Financial Accounting Report: AASB 138 and Technology Enterprises

VerifiedAdded on 2022/11/26

|10

|2621

|317

Report

AI Summary

This financial accounting report analyzes the case of Technology Enterprises Ltd., a company developing a new battery recharge technology, and its implications under AASB 138. The report details the recognition and measurement of the intangible asset (patent), differentiating between research and development phases, and determining the appropriate accounting treatment for associated costs. It covers capitalization of development expenditures, amortization, and presentation in financial statements. The report also addresses the limitations of AASB 138 on comparability and provides recommendations for the CFO to address investor concerns regarding the financial reporting of the project, including necessary disclosures to ensure transparency and compliance with accounting standards. The solution also includes the calculation of the amount of capitalisation and amortization. The report suggests that the research expenses should be charged off and the development expenses should be capitalised in the books of accounts.

FINANCIAL

ACCOUNTING

ASSIGNMENT

ACCOUNTING

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Executive Summary

In the given case, Technology Enterprises Ltd. is one of the company which is listed and did start a

research and development project in July 2017 in order to modify the method of recharge of batteries in

all its products. The product got fully completed in June 2018 and the company applied for the patent on

behalf of the same. The company is planning to modify the entire product range in the coming 2 years

and therefore has incorporated the same in the financial budget of the company. The company is

expecting to derive the economic benefit from the new technology on battery recharging for the next 10

years. The accountant of the company was not sure on the treatment of the salaries given to the

engineer and therefore he used the New R&D expenses to accumulate the salaries for the year ended

30th June 2018. The value in use as per present value as well as fair value of the design has been given.

The report below covers how the project should be accounted in the financial statements for the year

ended 30th June 2018 in reference of the relevant accounting standards. The report also highlights the

rules and restrictions which are mentioned in AASB 138 which compromise the comparability of the

financial statements. Lastly a response has been drafted for the CFO highlighting the points which will

help in mitigating the concerns regarding investor grievance on the information presented in the

financial statements.

2 | P a g e

Executive Summary

In the given case, Technology Enterprises Ltd. is one of the company which is listed and did start a

research and development project in July 2017 in order to modify the method of recharge of batteries in

all its products. The product got fully completed in June 2018 and the company applied for the patent on

behalf of the same. The company is planning to modify the entire product range in the coming 2 years

and therefore has incorporated the same in the financial budget of the company. The company is

expecting to derive the economic benefit from the new technology on battery recharging for the next 10

years. The accountant of the company was not sure on the treatment of the salaries given to the

engineer and therefore he used the New R&D expenses to accumulate the salaries for the year ended

30th June 2018. The value in use as per present value as well as fair value of the design has been given.

The report below covers how the project should be accounted in the financial statements for the year

ended 30th June 2018 in reference of the relevant accounting standards. The report also highlights the

rules and restrictions which are mentioned in AASB 138 which compromise the comparability of the

financial statements. Lastly a response has been drafted for the CFO highlighting the points which will

help in mitigating the concerns regarding investor grievance on the information presented in the

financial statements.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Analysis and Calculation..............................................................................................................................4

Interpretation and Representation..............................................................................................................5

Assumptions................................................................................................................................................7

References...................................................................................................................................................8

3 | P a g e

Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

Analysis and Calculation..............................................................................................................................4

Interpretation and Representation..............................................................................................................5

Assumptions................................................................................................................................................7

References...................................................................................................................................................8

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

For an asset to be recognised as intangible asset in the books of accounts, the same should be within the

control of the entity and it should give future economic benefits to the entity. It must also possess 3

other characteristics namely it should be identifiable, non-monetary and without any physical substance

(para 8 of AASB 138). Hence, in case any of these 3 characteristics are not being fulfilled the same

cannot be recognised as intangible assets (Alexander, 2016). Before the same can be shown as

intangible assets in the accounting books, the asset also needs to meet the recognition criteria as

mentioned in Para 21 of AASB 138 namely:

1. It is expected to give future economic benefits to the entity

2. The amount of the asset can be measured reliably.

Analysis and Calculation

In the given case, several labour expenditure has been incurred on the generation of the design of new

battery recharging technology and hence it cannot be said to the internally generated asset and

therefore the same can be recognised in the books (Para 63 of AASB 138). Furthermore, as per the

standard, in case any research cost has been incurred in the development of the asset, it cannot be

capitalised in the value of the asset and has to be expensed off in the profit and loss account. As per

Para 52 of AASB 138, the company needs to bifurcate and distinguish between the research phase and

the development phase before going ahead with the capitalisation (Heminway, 2017).

Para 8 of AASB 138 defines the research phase as the original and planned investigation undertaken

with the intention of the getting the scientific or technical knowhow on any new subject. On the other

hand, Development has been defined as application of the research done earlier to plan or design the

production of a new product, device, material, process, services, etc. before the commercial production

actually starts. An intangible asset can only come into existence once the development expenditure is

incurred. Some of the recognition criteria which has to be met in this regard (Para 57 of AASB 138) are:

1. The intangible asset to be developed should be technically feasible such that it is available for

sale;

2. There should be an intention to develop the intangible asset or to use it or sell the same;

3. There is an ability to use or sell the intangible asset (Dichev, 2017);

4. The intangible asset is expected to generate future economic benefits for the entity – the same

should either have an active market for sale or if the same is used internally, the intangible asset

should be useful to the entity (Loftus, et al., 2018).

5. There should be sufficient technical, financial and other resources which should be present for

the completion of the intangible asset.

6. The expenditure incurred on the intangible asset during the period of development should be

reliably measured (Sithole, et al., 2017).

In case all the above criteria are being met, then the asset can be recognised in the books as the

intangible asset being the sum total of the development related expenditures. In case the above

mentioned recognition criteria is not being met, all such expenses should be charged off.

4 | P a g e

Introduction

For an asset to be recognised as intangible asset in the books of accounts, the same should be within the

control of the entity and it should give future economic benefits to the entity. It must also possess 3

other characteristics namely it should be identifiable, non-monetary and without any physical substance

(para 8 of AASB 138). Hence, in case any of these 3 characteristics are not being fulfilled the same

cannot be recognised as intangible assets (Alexander, 2016). Before the same can be shown as

intangible assets in the accounting books, the asset also needs to meet the recognition criteria as

mentioned in Para 21 of AASB 138 namely:

1. It is expected to give future economic benefits to the entity

2. The amount of the asset can be measured reliably.

Analysis and Calculation

In the given case, several labour expenditure has been incurred on the generation of the design of new

battery recharging technology and hence it cannot be said to the internally generated asset and

therefore the same can be recognised in the books (Para 63 of AASB 138). Furthermore, as per the

standard, in case any research cost has been incurred in the development of the asset, it cannot be

capitalised in the value of the asset and has to be expensed off in the profit and loss account. As per

Para 52 of AASB 138, the company needs to bifurcate and distinguish between the research phase and

the development phase before going ahead with the capitalisation (Heminway, 2017).

Para 8 of AASB 138 defines the research phase as the original and planned investigation undertaken

with the intention of the getting the scientific or technical knowhow on any new subject. On the other

hand, Development has been defined as application of the research done earlier to plan or design the

production of a new product, device, material, process, services, etc. before the commercial production

actually starts. An intangible asset can only come into existence once the development expenditure is

incurred. Some of the recognition criteria which has to be met in this regard (Para 57 of AASB 138) are:

1. The intangible asset to be developed should be technically feasible such that it is available for

sale;

2. There should be an intention to develop the intangible asset or to use it or sell the same;

3. There is an ability to use or sell the intangible asset (Dichev, 2017);

4. The intangible asset is expected to generate future economic benefits for the entity – the same

should either have an active market for sale or if the same is used internally, the intangible asset

should be useful to the entity (Loftus, et al., 2018).

5. There should be sufficient technical, financial and other resources which should be present for

the completion of the intangible asset.

6. The expenditure incurred on the intangible asset during the period of development should be

reliably measured (Sithole, et al., 2017).

In case all the above criteria are being met, then the asset can be recognised in the books as the

intangible asset being the sum total of the development related expenditures. In case the above

mentioned recognition criteria is not being met, all such expenses should be charged off.

4 | P a g e

5

Para 74 of AASB 138 states that the asset should be recorded at the initial cost and then the same is

subject to amortization. As per Para 75, an intangible asset can be revalued at the fair value subject to

amortization and impairment charges under the revaluation model however, the intangible asset can

only be revalued if the fair value is measured in reference to the active market for the given asset. Some

assets like brands mastheads, patents, newspapers and trademarks are being prohibited from being

revalued using the revaluation model simply because of the fact that there is no active market for these

asset and also these assets are generally considered to be unique (Linden & Freeman, 2017).

As per Para 90 of AASB 138, With respect to determination of the depreciable or the useful life of the

intangible asset, several factors have to be considered, some of which have been mentioned below:

a. The expected use of the asset by the entity or the period for which it can be efficiently managed

by some other management team.

b. The life cycle of the asset or the similar assets.

c. The stability of the industry and the changes in the market scenario

d. The technological and commercial and other types of obsolescence

e. The actions of the competitors

f. The level of asset maintenance by the company in question

g. If the useful life of the asset is dependent on the life of other assets of the entity.

Interpretation and Representation

1. In the light of the above discussion the accounting of the given project in the financial

statements as for the year ended 30th June 2018 can be done in the following manner:

a. The new method of recharging the batteries used in the products can be recognised as the

patent in the books of accounts as it meets the recognition criteria of the intangible asset.

b. Furthermore it also meets all the six criteria which has been mentioned above as a part of

development expenditure and therefore the same can be recognised in the books as

patents.

c. The cost incurred by the company during the research phase is to be charged off in the

profit and loss account of the company and therefore the cost of time spent on searching

for and evaluating the alternative materials amounting to $100000 should be charged off in

the statement of income and expenses.

d. The cost of time spent on designing the models and constructing and testing the prototypes

should be capitalised as the value of the asset, being the development expenditure. The

amount of capitalization here will be $700000 (ICAEW, 2011).

e. The cost of the time spent on training of the maintenance workers for the new design is the

expense which has been incurred post the development of the new method of recharging

the batteries. Thus, this is an expense which is incurred post the development stage of the

intangible asset and hence is not eligible to be capitalised in the value of the asset.

f. Therefore the initial recognition of the asset in the books of accounts should be at the value

of $700000 (Van Rinsum, 2018).

g. Furthermore since the life of the asset has been considered to be finite – 10 years based on

the estimated economic benefits that could be derived out of the asset – the amortization

5 | P a g e

Para 74 of AASB 138 states that the asset should be recorded at the initial cost and then the same is

subject to amortization. As per Para 75, an intangible asset can be revalued at the fair value subject to

amortization and impairment charges under the revaluation model however, the intangible asset can

only be revalued if the fair value is measured in reference to the active market for the given asset. Some

assets like brands mastheads, patents, newspapers and trademarks are being prohibited from being

revalued using the revaluation model simply because of the fact that there is no active market for these

asset and also these assets are generally considered to be unique (Linden & Freeman, 2017).

As per Para 90 of AASB 138, With respect to determination of the depreciable or the useful life of the

intangible asset, several factors have to be considered, some of which have been mentioned below:

a. The expected use of the asset by the entity or the period for which it can be efficiently managed

by some other management team.

b. The life cycle of the asset or the similar assets.

c. The stability of the industry and the changes in the market scenario

d. The technological and commercial and other types of obsolescence

e. The actions of the competitors

f. The level of asset maintenance by the company in question

g. If the useful life of the asset is dependent on the life of other assets of the entity.

Interpretation and Representation

1. In the light of the above discussion the accounting of the given project in the financial

statements as for the year ended 30th June 2018 can be done in the following manner:

a. The new method of recharging the batteries used in the products can be recognised as the

patent in the books of accounts as it meets the recognition criteria of the intangible asset.

b. Furthermore it also meets all the six criteria which has been mentioned above as a part of

development expenditure and therefore the same can be recognised in the books as

patents.

c. The cost incurred by the company during the research phase is to be charged off in the

profit and loss account of the company and therefore the cost of time spent on searching

for and evaluating the alternative materials amounting to $100000 should be charged off in

the statement of income and expenses.

d. The cost of time spent on designing the models and constructing and testing the prototypes

should be capitalised as the value of the asset, being the development expenditure. The

amount of capitalization here will be $700000 (ICAEW, 2011).

e. The cost of the time spent on training of the maintenance workers for the new design is the

expense which has been incurred post the development of the new method of recharging

the batteries. Thus, this is an expense which is incurred post the development stage of the

intangible asset and hence is not eligible to be capitalised in the value of the asset.

f. Therefore the initial recognition of the asset in the books of accounts should be at the value

of $700000 (Van Rinsum, 2018).

g. Furthermore since the life of the asset has been considered to be finite – 10 years based on

the estimated economic benefits that could be derived out of the asset – the amortization

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

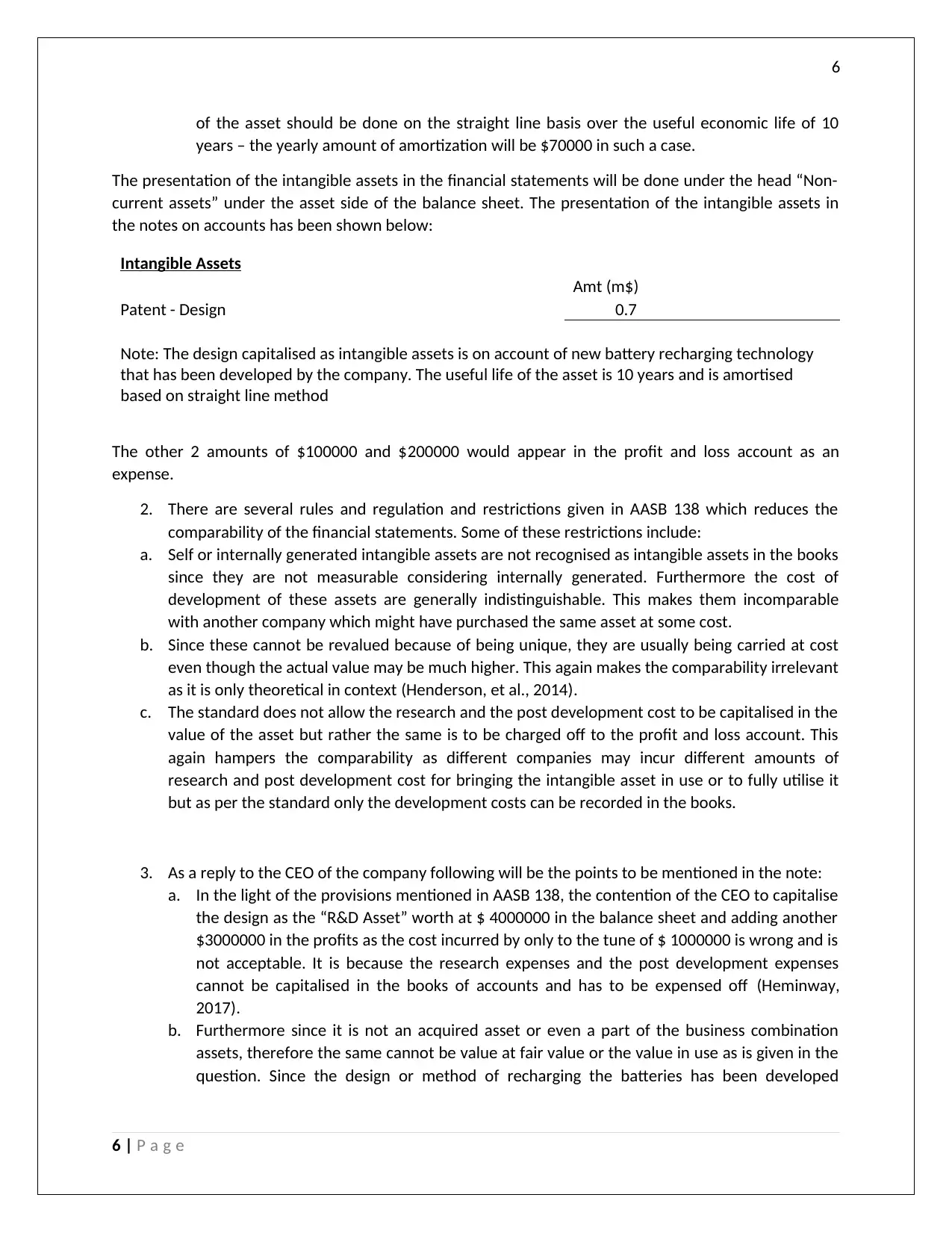

of the asset should be done on the straight line basis over the useful economic life of 10

years – the yearly amount of amortization will be $70000 in such a case.

The presentation of the intangible assets in the financial statements will be done under the head “Non-

current assets” under the asset side of the balance sheet. The presentation of the intangible assets in

the notes on accounts has been shown below:

Intangible Assets

Amt (m$)

Patent - Design 0.7

Note: The design capitalised as intangible assets is on account of new battery recharging technology

that has been developed by the company. The useful life of the asset is 10 years and is amortised

based on straight line method

The other 2 amounts of $100000 and $200000 would appear in the profit and loss account as an

expense.

2. There are several rules and regulation and restrictions given in AASB 138 which reduces the

comparability of the financial statements. Some of these restrictions include:

a. Self or internally generated intangible assets are not recognised as intangible assets in the books

since they are not measurable considering internally generated. Furthermore the cost of

development of these assets are generally indistinguishable. This makes them incomparable

with another company which might have purchased the same asset at some cost.

b. Since these cannot be revalued because of being unique, they are usually being carried at cost

even though the actual value may be much higher. This again makes the comparability irrelevant

as it is only theoretical in context (Henderson, et al., 2014).

c. The standard does not allow the research and the post development cost to be capitalised in the

value of the asset but rather the same is to be charged off to the profit and loss account. This

again hampers the comparability as different companies may incur different amounts of

research and post development cost for bringing the intangible asset in use or to fully utilise it

but as per the standard only the development costs can be recorded in the books.

3. As a reply to the CEO of the company following will be the points to be mentioned in the note:

a. In the light of the provisions mentioned in AASB 138, the contention of the CEO to capitalise

the design as the “R&D Asset” worth at $ 4000000 in the balance sheet and adding another

$3000000 in the profits as the cost incurred by only to the tune of $ 1000000 is wrong and is

not acceptable. It is because the research expenses and the post development expenses

cannot be capitalised in the books of accounts and has to be expensed off (Heminway,

2017).

b. Furthermore since it is not an acquired asset or even a part of the business combination

assets, therefore the same cannot be value at fair value or the value in use as is given in the

question. Since the design or method of recharging the batteries has been developed

6 | P a g e

of the asset should be done on the straight line basis over the useful economic life of 10

years – the yearly amount of amortization will be $70000 in such a case.

The presentation of the intangible assets in the financial statements will be done under the head “Non-

current assets” under the asset side of the balance sheet. The presentation of the intangible assets in

the notes on accounts has been shown below:

Intangible Assets

Amt (m$)

Patent - Design 0.7

Note: The design capitalised as intangible assets is on account of new battery recharging technology

that has been developed by the company. The useful life of the asset is 10 years and is amortised

based on straight line method

The other 2 amounts of $100000 and $200000 would appear in the profit and loss account as an

expense.

2. There are several rules and regulation and restrictions given in AASB 138 which reduces the

comparability of the financial statements. Some of these restrictions include:

a. Self or internally generated intangible assets are not recognised as intangible assets in the books

since they are not measurable considering internally generated. Furthermore the cost of

development of these assets are generally indistinguishable. This makes them incomparable

with another company which might have purchased the same asset at some cost.

b. Since these cannot be revalued because of being unique, they are usually being carried at cost

even though the actual value may be much higher. This again makes the comparability irrelevant

as it is only theoretical in context (Henderson, et al., 2014).

c. The standard does not allow the research and the post development cost to be capitalised in the

value of the asset but rather the same is to be charged off to the profit and loss account. This

again hampers the comparability as different companies may incur different amounts of

research and post development cost for bringing the intangible asset in use or to fully utilise it

but as per the standard only the development costs can be recorded in the books.

3. As a reply to the CEO of the company following will be the points to be mentioned in the note:

a. In the light of the provisions mentioned in AASB 138, the contention of the CEO to capitalise

the design as the “R&D Asset” worth at $ 4000000 in the balance sheet and adding another

$3000000 in the profits as the cost incurred by only to the tune of $ 1000000 is wrong and is

not acceptable. It is because the research expenses and the post development expenses

cannot be capitalised in the books of accounts and has to be expensed off (Heminway,

2017).

b. Furthermore since it is not an acquired asset or even a part of the business combination

assets, therefore the same cannot be value at fair value or the value in use as is given in the

question. Since the design or method of recharging the batteries has been developed

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

internally by the company the same should be valued at cost and here it will be amounting

to $ 700000.

c. As per the theory of efficient markets, the prices of the assets fully reflect all the financial

information. In simple words, it is impossible to beat the market and the market prices are

only expected to reach only to the new information.

d. As a measure of recommendation, the company should be making appropriate disclosures

in the financial statements to mitigate the concern of the investors’ interpretation. The

disclosures should be clear and understandable and not ambiguous which will help them in

understanding the requirement of the law and accounting standards. Some of these

disclosures are:

1. Nature of the intangible asset and basis of measurement of the same

2. The gross carrying amount, the accumulated depreciation till date, the impairment

losses, if any (Jefferson, 2017).

3. The bifurcation between the research and development expenditure

4. The amortization method being used along with the estimated economic life of the

asset

5. The movement, addition, deletion, revaluation, amortization, impairment of the asset

during the given period.

Assumptions

Following are the major assumptions which have been considered in the given case.

1. The intangible asset in the form of the design meets all the recognition criteria as mentioned in

the Para 57 of AASB 138 on development phase.

2. It has also been assumed that the design is one of such intangible assets which does not has an

active market since it is unique for the company and therefore the revaluation of the same has

not been done.

3. The life of the asset has been considered to be 10 years considering the best possible estimate

by the management of the company.

7 | P a g e

internally by the company the same should be valued at cost and here it will be amounting

to $ 700000.

c. As per the theory of efficient markets, the prices of the assets fully reflect all the financial

information. In simple words, it is impossible to beat the market and the market prices are

only expected to reach only to the new information.

d. As a measure of recommendation, the company should be making appropriate disclosures

in the financial statements to mitigate the concern of the investors’ interpretation. The

disclosures should be clear and understandable and not ambiguous which will help them in

understanding the requirement of the law and accounting standards. Some of these

disclosures are:

1. Nature of the intangible asset and basis of measurement of the same

2. The gross carrying amount, the accumulated depreciation till date, the impairment

losses, if any (Jefferson, 2017).

3. The bifurcation between the research and development expenditure

4. The amortization method being used along with the estimated economic life of the

asset

5. The movement, addition, deletion, revaluation, amortization, impairment of the asset

during the given period.

Assumptions

Following are the major assumptions which have been considered in the given case.

1. The intangible asset in the form of the design meets all the recognition criteria as mentioned in

the Para 57 of AASB 138 on development phase.

2. It has also been assumed that the design is one of such intangible assets which does not has an

active market since it is unique for the company and therefore the revaluation of the same has

not been done.

3. The life of the asset has been considered to be 10 years considering the best possible estimate

by the management of the company.

7 | P a g e

8

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Henderson, S. et al., 2014. Ethics in accounting. Issues in financial accounting, 15(1), pp. 949-971.

ICAEW, 2011. Measurement of Financial Reporting. Financial Reporting Faculty, pp. 6-22.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Loftus, J. et al., 2018. Financial reporting. 2 ed. Australia: John Wiley & Sons Australia, Ltd.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

8 | P a g e

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Henderson, S. et al., 2014. Ethics in accounting. Issues in financial accounting, 15(1), pp. 949-971.

ICAEW, 2011. Measurement of Financial Reporting. Financial Reporting Faculty, pp. 6-22.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Loftus, J. et al., 2018. Financial reporting. 2 ed. Australia: John Wiley & Sons Australia, Ltd.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Van Rinsum, M. M. V. S. &. S. D., 2018. Disclosure Checklists and Auditors’ Judgments of Aggressive

Accounting. European Accounting Review, 27(2), pp. 383-399.

9 | P a g e

Van Rinsum, M. M. V. S. &. S. D., 2018. Disclosure Checklists and Auditors’ Judgments of Aggressive

Accounting. European Accounting Review, 27(2), pp. 383-399.

9 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.