AASB 2 'Share-Based Payment': Implications for Financial Reporting

VerifiedAdded on 2023/04/20

|9

|1321

|335

Essay

AI Summary

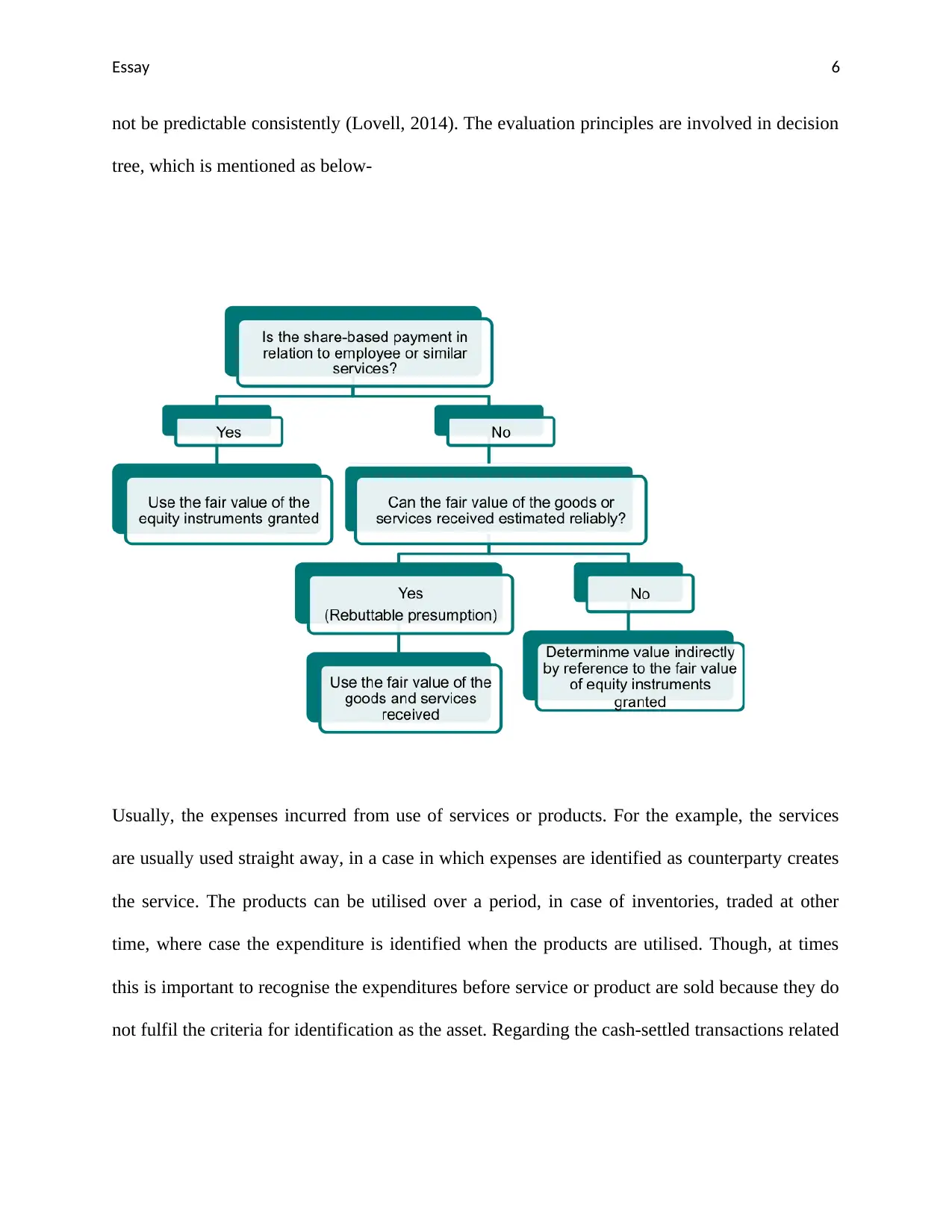

This essay examines the implications of AASB 2 'Share-based payment' on an entity's financial performance and position, particularly concerning the reporting of expenses associated with share options granted to employees. Before AASB 2, companies often did not record journal entries for share options, leading to inaccurate financial reporting. The essay provides examples illustrating the differences in accounting treatment before and after the introduction of AASB 2, highlighting the standard's impact on recognizing share-based payment transactions, whether equity-settled or cash-settled. It also covers the accounting procedures for both types of transactions, including the valuation of services or products purchased and the recognition of liabilities or equity. The essay concludes by emphasizing the importance of re-examining the fair value of liabilities at the end of each reporting period for cash-settled transactions.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.