University Financial Accounting Report: AASB 16 Lease Standard Impact

VerifiedAdded on 2022/08/14

|15

|3932

|164

Report

AI Summary

This report delves into the transition from AASB 117 to the new AASB 16 lease accounting standard. It begins by outlining the rationale behind the replacement, emphasizing the limitations of the previous standard in providing a comprehensive view of a company's liabilities, particularly concerning off-balance-sheet operating leases. The report then explores the significance of contracts within leasing agreements under AASB 16, highlighting the importance of determining whether a contract contains a lease. It details the three key evaluations used to make this determination, including the identification of assets, the customer's ability to obtain economic benefits, and the customer's right to direct the use of the asset. Finally, the report examines the impact of substantive substitution rights on lease agreements, clarifying how these rights affect the classification and accounting treatment of leases. The report provides a detailed analysis of the new lease standard including financial reporting implications, contract significance, and the impact of substantive substitution rights.

Running head: FINANCIAL ACCOUNTING

Financial accounting

Name of the Student

Name of the University

Author Note

Financial accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................2

Part 1:.........................................................................................................................................3

Outlining the reasons for replacing AASB 117 leases with AASB 16:.....................................3

Part 2:.........................................................................................................................................5

Evaluating the contract significance in leasing agreement as per AASB 16:............................5

Part 3:.........................................................................................................................................9

Identifying the impact of substantive substitution right on the agreement of lease:..................9

Conclusion:..............................................................................................................................11

References list:.........................................................................................................................12

Table of Contents

Introduction:...............................................................................................................................2

Part 1:.........................................................................................................................................3

Outlining the reasons for replacing AASB 117 leases with AASB 16:.....................................3

Part 2:.........................................................................................................................................5

Evaluating the contract significance in leasing agreement as per AASB 16:............................5

Part 3:.........................................................................................................................................9

Identifying the impact of substantive substitution right on the agreement of lease:..................9

Conclusion:..............................................................................................................................11

References list:.........................................................................................................................12

FINANCIAL ACCOUNTING

Introduction:

The paper conducts an investigation into the introduction of new leasing standard by

replacing the existing old standard. The reason for introducing the new lease standard that is

AASB 16 and why the existing lease standard AASB 117 was replaced has been outlined in

the paper. In addition to this, paper also discusses about the significance of contract in the

agreement of lease in accordance with lease standard AASB 16. The rights of substantive

substitution has been discussed by evaluating the impact on lease agreement. The new lease

standard IFRS 16 that has been effective from 1st January, 2019 is expected to significantly

impact the financial reporting of lessee (Peprníčková 2018). Some of the arguments presented

as the critics of the new lease standard might not be necessarily valid.

Part 1:

Outlining the reasons for replacing AASB 117 leases with AASB 16:

IFRS 16 or AASB 16 has replaced the lease standard IASB 117 and the most

impactful and obvious difference is disclosure of the operating lease on the balance sheet of

the reporting entities. The account for lease by the reporting entity in their financial reporting

disclosures particularly on the income statements and balance sheet has been changed due to

the introduction of new lease standard AASB 16. The major loophole in the accounting for

lease under the existing standard AASB 117 that is operating lease which is off balance sheet

has been addressed by the introduction of the new lease standard. This loophole is closed by

the new standard as it requires all the lease accounted by the organizations to be recognized

as finance lease and disclosed on the balance sheet of the reporting entities. The need for

replacing the existing lease standard with new one was to provide the users with the true

nature of liabilities of company by avoiding any misleading facts about the financial nature. It

is so because under the old lease standard, operating lease were mentioned in the footnotes of

Introduction:

The paper conducts an investigation into the introduction of new leasing standard by

replacing the existing old standard. The reason for introducing the new lease standard that is

AASB 16 and why the existing lease standard AASB 117 was replaced has been outlined in

the paper. In addition to this, paper also discusses about the significance of contract in the

agreement of lease in accordance with lease standard AASB 16. The rights of substantive

substitution has been discussed by evaluating the impact on lease agreement. The new lease

standard IFRS 16 that has been effective from 1st January, 2019 is expected to significantly

impact the financial reporting of lessee (Peprníčková 2018). Some of the arguments presented

as the critics of the new lease standard might not be necessarily valid.

Part 1:

Outlining the reasons for replacing AASB 117 leases with AASB 16:

IFRS 16 or AASB 16 has replaced the lease standard IASB 117 and the most

impactful and obvious difference is disclosure of the operating lease on the balance sheet of

the reporting entities. The account for lease by the reporting entity in their financial reporting

disclosures particularly on the income statements and balance sheet has been changed due to

the introduction of new lease standard AASB 16. The major loophole in the accounting for

lease under the existing standard AASB 117 that is operating lease which is off balance sheet

has been addressed by the introduction of the new lease standard. This loophole is closed by

the new standard as it requires all the lease accounted by the organizations to be recognized

as finance lease and disclosed on the balance sheet of the reporting entities. The need for

replacing the existing lease standard with new one was to provide the users with the true

nature of liabilities of company by avoiding any misleading facts about the financial nature. It

is so because under the old lease standard, operating lease were mentioned in the footnotes of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

the financial statements of the companies and this might contribute in misleading the users

about the financial performance (Assets.kpmg 2020).

Under AASB 117, lessors were provided limited information to make financial

decision and under new standard, there is an enhanced and improved disclosure about the risk

exposure of lessor and specifically to residual value risk. A straight line lease expense is

reported by the companies under AASB 117 and in each period of lease, the amount of lease

expense is same. However, under new lease standard, there is reduction in the amount of

interest over the contract term and this causes the total amount of expenses pertaining to lease

to be front loaded (Forbes.com 2020).

Lease transactions under the old lease standard was accounted either as the operating

or finance lease depending upon the complex test and rules and using bright lines that

resulted in nothing or all being recognized on the balance sheet. Earlier, the big ticket assets

such as manufacturing equipment’s, real estate, technology, ships, trains and aircraft was not

affected and the new lease standard created an impact on such assets. The expense character

under new standard would change along with decreasing capital ratios and increasing gearing

ratios would cause balance sheet to grow. The comparative figures is not required to be

restated under the transition approach and the new lease liability is measured at the

incremental borrowing rate of agency by discounting the remaining lease payments (Yu

2019).

Lessee under the old lease standard are not required to classify their operating lease

into assets and liabilities and disclose it on the financial statement that is balance sheet. Such

practice has resulted in providing the users with incomplete and inaccurate information of the

expenses and results in overestimations due to making estimate of the off balance sheet

obligations. Moreover, comparing the business with those buying assets and using lease

the financial statements of the companies and this might contribute in misleading the users

about the financial performance (Assets.kpmg 2020).

Under AASB 117, lessors were provided limited information to make financial

decision and under new standard, there is an enhanced and improved disclosure about the risk

exposure of lessor and specifically to residual value risk. A straight line lease expense is

reported by the companies under AASB 117 and in each period of lease, the amount of lease

expense is same. However, under new lease standard, there is reduction in the amount of

interest over the contract term and this causes the total amount of expenses pertaining to lease

to be front loaded (Forbes.com 2020).

Lease transactions under the old lease standard was accounted either as the operating

or finance lease depending upon the complex test and rules and using bright lines that

resulted in nothing or all being recognized on the balance sheet. Earlier, the big ticket assets

such as manufacturing equipment’s, real estate, technology, ships, trains and aircraft was not

affected and the new lease standard created an impact on such assets. The expense character

under new standard would change along with decreasing capital ratios and increasing gearing

ratios would cause balance sheet to grow. The comparative figures is not required to be

restated under the transition approach and the new lease liability is measured at the

incremental borrowing rate of agency by discounting the remaining lease payments (Yu

2019).

Lessee under the old lease standard are not required to classify their operating lease

into assets and liabilities and disclose it on the financial statement that is balance sheet. Such

practice has resulted in providing the users with incomplete and inaccurate information of the

expenses and results in overestimations due to making estimate of the off balance sheet

obligations. Moreover, comparing the business with those buying assets and using lease

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

assets under the old standard was difficult. Such accounting practice has changed under the

new standard as the lease liabilities and right of use assets is required to recognize by the

lessee. The consequence of recognizing operating lease on the balance sheet is one of the

biggest changes under lease accounting and this has brought changes to various financial

metrics (Tanase et al. 2018).

Due to the introduction of lease standard, the existing issues with the old standard has

been addressed and this is expected to benefit the users of the financial statements. Disclosure

of the operating lease on the balance sheet in the financial report has enhanced transparency

and improved comparability of the information disclosed by the reporting entities in their

financial report. The effect of operating lease can be clearly identified by the users and such

disclosure offers a useful basis for comparing the performance between the companies. It was

difficult for the users under AASB 117 to compare the performance of the companies buying

assets and the one that leases (Giner and Pardo 2018). However, in order to explain the shift

in figures due to change in various financial metrics, liabilities and ratios, it is required by the

companies to take due care and diligence related to the disclosures.

Operating lease under the old lease standard was accounted for using a less complex

method compared to finance lease and this causes the volume of finance lease to be

predominantly lower than the value of operating lease reported. Under the new standard,

accountants have to face higher degree of complexities as all leases are treated under the

same accounting system and this results in calculations to be complex.

Compared to the old lease standard, new lease standard AASB 16 introduced

significant changes particularly for lessees. A preliminary assessment is required to be

performed by the entities for determining the impact created by the lease standard on entity.

For many entities, the knock effects of lease standard IFRS 16 or AASB 16 would be

assets under the old standard was difficult. Such accounting practice has changed under the

new standard as the lease liabilities and right of use assets is required to recognize by the

lessee. The consequence of recognizing operating lease on the balance sheet is one of the

biggest changes under lease accounting and this has brought changes to various financial

metrics (Tanase et al. 2018).

Due to the introduction of lease standard, the existing issues with the old standard has

been addressed and this is expected to benefit the users of the financial statements. Disclosure

of the operating lease on the balance sheet in the financial report has enhanced transparency

and improved comparability of the information disclosed by the reporting entities in their

financial report. The effect of operating lease can be clearly identified by the users and such

disclosure offers a useful basis for comparing the performance between the companies. It was

difficult for the users under AASB 117 to compare the performance of the companies buying

assets and the one that leases (Giner and Pardo 2018). However, in order to explain the shift

in figures due to change in various financial metrics, liabilities and ratios, it is required by the

companies to take due care and diligence related to the disclosures.

Operating lease under the old lease standard was accounted for using a less complex

method compared to finance lease and this causes the volume of finance lease to be

predominantly lower than the value of operating lease reported. Under the new standard,

accountants have to face higher degree of complexities as all leases are treated under the

same accounting system and this results in calculations to be complex.

Compared to the old lease standard, new lease standard AASB 16 introduced

significant changes particularly for lessees. A preliminary assessment is required to be

performed by the entities for determining the impact created by the lease standard on entity.

For many entities, the knock effects of lease standard IFRS 16 or AASB 16 would be

FINANCIAL ACCOUNTING

significant as there will be expansion in the balance sheet of lessees as the new lease assets

and liabilities are to be disclosed in the balance sheet (Segal and Naik 2019).

Part 2:

Evaluating the contract significance in leasing agreement as per AASB 16:

The evaluation of fact whether the contract contains a lease or is a lease has become

more important under AASB 16 as under this standard, in terms of lease accounting,

substantially all the leases are to be recorded in the balance sheet of lessee. In practice,

contracts that do not have legal form and incorporate some assets that might factor lease such

as contract manufacturing, outsourcing, power supply agreements and transportation would

be mainly impacted. The definition of lease is changed under the new standard and the

application of this definition is done by following the guidance provided in the new standard

(Aasb.gov.au 2020). Consequently, the definition of lease under AASB 16 would be fulfilled

by some contracts not containing lease. Determination of the contract containing lease or not

is done using three key evaluations outlined in the new standard (Cristin 2017). In order to

conclude whether the contract contains a lease or is a contract, it is necessary that all the key

evaluations are met.

significant as there will be expansion in the balance sheet of lessees as the new lease assets

and liabilities are to be disclosed in the balance sheet (Segal and Naik 2019).

Part 2:

Evaluating the contract significance in leasing agreement as per AASB 16:

The evaluation of fact whether the contract contains a lease or is a lease has become

more important under AASB 16 as under this standard, in terms of lease accounting,

substantially all the leases are to be recorded in the balance sheet of lessee. In practice,

contracts that do not have legal form and incorporate some assets that might factor lease such

as contract manufacturing, outsourcing, power supply agreements and transportation would

be mainly impacted. The definition of lease is changed under the new standard and the

application of this definition is done by following the guidance provided in the new standard

(Aasb.gov.au 2020). Consequently, the definition of lease under AASB 16 would be fulfilled

by some contracts not containing lease. Determination of the contract containing lease or not

is done using three key evaluations outlined in the new standard (Cristin 2017). In order to

conclude whether the contract contains a lease or is a contract, it is necessary that all the key

evaluations are met.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

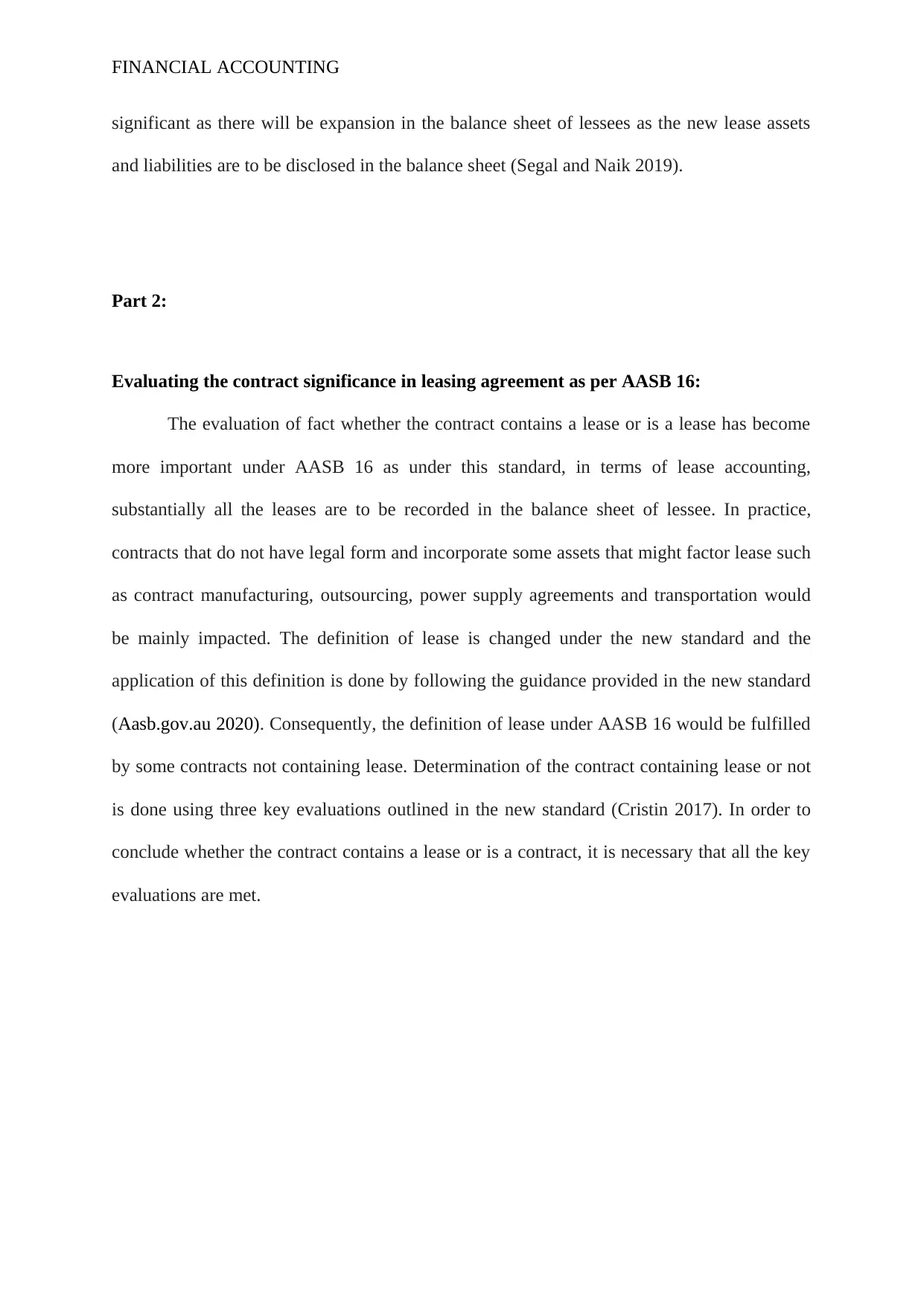

Evaluation criteria of contract:

(Source: Www2.deloitte.com 2020)

The first evaluation is that whether there exist any identified assets which is either

implicitly or explicitly identified. Customers does not have the right to use the explicitly

specified assets as an identified assets and this is exercised when the substantive supplier

rights is enjoyed by the suppliers. The second evaluation requires to determine whether the

economic benefits can be substantially obtained by the customers from using identified assets

and such benefits can be obtained by the customers by holding, leasing and sub holding the

assets. Third evaluation is to identify whether the customers possess the rights to use

identified assets. The decision impacting the benefits directly is considered by the customers

when making third evaluation. Contracts in many cases incorporates conditions and terms

where the interest of suppliers in the assets are protected (Ulrich 2020).

The distinction between service and lease contracts are done by identifying the leases

by the application of control model under IFRS 16 and such distinction is done based on

identified assets which the customer controls. While the classification of majority of contracts

Evaluation criteria of contract:

(Source: Www2.deloitte.com 2020)

The first evaluation is that whether there exist any identified assets which is either

implicitly or explicitly identified. Customers does not have the right to use the explicitly

specified assets as an identified assets and this is exercised when the substantive supplier

rights is enjoyed by the suppliers. The second evaluation requires to determine whether the

economic benefits can be substantially obtained by the customers from using identified assets

and such benefits can be obtained by the customers by holding, leasing and sub holding the

assets. Third evaluation is to identify whether the customers possess the rights to use

identified assets. The decision impacting the benefits directly is considered by the customers

when making third evaluation. Contracts in many cases incorporates conditions and terms

where the interest of suppliers in the assets are protected (Ulrich 2020).

The distinction between service and lease contracts are done by identifying the leases

by the application of control model under IFRS 16 and such distinction is done based on

identified assets which the customer controls. While the classification of majority of contracts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

as a service or lease contracts under the new standard might not be different to the

classification under risk and reward model of the old standard AASB 117. It is required and

important for the entity to consider all the relevant conditions and terms of the contracts

along with the relevant circumstances for the application of AASB 16. It is also entitled by

the entity to conduct an assessment of lease whether it contains the contract or not.

Identification of contracts containing lease or not is done by bringing the new definition of

lease under the new standard that superseded the related interpretations in the old standard

and the standard itself. Each component of lease within the contract shall be accounted by the

entity as a lease that is separate from the non-lease component. The contract consideration

shall be allocated to each lease contracts for the contracts that contains one or more additional

lease and a components that is non lease. Such allocation is done based on aggregate

standalone price on non-lease components and standard alone price of lease components.

The new lease standard IFRS 16 requires the entity to determine whether the lease is

at the inception of contract or the contract is a lease. In event of application of definition of

lease or identifying it whether it contains the contract or not requires the judgment. IFRS 16

includes all the contracts that carries the right to use the assets by exchanging some

considerations and some of the contracts under the new standard might be treated differently.

Analysis in relation to contract is initiated by identifying whether the contract meets the lease

definition.

The arrangements under new standard embeds non lease components in the operating

lease or operating lease in the contract. However, the components of operating lease in the

contracts is not separated by many entities. This is because similar impact is created by the

accounting for operating lease The two elements of contracts in lessee accounting under the

new standard changes because recognition of leases are to be done on the balance sheet. The

treatment of two components of lease that is operating and service would is different under

as a service or lease contracts under the new standard might not be different to the

classification under risk and reward model of the old standard AASB 117. It is required and

important for the entity to consider all the relevant conditions and terms of the contracts

along with the relevant circumstances for the application of AASB 16. It is also entitled by

the entity to conduct an assessment of lease whether it contains the contract or not.

Identification of contracts containing lease or not is done by bringing the new definition of

lease under the new standard that superseded the related interpretations in the old standard

and the standard itself. Each component of lease within the contract shall be accounted by the

entity as a lease that is separate from the non-lease component. The contract consideration

shall be allocated to each lease contracts for the contracts that contains one or more additional

lease and a components that is non lease. Such allocation is done based on aggregate

standalone price on non-lease components and standard alone price of lease components.

The new lease standard IFRS 16 requires the entity to determine whether the lease is

at the inception of contract or the contract is a lease. In event of application of definition of

lease or identifying it whether it contains the contract or not requires the judgment. IFRS 16

includes all the contracts that carries the right to use the assets by exchanging some

considerations and some of the contracts under the new standard might be treated differently.

Analysis in relation to contract is initiated by identifying whether the contract meets the lease

definition.

The arrangements under new standard embeds non lease components in the operating

lease or operating lease in the contract. However, the components of operating lease in the

contracts is not separated by many entities. This is because similar impact is created by the

accounting for operating lease The two elements of contracts in lessee accounting under the

new standard changes because recognition of leases are to be done on the balance sheet. The

treatment of two components of lease that is operating and service would is different under

FINANCIAL ACCOUNTING

the new standard. It might be decided by lessee not to separate the lease components from

non-lease component as a practical usefulness. In the event of application of such exemption

by the lessee, then the non-lease component and the associated lease component is accounted

as the single component of lease. In such treatment, either the entire contract will be treated

as lease or there will be separation of the service components.

Reassessment of the existing contract containing lease upon transition is not required

to be done by lessors and lessees. If it is concluded that contract is not considered as lease

under the previous standard AASB 117, such contracts is not required to be reassessed in

accordance with the new standard AASB 16. It is up to the lessors and lessee to apply the

definition of new lease to all of their contracts under new standard. However, for the

reassessment of the contracts whether they contain a lease can be done by applying

transitional relief. Application of new else definition would be done to the contracts modified

on or entered into after the date of initial application in the event when the application of

relief is chosen by the entity (Stancheva et al. 2019).

Lease payments relating to the contracts of operating lease are not completely

disclosed in the operating cash flow. Realization of the payment of lease would be done in

the cash flow if such payment is related to interest for the lease liability.

Part 3:

Identifying the impact of substantive substitution right on the agreement of lease:

When the cost of substituting the assets is less than the economic benefits and the

suppliers possess the practical ability to substitute the alternative assets throughout the period

of the use of such assets, then this implies the existence of substantive substitution rights. It is

the new standard. It might be decided by lessee not to separate the lease components from

non-lease component as a practical usefulness. In the event of application of such exemption

by the lessee, then the non-lease component and the associated lease component is accounted

as the single component of lease. In such treatment, either the entire contract will be treated

as lease or there will be separation of the service components.

Reassessment of the existing contract containing lease upon transition is not required

to be done by lessors and lessees. If it is concluded that contract is not considered as lease

under the previous standard AASB 117, such contracts is not required to be reassessed in

accordance with the new standard AASB 16. It is up to the lessors and lessee to apply the

definition of new lease to all of their contracts under new standard. However, for the

reassessment of the contracts whether they contain a lease can be done by applying

transitional relief. Application of new else definition would be done to the contracts modified

on or entered into after the date of initial application in the event when the application of

relief is chosen by the entity (Stancheva et al. 2019).

Lease payments relating to the contracts of operating lease are not completely

disclosed in the operating cash flow. Realization of the payment of lease would be done in

the cash flow if such payment is related to interest for the lease liability.

Part 3:

Identifying the impact of substantive substitution right on the agreement of lease:

When the cost of substituting the assets is less than the economic benefits and the

suppliers possess the practical ability to substitute the alternative assets throughout the period

of the use of such assets, then this implies the existence of substantive substitution rights. It is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL ACCOUNTING

likely that the cost for substituting the assets would be higher when the location of assets is at

the premise of customer. This implies that the economically benefits of such substitution to

the suppliers would be less. The substances and the facts presented at the commencement of

the contract forms the basis of assessing whether the substitution rights of supplies is

substantive. It implies that the events that are not likely to occur in the future are ignored by

the customers. Such events includes new technology introduction which is not developed

substantially at the contract commencement. This also include other events such as

substantial difference between market price of assets at the commencement of contract and

actual market price of asset and future customer agreement to pay more than market rate for

using the assets (Pwc.com 2020). The lessor enjoying substantive rights that permits him to

substitute the assets throughout the period of use, however, it does not permit the lessee to

control the identified assets use even if the asset is specified.

With respect to the leased assets, it is required to evaluate whether the substantive

substitution rights is enjoyed by the lessor. The contracts containing substitution rights but is

not substantive can be explained using one example. Supplier under a contract is entitled to

use a copy machine and it can be replaced under certain circumstances such as machine is not

functioning properly (Grosu and Hlaciuc 2018). For evaluating the existence of substantive

substitution right, the ability of suppliers for deriving the economic benefits and exercising

substitution rights is determined by the customers. Assets can be substituted as per the right

of supplier because the machine is not functioning properly and exercising such right does

not implies that there exist substantive substitution right. It is important for the machine to be

located on the premise of customers, if the supplier has the rights to substitute the assets. In

the absence of permission of the customers to access the machine, substitution rights cannot

be exercised by the suppliers and this imposes a limit on the ability of supplier to exercise the

rights of substitution (Cpaaustralia.com.au 2020). Therefore, it is costly for the suppliers to

likely that the cost for substituting the assets would be higher when the location of assets is at

the premise of customer. This implies that the economically benefits of such substitution to

the suppliers would be less. The substances and the facts presented at the commencement of

the contract forms the basis of assessing whether the substitution rights of supplies is

substantive. It implies that the events that are not likely to occur in the future are ignored by

the customers. Such events includes new technology introduction which is not developed

substantially at the contract commencement. This also include other events such as

substantial difference between market price of assets at the commencement of contract and

actual market price of asset and future customer agreement to pay more than market rate for

using the assets (Pwc.com 2020). The lessor enjoying substantive rights that permits him to

substitute the assets throughout the period of use, however, it does not permit the lessee to

control the identified assets use even if the asset is specified.

With respect to the leased assets, it is required to evaluate whether the substantive

substitution rights is enjoyed by the lessor. The contracts containing substitution rights but is

not substantive can be explained using one example. Supplier under a contract is entitled to

use a copy machine and it can be replaced under certain circumstances such as machine is not

functioning properly (Grosu and Hlaciuc 2018). For evaluating the existence of substantive

substitution right, the ability of suppliers for deriving the economic benefits and exercising

substitution rights is determined by the customers. Assets can be substituted as per the right

of supplier because the machine is not functioning properly and exercising such right does

not implies that there exist substantive substitution right. It is important for the machine to be

located on the premise of customers, if the supplier has the rights to substitute the assets. In

the absence of permission of the customers to access the machine, substitution rights cannot

be exercised by the suppliers and this imposes a limit on the ability of supplier to exercise the

rights of substitution (Cpaaustralia.com.au 2020). Therefore, it is costly for the suppliers to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL ACCOUNTING

perform substitution because of the location of assets as against the location of assets in the

premises of supplier. Hence, it is determined by the customers that exercising the substitution

right would benefit the supplier given the cost of substituting the new equipment. It is

determined by the customer from the basis of this assessment that substitution rights of

suppliers is not substantive. In the absence of such determination of benefit derived by the

supplies from the substitution, it is assumed that such right is not substantive. It can be

inferred from the above discussion that evaluation of whether the substitution right is

substantive or not if complex as it is required to consider the wide range of factors such as

costs and benefit of substituting.

Lease accounting might be avoided by the customer due to the substitution rights that

is substantive. Nevertheless, the desirable outcome should be weighted by the suppliers

against any inconvenience and practical aspects that might necessitate the allowance of such

substantive rights. For evaluating the contracts for the existence of the substantive

substitution rights is to be done at the commencement of the contract. The obligations and

rights of lessor that do not constitute substantive substitution right would not prevent the

lessee from the right to use an identified assets (Giner and Pardo 2018).

The new lease standard incorporates some requirements in the form of creating a

detailed analysis of the lease arrangements and contracts. On the basis of new definition of

lease, some arrangements that might not have fallen under the category of lease under the

previous standard might be categorized as lease under new standard. When analyzing the

lease arrangements and contracts, it is required by the adopters and practitioners to be diligent

for ensuring all the leases are accounted and disclosed in the balance sheet. Therefore, the

key to identify the contract as lease or not is to perform a careful analysis by using three

evaluations as outlined by AASB 16 (Morales et al. 2018).

perform substitution because of the location of assets as against the location of assets in the

premises of supplier. Hence, it is determined by the customers that exercising the substitution

right would benefit the supplier given the cost of substituting the new equipment. It is

determined by the customer from the basis of this assessment that substitution rights of

suppliers is not substantive. In the absence of such determination of benefit derived by the

supplies from the substitution, it is assumed that such right is not substantive. It can be

inferred from the above discussion that evaluation of whether the substitution right is

substantive or not if complex as it is required to consider the wide range of factors such as

costs and benefit of substituting.

Lease accounting might be avoided by the customer due to the substitution rights that

is substantive. Nevertheless, the desirable outcome should be weighted by the suppliers

against any inconvenience and practical aspects that might necessitate the allowance of such

substantive rights. For evaluating the contracts for the existence of the substantive

substitution rights is to be done at the commencement of the contract. The obligations and

rights of lessor that do not constitute substantive substitution right would not prevent the

lessee from the right to use an identified assets (Giner and Pardo 2018).

The new lease standard incorporates some requirements in the form of creating a

detailed analysis of the lease arrangements and contracts. On the basis of new definition of

lease, some arrangements that might not have fallen under the category of lease under the

previous standard might be categorized as lease under new standard. When analyzing the

lease arrangements and contracts, it is required by the adopters and practitioners to be diligent

for ensuring all the leases are accounted and disclosed in the balance sheet. Therefore, the

key to identify the contract as lease or not is to perform a careful analysis by using three

evaluations as outlined by AASB 16 (Morales et al. 2018).

FINANCIAL ACCOUNTING

Contract is considered not to contain a lease even if there is no identified assets in the

event if the substantive rights of the suppliers is substantive. In order for the rights to be

considered substantive, the requirement of substitution right providing suppliers with

economic benefits requires to exercise significant judgment. The guidance provided by the

new lease standard make more and more contracts deemed to be included in lease as the

identified assets is incorporated in it. This determination is more crucial under the new

standard as this cause implications on the balance sheet of lessee (Joubert et al. 2017).

Therefore, from the overall analysis of the examination of the substantive substitution rights,

it can be said that the lease accounting is considerably impacted under the concept of the

substitution rights introduced under the new standard.

Conclusion:

The detailed discussion on the new lease standard AASB 16 has been done for

examining the flaws in the previous standard and how the new standard has addressed the

existing loopholes in accounting for lease. Moreover, the treatment of the components of

contract under new standard is different and the component can either be treated at lease or is

separated entirely. Leas contracts under the new standard is expected to change the cash flow

statements of entity as contracts classified as operating are not disclosed completely in the

cash flow statement. Determining whether the contract contains a lease requires the entity to

identify the conditions such as existence of identified assets and identifying the right to

control for using the identified assets. The later section identifies that the lease agreement is

also impacted to a significant extent due to the existence of substantive substitution rights.

Contract is considered not to contain a lease even if there is no identified assets in the

event if the substantive rights of the suppliers is substantive. In order for the rights to be

considered substantive, the requirement of substitution right providing suppliers with

economic benefits requires to exercise significant judgment. The guidance provided by the

new lease standard make more and more contracts deemed to be included in lease as the

identified assets is incorporated in it. This determination is more crucial under the new

standard as this cause implications on the balance sheet of lessee (Joubert et al. 2017).

Therefore, from the overall analysis of the examination of the substantive substitution rights,

it can be said that the lease accounting is considerably impacted under the concept of the

substitution rights introduced under the new standard.

Conclusion:

The detailed discussion on the new lease standard AASB 16 has been done for

examining the flaws in the previous standard and how the new standard has addressed the

existing loopholes in accounting for lease. Moreover, the treatment of the components of

contract under new standard is different and the component can either be treated at lease or is

separated entirely. Leas contracts under the new standard is expected to change the cash flow

statements of entity as contracts classified as operating are not disclosed completely in the

cash flow statement. Determining whether the contract contains a lease requires the entity to

identify the conditions such as existence of identified assets and identifying the right to

control for using the identified assets. The later section identifies that the lease agreement is

also impacted to a significant extent due to the existence of substantive substitution rights.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.