Impact of AASB 16 Leases on Financial Statements: A Report

VerifiedAdded on 2023/01/20

|11

|741

|60

Report

AI Summary

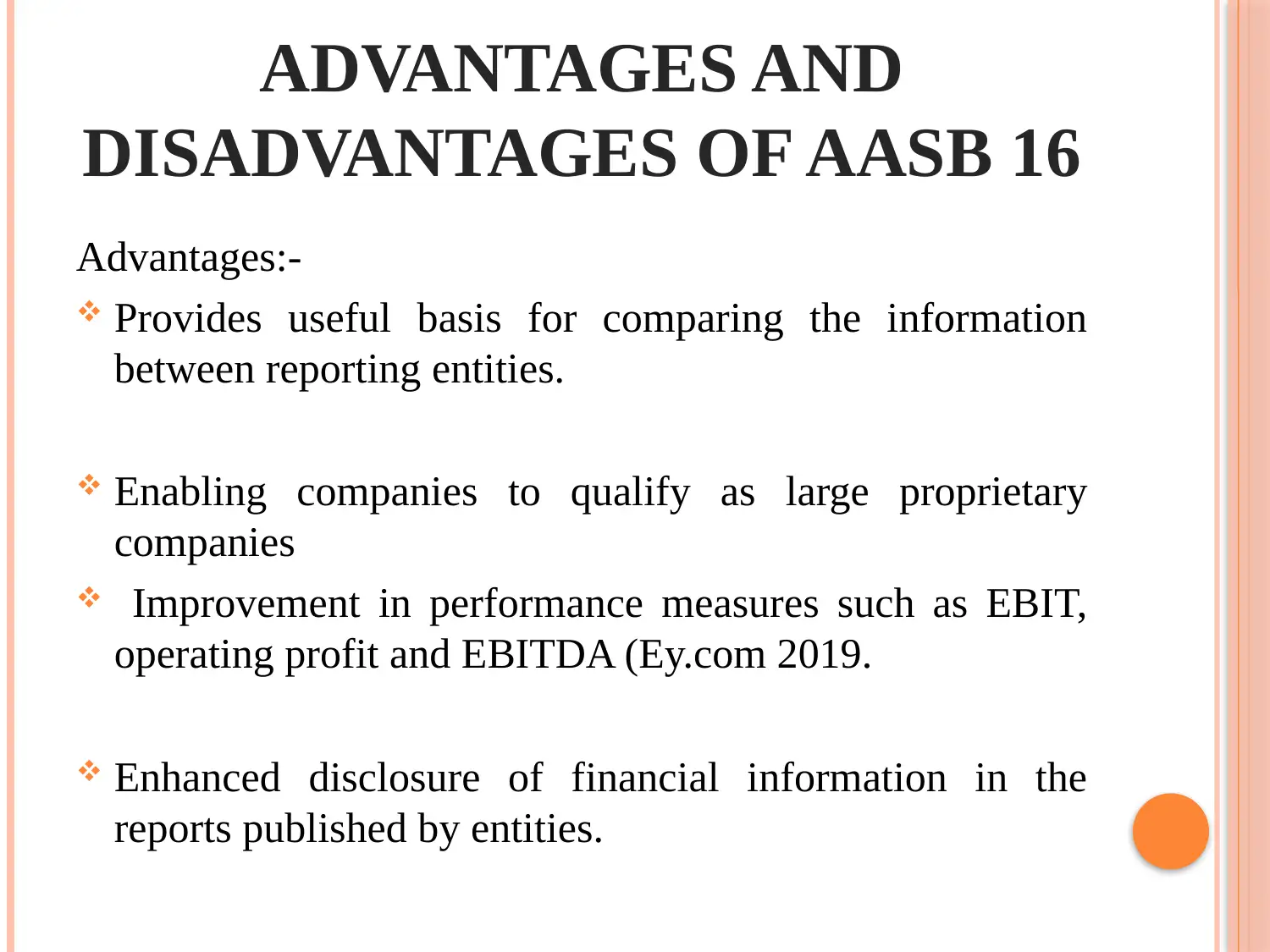

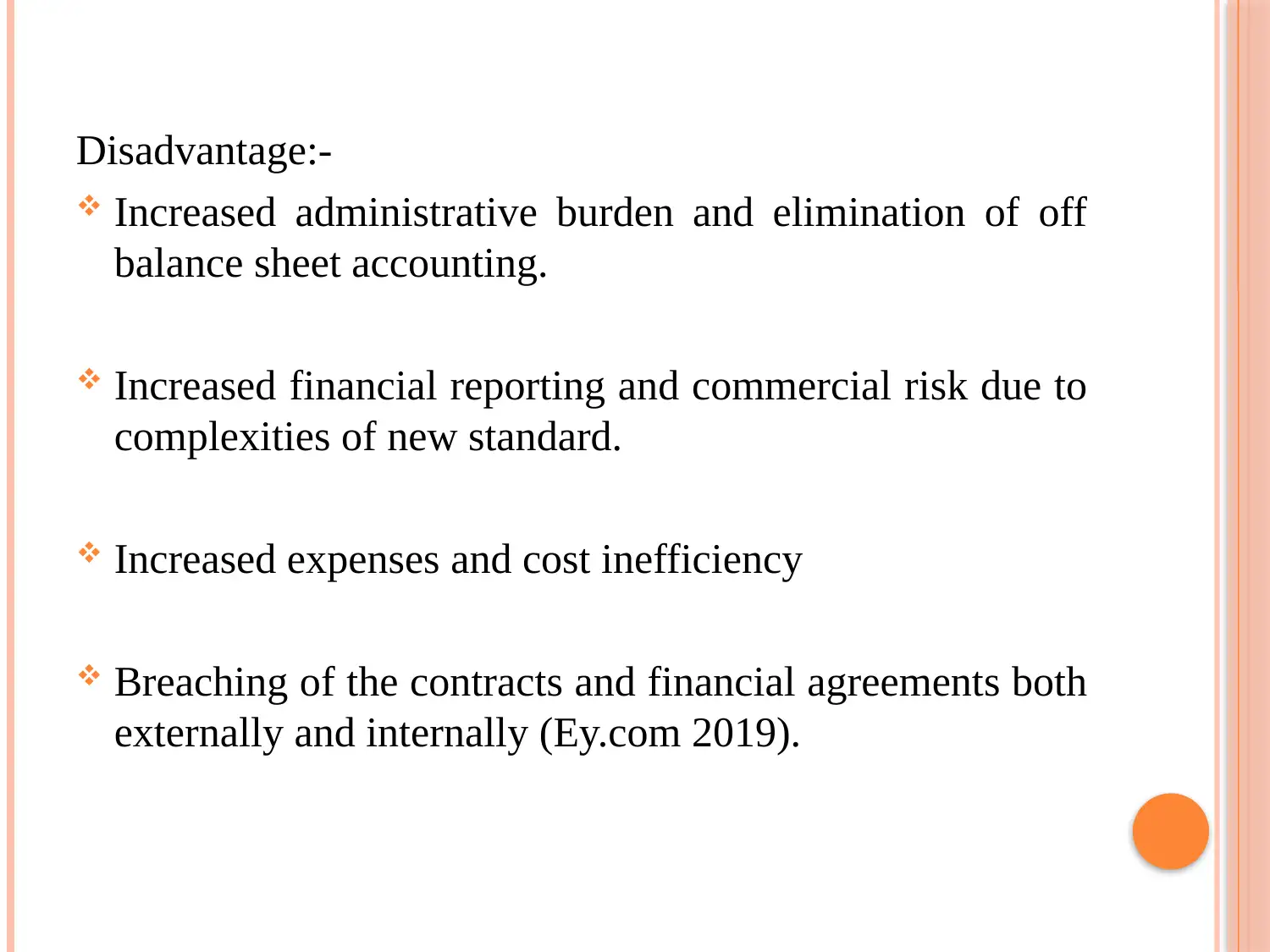

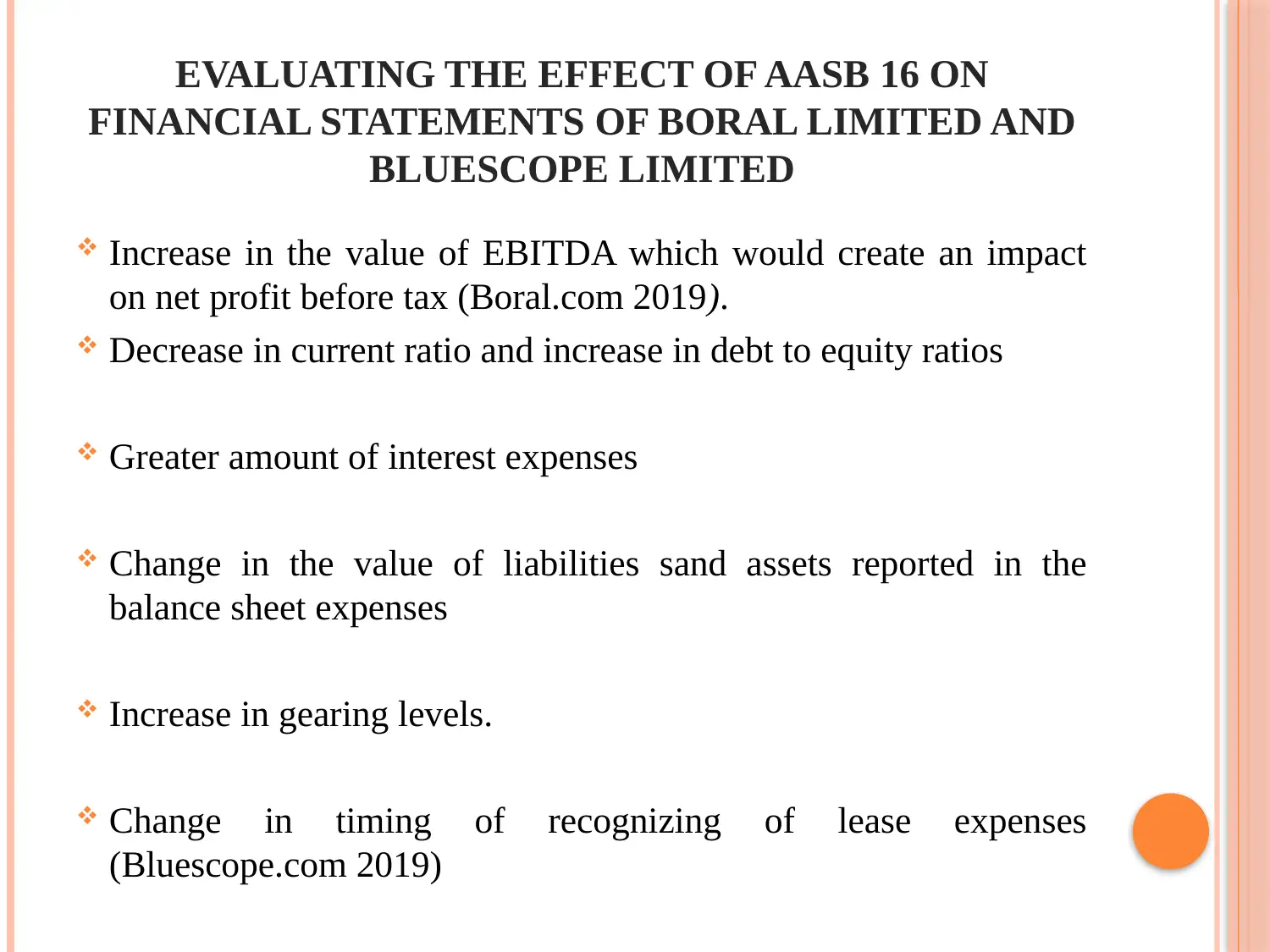

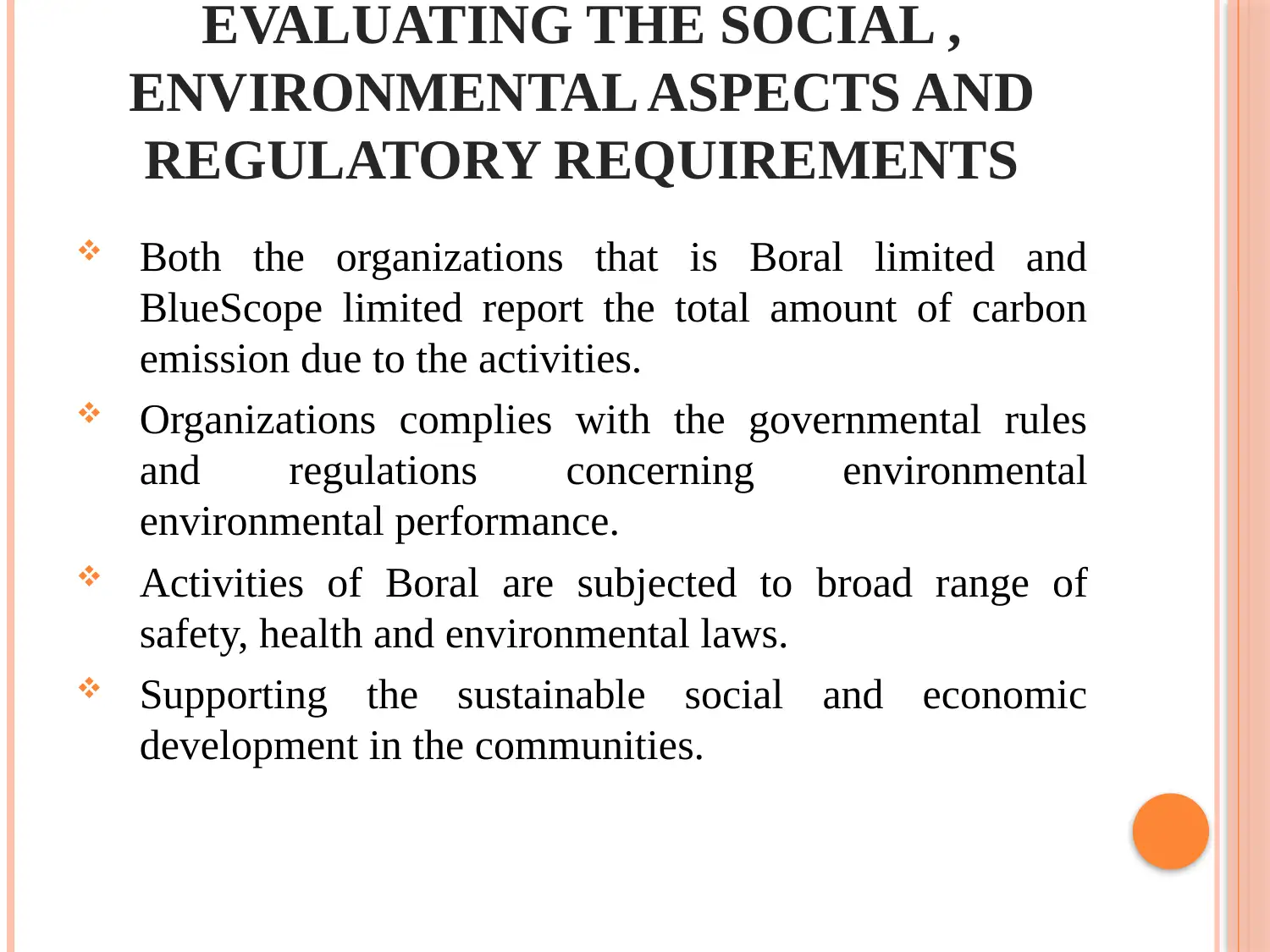

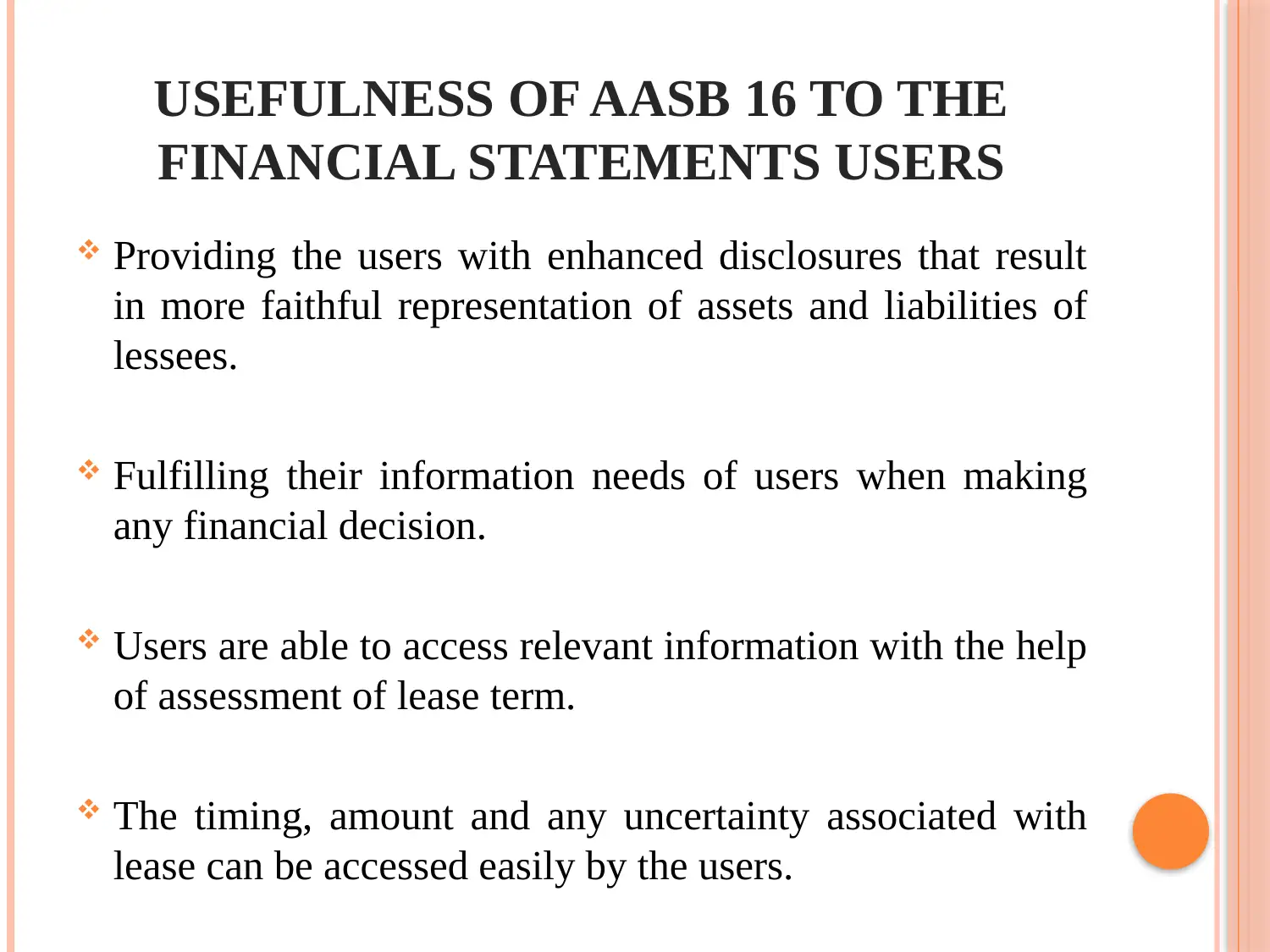

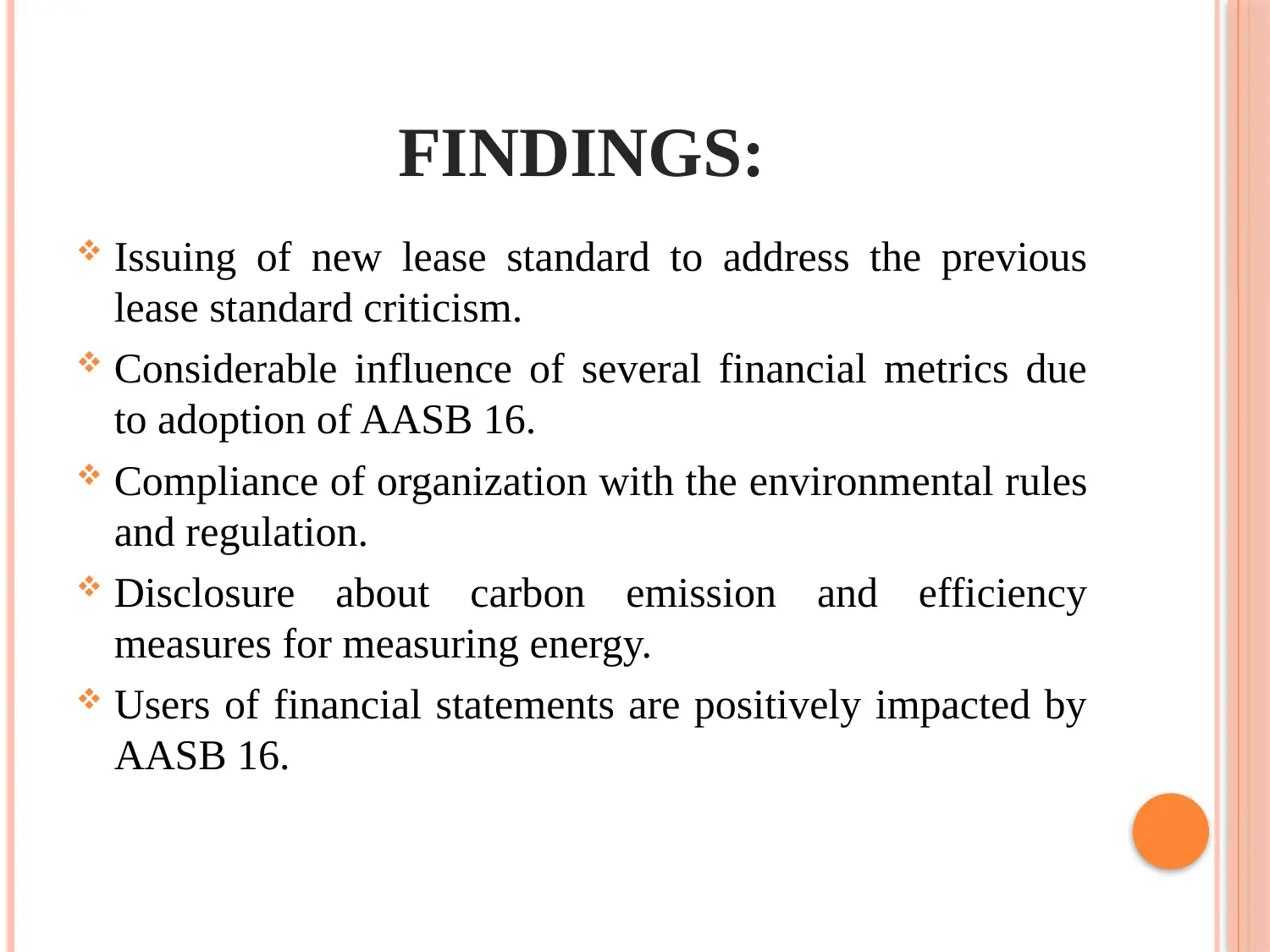

This report examines the new lease standard AASB 16, which addresses criticisms of the previous IAS 17 standard. It details the reasons behind AASB 16's introduction, including providing relevant financial information and a suitable basis for assessing financial performance. The report evaluates the implications of AASB 16, such as the increase in assets and liabilities, and the elimination of the distinction between operating and financial leases. It analyzes the advantages and disadvantages of the standard, including improved performance measures and increased administrative burdens. The report assesses the impact of AASB 16 on the financial statements of Boral Limited and BlueScope Limited, specifically focusing on changes in EBITDA, debt-to-equity ratios, and gearing levels. Additionally, it evaluates the social, environmental aspects, and regulatory requirements of these organizations, including carbon emission reporting and compliance with environmental laws. The report concludes by highlighting the usefulness of AASB 16 to financial statement users, emphasizing enhanced disclosures and access to relevant information for decision-making.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.