Impact of AASB 16 on Lease Accounting: An Analysis and Evaluation

VerifiedAdded on 2022/11/17

|14

|4560

|166

Report

AI Summary

This report provides a detailed analysis of the AASB 16 accounting standard for leases, which replaced AASB 117. It highlights the drawbacks of the old standard, such as the differing treatment of operating and finance leases, and the opportunities for off-balance sheet accounting. The report explains the necessity for change, emphasizing the harmonization of lease accounting and the improved understanding of risks for lenders. It outlines the key changes incorporated in AASB 16, including the uniform treatment of all leases (similar to finance leases in AASB 117), the increased recognition of assets and liabilities on the balance sheet, and the impact on income statements. The report also discusses how companies with significant lease financing will be affected, the reasons for classifying leases as operating leases under AASB 117, and the relevance of positive accounting theory in explaining management behavior. Finally, it explains how AASB 16 is expected to improve comparability between companies and provides an example to illustrate this view.

ACCOUNTING THEORY AND CURRENT ISSUES 1

Accounting Theory and Current Issues

Name

Tutor

School

Affiliation

Accounting Theory and Current Issues

Name

Tutor

School

Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES 2

Abstract

The birth of AASB came about as a result of concerns that arose about integrity in the

way leases were being obligated. So as to reduce these issues,the FASB and IASBcame up with a

new set of requirements to harmonize all assets and liabilities of the lessee. The lack of lease

information meant that analysts and investors were in darkness and therefore cannot make

comparisons of companies nor be able to purchase assets. This led to the formulation of a new

set of requirements to guide leasing(AASB 16), that consequently replaced AASB 117.

Abstract

The birth of AASB came about as a result of concerns that arose about integrity in the

way leases were being obligated. So as to reduce these issues,the FASB and IASBcame up with a

new set of requirements to harmonize all assets and liabilities of the lessee. The lack of lease

information meant that analysts and investors were in darkness and therefore cannot make

comparisons of companies nor be able to purchase assets. This led to the formulation of a new

set of requirements to guide leasing(AASB 16), that consequently replaced AASB 117.

ACCOUNTING THEORY AND CURRENT ISSUES 3

Introduction

The IASB has come up with a new set of requirements for leasing (AASB 16), replacing AASB

117.the IASB coordinated with the IFRS to come up with this new standard. All companies were

required to rollout this new standards as from January 2019. The IASB and the IFRS agreed on

many areas, especially the requirementfor leases should be captured on the balance sheet.

Critical evaluation of the old accounting standard for lease (AASB 117) specifically

highlighting the draw backs

One of the major drawbacks of the AASB 117 standard of lease was its difference between the

accounts of the lessee and the leases of operation (Joubert, Garvie& Parle 2017).With the

application of this lease of standard, all leases that would be similar economically are most likely

to be reported differently in the balance sheet. Applying AASB 117, the burden of accounting

largely depended on comparing payments of the lease with the value of the asset, depicting an

assessment that purely rested on the judgement of an individual. Thus, a small difference as

regards with the conditions and terms of the leases could result to a big change in accounting

reporting. This limited comparability between companies and offered few opportunities for

structuring of transactions in order to realize a targeted result of accounting (Cheong, Kim and

Zurbruegg, 2010). AASB 16 is expected to decrease the opportunities for restructuring of leasing

transactions in order to realize off-balance sheet accounting.

In AASB 117, a good number of leases did not support the consideration of liabilities and lease

items. Therefore, companies that obviously show a notable difference in the off balance sheets

would be seen to be similar in their financial and performance report. However, this drawback

has been overcome in AASB 16 as any differences in leasing portfolios would be captured in the

balance sheet. Applying AASB 16, all changes in the companies’ leasing portfolios would be

captured in the balance sheets. Applying AASB 117, the change would have only been reflected

in the balance sheet if only the lease was considered as a finance lease, or when an operating

lease would be changed to become a finance lease. For example, if a company would make a

change in its portfolio such that the portfolio consisted in 10 year lease in the off balance sheet as

opposed to a five year lease in the balance sheet. In this case, the company commitments and the

economic stand of the company would not be captured in the balance sheet of the particular

Introduction

The IASB has come up with a new set of requirements for leasing (AASB 16), replacing AASB

117.the IASB coordinated with the IFRS to come up with this new standard. All companies were

required to rollout this new standards as from January 2019. The IASB and the IFRS agreed on

many areas, especially the requirementfor leases should be captured on the balance sheet.

Critical evaluation of the old accounting standard for lease (AASB 117) specifically

highlighting the draw backs

One of the major drawbacks of the AASB 117 standard of lease was its difference between the

accounts of the lessee and the leases of operation (Joubert, Garvie& Parle 2017).With the

application of this lease of standard, all leases that would be similar economically are most likely

to be reported differently in the balance sheet. Applying AASB 117, the burden of accounting

largely depended on comparing payments of the lease with the value of the asset, depicting an

assessment that purely rested on the judgement of an individual. Thus, a small difference as

regards with the conditions and terms of the leases could result to a big change in accounting

reporting. This limited comparability between companies and offered few opportunities for

structuring of transactions in order to realize a targeted result of accounting (Cheong, Kim and

Zurbruegg, 2010). AASB 16 is expected to decrease the opportunities for restructuring of leasing

transactions in order to realize off-balance sheet accounting.

In AASB 117, a good number of leases did not support the consideration of liabilities and lease

items. Therefore, companies that obviously show a notable difference in the off balance sheets

would be seen to be similar in their financial and performance report. However, this drawback

has been overcome in AASB 16 as any differences in leasing portfolios would be captured in the

balance sheet. Applying AASB 16, all changes in the companies’ leasing portfolios would be

captured in the balance sheets. Applying AASB 117, the change would have only been reflected

in the balance sheet if only the lease was considered as a finance lease, or when an operating

lease would be changed to become a finance lease. For example, if a company would make a

change in its portfolio such that the portfolio consisted in 10 year lease in the off balance sheet as

opposed to a five year lease in the balance sheet. In this case, the company commitments and the

economic stand of the company would not be captured in the balance sheet of the particular

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY AND CURRENT ISSUES 4

company that is applying AASB 117. Additionally, the change would not be reflected in the

statement of income of the company or in the statement of cash flow (AASB 2015).

AASB 117 was majorly focused on determining whether a lease can be associated with

purchasing property that is out for leasing. If a lease is considered to be equal to purchasing the

underlying property, the lease would be categorized in the category of a finance lease that is

commonly called a ‘capital lease.’ In this lease standard, every other lease was put in the

category of operating leases, which consequently would not be captured in the balance sheet of

the company (Bond, Govendir and Wells, 2016).

Why was the change necessary?

It was necessary to change the Lease standard because the AAS 17 was laden with many

drawbacks and limitations. The IASB in coordination with FASB, saw the need for harmonizing

lease accounting. One of the most notable areas that called for this change is the requirement for

leases to be captured in the balance sheet, and that leases be clearly defined and liabilities be

properly measured. Furthermore, the two bodies (FASB and IASB) agreed to maintain the

requirements of lessor accounting as maintained in the AASB 117. Whileaccounting in the lessor

category has changed drastically, and there is no change to do with lessors. The new ruleset out

in this new lease release will ensure that the state of affairs in the financial state is correct, and

that it is properly reflected in the balance sheets. Furthermore, the new release ensures that

lenders will be subjected to a better understanding of the risk that is involved in lending to a

lessee (Ahmed&Alam2012).

It was necessary for the change to be there so as to reduce the administrative costs as the rules do

not apply to leases that are less than 12 months, and to leases that apply to small asses.

What changes have been incorporated in the new accounting standard for lease AASB 16?

The most notable change in AASB 16 is the fact that the new standard of lease informs lenders to

better understand all risk that is involved while lending to lessees. Furthermore, the new lease

will disrupt operation of all leases that deal with both movable and immovable assets, except for

company that is applying AASB 117. Additionally, the change would not be reflected in the

statement of income of the company or in the statement of cash flow (AASB 2015).

AASB 117 was majorly focused on determining whether a lease can be associated with

purchasing property that is out for leasing. If a lease is considered to be equal to purchasing the

underlying property, the lease would be categorized in the category of a finance lease that is

commonly called a ‘capital lease.’ In this lease standard, every other lease was put in the

category of operating leases, which consequently would not be captured in the balance sheet of

the company (Bond, Govendir and Wells, 2016).

Why was the change necessary?

It was necessary to change the Lease standard because the AAS 17 was laden with many

drawbacks and limitations. The IASB in coordination with FASB, saw the need for harmonizing

lease accounting. One of the most notable areas that called for this change is the requirement for

leases to be captured in the balance sheet, and that leases be clearly defined and liabilities be

properly measured. Furthermore, the two bodies (FASB and IASB) agreed to maintain the

requirements of lessor accounting as maintained in the AASB 117. Whileaccounting in the lessor

category has changed drastically, and there is no change to do with lessors. The new ruleset out

in this new lease release will ensure that the state of affairs in the financial state is correct, and

that it is properly reflected in the balance sheets. Furthermore, the new release ensures that

lenders will be subjected to a better understanding of the risk that is involved in lending to a

lessee (Ahmed&Alam2012).

It was necessary for the change to be there so as to reduce the administrative costs as the rules do

not apply to leases that are less than 12 months, and to leases that apply to small asses.

What changes have been incorporated in the new accounting standard for lease AASB 16?

The most notable change in AASB 16 is the fact that the new standard of lease informs lenders to

better understand all risk that is involved while lending to lessees. Furthermore, the new lease

will disrupt operation of all leases that deal with both movable and immovable assets, except for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES 5

leases that are for exploring mining of biological assets such as oil and gas. Some of the changes

that are expected to be seen as a result of this new standard of lease include the following:

The profiles of balance sheets will be significantly changed, making lessees to appear a little bit

leveraged, as they may not really actually be. This may lead to an increment in the borrowing

cost of the lessees. IAAS 16 will do away with the lease classification as either finance leases

operating leases for lessees. All leases will be treated uniformly, just as finance leases are

applied in the AASB 117. The AASB 16 provides that when payments for a lease are made over

time, a company has to take responsibility to be liable financially, therefore giving it an

obligation for making future payments for the lease.

The most significant change in AASB 16 is the increase in leasing of assets and liabilities. There

will be a change in a company’s off balance leasing sheet in terms of how reporting for of assets

and liabilities will be done. The reporting process in terms of complexity and cost is expected to

get more complex as regards to leases dealing with big volumes comprising of little assets (Kang

& Gray 2013).

The AASB 16 has also brought changes in the income statement of a company. UnderAASB 16,

changes have been introduced to the character of expenses that are associated withleases for the

companies having off balance sheets for material leases. This change harmonizes expenses for all

leases.

The new leasing standard is not expected to change the lessor accounting process rigorously, as it

will only need the lessor to unveil information on how it does its risk management as regards to

the residual interests of assets leased. In summary, the accounting requirements on the part of the

lessor will remain unchanged. However, lessor disclosure is a requirement (Zeff and Nobes,

2010, pp.784-789).

Lastly, under the new lease, off-balance sheet leases’ effects do not have to be capture on the

balance sheet as they already can be estimated by the lenders. Qualifying leases that that do not

appear in the balance sheet of lessees have to be captured in the balance sheet

leases that are for exploring mining of biological assets such as oil and gas. Some of the changes

that are expected to be seen as a result of this new standard of lease include the following:

The profiles of balance sheets will be significantly changed, making lessees to appear a little bit

leveraged, as they may not really actually be. This may lead to an increment in the borrowing

cost of the lessees. IAAS 16 will do away with the lease classification as either finance leases

operating leases for lessees. All leases will be treated uniformly, just as finance leases are

applied in the AASB 117. The AASB 16 provides that when payments for a lease are made over

time, a company has to take responsibility to be liable financially, therefore giving it an

obligation for making future payments for the lease.

The most significant change in AASB 16 is the increase in leasing of assets and liabilities. There

will be a change in a company’s off balance leasing sheet in terms of how reporting for of assets

and liabilities will be done. The reporting process in terms of complexity and cost is expected to

get more complex as regards to leases dealing with big volumes comprising of little assets (Kang

& Gray 2013).

The AASB 16 has also brought changes in the income statement of a company. UnderAASB 16,

changes have been introduced to the character of expenses that are associated withleases for the

companies having off balance sheets for material leases. This change harmonizes expenses for all

leases.

The new leasing standard is not expected to change the lessor accounting process rigorously, as it

will only need the lessor to unveil information on how it does its risk management as regards to

the residual interests of assets leased. In summary, the accounting requirements on the part of the

lessor will remain unchanged. However, lessor disclosure is a requirement (Zeff and Nobes,

2010, pp.784-789).

Lastly, under the new lease, off-balance sheet leases’ effects do not have to be capture on the

balance sheet as they already can be estimated by the lenders. Qualifying leases that that do not

appear in the balance sheet of lessees have to be captured in the balance sheet

ACCOUNTING THEORY AND CURRENT ISSUES 6

How will companies that have a significant level of lease financing be affected by the

change in the accounting standard for lease?

Listed companies that use IFRS are projected to be drastically affected by the changes that have

been effected in this new standard in leasing. Values of enterprise are expected to increase while

and EV multiples will reduce. However, the effect of AASB 16 depends on a company’s

financial metrics. Generally, a significant impact of this new lease standard is that listed

companies. The companies that have a significant level of lease will have to roll up their sleeves

in order to meet the standards of the new lease requirements. The companies will have to gather

all the information that is associated with the already existing leases of the year on which the

new lease is rolled out. This information will have to be reflected on the balance sheets of these

companies. Lastly, the companies will have to engage their stakeholders, especially those who

are ready to offer loans or lessees who that have their leases terminating after the new lease

standard is rolled out, that is, after 2019 (Xu, Davidson& Cheong 2017).

In the former accounting standard for lease (AASB 117) both operating lease and finance

lease were allowed, why did companies have a tendency to classify most of the lease

contract as operating lease? How does positive accounting theory relate to this behavior of

managers?

The AASB 117 defines operating lease as any other lease apart from a finance lease. On the

other hand, a finance lease is a means by which finance is provided by a leasing company, to

enable the lessor to acquire an asset and rent the asset to the user for an agreed part of time. Most

of the companies have the tendency of classifying equalizing most leases as operating leases

because operating leases give the lessee an opportunity to access all the rights to use property or

equipment, after which the rights of ownership are transferred back to the lessor. Since most of

the lease contracts involve transfer of finances of property, therefore most of the companies had

the tendency of classifying most contrast as operating leases. AASBB 16 changes drastically the

way a company accounts for its operating leases, except for leases that are of a short term (12

months or under) and leases that involve assets that have a low value (AASB, C.A.S., 2013).

AASB 16 will not significantly change the process of lessor accounting. This is because the

overall costs of overhauling the lessor accounting procedure would surpass all the advantages

that would be accrued from the same. In this new standard, leases will be categorized as either

How will companies that have a significant level of lease financing be affected by the

change in the accounting standard for lease?

Listed companies that use IFRS are projected to be drastically affected by the changes that have

been effected in this new standard in leasing. Values of enterprise are expected to increase while

and EV multiples will reduce. However, the effect of AASB 16 depends on a company’s

financial metrics. Generally, a significant impact of this new lease standard is that listed

companies. The companies that have a significant level of lease will have to roll up their sleeves

in order to meet the standards of the new lease requirements. The companies will have to gather

all the information that is associated with the already existing leases of the year on which the

new lease is rolled out. This information will have to be reflected on the balance sheets of these

companies. Lastly, the companies will have to engage their stakeholders, especially those who

are ready to offer loans or lessees who that have their leases terminating after the new lease

standard is rolled out, that is, after 2019 (Xu, Davidson& Cheong 2017).

In the former accounting standard for lease (AASB 117) both operating lease and finance

lease were allowed, why did companies have a tendency to classify most of the lease

contract as operating lease? How does positive accounting theory relate to this behavior of

managers?

The AASB 117 defines operating lease as any other lease apart from a finance lease. On the

other hand, a finance lease is a means by which finance is provided by a leasing company, to

enable the lessor to acquire an asset and rent the asset to the user for an agreed part of time. Most

of the companies have the tendency of classifying equalizing most leases as operating leases

because operating leases give the lessee an opportunity to access all the rights to use property or

equipment, after which the rights of ownership are transferred back to the lessor. Since most of

the lease contracts involve transfer of finances of property, therefore most of the companies had

the tendency of classifying most contrast as operating leases. AASBB 16 changes drastically the

way a company accounts for its operating leases, except for leases that are of a short term (12

months or under) and leases that involve assets that have a low value (AASB, C.A.S., 2013).

AASB 16 will not significantly change the process of lessor accounting. This is because the

overall costs of overhauling the lessor accounting procedure would surpass all the advantages

that would be accrued from the same. In this new standard, leases will be categorized as either

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY AND CURRENT ISSUES 7

‘finance’ or ‘operating’ leases in the new lease standard. The two categories of leases (finance

and operating) will be accounted for differently. The burden of Positive accounting theory (PAT)

is to explain the practices of accounting. This theory was formulated so as to explain and make

predictions on the firms that will not employ a particular methodology (Wong & Joshi 2015).

The theory does not give its own input on which methodology a particular firm can use.

According to IASB, the implementation of AASB 16 is expected to improve comparability

between companies that lease assets and companies that borrow to buy assets. Explain this

view of the IASB with suitable example.

The IASB projects that the AASB 16 will change how different leasing and borrowing

companies compare. Furthermore, comparison of financial information is expected to be less

complicated. Improvement of compatibility between companies will be improved because the

companies will:

i. Consider all liabilities and assets for leases

ii. Measure liability and asset leases in parallel and

iii. Consider all rights obtained and incurred liabilities.

Therefore, different operating conditions by various companies will an asset, for example, when

a car is leased for five years, applying ASB 16, the be made clear by their financial statements.

In the case whereby a lease is associated with borrowing company would report an amount

similar to that which would be realized if the car would have been bought out of borrowed

money. However, notwithstanding the fact that there is an economic difference between leasing

and borrowing to purchase an asset, (take for example leasing a brand car for six years), in that

case the amount that would be reflected in the application of AAB 16B would be depicting the

economic decisions that were made. Less liabilities and assets will be captured in the balance

sheet, as opposed to when the company would have made a decision to borrow money to

purchase the car. In this case, the entitlement of use of the car for six years would be different

from the entitlement that it would have were it to borrow in order to purchase the car

(Firth&Gounopoulos2017).

At the same time, applying AASB 16, the amount that would be captured is more likely to differ

from the amount that would be recognized in borrowing the asset. Borrowing to buy assets and

‘finance’ or ‘operating’ leases in the new lease standard. The two categories of leases (finance

and operating) will be accounted for differently. The burden of Positive accounting theory (PAT)

is to explain the practices of accounting. This theory was formulated so as to explain and make

predictions on the firms that will not employ a particular methodology (Wong & Joshi 2015).

The theory does not give its own input on which methodology a particular firm can use.

According to IASB, the implementation of AASB 16 is expected to improve comparability

between companies that lease assets and companies that borrow to buy assets. Explain this

view of the IASB with suitable example.

The IASB projects that the AASB 16 will change how different leasing and borrowing

companies compare. Furthermore, comparison of financial information is expected to be less

complicated. Improvement of compatibility between companies will be improved because the

companies will:

i. Consider all liabilities and assets for leases

ii. Measure liability and asset leases in parallel and

iii. Consider all rights obtained and incurred liabilities.

Therefore, different operating conditions by various companies will an asset, for example, when

a car is leased for five years, applying ASB 16, the be made clear by their financial statements.

In the case whereby a lease is associated with borrowing company would report an amount

similar to that which would be realized if the car would have been bought out of borrowed

money. However, notwithstanding the fact that there is an economic difference between leasing

and borrowing to purchase an asset, (take for example leasing a brand car for six years), in that

case the amount that would be reflected in the application of AAB 16B would be depicting the

economic decisions that were made. Less liabilities and assets will be captured in the balance

sheet, as opposed to when the company would have made a decision to borrow money to

purchase the car. In this case, the entitlement of use of the car for six years would be different

from the entitlement that it would have were it to borrow in order to purchase the car

(Firth&Gounopoulos2017).

At the same time, applying AASB 16, the amount that would be captured is more likely to differ

from the amount that would be recognized in borrowing the asset. Borrowing to buy assets and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES 8

leasing accounts normally would show a big difference in the application of AASB 16. IASB

agrees that analysis’s and investors are interested in this comparison. In the application of AASB

16, companies that specialize in leasing assets and those that would borrow in order to purchase

assets normally do not report equal amounts in their balance sheets. This means that the amount

that would be realized if an asset were leased would be different from the amount that would be

realized if the same asset were bought. This is because the money that is paid for leasing the item

excludes what is called ‘residual value’ that is normally attached to an asset that is leased when

the lease comes to an end. IASB recognizes that leasing and borrowing to purchase an asset are

different transactions, although economically they may be similar (De George, Ferguson&Spear

2012).

Recognition of liabilities and assets that come as a result of leasing enhances comparison

between companies that specialize in leasing assets and those that specialize in borrowing to buy

assets, while at the same time considering the differences in economy that is involved between

the transactions.

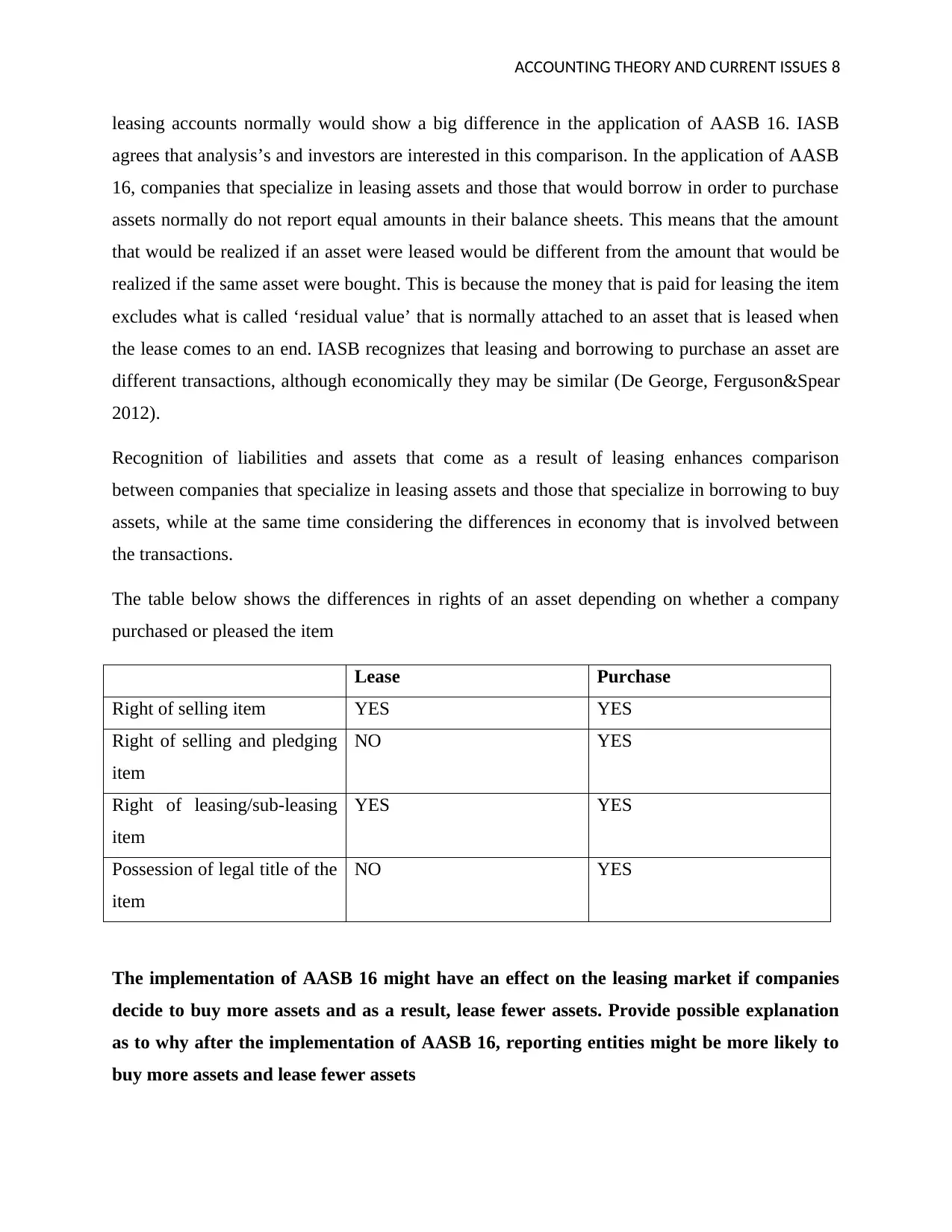

The table below shows the differences in rights of an asset depending on whether a company

purchased or pleased the item

Lease Purchase

Right of selling item YES YES

Right of selling and pledging

item

NO YES

Right of leasing/sub-leasing

item

YES YES

Possession of legal title of the

item

NO YES

The implementation of AASB 16 might have an effect on the leasing market if companies

decide to buy more assets and as a result, lease fewer assets. Provide possible explanation

as to why after the implementation of AASB 16, reporting entities might be more likely to

buy more assets and lease fewer assets

leasing accounts normally would show a big difference in the application of AASB 16. IASB

agrees that analysis’s and investors are interested in this comparison. In the application of AASB

16, companies that specialize in leasing assets and those that would borrow in order to purchase

assets normally do not report equal amounts in their balance sheets. This means that the amount

that would be realized if an asset were leased would be different from the amount that would be

realized if the same asset were bought. This is because the money that is paid for leasing the item

excludes what is called ‘residual value’ that is normally attached to an asset that is leased when

the lease comes to an end. IASB recognizes that leasing and borrowing to purchase an asset are

different transactions, although economically they may be similar (De George, Ferguson&Spear

2012).

Recognition of liabilities and assets that come as a result of leasing enhances comparison

between companies that specialize in leasing assets and those that specialize in borrowing to buy

assets, while at the same time considering the differences in economy that is involved between

the transactions.

The table below shows the differences in rights of an asset depending on whether a company

purchased or pleased the item

Lease Purchase

Right of selling item YES YES

Right of selling and pledging

item

NO YES

Right of leasing/sub-leasing

item

YES YES

Possession of legal title of the

item

NO YES

The implementation of AASB 16 might have an effect on the leasing market if companies

decide to buy more assets and as a result, lease fewer assets. Provide possible explanation

as to why after the implementation of AASB 16, reporting entities might be more likely to

buy more assets and lease fewer assets

ACCOUNTING THEORY AND CURRENT ISSUES 9

AASB 16 has made company comparability easier. Therefore, most reporting companies have

come to realize that it is less costly to borrow so as to buy assets as opposed to leasing assets.

With the adoption of the new standard of leasing, AASB 16, it will be easier to compare the

financial implications for companies that seek to borrow to buy assets and those that specialize in

leasingassets. Economically, leasing an asset would be considered equal to borrowing cash to

purchase an asset. It has been reported that applying AASB 16, the amount that would be

reported when leasing an asset is not so much different from the amount that would be realized

when borrowing to buy the same asset. The reason why reporting entities would be more ready

to purchase assets as opposed to leasing is because with the introduction of AASB 16, it will be

easier for the reporting entities to realize that there is no much economic difference when leasing

assets as when borrowing to purchase assets. Furthermore, AASB 16 removes all the obligations

of the lessees in terms of having to take liability for any damages done to the leased items.

However, still the cost of acquiring and maintaining leased items is more than that of borrowing

cash to purchase assets (Nethercott&Anamourlis2009).

Applying AASB 16, the notable differences that would be seen in the portfolios for leasing will

be captured in the amount that would be seen in the balance sheet. Therefore, application of

AASB 16 will be contribute greatly to the profitability of the reporting companies when they will

decide to borrow to purchase assets than when they will only be leasing. Application of AASB

16 changes the economic status of a company and this is depicted in the balance sheet (Xu,

Davidson, and Cheong, 2017). AASB 117 could not do that since it considered operational

expenses to be equal to the financial expenses. However, AASB 16 removes all these

redundancies, and therefore makes it easier for reporting companies to make comparisons items

of financial expenses, to reach the fact that it is actually cheaper to borrow to purchase assets as

opposed to leasing assets

The IASB expects that at this time, sales transactions and leaseback agreements shall reduce

drastically with the implementation of this current leasing standard. Additionally with the

implementation of AAS 16, it would be easier to measure the liabilities for projection of lease

payments in the future. Therefore, this will make it easier for companies to make comparisons

and projections more easily. The nature of the AASB 16 is indeed to encourage borrowing to

purchase assets as opposed to leasing (Carey, Potter&Tanewski2014).

AASB 16 has made company comparability easier. Therefore, most reporting companies have

come to realize that it is less costly to borrow so as to buy assets as opposed to leasing assets.

With the adoption of the new standard of leasing, AASB 16, it will be easier to compare the

financial implications for companies that seek to borrow to buy assets and those that specialize in

leasingassets. Economically, leasing an asset would be considered equal to borrowing cash to

purchase an asset. It has been reported that applying AASB 16, the amount that would be

reported when leasing an asset is not so much different from the amount that would be realized

when borrowing to buy the same asset. The reason why reporting entities would be more ready

to purchase assets as opposed to leasing is because with the introduction of AASB 16, it will be

easier for the reporting entities to realize that there is no much economic difference when leasing

assets as when borrowing to purchase assets. Furthermore, AASB 16 removes all the obligations

of the lessees in terms of having to take liability for any damages done to the leased items.

However, still the cost of acquiring and maintaining leased items is more than that of borrowing

cash to purchase assets (Nethercott&Anamourlis2009).

Applying AASB 16, the notable differences that would be seen in the portfolios for leasing will

be captured in the amount that would be seen in the balance sheet. Therefore, application of

AASB 16 will be contribute greatly to the profitability of the reporting companies when they will

decide to borrow to purchase assets than when they will only be leasing. Application of AASB

16 changes the economic status of a company and this is depicted in the balance sheet (Xu,

Davidson, and Cheong, 2017). AASB 117 could not do that since it considered operational

expenses to be equal to the financial expenses. However, AASB 16 removes all these

redundancies, and therefore makes it easier for reporting companies to make comparisons items

of financial expenses, to reach the fact that it is actually cheaper to borrow to purchase assets as

opposed to leasing assets

The IASB expects that at this time, sales transactions and leaseback agreements shall reduce

drastically with the implementation of this current leasing standard. Additionally with the

implementation of AAS 16, it would be easier to measure the liabilities for projection of lease

payments in the future. Therefore, this will make it easier for companies to make comparisons

and projections more easily. The nature of the AASB 16 is indeed to encourage borrowing to

purchase assets as opposed to leasing (Carey, Potter&Tanewski2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING THEORY AND CURRENT ISSUES 10

Select the latest financial year report of an ASX listed company. Summarize the key

disclosures the company has made on its accounting for leases including on the transitional

provision and effect of the transition of AASB 16 from AASB 117.

Financial year report for Air New Zealand Limitedfor the year 2017 2018

Disclosures

Balance Sheet

In comparison with AASB 117, increasing the leasing liabilities and the assets led to a 5%

increase in the profit margin. The company has developed an offset balance sheet for leasing,

which has increased its lease assets and finance liability.The amount for carrying leases has been

drastically reduced, with a reduction in the equity when compared to AASB 117.

Assets and Liabilities

The company has reported all its balance sheet leases. In summary, the following can be

observed from the financial statement: Due to the adoption of AASB 16, leased assets applying

AASB 117 on the shares of the upholders has reduced as compared to when AASB 16 was

applied. The IASB projects that the adoption of the AASB 16 is going to improve the

profitability of companies, especially as they get to fully implement the new standard of leasing.

Applying AASB 16, the carrying finances are seen to reduce quickly as opposed to the leasing

liabilities. Furthermore, application of the AASB 16 typically brought down the equity of the

shareholders by 25% (AASB 16, n.d.).

Profit Margin

With the application of the AASB 16, the profit margin before interest and tax considerations are

taken into account is lower than 1 percent for this company.

Cash flow statement

Select the latest financial year report of an ASX listed company. Summarize the key

disclosures the company has made on its accounting for leases including on the transitional

provision and effect of the transition of AASB 16 from AASB 117.

Financial year report for Air New Zealand Limitedfor the year 2017 2018

Disclosures

Balance Sheet

In comparison with AASB 117, increasing the leasing liabilities and the assets led to a 5%

increase in the profit margin. The company has developed an offset balance sheet for leasing,

which has increased its lease assets and finance liability.The amount for carrying leases has been

drastically reduced, with a reduction in the equity when compared to AASB 117.

Assets and Liabilities

The company has reported all its balance sheet leases. In summary, the following can be

observed from the financial statement: Due to the adoption of AASB 16, leased assets applying

AASB 117 on the shares of the upholders has reduced as compared to when AASB 16 was

applied. The IASB projects that the adoption of the AASB 16 is going to improve the

profitability of companies, especially as they get to fully implement the new standard of leasing.

Applying AASB 16, the carrying finances are seen to reduce quickly as opposed to the leasing

liabilities. Furthermore, application of the AASB 16 typically brought down the equity of the

shareholders by 25% (AASB 16, n.d.).

Profit Margin

With the application of the AASB 16, the profit margin before interest and tax considerations are

taken into account is lower than 1 percent for this company.

Cash flow statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING THEORY AND CURRENT ISSUES 11

There is no change observed in the former years, as far as AASB 16 is concerned. Profit for the

year 2018 is seen to be little though. The operational profit margin, and other profit margins are

higher when AASB 16 is applied as opposed to when AASB 117 was applied. The profit realized

in the year ending 2017 is only slightly smaller than the one realized in the following year

because the company held different lease portfolios that start and end in differing years.

Most of the liabilities are assumed, and therefore the portion of the interest is still bigger. This,

compared to the interest that would be accrued when AASB 17 was applied, is far much

profitable. The profit margin with the application of AASB 16 is higher (AASB 16. 2019).

Furthermore, the outflows of the operating cash have increased as compared to that indicated in

the off- balance sheet for operational activities.

AAS 16 provides that the all the expenses that are related to the leases be properly noted down in

the balance sheet. However, AAS 16 requires that provide information in terms of classes, as this

will be important in showing a company’s whole picture of all leasing activities that it conducts.

Interest Cover

The ratio of the interest coverage seems to reduce over the year 2017 approaching 2018. This is

because the company dealt with leases for balance sheets that are of a long term nature. The

effect created in this case can be compared to the effect that comes about when an asset is

purchased through debt financing.

Financial leverage

When applying AASB 117, the debt earnings ratio is seen to be higher than when AASB 16 is

applied. This is because when applying AASB 16, the measurement for earnings includes off

balance expenses that would be related to past leases’ balance sheets where AASB 16 was not

applicable.

Performance

While the profit for operational costs remains to be constant, the capital that is used is seen to be

higher, showing that the company made use of both owned and leased items in its business

operation.

Portfolio Effect

There is no change observed in the former years, as far as AASB 16 is concerned. Profit for the

year 2018 is seen to be little though. The operational profit margin, and other profit margins are

higher when AASB 16 is applied as opposed to when AASB 117 was applied. The profit realized

in the year ending 2017 is only slightly smaller than the one realized in the following year

because the company held different lease portfolios that start and end in differing years.

Most of the liabilities are assumed, and therefore the portion of the interest is still bigger. This,

compared to the interest that would be accrued when AASB 17 was applied, is far much

profitable. The profit margin with the application of AASB 16 is higher (AASB 16. 2019).

Furthermore, the outflows of the operating cash have increased as compared to that indicated in

the off- balance sheet for operational activities.

AAS 16 provides that the all the expenses that are related to the leases be properly noted down in

the balance sheet. However, AAS 16 requires that provide information in terms of classes, as this

will be important in showing a company’s whole picture of all leasing activities that it conducts.

Interest Cover

The ratio of the interest coverage seems to reduce over the year 2017 approaching 2018. This is

because the company dealt with leases for balance sheets that are of a long term nature. The

effect created in this case can be compared to the effect that comes about when an asset is

purchased through debt financing.

Financial leverage

When applying AASB 117, the debt earnings ratio is seen to be higher than when AASB 16 is

applied. This is because when applying AASB 16, the measurement for earnings includes off

balance expenses that would be related to past leases’ balance sheets where AASB 16 was not

applicable.

Performance

While the profit for operational costs remains to be constant, the capital that is used is seen to be

higher, showing that the company made use of both owned and leased items in its business

operation.

Portfolio Effect

ACCOUNTING THEORY AND CURRENT ISSUES 12

The lease portfolio for the company is distributed uniformly, and there is no difference after the

interest is deprecated. Comparing with the lease portfolio whenAASB 16 is applied, there is a

notable difference. However, the range of the lease discount has fallen drastically, as indicated

by the large depreciation noted. It is clear that the company has depicted a starting point in the

portfolios that is distributed evenly. The lease assets have depreciated a lot, and when AASB 16

is applied, the off-balance expenses drastically decrease.

Applying AASB 16, the expenses in total of the portfolios of the leases amounts to almost 10 %,

a percentage that is lower when applying AASB 117.

Additional Disclosures

AASB 16 provides that a company is required to provide the residualvalue for its assets and

liabilities.

Conclusion

AASB 16 suspends AASB 117, and there are a number of advantages that come with it. The

effects of AASB 16 have been discussed, and the various considerations of the new leasing

standard have been considered too. The most notable impact of this new requirement is the

increment of both financial liabilities and leasing assets.

The lease portfolio for the company is distributed uniformly, and there is no difference after the

interest is deprecated. Comparing with the lease portfolio whenAASB 16 is applied, there is a

notable difference. However, the range of the lease discount has fallen drastically, as indicated

by the large depreciation noted. It is clear that the company has depicted a starting point in the

portfolios that is distributed evenly. The lease assets have depreciated a lot, and when AASB 16

is applied, the off-balance expenses drastically decrease.

Applying AASB 16, the expenses in total of the portfolios of the leases amounts to almost 10 %,

a percentage that is lower when applying AASB 117.

Additional Disclosures

AASB 16 provides that a company is required to provide the residualvalue for its assets and

liabilities.

Conclusion

AASB 16 suspends AASB 117, and there are a number of advantages that come with it. The

effects of AASB 16 have been discussed, and the various considerations of the new leasing

standard have been considered too. The most notable impact of this new requirement is the

increment of both financial liabilities and leasing assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.