Accounting Standards (AASB 138) and Financial Reporting: Case Study

VerifiedAdded on 2020/12/10

|10

|2644

|150

Case Study

AI Summary

This case study report analyzes the application of AASB 138 (Australian Accounting Standards Board) in the context of Technology Enterprises Ltd., focusing on the accounting treatment of a modified battery recharging process and its impact on financial statements for the year ended June 30, 2018. The report delves into the concept of AASB 138 concerning intangible assets, particularly the patent design, outlining recognition and measurement criteria during the research and development phases. It details the costs associated with the internally generated intangible asset and discusses the rules and restrictions in AASB 138 that affect the comparability of financial statements. Furthermore, the report provides recommendations to address investor interpretation concerns, emphasizing the need for clear, transparent, and compliant financial reporting to ensure stakeholders can make informed decisions. The study highlights the importance of disclosing all material information, adhering to accounting standards, and providing sufficient provisions for business obligations.

Case Study Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

AASB is defined as the Australian Accounting Standards Board, a Commen wealth Government

Body governing and regulating the accounting standards by focusing on necessary requirements

which every company, public sector enterprises as well as not profit business organisation has to

follow or comply with. This report is based on Technology Enterprises Ltd which has modified its

methodology related to the recharging of batteries used by its products. This report will streamline

about the Accounting standard to be followed and its concept for preparation of the financial

statement for the year ended 30 June 2018.

AASB is defined as the Australian Accounting Standards Board, a Commen wealth Government

Body governing and regulating the accounting standards by focusing on necessary requirements

which every company, public sector enterprises as well as not profit business organisation has to

follow or comply with. This report is based on Technology Enterprises Ltd which has modified its

methodology related to the recharging of batteries used by its products. This report will streamline

about the Accounting standard to be followed and its concept for preparation of the financial

statement for the year ended 30 June 2018.

Table of Contents

EXECUTIVE SUMMARY..................................................................................................................2

INTRODUCTION...............................................................................................................................4

MAIN BODY.......................................................................................................................................4

1. Concept of AASB 138 in relation to preparation of financial statements...................................4

2. Rules or Restrictions in AASB 138 impacting comparability features of financial statements..6

3. Recommendation related to concern with Investor's Interpretation in relation with the

financial statement..........................................................................................................................7

CONCLUSIONS..................................................................................................................................8

REFERENCES..................................................................................................................................10

EXECUTIVE SUMMARY..................................................................................................................2

INTRODUCTION...............................................................................................................................4

MAIN BODY.......................................................................................................................................4

1. Concept of AASB 138 in relation to preparation of financial statements...................................4

2. Rules or Restrictions in AASB 138 impacting comparability features of financial statements..6

3. Recommendation related to concern with Investor's Interpretation in relation with the

financial statement..........................................................................................................................7

CONCLUSIONS..................................................................................................................................8

REFERENCES..................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

AASB stands for Australian Accounting Standards Board. It is a Common wealth government body

which functions is to regulate all the accounting standards by laying down necessary requirements

which has to be followed by company and other NPO. The present report is based on Technology

Enterprises Ltd, which has conduct the Research and Development project for making modification

in the manner of recharging of batteries which are used in its own product and goods. Report will

shed light on defining the proper accounting standards for evaluating the correct cost of Patent

design. Further, it will define all the rules and restrictions in AASB 138 which is reducing the

comparability feature of financial statements of Technology Enterprises Ltd. At last, it will provide

a recommendation related to the process to be adopted to mitigate concern related to the

interpretations factor of the financial statements to the investor of Technology Enterprises Limited.

MAIN BODY

1. Concept of AASB 138 in relation to preparation of financial statements.

The Australian Accounting Standards Board is defined as one of the Commonwealth

Government body which regulates, monitors and supervises the accounting standards and rules by

providing all the requirements as applicable to all the companies, not-for-profit entities and the

public sector must follow. These AASB helps in the development of proper accounting standards

and norms which can be useful for company and other bodies in preparing the financial statement

of the business for the relevant accounting period (Henderson and et.al., 2015). With the helps of

clear accounting standards and norms, investors and other stakeholders of the company can make

correct and useful interpretations related to the particular business as well as financial transactions,

activities which allows stakeholders as well as investors in evaluating the financial position of

company and making of decisions accordingly.

All the statistical and financial data and information given in the financial statements of the

company are prepared by making proper and full compliance of all the accounting standards of

AASB. Due to complying factor, it helps the company in ensuring the transparency of business.

Technology Enterprises Ltd initiated research and development project with the aim of

bringing modification in the process of charging of all the batteries which are used in by its own

company products. After successful completion of research and development project in June 2018,

company has applied for undertaking of Patent right for its new modified design. Patent is provides

a monopoly right in form of government authority or license of making, selling, utilising or

developing the invention made.

Concept of AASB 138 – The Australian Accounting Standards Board 138 gives definition of an

Intangible Asset. The accounting standard 138 defines following:

AASB stands for Australian Accounting Standards Board. It is a Common wealth government body

which functions is to regulate all the accounting standards by laying down necessary requirements

which has to be followed by company and other NPO. The present report is based on Technology

Enterprises Ltd, which has conduct the Research and Development project for making modification

in the manner of recharging of batteries which are used in its own product and goods. Report will

shed light on defining the proper accounting standards for evaluating the correct cost of Patent

design. Further, it will define all the rules and restrictions in AASB 138 which is reducing the

comparability feature of financial statements of Technology Enterprises Ltd. At last, it will provide

a recommendation related to the process to be adopted to mitigate concern related to the

interpretations factor of the financial statements to the investor of Technology Enterprises Limited.

MAIN BODY

1. Concept of AASB 138 in relation to preparation of financial statements.

The Australian Accounting Standards Board is defined as one of the Commonwealth

Government body which regulates, monitors and supervises the accounting standards and rules by

providing all the requirements as applicable to all the companies, not-for-profit entities and the

public sector must follow. These AASB helps in the development of proper accounting standards

and norms which can be useful for company and other bodies in preparing the financial statement

of the business for the relevant accounting period (Henderson and et.al., 2015). With the helps of

clear accounting standards and norms, investors and other stakeholders of the company can make

correct and useful interpretations related to the particular business as well as financial transactions,

activities which allows stakeholders as well as investors in evaluating the financial position of

company and making of decisions accordingly.

All the statistical and financial data and information given in the financial statements of the

company are prepared by making proper and full compliance of all the accounting standards of

AASB. Due to complying factor, it helps the company in ensuring the transparency of business.

Technology Enterprises Ltd initiated research and development project with the aim of

bringing modification in the process of charging of all the batteries which are used in by its own

company products. After successful completion of research and development project in June 2018,

company has applied for undertaking of Patent right for its new modified design. Patent is provides

a monopoly right in form of government authority or license of making, selling, utilising or

developing the invention made.

Concept of AASB 138 – The Australian Accounting Standards Board 138 gives definition of an

Intangible Asset. The accounting standard 138 defines following:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Recognition process of an Intangible Asset.

2. Method of measuring an Intangible Asset

3. Provides requirements related to the disclosure of an Intangible Asset (Steenkamp and

Steenkamp, 2016).

As per AASB 138, Patent of design is considered as internally generated Intangible asset for

Technology Enterprises Ltd. of which recognition and measurement has to be done under the rules,

regulations and norms as applicable. First intangible asset generated has to be identified that

whether such asset is meeting the criteria for recognition under the research phase and development

phase.

1. Research Phase – If an intangible asset is arising as a result of research made, then no

recognition will be provided to such asset. In case of Technology Enterprises Ltd, patent is

an intangible asset for which the company has already applied. Expenditure incurred on

conducting of the research and development will be recognised as expense as and when it

will be incurred.

2. Development Phase - If an intangible asset is arising from conducting of development

process, then recognition will be provided to such intangible asset on the fulfilment of the

following requisites:

Technical feasibility of completing intangible asset for assessing its future use or sale

Intention of completing intangible asset and its ability to use or sell

Availability of financial, technical and other resources in adequate manner for completing

such development and its use and sell option

Ability of measuring the amount of expenditure taking place in case of development of such

intangible asset (Russell, 2017).

Cost associated with an Intangible asset generated internally - The cost of an Intangible

asset generated internally during research and development process is calculated by taking sum of

all the expenditure which are incurred from that date when intangible asset has first meet the

criteria of recognition. The cost calculation for Technology Enterprises Ltd of its internally

generated intangible asset i.e. Patent design includes all the cost which are directly attributable as

well as necessary for creating, producing and preparing the asset so as to make it capable of

operating in manner which is specified and required by the management of the company.

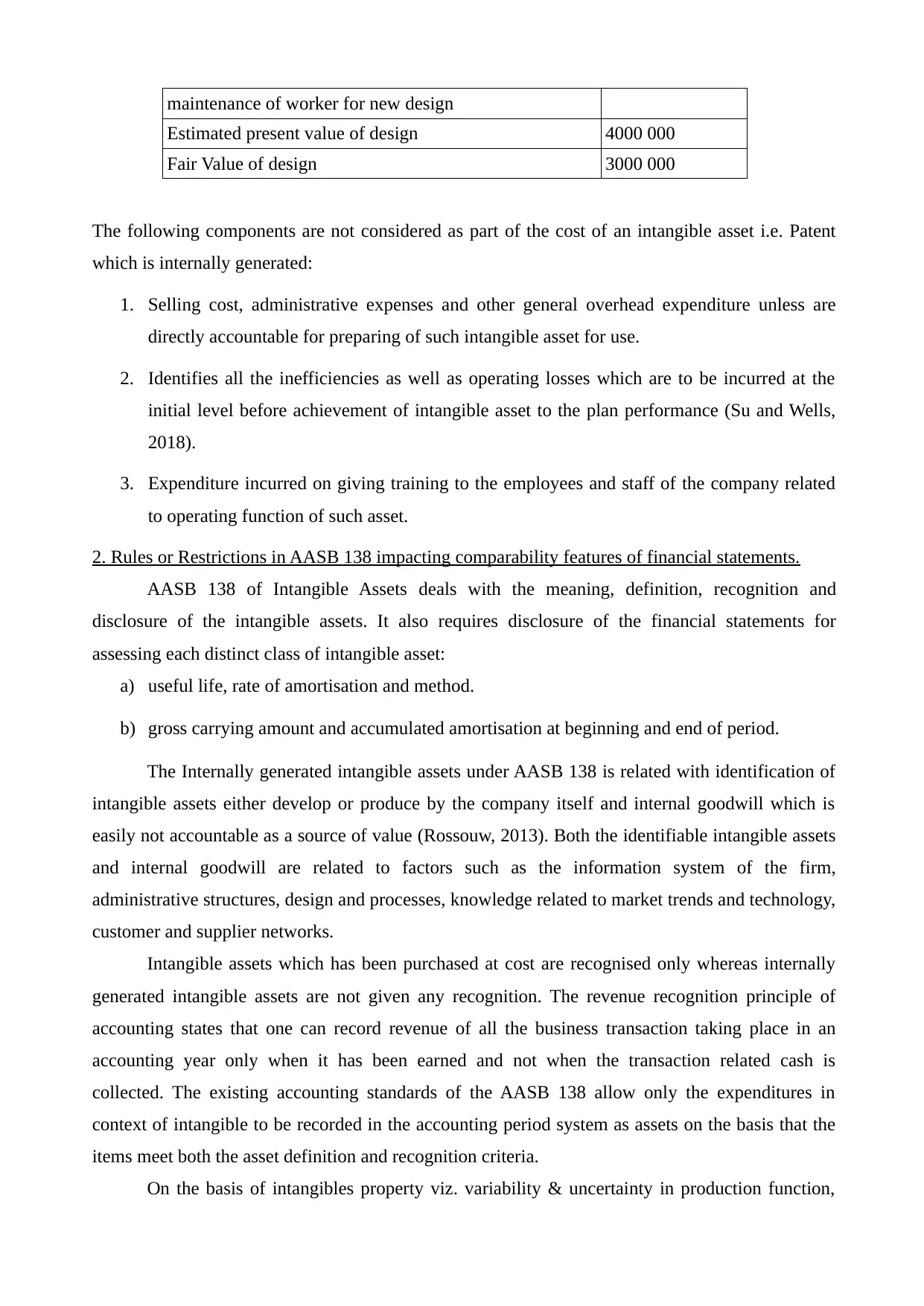

Particulars Cost (in $)

Cost related to the time spent on searching and

evaluating alternative materials

100 000

Cost incurred in respect of time taken for designing

models, constructing and testing of prototypes

700 000

Cost of time incurred on imparting training and 200 000

2. Method of measuring an Intangible Asset

3. Provides requirements related to the disclosure of an Intangible Asset (Steenkamp and

Steenkamp, 2016).

As per AASB 138, Patent of design is considered as internally generated Intangible asset for

Technology Enterprises Ltd. of which recognition and measurement has to be done under the rules,

regulations and norms as applicable. First intangible asset generated has to be identified that

whether such asset is meeting the criteria for recognition under the research phase and development

phase.

1. Research Phase – If an intangible asset is arising as a result of research made, then no

recognition will be provided to such asset. In case of Technology Enterprises Ltd, patent is

an intangible asset for which the company has already applied. Expenditure incurred on

conducting of the research and development will be recognised as expense as and when it

will be incurred.

2. Development Phase - If an intangible asset is arising from conducting of development

process, then recognition will be provided to such intangible asset on the fulfilment of the

following requisites:

Technical feasibility of completing intangible asset for assessing its future use or sale

Intention of completing intangible asset and its ability to use or sell

Availability of financial, technical and other resources in adequate manner for completing

such development and its use and sell option

Ability of measuring the amount of expenditure taking place in case of development of such

intangible asset (Russell, 2017).

Cost associated with an Intangible asset generated internally - The cost of an Intangible

asset generated internally during research and development process is calculated by taking sum of

all the expenditure which are incurred from that date when intangible asset has first meet the

criteria of recognition. The cost calculation for Technology Enterprises Ltd of its internally

generated intangible asset i.e. Patent design includes all the cost which are directly attributable as

well as necessary for creating, producing and preparing the asset so as to make it capable of

operating in manner which is specified and required by the management of the company.

Particulars Cost (in $)

Cost related to the time spent on searching and

evaluating alternative materials

100 000

Cost incurred in respect of time taken for designing

models, constructing and testing of prototypes

700 000

Cost of time incurred on imparting training and 200 000

maintenance of worker for new design

Estimated present value of design 4000 000

Fair Value of design 3000 000

The following components are not considered as part of the cost of an intangible asset i.e. Patent

which is internally generated:

1. Selling cost, administrative expenses and other general overhead expenditure unless are

directly accountable for preparing of such intangible asset for use.

2. Identifies all the inefficiencies as well as operating losses which are to be incurred at the

initial level before achievement of intangible asset to the plan performance (Su and Wells,

2018).

3. Expenditure incurred on giving training to the employees and staff of the company related

to operating function of such asset.

2. Rules or Restrictions in AASB 138 impacting comparability features of financial statements.

AASB 138 of Intangible Assets deals with the meaning, definition, recognition and

disclosure of the intangible assets. It also requires disclosure of the financial statements for

assessing each distinct class of intangible asset:

a) useful life, rate of amortisation and method.

b) gross carrying amount and accumulated amortisation at beginning and end of period.

The Internally generated intangible assets under AASB 138 is related with identification of

intangible assets either develop or produce by the company itself and internal goodwill which is

easily not accountable as a source of value (Rossouw, 2013). Both the identifiable intangible assets

and internal goodwill are related to factors such as the information system of the firm,

administrative structures, design and processes, knowledge related to market trends and technology,

customer and supplier networks.

Intangible assets which has been purchased at cost are recognised only whereas internally

generated intangible assets are not given any recognition. The revenue recognition principle of

accounting states that one can record revenue of all the business transaction taking place in an

accounting year only when it has been earned and not when the transaction related cash is

collected. The existing accounting standards of the AASB 138 allow only the expenditures in

context of intangible to be recorded in the accounting period system as assets on the basis that the

items meet both the asset definition and recognition criteria.

On the basis of intangibles property viz. variability & uncertainty in production function,

Estimated present value of design 4000 000

Fair Value of design 3000 000

The following components are not considered as part of the cost of an intangible asset i.e. Patent

which is internally generated:

1. Selling cost, administrative expenses and other general overhead expenditure unless are

directly accountable for preparing of such intangible asset for use.

2. Identifies all the inefficiencies as well as operating losses which are to be incurred at the

initial level before achievement of intangible asset to the plan performance (Su and Wells,

2018).

3. Expenditure incurred on giving training to the employees and staff of the company related

to operating function of such asset.

2. Rules or Restrictions in AASB 138 impacting comparability features of financial statements.

AASB 138 of Intangible Assets deals with the meaning, definition, recognition and

disclosure of the intangible assets. It also requires disclosure of the financial statements for

assessing each distinct class of intangible asset:

a) useful life, rate of amortisation and method.

b) gross carrying amount and accumulated amortisation at beginning and end of period.

The Internally generated intangible assets under AASB 138 is related with identification of

intangible assets either develop or produce by the company itself and internal goodwill which is

easily not accountable as a source of value (Rossouw, 2013). Both the identifiable intangible assets

and internal goodwill are related to factors such as the information system of the firm,

administrative structures, design and processes, knowledge related to market trends and technology,

customer and supplier networks.

Intangible assets which has been purchased at cost are recognised only whereas internally

generated intangible assets are not given any recognition. The revenue recognition principle of

accounting states that one can record revenue of all the business transaction taking place in an

accounting year only when it has been earned and not when the transaction related cash is

collected. The existing accounting standards of the AASB 138 allow only the expenditures in

context of intangible to be recorded in the accounting period system as assets on the basis that the

items meet both the asset definition and recognition criteria.

On the basis of intangibles property viz. variability & uncertainty in production function,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

heterogeneity & specificity and appropriability may result in arising of uncertainty on behalf of the

ability of firm in realising expected benefits from their intangibles for managers of the company.

This uncertainty may further creates problem for GAAP as accounting regulations are concerned

more with two important factors of financial information i.e. reliability & relevance and are

contained in AASB 138 (Overland, 2017). This accounting standard is not aim at identifying and

evaluating the expenditure incurred on all the intangible assets. In-spite its objectives is to allow

recording of only those intangible assets which is having price from an exchange business

transaction. Also, on the basis of mode of acquisition accounting standard differentiates accounting

methods for expenditure on intangibles. Items which has been excluded from recognition as an

intangible asset include brands names, mastheads, publishing titles, customer software etc. But

these items can be recognized as an intangible asset if purchased

Intangible Assets consists three basic themes which are as follows:

1. Expenditure on purchase of intangibles (either separately acquired or as part of an

acquisition) which has met definition of an intangible asset are deemed to be recognisable

as intangible assets.

2. All the other intangible expenditure will be under heading of provisions of internally

generated intangible asset & are further classifiable only as either Research or

Development.

3. Out of expenditure incurred on the research and development, only development

expenditure which met the intangible asset definition and recognition standards or rules plus

the six tests in AASB 138 Intangible Assets are recognisable as an intangible asset.

3. Recommendation related to concern with Investor's Interpretation in relation with the financial

statement.

Every business organisation or company is required to present its financial statements to its

investors and other stakeholders which is depicting the clear, true and correct picture of the

company financial and liquidity position for a specified period of time. Recommendation related to

solving business concerns of making investor interpretation are as follows:

1. Identifying the information needs and requirements of different investors and stakeholders

and then furnished financials accordingly (Barman, 2015).

2. It is the duty of every business organisation, to make disclosure of every small and big

material information in its financials and books of accounts which is of nature impacting the

decision making process of investors and changes the interpretation level.

3. Communication of financial and other business information with the help of financial

statements should be done by the company in a manner which facilitates stakeholders and

ability of firm in realising expected benefits from their intangibles for managers of the company.

This uncertainty may further creates problem for GAAP as accounting regulations are concerned

more with two important factors of financial information i.e. reliability & relevance and are

contained in AASB 138 (Overland, 2017). This accounting standard is not aim at identifying and

evaluating the expenditure incurred on all the intangible assets. In-spite its objectives is to allow

recording of only those intangible assets which is having price from an exchange business

transaction. Also, on the basis of mode of acquisition accounting standard differentiates accounting

methods for expenditure on intangibles. Items which has been excluded from recognition as an

intangible asset include brands names, mastheads, publishing titles, customer software etc. But

these items can be recognized as an intangible asset if purchased

Intangible Assets consists three basic themes which are as follows:

1. Expenditure on purchase of intangibles (either separately acquired or as part of an

acquisition) which has met definition of an intangible asset are deemed to be recognisable

as intangible assets.

2. All the other intangible expenditure will be under heading of provisions of internally

generated intangible asset & are further classifiable only as either Research or

Development.

3. Out of expenditure incurred on the research and development, only development

expenditure which met the intangible asset definition and recognition standards or rules plus

the six tests in AASB 138 Intangible Assets are recognisable as an intangible asset.

3. Recommendation related to concern with Investor's Interpretation in relation with the financial

statement.

Every business organisation or company is required to present its financial statements to its

investors and other stakeholders which is depicting the clear, true and correct picture of the

company financial and liquidity position for a specified period of time. Recommendation related to

solving business concerns of making investor interpretation are as follows:

1. Identifying the information needs and requirements of different investors and stakeholders

and then furnished financials accordingly (Barman, 2015).

2. It is the duty of every business organisation, to make disclosure of every small and big

material information in its financials and books of accounts which is of nature impacting the

decision making process of investors and changes the interpretation level.

3. Communication of financial and other business information with the help of financial

statements should be done by the company in a manner which facilitates stakeholders and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investors in easy understanding about the history of business transaction taking place in past

2 years.

4. It is very important for Technology Enterprises Limited to make compliance of laws and

regulations applicable on it while making preparation of the financial statements and books

of accounts such as provisions related to the Business Law, Company Act etc.

5. One of the recommendation for Technology Enterprises will included that it is the

responsibility of the Company's auditor and other managerial personnel, to prepare and

compute financial statement in accordance with accounting standards and principles

consistently and should be contain fair and true business value.

6. Company should also ensure that all the assumptions are taken into consideration while

preparing the financials for a specified business period. And also in that financial statement

disclosure has been made about such assumptions made for better understanding and getting

clear picture of financials made by the company to its investors and other stakeholders

(Guay, Samuels and Taylor, 2016).

7. Financial Statement should also make a good and sufficient provisions related to all the

business obligations and dues on behalf of the company.

8. Financial statements, Books of accounts should contain some keywords, themes or

terminologies related to the financial information contain in it. The managers and

accountant is required to make proper disclosure of such key terminologies in the financials,

so that the investors of Technology Enterprises Limited can make better and clear

interpretation and use it accordingly.

CONCLUSIONS

From the above report it has been summarised that Research and development is considered as one

of the most important feature for every business organisation in its growth. With the help of

research and development projects, company can further growth and achieve success and market

share. This report has discussed about AASB 138 which is a commonwealth government body

governing and controlling all the accounting standards and rules which every business organisation

has to comply with while preparing its final financial statements and books of account. Further, this

report has defined different restriction or rules which has been imposed by AASB 138 for

recognition of an intangible asset and its impact on comparability feature of the financial

statements. Every business transaction revenue should be recorded as and when earned for better

disclosure in the financials. At last, report has recommended CEO about measures which can assists

the company in mitigating concerns related to the investors' interpretation. By making proper and

2 years.

4. It is very important for Technology Enterprises Limited to make compliance of laws and

regulations applicable on it while making preparation of the financial statements and books

of accounts such as provisions related to the Business Law, Company Act etc.

5. One of the recommendation for Technology Enterprises will included that it is the

responsibility of the Company's auditor and other managerial personnel, to prepare and

compute financial statement in accordance with accounting standards and principles

consistently and should be contain fair and true business value.

6. Company should also ensure that all the assumptions are taken into consideration while

preparing the financials for a specified business period. And also in that financial statement

disclosure has been made about such assumptions made for better understanding and getting

clear picture of financials made by the company to its investors and other stakeholders

(Guay, Samuels and Taylor, 2016).

7. Financial Statement should also make a good and sufficient provisions related to all the

business obligations and dues on behalf of the company.

8. Financial statements, Books of accounts should contain some keywords, themes or

terminologies related to the financial information contain in it. The managers and

accountant is required to make proper disclosure of such key terminologies in the financials,

so that the investors of Technology Enterprises Limited can make better and clear

interpretation and use it accordingly.

CONCLUSIONS

From the above report it has been summarised that Research and development is considered as one

of the most important feature for every business organisation in its growth. With the help of

research and development projects, company can further growth and achieve success and market

share. This report has discussed about AASB 138 which is a commonwealth government body

governing and controlling all the accounting standards and rules which every business organisation

has to comply with while preparing its final financial statements and books of account. Further, this

report has defined different restriction or rules which has been imposed by AASB 138 for

recognition of an intangible asset and its impact on comparability feature of the financial

statements. Every business transaction revenue should be recorded as and when earned for better

disclosure in the financials. At last, report has recommended CEO about measures which can assists

the company in mitigating concerns related to the investors' interpretation. By making proper and

correct disclosures of information the material nature, Technology Enterprises Limited is able to

make its investors more capable of making sound investment decision.

make its investors more capable of making sound investment decision.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Barman, E., 2015. Of principle and principal: Value plurality in the market of impact investing.

Valuation Studies. 3(1). pp.9-44.

Guay, W., Samuels, D. and Taylor, D., 2016. Guiding through the fog: Financial statement

complexity and voluntary disclosure. Journal of Accounting and Economics. 62(2-3). pp.234-

269.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Overland, S., 2017. 20. FINANCIAL STATEMENTS.

Rossouw, C., 2013. The need for specific accounting principles for non-profit organisations' assets

without economic benefits, restricted donations and funds. Journal of Economic and Financial

Sciences. 6(2). pp.459-478.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting & Finance.

57. pp.211-234.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting.14(1). pp.116-130.

Su, W. H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable intangible

assets in business combinations pre-and post-IFRS adoption. Accounting Research Journal.

31(2). pp.135-156.

Online

AASB 138 Intangible Assets. 2015. [Online]. Available through:

<https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-

18.pdf>.

Accounting for Expenditure On Intangibles. 2019. [Online]. Available through:

<https://eprints.utas.edu.au/12474/2/thesis_hartini_jaafar.pdf>.

Books and Journals

Barman, E., 2015. Of principle and principal: Value plurality in the market of impact investing.

Valuation Studies. 3(1). pp.9-44.

Guay, W., Samuels, D. and Taylor, D., 2016. Guiding through the fog: Financial statement

complexity and voluntary disclosure. Journal of Accounting and Economics. 62(2-3). pp.234-

269.

Henderson, S. and et.al., 2015. Issues in financial accounting. Pearson Higher Education AU.

Overland, S., 2017. 20. FINANCIAL STATEMENTS.

Rossouw, C., 2013. The need for specific accounting principles for non-profit organisations' assets

without economic benefits, restricted donations and funds. Journal of Economic and Financial

Sciences. 6(2). pp.459-478.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting & Finance.

57. pp.211-234.

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions reducing

R&D spending?. Journal of Financial Reporting and Accounting.14(1). pp.116-130.

Su, W. H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable intangible

assets in business combinations pre-and post-IFRS adoption. Accounting Research Journal.

31(2). pp.135-156.

Online

AASB 138 Intangible Assets. 2015. [Online]. Available through:

<https://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-

18.pdf>.

Accounting for Expenditure On Intangibles. 2019. [Online]. Available through:

<https://eprints.utas.edu.au/12474/2/thesis_hartini_jaafar.pdf>.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.