Evaluation of Accounting Concepts in Advanced Financial Accounting

VerifiedAdded on 2022/10/19

|11

|3291

|448

Report

AI Summary

This report provides an in-depth analysis of the AASB Conceptual Framework within the context of advanced financial accounting. It begins by defining and describing key accounting concepts, including financial statements, reporting entities, elements of financial statements, recognition and derecognition, measurement, and presentation/disclosure. The report then delves into the issue of measurement, exploring the conceptual framework's approaches, the debate between historical cost and fair value, and providing an example using Speedcast International Limited. Finally, it examines the fundamental qualitative characteristics of relevance and faithful representation in financial information. The report aims to provide a comprehensive understanding of the framework's implications for financial reporting and its application in the real world.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction...................................................................................................................2

Description of Accounting Concepts............................................................................2

Conceptual Framework and the Issue of Measurement..............................................3

Fundamental Qualitative Characteristics – Relevance and Faithful Representation...4

Conclusion....................................................................................................................9

References.................................................................................................................10

Table of Contents

Introduction...................................................................................................................2

Description of Accounting Concepts............................................................................2

Conceptual Framework and the Issue of Measurement..............................................3

Fundamental Qualitative Characteristics – Relevance and Faithful Representation...4

Conclusion....................................................................................................................9

References.................................................................................................................10

2ADVANCED FINANCIAL ACCOUNTING

Introduction

Accounting concepts have certain major implications on the business

organizations since it leads to effective financial reporting practice within the

companies (Weil, Schipper and Francis 2013). This is also applicable for the

companies in Australia because of the presence of the Australian Accounting

Standards Board (AASB) Conceptual Framework which provides the Australian

listed companies with the appropriate accounting policies and procedures for

effective continuation of the processes of financial reporting (Schaltegger and Burritt

2017). In addition, the companies can get help from this accounting conceptual

framework for resolving different kinds of accounting issues such as measurement

related issues, valuation and recognition of financial substances related issues and

others. It is needed for all the Australian listed companies to adhere to the AASB

conceptual framework for the purpose of financial reporting. The main objective of

this report is the analysis and evaluation of different crucial aspects of the AASB

conceptual framework for the purpose of financial reporting. This report considers

analyzing different types of accounting concepts in the selected company. After that,

it considers the analysis of the measurement related issues in the company through

the effective consideration of the measurement debate. Lastly, it sheds light in

financial information’s fundamental qualitative characteristics. The company selected

for this report is Speedcast International Limited.

Description of Accounting Concepts

The presence of certain accounting concepts can be seen in the AASB

Conceptual Framework which the companies must consider in financial reporting

(aasb.gov.au 2019). They are discussed below:

Financial Statement and Reporting Entities

As per this accounting concept, the main role of financial statements can be

found in delivering relevant information about the assets, liabilities, equity, income

and expenses of the companies and the companies are needed to use this

accounting concept for the same purpose (aasb.gov.au 2019). It is visible in the

latest annual report of Speedcast International Limited that the firm has provided the

relevant information about the above-discussed economic substances through

different financial statement and notes. In addition, according to this concept,

business organizations must maintain their going concern status which indicates

towards the ability to continue operation for foreseeable future. Speedcast

International Limited has prepared their financial statements on the going concern

basis. In addition, the firm has introduced as well as implemented effective capital

management strategies for securing their ability to continue their business operations

as a going concern (asx.com.au 2019).

Elements of Financial Statements

This is considered as another most important accounting concept as per the

AASB Conceptual Framework. Assets, liabilities, equity, income and expenses are

the main elements of financial statements and AASB Conceptual Framework has

provided the definition of these elements. As per the definitions, assets and liabilities

are the present resources and obligations of the firms respectively arising due to

past events or transactions. Equity is the asset’s residual interests after deducting

the company’s liabilities. Income is the decrease in liabilities or increase in assets

that contributes to increased equity. Lastly, expenses are the decrease in income or

increase in liabilities which contribute to decreased equity (Flower 2018). According

Introduction

Accounting concepts have certain major implications on the business

organizations since it leads to effective financial reporting practice within the

companies (Weil, Schipper and Francis 2013). This is also applicable for the

companies in Australia because of the presence of the Australian Accounting

Standards Board (AASB) Conceptual Framework which provides the Australian

listed companies with the appropriate accounting policies and procedures for

effective continuation of the processes of financial reporting (Schaltegger and Burritt

2017). In addition, the companies can get help from this accounting conceptual

framework for resolving different kinds of accounting issues such as measurement

related issues, valuation and recognition of financial substances related issues and

others. It is needed for all the Australian listed companies to adhere to the AASB

conceptual framework for the purpose of financial reporting. The main objective of

this report is the analysis and evaluation of different crucial aspects of the AASB

conceptual framework for the purpose of financial reporting. This report considers

analyzing different types of accounting concepts in the selected company. After that,

it considers the analysis of the measurement related issues in the company through

the effective consideration of the measurement debate. Lastly, it sheds light in

financial information’s fundamental qualitative characteristics. The company selected

for this report is Speedcast International Limited.

Description of Accounting Concepts

The presence of certain accounting concepts can be seen in the AASB

Conceptual Framework which the companies must consider in financial reporting

(aasb.gov.au 2019). They are discussed below:

Financial Statement and Reporting Entities

As per this accounting concept, the main role of financial statements can be

found in delivering relevant information about the assets, liabilities, equity, income

and expenses of the companies and the companies are needed to use this

accounting concept for the same purpose (aasb.gov.au 2019). It is visible in the

latest annual report of Speedcast International Limited that the firm has provided the

relevant information about the above-discussed economic substances through

different financial statement and notes. In addition, according to this concept,

business organizations must maintain their going concern status which indicates

towards the ability to continue operation for foreseeable future. Speedcast

International Limited has prepared their financial statements on the going concern

basis. In addition, the firm has introduced as well as implemented effective capital

management strategies for securing their ability to continue their business operations

as a going concern (asx.com.au 2019).

Elements of Financial Statements

This is considered as another most important accounting concept as per the

AASB Conceptual Framework. Assets, liabilities, equity, income and expenses are

the main elements of financial statements and AASB Conceptual Framework has

provided the definition of these elements. As per the definitions, assets and liabilities

are the present resources and obligations of the firms respectively arising due to

past events or transactions. Equity is the asset’s residual interests after deducting

the company’s liabilities. Income is the decrease in liabilities or increase in assets

that contributes to increased equity. Lastly, expenses are the decrease in income or

increase in liabilities which contribute to decreased equity (Flower 2018). According

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

to the latest annual report of Speedcast International Limited, the company has used

this accounting concept with the inclusion of all the details and information on their

assets, liabilities, equity, income and expenses. In addition, the company has

provided the recognition as well as measurement criteria of these substances in the

notes to the financial statements (asx.com.au 2019).

Recognition and Derecognition

These two are crucial accounting concept related to the above discussed

elements of financial statement. Recognition refers to the procedures to capture an

element so that it can be included in the financial statements where derecognition

refers to the elimination of a part or a whole element from the financial statements of

the companies, especially from the balance sheets (Ponomareva and Melnikova

2015). It is observable in the latest annual report of Speedcast International Limited

that all the processes as well as procedures of the recognition and derecognition of

the financial statement’s elements are provided by the management of Speedcast

International Limited which indicates towards the adoption of these accounting

concepts by the firm (asx.com.au 2019).

Measurement

According to AASB Conceptual Framework, measurement helps in reflecting

the most relevant value of an element of financial statement. The presence of two

measurement approach can be seen in the AASB conceptual framework; they are

historical cost measurement and current value measurement (Barth 2013). Fair

value measurement and value-in-use measurement are the two measurement bases

under the current value measurement. It is observable in the latest annual report of

the selected company that the management has undertaken the use of both

historical cost and fair value measurement of their assets and liabilities (asx.com.au

2019).

Presentation and Disclosure

This accounting concept is concerned with the proper communication of the

information about the financial elements thorough their effective presentation and

disclosure. As per AASB conceptual framework, the managements of the companies

must effectively present and disclose all the required financial information through

the financial statements (Kieso, Weygandt and Warfield 2016). According to the

latest annual report of Speedcast International Limited, the company has effectively

presented and disclosed the required information by complying with the standards of

Australian Accounting Standard, AASB, Corporations Act 2001 and IFRS

(asx.com.au 2019).

Conceptual Framework and the Issue of Measurement

Conceptual Framework – It is crucial for the companies to adopt the appropriate

measurement base for the financial elements. In the AASB conceptual framework,

two measurement approaches are mentioned that are historical cost measurement

and fair value measurement under the current value method (aasb.gov.au 2019).

AASB conceptual framework states that fair value is the price received a firm due to

the sale of an asset or any payment or trainer of any liability at the measurement

date between two parties. The present value of an asset or liability reflects when the

companies adopt the fair value measurement base (Palea 2014). On the other hand,

the cost of an asset or liability at the date of acquisition can be obtained under the

historical cost accounting (Ellul et al. 2015). It is fair enough to mention the fact that

there are some major differences between these two measurement bases.

to the latest annual report of Speedcast International Limited, the company has used

this accounting concept with the inclusion of all the details and information on their

assets, liabilities, equity, income and expenses. In addition, the company has

provided the recognition as well as measurement criteria of these substances in the

notes to the financial statements (asx.com.au 2019).

Recognition and Derecognition

These two are crucial accounting concept related to the above discussed

elements of financial statement. Recognition refers to the procedures to capture an

element so that it can be included in the financial statements where derecognition

refers to the elimination of a part or a whole element from the financial statements of

the companies, especially from the balance sheets (Ponomareva and Melnikova

2015). It is observable in the latest annual report of Speedcast International Limited

that all the processes as well as procedures of the recognition and derecognition of

the financial statement’s elements are provided by the management of Speedcast

International Limited which indicates towards the adoption of these accounting

concepts by the firm (asx.com.au 2019).

Measurement

According to AASB Conceptual Framework, measurement helps in reflecting

the most relevant value of an element of financial statement. The presence of two

measurement approach can be seen in the AASB conceptual framework; they are

historical cost measurement and current value measurement (Barth 2013). Fair

value measurement and value-in-use measurement are the two measurement bases

under the current value measurement. It is observable in the latest annual report of

the selected company that the management has undertaken the use of both

historical cost and fair value measurement of their assets and liabilities (asx.com.au

2019).

Presentation and Disclosure

This accounting concept is concerned with the proper communication of the

information about the financial elements thorough their effective presentation and

disclosure. As per AASB conceptual framework, the managements of the companies

must effectively present and disclose all the required financial information through

the financial statements (Kieso, Weygandt and Warfield 2016). According to the

latest annual report of Speedcast International Limited, the company has effectively

presented and disclosed the required information by complying with the standards of

Australian Accounting Standard, AASB, Corporations Act 2001 and IFRS

(asx.com.au 2019).

Conceptual Framework and the Issue of Measurement

Conceptual Framework – It is crucial for the companies to adopt the appropriate

measurement base for the financial elements. In the AASB conceptual framework,

two measurement approaches are mentioned that are historical cost measurement

and fair value measurement under the current value method (aasb.gov.au 2019).

AASB conceptual framework states that fair value is the price received a firm due to

the sale of an asset or any payment or trainer of any liability at the measurement

date between two parties. The present value of an asset or liability reflects when the

companies adopt the fair value measurement base (Palea 2014). On the other hand,

the cost of an asset or liability at the date of acquisition can be obtained under the

historical cost accounting (Ellul et al. 2015). It is fair enough to mention the fact that

there are some major differences between these two measurement bases.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

Measurement Debate – Over the decade, it can be seen that there has been the

continuation of a major debate regarding the superiority of the above mentioned two

measurement bases. People who support the fair value measurement base states

that fair value id the most relevant measurement base since factors like depreciation,

market trend and others are considered by it. In this manner, fair value becomes

more relevant in the current market situation. On the other hand, there are many

people who are in the support of the historical cost accounting through this method is

considered as the conservative method of measurement since it considers the cost

of the elements at the acquisition date. Vast use of fair value measurement could be

seen in the nineteenth and twentieth century. Due to the tendency of the fair value

measurement of overstating the asset values, most of the people blamed this

particular measurement base at the time of the economic collapse of 1920

(Christensen and Nikolaev 201). For this reason, there is significant doubt over the

use of fair value accounting measurement base. It is crucial to mention the fact that

the use of both the fair value measurement base and historical cost measurement

base is permissible as per AASB conceptual framework.

Example – The example of Speedcast International Limited can be provided in this

situation. As per the Note 2 (a) of the 2018 Annual Report of Speedcast International

Limited, both the use of historical cost accounting as well as fair value measurement

can be seen in the company. The financial statements of the company have been

prepared in accordance with the fair value accounting, but there are some

exceptions where fair value measurement has been used by the company

(asx.com.au 2019).

Note 2 (l) of the 2018 Annual Report of Speedcast International Limited shows

that the inventories of the firm are valued at the lower of cost and net realizable

value when the company determines the cost on the basis of average cost method.

After that Note 2 (m) of the latest annual report states that the property, plant and

equipment are stated at the historical cost less accumulated losses of impairment

and accumulated depreciation (asx.com.au 2019). The company has also used the

fair value measurement base in their financial reporting. Note 2 (j) of the annual

report shows the use of fair value for the initial recognition of trade receivable; fair

value is also used for the initial recognition of loans and receivable as per Note 2 (K)

(i). As per Note 2 (o), the initial recognition of trade payables is done at fair value.

Note 2 (r) (ii) shows the use of fair value for the capitalisation of finance leases. After

that, as per Note 2 (s), the initial recognition of the borrowings is done on the basis of

fair value (asx.com.au 2019).

The above discussion shows the effective use of both the historical cost and

fair value measurement by the management of Speedcast International Limited.

However, the company has provided effective justification behind the use of fair

value or historical cost in the notes to the financial statement in order to avoid the

effects of measurement debate.

Fundamental Qualitative Characteristics – Relevance and Faithful

Representation

Financial information must contain both the fundamental qualitative

characteristics of relevance and faithful representation in order to be useful in the

decision making process of the users. These are considered as crucial aspects in

appropriate financial reporting (aasb.gov.au 2019). The following discussion shows

the details of these two qualitative characteristics.

Relevance

Measurement Debate – Over the decade, it can be seen that there has been the

continuation of a major debate regarding the superiority of the above mentioned two

measurement bases. People who support the fair value measurement base states

that fair value id the most relevant measurement base since factors like depreciation,

market trend and others are considered by it. In this manner, fair value becomes

more relevant in the current market situation. On the other hand, there are many

people who are in the support of the historical cost accounting through this method is

considered as the conservative method of measurement since it considers the cost

of the elements at the acquisition date. Vast use of fair value measurement could be

seen in the nineteenth and twentieth century. Due to the tendency of the fair value

measurement of overstating the asset values, most of the people blamed this

particular measurement base at the time of the economic collapse of 1920

(Christensen and Nikolaev 201). For this reason, there is significant doubt over the

use of fair value accounting measurement base. It is crucial to mention the fact that

the use of both the fair value measurement base and historical cost measurement

base is permissible as per AASB conceptual framework.

Example – The example of Speedcast International Limited can be provided in this

situation. As per the Note 2 (a) of the 2018 Annual Report of Speedcast International

Limited, both the use of historical cost accounting as well as fair value measurement

can be seen in the company. The financial statements of the company have been

prepared in accordance with the fair value accounting, but there are some

exceptions where fair value measurement has been used by the company

(asx.com.au 2019).

Note 2 (l) of the 2018 Annual Report of Speedcast International Limited shows

that the inventories of the firm are valued at the lower of cost and net realizable

value when the company determines the cost on the basis of average cost method.

After that Note 2 (m) of the latest annual report states that the property, plant and

equipment are stated at the historical cost less accumulated losses of impairment

and accumulated depreciation (asx.com.au 2019). The company has also used the

fair value measurement base in their financial reporting. Note 2 (j) of the annual

report shows the use of fair value for the initial recognition of trade receivable; fair

value is also used for the initial recognition of loans and receivable as per Note 2 (K)

(i). As per Note 2 (o), the initial recognition of trade payables is done at fair value.

Note 2 (r) (ii) shows the use of fair value for the capitalisation of finance leases. After

that, as per Note 2 (s), the initial recognition of the borrowings is done on the basis of

fair value (asx.com.au 2019).

The above discussion shows the effective use of both the historical cost and

fair value measurement by the management of Speedcast International Limited.

However, the company has provided effective justification behind the use of fair

value or historical cost in the notes to the financial statement in order to avoid the

effects of measurement debate.

Fundamental Qualitative Characteristics – Relevance and Faithful

Representation

Financial information must contain both the fundamental qualitative

characteristics of relevance and faithful representation in order to be useful in the

decision making process of the users. These are considered as crucial aspects in

appropriate financial reporting (aasb.gov.au 2019). The following discussion shows

the details of these two qualitative characteristics.

Relevance

5ADVANCED FINANCIAL ACCOUNTING

The availability of relevant financial information is required with the aim to

positively influence the decision-making process of the users. It needs to be

mentioned that the inclusion of both confirmatory value and predictive value makes

the information relevant to the users of the financial reports. Usefulness of the

financial information is increased by the confirmatory value though giving feedback

of previous evaluation. After that, usefulness of financial information is increased by

the predictive value through providing the prediction n the future financial outcome of

the companies. Under this characteristic, it is required to take into consideration the

materiality aspect and the aspect of uncertainty in measurement (Palea 2013).

Faithful Representation

In order to increase the usefulness of financial information to the users of the

financial reports, the managements of the companies should faithfully represent the

financial information of different elements of financial statements. The important

factors that are complete, neutral and error-free needs to be there in the financial

statements in case the companies want to present the information in faithful manner.

Financial information which is complete, free of error and neutral is of great help for

the users of the financial statements to make different decisions about the

companies (Tsoncheva 2014).

In order to verify the presence of these fundamental characteristics of

financial information, there are three steps which need to be followed. They are as

below:

1. Consideration of the essential elements of financial statements required for

decision-making process;

2. Identification of the type of information about the elements which is most

relevant to the users of the financial statements; and,

3. Determination of the fact that whether the company has provided this relevant

information about the financial element in faithful manner (Wang 2013).

Example

This part considers the analysis of thee major economic phenomena of

Speedcast International Limited’s annual report in order to assess the presence of

fundamental characteristics of financial information; they are Property, Plant and

Equipment, Inventory and Borrowings.

Property, Plant and Equipment – In the non-current assets of Speedcast

International Limited, property, plant and equipments form a crucial part which is

relevant to the uses for ascertaining the financial position of the firm. Most relevant

types of information on these assets are their book value and adopted accounting

policies.

The availability of relevant financial information is required with the aim to

positively influence the decision-making process of the users. It needs to be

mentioned that the inclusion of both confirmatory value and predictive value makes

the information relevant to the users of the financial reports. Usefulness of the

financial information is increased by the confirmatory value though giving feedback

of previous evaluation. After that, usefulness of financial information is increased by

the predictive value through providing the prediction n the future financial outcome of

the companies. Under this characteristic, it is required to take into consideration the

materiality aspect and the aspect of uncertainty in measurement (Palea 2013).

Faithful Representation

In order to increase the usefulness of financial information to the users of the

financial reports, the managements of the companies should faithfully represent the

financial information of different elements of financial statements. The important

factors that are complete, neutral and error-free needs to be there in the financial

statements in case the companies want to present the information in faithful manner.

Financial information which is complete, free of error and neutral is of great help for

the users of the financial statements to make different decisions about the

companies (Tsoncheva 2014).

In order to verify the presence of these fundamental characteristics of

financial information, there are three steps which need to be followed. They are as

below:

1. Consideration of the essential elements of financial statements required for

decision-making process;

2. Identification of the type of information about the elements which is most

relevant to the users of the financial statements; and,

3. Determination of the fact that whether the company has provided this relevant

information about the financial element in faithful manner (Wang 2013).

Example

This part considers the analysis of thee major economic phenomena of

Speedcast International Limited’s annual report in order to assess the presence of

fundamental characteristics of financial information; they are Property, Plant and

Equipment, Inventory and Borrowings.

Property, Plant and Equipment – In the non-current assets of Speedcast

International Limited, property, plant and equipments form a crucial part which is

relevant to the uses for ascertaining the financial position of the firm. Most relevant

types of information on these assets are their book value and adopted accounting

policies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

(Source: asx.com.au 2019)

(Source: asx.com.au 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

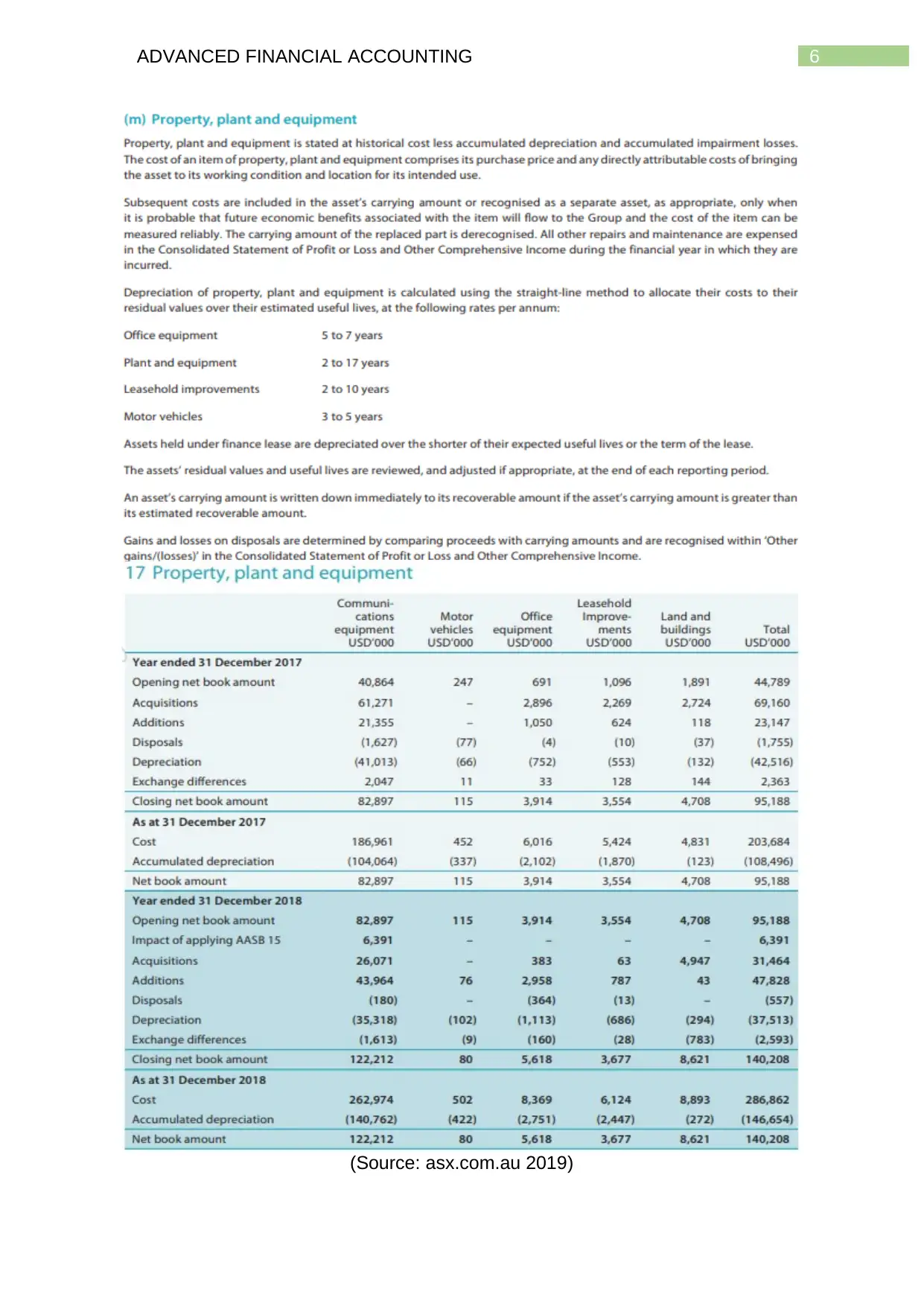

According to the above extracts of the latest annual report of the company

shows that all the relevant information on the property, plant and equipment is

provided by the management such as net book value, reasons for the change in net

book value and policies related to measurement, depreciation, impairment and

others about these assets (Braam and Beest 2013). This is essential for the users of

the financial statements.

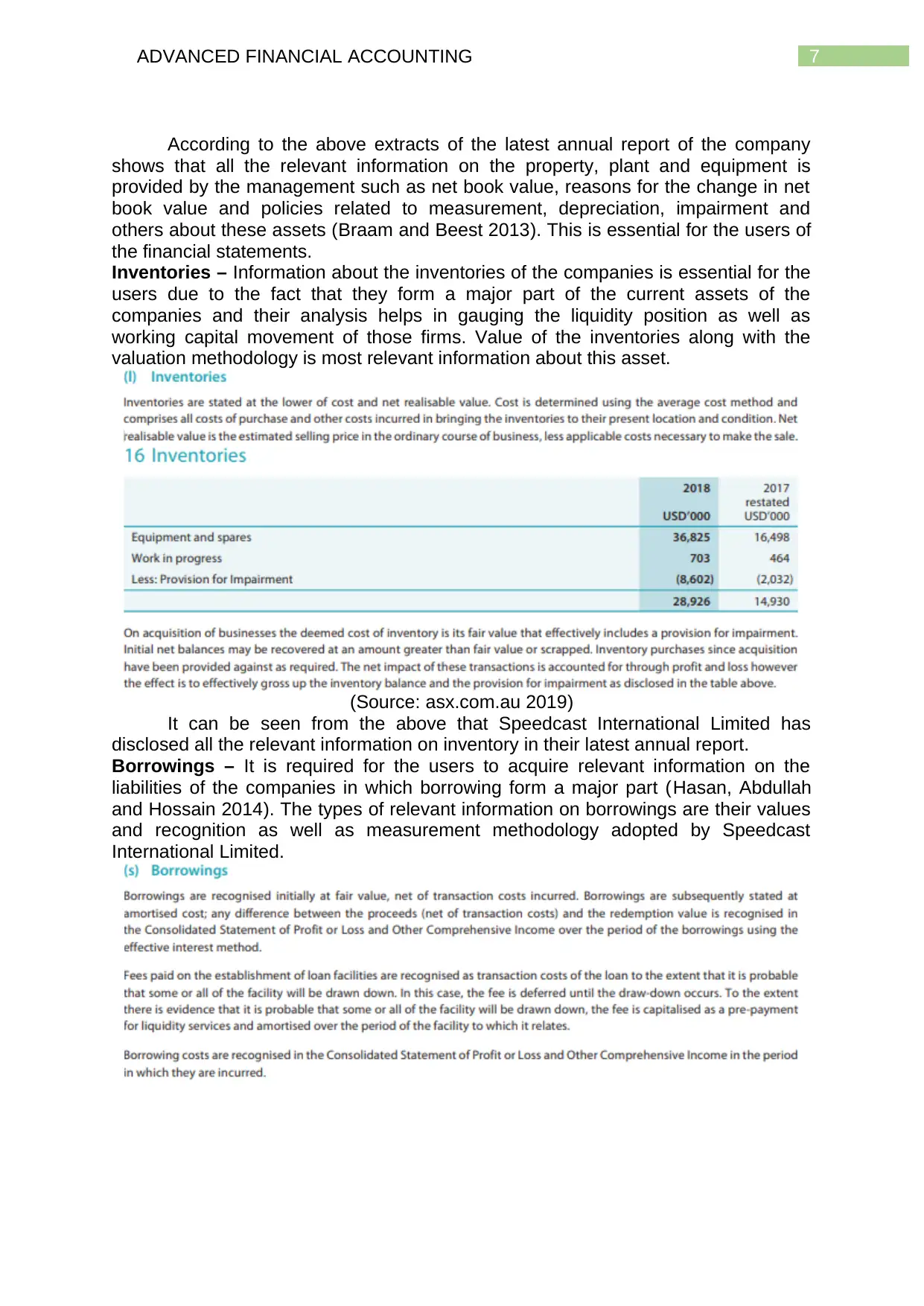

Inventories – Information about the inventories of the companies is essential for the

users due to the fact that they form a major part of the current assets of the

companies and their analysis helps in gauging the liquidity position as well as

working capital movement of those firms. Value of the inventories along with the

valuation methodology is most relevant information about this asset.

(Source: asx.com.au 2019)

It can be seen from the above that Speedcast International Limited has

disclosed all the relevant information on inventory in their latest annual report.

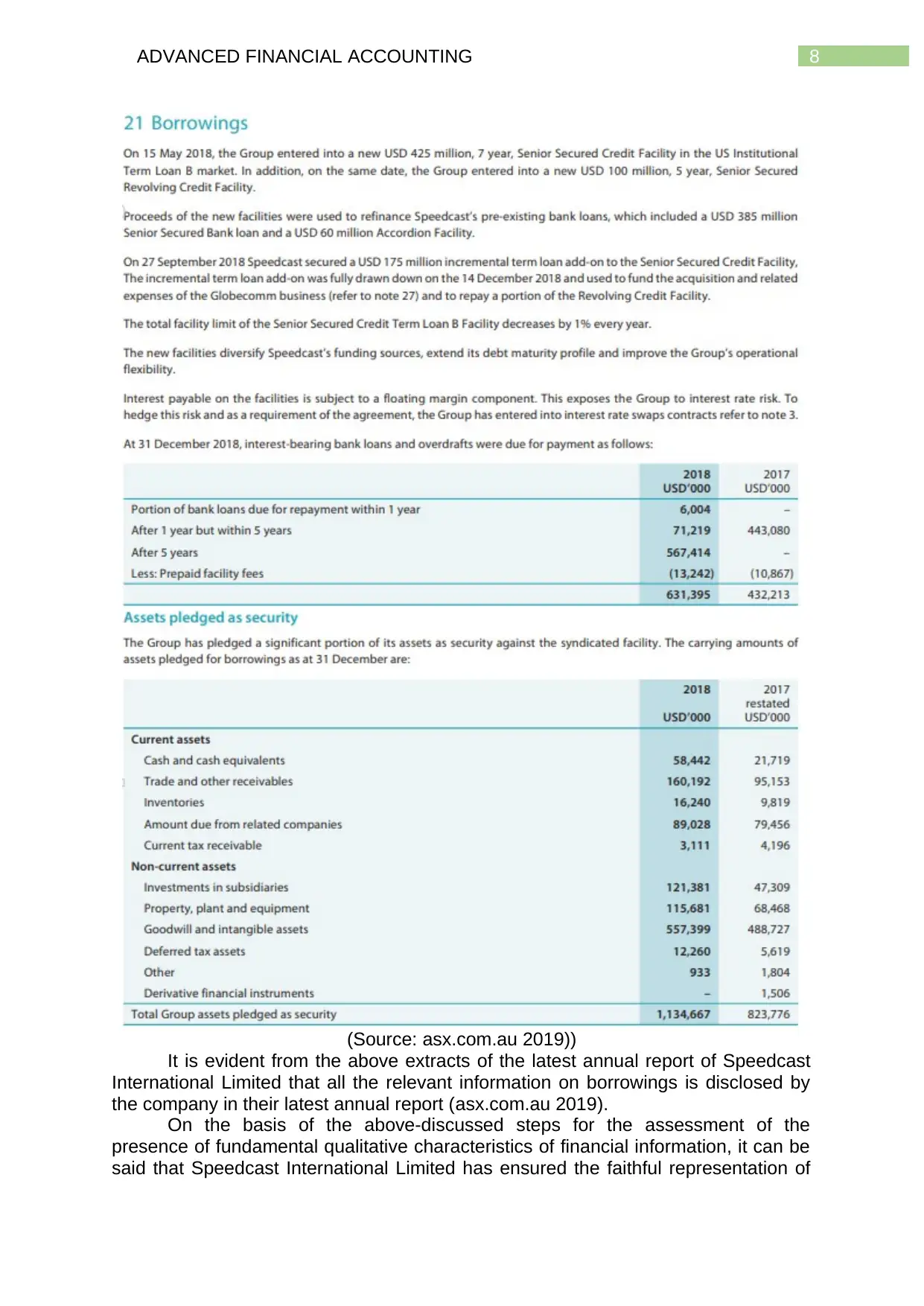

Borrowings – It is required for the users to acquire relevant information on the

liabilities of the companies in which borrowing form a major part (Hasan, Abdullah

and Hossain 2014). The types of relevant information on borrowings are their values

and recognition as well as measurement methodology adopted by Speedcast

International Limited.

According to the above extracts of the latest annual report of the company

shows that all the relevant information on the property, plant and equipment is

provided by the management such as net book value, reasons for the change in net

book value and policies related to measurement, depreciation, impairment and

others about these assets (Braam and Beest 2013). This is essential for the users of

the financial statements.

Inventories – Information about the inventories of the companies is essential for the

users due to the fact that they form a major part of the current assets of the

companies and their analysis helps in gauging the liquidity position as well as

working capital movement of those firms. Value of the inventories along with the

valuation methodology is most relevant information about this asset.

(Source: asx.com.au 2019)

It can be seen from the above that Speedcast International Limited has

disclosed all the relevant information on inventory in their latest annual report.

Borrowings – It is required for the users to acquire relevant information on the

liabilities of the companies in which borrowing form a major part (Hasan, Abdullah

and Hossain 2014). The types of relevant information on borrowings are their values

and recognition as well as measurement methodology adopted by Speedcast

International Limited.

8ADVANCED FINANCIAL ACCOUNTING

(Source: asx.com.au 2019))

It is evident from the above extracts of the latest annual report of Speedcast

International Limited that all the relevant information on borrowings is disclosed by

the company in their latest annual report (asx.com.au 2019).

On the basis of the above-discussed steps for the assessment of the

presence of fundamental qualitative characteristics of financial information, it can be

said that Speedcast International Limited has ensured the faithful representation of

(Source: asx.com.au 2019))

It is evident from the above extracts of the latest annual report of Speedcast

International Limited that all the relevant information on borrowings is disclosed by

the company in their latest annual report (asx.com.au 2019).

On the basis of the above-discussed steps for the assessment of the

presence of fundamental qualitative characteristics of financial information, it can be

said that Speedcast International Limited has ensured the faithful representation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED FINANCIAL ACCOUNTING

all the relevant information about the above-discussed three major economic

substances of their financial reporting. This information is crucial for the users of the

financial statements for making required decisions on Speedcast International

Limited.

Conclusion

The above discussion sheds light on some of the most crucial accounting

concepts that the companies are needed to consider for the purpose of financial

reporting. It can be seen from the above discussion that the management of

Speedcast International Limited has ensured the application of these accounting

concepts in the financial reporting for increasing the efficiency of financial reporting.

The above discussion also sheds light on the debate around the measurement

bases regarding the use of historical cost accounting and fair value accounting.

Proper examples from the 2018 Annual Report of Speedcast International Limited

are provided where it can be seen that the company has utilized both the

measurement bases on the basis of the nature of financial elements while complying

with the requirements of the AASB conceptual framework. The last part of the report

sheds light on the importance of two fundamental qualitative characteristics of

financial information which are relevance and faithful representation. Evidences from

the latest annual report of Speedcast International Limited are provided that support

the notion that the company has well complied with these two fundamental

characteristics in order to increase the usefulness of the financial information of their

business to the users of the financial statements.

all the relevant information about the above-discussed three major economic

substances of their financial reporting. This information is crucial for the users of the

financial statements for making required decisions on Speedcast International

Limited.

Conclusion

The above discussion sheds light on some of the most crucial accounting

concepts that the companies are needed to consider for the purpose of financial

reporting. It can be seen from the above discussion that the management of

Speedcast International Limited has ensured the application of these accounting

concepts in the financial reporting for increasing the efficiency of financial reporting.

The above discussion also sheds light on the debate around the measurement

bases regarding the use of historical cost accounting and fair value accounting.

Proper examples from the 2018 Annual Report of Speedcast International Limited

are provided where it can be seen that the company has utilized both the

measurement bases on the basis of the nature of financial elements while complying

with the requirements of the AASB conceptual framework. The last part of the report

sheds light on the importance of two fundamental qualitative characteristics of

financial information which are relevance and faithful representation. Evidences from

the latest annual report of Speedcast International Limited are provided that support

the notion that the company has well complied with these two fundamental

characteristics in order to increase the usefulness of the financial information of their

business to the users of the financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED FINANCIAL ACCOUNTING

References

Aasb.gov.au. 2019.Conceptual Framework for Financial Reporting. [online] Available

at: https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf

[Accessed 25 May 2019].

Asx.com.au. 2019. Speedcast International Limited: Annual Report 2018. [online]

Available at: https://www.asx.com.au/asxpdf/20190418/pdf/444f26fjf56yz5.pdf

[Accessed 27 May 2019].

Barth, M.E., 2013. Measurement in financial reporting: The need for

concepts. Accounting Horizons, 28(2), pp.331-352.

Braam, G.J.M. and Beest, F.V., 2013. A conceptually-based empirical analysis on

quality differences between UK annual reports and US 10-K reports.

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-

financial assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-

775.

Ellul, A., Jotikasthira, C., Lundblad, C.T. and Wang, Y., 2015. Is historical cost

accounting a panacea? Market stress, incentive distortions, and gains trading. The

Journal of Finance, 70(6), pp.2489-2538.

Flower, J., 2018. Global financial reporting. Macmillan International Higher

Education.

Hasan, M., Abdullah, S.N. and Hossain, S.Z.H., 2014. Qualitative characteristics of

financial reporting. The Pakistan Accountant, 50(1), pp.23-31.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting,

Binder Ready Version. John Wiley & Sons.

Palea, V., 2013. IAS/IFRS and financial reporting quality: Lessons from the

European experience. China Journal of Accounting Research, 6(4), pp.247-263.

Palea, V., 2014. Fair value accounting and its usefulness to financial statement

users. Journal of Financial Reporting and Accounting, 12(2), pp.102-116.

Ponomareva, S.V. and Melnikova, A.S., 2015. Financial instruments reflected by

organizations in accordance with international standards of financial accounting of

public sector. Mediterranean Journal of Social Sciences, 6(3 S3), p.213.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting:

issues, concepts and practice. Routledge.

Tsoncheva, G., 2014. Measuring and assessing the quality and usefulness of

accounting information. Izvestiya, (1), pp.52-64.

Wang, J.L., 2013. Accounting conservatism and information asymmetry: Evidence

from Taiwan. International Business Research, 6(7), p.32.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction

to concepts, methods and uses. Cengage Learning.

References

Aasb.gov.au. 2019.Conceptual Framework for Financial Reporting. [online] Available

at: https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf

[Accessed 25 May 2019].

Asx.com.au. 2019. Speedcast International Limited: Annual Report 2018. [online]

Available at: https://www.asx.com.au/asxpdf/20190418/pdf/444f26fjf56yz5.pdf

[Accessed 27 May 2019].

Barth, M.E., 2013. Measurement in financial reporting: The need for

concepts. Accounting Horizons, 28(2), pp.331-352.

Braam, G.J.M. and Beest, F.V., 2013. A conceptually-based empirical analysis on

quality differences between UK annual reports and US 10-K reports.

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-

financial assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-

775.

Ellul, A., Jotikasthira, C., Lundblad, C.T. and Wang, Y., 2015. Is historical cost

accounting a panacea? Market stress, incentive distortions, and gains trading. The

Journal of Finance, 70(6), pp.2489-2538.

Flower, J., 2018. Global financial reporting. Macmillan International Higher

Education.

Hasan, M., Abdullah, S.N. and Hossain, S.Z.H., 2014. Qualitative characteristics of

financial reporting. The Pakistan Accountant, 50(1), pp.23-31.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting,

Binder Ready Version. John Wiley & Sons.

Palea, V., 2013. IAS/IFRS and financial reporting quality: Lessons from the

European experience. China Journal of Accounting Research, 6(4), pp.247-263.

Palea, V., 2014. Fair value accounting and its usefulness to financial statement

users. Journal of Financial Reporting and Accounting, 12(2), pp.102-116.

Ponomareva, S.V. and Melnikova, A.S., 2015. Financial instruments reflected by

organizations in accordance with international standards of financial accounting of

public sector. Mediterranean Journal of Social Sciences, 6(3 S3), p.213.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting:

issues, concepts and practice. Routledge.

Tsoncheva, G., 2014. Measuring and assessing the quality and usefulness of

accounting information. Izvestiya, (1), pp.52-64.

Wang, J.L., 2013. Accounting conservatism and information asymmetry: Evidence

from Taiwan. International Business Research, 6(7), p.32.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction

to concepts, methods and uses. Cengage Learning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.