Woolworths Limited: Analyzing the Impact of AASB 16 on Leases

VerifiedAdded on 2023/06/12

|14

|3298

|199

Report

AI Summary

This report evaluates lease agreements and their impact on financial reports, focusing on Woolworths Limited and the effects of AASB 16. It contrasts operating and financial leases, examines Woolworths' leasing practices, and analyzes the short and long-term impacts of AASB 16 on the company's financial statements and gearing ratios. The report highlights that AASB 16's implementation will likely increase Woolworths' profit before tax due to the treatment of off-balance sheet leases. Furthermore, it discusses the broader implications of AASB 16 on the Australian retail industry, noting potential increases in debt and EBITDA, with a particularly significant impact on the retail sector. The report also explores the rationale behind the IASB's viewpoint on lease accounting and addresses concerns regarding increased debt and the lack of a level playing field among companies.

Running head: ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

Accounting for Leases- The Impact of AASB (IFRS) 16

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting for Leases- The Impact of AASB (IFRS) 16

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

Executive Summary:

The current report intends to evaluate the concept of lease agreements and their impact on

financial reports by providing a description of operating and financial leases. For simplifying this

report further, Woolworths Limited is selected as the organisation operating in the Australian

supermarket along with depicting its leasing procedure. Once AASB 16 comes into effect on 1st

January 2019, it would have considerable effect on the financial statements and gearing ratios of

Woolworths Limited both in short-run and long-run. Due to the presence of off-balance sheet

lease, the application of AASB 16 would increase the profit before tax of Woolworths. Finally, it

has been evaluated that AASB 16 would result in global increase in debt and EBITDA in all the

industries; however, the impact would be severe on the retail sector.

Executive Summary:

The current report intends to evaluate the concept of lease agreements and their impact on

financial reports by providing a description of operating and financial leases. For simplifying this

report further, Woolworths Limited is selected as the organisation operating in the Australian

supermarket along with depicting its leasing procedure. Once AASB 16 comes into effect on 1st

January 2019, it would have considerable effect on the financial statements and gearing ratios of

Woolworths Limited both in short-run and long-run. Due to the presence of off-balance sheet

lease, the application of AASB 16 would increase the profit before tax of Woolworths. Finally, it

has been evaluated that AASB 16 would result in global increase in debt and EBITDA in all the

industries; however, the impact would be severe on the retail sector.

2ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

Table of Contents

Introduction:....................................................................................................................................3

Lease agreements and impact on financial reports:.........................................................................3

Overview of Woolworths Limited and its lease values:..................................................................4

Impact of the accounting rules for leases on Woolworths Limited:................................................6

Short and long term impacts of the changes to reporting for leases:...............................................7

Impact of leasing agreements on the Australian retail industry:.....................................................8

Reasons behind the viewpoint of the chairperson of IASB:............................................................9

Greater amount of debt in contrast to the amount reported in the balance sheet statement:...........9

Absence of level playing field between some airline companies:.................................................10

Reasons behind the unpopularity of the new accounting standards for leases:.............................10

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

Table of Contents

Introduction:....................................................................................................................................3

Lease agreements and impact on financial reports:.........................................................................3

Overview of Woolworths Limited and its lease values:..................................................................4

Impact of the accounting rules for leases on Woolworths Limited:................................................6

Short and long term impacts of the changes to reporting for leases:...............................................7

Impact of leasing agreements on the Australian retail industry:.....................................................8

Reasons behind the viewpoint of the chairperson of IASB:............................................................9

Greater amount of debt in contrast to the amount reported in the balance sheet statement:...........9

Absence of level playing field between some airline companies:.................................................10

Reasons behind the unpopularity of the new accounting standards for leases:.............................10

Conclusion:....................................................................................................................................11

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

Introduction:

The current report intends to evaluate the concept of lease agreements and their impact on

financial reports by providing a description of operating and financial leases. For simplifying this

report further, Woolworths Limited is selected as the organisation operating in the Australian

supermarket along with depicting its leasing procedure. In addition, the paper covers short-term

as well as long-term effects of the changes to reporting for leases. Finally, the report would shed

light on the former and new accounting standards for leases based on the provided case study.

Lease agreements and impact on financial reports:

Lease agreements:

In the words of Bamber & McMeeking (2016), lease agreements are contractual

agreements, which need a user to pay for using an asset to the owner of that asset. The most

common types of assets that are used in leasing agreements in the Australian business

organisations comprise of buildings, property, vehicles, business and industrial equipment.

Operating versus financial leases:

Lease agreements are of two types, which include operating lease and financial lease.

Operating lease is the lease where the risks and rewards associated with the ownership of the

asset stay with the lessor for the leased asset. Financial lease could be defined as the lease, in

which the rewards and risks related to asset ownership are passed over to the lessee. The

treatment of operating lease is like rent, which implies that lease payments are considered as

operating expenses and they are not included in the statement of financial position (Benson et al.,

2015). On the other hand, the treatment of financial lease is like loan, in which the lessee

Introduction:

The current report intends to evaluate the concept of lease agreements and their impact on

financial reports by providing a description of operating and financial leases. For simplifying this

report further, Woolworths Limited is selected as the organisation operating in the Australian

supermarket along with depicting its leasing procedure. In addition, the paper covers short-term

as well as long-term effects of the changes to reporting for leases. Finally, the report would shed

light on the former and new accounting standards for leases based on the provided case study.

Lease agreements and impact on financial reports:

Lease agreements:

In the words of Bamber & McMeeking (2016), lease agreements are contractual

agreements, which need a user to pay for using an asset to the owner of that asset. The most

common types of assets that are used in leasing agreements in the Australian business

organisations comprise of buildings, property, vehicles, business and industrial equipment.

Operating versus financial leases:

Lease agreements are of two types, which include operating lease and financial lease.

Operating lease is the lease where the risks and rewards associated with the ownership of the

asset stay with the lessor for the leased asset. Financial lease could be defined as the lease, in

which the rewards and risks related to asset ownership are passed over to the lessee. The

treatment of operating lease is like rent, which implies that lease payments are considered as

operating expenses and they are not included in the statement of financial position (Benson et al.,

2015). On the other hand, the treatment of financial lease is like loan, in which the lessee

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

considers the asset ownership and thus, the asset is disclosed in the balance sheet statement of

the concerned organisation.

Impact on financial reports:

Due to financial lease, the asset and liability values tend to increase in comparison to

operating lease. In the initial years of the life of an asset, there is lower net income in financial

lease, as depreciation expense is higher. However, with the passage of time, there would be

decline in depreciation expense and as a result; the net income is greater under financial lease

compared to operating lease (Dagwell, Wines & Lambert, 2015). In addition, under financial

lease, the operating income would be greater, since interest expense is not taken into account to

arrive at the operating income. However, in case of operating lease, operating income would be

minimised, since rent expense is included for computing operating income.

In financial lease, there would be increase in operating cash flow, since only interest

expense is considered in the form of operating outflow. However, in operating lease, both

principal amount and interest amount are included as operating outflows. There would be

reduction in financing cash flows under financial lease, since repayment of principal is

considered in the form of financing outflow. In opposition, there is no such record under

operating lease.

Overview of Woolworths Limited and its lease values:

Woolworths Limited is a leading retailer in the Australian supermarket operating mainly

in Australia and New Zealand and in terms of revenue, it is the second largest organisation

placed after its fierce competitor, Wesfarmers Limited. The major operations of the organisation

comprise of supermarkets, liquor retailing, pubs, hotels and discount department stores.

considers the asset ownership and thus, the asset is disclosed in the balance sheet statement of

the concerned organisation.

Impact on financial reports:

Due to financial lease, the asset and liability values tend to increase in comparison to

operating lease. In the initial years of the life of an asset, there is lower net income in financial

lease, as depreciation expense is higher. However, with the passage of time, there would be

decline in depreciation expense and as a result; the net income is greater under financial lease

compared to operating lease (Dagwell, Wines & Lambert, 2015). In addition, under financial

lease, the operating income would be greater, since interest expense is not taken into account to

arrive at the operating income. However, in case of operating lease, operating income would be

minimised, since rent expense is included for computing operating income.

In financial lease, there would be increase in operating cash flow, since only interest

expense is considered in the form of operating outflow. However, in operating lease, both

principal amount and interest amount are included as operating outflows. There would be

reduction in financing cash flows under financial lease, since repayment of principal is

considered in the form of financing outflow. In opposition, there is no such record under

operating lease.

Overview of Woolworths Limited and its lease values:

Woolworths Limited is a leading retailer in the Australian supermarket operating mainly

in Australia and New Zealand and in terms of revenue, it is the second largest organisation

placed after its fierce competitor, Wesfarmers Limited. The major operations of the organisation

comprise of supermarkets, liquor retailing, pubs, hotels and discount department stores.

5ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

However, it has incurred a significant loss amounting to $1.235 billion in 2016, which is the

largest among the previous 20 years. Such loss is due to the write-downs of $2 billion of the

failed Masters Business and losses incurred in the Big W business (Woolworthsgroup.com.au,

2018).

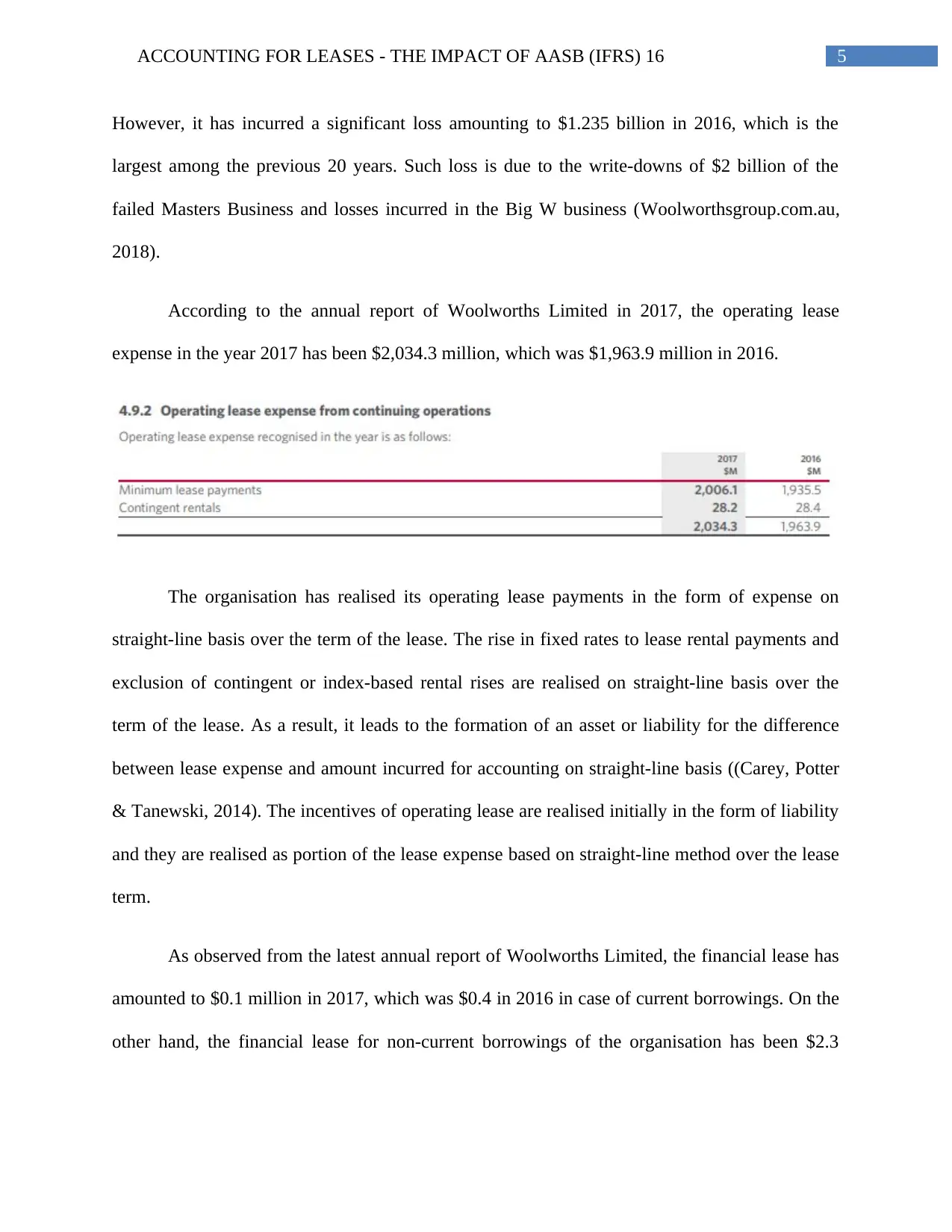

According to the annual report of Woolworths Limited in 2017, the operating lease

expense in the year 2017 has been $2,034.3 million, which was $1,963.9 million in 2016.

The organisation has realised its operating lease payments in the form of expense on

straight-line basis over the term of the lease. The rise in fixed rates to lease rental payments and

exclusion of contingent or index-based rental rises are realised on straight-line basis over the

term of the lease. As a result, it leads to the formation of an asset or liability for the difference

between lease expense and amount incurred for accounting on straight-line basis ((Carey, Potter

& Tanewski, 2014). The incentives of operating lease are realised initially in the form of liability

and they are realised as portion of the lease expense based on straight-line method over the lease

term.

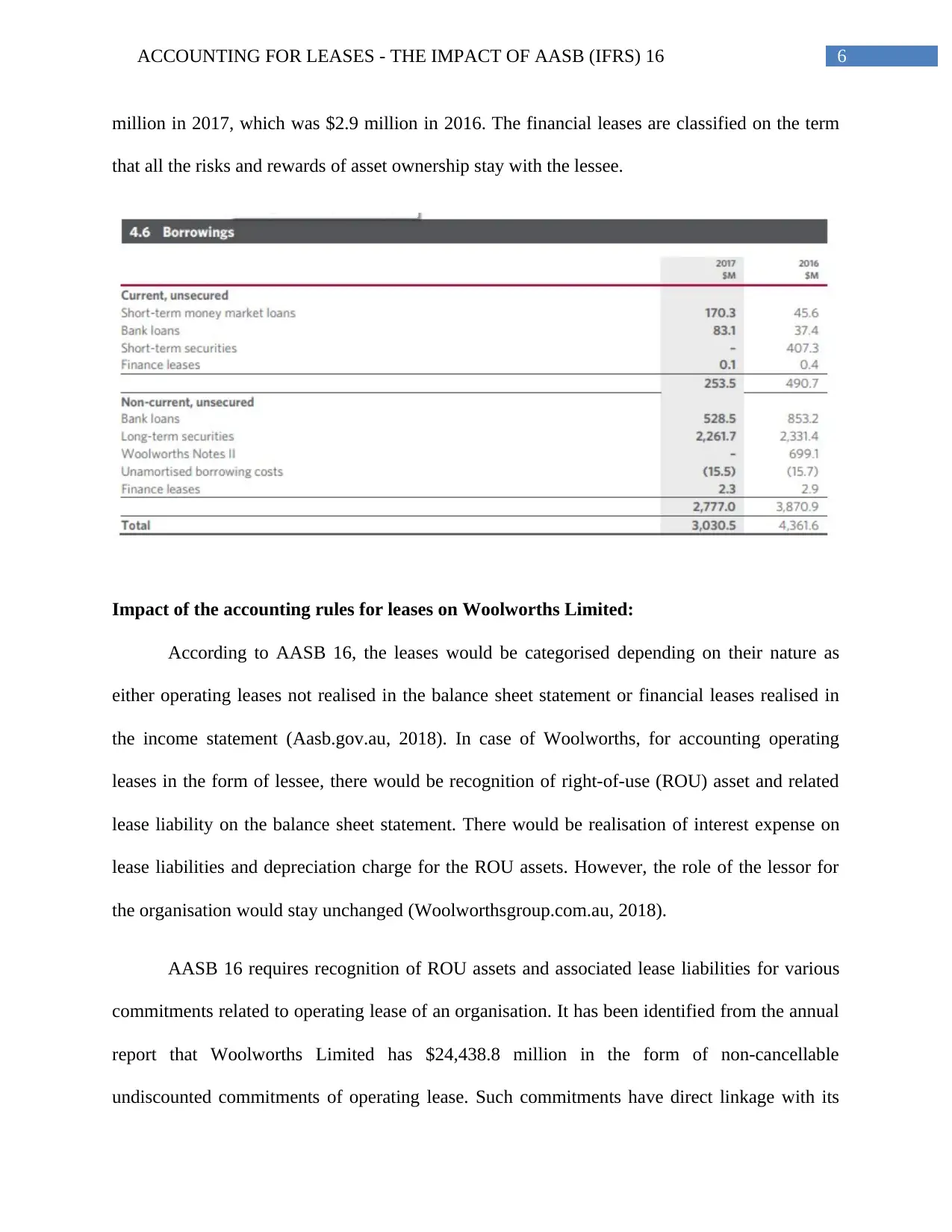

As observed from the latest annual report of Woolworths Limited, the financial lease has

amounted to $0.1 million in 2017, which was $0.4 in 2016 in case of current borrowings. On the

other hand, the financial lease for non-current borrowings of the organisation has been $2.3

However, it has incurred a significant loss amounting to $1.235 billion in 2016, which is the

largest among the previous 20 years. Such loss is due to the write-downs of $2 billion of the

failed Masters Business and losses incurred in the Big W business (Woolworthsgroup.com.au,

2018).

According to the annual report of Woolworths Limited in 2017, the operating lease

expense in the year 2017 has been $2,034.3 million, which was $1,963.9 million in 2016.

The organisation has realised its operating lease payments in the form of expense on

straight-line basis over the term of the lease. The rise in fixed rates to lease rental payments and

exclusion of contingent or index-based rental rises are realised on straight-line basis over the

term of the lease. As a result, it leads to the formation of an asset or liability for the difference

between lease expense and amount incurred for accounting on straight-line basis ((Carey, Potter

& Tanewski, 2014). The incentives of operating lease are realised initially in the form of liability

and they are realised as portion of the lease expense based on straight-line method over the lease

term.

As observed from the latest annual report of Woolworths Limited, the financial lease has

amounted to $0.1 million in 2017, which was $0.4 in 2016 in case of current borrowings. On the

other hand, the financial lease for non-current borrowings of the organisation has been $2.3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

million in 2017, which was $2.9 million in 2016. The financial leases are classified on the term

that all the risks and rewards of asset ownership stay with the lessee.

Impact of the accounting rules for leases on Woolworths Limited:

According to AASB 16, the leases would be categorised depending on their nature as

either operating leases not realised in the balance sheet statement or financial leases realised in

the income statement (Aasb.gov.au, 2018). In case of Woolworths, for accounting operating

leases in the form of lessee, there would be recognition of right-of-use (ROU) asset and related

lease liability on the balance sheet statement. There would be realisation of interest expense on

lease liabilities and depreciation charge for the ROU assets. However, the role of the lessor for

the organisation would stay unchanged (Woolworthsgroup.com.au, 2018).

AASB 16 requires recognition of ROU assets and associated lease liabilities for various

commitments related to operating lease of an organisation. It has been identified from the annual

report that Woolworths Limited has $24,438.8 million in the form of non-cancellable

undiscounted commitments of operating lease. Such commitments have direct linkage with its

million in 2017, which was $2.9 million in 2016. The financial leases are classified on the term

that all the risks and rewards of asset ownership stay with the lessee.

Impact of the accounting rules for leases on Woolworths Limited:

According to AASB 16, the leases would be categorised depending on their nature as

either operating leases not realised in the balance sheet statement or financial leases realised in

the income statement (Aasb.gov.au, 2018). In case of Woolworths, for accounting operating

leases in the form of lessee, there would be recognition of right-of-use (ROU) asset and related

lease liability on the balance sheet statement. There would be realisation of interest expense on

lease liabilities and depreciation charge for the ROU assets. However, the role of the lessor for

the organisation would stay unchanged (Woolworthsgroup.com.au, 2018).

AASB 16 requires recognition of ROU assets and associated lease liabilities for various

commitments related to operating lease of an organisation. It has been identified from the annual

report that Woolworths Limited has $24,438.8 million in the form of non-cancellable

undiscounted commitments of operating lease. Such commitments have direct linkage with its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

retail premises, centres of distribution, support offices and warehouse facilities that are to be

realised in the form of ROU assets and related lease liabilities (Dakis, 2016).

Short and long term impacts of the changes to reporting for leases:

Once AASB 16 comes into effect on 1st January 2019, it would have considerable effect

on the financial statements and gearing ratios of Woolworths Limited both in short-run and long-

run. Due to the presence of off-balance sheet lease, the application of AASB 16 would increase

the profit before tax of Woolworths. This is because the presentation of implicit interest would

be made in the lease payments for leases related to former off-balance sheet in the form of

finance costs (AASB, 2014). In opposition, as per the old standard, the off-balance sheet

expenses would be incorporated in the form of operating expenses.

On the other hand, it is necessary to capitalise operating leases for complying with the

requirements of AASB 16. As a result, when Woolworths capitalises its operating leases, there

would be increase in asset as well as liability. However, it is to be borne in mind that there is

linearity in asset amortisation, while no such linearity is inherent in liabilities. As a result, the

liabilities increase rapidly in contrast to assets implying greater leverage (Henderson et al.,

2015). Hence, under AASB 16, there would be increases in debt ratio and debt-to-equity ratio,

while equity ratio would decline. However, the new standard would not have any effect on the

cash flow statement of Woolworths Limited, as inflow and drainage of cash would remain

identical between both lease parties.

retail premises, centres of distribution, support offices and warehouse facilities that are to be

realised in the form of ROU assets and related lease liabilities (Dakis, 2016).

Short and long term impacts of the changes to reporting for leases:

Once AASB 16 comes into effect on 1st January 2019, it would have considerable effect

on the financial statements and gearing ratios of Woolworths Limited both in short-run and long-

run. Due to the presence of off-balance sheet lease, the application of AASB 16 would increase

the profit before tax of Woolworths. This is because the presentation of implicit interest would

be made in the lease payments for leases related to former off-balance sheet in the form of

finance costs (AASB, 2014). In opposition, as per the old standard, the off-balance sheet

expenses would be incorporated in the form of operating expenses.

On the other hand, it is necessary to capitalise operating leases for complying with the

requirements of AASB 16. As a result, when Woolworths capitalises its operating leases, there

would be increase in asset as well as liability. However, it is to be borne in mind that there is

linearity in asset amortisation, while no such linearity is inherent in liabilities. As a result, the

liabilities increase rapidly in contrast to assets implying greater leverage (Henderson et al.,

2015). Hence, under AASB 16, there would be increases in debt ratio and debt-to-equity ratio,

while equity ratio would decline. However, the new standard would not have any effect on the

cash flow statement of Woolworths Limited, as inflow and drainage of cash would remain

identical between both lease parties.

8ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

Impact of leasing agreements on the Australian retail industry:

As Woolworths operates in the Australian supermarket, it falls under the retail industry. It

has been identified that the retailers use real estate leases for their stores (Hoggett et al., 2014).

The impact would be severe on the Australian retail industry after the implementation of AASB

16, which is summarised briefly as follows:

Renewal options:

One of the core businesses of a retailer is leasing real estate. As a result, considerable

judgement is needed for ascertaining and re-evaluating at the time the retailer has an economic

incentive of renewing retail lease location (Holland, 2016).

Relationship between rate/index and variable payments:

It is necessary for the retailers to implement systems for projecting and re-gauging

variable payments associated with an index at the spot rate for each reporting year like consumer

price index.

Segregation of leasing and non-leasing elements:

It would become mandatory for the retailers to segregate service charges. The service

charges could be in the form of marketing, administration and utilities (Jamburia &

Lankeviciute, 2015). The segregation needs to be made from lease components with the

landlords like large retail outlets and leases pertaining to shop-in-shop.

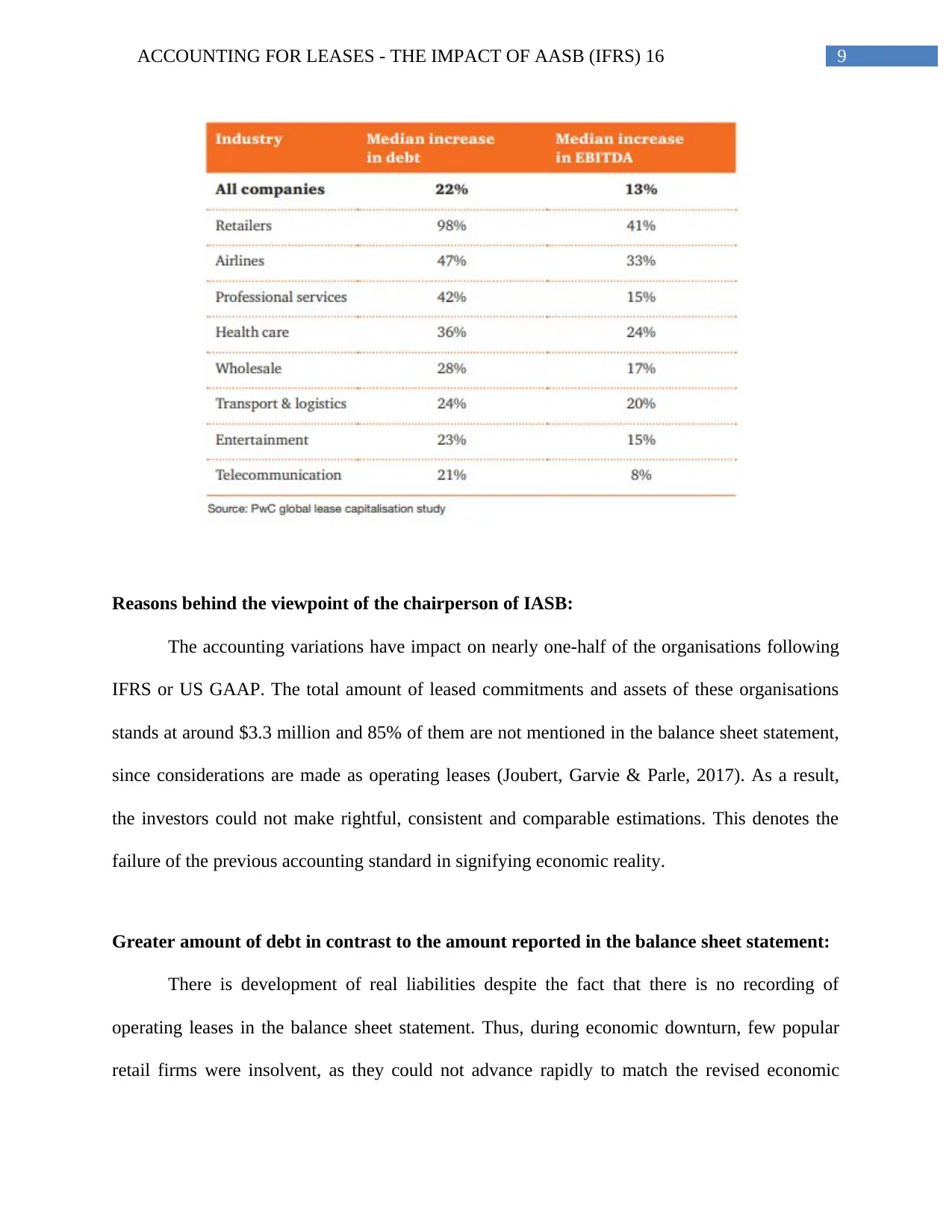

It has been observed that AASB 16 would result in global increase in debt and EBITDA

in all the industries; however, the impact would be severe on the retail sector.

Impact of leasing agreements on the Australian retail industry:

As Woolworths operates in the Australian supermarket, it falls under the retail industry. It

has been identified that the retailers use real estate leases for their stores (Hoggett et al., 2014).

The impact would be severe on the Australian retail industry after the implementation of AASB

16, which is summarised briefly as follows:

Renewal options:

One of the core businesses of a retailer is leasing real estate. As a result, considerable

judgement is needed for ascertaining and re-evaluating at the time the retailer has an economic

incentive of renewing retail lease location (Holland, 2016).

Relationship between rate/index and variable payments:

It is necessary for the retailers to implement systems for projecting and re-gauging

variable payments associated with an index at the spot rate for each reporting year like consumer

price index.

Segregation of leasing and non-leasing elements:

It would become mandatory for the retailers to segregate service charges. The service

charges could be in the form of marketing, administration and utilities (Jamburia &

Lankeviciute, 2015). The segregation needs to be made from lease components with the

landlords like large retail outlets and leases pertaining to shop-in-shop.

It has been observed that AASB 16 would result in global increase in debt and EBITDA

in all the industries; however, the impact would be severe on the retail sector.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

Reasons behind the viewpoint of the chairperson of IASB:

The accounting variations have impact on nearly one-half of the organisations following

IFRS or US GAAP. The total amount of leased commitments and assets of these organisations

stands at around $3.3 million and 85% of them are not mentioned in the balance sheet statement,

since considerations are made as operating leases (Joubert, Garvie & Parle, 2017). As a result,

the investors could not make rightful, consistent and comparable estimations. This denotes the

failure of the previous accounting standard in signifying economic reality.

Greater amount of debt in contrast to the amount reported in the balance sheet statement:

There is development of real liabilities despite the fact that there is no recording of

operating leases in the balance sheet statement. Thus, during economic downturn, few popular

retail firms were insolvent, as they could not advance rapidly to match the revised economic

Reasons behind the viewpoint of the chairperson of IASB:

The accounting variations have impact on nearly one-half of the organisations following

IFRS or US GAAP. The total amount of leased commitments and assets of these organisations

stands at around $3.3 million and 85% of them are not mentioned in the balance sheet statement,

since considerations are made as operating leases (Joubert, Garvie & Parle, 2017). As a result,

the investors could not make rightful, consistent and comparable estimations. This denotes the

failure of the previous accounting standard in signifying economic reality.

Greater amount of debt in contrast to the amount reported in the balance sheet statement:

There is development of real liabilities despite the fact that there is no recording of

operating leases in the balance sheet statement. Thus, during economic downturn, few popular

retail firms were insolvent, as they could not advance rapidly to match the revised economic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

reality. Moreover, considerations commitments could be observed for long-term operating

leases; however, there was deceptive leaning in the balance sheet statement. Hence, the lease

liabilities had been 66 times more than the debt amounts reported in balance sheet statements.

Absence of level playing field between some airline companies:

Comparability was incredibly low in the previous accounting system for leasing. In the

airline sector, operating leases are mostly inherent and disclosures are not made in the balance

sheet statement. Thus, an airline leasing aircraft fleet does not match with the competitors buying

all fleets; however, similarity could be observed in their financial obligations (Wong, Wong &

Jeter, 2016). This denotes that level playing field is not present in the aviation industry. The new

standard would account leases as assets, while they would be recorded as liabilities on the part of

the lessees and this would helping in solving the issue.

Reasons behind the unpopularity of the new accounting standards for leases:

Since AASB is a new leasing standard, the effect would be on more than half of the listed

firms, since changes might result in debates and warnings in terms of adverse economic

conditions and costs related to system changes (Wong & Joshi, 2015). The commercial effects

would be inherent as well, if such changes are implemented.

For instance, the various covenants of banking and contractual agreements related to the

financial statements like profit targets for providing bonus payments are required to make

revisions before the enforcement of the standard. In addition, all business departments in an

organisation are needed to understand the impact of changes such as finance, human resource,

reality. Moreover, considerations commitments could be observed for long-term operating

leases; however, there was deceptive leaning in the balance sheet statement. Hence, the lease

liabilities had been 66 times more than the debt amounts reported in balance sheet statements.

Absence of level playing field between some airline companies:

Comparability was incredibly low in the previous accounting system for leasing. In the

airline sector, operating leases are mostly inherent and disclosures are not made in the balance

sheet statement. Thus, an airline leasing aircraft fleet does not match with the competitors buying

all fleets; however, similarity could be observed in their financial obligations (Wong, Wong &

Jeter, 2016). This denotes that level playing field is not present in the aviation industry. The new

standard would account leases as assets, while they would be recorded as liabilities on the part of

the lessees and this would helping in solving the issue.

Reasons behind the unpopularity of the new accounting standards for leases:

Since AASB is a new leasing standard, the effect would be on more than half of the listed

firms, since changes might result in debates and warnings in terms of adverse economic

conditions and costs related to system changes (Wong & Joshi, 2015). The commercial effects

would be inherent as well, if such changes are implemented.

For instance, the various covenants of banking and contractual agreements related to the

financial statements like profit targets for providing bonus payments are required to make

revisions before the enforcement of the standard. In addition, all business departments in an

organisation are needed to understand the impact of changes such as finance, human resource,

11ACCOUNTING FOR LEASES - THE IMPACT OF AASB (IFRS) 16

asset procurement and others (Xu, Davidson & Cheong, 2017). Due to these reasons, it would

become difficult to gain popularity for AASB 16.

Conclusion:

Based on the above discussion, it could be found that Woolworths Limited has realised

its operating lease payments in the form of expense on straight-line basis over the term of the

lease. The rise in fixed rates to lease rental payments and exclusion of contingent or index-based

rental rises are realised on straight-line basis over the term of the lease. Once AASB 16 comes

into effect on 1st January 2019, it would have considerable effect on the financial statements and

gearing ratios of Woolworths Limited both in short-run and long-run. Due to the presence of off-

balance sheet lease, the application of AASB 16 would increase the profit before tax of

Woolworths. Finally, it has been evaluated that AASB 16 would result in global increase in debt

and EBITDA in all the industries; however, the impact would be severe on the retail sector.

asset procurement and others (Xu, Davidson & Cheong, 2017). Due to these reasons, it would

become difficult to gain popularity for AASB 16.

Conclusion:

Based on the above discussion, it could be found that Woolworths Limited has realised

its operating lease payments in the form of expense on straight-line basis over the term of the

lease. The rise in fixed rates to lease rental payments and exclusion of contingent or index-based

rental rises are realised on straight-line basis over the term of the lease. Once AASB 16 comes

into effect on 1st January 2019, it would have considerable effect on the financial statements and

gearing ratios of Woolworths Limited both in short-run and long-run. Due to the presence of off-

balance sheet lease, the application of AASB 16 would increase the profit before tax of

Woolworths. Finally, it has been evaluated that AASB 16 would result in global increase in debt

and EBITDA in all the industries; however, the impact would be severe on the retail sector.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.