory Inventory / (COGS/365) 4080.4/(39,739.7/365) 4,558.5/(42,676.7/365)

37.48 38.99

5 Gross Profit Ratio Gross Profit / Sales 15928.9/55,475.0 15,598.8/58,085.7

28.71% 26.85%

6

Accounts receivable

turnover ratio Sales / Average receivables 55475/ ((744.7+763.9)/2) 58,085.7/ ((763.9+885.2)/2)

73.55 70.45

7

Day's Sales in

Receivables Receivable / (sales/365) 744.7/(55475/365) 763.9/(58,085.7/365)

4.90 4.80

8 Debt Ratio Total debt / Total Assets (2,777.0+253.5)/22,915.8 (3,870.9+490.7)/23,502.2

13.22% 18.56%

9 Debt to Equity Ratio Total Debt / Total Equity (2,777.0+253.5)/9,876.1 (3,870.9+490.7)/8,781.9

0.31 0.50

10

Rate of return on net

sales ratio EBIT / Sales 2326/55,475.0 1,605.2/58,085.7

4.19% 2.76%

11

Rate of return on

total assets ratio EBIT / Total Assets 2326/22,915.8 1,605.2/23,502.2

10.15% 6.83%

12

Assets Turnover

Ratio

Net sales / Average total

assets

55,475.0/

((22,915.8+23,502.2)/2)

58,085.7/

((23,502.2+25,336.8)/2)

Part – A – Ratio Calculation

Sr.

No. Particulars Formula 2017 2016

1 Current Ratio

Current assets/ Current

liabilities 6994.2/8824.2 7427/8992.7

0.79 0.83

2 Acid Test Ratio

(Current assets-Inventories)/

Current liabilities (6994.2-4080.4)/8824.2 (7427-4558.5)/8992.7

0.33 0.32

3

Inventory Turnover

ratio COGS/ average inventory

39,739.7/

((4080.4+4558.5)/2)

42,676.7/

((4558.5+4,872.2)/2)

9.20 9.05

4 Days in Inventory Inventory / (COGS/365) 4080.4/(39,739.7/365) 4,558.5/(42,676.7/365)

37.48 38.99

5 Gross Profit Ratio Gross Profit / Sales 15928.9/55,475.0 15,598.8/58,085.7

28.71% 26.85%

6

Accounts receivable

turnover ratio Sales / Average receivables 55475/ ((744.7+763.9)/2) 58,085.7/ ((763.9+885.2)/2)

73.55 70.45

7

Day's Sales in

Receivables Receivable / (sales/365) 744.7/(55475/365) 763.9/(58,085.7/365)

4.90 4.80

8 Debt Ratio Total debt / Total Assets (2,777.0+253.5)/22,915.8 (3,870.9+490.7)/23,502.2

13.22% 18.56%

9 Debt to Equity Ratio Total Debt / Total Equity (2,777.0+253.5)/9,876.1 (3,870.9+490.7)/8,781.9

0.31 0.50

10

Rate of return on net

sales ratio EBIT / Sales 2326/55,475.0 1,605.2/58,085.7

4.19% 2.76%

11

Rate of return on

total assets ratio EBIT / Total Assets 2326/22,915.8 1,605.2/23,502.2

10.15% 6.83%

12

Assets Turnover

Ratio

Net sales / Average total

assets

55,475.0/

((22,915.8+23,502.2)/2)

58,085.7/

((23,502.2+25,336.8)/2)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

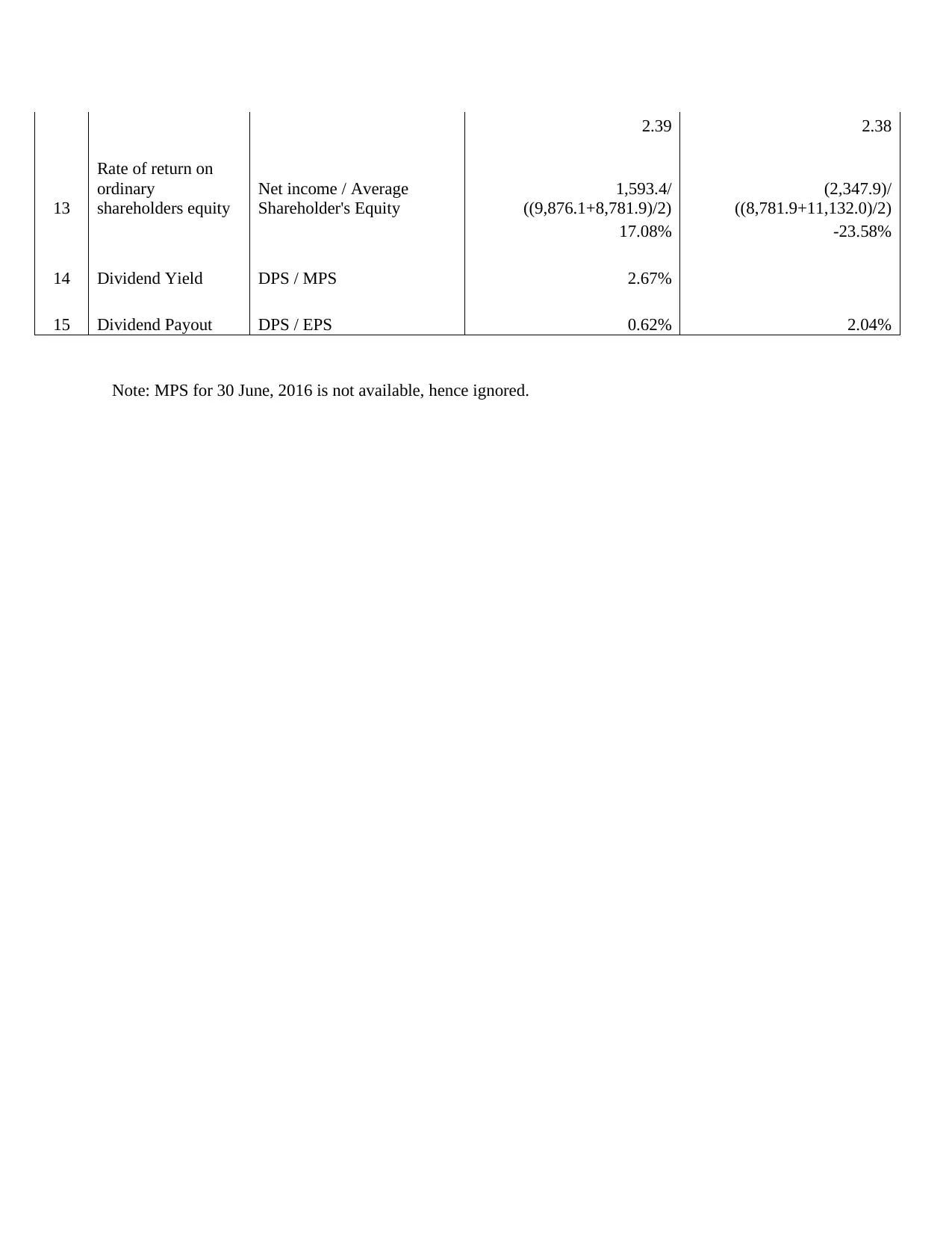

2.39 2.38

13

Rate of return on

ordinary

shareholders equity

Net income / Average

Shareholder's Equity

1,593.4/

((9,876.1+8,781.9)/2)

(2,347.9)/

((8,781.9+11,132.0)/2)

17.08% -23.58%

14 Dividend Yield DPS / MPS 2.67%

15 Dividend Payout DPS / EPS 0.62% 2.04%

Note: MPS for 30 June, 2016 is not available, hence ignored.

13

Rate of return on

ordinary

shareholders equity

Net income / Average

Shareholder's Equity

1,593.4/

((9,876.1+8,781.9)/2)

(2,347.9)/

((8,781.9+11,132.0)/2)

17.08% -23.58%

14 Dividend Yield DPS / MPS 2.67%

15 Dividend Payout DPS / EPS 0.62% 2.04%

Note: MPS for 30 June, 2016 is not available, hence ignored.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part – B – Report

Report

EXECUTIVE SUMMARY

The purpose of this report is to provide insight of the financial performance of Woolworths Limited to its

potential investors. This report summarizes the financial performance of the company on the basis of

financial ratios calculated for the year 2017.

INTRODUCTION

In this report, we are going to discuss the various ratios and to find whether the company is a good

investment option or not. The ratios are important aspects of the financial reporting which summarizes

and provide the birds eye view to the reader of the financial statements. In this report we are going to

discuss these ratios.

FINDINGS

On the basis of ratios attached in the appendix, we have noticed the following:

(a) The company is growing at a good pace which is reflected from its gross profit ratio which has

been increased from 26.85% to 28.71%. Gross profit ratio shows the percentage of profit earned

by the company from its sales less cost of sales.

(b) The company’s return on net sales ratio reflects that for every sale of $1 the company is earning

$0.0419, which is considered to be an healthy situation.

(c) The company is providing a return of 17.08% to its investors, meaning thereby by investing $1,

an investor can earn $0.178 from it, which is again a very good number.

Report

EXECUTIVE SUMMARY

The purpose of this report is to provide insight of the financial performance of Woolworths Limited to its

potential investors. This report summarizes the financial performance of the company on the basis of

financial ratios calculated for the year 2017.

INTRODUCTION

In this report, we are going to discuss the various ratios and to find whether the company is a good

investment option or not. The ratios are important aspects of the financial reporting which summarizes

and provide the birds eye view to the reader of the financial statements. In this report we are going to

discuss these ratios.

FINDINGS

On the basis of ratios attached in the appendix, we have noticed the following:

(a) The company is growing at a good pace which is reflected from its gross profit ratio which has

been increased from 26.85% to 28.71%. Gross profit ratio shows the percentage of profit earned

by the company from its sales less cost of sales.

(b) The company’s return on net sales ratio reflects that for every sale of $1 the company is earning

$0.0419, which is considered to be an healthy situation.

(c) The company is providing a return of 17.08% to its investors, meaning thereby by investing $1,

an investor can earn $0.178 from it, which is again a very good number.

(d) Further, the company is in growing stage as most of its ratios are favorable from the earlier year

ended on 30 June, 2016, as in the last year, the company was having a net loss of $2,347 mn

whereas in the current year, the company has managed to make a profit of $1593.4. It shows that

the company is on a good path.

(e) The company is also providing dividends to its shareholders, the dividend payout ratio has been

0.62% in current year whereas the dividend yield is 2.67% which shows that company is

providing 2.67% of market price of share as dividend.

CONCLUSION

So, all the above factors indicate that the company is a good investment opportunity for potential

investors and the investors should invest to earn a good return on their money.

ended on 30 June, 2016, as in the last year, the company was having a net loss of $2,347 mn

whereas in the current year, the company has managed to make a profit of $1593.4. It shows that

the company is on a good path.

(e) The company is also providing dividends to its shareholders, the dividend payout ratio has been

0.62% in current year whereas the dividend yield is 2.67% which shows that company is

providing 2.67% of market price of share as dividend.

CONCLUSION

So, all the above factors indicate that the company is a good investment opportunity for potential

investors and the investors should invest to earn a good return on their money.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part – C

Current ratio is current assets divided by current liabilities, current ratio is a liquidity ratio which shows

the ability of the company to payoff its current liabilities from its current assets. It is the most important

ratio, as liquidity is the vital element for any business. The ideal current ratio is 2:1 which means that an

ideal company should have its current assets as twice of its current liabilities. The Woolsworth Limited is

having a current ratio of 0.79:1 in current year and 0.83:1 in previous year, which is not a good sign for

the company. It shows that for every $1 of current liabilities the company is having only $0.79 to pay off.

In short run it can prove dangerous for the company as company can face liquidity crunches.

Similarly, the quick ratio or acid test ratio is also a liquidity ratio which shows the ability of company to

pay off its current liabilities for its current assets excluding inventory. It is calculated by dividing current

assets less inventories to its current liabilities. The ideal acid test ratio is 1.5:1 which means the

company’s current assets less inventories should be 1.5 times of its current liabilities. The Woolsworth

Limited is having an acid test ratio of 0.33:1 in current year and 0.32:1 in previous year, which is very

below from industry standards. This is also a negative symbol for the company and shows the inefficiency

of liquidity measures within the company.

So, to conclude, the company lacks on the part of liquidity, so the management should emphasis on

increasing its current assets over its current liabilities so that the company does not face liquidity issues in

the future.

Current ratio is current assets divided by current liabilities, current ratio is a liquidity ratio which shows

the ability of the company to payoff its current liabilities from its current assets. It is the most important

ratio, as liquidity is the vital element for any business. The ideal current ratio is 2:1 which means that an

ideal company should have its current assets as twice of its current liabilities. The Woolsworth Limited is

having a current ratio of 0.79:1 in current year and 0.83:1 in previous year, which is not a good sign for

the company. It shows that for every $1 of current liabilities the company is having only $0.79 to pay off.

In short run it can prove dangerous for the company as company can face liquidity crunches.

Similarly, the quick ratio or acid test ratio is also a liquidity ratio which shows the ability of company to

pay off its current liabilities for its current assets excluding inventory. It is calculated by dividing current

assets less inventories to its current liabilities. The ideal acid test ratio is 1.5:1 which means the

company’s current assets less inventories should be 1.5 times of its current liabilities. The Woolsworth

Limited is having an acid test ratio of 0.33:1 in current year and 0.32:1 in previous year, which is very

below from industry standards. This is also a negative symbol for the company and shows the inefficiency

of liquidity measures within the company.

So, to conclude, the company lacks on the part of liquidity, so the management should emphasis on

increasing its current assets over its current liabilities so that the company does not face liquidity issues in

the future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution-3

The stated note deals with the situation when any entity is acquired whose functional currency is different

from ours functional currency. In such a scenario, to prepare the financial statements or to record the

above transaction in our books, we need to translate the amount involved into our functional currency.

For this translation into our functional currency i.e. Australian dollars, the exchange rate as on the date of

reporting of financials is considered. Similarly, to record the income and expenses of above acquired

entity the exchange rates on the date of transactions are considered.

The resultant exchange difference arising due to above conversion is reported in the statement of

comprehensive income under the heading foreign exchange differences. These differences arise because

of fluctuation in the exchange rates over the time span. For example, the company acquired a subsidiary

in the FY 2016-17 for 10,000 USD when the USD was trading at 60 and Australian dollar was trading at

50. At the reporting date, i.e. on 30 June, 2017, the USD was at 62 and Australian dollar was at 49. Now,

due to this change, the company has incurred a loss, this loss is known as exchange difference and is

reported as stated above.

The stated note deals with the situation when any entity is acquired whose functional currency is different

from ours functional currency. In such a scenario, to prepare the financial statements or to record the

above transaction in our books, we need to translate the amount involved into our functional currency.

For this translation into our functional currency i.e. Australian dollars, the exchange rate as on the date of

reporting of financials is considered. Similarly, to record the income and expenses of above acquired

entity the exchange rates on the date of transactions are considered.

The resultant exchange difference arising due to above conversion is reported in the statement of

comprehensive income under the heading foreign exchange differences. These differences arise because

of fluctuation in the exchange rates over the time span. For example, the company acquired a subsidiary

in the FY 2016-17 for 10,000 USD when the USD was trading at 60 and Australian dollar was trading at

50. At the reporting date, i.e. on 30 June, 2017, the USD was at 62 and Australian dollar was at 49. Now,

due to this change, the company has incurred a loss, this loss is known as exchange difference and is

reported as stated above.

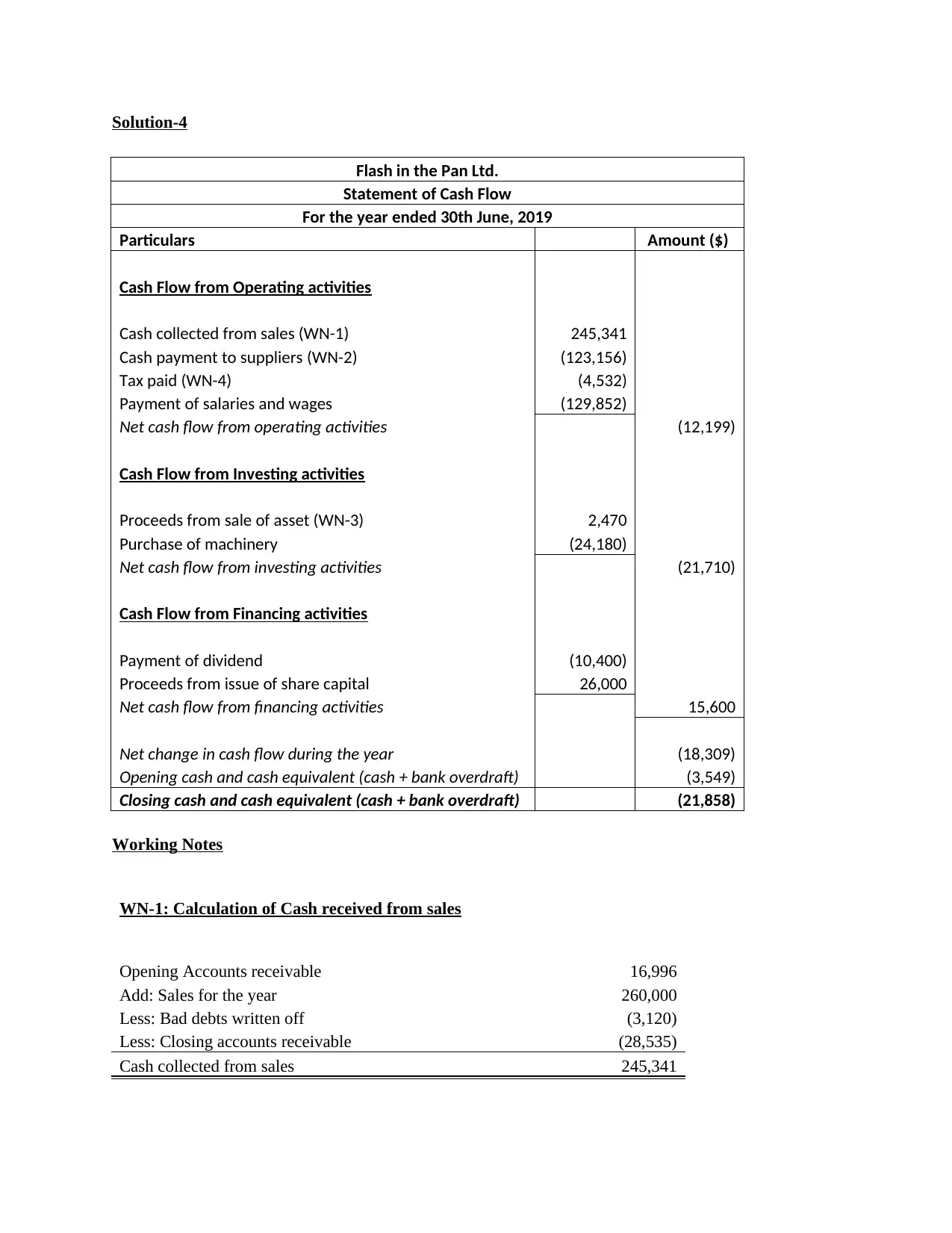

Solution-4

Flash in the Pan Ltd.

Statement of Cash Flow

For the year ended 30th June, 2019

Particulars Amount ($)

Cash Flow from Operating activities

Cash collected from sales (WN-1) 245,341

Cash payment to suppliers (WN-2) (123,156)

Tax paid (WN-4) (4,532)

Payment of salaries and wages (129,852)

Net cash flow from operating activities (12,199)

Cash Flow from Investing activities

Proceeds from sale of asset (WN-3) 2,470

Purchase of machinery (24,180)

Net cash flow from investing activities (21,710)

Cash Flow from Financing activities

Payment of dividend (10,400)

Proceeds from issue of share capital 26,000

Net cash flow from financing activities 15,600

Net change in cash flow during the year (18,309)

Opening cash and cash equivalent (cash + bank overdraft) (3,549)

Closing cash and cash equivalent (cash + bank overdraft) (21,858)

Working Notes

WN-1: Calculation of Cash received from sales

Opening Accounts receivable 16,996

Add: Sales for the year 260,000

Less: Bad debts written off (3,120)

Less: Closing accounts receivable (28,535)

Cash collected from sales 245,341

Flash in the Pan Ltd.

Statement of Cash Flow

For the year ended 30th June, 2019

Particulars Amount ($)

Cash Flow from Operating activities

Cash collected from sales (WN-1) 245,341

Cash payment to suppliers (WN-2) (123,156)

Tax paid (WN-4) (4,532)

Payment of salaries and wages (129,852)

Net cash flow from operating activities (12,199)

Cash Flow from Investing activities

Proceeds from sale of asset (WN-3) 2,470

Purchase of machinery (24,180)

Net cash flow from investing activities (21,710)

Cash Flow from Financing activities

Payment of dividend (10,400)

Proceeds from issue of share capital 26,000

Net cash flow from financing activities 15,600

Net change in cash flow during the year (18,309)

Opening cash and cash equivalent (cash + bank overdraft) (3,549)

Closing cash and cash equivalent (cash + bank overdraft) (21,858)

Working Notes

WN-1: Calculation of Cash received from sales

Opening Accounts receivable 16,996

Add: Sales for the year 260,000

Less: Bad debts written off (3,120)

Less: Closing accounts receivable (28,535)

Cash collected from sales 245,341

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

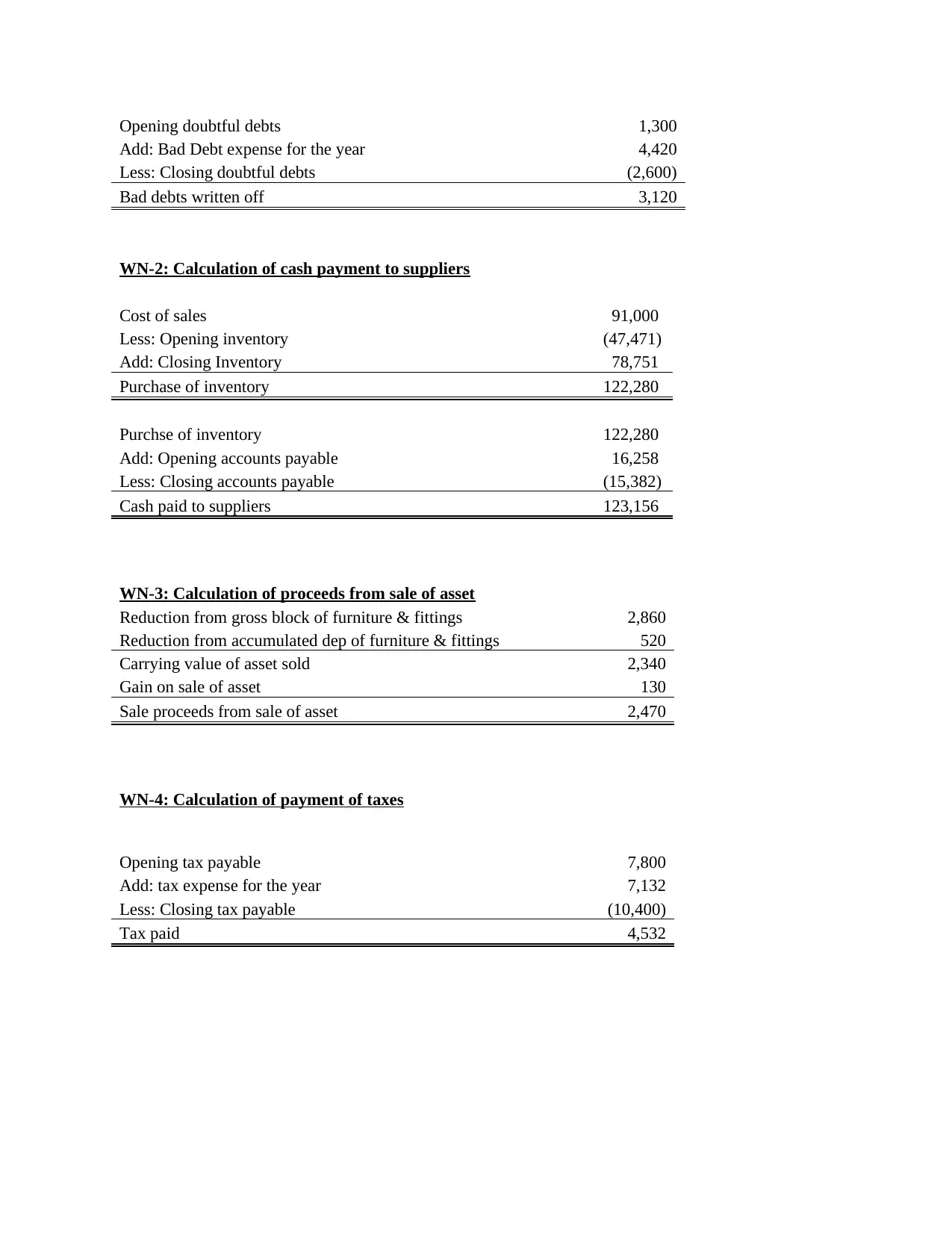

Opening doubtful debts 1,300

Add: Bad Debt expense for the year 4,420

Less: Closing doubtful debts (2,600)

Bad debts written off 3,120

WN-2: Calculation of cash payment to suppliers

Cost of sales 91,000

Less: Opening inventory (47,471)

Add: Closing Inventory 78,751

Purchase of inventory 122,280

Purchse of inventory 122,280

Add: Opening accounts payable 16,258

Less: Closing accounts payable (15,382)

Cash paid to suppliers 123,156

WN-3: Calculation of proceeds from sale of asset

Reduction from gross block of furniture & fittings 2,860

Reduction from accumulated dep of furniture & fittings 520

Carrying value of asset sold 2,340

Gain on sale of asset 130

Sale proceeds from sale of asset 2,470

WN-4: Calculation of payment of taxes

Opening tax payable 7,800

Add: tax expense for the year 7,132

Less: Closing tax payable (10,400)

Tax paid 4,532

Add: Bad Debt expense for the year 4,420

Less: Closing doubtful debts (2,600)

Bad debts written off 3,120

WN-2: Calculation of cash payment to suppliers

Cost of sales 91,000

Less: Opening inventory (47,471)

Add: Closing Inventory 78,751

Purchase of inventory 122,280

Purchse of inventory 122,280

Add: Opening accounts payable 16,258

Less: Closing accounts payable (15,382)

Cash paid to suppliers 123,156

WN-3: Calculation of proceeds from sale of asset

Reduction from gross block of furniture & fittings 2,860

Reduction from accumulated dep of furniture & fittings 520

Carrying value of asset sold 2,340

Gain on sale of asset 130

Sale proceeds from sale of asset 2,470

WN-4: Calculation of payment of taxes

Opening tax payable 7,800

Add: tax expense for the year 7,132

Less: Closing tax payable (10,400)

Tax paid 4,532

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References:

Aasb.gov.au. (2018). Impairment of Assets. [online] Available at:

http://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

[Accessed 26 Apr. 2018].

Aasb.gov.au. (2018). Impairment of Assets. [online] Available at:

http://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

[Accessed 26 Apr. 2018].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.