Financial Accounting (ACC701): AASB 138 Report - KOI - T119

VerifiedAdded on 2023/03/20

|13

|2731

|29

Report

AI Summary

This report meticulously examines the application of AASB 138, focusing on the accounting treatment of intangible assets within the context of Technology Enterprises Ltd. It begins with an introduction to the standard, emphasizing its role in ensuring accurate financial reporting. The report then addresses key questions regarding the recognition of intangible assets, differentiating between research and development phases, and determining the appropriate cost. A detailed analysis of the case study reveals the correct accounting for internally generated intangible assets, including the capitalization of specific costs and the exclusion of others, in alignment with AASB 138 provisions. Furthermore, it compares and contrasts AASB 138 and IAS 38, highlighting their similarities and the importance of management judgment. The report also analyzes the CEO's perspective on market hypotheses and provides recommendations to address investor concerns. Finally, it concludes by summarizing the significance of AASB 138 in fostering transparency and ensuring the true and fair value of assets.

AASB-138

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...........................................................................................................................................1

Answer to question no- 1.......................................................................................................................1

Answer to question no-2........................................................................................................................5

Answer to question no- 3.......................................................................................................................6

Response to CEO in relation to market hypothesis set by AASB 138...............................................6

Recommendations to meet the concerns about investor interpretation..............................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

Introduction...........................................................................................................................................1

Answer to question no- 1.......................................................................................................................1

Answer to question no-2........................................................................................................................5

Answer to question no- 3.......................................................................................................................6

Response to CEO in relation to market hypothesis set by AASB 138...............................................6

Recommendations to meet the concerns about investor interpretation..............................................8

Conclusion.............................................................................................................................................8

References...........................................................................................................................................10

Introduction

This report reveal the compliance of the AASB 138 for recording of the intangible

assets in the books of account. To establish an alignment between the domestic reporting

frameworks and the international reporting frameworks in the rapidly changing economic

environment, it is necessary for every organisation to comply with the required laws and

accounting standards. In this report we will discuss the provisions of AASB 138 and their

role in depicting the true and fair value of recorded assets and liabilities in the books of

accounts and in showing the ability of company. For making the key understanding regarding

the subject a case study of Technology Enterprises Ltd has been considered. The case consist

the queries regarding the internally generated intangible assets and its cost. The report

demonstrates the significant features of AASB 138 and the legal obligations in the company’s

accounting and recording framework.

Answer to question no- 1

RECOGNITION AS INTANGIBLE ASSET OR NOT

For proper treatment of accounts of Technology Enterprises Ltd. For intangible assets it is

required to ascertain the fact that whether the generated assets of the company falls into the

category of intangible assets or not. The provisions of AASB 138 (equivalent to the

requirements of IAS 38) are needed to be examine and check out, which are given below:

Relevant

paragraph of

AASB 138

Requirement set by the paragraph

Paragraph 9 The intangible asset is defined by this paragraph. According to the

definition an intangible asset involves the maintenance, acquisition,

enhancement or development of scientific or technological

knowledge in the category of items specifically considered as

intangible asset (Denicolai, Cotta Ramusino, & Sotti, 2015).

This report reveal the compliance of the AASB 138 for recording of the intangible

assets in the books of account. To establish an alignment between the domestic reporting

frameworks and the international reporting frameworks in the rapidly changing economic

environment, it is necessary for every organisation to comply with the required laws and

accounting standards. In this report we will discuss the provisions of AASB 138 and their

role in depicting the true and fair value of recorded assets and liabilities in the books of

accounts and in showing the ability of company. For making the key understanding regarding

the subject a case study of Technology Enterprises Ltd has been considered. The case consist

the queries regarding the internally generated intangible assets and its cost. The report

demonstrates the significant features of AASB 138 and the legal obligations in the company’s

accounting and recording framework.

Answer to question no- 1

RECOGNITION AS INTANGIBLE ASSET OR NOT

For proper treatment of accounts of Technology Enterprises Ltd. For intangible assets it is

required to ascertain the fact that whether the generated assets of the company falls into the

category of intangible assets or not. The provisions of AASB 138 (equivalent to the

requirements of IAS 38) are needed to be examine and check out, which are given below:

Relevant

paragraph of

AASB 138

Requirement set by the paragraph

Paragraph 9 The intangible asset is defined by this paragraph. According to the

definition an intangible asset involves the maintenance, acquisition,

enhancement or development of scientific or technological

knowledge in the category of items specifically considered as

intangible asset (Denicolai, Cotta Ramusino, & Sotti, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paragraph 18 In the paragraph the requirements to fulfil the recognition criteria

for the asset in financial statements to be approved by the definition

of intangible assets

Paragraph 21 An asset is to be met with the following conditions of recognition

criteria:

The intangible asset has the cost which can be measured by the

organisation with the reliability and

Entity has certain profitability of “expected future economic

benefits” due to the intangible asset.

Paragraph 22 The management uses the reasonable and supportable judgements

to determine the profitability of “expected future economic

benefits”. It is taken by the best estimation of upcoming economic

conditions.

Paragraph 23 The management judgements are used to ascertain the above

discussed profitability by giving favourable weight to external

evidence.

In the case of Technology Enterprises Ltd, in June, 2018 they have a new project which is

related to method of recharging batteries. The expectations of company are for next 10 years

regarding the economic benefits from such technology. The incurred cost in the establishment

of technology has also been disclosed by the company. With the help of best judgement of

management the profitability of “expected future economic benefits” can be determined.

The project established under the organisation based on the technological and scientific

knowledge which makes it eligible to be an intangible asset as per the definition defined

under paragraph 9. Also the asset can be identified as an intangible asset because as per the

conditions of recognition criteria mentioned under paragraph 18 and 21, this is an Internally

Generated Intangible Asset.

for the asset in financial statements to be approved by the definition

of intangible assets

Paragraph 21 An asset is to be met with the following conditions of recognition

criteria:

The intangible asset has the cost which can be measured by the

organisation with the reliability and

Entity has certain profitability of “expected future economic

benefits” due to the intangible asset.

Paragraph 22 The management uses the reasonable and supportable judgements

to determine the profitability of “expected future economic

benefits”. It is taken by the best estimation of upcoming economic

conditions.

Paragraph 23 The management judgements are used to ascertain the above

discussed profitability by giving favourable weight to external

evidence.

In the case of Technology Enterprises Ltd, in June, 2018 they have a new project which is

related to method of recharging batteries. The expectations of company are for next 10 years

regarding the economic benefits from such technology. The incurred cost in the establishment

of technology has also been disclosed by the company. With the help of best judgement of

management the profitability of “expected future economic benefits” can be determined.

The project established under the organisation based on the technological and scientific

knowledge which makes it eligible to be an intangible asset as per the definition defined

under paragraph 9. Also the asset can be identified as an intangible asset because as per the

conditions of recognition criteria mentioned under paragraph 18 and 21, this is an Internally

Generated Intangible Asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

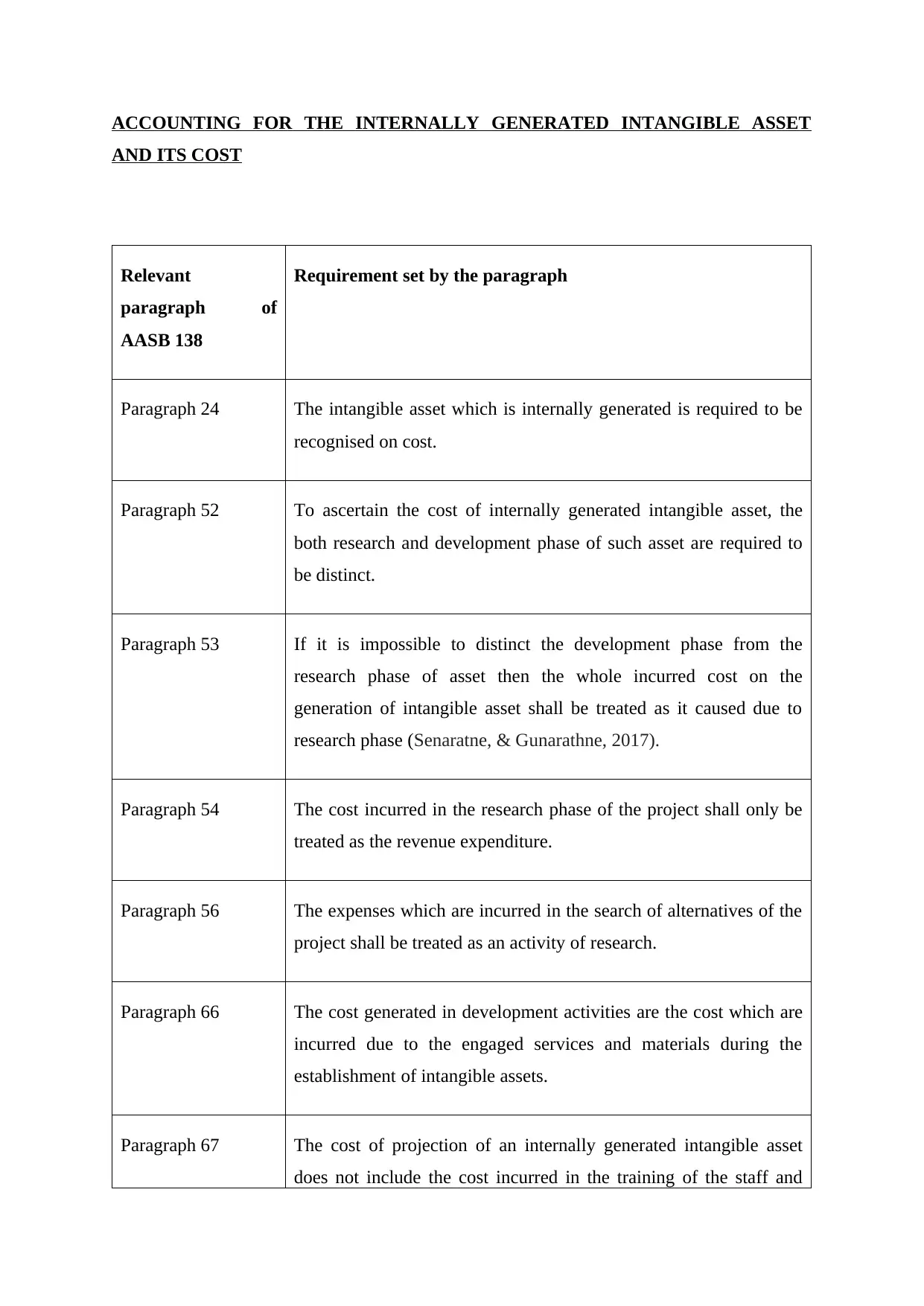

ACCOUNTING FOR THE INTERNALLY GENERATED INTANGIBLE ASSET

AND ITS COST

Relevant

paragraph of

AASB 138

Requirement set by the paragraph

Paragraph 24 The intangible asset which is internally generated is required to be

recognised on cost.

Paragraph 52 To ascertain the cost of internally generated intangible asset, the

both research and development phase of such asset are required to

be distinct.

Paragraph 53 If it is impossible to distinct the development phase from the

research phase of asset then the whole incurred cost on the

generation of intangible asset shall be treated as it caused due to

research phase (Senaratne, & Gunarathne, 2017).

Paragraph 54 The cost incurred in the research phase of the project shall only be

treated as the revenue expenditure.

Paragraph 56 The expenses which are incurred in the search of alternatives of the

project shall be treated as an activity of research.

Paragraph 66 The cost generated in development activities are the cost which are

incurred due to the engaged services and materials during the

establishment of intangible assets.

Paragraph 67 The cost of projection of an internally generated intangible asset

does not include the cost incurred in the training of the staff and

AND ITS COST

Relevant

paragraph of

AASB 138

Requirement set by the paragraph

Paragraph 24 The intangible asset which is internally generated is required to be

recognised on cost.

Paragraph 52 To ascertain the cost of internally generated intangible asset, the

both research and development phase of such asset are required to

be distinct.

Paragraph 53 If it is impossible to distinct the development phase from the

research phase of asset then the whole incurred cost on the

generation of intangible asset shall be treated as it caused due to

research phase (Senaratne, & Gunarathne, 2017).

Paragraph 54 The cost incurred in the research phase of the project shall only be

treated as the revenue expenditure.

Paragraph 56 The expenses which are incurred in the search of alternatives of the

project shall be treated as an activity of research.

Paragraph 66 The cost generated in development activities are the cost which are

incurred due to the engaged services and materials during the

establishment of intangible assets.

Paragraph 67 The cost of projection of an internally generated intangible asset

does not include the cost incurred in the training of the staff and

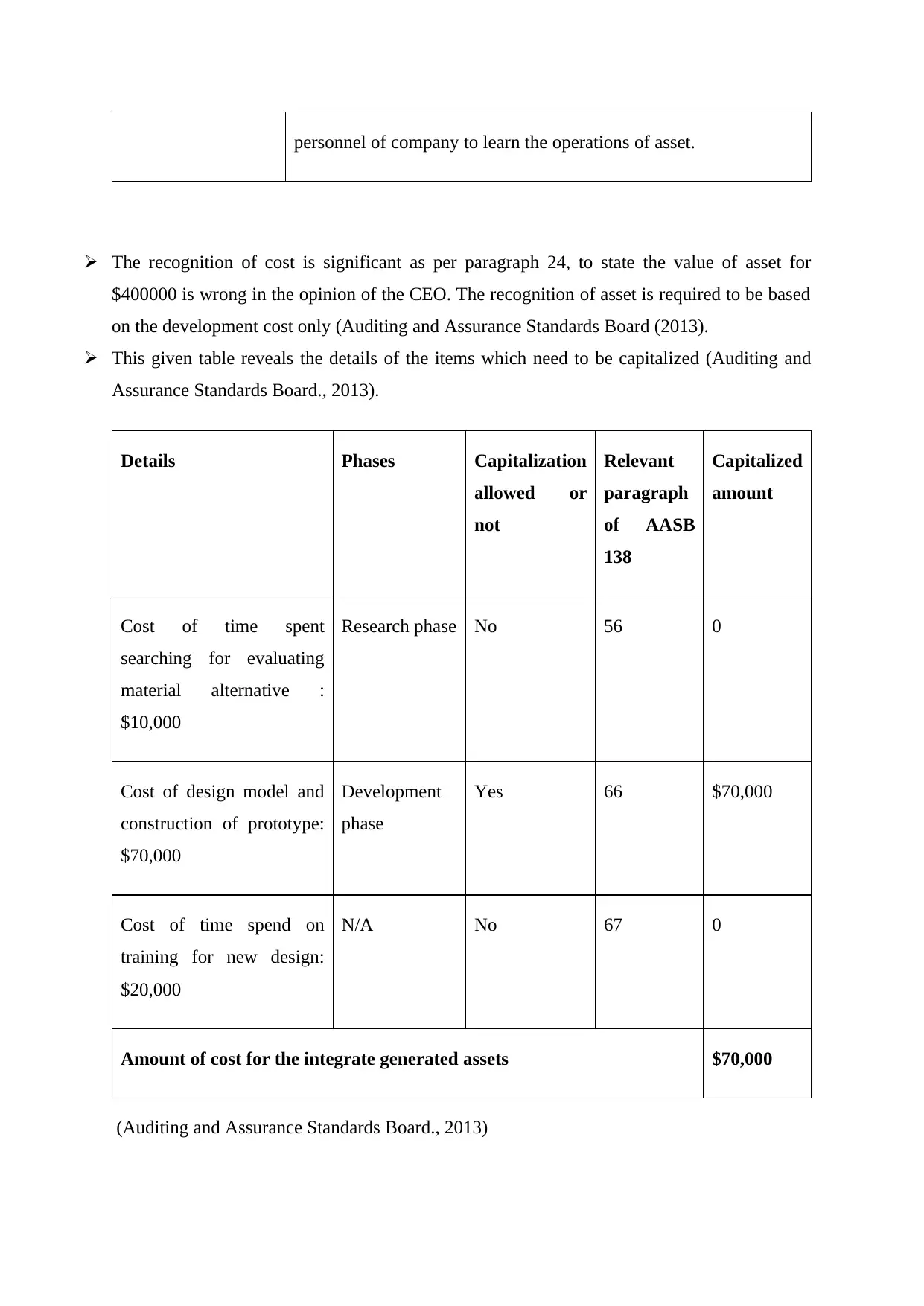

personnel of company to learn the operations of asset.

The recognition of cost is significant as per paragraph 24, to state the value of asset for

$400000 is wrong in the opinion of the CEO. The recognition of asset is required to be based

on the development cost only (Auditing and Assurance Standards Board (2013).

This given table reveals the details of the items which need to be capitalized (Auditing and

Assurance Standards Board., 2013).

Details Phases Capitalization

allowed or

not

Relevant

paragraph

of AASB

138

Capitalized

amount

Cost of time spent

searching for evaluating

material alternative :

$10,000

Research phase No 56 0

Cost of design model and

construction of prototype:

$70,000

Development

phase

Yes 66 $70,000

Cost of time spend on

training for new design:

$20,000

N/A No 67 0

Amount of cost for the integrate generated assets $70,000

(Auditing and Assurance Standards Board., 2013)

The recognition of cost is significant as per paragraph 24, to state the value of asset for

$400000 is wrong in the opinion of the CEO. The recognition of asset is required to be based

on the development cost only (Auditing and Assurance Standards Board (2013).

This given table reveals the details of the items which need to be capitalized (Auditing and

Assurance Standards Board., 2013).

Details Phases Capitalization

allowed or

not

Relevant

paragraph

of AASB

138

Capitalized

amount

Cost of time spent

searching for evaluating

material alternative :

$10,000

Research phase No 56 0

Cost of design model and

construction of prototype:

$70,000

Development

phase

Yes 66 $70,000

Cost of time spend on

training for new design:

$20,000

N/A No 67 0

Amount of cost for the integrate generated assets $70,000

(Auditing and Assurance Standards Board., 2013)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer to question no-2

The rules and obligations mentioned by AASB 138 and IAS 38 are quite similar to each

other. The company follows such rules and regulations to make its legal compliances and

accounting reporting much better and favourable as per the obligations. Both the standards

have their own guidelines which are necessary and obligatory for the companies to manage

their books of accounts and also mandatory to recognise and disclose the intangible assets

into the accounts books. To comply with the requirements of IAS 38, the provisions under

AASB 138 have been updated. The major object behind this is to bring the convergence in

the accounting methods which are followed by the number of listed companies in several

countries. Such convergence has been brought to establish the uniformity and comparability

in the financial statements of the listed companies. For every organisation the policies

relating to recognition, measurement, cost inclusion or exclusion, revaluation and disclosure

of the intangible assets have been defined similar (Lin, et al. 2017)

Sometimes the rules and obligations defined under both AASB 138 and IAS 38 proves

flexible in certain cases. At these certain places the use of best estimated management

judgements and external evidence is asserted by these both accounting measures. For

example paragraph 22 permits the management to use their best judgement to ascertain the

future profitability but it can be results into flexibility in the consideration of profitability and

may also reduce the uniformity of estimates. The management judgement estimates are taken

by the several listed companies situated in different countries around the world which makes

them differ. It raises the finger on the comparable factor of financial statement (Gunarathne,

& Alahakoon, 2016).

Apart from that all the remaining rules and restrictions defined under AASB138/IAS 38 have

established the comparability between financial statements whether between the domestic

entities in Australia or at the international corporate platform. Also, the comparison of the

company’s own performance over the past years results into more transparent and relevant

judgements.

The rules and obligations mentioned by AASB 138 and IAS 38 are quite similar to each

other. The company follows such rules and regulations to make its legal compliances and

accounting reporting much better and favourable as per the obligations. Both the standards

have their own guidelines which are necessary and obligatory for the companies to manage

their books of accounts and also mandatory to recognise and disclose the intangible assets

into the accounts books. To comply with the requirements of IAS 38, the provisions under

AASB 138 have been updated. The major object behind this is to bring the convergence in

the accounting methods which are followed by the number of listed companies in several

countries. Such convergence has been brought to establish the uniformity and comparability

in the financial statements of the listed companies. For every organisation the policies

relating to recognition, measurement, cost inclusion or exclusion, revaluation and disclosure

of the intangible assets have been defined similar (Lin, et al. 2017)

Sometimes the rules and obligations defined under both AASB 138 and IAS 38 proves

flexible in certain cases. At these certain places the use of best estimated management

judgements and external evidence is asserted by these both accounting measures. For

example paragraph 22 permits the management to use their best judgement to ascertain the

future profitability but it can be results into flexibility in the consideration of profitability and

may also reduce the uniformity of estimates. The management judgement estimates are taken

by the several listed companies situated in different countries around the world which makes

them differ. It raises the finger on the comparable factor of financial statement (Gunarathne,

& Alahakoon, 2016).

Apart from that all the remaining rules and restrictions defined under AASB138/IAS 38 have

established the comparability between financial statements whether between the domestic

entities in Australia or at the international corporate platform. Also, the comparison of the

company’s own performance over the past years results into more transparent and relevant

judgements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

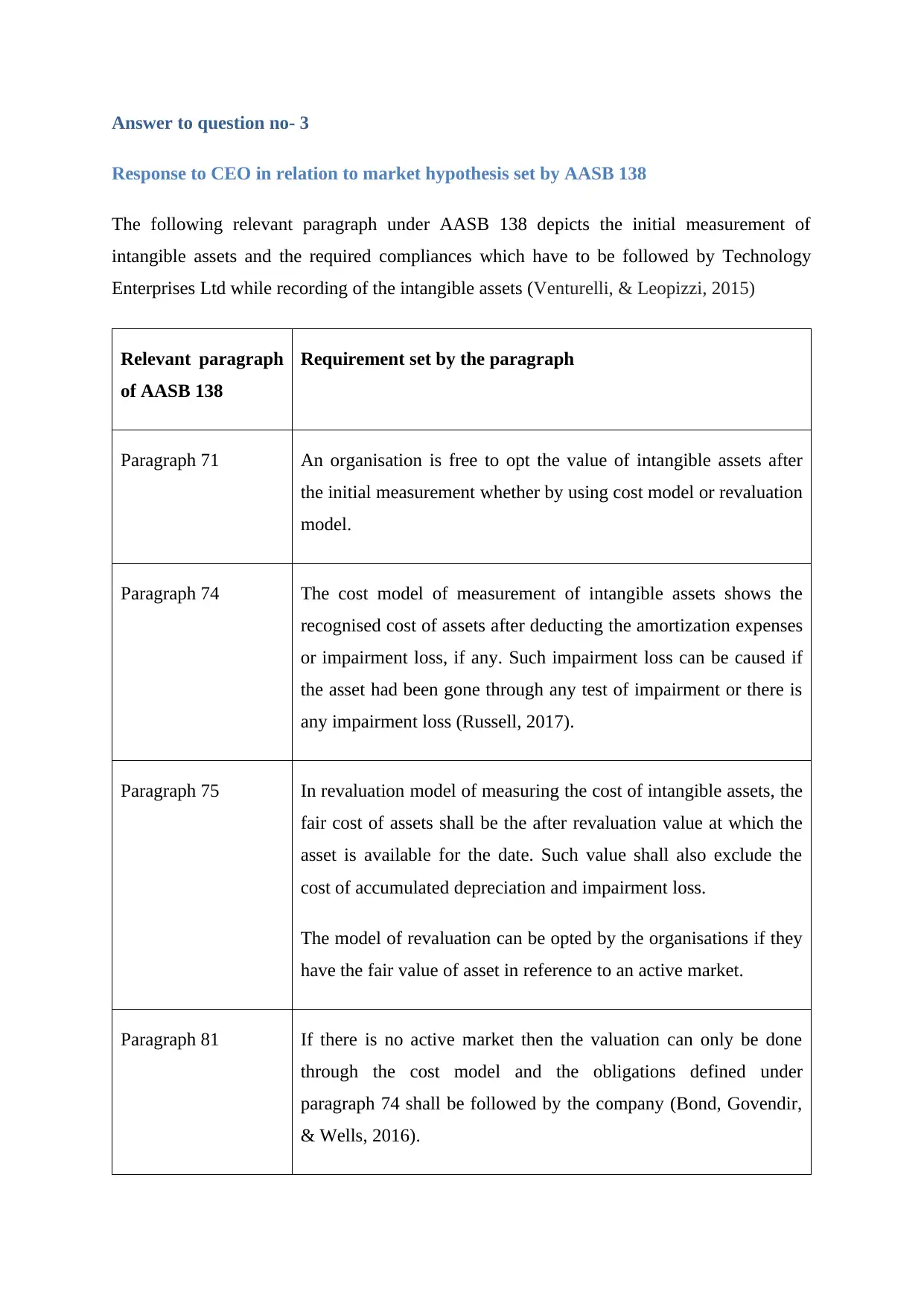

Answer to question no- 3

Response to CEO in relation to market hypothesis set by AASB 138

The following relevant paragraph under AASB 138 depicts the initial measurement of

intangible assets and the required compliances which have to be followed by Technology

Enterprises Ltd while recording of the intangible assets (Venturelli, & Leopizzi, 2015)

Relevant paragraph

of AASB 138

Requirement set by the paragraph

Paragraph 71 An organisation is free to opt the value of intangible assets after

the initial measurement whether by using cost model or revaluation

model.

Paragraph 74 The cost model of measurement of intangible assets shows the

recognised cost of assets after deducting the amortization expenses

or impairment loss, if any. Such impairment loss can be caused if

the asset had been gone through any test of impairment or there is

any impairment loss (Russell, 2017).

Paragraph 75 In revaluation model of measuring the cost of intangible assets, the

fair cost of assets shall be the after revaluation value at which the

asset is available for the date. Such value shall also exclude the

cost of accumulated depreciation and impairment loss.

The model of revaluation can be opted by the organisations if they

have the fair value of asset in reference to an active market.

Paragraph 81 If there is no active market then the valuation can only be done

through the cost model and the obligations defined under

paragraph 74 shall be followed by the company (Bond, Govendir,

& Wells, 2016).

Response to CEO in relation to market hypothesis set by AASB 138

The following relevant paragraph under AASB 138 depicts the initial measurement of

intangible assets and the required compliances which have to be followed by Technology

Enterprises Ltd while recording of the intangible assets (Venturelli, & Leopizzi, 2015)

Relevant paragraph

of AASB 138

Requirement set by the paragraph

Paragraph 71 An organisation is free to opt the value of intangible assets after

the initial measurement whether by using cost model or revaluation

model.

Paragraph 74 The cost model of measurement of intangible assets shows the

recognised cost of assets after deducting the amortization expenses

or impairment loss, if any. Such impairment loss can be caused if

the asset had been gone through any test of impairment or there is

any impairment loss (Russell, 2017).

Paragraph 75 In revaluation model of measuring the cost of intangible assets, the

fair cost of assets shall be the after revaluation value at which the

asset is available for the date. Such value shall also exclude the

cost of accumulated depreciation and impairment loss.

The model of revaluation can be opted by the organisations if they

have the fair value of asset in reference to an active market.

Paragraph 81 If there is no active market then the valuation can only be done

through the cost model and the obligations defined under

paragraph 74 shall be followed by the company (Bond, Govendir,

& Wells, 2016).

There is active market which is defined under the AASB 138 in which availability o the

homogenous items would be considered for the true and fair view of the recorded items.

Nonetheless, in this both buyers and sellers would be indulged for trading on the basis often

fair trade price of the intangible assets shown as per the AASB 138.

It is analysed that in the given case, there is no available data or market for the intangible

assets sold in the market. However, there is also not found any homogenous items which are

traded by the given organization in this case. It is hard to determine the price of the intangible

assets sold in the market. In this case, the intangible assets would be valued at $400,000.

Nonetheless, this value would be wrongly considered as per the 75 and 81 of AASB 138.

The recording of the intangible assets in the books of account would be made as per the cost

model given 74 (Mrša, 2018).

homogenous items would be considered for the true and fair view of the recorded items.

Nonetheless, in this both buyers and sellers would be indulged for trading on the basis often

fair trade price of the intangible assets shown as per the AASB 138.

It is analysed that in the given case, there is no available data or market for the intangible

assets sold in the market. However, there is also not found any homogenous items which are

traded by the given organization in this case. It is hard to determine the price of the intangible

assets sold in the market. In this case, the intangible assets would be valued at $400,000.

Nonetheless, this value would be wrongly considered as per the 75 and 81 of AASB 138.

The recording of the intangible assets in the books of account would be made as per the cost

model given 74 (Mrša, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The amortisation expense is calculated as follows:

Life of asset: 10 years

Cost of asset: $70,000

Amortisation expense per year: 70,000/10

: $7,000

Recommendations to meet the concerns about investor interpretation

There must be proper disclosures on the foot of financial statements. As per the provisions set

by AASB 138, a detailed computation of the cost of intangible assets must be shown. The

reason must also be defined as why the cost model is only followed and why the present

value is ignored (Akgün, 2016).

The management should also disclose the estimates used by them in ascertaining “expected

future economic benefits”. It makes the investors enable to understand the profits and benefits

which are economically attached to the development of asset.

The economic and other benefits from the performance of organisation shall also be included

into the financials of company so the investors can understand the future economic and brand

image additions to the organisation (Yao, Percy, & Hu, 2015).

It guides the stakeholders that what key details and recordings related to the intangible assets

are required to recorded and accounted in the books of account of the organisation.

It also assists the investors to identify the economic benefits and profits on the capital which

are offered by the company to them. It also helps to analyse the return on total assets as it is

based on the fair recording of the cost of intangible assets in the books of accounts.

Conclusion

Conclusively after the entire discussion about the recording and valuation of

intangible assets as per the AASB 138 of Technology Enterprises Ltd, it can be stated that

with the help of AASB 138 a company can strengthen transparency of its business assets to

its stakeholders. Through this the company keeps and records the true and fair value of its all

assets in the books of account. Technology Enterprises Ltd has maintained the proper

accounts, recordings and other supporting details in its financial statements which would

Life of asset: 10 years

Cost of asset: $70,000

Amortisation expense per year: 70,000/10

: $7,000

Recommendations to meet the concerns about investor interpretation

There must be proper disclosures on the foot of financial statements. As per the provisions set

by AASB 138, a detailed computation of the cost of intangible assets must be shown. The

reason must also be defined as why the cost model is only followed and why the present

value is ignored (Akgün, 2016).

The management should also disclose the estimates used by them in ascertaining “expected

future economic benefits”. It makes the investors enable to understand the profits and benefits

which are economically attached to the development of asset.

The economic and other benefits from the performance of organisation shall also be included

into the financials of company so the investors can understand the future economic and brand

image additions to the organisation (Yao, Percy, & Hu, 2015).

It guides the stakeholders that what key details and recordings related to the intangible assets

are required to recorded and accounted in the books of account of the organisation.

It also assists the investors to identify the economic benefits and profits on the capital which

are offered by the company to them. It also helps to analyse the return on total assets as it is

based on the fair recording of the cost of intangible assets in the books of accounts.

Conclusion

Conclusively after the entire discussion about the recording and valuation of

intangible assets as per the AASB 138 of Technology Enterprises Ltd, it can be stated that

with the help of AASB 138 a company can strengthen transparency of its business assets to

its stakeholders. Through this the company keeps and records the true and fair value of its all

assets in the books of account. Technology Enterprises Ltd has maintained the proper

accounts, recordings and other supporting details in its financial statements which would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assist the stakeholders of the Technology Enterprises Ltd to easily ascertain the actual

financial results of the company. In the end, it could be stated that every listed company must

comply with the rules, restrictions, provisions and laws of the AASB 138 for proper, fair and

true recording of intangible assets. To determine the value of intangible assets the cost model

should be used by the company and a comparative analysis of the recorded assets should be

held on the periodic basis.

financial results of the company. In the end, it could be stated that every listed company must

comply with the rules, restrictions, provisions and laws of the AASB 138 for proper, fair and

true recording of intangible assets. To determine the value of intangible assets the cost model

should be used by the company and a comparative analysis of the recorded assets should be

held on the periodic basis.

References

Akgün, A. İ. (2016). Quality of the Financial Reporting within the IFRS: Research on

Determining the Attitudes and Evaluations of Financial Information Users. Journal of

Accounting & Finance, (69).

Auditing and Assurance Standards Board (2013) .Auditing Standard ASA 570 Going

Concern. Retrieved May 12th , 2019 from

https://www.auasb.gov.au/admin/file/content102/c3/Jul13_Compiled_Auditing_Stand

ard_ASA_570.pdf

Auditing and Assurance Standards Board (2015a) .Auditing Standard ASA 570 Going

Concern . Retrieved May 12th , 2019 from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf

Auditing and Assurance Standards Board(2015b) Auditing Standard ASA 701

Communicating Key Audit Matters in the Independent Auditor’s Report. Retrieved

May 12th , 2019 from https://www.auasb.gov.au/admin/file/content102/c3/12-

15_AI_5.31_New_Auditing_Standard_ASA_701_(mark-up)_electronic.pdf

Bond, D., Govendir, B., & Wells, P. (2016). An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Denicolai, S., Cotta Ramusino, E., & Sotti, F. (2015). The impact of intangibles on firm

growth. Technology Analysis & Strategic Management, 27(2), 219-236.

Gunarathne, A. N., & Alahakoon, Y. (2016). Environmental management accounting

practices and their diffusion: the Sri Lankan experience.

Lin, S., Riccardi, W., Wang, C., Hopkins, P. E., & Kabureck, G. (2017). Relative Effects of

IFRS Adoption and IFRS Convergence on Financial Statement

Comparability. Contemporary Accounting Research.

Mrša, J. (2018). Valuation of Internally Generated Intangible Assets in Accounting. Acta

Economica Et Turistica, 4(2), 181-195.

Akgün, A. İ. (2016). Quality of the Financial Reporting within the IFRS: Research on

Determining the Attitudes and Evaluations of Financial Information Users. Journal of

Accounting & Finance, (69).

Auditing and Assurance Standards Board (2013) .Auditing Standard ASA 570 Going

Concern. Retrieved May 12th , 2019 from

https://www.auasb.gov.au/admin/file/content102/c3/Jul13_Compiled_Auditing_Stand

ard_ASA_570.pdf

Auditing and Assurance Standards Board (2015a) .Auditing Standard ASA 570 Going

Concern . Retrieved May 12th , 2019 from

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf

Auditing and Assurance Standards Board(2015b) Auditing Standard ASA 701

Communicating Key Audit Matters in the Independent Auditor’s Report. Retrieved

May 12th , 2019 from https://www.auasb.gov.au/admin/file/content102/c3/12-

15_AI_5.31_New_Auditing_Standard_ASA_701_(mark-up)_electronic.pdf

Bond, D., Govendir, B., & Wells, P. (2016). An evaluation of asset impairment decisions by

Australian firms and whether this was impacted by AASB 136.

Denicolai, S., Cotta Ramusino, E., & Sotti, F. (2015). The impact of intangibles on firm

growth. Technology Analysis & Strategic Management, 27(2), 219-236.

Gunarathne, A. N., & Alahakoon, Y. (2016). Environmental management accounting

practices and their diffusion: the Sri Lankan experience.

Lin, S., Riccardi, W., Wang, C., Hopkins, P. E., & Kabureck, G. (2017). Relative Effects of

IFRS Adoption and IFRS Convergence on Financial Statement

Comparability. Contemporary Accounting Research.

Mrša, J. (2018). Valuation of Internally Generated Intangible Assets in Accounting. Acta

Economica Et Turistica, 4(2), 181-195.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.