Case Study: Technology Enterprises Ltd - AASB 138/IAS 38 Application

VerifiedAdded on 2023/03/23

|8

|2874

|71

Case Study

AI Summary

This case study report delves into the accounting treatments required for Technology Enterprises Limited's R&D project, focusing on compliance with AASB 138/IAS 38 guidelines for intangible asset recognition. It addresses the comparability challenges in financial statements and offers a detailed explanation of AASB 138/IAS 38, providing recommendations for the organization to effectively manage related concerns. The report covers aspects such as present value techniques for asset valuation, the realization and measurement of intangible assets, treatment of research costs, and asset development considerations, ultimately aiming to provide a clear understanding of the standard's application within the context of the company's innovative battery recharge technology project.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Executive Summary:

The report focuses on the accounting treatments need to be followed by Technology Enterprises Limited

for the recognition of the project by adhering to the guidelines mentioned in AASB 138/IAS 38. The next

section emphasises on the demerit of the comparability feature related to the financial statements, Finally,

the report has provided explanation of AASB 138/IAS 38 along with suggestion of certain actions for the

organisation so that the concerns could be addressed effectively.

Executive Summary:

The report focuses on the accounting treatments need to be followed by Technology Enterprises Limited

for the recognition of the project by adhering to the guidelines mentioned in AASB 138/IAS 38. The next

section emphasises on the demerit of the comparability feature related to the financial statements, Finally,

the report has provided explanation of AASB 138/IAS 38 along with suggestion of certain actions for the

organisation so that the concerns could be addressed effectively.

2FINANCIAL ACCOUNTING

Table of Contents

Introduction:................................................................................................................................................. 3

1. Accounting treatment for the project in accordance with AASB 138/IAS 38:...........................................3

2. Minimisation of comparability of the financial statements:.......................................................................5

3. Understanding of AASB 138/IAS 38:....................................................................................................... 5

Conclusion and recommendations:.............................................................................................................. 6

References:................................................................................................................................................. 7

Table of Contents

Introduction:................................................................................................................................................. 3

1. Accounting treatment for the project in accordance with AASB 138/IAS 38:...........................................3

2. Minimisation of comparability of the financial statements:.......................................................................5

3. Understanding of AASB 138/IAS 38:....................................................................................................... 5

Conclusion and recommendations:.............................................................................................................. 6

References:................................................................................................................................................. 7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

Introduction:

The organisations have to ensure compliance with different accounting standards as well as

principles for conducting the accounting treatment of their intangible assets. Similarly, the management of

the organisation has to take into account expense related to research and development (R&D) for

intangible asset development. The ASX listed firms in Australia are mandated to follow the standards and

principles mentioned in “AASB 138 Intangible Assets” in order to perform accounting treatments of

intangible assets and various costs pertaining to the same such as R&D and others (Abuaddous, Hanefah

and Laili, 2014). Based on the provided information, it could be observed that Technology Enterprise

Limited has made successful completion of its R&D project in order to modify the methods of battery

recharge. The reports intends to provide an insight of the necessary accounting treatment for the project

by taking into account various paragraphs and sections in accordance with AASB 138/IAS 38.

1. Accounting treatment for the project in accordance with AASB 138/IAS 38:

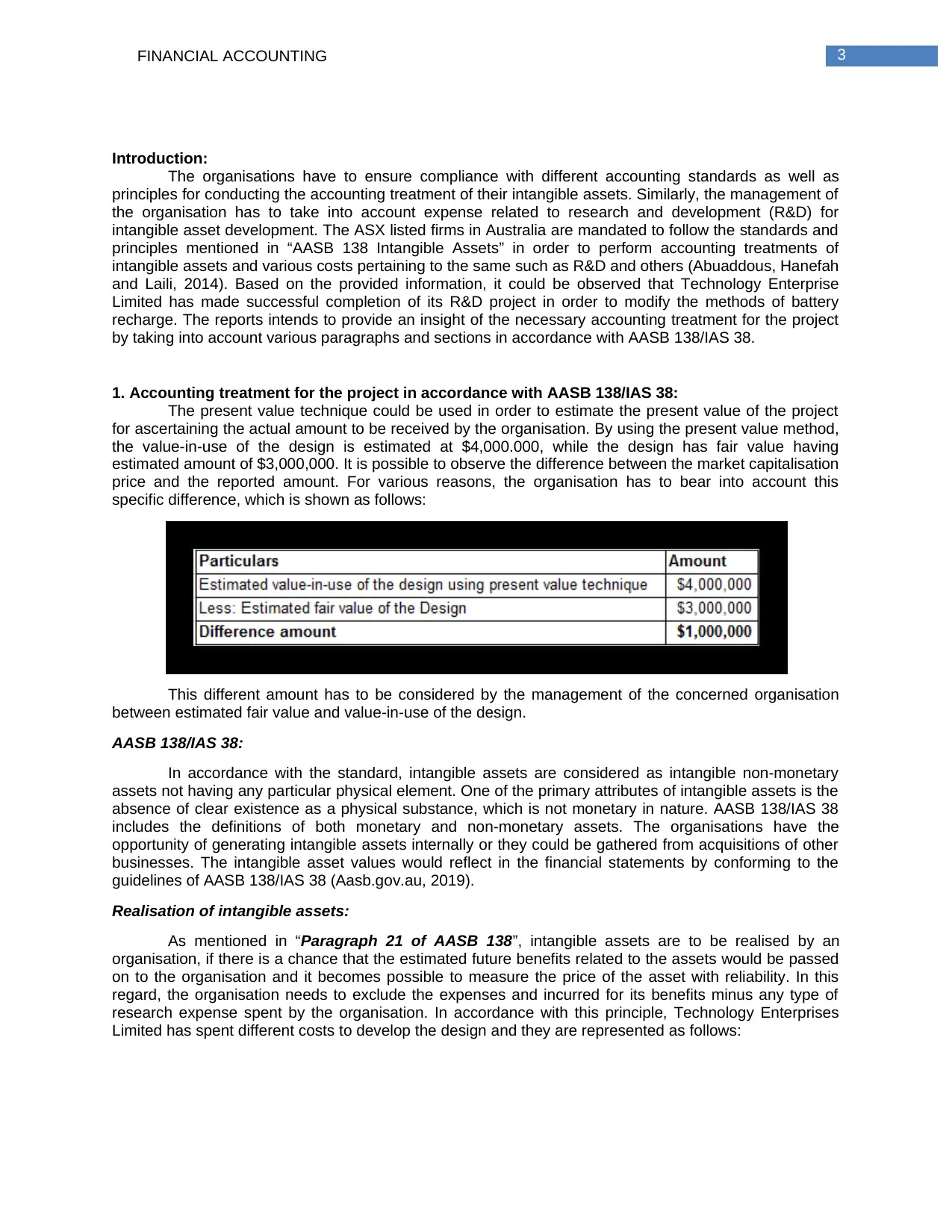

The present value technique could be used in order to estimate the present value of the project

for ascertaining the actual amount to be received by the organisation. By using the present value method,

the value-in-use of the design is estimated at $4,000.000, while the design has fair value having

estimated amount of $3,000,000. It is possible to observe the difference between the market capitalisation

price and the reported amount. For various reasons, the organisation has to bear into account this

specific difference, which is shown as follows:

This different amount has to be considered by the management of the concerned organisation

between estimated fair value and value-in-use of the design.

AASB 138/IAS 38:

In accordance with the standard, intangible assets are considered as intangible non-monetary

assets not having any particular physical element. One of the primary attributes of intangible assets is the

absence of clear existence as a physical substance, which is not monetary in nature. AASB 138/IAS 38

includes the definitions of both monetary and non-monetary assets. The organisations have the

opportunity of generating intangible assets internally or they could be gathered from acquisitions of other

businesses. The intangible asset values would reflect in the financial statements by conforming to the

guidelines of AASB 138/IAS 38 (Aasb.gov.au, 2019).

Realisation of intangible assets:

As mentioned in “Paragraph 21 of AASB 138”, intangible assets are to be realised by an

organisation, if there is a chance that the estimated future benefits related to the assets would be passed

on to the organisation and it becomes possible to measure the price of the asset with reliability. In this

regard, the organisation needs to exclude the expenses and incurred for its benefits minus any type of

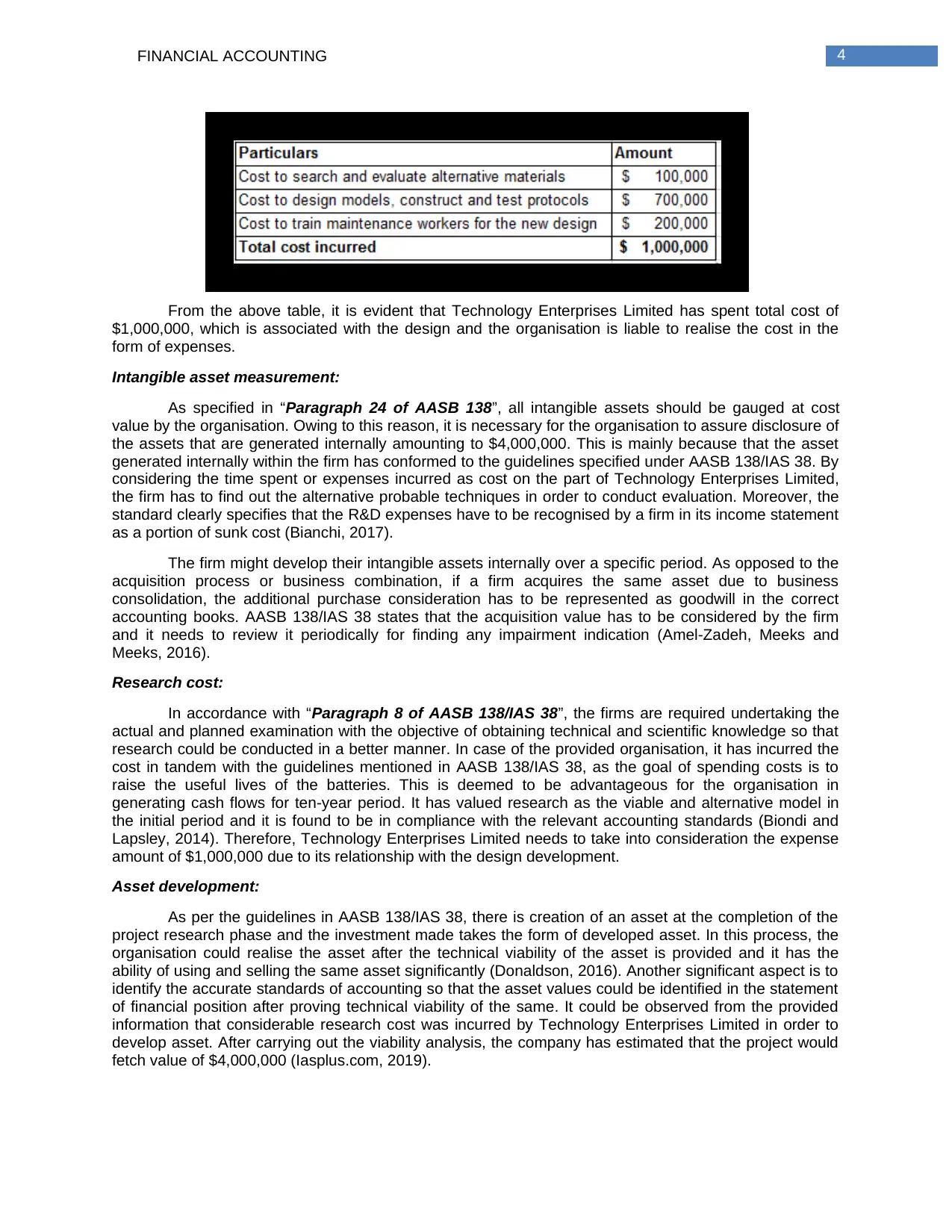

research expense spent by the organisation. In accordance with this principle, Technology Enterprises

Limited has spent different costs to develop the design and they are represented as follows:

Introduction:

The organisations have to ensure compliance with different accounting standards as well as

principles for conducting the accounting treatment of their intangible assets. Similarly, the management of

the organisation has to take into account expense related to research and development (R&D) for

intangible asset development. The ASX listed firms in Australia are mandated to follow the standards and

principles mentioned in “AASB 138 Intangible Assets” in order to perform accounting treatments of

intangible assets and various costs pertaining to the same such as R&D and others (Abuaddous, Hanefah

and Laili, 2014). Based on the provided information, it could be observed that Technology Enterprise

Limited has made successful completion of its R&D project in order to modify the methods of battery

recharge. The reports intends to provide an insight of the necessary accounting treatment for the project

by taking into account various paragraphs and sections in accordance with AASB 138/IAS 38.

1. Accounting treatment for the project in accordance with AASB 138/IAS 38:

The present value technique could be used in order to estimate the present value of the project

for ascertaining the actual amount to be received by the organisation. By using the present value method,

the value-in-use of the design is estimated at $4,000.000, while the design has fair value having

estimated amount of $3,000,000. It is possible to observe the difference between the market capitalisation

price and the reported amount. For various reasons, the organisation has to bear into account this

specific difference, which is shown as follows:

This different amount has to be considered by the management of the concerned organisation

between estimated fair value and value-in-use of the design.

AASB 138/IAS 38:

In accordance with the standard, intangible assets are considered as intangible non-monetary

assets not having any particular physical element. One of the primary attributes of intangible assets is the

absence of clear existence as a physical substance, which is not monetary in nature. AASB 138/IAS 38

includes the definitions of both monetary and non-monetary assets. The organisations have the

opportunity of generating intangible assets internally or they could be gathered from acquisitions of other

businesses. The intangible asset values would reflect in the financial statements by conforming to the

guidelines of AASB 138/IAS 38 (Aasb.gov.au, 2019).

Realisation of intangible assets:

As mentioned in “Paragraph 21 of AASB 138”, intangible assets are to be realised by an

organisation, if there is a chance that the estimated future benefits related to the assets would be passed

on to the organisation and it becomes possible to measure the price of the asset with reliability. In this

regard, the organisation needs to exclude the expenses and incurred for its benefits minus any type of

research expense spent by the organisation. In accordance with this principle, Technology Enterprises

Limited has spent different costs to develop the design and they are represented as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

From the above table, it is evident that Technology Enterprises Limited has spent total cost of

$1,000,000, which is associated with the design and the organisation is liable to realise the cost in the

form of expenses.

Intangible asset measurement:

As specified in “Paragraph 24 of AASB 138”, all intangible assets should be gauged at cost

value by the organisation. Owing to this reason, it is necessary for the organisation to assure disclosure of

the assets that are generated internally amounting to $4,000,000. This is mainly because that the asset

generated internally within the firm has conformed to the guidelines specified under AASB 138/IAS 38. By

considering the time spent or expenses incurred as cost on the part of Technology Enterprises Limited,

the firm has to find out the alternative probable techniques in order to conduct evaluation. Moreover, the

standard clearly specifies that the R&D expenses have to be recognised by a firm in its income statement

as a portion of sunk cost (Bianchi, 2017).

The firm might develop their intangible assets internally over a specific period. As opposed to the

acquisition process or business combination, if a firm acquires the same asset due to business

consolidation, the additional purchase consideration has to be represented as goodwill in the correct

accounting books. AASB 138/IAS 38 states that the acquisition value has to be considered by the firm

and it needs to review it periodically for finding any impairment indication (Amel-Zadeh, Meeks and

Meeks, 2016).

Research cost:

In accordance with “Paragraph 8 of AASB 138/IAS 38”, the firms are required undertaking the

actual and planned examination with the objective of obtaining technical and scientific knowledge so that

research could be conducted in a better manner. In case of the provided organisation, it has incurred the

cost in tandem with the guidelines mentioned in AASB 138/IAS 38, as the goal of spending costs is to

raise the useful lives of the batteries. This is deemed to be advantageous for the organisation in

generating cash flows for ten-year period. It has valued research as the viable and alternative model in

the initial period and it is found to be in compliance with the relevant accounting standards (Biondi and

Lapsley, 2014). Therefore, Technology Enterprises Limited needs to take into consideration the expense

amount of $1,000,000 due to its relationship with the design development.

Asset development:

As per the guidelines in AASB 138/IAS 38, there is creation of an asset at the completion of the

project research phase and the investment made takes the form of developed asset. In this process, the

organisation could realise the asset after the technical viability of the asset is provided and it has the

ability of using and selling the same asset significantly (Donaldson, 2016). Another significant aspect is to

identify the accurate standards of accounting so that the asset values could be identified in the statement

of financial position after proving technical viability of the same. It could be observed from the provided

information that considerable research cost was incurred by Technology Enterprises Limited in order to

develop asset. After carrying out the viability analysis, the company has estimated that the project would

fetch value of $4,000,000 (Iasplus.com, 2019).

From the above table, it is evident that Technology Enterprises Limited has spent total cost of

$1,000,000, which is associated with the design and the organisation is liable to realise the cost in the

form of expenses.

Intangible asset measurement:

As specified in “Paragraph 24 of AASB 138”, all intangible assets should be gauged at cost

value by the organisation. Owing to this reason, it is necessary for the organisation to assure disclosure of

the assets that are generated internally amounting to $4,000,000. This is mainly because that the asset

generated internally within the firm has conformed to the guidelines specified under AASB 138/IAS 38. By

considering the time spent or expenses incurred as cost on the part of Technology Enterprises Limited,

the firm has to find out the alternative probable techniques in order to conduct evaluation. Moreover, the

standard clearly specifies that the R&D expenses have to be recognised by a firm in its income statement

as a portion of sunk cost (Bianchi, 2017).

The firm might develop their intangible assets internally over a specific period. As opposed to the

acquisition process or business combination, if a firm acquires the same asset due to business

consolidation, the additional purchase consideration has to be represented as goodwill in the correct

accounting books. AASB 138/IAS 38 states that the acquisition value has to be considered by the firm

and it needs to review it periodically for finding any impairment indication (Amel-Zadeh, Meeks and

Meeks, 2016).

Research cost:

In accordance with “Paragraph 8 of AASB 138/IAS 38”, the firms are required undertaking the

actual and planned examination with the objective of obtaining technical and scientific knowledge so that

research could be conducted in a better manner. In case of the provided organisation, it has incurred the

cost in tandem with the guidelines mentioned in AASB 138/IAS 38, as the goal of spending costs is to

raise the useful lives of the batteries. This is deemed to be advantageous for the organisation in

generating cash flows for ten-year period. It has valued research as the viable and alternative model in

the initial period and it is found to be in compliance with the relevant accounting standards (Biondi and

Lapsley, 2014). Therefore, Technology Enterprises Limited needs to take into consideration the expense

amount of $1,000,000 due to its relationship with the design development.

Asset development:

As per the guidelines in AASB 138/IAS 38, there is creation of an asset at the completion of the

project research phase and the investment made takes the form of developed asset. In this process, the

organisation could realise the asset after the technical viability of the asset is provided and it has the

ability of using and selling the same asset significantly (Donaldson, 2016). Another significant aspect is to

identify the accurate standards of accounting so that the asset values could be identified in the statement

of financial position after proving technical viability of the same. It could be observed from the provided

information that considerable research cost was incurred by Technology Enterprises Limited in order to

develop asset. After carrying out the viability analysis, the company has estimated that the project would

fetch value of $4,000,000 (Iasplus.com, 2019).

5FINANCIAL ACCOUNTING

2. Minimisation of comparability of the financial statements:

Financial statements contain a crucial characteristic, which is identified as comparability. The

accounting policies and standards that the firm has adopted signify the comparability characteristic

related to the financial statements. In compliance with AASB, both the processes are seen to be applied

that include measuring goodwill at cost and intangible asset acquisition via business combination (Kieso,

Weygandt and Warfield, 2016). As per the previous discussion, it is possible to identify intangible assets;

however, their nature is non-monetary having no physical existence. Hence, the realisation of these types

of assets differs in each organisation depending on the benefits to be obtained from the assets and such

benefits have to be realised as assets. Moreover, pertinent expenses spent on these assets have to be

classified having with relationship with the assets (Kimouche and Rouabhi, 2016).

In accordance with AASB 138/IAS 38, it is necessary to recognise profit from the asset on similar

basis, if the organisation has made acquisition of intangible assets as portion of different assets. Due to

this, the firm has to comply with the accounting guidelines mentioned in AASB 138/IAS 38 to realise these

assets and the capitalisation of the costs incurred is necessary in relation to research and development

(Linnenluecke, et al., 2015). One crucial aspect is that the comparability characteristic is present in the

financial statements of the firm for intangible assets. This specific characteristic of the financial

statements has to be in a manner providing the users with the scope of contrasting the financial

information of the firm with other firm or varying timeline of the similar firm. In this respect, it is noteworthy

to mention that if recognition, measurement and valuation of intangible assets of one form differ

significantly with similar aspects of other firms, there is possibly of material effects on the financial

statements of the firm. The effect would be considerable on the financial decision-making process of the

financial statement users (Nwogugu, 2015).

In relation to the guidelines mentioned in AASB 138/IAS 38 Intangible Assets, it is necessary for

the firms to adhere to different types of regulations so that it could apply the right accounting treatment of

various developments and expenses (Teixeira, 2014). The firm is needed to take into account the cost

incurred for researching any product or developing the same in the form of sunk cost. In addition, this

needs to be treated as an expense in the income statement rather than capitalisation of the same. The

rules pertaining to recognition, classification and measurement need the organisations to take into

account such expenses along with recording the same in the accurate books of accounts.

3. Understanding of AASB 138/IAS 38:

AASB considers AASB 138/IAS 38 as the crucial document for all the ASX listed firms, which

provide these firms with the necessary standards and accounting policies for accurate accounting

treatment related to intangible assets and other aspects associated with such assets. As per the

accounting policy of AASB 138/IAS 38, it has been stated that intangible assets and non-monetary assets

are identifiable and it lacks the presence of any physical existence (Yallwe and Buscemi, 2014). In

accordance with the similar accounting standard, the asset to be identified in the form of intangible asset

has to be divisible from the organisation in a way that they could be exchanged or sold in the market. The

definition of monetary and non-monetary assets could be gathered from AASB 138/IAS 38. In accordance

with this particular standard, it becomes possible for the companies to acquire intangible assets owing to

the outcome of business combination and they could derive these assets internally, which is goodwill

(Zambon, 2017).

The values of these types of assets based on the created assets is represented from the

regulations mentioned in AASB 138/IAS 38. According to the guidelines of AASB 138/IAS 38, the

organisations have to gauge the intangible assets at cost value in the initial stage, in which the

organisation has to report intangible assets generated internally at cost value. It is possible for the firms to

realise these asset values when there is a chance that the future economic advantages would be

transferred to the organisations and the values of these assets at cost could be gauged reliably. In

addition, the standard denotes towards the aspect that the business organisations have to prove the

technical viability of such assets before their values are identified in the balance sheet statement of the

organisation (Zhang and Zhang, 2017).

2. Minimisation of comparability of the financial statements:

Financial statements contain a crucial characteristic, which is identified as comparability. The

accounting policies and standards that the firm has adopted signify the comparability characteristic

related to the financial statements. In compliance with AASB, both the processes are seen to be applied

that include measuring goodwill at cost and intangible asset acquisition via business combination (Kieso,

Weygandt and Warfield, 2016). As per the previous discussion, it is possible to identify intangible assets;

however, their nature is non-monetary having no physical existence. Hence, the realisation of these types

of assets differs in each organisation depending on the benefits to be obtained from the assets and such

benefits have to be realised as assets. Moreover, pertinent expenses spent on these assets have to be

classified having with relationship with the assets (Kimouche and Rouabhi, 2016).

In accordance with AASB 138/IAS 38, it is necessary to recognise profit from the asset on similar

basis, if the organisation has made acquisition of intangible assets as portion of different assets. Due to

this, the firm has to comply with the accounting guidelines mentioned in AASB 138/IAS 38 to realise these

assets and the capitalisation of the costs incurred is necessary in relation to research and development

(Linnenluecke, et al., 2015). One crucial aspect is that the comparability characteristic is present in the

financial statements of the firm for intangible assets. This specific characteristic of the financial

statements has to be in a manner providing the users with the scope of contrasting the financial

information of the firm with other firm or varying timeline of the similar firm. In this respect, it is noteworthy

to mention that if recognition, measurement and valuation of intangible assets of one form differ

significantly with similar aspects of other firms, there is possibly of material effects on the financial

statements of the firm. The effect would be considerable on the financial decision-making process of the

financial statement users (Nwogugu, 2015).

In relation to the guidelines mentioned in AASB 138/IAS 38 Intangible Assets, it is necessary for

the firms to adhere to different types of regulations so that it could apply the right accounting treatment of

various developments and expenses (Teixeira, 2014). The firm is needed to take into account the cost

incurred for researching any product or developing the same in the form of sunk cost. In addition, this

needs to be treated as an expense in the income statement rather than capitalisation of the same. The

rules pertaining to recognition, classification and measurement need the organisations to take into

account such expenses along with recording the same in the accurate books of accounts.

3. Understanding of AASB 138/IAS 38:

AASB considers AASB 138/IAS 38 as the crucial document for all the ASX listed firms, which

provide these firms with the necessary standards and accounting policies for accurate accounting

treatment related to intangible assets and other aspects associated with such assets. As per the

accounting policy of AASB 138/IAS 38, it has been stated that intangible assets and non-monetary assets

are identifiable and it lacks the presence of any physical existence (Yallwe and Buscemi, 2014). In

accordance with the similar accounting standard, the asset to be identified in the form of intangible asset

has to be divisible from the organisation in a way that they could be exchanged or sold in the market. The

definition of monetary and non-monetary assets could be gathered from AASB 138/IAS 38. In accordance

with this particular standard, it becomes possible for the companies to acquire intangible assets owing to

the outcome of business combination and they could derive these assets internally, which is goodwill

(Zambon, 2017).

The values of these types of assets based on the created assets is represented from the

regulations mentioned in AASB 138/IAS 38. According to the guidelines of AASB 138/IAS 38, the

organisations have to gauge the intangible assets at cost value in the initial stage, in which the

organisation has to report intangible assets generated internally at cost value. It is possible for the firms to

realise these asset values when there is a chance that the future economic advantages would be

transferred to the organisations and the values of these assets at cost could be gauged reliably. In

addition, the standard denotes towards the aspect that the business organisations have to prove the

technical viability of such assets before their values are identified in the balance sheet statement of the

organisation (Zhang and Zhang, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

Conclusion and recommendations:

In compliance with the guidelines of financial reporting, regulations related to financial reporting

and accounting policies, it is significant for the firms to disclose the values of their liabilities and assets, as

per the accurate standards of accounting. For Technology Enterprises Limited, it has the alternative of

minimising the issues of the investors through proper disclosures associated with different financial

aspects, in which the organisation would be liable in order to disclose asset valuation on regular basis.

The firms are required undertaking the actual and planned examination with the objective of obtaining

technical and scientific knowledge so that research could be conducted in a better manner. In case of the

provided organisation, it has incurred the cost in tandem with the guidelines mentioned in AASB 138/IAS

38, as the goal of spending costs is to raise the useful lives of the batteries. Moreover, it is required for

the business organisations to conduct estimation and valuation of financial assets by projecting the

financial feasibility of the same, which is made from the end of Technology Enterprises Limited. This is

because it has ascertained the asset values by evaluating the financial feasibility of identical assets.

Due to this, the organisation is needed to implement different guidelines and regulations by

disclosing the financial assets with adherence to the accounting standards. Such financial disclosures

regarding the financial assets play a significant role in the assessment of financial information about

liabilities and assets. The similar aspect has to be followed when it comes to the flow related to economic

benefits, as the organisation has to assure that there would be flow of economic benefit towards it.

Conclusion and recommendations:

In compliance with the guidelines of financial reporting, regulations related to financial reporting

and accounting policies, it is significant for the firms to disclose the values of their liabilities and assets, as

per the accurate standards of accounting. For Technology Enterprises Limited, it has the alternative of

minimising the issues of the investors through proper disclosures associated with different financial

aspects, in which the organisation would be liable in order to disclose asset valuation on regular basis.

The firms are required undertaking the actual and planned examination with the objective of obtaining

technical and scientific knowledge so that research could be conducted in a better manner. In case of the

provided organisation, it has incurred the cost in tandem with the guidelines mentioned in AASB 138/IAS

38, as the goal of spending costs is to raise the useful lives of the batteries. Moreover, it is required for

the business organisations to conduct estimation and valuation of financial assets by projecting the

financial feasibility of the same, which is made from the end of Technology Enterprises Limited. This is

because it has ascertained the asset values by evaluating the financial feasibility of identical assets.

Due to this, the organisation is needed to implement different guidelines and regulations by

disclosing the financial assets with adherence to the accounting standards. Such financial disclosures

regarding the financial assets play a significant role in the assessment of financial information about

liabilities and assets. The similar aspect has to be followed when it comes to the flow related to economic

benefits, as the organisation has to assure that there would be flow of economic benefit towards it.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

References:

Aasb.gov.au., 2019. Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-

15_COMPoct15_01-18.pdf [Accessed 14 May 2019].

Abuaddous, M., Hanefah, M.M. and Laili, N.H., 2014. Accounting standards, goodwill impairment and

earnings management in Malaysia. International Journal of Economics and Finance, 26(4), pp.114-121.

Amel-Zadeh, A., Meeks, G. and Meeks, J.G., 2016. Historical perspectives on accounting for

M&A. Accounting and Business Research, 46(5), pp.501-524.

Bianchi, P., 2017. The economic importance of intangible assets. Routledge.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the heritage assets

problem. Qualitative Research in Accounting & Management, 11(2), pp.146-164.

Donaldson, T. H., 2016. The treatment of intangibles: A banker’s view. Springer.

Iasplus.com., 2019. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 14 May 2019].

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2016. Intermediate Accounting, Binder Ready Version.

John Wiley & Sons.

Kimouche, B. and Rouabhi, A., 2016. The impact of intangibles on the value relevance of accounting

information: Evidence from French companies. Intangible Capital, 12(2), pp.506-529.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries: implications for asset

impairment. Accounting & Finance, 55(4), pp.911-929.

Nwogugu, M.I., 2015. Goodwill/Intangibles Accounting Rules, Earnings Management, and

Competition. Eur. JL Reform, 17, p.117.

Teixeira, A., 2014. The international accounting standards board and evidence-informed standard-

setting. Accounting in Europe, 11(1), pp.5-12.

Yallwe, A. H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance and

Banking, 4(5), p.17.

Zambon, S., 2017. Intangibles and intellectual capital: an overview of the reporting issues and some

measurement models. In The economic importance of intangible assets (pp. 165-196). Routledge.

Zhang, I.X. and Zhang, Y., 2017. Accounting discretion and purchase price allocation after

acquisitions. Journal of Accounting, Auditing & Finance, 32(2), pp.241-270.

References:

Aasb.gov.au., 2019. Available at: https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-

15_COMPoct15_01-18.pdf [Accessed 14 May 2019].

Abuaddous, M., Hanefah, M.M. and Laili, N.H., 2014. Accounting standards, goodwill impairment and

earnings management in Malaysia. International Journal of Economics and Finance, 26(4), pp.114-121.

Amel-Zadeh, A., Meeks, G. and Meeks, J.G., 2016. Historical perspectives on accounting for

M&A. Accounting and Business Research, 46(5), pp.501-524.

Bianchi, P., 2017. The economic importance of intangible assets. Routledge.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the heritage assets

problem. Qualitative Research in Accounting & Management, 11(2), pp.146-164.

Donaldson, T. H., 2016. The treatment of intangibles: A banker’s view. Springer.

Iasplus.com., 2019. IAS 38 — Intangible Assets. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias38 [Accessed 14 May 2019].

Kieso, D. E., Weygandt, J. J. and Warfield, T. D., 2016. Intermediate Accounting, Binder Ready Version.

John Wiley & Sons.

Kimouche, B. and Rouabhi, A., 2016. The impact of intangibles on the value relevance of accounting

information: Evidence from French companies. Intangible Capital, 12(2), pp.506-529.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries: implications for asset

impairment. Accounting & Finance, 55(4), pp.911-929.

Nwogugu, M.I., 2015. Goodwill/Intangibles Accounting Rules, Earnings Management, and

Competition. Eur. JL Reform, 17, p.117.

Teixeira, A., 2014. The international accounting standards board and evidence-informed standard-

setting. Accounting in Europe, 11(1), pp.5-12.

Yallwe, A. H. and Buscemi, A., 2014. An era of intangible assets. Journal of Applied Finance and

Banking, 4(5), p.17.

Zambon, S., 2017. Intangibles and intellectual capital: an overview of the reporting issues and some

measurement models. In The economic importance of intangible assets (pp. 165-196). Routledge.

Zhang, I.X. and Zhang, Y., 2017. Accounting discretion and purchase price allocation after

acquisitions. Journal of Accounting, Auditing & Finance, 32(2), pp.241-270.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.