Financial Reporting: AASB Framework, Elements, and Asset Measurement

VerifiedAdded on 2023/06/05

|16

|3317

|395

Report

AI Summary

This report provides an in-depth analysis of the Australian Accounting Standards Board's (AASB) conceptual framework, particularly the amendments made in 2014. It assesses the core elements of financial statements, including assets, liabilities, equity, income, and expenses, in accordance with AASB guidelines. The report compares and contrasts the definitions and recognition criteria for these elements, evaluates the essential characteristics of assets, and examines various measurement bases such as historical cost, current cost, settlement value, and present value. It further discusses the preference for historical cost in asset measurement and its role in promoting the stewardship function of accounting. The report also references disclosure practices in financial reporting and includes an analysis of the measurement and reporting system of an ASX-listed company, Infigen Energy, using its balance sheet as an example. The analysis highlights the practical application of AASB standards and their impact on financial reporting.

Theory and Current Issues in Accounting 1

Theory and Current Issues in Accounting

Theory and Current Issues in Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Theory and Current Issues in Accounting 2

Executive summary

The Australian conceptual framework is amended according to the need or changes in the

financial reporting or disclosure of financial information of an entity. In relation to this report,

latest conceptual framework by the Australian Accounting Standard Board is evaluated as per the

new framework amended in year 2014. In addition to this, the elements of financial statement as

assets, liabilities, equity, revenues and expenses are assessed with reference to the AASB 2014.

In addition to this, the measurement bases for the assets measurement are assessed in the

accounting standard context. Along with this, the measurement bases for the assets such as

historical cost, settlement cost, current cost and the present value are also elaborated along with

this stewardship function of accounting under the Australian Accounting Standard Board agency.

Apart from this, the preference of historical cost for the measurement of assets is also evaluated

under the Australian conceptual framework of Australian.

Executive summary

The Australian conceptual framework is amended according to the need or changes in the

financial reporting or disclosure of financial information of an entity. In relation to this report,

latest conceptual framework by the Australian Accounting Standard Board is evaluated as per the

new framework amended in year 2014. In addition to this, the elements of financial statement as

assets, liabilities, equity, revenues and expenses are assessed with reference to the AASB 2014.

In addition to this, the measurement bases for the assets measurement are assessed in the

accounting standard context. Along with this, the measurement bases for the assets such as

historical cost, settlement cost, current cost and the present value are also elaborated along with

this stewardship function of accounting under the Australian Accounting Standard Board agency.

Apart from this, the preference of historical cost for the measurement of assets is also evaluated

under the Australian conceptual framework of Australian.

Theory and Current Issues in Accounting 3

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Assessment of elements of financial statement...............................................................................5

Compare and contrast between the definition and the recognition of elements in the financial

statements........................................................................................................................................7

Evaluate the nature of the essential characteristics of assets...........................................................7

Assessment of measurement criteria for assets which is recognized in accounting framework

2014.................................................................................................................................................8

Preference of assets measurement by historical cost and promoting the stewardship function of

accounting........................................................................................................................................9

Reference about the disclosure practice in financial reporting......................................................10

Analysis of measurement and reporting system of an ASX listed company.................................11

Balance sheet of ASX listed Company: Infigen Energy...........................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Assessment of elements of financial statement...............................................................................5

Compare and contrast between the definition and the recognition of elements in the financial

statements........................................................................................................................................7

Evaluate the nature of the essential characteristics of assets...........................................................7

Assessment of measurement criteria for assets which is recognized in accounting framework

2014.................................................................................................................................................8

Preference of assets measurement by historical cost and promoting the stewardship function of

accounting........................................................................................................................................9

Reference about the disclosure practice in financial reporting......................................................10

Analysis of measurement and reporting system of an ASX listed company.................................11

Balance sheet of ASX listed Company: Infigen Energy...........................................................12

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Theory and Current Issues in Accounting 4

Introduction

The main aim of this report is to engage with the assessment of Australian Accounting Standards

Board’s currently amended accounting framework in the year 2014. In addition to this, the

financial reporting is assessed with respect to the elements of financial statement according to the

Australian Accounting Framework. Along with this, the theories and the issues in concern of

AASB are interpreted at the time of preparing the financial information about the companies. On

the other hand, recognition of financial statement elements is also assessed under the accounting

theories. In context to this, the measurement basis for the elements of financial statements is also

chosen in appropriate manner. The additional disclosures which are required in disclosing the

financial statement preparation is determined as per the conceptual framework of Australian

Accounting Standard Board’s which is amended in the year 2014. In relation to this, the nature

and essential characteristics of assets are discussed as per the accounting rules and regulations.

The evaluation is also carried with the recognition of criteria for assets in accounting framework

2014. Further, the preference of accounting for measuring the historical cost is also assessed

along with the stewardship function of accounting. The measurement and reporting of assets

under the ASX listed companies are analyzed is also stated as per the annual report statement.

Introduction

The main aim of this report is to engage with the assessment of Australian Accounting Standards

Board’s currently amended accounting framework in the year 2014. In addition to this, the

financial reporting is assessed with respect to the elements of financial statement according to the

Australian Accounting Framework. Along with this, the theories and the issues in concern of

AASB are interpreted at the time of preparing the financial information about the companies. On

the other hand, recognition of financial statement elements is also assessed under the accounting

theories. In context to this, the measurement basis for the elements of financial statements is also

chosen in appropriate manner. The additional disclosures which are required in disclosing the

financial statement preparation is determined as per the conceptual framework of Australian

Accounting Standard Board’s which is amended in the year 2014. In relation to this, the nature

and essential characteristics of assets are discussed as per the accounting rules and regulations.

The evaluation is also carried with the recognition of criteria for assets in accounting framework

2014. Further, the preference of accounting for measuring the historical cost is also assessed

along with the stewardship function of accounting. The measurement and reporting of assets

under the ASX listed companies are analyzed is also stated as per the annual report statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Theory and Current Issues in Accounting 5

Assessment of elements of financial statement

The Australian Accounting Standard Board is one of the major Australian agencies which are

committed towards developing and maintaining the financial reporting of companies that comes

under the Australian Accounting Board. The standards are developed by the AASB in order to

maintain the regulations over the private and public entities. Australian Accounting Standard

Board develops the conceptual framework so that the accounting standards can be assessed in

relevant manner. The conceptual framework is used in the financial reporting under AASB

standard and it employed as the theory of accounting through which the practical problem can be

resolved in significant manner (Henderson et. al, 2015). The main purpose of this conceptual

framework is to assist the IASB in order to developing the financial reporting and maintaining

the policies which are not exist in the concurrent accounting standards. The accounting standard

as AASB 101 is concerned to the preparation and reporting of financial statement of entities.

The position of financial statement is determined with the several elements and items that are

reported by the companies under the rules and regulations of AASB. The major elements of

financial reporting is as follows

Assets

The asset is one of the important elements of financial reporting by Australian Accounting

Boards. The assets can be termed as a resource for the business which portrays the results of past

activities of entity operations by which the future benefits for the entities in terms of economical

aspects can be obtained.

Liabilities

Assessment of elements of financial statement

The Australian Accounting Standard Board is one of the major Australian agencies which are

committed towards developing and maintaining the financial reporting of companies that comes

under the Australian Accounting Board. The standards are developed by the AASB in order to

maintain the regulations over the private and public entities. Australian Accounting Standard

Board develops the conceptual framework so that the accounting standards can be assessed in

relevant manner. The conceptual framework is used in the financial reporting under AASB

standard and it employed as the theory of accounting through which the practical problem can be

resolved in significant manner (Henderson et. al, 2015). The main purpose of this conceptual

framework is to assist the IASB in order to developing the financial reporting and maintaining

the policies which are not exist in the concurrent accounting standards. The accounting standard

as AASB 101 is concerned to the preparation and reporting of financial statement of entities.

The position of financial statement is determined with the several elements and items that are

reported by the companies under the rules and regulations of AASB. The major elements of

financial reporting is as follows

Assets

The asset is one of the important elements of financial reporting by Australian Accounting

Boards. The assets can be termed as a resource for the business which portrays the results of past

activities of entity operations by which the future benefits for the entities in terms of economical

aspects can be obtained.

Liabilities

Theory and Current Issues in Accounting 6

The liabilities are defined by the Australian Accounting Standard Board under the conceptual

framework as the obligation of the company which occurs due to the past operational activities

of entity which results into an outflow from the available resources of entity (Ordelheide, 2016).

Equity

The equity of entity is defined as the residual value of the assets of company which is determined

from the assets after reducing the perceived liabilities over the entity in a specified financial year.

The equity is reported under the sub-classification state of balance sheet. For instance, the equity

can be as reserves, retained earnings and retaining under the capital adjustment.

Performance

The performance of entity’s activities is determined from the operations of business and the

results are generated as the profit. The profit can be meaning as the earnings on the per share

capital of the entity.

Income

The income is the results of significant entity’s operations which arise from the operations of

business activity as sales, interest, rent and dividends (Dagwell et. al, 2015).

Expenses

The expenses are also the major elements of financial reporting that are portrays as the loss or

spending which increases due to the daily business activities of entity. The expenses can be

included as the cost for selling goods, depreciation of assets, payment of wages and salaries and

outflow for meeting the need of economic performance.

The liabilities are defined by the Australian Accounting Standard Board under the conceptual

framework as the obligation of the company which occurs due to the past operational activities

of entity which results into an outflow from the available resources of entity (Ordelheide, 2016).

Equity

The equity of entity is defined as the residual value of the assets of company which is determined

from the assets after reducing the perceived liabilities over the entity in a specified financial year.

The equity is reported under the sub-classification state of balance sheet. For instance, the equity

can be as reserves, retained earnings and retaining under the capital adjustment.

Performance

The performance of entity’s activities is determined from the operations of business and the

results are generated as the profit. The profit can be meaning as the earnings on the per share

capital of the entity.

Income

The income is the results of significant entity’s operations which arise from the operations of

business activity as sales, interest, rent and dividends (Dagwell et. al, 2015).

Expenses

The expenses are also the major elements of financial reporting that are portrays as the loss or

spending which increases due to the daily business activities of entity. The expenses can be

included as the cost for selling goods, depreciation of assets, payment of wages and salaries and

outflow for meeting the need of economic performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Theory and Current Issues in Accounting 7

Compare and contrast between the definition and the recognition of elements in the

financial statements

The Australian Accounting Standard Board has set the definition and the recognition criteria for

the elements of financial statements. From the conceptual framework of AASB, the comparison

and contrast over the elements of financial statement is as the assets are defined as the future

economic benefits but the recognition state as the probability of assets to be recognized under the

statement of financial position. On the other hand, assets recognition criteria for the assets are

also endowed as the cost or other value so that the reliability can be determined. In context to the

liability elements, the definition is deterred as the obligation as future scarifies from entity

(Horngren and Harrison, 2015). The recognition criteria are determined as the economic benefits

will be required. Recognition also states that liability can easily measure the reliability.

Furthermore, equity is defined as the residential value but the recognition described that the

equity is reported as the results of deducted value from its assets. Moreover, the revenues are

determined as the inflow of future economics but the recognition is described as only when the

expenses are probable to increase the assets of entity. On the other hand, expenses are the loss

value for the operational activities of entity (Readyratios, 2018). In contrast to this, the

recognition of expenses is conceptualized as the future economic values can be improved in

reliable manner. The expenses are the recognized consumption or reduction of assets from its

book value.

Evaluate the nature of the essential characteristics of assets

The nature of the essential characteristics of assets is as that there should be future economic

benefits from the recognition of asset in its operating statement. Along with this, another

characteristic is detained as the entity should have proper control and monitoring over the assets

Compare and contrast between the definition and the recognition of elements in the

financial statements

The Australian Accounting Standard Board has set the definition and the recognition criteria for

the elements of financial statements. From the conceptual framework of AASB, the comparison

and contrast over the elements of financial statement is as the assets are defined as the future

economic benefits but the recognition state as the probability of assets to be recognized under the

statement of financial position. On the other hand, assets recognition criteria for the assets are

also endowed as the cost or other value so that the reliability can be determined. In context to the

liability elements, the definition is deterred as the obligation as future scarifies from entity

(Horngren and Harrison, 2015). The recognition criteria are determined as the economic benefits

will be required. Recognition also states that liability can easily measure the reliability.

Furthermore, equity is defined as the residential value but the recognition described that the

equity is reported as the results of deducted value from its assets. Moreover, the revenues are

determined as the inflow of future economics but the recognition is described as only when the

expenses are probable to increase the assets of entity. On the other hand, expenses are the loss

value for the operational activities of entity (Readyratios, 2018). In contrast to this, the

recognition of expenses is conceptualized as the future economic values can be improved in

reliable manner. The expenses are the recognized consumption or reduction of assets from its

book value.

Evaluate the nature of the essential characteristics of assets

The nature of the essential characteristics of assets is as that there should be future economic

benefits from the recognition of asset in its operating statement. Along with this, another

characteristic is detained as the entity should have proper control and monitoring over the assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Theory and Current Issues in Accounting 8

of the company so that the benefits can easily be accessed (AASB, 2016). On the other hand, it is

also endowed that the transaction that is taking place in the control and measuring of financial

statement should also be covered in the context of future economic benefits. Along with this, the

nature of characteristics of assets is that it is acquired at a cost which is incurred for the entity.

Moreover, the legal enforceability might also be an essential characteristic of assets so that the

assets can measured in proper manner.

Assessment of measurement criteria for assets which is recognized in accounting

framework 2014

The measurement of financial statement’s elements is also a crucial aspect for the entity under

the Australian Accenting Standard Board. Measurement can be determined as the process in

which the monetary value of elements is recognized and the amount of elements is carried out in

respective to the income statement and balance sheet. There are number bases through which the

asset of entity is measured under the amended ASSB 2014.

In context to the asset, the assets are measured by the historical cost in which the assets are

recorded at the amount for which it is acquired in the terms of cash of cash equitant

consideration value. On the other hand, current cost measurement bases are also applied over the

asset measurement in which the asset is carried out. In addition to this, the assets are also

measured over the realizable or settlement value of the assets at which the cash or cash equitant

amount is paid with the selling of an asset in disposal manner (Legislation, 2013). In comparison

to this, the assets can also be measured by the present value bases which the assets are measured

at the present discount value from the net cash inflow; by this amount the item might generate

the operating activities for business.

of the company so that the benefits can easily be accessed (AASB, 2016). On the other hand, it is

also endowed that the transaction that is taking place in the control and measuring of financial

statement should also be covered in the context of future economic benefits. Along with this, the

nature of characteristics of assets is that it is acquired at a cost which is incurred for the entity.

Moreover, the legal enforceability might also be an essential characteristic of assets so that the

assets can measured in proper manner.

Assessment of measurement criteria for assets which is recognized in accounting

framework 2014

The measurement of financial statement’s elements is also a crucial aspect for the entity under

the Australian Accenting Standard Board. Measurement can be determined as the process in

which the monetary value of elements is recognized and the amount of elements is carried out in

respective to the income statement and balance sheet. There are number bases through which the

asset of entity is measured under the amended ASSB 2014.

In context to the asset, the assets are measured by the historical cost in which the assets are

recorded at the amount for which it is acquired in the terms of cash of cash equitant

consideration value. On the other hand, current cost measurement bases are also applied over the

asset measurement in which the asset is carried out. In addition to this, the assets are also

measured over the realizable or settlement value of the assets at which the cash or cash equitant

amount is paid with the selling of an asset in disposal manner (Legislation, 2013). In comparison

to this, the assets can also be measured by the present value bases which the assets are measured

at the present discount value from the net cash inflow; by this amount the item might generate

the operating activities for business.

Theory and Current Issues in Accounting 9

Preference of assets measurement by historical cost and promoting the stewardship

function of accounting

The accounting standards changes time to time when there is a need of changes in the financial

reporting system of accounting and the new and suitable method and base is adopted for the

measurement of assets in the income statement and the balance sheet. The accountant basically

uses the historical cost of measurement method for the assets determination for the entity. The

main reason behind the adoption and following the historical cost method is that the market

value of assets changes according to the movement in the market fluctuation that the whole

reporting of assets are distorted than the accountants do not wants to create hurdles in the

recording of financial information in the income statements and balance sheet. At the same time,

the historical cost is reliable base for the assets measurement as it is supportive to make the

comparison in between the assets of entity. Along with this, using historical cost base for assets

management, it enables the accountants to maintain the transparency in the reporting of

accounting information (AASB, 2017). On the other hand, using another methods as present

value of settled value base might be resulted into understate or overstate of assets valuation for

the perspective entity. Along with this, the historical cost is also used as this base is suitable

principle for trading off in between the usefulness and reliability.

In context to the accounting stewardship, it is used by the accountant in the reporting of financial

information under the objectives of financial reporting. The accountant uses the stewardship

function in efficient decision making for the reporting of information as they follow the ethical

responsibility in order to take care about the depiction of reliable and important information for

Preference of assets measurement by historical cost and promoting the stewardship

function of accounting

The accounting standards changes time to time when there is a need of changes in the financial

reporting system of accounting and the new and suitable method and base is adopted for the

measurement of assets in the income statement and the balance sheet. The accountant basically

uses the historical cost of measurement method for the assets determination for the entity. The

main reason behind the adoption and following the historical cost method is that the market

value of assets changes according to the movement in the market fluctuation that the whole

reporting of assets are distorted than the accountants do not wants to create hurdles in the

recording of financial information in the income statements and balance sheet. At the same time,

the historical cost is reliable base for the assets measurement as it is supportive to make the

comparison in between the assets of entity. Along with this, using historical cost base for assets

management, it enables the accountants to maintain the transparency in the reporting of

accounting information (AASB, 2017). On the other hand, using another methods as present

value of settled value base might be resulted into understate or overstate of assets valuation for

the perspective entity. Along with this, the historical cost is also used as this base is suitable

principle for trading off in between the usefulness and reliability.

In context to the accounting stewardship, it is used by the accountant in the reporting of financial

information under the objectives of financial reporting. The accountant uses the stewardship

function in efficient decision making for the reporting of information as they follow the ethical

responsibility in order to take care about the depiction of reliable and important information for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Theory and Current Issues in Accounting 10

the users. In addition to this, the accountant has also adopted the ethical practices as per the

stewardship function of accounting report under the Australian conceptual framework.

Reference about the disclosure practice in financial reporting

According to Australian Accounting Framework, the Exposure Draft includes complicated

concepts that illustrate what information should be shown in the financial statements, and how

that information is need to be disclosed. The IASB has also worked on the Disclosure Initiative,

which is a set research projects designed to enhance the disclosure requirements in the financial

reporting (Kent, & Zunker, 2017). In the Disclosure Initiative, the Australian Accounting Board

seeks to expand the theory contained in this Exposure Draft in order to provide further regulation

on disclosure and presentation. In addition to this, the Accounting Framework has undertaken a

research project for discovering whether it adds to the performance reporting transparency in the

financial statements.

The framework, 2014 has described that all those accounting items that show essential attributes

but unable to fulfill the criteria for recognition in the financial statements are not required to be

disclosed in the clarifying material, notes, or any complementary schedules. However, this is

allowed only when the knowledge of the item is considered significant for the assessment of the

financial state, and changes in it of a firm by the stakeholders of financial statements (Kent, &

Zunker, 2017). Moreover, the standard setters view this known information as more valuable

than the disclosed information. This is mainly due to the fact that the recognized information is

most likely to be more appropriate and reliable. However, The Framework 2014 recognition

states that the all those financial items that meet all the criteria of financial statement but fail any

of the recognition criteria are required to be disclosed in the notes by every entity.

the users. In addition to this, the accountant has also adopted the ethical practices as per the

stewardship function of accounting report under the Australian conceptual framework.

Reference about the disclosure practice in financial reporting

According to Australian Accounting Framework, the Exposure Draft includes complicated

concepts that illustrate what information should be shown in the financial statements, and how

that information is need to be disclosed. The IASB has also worked on the Disclosure Initiative,

which is a set research projects designed to enhance the disclosure requirements in the financial

reporting (Kent, & Zunker, 2017). In the Disclosure Initiative, the Australian Accounting Board

seeks to expand the theory contained in this Exposure Draft in order to provide further regulation

on disclosure and presentation. In addition to this, the Accounting Framework has undertaken a

research project for discovering whether it adds to the performance reporting transparency in the

financial statements.

The framework, 2014 has described that all those accounting items that show essential attributes

but unable to fulfill the criteria for recognition in the financial statements are not required to be

disclosed in the clarifying material, notes, or any complementary schedules. However, this is

allowed only when the knowledge of the item is considered significant for the assessment of the

financial state, and changes in it of a firm by the stakeholders of financial statements (Kent, &

Zunker, 2017). Moreover, the standard setters view this known information as more valuable

than the disclosed information. This is mainly due to the fact that the recognized information is

most likely to be more appropriate and reliable. However, The Framework 2014 recognition

states that the all those financial items that meet all the criteria of financial statement but fail any

of the recognition criteria are required to be disclosed in the notes by every entity.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Theory and Current Issues in Accounting 11

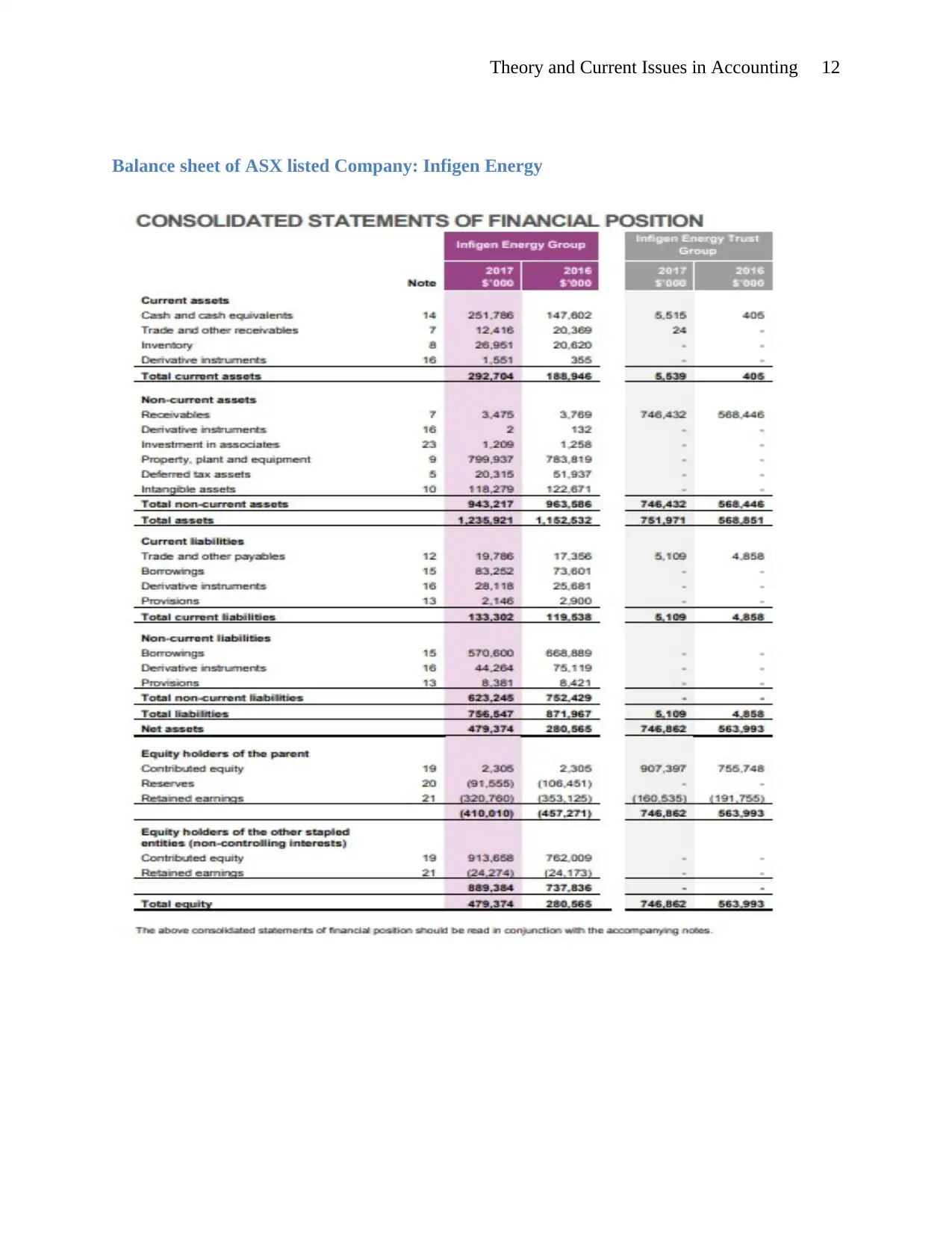

Analysis of measurement and reporting system of an ASX listed company

In order to determine the measurement and reporting system of ASX listed companies, Infigen

Energy business has been referenced for the assets reporting and measurement in the balance

sheet of company for the year 2017.

From the consideration of balance sheet of Infigen energy 2017, it is determined that the assets

of company as plant, property and equipments, the major assets for the company are as wind

turbines and associated plant of the company. In relation to the measurement and reporting of

assets, the assets are measured at the cost of the asset by less accumulated depreciation and

impairment method. In relation to the cost of assets is reported as the expense that occurred

while acquitting the assets (Southeast, 2017). On the other hand, the assets of company which are

under construction have not been considered for depreciation. Along with this, the intangible

assets of the company are valued at the fair value of the net assets and contingent liability which

are acquired at the date of reporting. Moreover, the inventories of the Infigen energy business are

measured at the lower of cost and net realizable value.

According to the Australian Accounting Standards, every ASX listed company is required by the

statue to produce an annual report, basically in 2 parts. The first part is descriptive, providing

relevant information about the entity’s operations while the other part illustrates the set of

accounts such as profit and loss account, a balance sheet, and cash flow statement along with the

notes to accounts (Chandrakumara et al., 2018). Also, the Board requires the company to provide

all the stakeholders with a true picture of the financial health of the company. These documents

are fundamental for providing financial reporting to the users.

Analysis of measurement and reporting system of an ASX listed company

In order to determine the measurement and reporting system of ASX listed companies, Infigen

Energy business has been referenced for the assets reporting and measurement in the balance

sheet of company for the year 2017.

From the consideration of balance sheet of Infigen energy 2017, it is determined that the assets

of company as plant, property and equipments, the major assets for the company are as wind

turbines and associated plant of the company. In relation to the measurement and reporting of

assets, the assets are measured at the cost of the asset by less accumulated depreciation and

impairment method. In relation to the cost of assets is reported as the expense that occurred

while acquitting the assets (Southeast, 2017). On the other hand, the assets of company which are

under construction have not been considered for depreciation. Along with this, the intangible

assets of the company are valued at the fair value of the net assets and contingent liability which

are acquired at the date of reporting. Moreover, the inventories of the Infigen energy business are

measured at the lower of cost and net realizable value.

According to the Australian Accounting Standards, every ASX listed company is required by the

statue to produce an annual report, basically in 2 parts. The first part is descriptive, providing

relevant information about the entity’s operations while the other part illustrates the set of

accounts such as profit and loss account, a balance sheet, and cash flow statement along with the

notes to accounts (Chandrakumara et al., 2018). Also, the Board requires the company to provide

all the stakeholders with a true picture of the financial health of the company. These documents

are fundamental for providing financial reporting to the users.

Theory and Current Issues in Accounting 12

Balance sheet of ASX listed Company: Infigen Energy

Balance sheet of ASX listed Company: Infigen Energy

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.