Accounting Assignment: AASB 16, AASB 15, and Financial Statements

VerifiedAdded on 2021/05/31

|12

|1961

|218

Homework Assignment

AI Summary

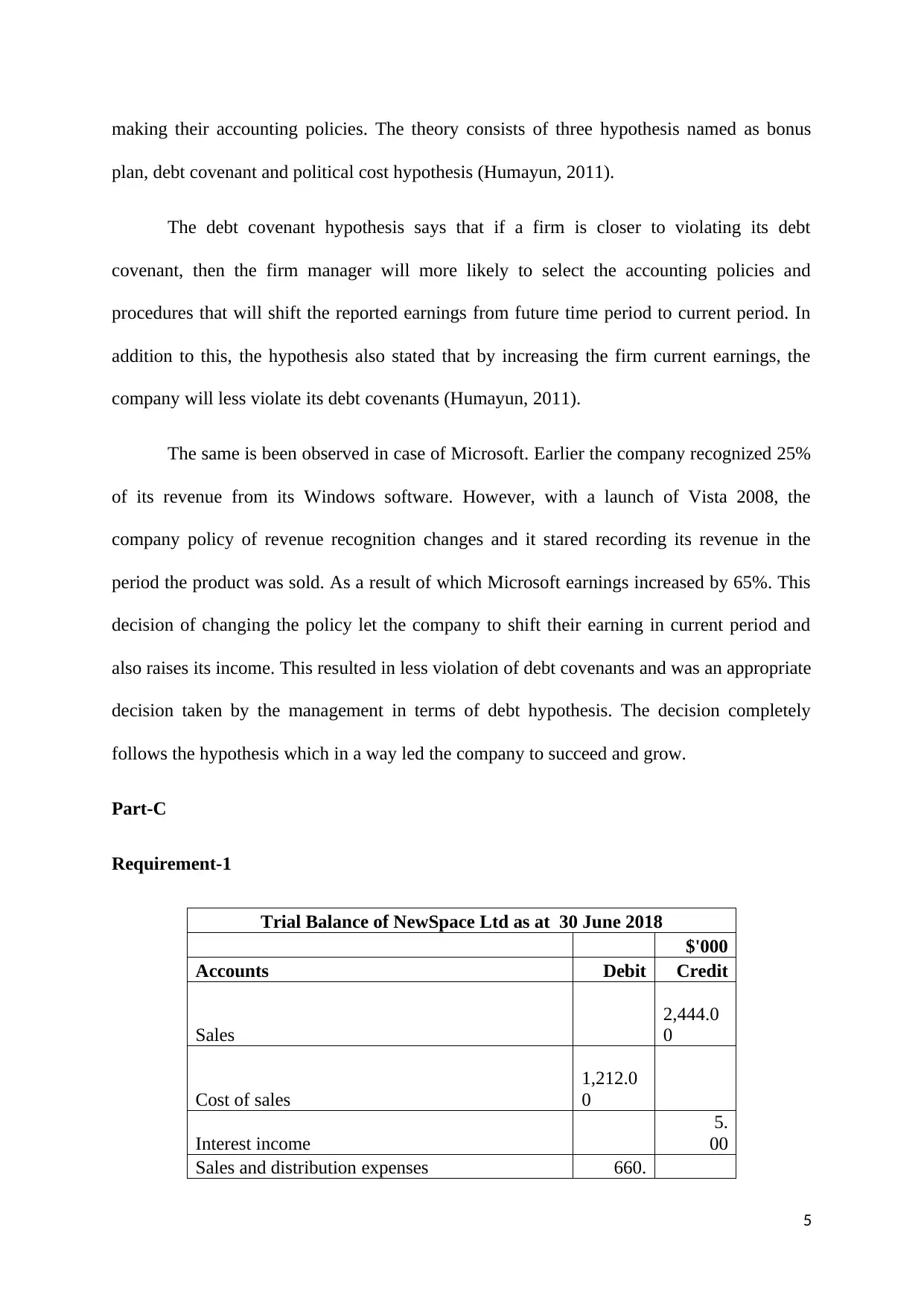

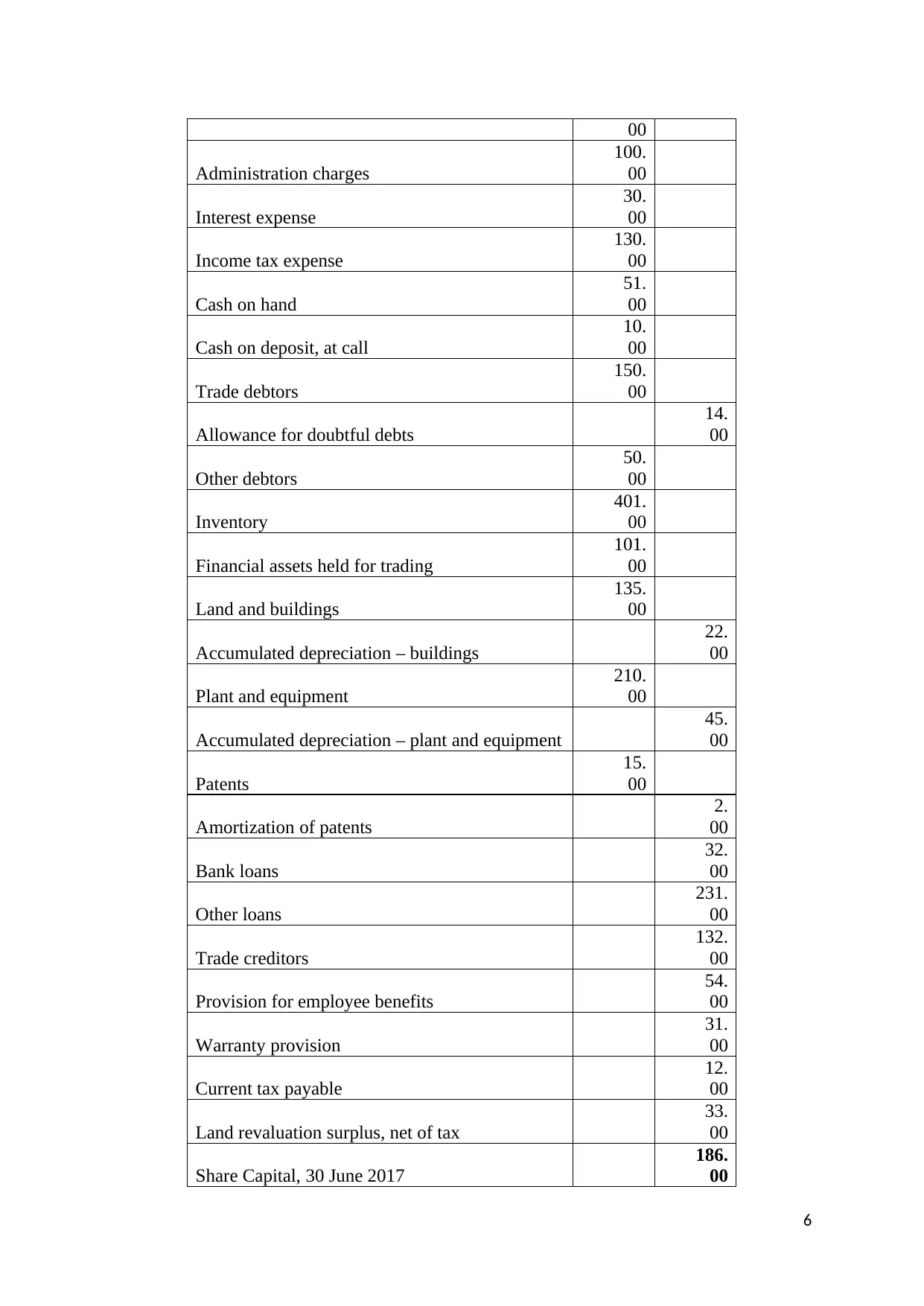

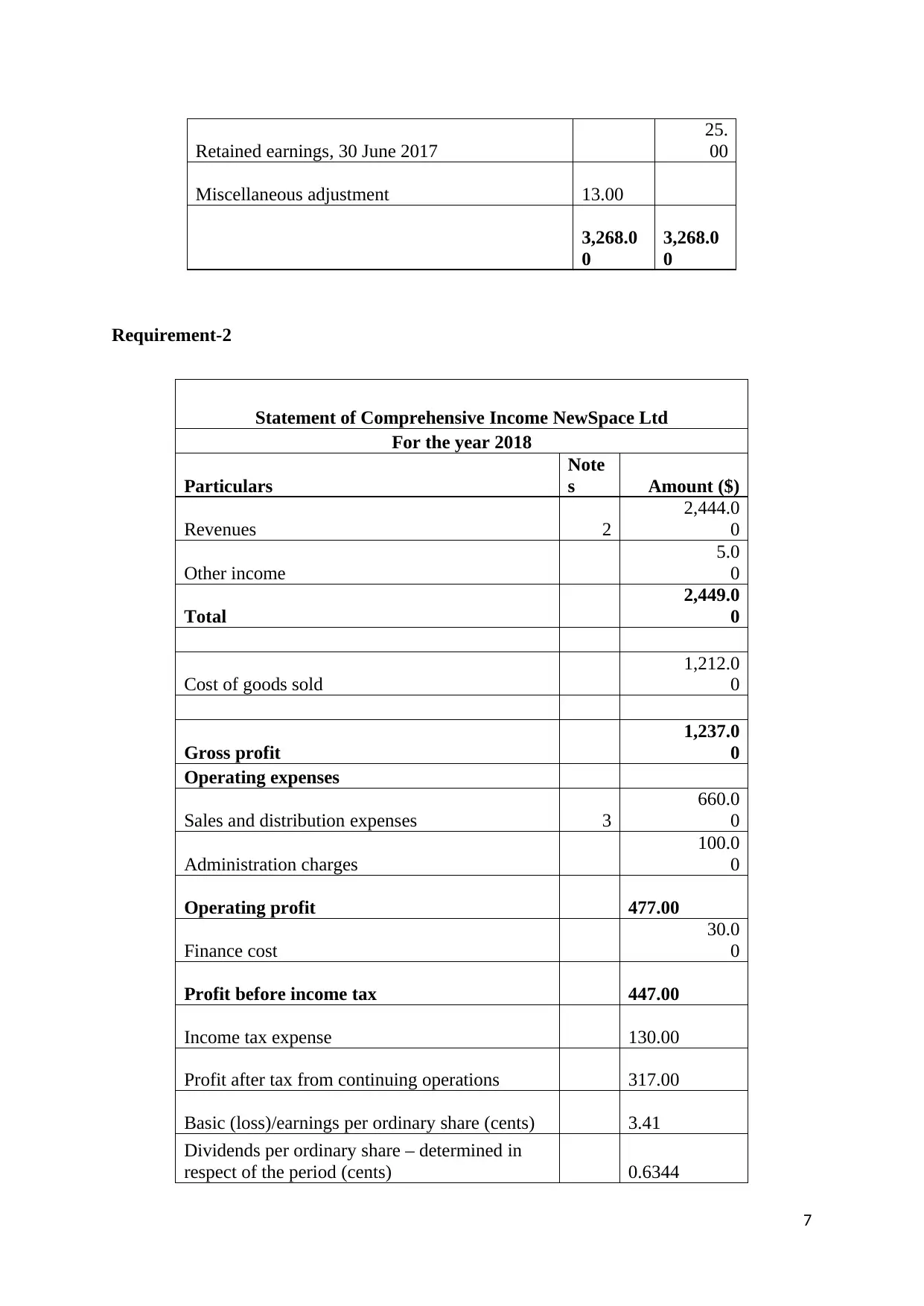

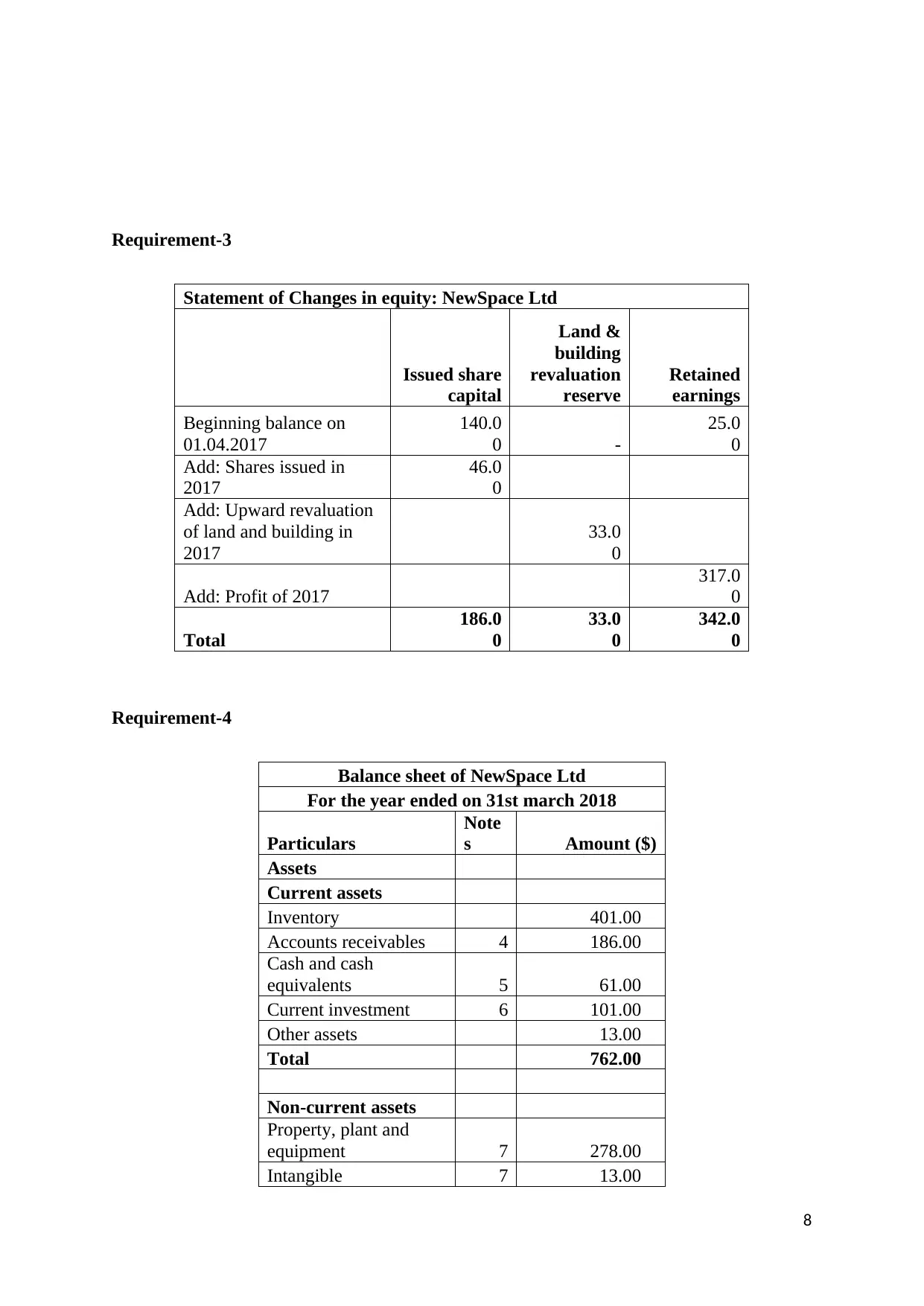

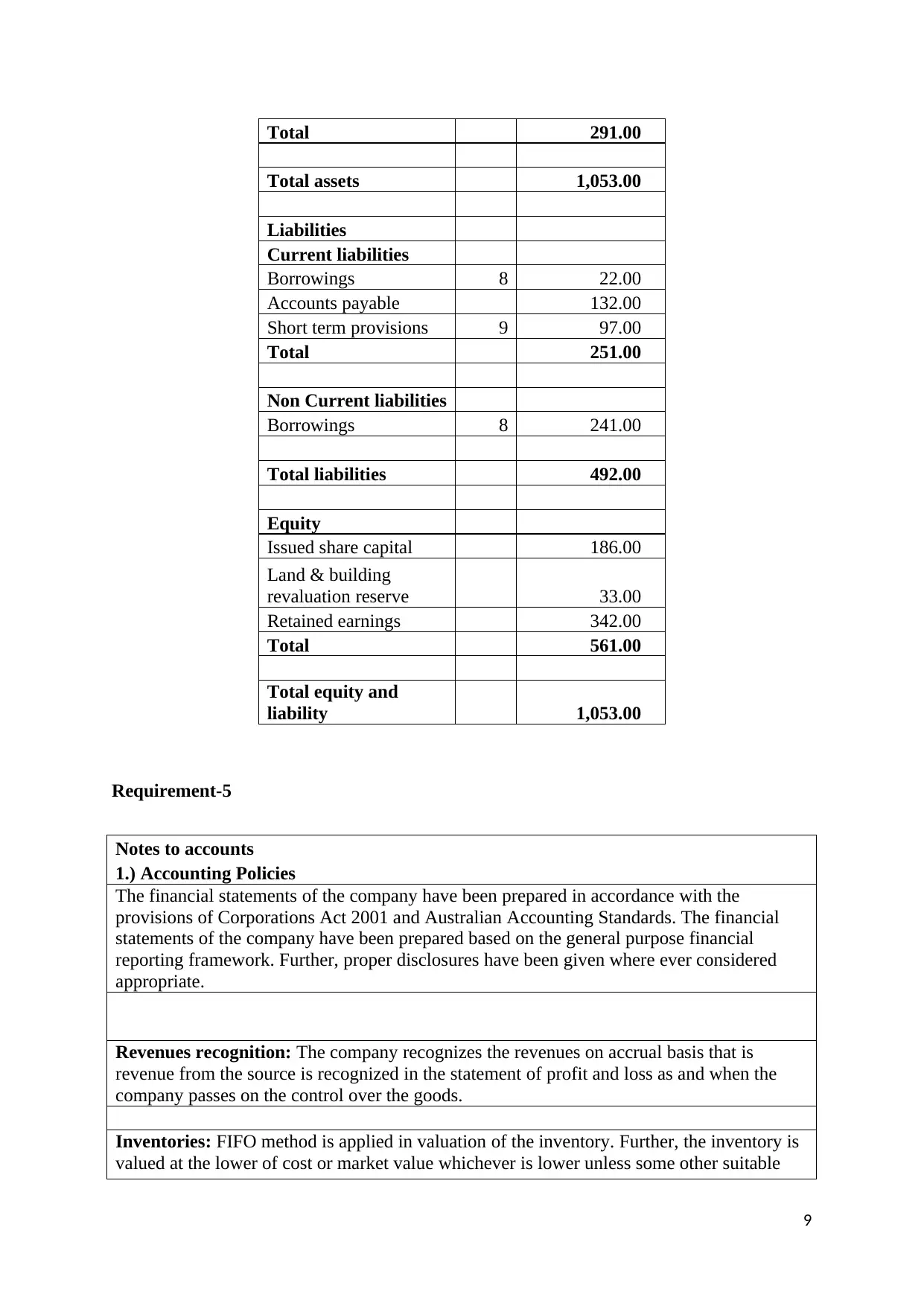

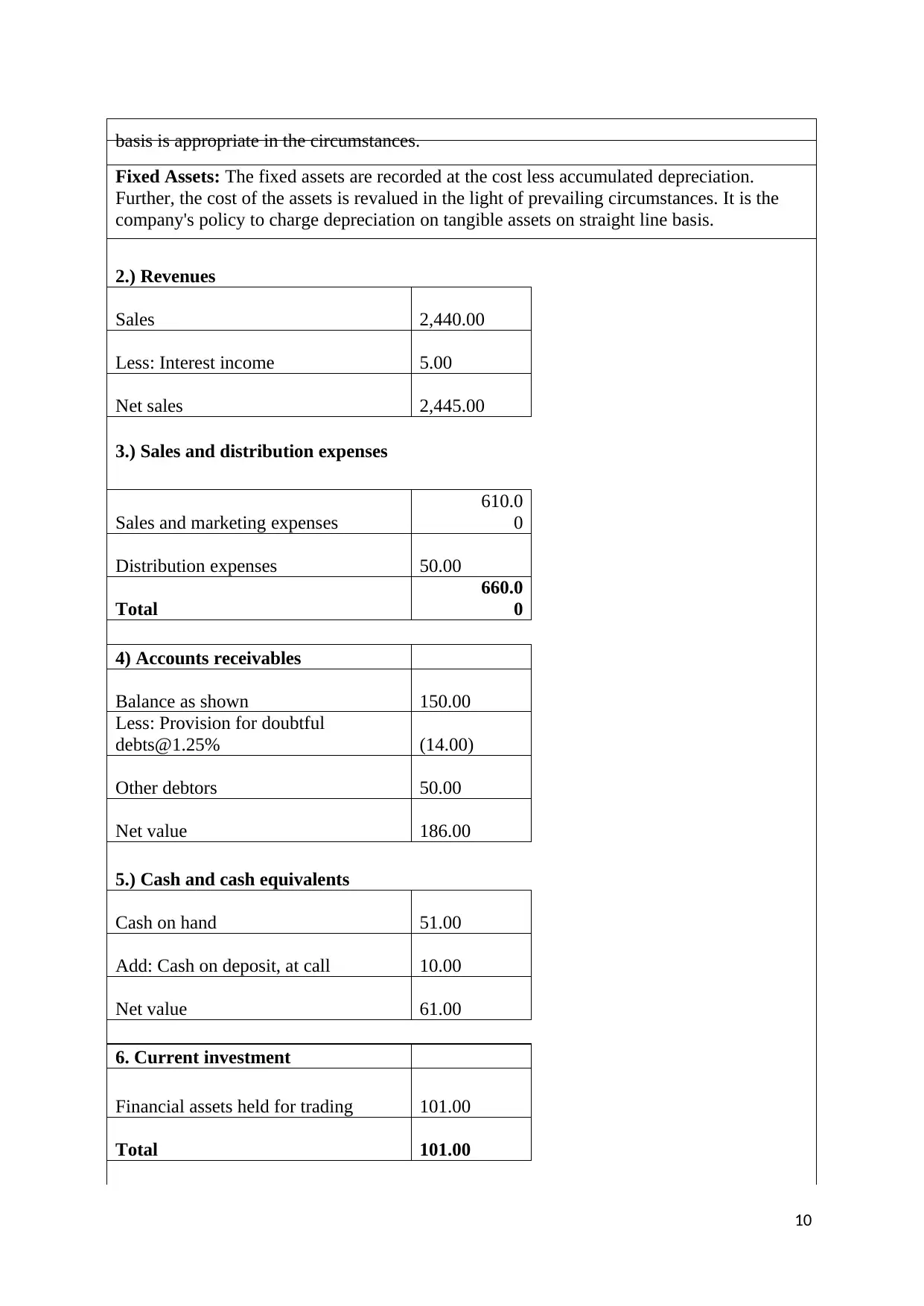

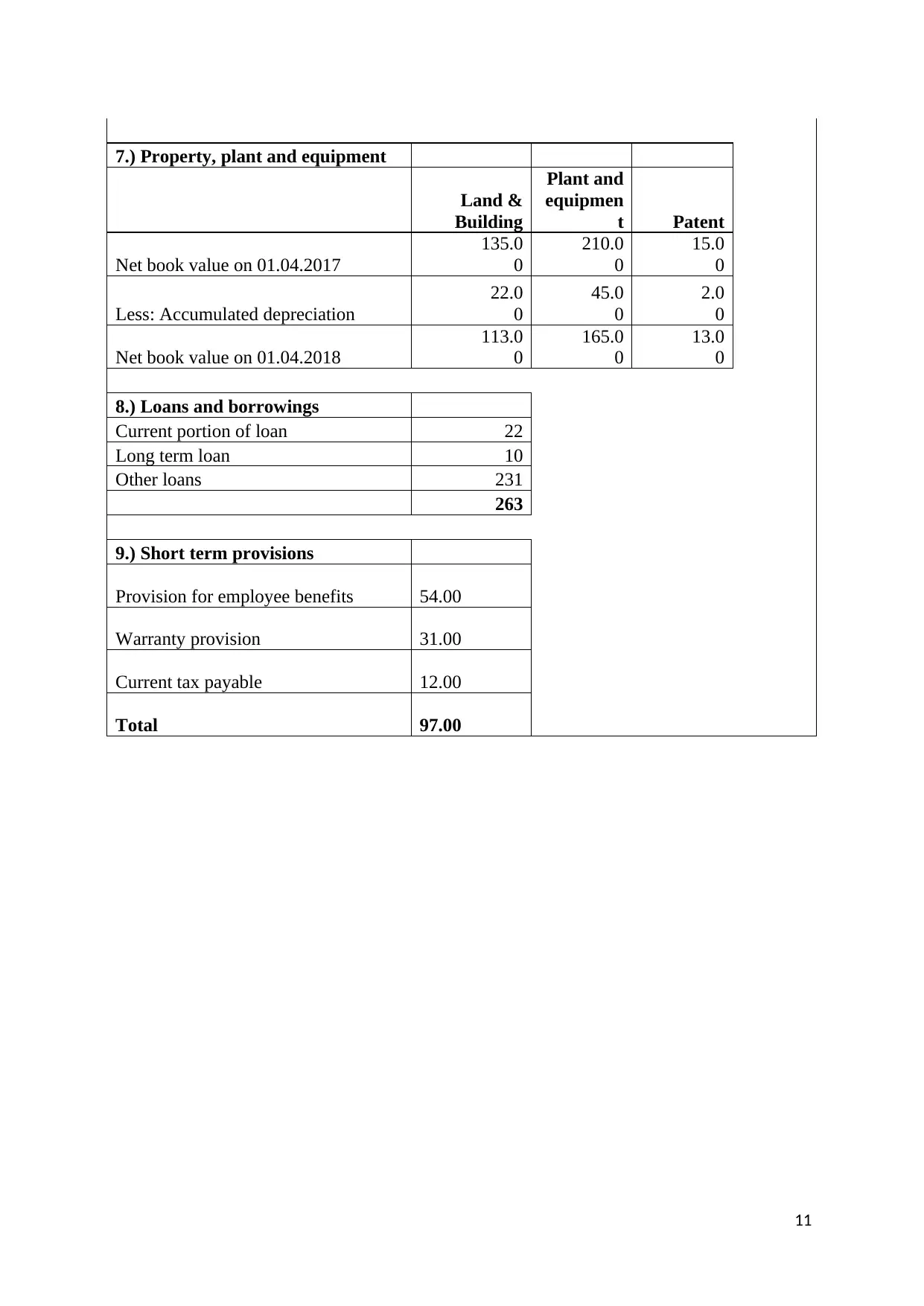

This accounting assignment is divided into three parts. Part A examines AASB 16, focusing on its impact on balance sheets, assets, liabilities, and equity, and its consistency with the IASB's conceptual framework. Part B explores AASB 15 on revenue recognition, including its five-step model, and how positive accounting theory, specifically the debt covenant hypothesis, influences accounting policy choices, illustrated by Microsoft's revenue recognition changes. Part C presents the trial balance, statement of comprehensive income, statement of changes in equity, and balance sheet of NewSpace Ltd, along with notes to the accounts, covering accounting policies, revenue, expenses, receivables, cash, investments, property, plant, equipment, and loans. The assignment integrates financial reporting standards and accounting principles, providing a comprehensive analysis of financial statement preparation and the effects of accounting standards on business decisions.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.