AASB 16: Analyzing the Impact on Australian Leasing Firms' Financials

VerifiedAdded on 2020/04/21

|11

|2364

|41

Report

AI Summary

This report examines the impact of AASB 16 on Australian leasing firms. The introduction highlights the changes in lease accounting standards and the significance of financial reporting characteristics like relevance and faithful representation. The paper analyzes the implications of AASB 16 on lease reporting, focusing on the recognition of right-of-use assets and lease liabilities, and its effect on key financial metrics such as EBITDA and debt. It discusses the classification of leases (Type A and Type B) and their impact on balance sheets and income statements, including examples of financial statement presentations. The report further explores how the new standards affect business agreements, banking covenants, and dividend planning, as well as the increased expenses and risks associated with leasing. The conclusion emphasizes the importance of AASB 16 in improving the quality and reliability of financial reports, ensuring compliance with financial statement characteristics.

Name of student:

Registration number:

Unit Title:

Unit Code:

Name of Supervisor:

Date due:

Registration number:

Unit Title:

Unit Code:

Name of Supervisor:

Date due:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

This report discusses the impact that the AASB 17 has had on leasing firms in

Australia. The report reviews and critically analyzes the article by Churyk, Reinstein

and Lander(2015). The fundamental characteristics of financial information include a

variety of qualitative aspects that a firm should meet to be considered to have fulfilled

the requirements of AASB. The paper analyzes the impact of the AASB 17 standard

on lease on Australian firms. This is because many lease obligations are not recorded

on the balance sheet and the current accounting for leases does not adequately

represent the economics of lease transactions. The characteristics of financial

reporting that the changes on lease standards are based on include; relevance and

faithful representation of information (Hancock, Bazley& Robinson, 2015). The paper

also discusses how the application of the new standards on leases is expected to affect

lease reporting and business agreement between the lesser and the lessee. The paper

also evaluates whether the implementation of the standards complies with the

financial reporting characteristics identified above.

The two fundamental characteristics of financial statements as stated in the

framework are; relevance and faithful representation. The characteristic of relevance

states that the information that is generated by an accounting system used by an entity

should impact on decision making by that particular entity (Deegan, 2013). All the

information obtained by an accounting system should be useful to the entity for which

the statements are prepared. It involves both content of the financial information and

its timeliness. Faithful representation is a concept that indicates that financial

information should be produced in an accurate manner and should represent a true and

This report discusses the impact that the AASB 17 has had on leasing firms in

Australia. The report reviews and critically analyzes the article by Churyk, Reinstein

and Lander(2015). The fundamental characteristics of financial information include a

variety of qualitative aspects that a firm should meet to be considered to have fulfilled

the requirements of AASB. The paper analyzes the impact of the AASB 17 standard

on lease on Australian firms. This is because many lease obligations are not recorded

on the balance sheet and the current accounting for leases does not adequately

represent the economics of lease transactions. The characteristics of financial

reporting that the changes on lease standards are based on include; relevance and

faithful representation of information (Hancock, Bazley& Robinson, 2015). The paper

also discusses how the application of the new standards on leases is expected to affect

lease reporting and business agreement between the lesser and the lessee. The paper

also evaluates whether the implementation of the standards complies with the

financial reporting characteristics identified above.

The two fundamental characteristics of financial statements as stated in the

framework are; relevance and faithful representation. The characteristic of relevance

states that the information that is generated by an accounting system used by an entity

should impact on decision making by that particular entity (Deegan, 2013). All the

information obtained by an accounting system should be useful to the entity for which

the statements are prepared. It involves both content of the financial information and

its timeliness. Faithful representation is a concept that indicates that financial

information should be produced in an accurate manner and should represent a true and

fair condition of the business. The information presented in the statements should be

true and accurate as per the date indicated in the reports. These two characteristics of

financial statement are the backbone of accounting standards and rules.

The AASB 16 standards will begin implementation in the year 2019. The AASB 16 is

a change brought to fill the gaps identified by the IASB on the current standards of

recording leases by companies. The AASB 16 has already been identified as a change

in standards which will have significant impact on the firms. The standards are

expected to affect the asset and liabilities ratio and also to affect the terms of contracts

between lessors and lessees (National Institute of Accountants Australia, 2015)`.

Implementation of the new standards on leases will result to changes in the financial

metrics that are used by various users of financial information. The standards propose

that both the lessee and the lesser should apply an ROU model to account for leases as

well as subleases (CCH Australia Limited, 2013). The lessor and the lessee should

classify whether the lease is Type A or Type B. Type A leases are non-property leases

such as those involving equipment and cars. The type B leases involves property lease

such as land and buildings. In type B lease, the lease term is a very little compared to

the economic value of the asset being leased. The liability of the lessee to pay rent fee

for the leased asset will increase the liability of the lessee. The lessee should

recognize the right of the residual asset for the time in which the lease term lasts. On

the lessors balance sheet, they are required to apportion part of the leased and

recognize any residual asset. The lessor is required to record the right to receive

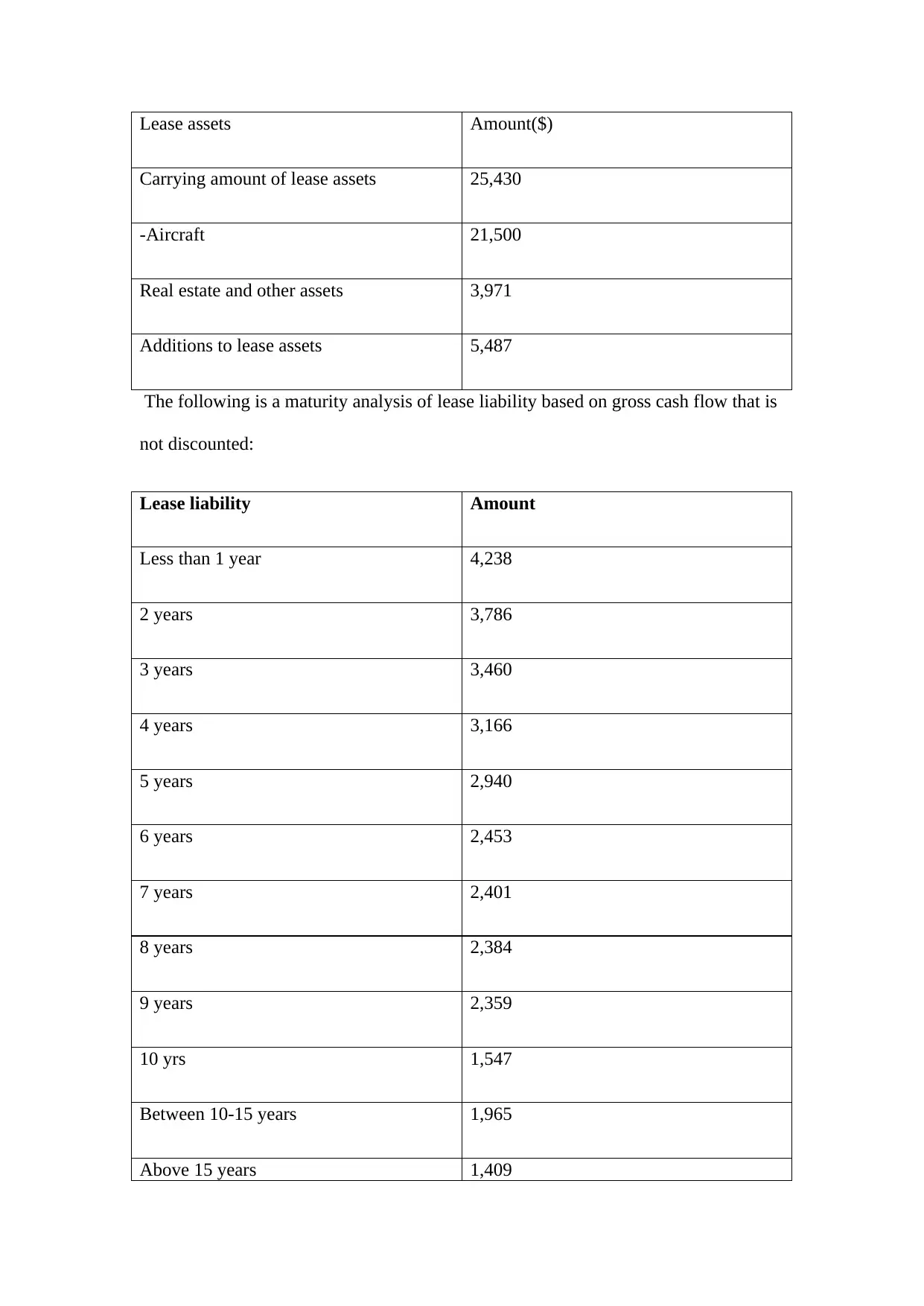

payments to the leased asset as income. The following is a table extracted from IFRS

website showing the presentation and requirement on disclosure under AASB

16;property, plant and equipment is used as an example.

true and accurate as per the date indicated in the reports. These two characteristics of

financial statement are the backbone of accounting standards and rules.

The AASB 16 standards will begin implementation in the year 2019. The AASB 16 is

a change brought to fill the gaps identified by the IASB on the current standards of

recording leases by companies. The AASB 16 has already been identified as a change

in standards which will have significant impact on the firms. The standards are

expected to affect the asset and liabilities ratio and also to affect the terms of contracts

between lessors and lessees (National Institute of Accountants Australia, 2015)`.

Implementation of the new standards on leases will result to changes in the financial

metrics that are used by various users of financial information. The standards propose

that both the lessee and the lesser should apply an ROU model to account for leases as

well as subleases (CCH Australia Limited, 2013). The lessor and the lessee should

classify whether the lease is Type A or Type B. Type A leases are non-property leases

such as those involving equipment and cars. The type B leases involves property lease

such as land and buildings. In type B lease, the lease term is a very little compared to

the economic value of the asset being leased. The liability of the lessee to pay rent fee

for the leased asset will increase the liability of the lessee. The lessee should

recognize the right of the residual asset for the time in which the lease term lasts. On

the lessors balance sheet, they are required to apportion part of the leased and

recognize any residual asset. The lessor is required to record the right to receive

payments to the leased asset as income. The following is a table extracted from IFRS

website showing the presentation and requirement on disclosure under AASB

16;property, plant and equipment is used as an example.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lease assets Amount($)

Carrying amount of lease assets 25,430

-Aircraft 21,500

Real estate and other assets 3,971

Additions to lease assets 5,487

The following is a maturity analysis of lease liability based on gross cash flow that is

not discounted:

Lease liability Amount

Less than 1 year 4,238

2 years 3,786

3 years 3,460

4 years 3,166

5 years 2,940

6 years 2,453

7 years 2,401

8 years 2,384

9 years 2,359

10 yrs 1,547

Between 10-15 years 1,965

Above 15 years 1,409

Carrying amount of lease assets 25,430

-Aircraft 21,500

Real estate and other assets 3,971

Additions to lease assets 5,487

The following is a maturity analysis of lease liability based on gross cash flow that is

not discounted:

Lease liability Amount

Less than 1 year 4,238

2 years 3,786

3 years 3,460

4 years 3,166

5 years 2,940

6 years 2,453

7 years 2,401

8 years 2,384

9 years 2,359

10 yrs 1,547

Between 10-15 years 1,965

Above 15 years 1,409

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

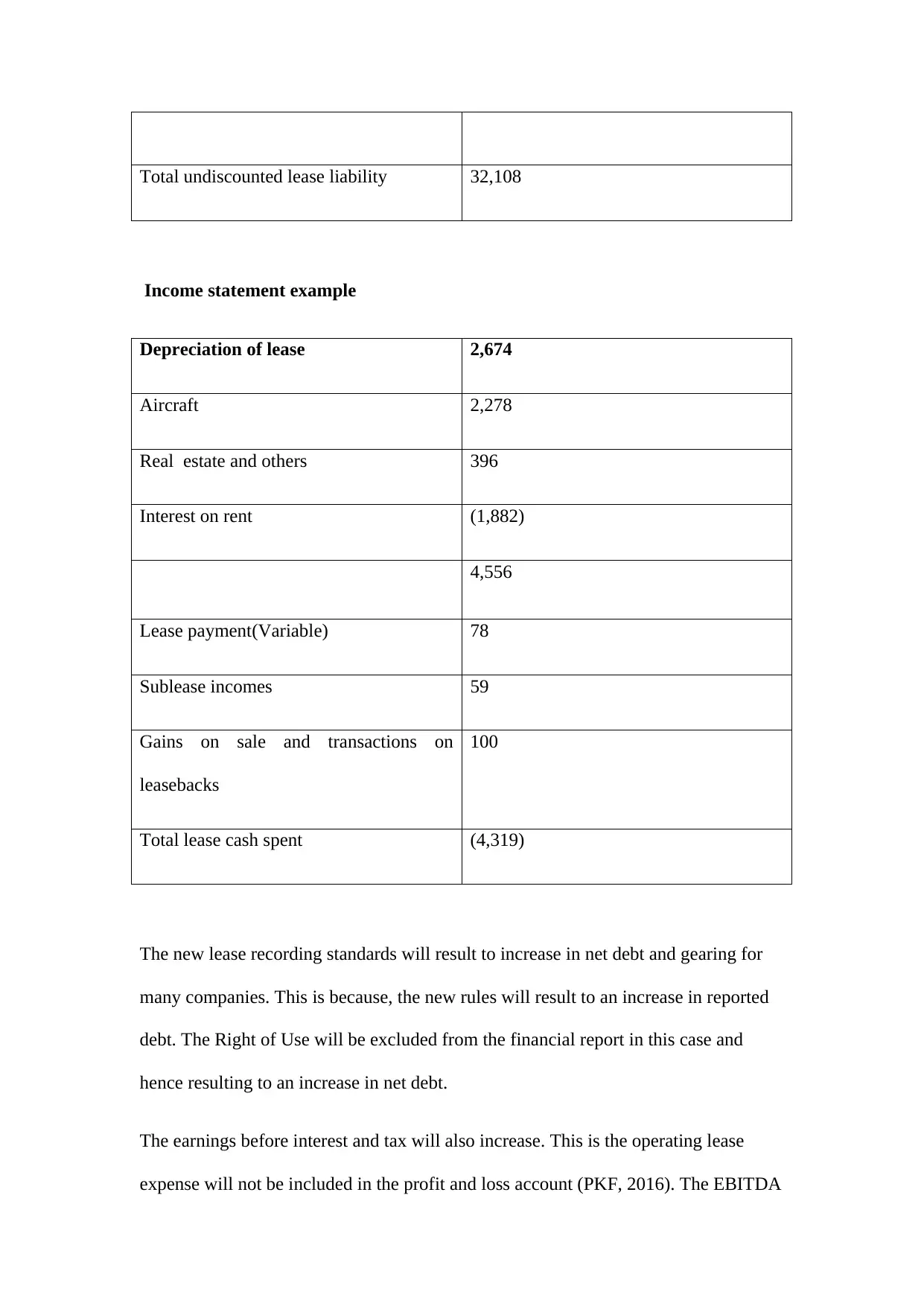

Total undiscounted lease liability 32,108

Income statement example

Depreciation of lease 2,674

Aircraft 2,278

Real estate and others 396

Interest on rent (1,882)

4,556

Lease payment(Variable) 78

Sublease incomes 59

Gains on sale and transactions on

leasebacks

100

Total lease cash spent (4,319)

The new lease recording standards will result to increase in net debt and gearing for

many companies. This is because, the new rules will result to an increase in reported

debt. The Right of Use will be excluded from the financial report in this case and

hence resulting to an increase in net debt.

The earnings before interest and tax will also increase. This is the operating lease

expense will not be included in the profit and loss account (PKF, 2016). The EBITDA

Income statement example

Depreciation of lease 2,674

Aircraft 2,278

Real estate and others 396

Interest on rent (1,882)

4,556

Lease payment(Variable) 78

Sublease incomes 59

Gains on sale and transactions on

leasebacks

100

Total lease cash spent (4,319)

The new lease recording standards will result to increase in net debt and gearing for

many companies. This is because, the new rules will result to an increase in reported

debt. The Right of Use will be excluded from the financial report in this case and

hence resulting to an increase in net debt.

The earnings before interest and tax will also increase. This is the operating lease

expense will not be included in the profit and loss account (PKF, 2016). The EBITDA

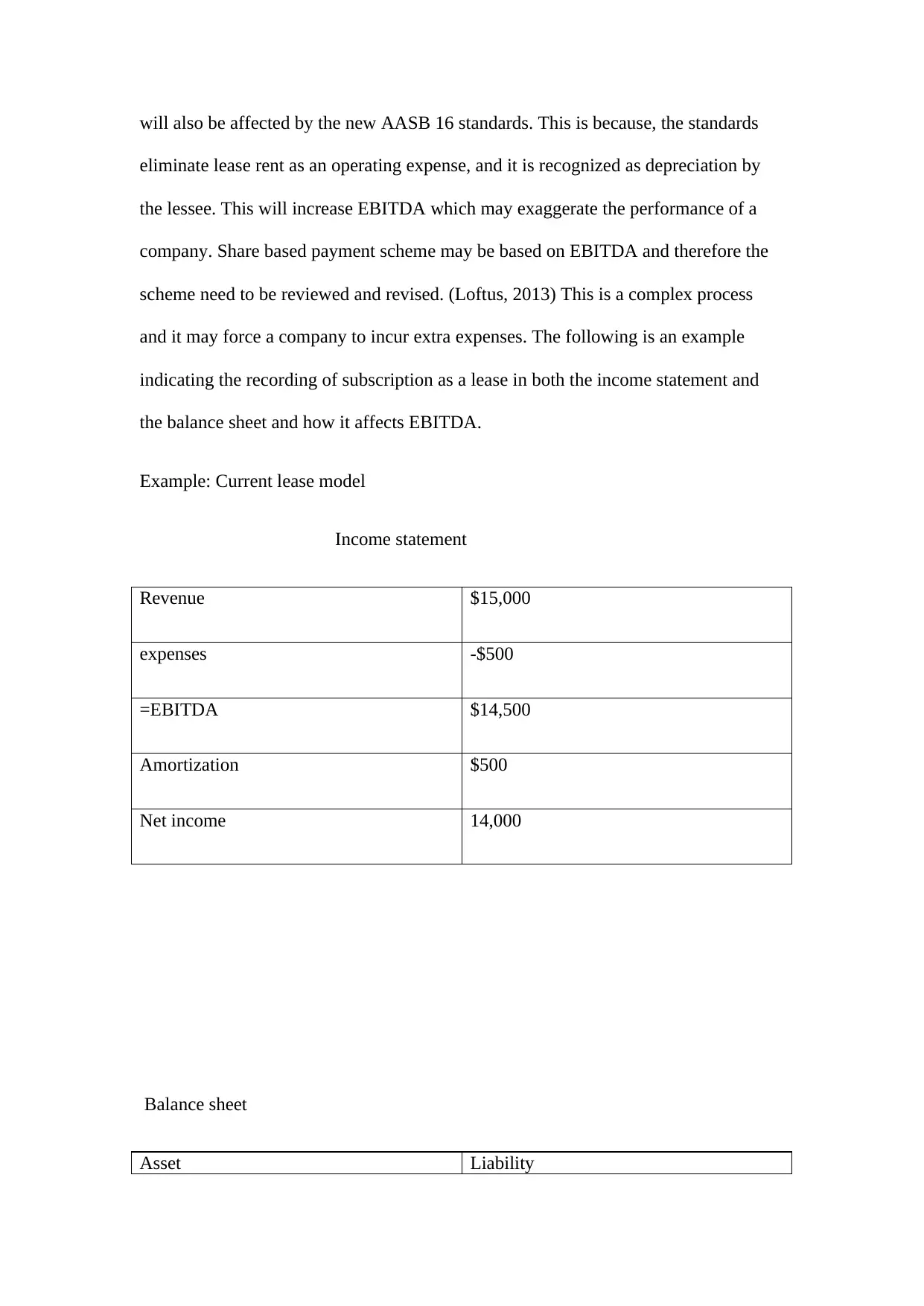

will also be affected by the new AASB 16 standards. This is because, the standards

eliminate lease rent as an operating expense, and it is recognized as depreciation by

the lessee. This will increase EBITDA which may exaggerate the performance of a

company. Share based payment scheme may be based on EBITDA and therefore the

scheme need to be reviewed and revised. (Loftus, 2013) This is a complex process

and it may force a company to incur extra expenses. The following is an example

indicating the recording of subscription as a lease in both the income statement and

the balance sheet and how it affects EBITDA.

Example: Current lease model

Income statement

Revenue $15,000

expenses -$500

=EBITDA $14,500

Amortization $500

Net income 14,000

Balance sheet

Asset Liability

eliminate lease rent as an operating expense, and it is recognized as depreciation by

the lessee. This will increase EBITDA which may exaggerate the performance of a

company. Share based payment scheme may be based on EBITDA and therefore the

scheme need to be reviewed and revised. (Loftus, 2013) This is a complex process

and it may force a company to incur extra expenses. The following is an example

indicating the recording of subscription as a lease in both the income statement and

the balance sheet and how it affects EBITDA.

Example: Current lease model

Income statement

Revenue $15,000

expenses -$500

=EBITDA $14,500

Amortization $500

Net income 14,000

Balance sheet

Asset Liability

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Lease fee -$2000

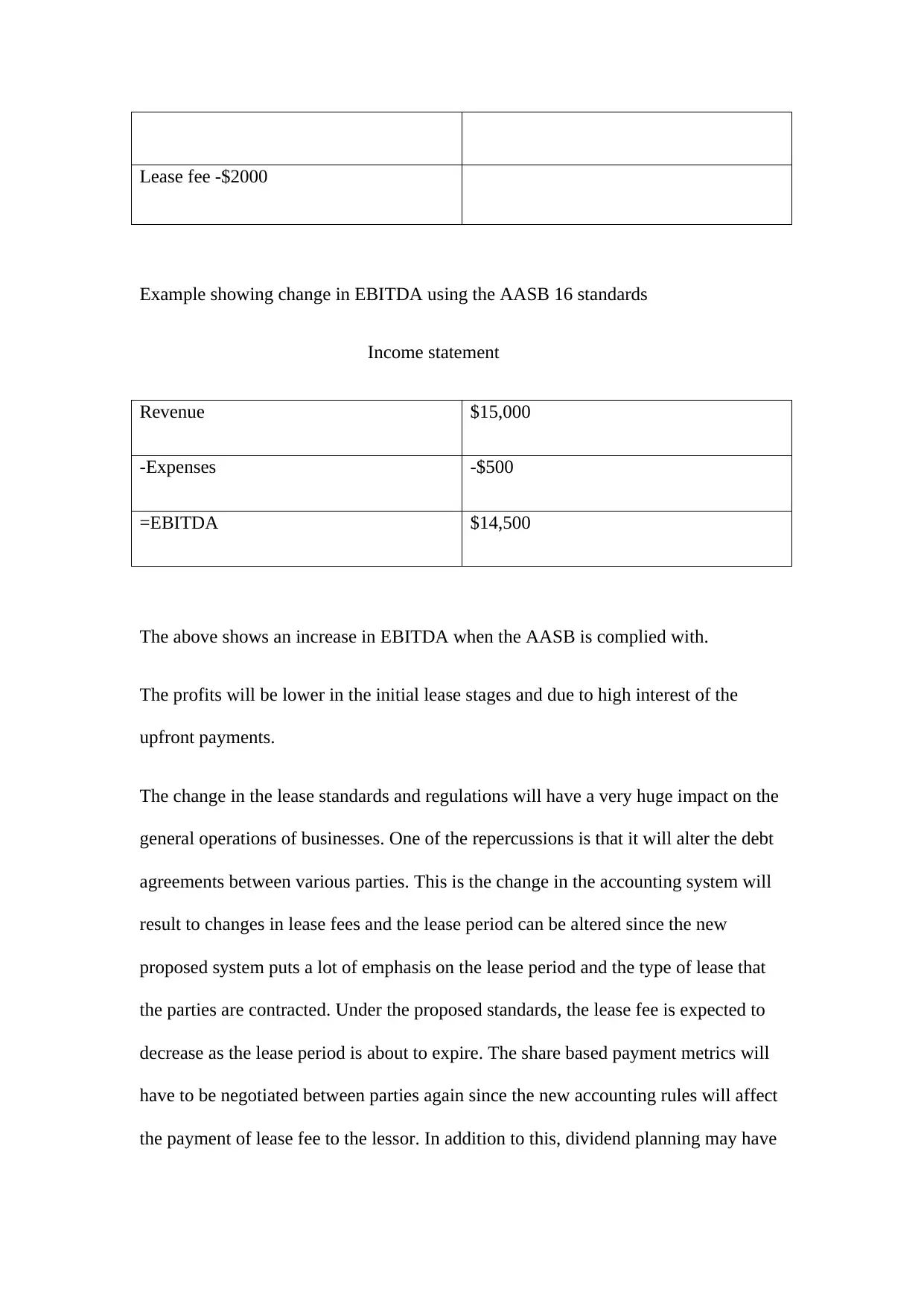

Example showing change in EBITDA using the AASB 16 standards

Income statement

Revenue $15,000

-Expenses -$500

=EBITDA $14,500

The above shows an increase in EBITDA when the AASB is complied with.

The profits will be lower in the initial lease stages and due to high interest of the

upfront payments.

The change in the lease standards and regulations will have a very huge impact on the

general operations of businesses. One of the repercussions is that it will alter the debt

agreements between various parties. This is the change in the accounting system will

result to changes in lease fees and the lease period can be altered since the new

proposed system puts a lot of emphasis on the lease period and the type of lease that

the parties are contracted. Under the proposed standards, the lease fee is expected to

decrease as the lease period is about to expire. The share based payment metrics will

have to be negotiated between parties again since the new accounting rules will affect

the payment of lease fee to the lessor. In addition to this, dividend planning may have

Example showing change in EBITDA using the AASB 16 standards

Income statement

Revenue $15,000

-Expenses -$500

=EBITDA $14,500

The above shows an increase in EBITDA when the AASB is complied with.

The profits will be lower in the initial lease stages and due to high interest of the

upfront payments.

The change in the lease standards and regulations will have a very huge impact on the

general operations of businesses. One of the repercussions is that it will alter the debt

agreements between various parties. This is the change in the accounting system will

result to changes in lease fees and the lease period can be altered since the new

proposed system puts a lot of emphasis on the lease period and the type of lease that

the parties are contracted. Under the proposed standards, the lease fee is expected to

decrease as the lease period is about to expire. The share based payment metrics will

have to be negotiated between parties again since the new accounting rules will affect

the payment of lease fee to the lessor. In addition to this, dividend planning may have

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to change especially among public companies since the income statement and initial

equity will be affected by the new accounting format for leases.

The other impact that the AASB 16 will result to increase in expenses by companies

and hence affect the profit margins of lessee. This is because, the new standards will

increase the risk of leasing and the increase in risk will result to increase in leasing

rates which will end up affecting many industries such as in transport and financial

sector. Banking covenants will also be significantly affected by the AASB 16.This is

because requirements such as complying to specific financial ratios such as

debt/equity ratio will be affected (Klynveld, Marwick, & KPMG, 2015). The costs

which are currently recorded as operating expenses will be recorded as interest

expense when AASB is complied with. The change in calculation of these ratios will

force banks to renegotiate many of their contracts and conflicts may therefore occur

between the parties.

The standards set by AASB 16 require that companies recognize the “right to use”

assets and lease liabilities. This is referred to as operating leases in the current system

of accounting for leases. By recognizing the right to use and lease liability, the

balance sheet may end grossing up and hence affecting the asset base and the debts of

a firm. This may in turn lead to more companies in Australia requiring audit since the

Corporations Act of 2001 firms must meet one of the following three thresholds in

order to be audited; Assets in excess of $12.5m,more than 50 employees and revenue

of $25 million and above (Carmichael, Whittington, Ray& Graham, Lynford, 2012).

Compliance with AASB 16 standards will result to adherence to the two basic

characteristics of financial records which includes relevance and faithful

equity will be affected by the new accounting format for leases.

The other impact that the AASB 16 will result to increase in expenses by companies

and hence affect the profit margins of lessee. This is because, the new standards will

increase the risk of leasing and the increase in risk will result to increase in leasing

rates which will end up affecting many industries such as in transport and financial

sector. Banking covenants will also be significantly affected by the AASB 16.This is

because requirements such as complying to specific financial ratios such as

debt/equity ratio will be affected (Klynveld, Marwick, & KPMG, 2015). The costs

which are currently recorded as operating expenses will be recorded as interest

expense when AASB is complied with. The change in calculation of these ratios will

force banks to renegotiate many of their contracts and conflicts may therefore occur

between the parties.

The standards set by AASB 16 require that companies recognize the “right to use”

assets and lease liabilities. This is referred to as operating leases in the current system

of accounting for leases. By recognizing the right to use and lease liability, the

balance sheet may end grossing up and hence affecting the asset base and the debts of

a firm. This may in turn lead to more companies in Australia requiring audit since the

Corporations Act of 2001 firms must meet one of the following three thresholds in

order to be audited; Assets in excess of $12.5m,more than 50 employees and revenue

of $25 million and above (Carmichael, Whittington, Ray& Graham, Lynford, 2012).

Compliance with AASB 16 standards will result to adherence to the two basic

characteristics of financial records which includes relevance and faithful

representation of information. This is because, the AASB 16 is able to fill the gaps

that exist in the current lease accounting standards. The AASB 16 requires firms to

recognize the right of use and the liability of paying lease fee. Previously the costs of

leasing were recognized as operating expenses under the rent expenses account. In the

new system, the costs of renting will be recorded as interests expenses (Berk,

Harford,Ford, Mollica& Finch, 2013). This will ensure that companies leasing an

asset recognize all the expenses that are incurred by the firms hence ensuring full

compliance with faithful representation of information. The depreciation expenses of

the leased asset also have to be recorded and ensure that as the asset is being used, its

value does not remain constant and hence disclosing all the relevant accounting

information. AASB also requires firms should distinguish leases based on whether the

lessee acquires and consumes a significant portion of the related assets during the

lease period. In this case, land and buildings and other tangible assets are amortized

using the straight line method.

The AASB 16 requires that terms of the lease can only be changed if a significant

change in factors affecting the economic incentive of the lessee occurs. This may

prompt him/her to extend or terminate the contract. The lessee should separate

changes in terms that have been agreed to currently and the terms under the previous

agreement (Camfferman& Zeff, 2015). This is necessary if there are changes in the

rent paid to the lesser and hence increasing the liability of the lessee. The changes

should be immediately recorded in the income statement. By recording these changes,

the standard is in line with the financial records characteristic of relevance and

faithful representation.

that exist in the current lease accounting standards. The AASB 16 requires firms to

recognize the right of use and the liability of paying lease fee. Previously the costs of

leasing were recognized as operating expenses under the rent expenses account. In the

new system, the costs of renting will be recorded as interests expenses (Berk,

Harford,Ford, Mollica& Finch, 2013). This will ensure that companies leasing an

asset recognize all the expenses that are incurred by the firms hence ensuring full

compliance with faithful representation of information. The depreciation expenses of

the leased asset also have to be recorded and ensure that as the asset is being used, its

value does not remain constant and hence disclosing all the relevant accounting

information. AASB also requires firms should distinguish leases based on whether the

lessee acquires and consumes a significant portion of the related assets during the

lease period. In this case, land and buildings and other tangible assets are amortized

using the straight line method.

The AASB 16 requires that terms of the lease can only be changed if a significant

change in factors affecting the economic incentive of the lessee occurs. This may

prompt him/her to extend or terminate the contract. The lessee should separate

changes in terms that have been agreed to currently and the terms under the previous

agreement (Camfferman& Zeff, 2015). This is necessary if there are changes in the

rent paid to the lesser and hence increasing the liability of the lessee. The changes

should be immediately recorded in the income statement. By recording these changes,

the standard is in line with the financial records characteristic of relevance and

faithful representation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusions

AASB 16 was developed to deal with the issues that arise with the current lease

recording standards. These issues are related to revenue recognition for lease rent,

disclosures, and matching expenses to revenues. These issues were found to cause

transactions and reports that did not represent faithful reporting. The AASB 16 is

expected to have a major impact on many firms operations. The new standards are

also expected to affect ratios such as Debt/equity ratio, EBIT, EBITDA, and interest

expense in comparison to the profit. The change in the calculation of these ratios will

affect users of financial information such as creditors and investors. Compliance to

the AASB 16 is likely to result o breaking of covenant related to banking and the

renegotiation of these covenants is costly and may lead to extra expenses and sour

relations between parties. Compliance with the AASB 16 will ensure that firms

comply with the basic characteristics of financial statements which include relevance

and faithful representation. This in turn improves the quality and reliability of

financial reports in general.

References

AASB 16 was developed to deal with the issues that arise with the current lease

recording standards. These issues are related to revenue recognition for lease rent,

disclosures, and matching expenses to revenues. These issues were found to cause

transactions and reports that did not represent faithful reporting. The AASB 16 is

expected to have a major impact on many firms operations. The new standards are

also expected to affect ratios such as Debt/equity ratio, EBIT, EBITDA, and interest

expense in comparison to the profit. The change in the calculation of these ratios will

affect users of financial information such as creditors and investors. Compliance to

the AASB 16 is likely to result o breaking of covenant related to banking and the

renegotiation of these covenants is costly and may lead to extra expenses and sour

relations between parties. Compliance with the AASB 16 will ensure that firms

comply with the basic characteristics of financial statements which include relevance

and faithful representation. This in turn improves the quality and reliability of

financial reports in general.

References

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Berk, ., Al, J. E., Harford, J., Ford, G., Mollica, V., & Finch, N. (2013).

Fundamentals of Corporate Finance. Sydney: P.Ed Australia.

Camfferman, K., & Zeff, S. A. (2015). Aiming for global accounting standards: The

International Accounting Standards Board, 2001-2011.

Carmichael, D.R., Whittington, O. Ray., & Graham, Lynford. (2012). Accountants'

Handbook, Financial Accounting and General Topics. John Wiley &

Sons Inc.

CCH Australia Limited,. (2013). Australian superannuation legislation.

Deegan, C. M. (2013). Financial Accounting theory. North Ryde: McGraw-Hill

Education.

Hancock, P., Bazley, M. E., & Robinson, P. (2015). Contemporary accounting: A

strategic approach for users.

Klynveld Peat Marwick Goerdeler., & KPMG International Standards Group. (2015).

Insights into IFRS: KPMG's practical guide to International Financial

Reporting Standards.

Loftus, J. (2013). Understanding Australian accounting standards. Milton, Qld: John

Wiley and Sons.

National Institute of Accountants (Australia). (2015). Corporate accounting and

reporting: A practical approach. Frenchs Forest, N.S.W: Pearson

Education Australia.

PKF, I. (2016). Wiley IFRS 2016: Interpretation and Application of International

Financial Reporting Standards.

Fundamentals of Corporate Finance. Sydney: P.Ed Australia.

Camfferman, K., & Zeff, S. A. (2015). Aiming for global accounting standards: The

International Accounting Standards Board, 2001-2011.

Carmichael, D.R., Whittington, O. Ray., & Graham, Lynford. (2012). Accountants'

Handbook, Financial Accounting and General Topics. John Wiley &

Sons Inc.

CCH Australia Limited,. (2013). Australian superannuation legislation.

Deegan, C. M. (2013). Financial Accounting theory. North Ryde: McGraw-Hill

Education.

Hancock, P., Bazley, M. E., & Robinson, P. (2015). Contemporary accounting: A

strategic approach for users.

Klynveld Peat Marwick Goerdeler., & KPMG International Standards Group. (2015).

Insights into IFRS: KPMG's practical guide to International Financial

Reporting Standards.

Loftus, J. (2013). Understanding Australian accounting standards. Milton, Qld: John

Wiley and Sons.

National Institute of Accountants (Australia). (2015). Corporate accounting and

reporting: A practical approach. Frenchs Forest, N.S.W: Pearson

Education Australia.

PKF, I. (2016). Wiley IFRS 2016: Interpretation and Application of International

Financial Reporting Standards.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.