Analyzing AASB 16 Leases: Impact on Wesfarmers Limited Reporting

VerifiedAdded on 2023/04/21

|10

|2725

|179

Essay

AI Summary

This essay provides a comprehensive review of the new lease standard AASB 16 and its impact on Wesfarmers Limited's financial reporting. It examines the differences between AASB 16 and AASB 117, focusing on how Wesfarmers will need to report lease liabilities and right-of-use assets on its balance sheet. The analysis covers the short-term and long-term impacts on the balance sheet, income statement, and cash flow statement. The essay also discusses the implications of AASB 16 for the Australian retail sector, highlighting changes in financial metrics, dividend policy, and debt agreements. Ultimately, the adoption of AASB 16 aims to enhance financial reporting transparency and provide a more faithful representation of lease transactions for companies like Wesfarmers.

Running head: ADVANCED ISSUED IN ACCOUNTING

Advanced Issued in Accounting

Name of the Student

Name of the University

Author’s Note

Advanced Issued in Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED ISSUED IN ACCOUNTING

Executive Summary

The aim of this essay is to provide the review of the new lease standard AASB 16 along with its impact on various

areas of financial reporting of Wesfarmers Limited. The company will have to report both the lease liabilities and

right-of-use lease assets in the balance sheet along with some additional disclosures under the new lease standard.

These will increase the financial reporting transparency and quality.

Executive Summary

The aim of this essay is to provide the review of the new lease standard AASB 16 along with its impact on various

areas of financial reporting of Wesfarmers Limited. The company will have to report both the lease liabilities and

right-of-use lease assets in the balance sheet along with some additional disclosures under the new lease standard.

These will increase the financial reporting transparency and quality.

2ADVANCED ISSUED IN ACCOUNTING

Introduction

The presence of many sources of financing can be seen for the business organizations and Lease Financing

is considered as one of them. Lease is considered as one of the most important source of medium and long-term

financing where the owner of a particular asset provides another person with the right to use that particular asset

against the periodic payments. The presence of two types of leases can be seen; they are Finance Lease and

Operating Lease. Business organizations have the obligation to follow the AASB lease standards for the accounting

of leases in the companies. In Australia, the companies are needed to comply with the principles and standards of

AASB 117 Leases for the purpose of lease accounting. According to the recent development of the Australian

Accounting Standard Board (AASB), there is the introduction of the new accounting standard for lease that is AASB

16 and all the Australian companies are needed to comply with this new lease standard from January 1, 2019 on

mandatory basis. The main aim of this report is the analysis and evaluation of the different aspects of this new lease

standard along with the existing one. This report also considers the analysis of lease accounting in Wesfarmers and

the impact of new lease standard on the financial statements.

Understanding of the Lease Arrangements

Operating vs. Financial Leases

As per the existing lease standard that is AASB 117, Operating Leases and Financial Leases are the two

types of leases; and the standard puts the obligation for the reporting of finance lease assets and liabilities in the

balance sheet. As per AASB 117, it is needed for the companies to disclose information about the operating leases.

The lessor has the asset ownership for the overall lease term in case of operating lease and the asset ownership stays

with the lessee at the end of the lease term in case of finance leases. However, the main reason for the introduction

of AASB 16 is that AASB 117 does not put the obligation on the companies to report the material amounts of

operating leases in the balance sheet (aasb.gov.au, 2018).

Changes in Lease Accounting Under the New Lease Standard

Certain changes are there in AASB 16 as compared to AASB 117, but the lease accounting for lessors will

remain unaltered. However, the lessees will be needed to adopt a single model for lease accounting. All the lease

contracts will be categorized under leases. The lessees will be required to consider the present value of the lease

liabilities along with the right-of-use assets in the balance sheet, but the short-term leases with owe values are the

exception. After that, as per AASB 116 Property, Plant and Equipment and AASB 136 Impairment of Assets, the

right-of-use assets will be depreciated and impaired respectively. In case of lease liabilities, interest would be

recognized as per AASB 140 Investment Property (aasb.gov.au, 2018). It is needed for both lessor and lessee to

adhere to the disclosure objective instead of rigorous checklists under AASB 16. It is needed for the lessees to report

right-of-use assets characteristically in the balance sheet along with the separate note for them. Separate segregation

is needed for depreciation and interest expenses in the profit and loss statement along with the categorization of the

Introduction

The presence of many sources of financing can be seen for the business organizations and Lease Financing

is considered as one of them. Lease is considered as one of the most important source of medium and long-term

financing where the owner of a particular asset provides another person with the right to use that particular asset

against the periodic payments. The presence of two types of leases can be seen; they are Finance Lease and

Operating Lease. Business organizations have the obligation to follow the AASB lease standards for the accounting

of leases in the companies. In Australia, the companies are needed to comply with the principles and standards of

AASB 117 Leases for the purpose of lease accounting. According to the recent development of the Australian

Accounting Standard Board (AASB), there is the introduction of the new accounting standard for lease that is AASB

16 and all the Australian companies are needed to comply with this new lease standard from January 1, 2019 on

mandatory basis. The main aim of this report is the analysis and evaluation of the different aspects of this new lease

standard along with the existing one. This report also considers the analysis of lease accounting in Wesfarmers and

the impact of new lease standard on the financial statements.

Understanding of the Lease Arrangements

Operating vs. Financial Leases

As per the existing lease standard that is AASB 117, Operating Leases and Financial Leases are the two

types of leases; and the standard puts the obligation for the reporting of finance lease assets and liabilities in the

balance sheet. As per AASB 117, it is needed for the companies to disclose information about the operating leases.

The lessor has the asset ownership for the overall lease term in case of operating lease and the asset ownership stays

with the lessee at the end of the lease term in case of finance leases. However, the main reason for the introduction

of AASB 16 is that AASB 117 does not put the obligation on the companies to report the material amounts of

operating leases in the balance sheet (aasb.gov.au, 2018).

Changes in Lease Accounting Under the New Lease Standard

Certain changes are there in AASB 16 as compared to AASB 117, but the lease accounting for lessors will

remain unaltered. However, the lessees will be needed to adopt a single model for lease accounting. All the lease

contracts will be categorized under leases. The lessees will be required to consider the present value of the lease

liabilities along with the right-of-use assets in the balance sheet, but the short-term leases with owe values are the

exception. After that, as per AASB 116 Property, Plant and Equipment and AASB 136 Impairment of Assets, the

right-of-use assets will be depreciated and impaired respectively. In case of lease liabilities, interest would be

recognized as per AASB 140 Investment Property (aasb.gov.au, 2018). It is needed for both lessor and lessee to

adhere to the disclosure objective instead of rigorous checklists under AASB 16. It is needed for the lessees to report

right-of-use assets characteristically in the balance sheet along with the separate note for them. Separate segregation

is needed for depreciation and interest expenses in the profit and loss statement along with the categorization of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED ISSUED IN ACCOUNTING

following payments in the statement of cash flows; they are payment of cash on lease liabilities under financing

activities, payments for short-term and lower leased assets and adherence to the interest payment on lease liabilities

as per AASB107 Statement of Cash Flows for Interest Paid (aasb.gov.au, 2018). These alterations help to enhance

the quality of financial reporting along with ensuring faithful representation of all the financial transactions for the

leases. All these aspects would lead to more transparency in the process of financial reporting.

Overview of Wesfarmers Limited and Their Leases

Wesfarmers is considered as one of the leading conglomerate companies in Australia and the company is

enlisted in Australian Securities Exchange (ASX). The company was established in the year of 1914 and it is

headquartered at Western Australia. Wesfarmers has a diverse business operation that include the supply of home

improvements department stores, office supplies; and the company also has an industrial division that includes the

business of chemicals, fertilizers, energy, safety products and others. It needs to be mentioned that Wesfarmers is the

largest employer of Australia as the current employee base of the company is more than 100,000; and the company

has a shareholder base of approximately 495,000 (wesfarmers.com.au, 2019). The following discussion shows the

information related to the leases of the business of Wesfarmers.

It can be seen from the 2018 Annual Report of Wesfarmers that the company has both the operating leases

and finance lease; and they use certain judgments for the classification of finance and operating leases. The major

lease assets of the company are office, retail and distribution properties, motor vehicles and office equipment.

Wesfarmers classifies the leases based on whether they hold substantially all the risks and rewards related to the

ownership of lease assets or not. It can be seen from the 2018 Annual Report of Wesfarmers that the company does

not have any finance lease in the year 2018 (wesfarmers.com.au, 2019). The details of the operating lease are shown

below:

following payments in the statement of cash flows; they are payment of cash on lease liabilities under financing

activities, payments for short-term and lower leased assets and adherence to the interest payment on lease liabilities

as per AASB107 Statement of Cash Flows for Interest Paid (aasb.gov.au, 2018). These alterations help to enhance

the quality of financial reporting along with ensuring faithful representation of all the financial transactions for the

leases. All these aspects would lead to more transparency in the process of financial reporting.

Overview of Wesfarmers Limited and Their Leases

Wesfarmers is considered as one of the leading conglomerate companies in Australia and the company is

enlisted in Australian Securities Exchange (ASX). The company was established in the year of 1914 and it is

headquartered at Western Australia. Wesfarmers has a diverse business operation that include the supply of home

improvements department stores, office supplies; and the company also has an industrial division that includes the

business of chemicals, fertilizers, energy, safety products and others. It needs to be mentioned that Wesfarmers is the

largest employer of Australia as the current employee base of the company is more than 100,000; and the company

has a shareholder base of approximately 495,000 (wesfarmers.com.au, 2019). The following discussion shows the

information related to the leases of the business of Wesfarmers.

It can be seen from the 2018 Annual Report of Wesfarmers that the company has both the operating leases

and finance lease; and they use certain judgments for the classification of finance and operating leases. The major

lease assets of the company are office, retail and distribution properties, motor vehicles and office equipment.

Wesfarmers classifies the leases based on whether they hold substantially all the risks and rewards related to the

ownership of lease assets or not. It can be seen from the 2018 Annual Report of Wesfarmers that the company does

not have any finance lease in the year 2018 (wesfarmers.com.au, 2019). The details of the operating lease are shown

below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED ISSUED IN ACCOUNTING

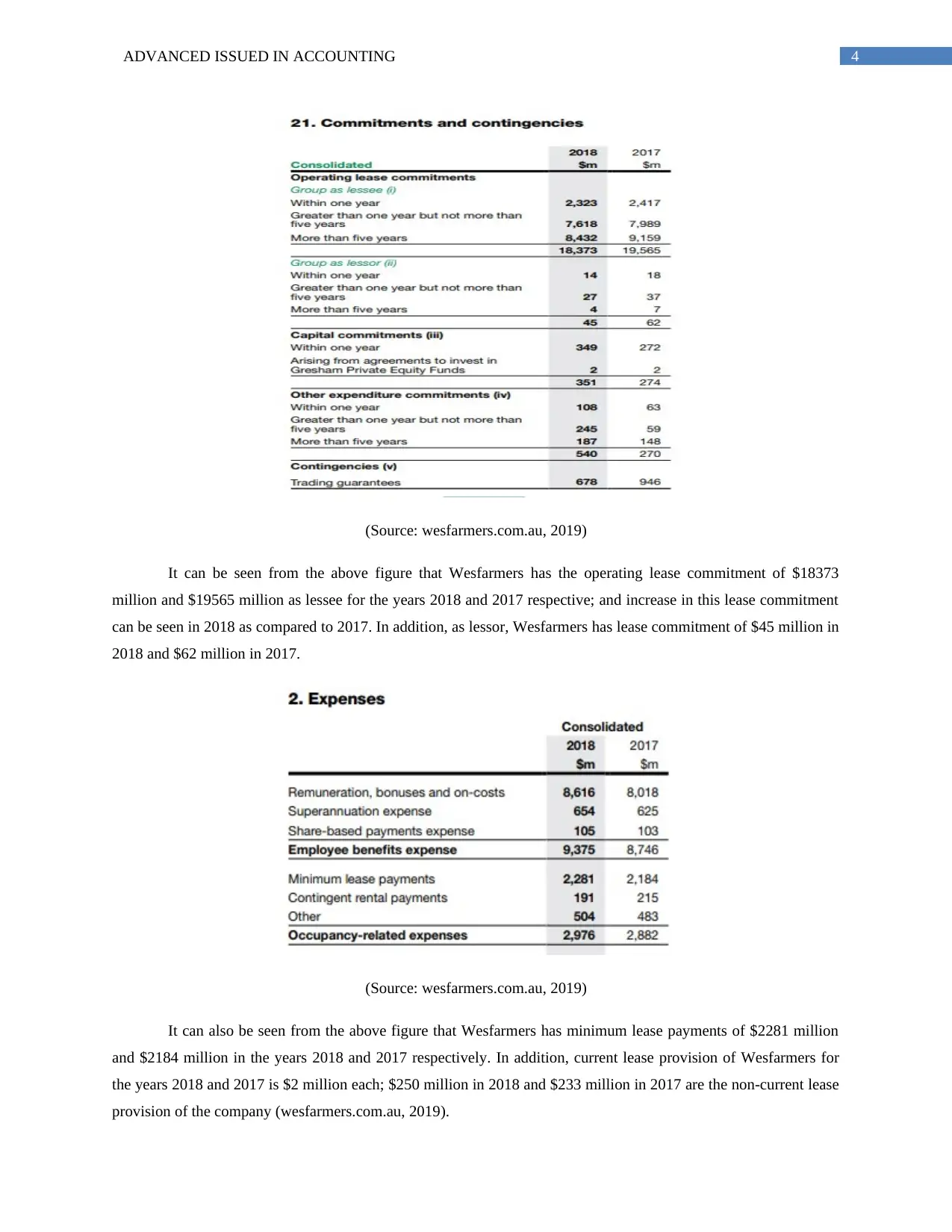

(Source: wesfarmers.com.au, 2019)

It can be seen from the above figure that Wesfarmers has the operating lease commitment of $18373

million and $19565 million as lessee for the years 2018 and 2017 respective; and increase in this lease commitment

can be seen in 2018 as compared to 2017. In addition, as lessor, Wesfarmers has lease commitment of $45 million in

2018 and $62 million in 2017.

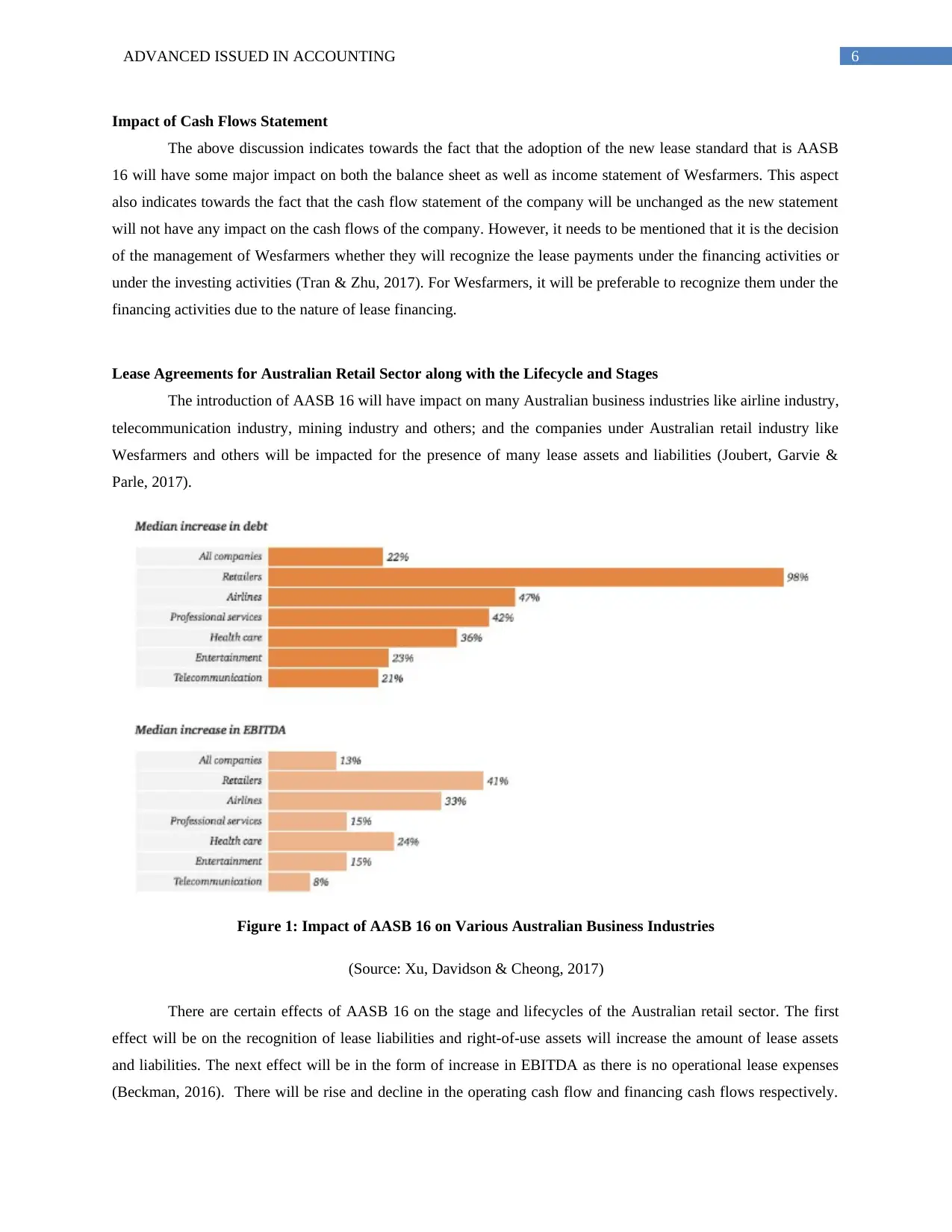

(Source: wesfarmers.com.au, 2019)

It can also be seen from the above figure that Wesfarmers has minimum lease payments of $2281 million

and $2184 million in the years 2018 and 2017 respectively. In addition, current lease provision of Wesfarmers for

the years 2018 and 2017 is $2 million each; $250 million in 2018 and $233 million in 2017 are the non-current lease

provision of the company (wesfarmers.com.au, 2019).

(Source: wesfarmers.com.au, 2019)

It can be seen from the above figure that Wesfarmers has the operating lease commitment of $18373

million and $19565 million as lessee for the years 2018 and 2017 respective; and increase in this lease commitment

can be seen in 2018 as compared to 2017. In addition, as lessor, Wesfarmers has lease commitment of $45 million in

2018 and $62 million in 2017.

(Source: wesfarmers.com.au, 2019)

It can also be seen from the above figure that Wesfarmers has minimum lease payments of $2281 million

and $2184 million in the years 2018 and 2017 respectively. In addition, current lease provision of Wesfarmers for

the years 2018 and 2017 is $2 million each; $250 million in 2018 and $233 million in 2017 are the non-current lease

provision of the company (wesfarmers.com.au, 2019).

5ADVANCED ISSUED IN ACCOUNTING

Impact of AASB 16 on Wesfarmers

It is mentioned in the 2018 Annual Report of Wesfarmers that the adoption of the new lease standards that

is AASB 16 Leases from 1 January 2019 will have certain material impact on the lease accounting of the company.

As per this new lease standard, it will be the obligation on the company to adopt a single lease model where they

will be needed to recognize assets and liabilities related to all leases. Under AASB 16, Wesfarmers will be required

to show the present value of the lease commitments as liability in the balance sheet; they will also be required to

show the right-of-use assets in the asset side of the balance sheet. The continuing classification in the income

statement will be divided between interest expenses and amortization (Joubert, Garvie & Parle, 2017). It needs to be

mentioned that the aim of Wesfarmers is to implement the modified retrospective transition technique as it will

provide the company with the option on lease-by-lease basis to for the calculation of right-of-use assets as either

equal to the lease liability or on the basis of historical lease payment. This techniques does not have any requirement

of restate comparatives (Wong & Joshi, 2015).

Short-term and Long-term Impacts on Lease Accounting

Impact on Balance Sheet

It needs to be mentioned that the adoption of the new lease standard that is AASB 16 will have impact on

the balance sheet of Wesfarmers due to the fact that the company will be needed to report the lease liabilities and

right-to-use assets in the balance sheet. It can be seen from the earlier discussion that Wesfarmers has $18373

million of operating lease commitment in the year 2018; and they will be needed to include the same in the balance

sheet as lease liability. This aspect will increase the liability position of the company that is not a favorable situation

for the companies (Xu, Davidson & Cheong, 2017). It can also be seen from the earlier discussion that Wesfarmers

has $45 million of lease commitments as lessor that they will be needed to include the balance sheet as right-of-use

assets and this will increase the asset position of the company, but will not make any material difference as lease

liability will be raised in large margin.

Impact on Income Statement

In this context, it also needs to be mentioned that the adoption of the new lease standard that is AASB 16

will create certain impact on the income statement of Wesfarmers in the presence of the fact that the company will

have to consider the interest related to the lease assets and liabilities. On a more precise note, there is a possibility

that there will be increase in the operating income of Wesfarmers due to the fact that the company will have to

report the off balance sheet lease asset’s interests (Giner, Merello & Pardo, 2018). At the same time, it will be

required for the company to report the interest expenses related to the lease liabilities as they will have to show this

expense in the company’s income statement. For this reason, the operating income of the company will be affected

with this.

Impact of AASB 16 on Wesfarmers

It is mentioned in the 2018 Annual Report of Wesfarmers that the adoption of the new lease standards that

is AASB 16 Leases from 1 January 2019 will have certain material impact on the lease accounting of the company.

As per this new lease standard, it will be the obligation on the company to adopt a single lease model where they

will be needed to recognize assets and liabilities related to all leases. Under AASB 16, Wesfarmers will be required

to show the present value of the lease commitments as liability in the balance sheet; they will also be required to

show the right-of-use assets in the asset side of the balance sheet. The continuing classification in the income

statement will be divided between interest expenses and amortization (Joubert, Garvie & Parle, 2017). It needs to be

mentioned that the aim of Wesfarmers is to implement the modified retrospective transition technique as it will

provide the company with the option on lease-by-lease basis to for the calculation of right-of-use assets as either

equal to the lease liability or on the basis of historical lease payment. This techniques does not have any requirement

of restate comparatives (Wong & Joshi, 2015).

Short-term and Long-term Impacts on Lease Accounting

Impact on Balance Sheet

It needs to be mentioned that the adoption of the new lease standard that is AASB 16 will have impact on

the balance sheet of Wesfarmers due to the fact that the company will be needed to report the lease liabilities and

right-to-use assets in the balance sheet. It can be seen from the earlier discussion that Wesfarmers has $18373

million of operating lease commitment in the year 2018; and they will be needed to include the same in the balance

sheet as lease liability. This aspect will increase the liability position of the company that is not a favorable situation

for the companies (Xu, Davidson & Cheong, 2017). It can also be seen from the earlier discussion that Wesfarmers

has $45 million of lease commitments as lessor that they will be needed to include the balance sheet as right-of-use

assets and this will increase the asset position of the company, but will not make any material difference as lease

liability will be raised in large margin.

Impact on Income Statement

In this context, it also needs to be mentioned that the adoption of the new lease standard that is AASB 16

will create certain impact on the income statement of Wesfarmers in the presence of the fact that the company will

have to consider the interest related to the lease assets and liabilities. On a more precise note, there is a possibility

that there will be increase in the operating income of Wesfarmers due to the fact that the company will have to

report the off balance sheet lease asset’s interests (Giner, Merello & Pardo, 2018). At the same time, it will be

required for the company to report the interest expenses related to the lease liabilities as they will have to show this

expense in the company’s income statement. For this reason, the operating income of the company will be affected

with this.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED ISSUED IN ACCOUNTING

Impact of Cash Flows Statement

The above discussion indicates towards the fact that the adoption of the new lease standard that is AASB

16 will have some major impact on both the balance sheet as well as income statement of Wesfarmers. This aspect

also indicates towards the fact that the cash flow statement of the company will be unchanged as the new statement

will not have any impact on the cash flows of the company. However, it needs to be mentioned that it is the decision

of the management of Wesfarmers whether they will recognize the lease payments under the financing activities or

under the investing activities (Tran & Zhu, 2017). For Wesfarmers, it will be preferable to recognize them under the

financing activities due to the nature of lease financing.

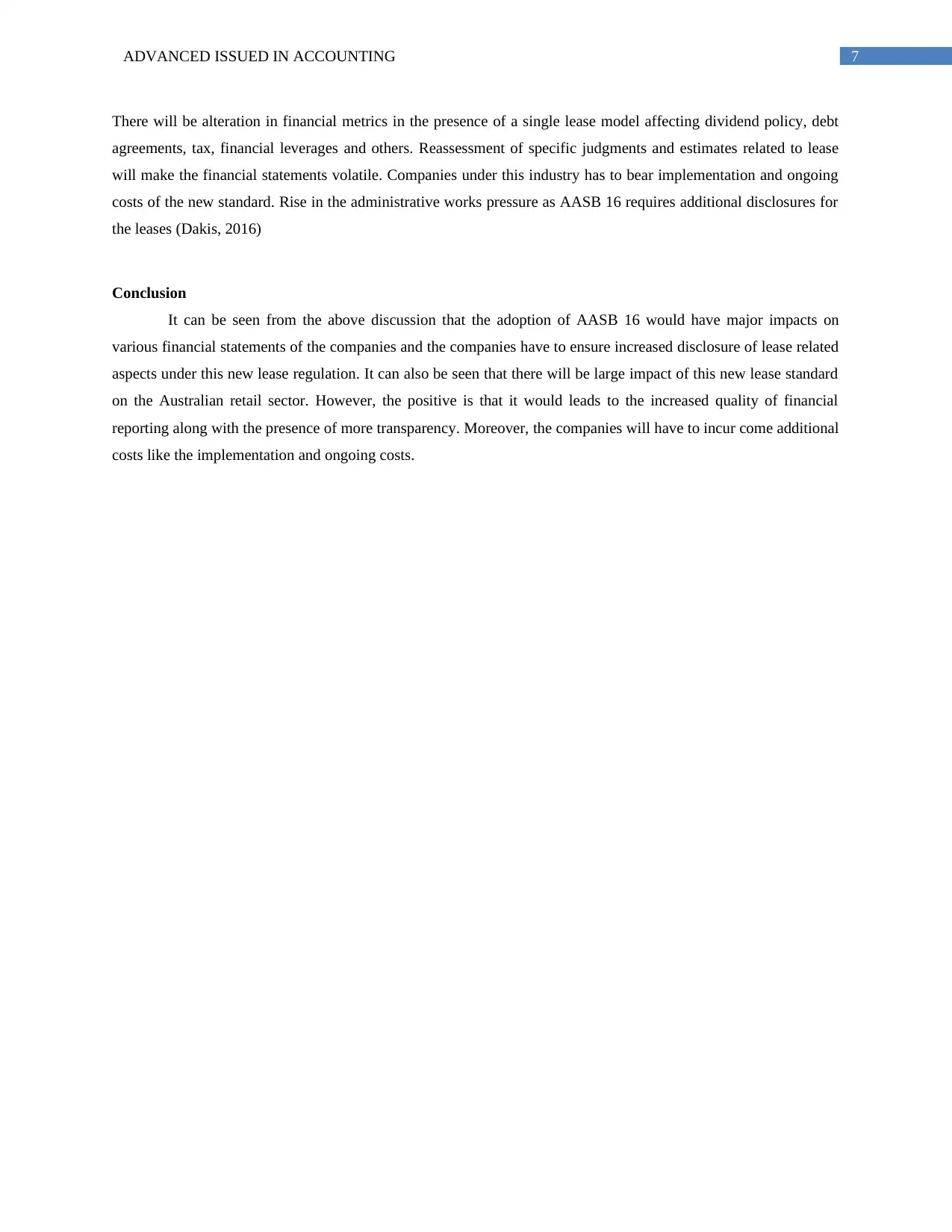

Lease Agreements for Australian Retail Sector along with the Lifecycle and Stages

The introduction of AASB 16 will have impact on many Australian business industries like airline industry,

telecommunication industry, mining industry and others; and the companies under Australian retail industry like

Wesfarmers and others will be impacted for the presence of many lease assets and liabilities (Joubert, Garvie &

Parle, 2017).

Figure 1: Impact of AASB 16 on Various Australian Business Industries

(Source: Xu, Davidson & Cheong, 2017)

There are certain effects of AASB 16 on the stage and lifecycles of the Australian retail sector. The first

effect will be on the recognition of lease liabilities and right-of-use assets will increase the amount of lease assets

and liabilities. The next effect will be in the form of increase in EBITDA as there is no operational lease expenses

(Beckman, 2016). There will be rise and decline in the operating cash flow and financing cash flows respectively.

Impact of Cash Flows Statement

The above discussion indicates towards the fact that the adoption of the new lease standard that is AASB

16 will have some major impact on both the balance sheet as well as income statement of Wesfarmers. This aspect

also indicates towards the fact that the cash flow statement of the company will be unchanged as the new statement

will not have any impact on the cash flows of the company. However, it needs to be mentioned that it is the decision

of the management of Wesfarmers whether they will recognize the lease payments under the financing activities or

under the investing activities (Tran & Zhu, 2017). For Wesfarmers, it will be preferable to recognize them under the

financing activities due to the nature of lease financing.

Lease Agreements for Australian Retail Sector along with the Lifecycle and Stages

The introduction of AASB 16 will have impact on many Australian business industries like airline industry,

telecommunication industry, mining industry and others; and the companies under Australian retail industry like

Wesfarmers and others will be impacted for the presence of many lease assets and liabilities (Joubert, Garvie &

Parle, 2017).

Figure 1: Impact of AASB 16 on Various Australian Business Industries

(Source: Xu, Davidson & Cheong, 2017)

There are certain effects of AASB 16 on the stage and lifecycles of the Australian retail sector. The first

effect will be on the recognition of lease liabilities and right-of-use assets will increase the amount of lease assets

and liabilities. The next effect will be in the form of increase in EBITDA as there is no operational lease expenses

(Beckman, 2016). There will be rise and decline in the operating cash flow and financing cash flows respectively.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED ISSUED IN ACCOUNTING

There will be alteration in financial metrics in the presence of a single lease model affecting dividend policy, debt

agreements, tax, financial leverages and others. Reassessment of specific judgments and estimates related to lease

will make the financial statements volatile. Companies under this industry has to bear implementation and ongoing

costs of the new standard. Rise in the administrative works pressure as AASB 16 requires additional disclosures for

the leases (Dakis, 2016)

Conclusion

It can be seen from the above discussion that the adoption of AASB 16 would have major impacts on

various financial statements of the companies and the companies have to ensure increased disclosure of lease related

aspects under this new lease regulation. It can also be seen that there will be large impact of this new lease standard

on the Australian retail sector. However, the positive is that it would leads to the increased quality of financial

reporting along with the presence of more transparency. Moreover, the companies will have to incur come additional

costs like the implementation and ongoing costs.

There will be alteration in financial metrics in the presence of a single lease model affecting dividend policy, debt

agreements, tax, financial leverages and others. Reassessment of specific judgments and estimates related to lease

will make the financial statements volatile. Companies under this industry has to bear implementation and ongoing

costs of the new standard. Rise in the administrative works pressure as AASB 16 requires additional disclosures for

the leases (Dakis, 2016)

Conclusion

It can be seen from the above discussion that the adoption of AASB 16 would have major impacts on

various financial statements of the companies and the companies have to ensure increased disclosure of lease related

aspects under this new lease regulation. It can also be seen that there will be large impact of this new lease standard

on the Australian retail sector. However, the positive is that it would leads to the increased quality of financial

reporting along with the presence of more transparency. Moreover, the companies will have to incur come additional

costs like the implementation and ongoing costs.

8ADVANCED ISSUED IN ACCOUNTING

References

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and key ratios: Evidence

from Australia. Australasian Accounting, Business and Finance Journal, 9(3), 27-44.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for Leases AASB 16

(IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal of New Business Ideas &

Trends, 15(2).

Xu, W., Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements: operating to capitalised

leases. Pacific Accounting Review, 29(1), 34-54.

Giner, B., Merello, P., & Pardo, F. (2018). Assessing the impact of operating lease capitalization with dynamic

Monte Carlo simulation. Journal of Business Research.

Tran, A., & Zhu, Y. H. (2017). The impact of adopting IFRS on corporate ETR and book-tax income gap.

Beckman, J. K. (2016). FASB and IASB diverging perspectives on the new lessee accounting: Implications for

international managerial decision-making. International Journal of Managerial Finance, 12(2), 161-176.

Dakis, G. S. (2016). Upcoming changes to contributions and leasing standards. Governance Directions, 68(2), 99.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for Leases AASB 16

(IFRS

16) with the Inclusion of Operating Leases in the Balance Sheet. Journal of New Business Ideas & Trends, 15(2),

113-119.

AASB 16. (2018) Leases. Retrieved 29 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf

AASB 117. (2018) Leases. Retrieved 29 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf

Wesfarmers. (2019). Our businesses. Retrieved 7 January 2019, from https://www.wesfarmers.com.au/our-

businesses/our-businesses

Wesfarmers. (2019). Annual Report 2018. Retrieved 7 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-report.pdf?sfvrsn=4

References

Wong, K., & Joshi, M. (2015). The impact of lease capitalisation on financial statements and key ratios: Evidence

from Australia. Australasian Accounting, Business and Finance Journal, 9(3), 27-44.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for Leases AASB 16

(IFRS 16) with the Inclusion of Operating Leases in the Balance Sheet. Journal of New Business Ideas &

Trends, 15(2).

Xu, W., Davidson, R. A., & Cheong, C. S. (2017). Converting financial statements: operating to capitalised

leases. Pacific Accounting Review, 29(1), 34-54.

Giner, B., Merello, P., & Pardo, F. (2018). Assessing the impact of operating lease capitalization with dynamic

Monte Carlo simulation. Journal of Business Research.

Tran, A., & Zhu, Y. H. (2017). The impact of adopting IFRS on corporate ETR and book-tax income gap.

Beckman, J. K. (2016). FASB and IASB diverging perspectives on the new lessee accounting: Implications for

international managerial decision-making. International Journal of Managerial Finance, 12(2), 161-176.

Dakis, G. S. (2016). Upcoming changes to contributions and leasing standards. Governance Directions, 68(2), 99.

Joubert, M., Garvie, L., & Parle, G. (2017). Implications of the New Accounting Standard for Leases AASB 16

(IFRS

16) with the Inclusion of Operating Leases in the Balance Sheet. Journal of New Business Ideas & Trends, 15(2),

113-119.

AASB 16. (2018) Leases. Retrieved 29 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf

AASB 117. (2018) Leases. Retrieved 29 December 2018, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf

Wesfarmers. (2019). Our businesses. Retrieved 7 January 2019, from https://www.wesfarmers.com.au/our-

businesses/our-businesses

Wesfarmers. (2019). Annual Report 2018. Retrieved 7 January 2019, from

https://www.wesfarmers.com.au/docs/default-source/reports/wes18-044-2018-annual-report.pdf?sfvrsn=4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED ISSUED IN ACCOUNTING

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.