Managerial Accounting HA2011: Activity Based Budgeting for DHL India

VerifiedAdded on 2023/06/04

|24

|4263

|334

Report

AI Summary

This report evaluates the feasibility of implementing activity based budgeting (ABB) at DHL Express (India) Private Limited. It begins with an overview of DHL Express (India), highlighting its operations and strategic transition. The report then describes ABB, detailing its features and contrasting it with traditional budgeting systems, emphasizing the importance of identifying cost drivers and aligning activities with organizational strategies. It discusses the suitability of ABB for DHL, considering the company's focus on cost management and competitive market environment. The report concludes by summarizing the potential benefits and challenges of adopting ABB within DHL Express (India).

Accounting

Assignment

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 23rd Sep 2018.

1 | Page

By student name

Professor

University

Date: 23rd Sep 2018.

1 | Page

2

Executive Summary

We have prepared this assignment on the activity based budgeting and have considered the

feasibility report of DHL Express (India) Private Limited. All the discussions have been done on

the advantages and drawbacks of ABB and the reason for its adoption has also been discussed

below. The assignment highlights the different ways in which ABC costing can be put to use by

the company

2 | Page

Executive Summary

We have prepared this assignment on the activity based budgeting and have considered the

feasibility report of DHL Express (India) Private Limited. All the discussions have been done on

the advantages and drawbacks of ABB and the reason for its adoption has also been discussed

below. The assignment highlights the different ways in which ABC costing can be put to use by

the company

2 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Introduction.................................................................................................................................................4

Key Points....................................................................................................................................................4

a). A brief description of the Client Company..............................................................................................5

b). Description of ABB and its features........................................................................................................6

Features of Activity Based Budgeting........................................................................................................10

c). Difference between ABB and Traditional Budgeting system.................................................................11

Difference between traditional budget and Activity based budgeting......................................................18

d). Discussion on the Suitability of ABB.....................................................................................................21

Conclusion.................................................................................................................................................21

References.................................................................................................................................................22

3 | Page

Contents

Introduction.................................................................................................................................................4

Key Points....................................................................................................................................................4

a). A brief description of the Client Company..............................................................................................5

b). Description of ABB and its features........................................................................................................6

Features of Activity Based Budgeting........................................................................................................10

c). Difference between ABB and Traditional Budgeting system.................................................................11

Difference between traditional budget and Activity based budgeting......................................................18

d). Discussion on the Suitability of ABB.....................................................................................................21

Conclusion.................................................................................................................................................21

References.................................................................................................................................................22

3 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

After viewing the current market trends and increasing competition in the industry, DHL Express

(India) Private Limited has become keen on introducing better reforms in the organization for

proper administration and cost management. The chief executive officer of the company has

stressed on replacing the current budgeting practices with a better and sound budgeting practice.

For this the chief executive officer of the company has been attending various seminars in this

regard and has recently come across activity based budgeting model (Andiola, et al., 2018). He is

considering the introduction of the activity based budgeting into the organization. But before the

adoption of this system of budgeting he wants analyze the system more deeply. The chief

executive officer of DHL Express (India) Private Limited approached ABC Management

Consultants for a proper evaluation of the system of activity based budgeting. The chief

executive officer need ABC Management Consultants to provide the CEO with a feasibility

report in this regard to analyze the viability of adopting activity based budgeting, the current

circumstances of the company (Bumgarner & Vasarhelyi, 2018).

Key Points

4 | Page

Introduction

After viewing the current market trends and increasing competition in the industry, DHL Express

(India) Private Limited has become keen on introducing better reforms in the organization for

proper administration and cost management. The chief executive officer of the company has

stressed on replacing the current budgeting practices with a better and sound budgeting practice.

For this the chief executive officer of the company has been attending various seminars in this

regard and has recently come across activity based budgeting model (Andiola, et al., 2018). He is

considering the introduction of the activity based budgeting into the organization. But before the

adoption of this system of budgeting he wants analyze the system more deeply. The chief

executive officer of DHL Express (India) Private Limited approached ABC Management

Consultants for a proper evaluation of the system of activity based budgeting. The chief

executive officer need ABC Management Consultants to provide the CEO with a feasibility

report in this regard to analyze the viability of adopting activity based budgeting, the current

circumstances of the company (Bumgarner & Vasarhelyi, 2018).

Key Points

4 | Page

5

a). A brief description of the Client Company

DHL Express (India) Private Limited is a wing of a German logistics company, being Deutsche

Post DHL, in India. It is one of the most renowned transportation and logistics company

involved in the courier services and logistics services to all types of customers being residential,

industrial, commercial and business customers. The various activities which are involved in the

business of DHL Express (India) Private Limited include repair and return, direct express

inventory and strategic inventory management. It is also engaged in the business of

transportation and has a fleet of vehicles (Charles H, et al., 2015). Apart from the above

mentioned activities the other value added activities in this business are services planning,

vehicles set up, customers order processing, manual loading, mechanical loading, fuel supply,

road journey, manual unloading, mechanical unloading, maintenance, technical support, etc, all

these activities have related activity drivers or cost drivers such as number of vehicles, site

orders, issuing fuel orders, number of liters, team working hours, loaded tons, distance

kilometers, unloaded tons, maintenance shop hours, etc. There were several non value added

activities as well like unnecessary transportation, waiting, non value added processing, excess

inventory, defects, unnecessary motion, etc. the company has spent a lot of amount on the

operational activities due to which the profit of the company in past few years were below

expectation. These costs were incurred in order to increase the quality of service provided by the

company to its customers. This has resulted in lower profits for the company.

There is cut throat competition in the market, which is ever increasing. Same has been the case in

the transportation and logistics sector (Garon, 2018). To face the competition the company has

5 | Page

a). A brief description of the Client Company

DHL Express (India) Private Limited is a wing of a German logistics company, being Deutsche

Post DHL, in India. It is one of the most renowned transportation and logistics company

involved in the courier services and logistics services to all types of customers being residential,

industrial, commercial and business customers. The various activities which are involved in the

business of DHL Express (India) Private Limited include repair and return, direct express

inventory and strategic inventory management. It is also engaged in the business of

transportation and has a fleet of vehicles (Charles H, et al., 2015). Apart from the above

mentioned activities the other value added activities in this business are services planning,

vehicles set up, customers order processing, manual loading, mechanical loading, fuel supply,

road journey, manual unloading, mechanical unloading, maintenance, technical support, etc, all

these activities have related activity drivers or cost drivers such as number of vehicles, site

orders, issuing fuel orders, number of liters, team working hours, loaded tons, distance

kilometers, unloaded tons, maintenance shop hours, etc. There were several non value added

activities as well like unnecessary transportation, waiting, non value added processing, excess

inventory, defects, unnecessary motion, etc. the company has spent a lot of amount on the

operational activities due to which the profit of the company in past few years were below

expectation. These costs were incurred in order to increase the quality of service provided by the

company to its customers. This has resulted in lower profits for the company.

There is cut throat competition in the market, which is ever increasing. Same has been the case in

the transportation and logistics sector (Garon, 2018). To face the competition the company has

5 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

been transitioning from the older strategy to the newer strategy, that is, from strategy 2015 to

strategy 2020.

b). Description of ABB and its features

There are various types of budgeting of which, one is Activity based budgeting. The activity

based budgeting is a system of budgeting which involves researching, recording and analyzing

the various activities of an organization which leads to costs for a business. Activity based

budgeting is different from traditional budgeting in a way that it involves identification of

different cost drivers or cost activities. Which goes to say that it is closely related to activity

based costing (Kangarluie & Aalizadeh, 2017).

The concept of activity based budgeting is very much like that of the activity based budgeting. In

order to understand this system of budgeting we have taken an example, which is presented

below:

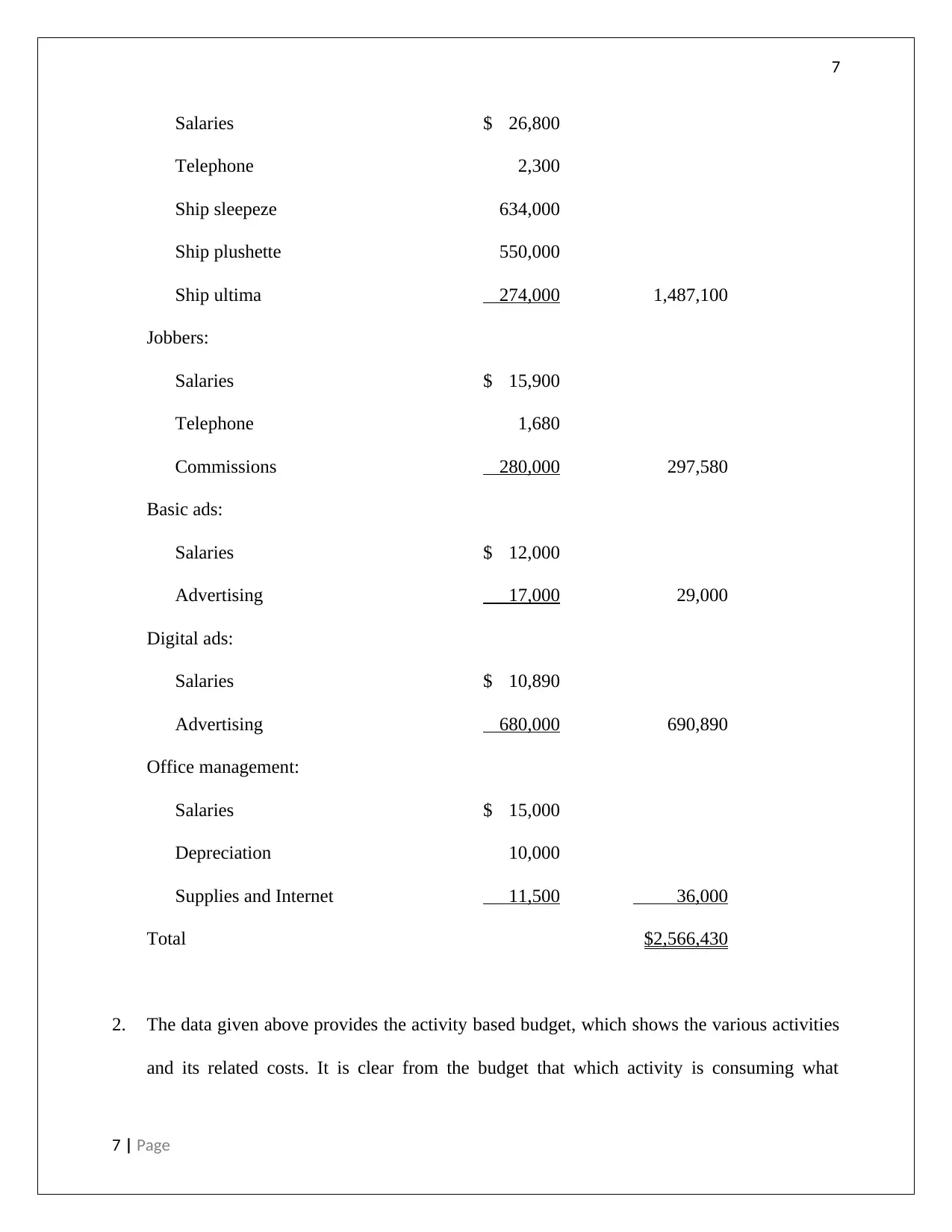

Activity-based budget:

Research:

Salaries $ 24000

Internet connection 1,860 $ 25,860

Shipping:

6 | Page

been transitioning from the older strategy to the newer strategy, that is, from strategy 2015 to

strategy 2020.

b). Description of ABB and its features

There are various types of budgeting of which, one is Activity based budgeting. The activity

based budgeting is a system of budgeting which involves researching, recording and analyzing

the various activities of an organization which leads to costs for a business. Activity based

budgeting is different from traditional budgeting in a way that it involves identification of

different cost drivers or cost activities. Which goes to say that it is closely related to activity

based costing (Kangarluie & Aalizadeh, 2017).

The concept of activity based budgeting is very much like that of the activity based budgeting. In

order to understand this system of budgeting we have taken an example, which is presented

below:

Activity-based budget:

Research:

Salaries $ 24000

Internet connection 1,860 $ 25,860

Shipping:

6 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Salaries $ 26,800

Telephone 2,300

Ship sleepeze 634,000

Ship plushette 550,000

Ship ultima 274,000 1,487,100

Jobbers:

Salaries $ 15,900

Telephone 1,680

Commissions 280,000 297,580

Basic ads:

Salaries $ 12,000

Advertising 17,000 29,000

Digital ads:

Salaries $ 10,890

Advertising 680,000 690,890

Office management:

Salaries $ 15,000

Depreciation 10,000

Supplies and Internet 11,500 36,000

Total $2,566,430

2. The data given above provides the activity based budget, which shows the various activities

and its related costs. It is clear from the budget that which activity is consuming what

7 | Page

Salaries $ 26,800

Telephone 2,300

Ship sleepeze 634,000

Ship plushette 550,000

Ship ultima 274,000 1,487,100

Jobbers:

Salaries $ 15,900

Telephone 1,680

Commissions 280,000 297,580

Basic ads:

Salaries $ 12,000

Advertising 17,000 29,000

Digital ads:

Salaries $ 10,890

Advertising 680,000 690,890

Office management:

Salaries $ 15,000

Depreciation 10,000

Supplies and Internet 11,500 36,000

Total $2,566,430

2. The data given above provides the activity based budget, which shows the various activities

and its related costs. It is clear from the budget that which activity is consuming what

7 | Page

8

portion of the company’s money. For example, we can say from looking at the budget that

the most cost intensive activity is advertising, where the highest amount of cost is involved

and jobbers is second costly activity in the budget. With the help of this budget, the

management of the organization can take measures to reduce the cost related to advertising

and jobbers. However, reducing the cost of advertising becomes quite problematic in case of

first year of operation of the company. Hence the management is required to look into this

matter with other possible measures (Mock, et al., 2018).

While the development of the activity based budgeting, there are several things that is needed to

be identified. Some such things have been mentioned below:

i) The association of the activity level volume driver with the source of an activity level

volume driver within the organization.

ii) Ways in which the main source of the activity level volume driver can affect the

requirements of resources in respect of an activity and how it can be changed.

iii) The activities being performed by the organization should be performed with efficacy

and should meet the levels of standard as laid down for this purpose (Lessambo,

2018).

While executing the process of activity based budgeting there are various other things which

requires attention. Some of these activities includes recognition of the resources which are used

8 | Page

portion of the company’s money. For example, we can say from looking at the budget that

the most cost intensive activity is advertising, where the highest amount of cost is involved

and jobbers is second costly activity in the budget. With the help of this budget, the

management of the organization can take measures to reduce the cost related to advertising

and jobbers. However, reducing the cost of advertising becomes quite problematic in case of

first year of operation of the company. Hence the management is required to look into this

matter with other possible measures (Mock, et al., 2018).

While the development of the activity based budgeting, there are several things that is needed to

be identified. Some such things have been mentioned below:

i) The association of the activity level volume driver with the source of an activity level

volume driver within the organization.

ii) Ways in which the main source of the activity level volume driver can affect the

requirements of resources in respect of an activity and how it can be changed.

iii) The activities being performed by the organization should be performed with efficacy

and should meet the levels of standard as laid down for this purpose (Lessambo,

2018).

While executing the process of activity based budgeting there are various other things which

requires attention. Some of these activities includes recognition of the resources which are used

8 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

in the production process along with the recognition of outputs that are being produced by the

organization. Just like activity based costing, the activity based budgeting is about allocation of

the costs to the respective activity on the basis of activity driver in respect of every products and

services. Such allocations are based on the characteristics of those products and services in

relation which they are being allocated.

We have already mentioned above the connection of the activity based budgeting with the

activity based costing. This connection is very important for the implementation of the aqctivity

based budgeting in an organization, since the implementation of the activity based budgeting

requires the organization to follow activity based costing as the system of cost account of the

organization or else the activity based budgeting will not work (Mock, et al., 2018).

There are several fundamental principles in relation to the activity based budgeting which the

organization is required to take under consideration. These fundamental principles are as

follows:

i) Proper and sufficient connection should be formed between the organization’s

activities and its strategies.

ii) Gap analysis should be conducted in order to form the connection between the

activities and organizational strategy.

iii) It is necessary to ascertain the management of the capacity and a sound prediction of

the company’s revenue.

iv) There must exist, a proper connection between the business of the organization and its

business processes.

9 | Page

in the production process along with the recognition of outputs that are being produced by the

organization. Just like activity based costing, the activity based budgeting is about allocation of

the costs to the respective activity on the basis of activity driver in respect of every products and

services. Such allocations are based on the characteristics of those products and services in

relation which they are being allocated.

We have already mentioned above the connection of the activity based budgeting with the

activity based costing. This connection is very important for the implementation of the aqctivity

based budgeting in an organization, since the implementation of the activity based budgeting

requires the organization to follow activity based costing as the system of cost account of the

organization or else the activity based budgeting will not work (Mock, et al., 2018).

There are several fundamental principles in relation to the activity based budgeting which the

organization is required to take under consideration. These fundamental principles are as

follows:

i) Proper and sufficient connection should be formed between the organization’s

activities and its strategies.

ii) Gap analysis should be conducted in order to form the connection between the

activities and organizational strategy.

iii) It is necessary to ascertain the management of the capacity and a sound prediction of

the company’s revenue.

iv) There must exist, a proper connection between the business of the organization and its

business processes.

9 | Page

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

The activity based budgeting is considered to be more effective in case of those organization

where the indirect costs consumes considerable portion of the total operational costs. As we

know that activity based budgeting involves allocation of costs based on cost drivers to their

respective activities, it is very famous in such kind of organizations where indirect cost is too

high and the organization is engaged in performing various kinds of activities (Mubako &

O'Donnell, 2018).

Features of Activity Based Budgeting

The key features of Activity Based Budgeting are being mentioned below:

i) Activity based budgeting is being considered as a participative process in order to

control and sustain continuous improvement (Eddy, et al., 2004)

ii) Activity based budgeting integrates the activity planning with accounting to provide

effective control within the organization

iii) Activity based budgeting enables the establishment of performance targets in the

organization for the purpose of control

iv) Activity based budgeting enables the management in the identification of various

opportunities for the improvement of the entity’s costs

v) Activity based budgeting assists in analyzing the various discretionary spending

options and prepares a priority ranking

vi) It is being considered as a process which links the organization’s strategic goals and

objectives to the planning process

10 | Page

The activity based budgeting is considered to be more effective in case of those organization

where the indirect costs consumes considerable portion of the total operational costs. As we

know that activity based budgeting involves allocation of costs based on cost drivers to their

respective activities, it is very famous in such kind of organizations where indirect cost is too

high and the organization is engaged in performing various kinds of activities (Mubako &

O'Donnell, 2018).

Features of Activity Based Budgeting

The key features of Activity Based Budgeting are being mentioned below:

i) Activity based budgeting is being considered as a participative process in order to

control and sustain continuous improvement (Eddy, et al., 2004)

ii) Activity based budgeting integrates the activity planning with accounting to provide

effective control within the organization

iii) Activity based budgeting enables the establishment of performance targets in the

organization for the purpose of control

iv) Activity based budgeting enables the management in the identification of various

opportunities for the improvement of the entity’s costs

v) Activity based budgeting assists in analyzing the various discretionary spending

options and prepares a priority ranking

vi) It is being considered as a process which links the organization’s strategic goals and

objectives to the planning process

10 | Page

11

vii) Activity based budgeting uses those activity analysis techniques which are well

proven, which is the source of all activity based system

viii) Activity based budgeting involves lots of complexity as it requires a thorough

research and assessment on the different activities and resources which are crucial for

the entity

ix) The orientation of the activity based budgeting is toward short term goals and

objectives of the organization instead of long term goals (Abdullah & Said, 2017)

x) This has been considered the best method of budgeting since it helps in the

identification of the value added and non value added activities in the organization

xi) Activity based budgeting is a process of planning which is connected to the strategic

objectives of the organization

c). Difference between ABB and Traditional Budgeting system

Traditional system of Budgeting

Traditional budgeting is method of budgeting which has become quite outdated in today’s

time. It is process of preparation of budget by taking the budget of the previous year as base.

The projection of the business revenue and business expenses of the current year is done on

the basis of those of last year. It is an accounting tool which helps in the prediction and

analysis of the earnings of the business along with its expenses. The budget of the last year is

11 | Page

vii) Activity based budgeting uses those activity analysis techniques which are well

proven, which is the source of all activity based system

viii) Activity based budgeting involves lots of complexity as it requires a thorough

research and assessment on the different activities and resources which are crucial for

the entity

ix) The orientation of the activity based budgeting is toward short term goals and

objectives of the organization instead of long term goals (Abdullah & Said, 2017)

x) This has been considered the best method of budgeting since it helps in the

identification of the value added and non value added activities in the organization

xi) Activity based budgeting is a process of planning which is connected to the strategic

objectives of the organization

c). Difference between ABB and Traditional Budgeting system

Traditional system of Budgeting

Traditional budgeting is method of budgeting which has become quite outdated in today’s

time. It is process of preparation of budget by taking the budget of the previous year as base.

The projection of the business revenue and business expenses of the current year is done on

the basis of those of last year. It is an accounting tool which helps in the prediction and

analysis of the earnings of the business along with its expenses. The budget of the last year is

11 | Page

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.