Activity Based Costing Analysis for Baulkham Hills Shire Council

VerifiedAdded on 2023/06/04

|14

|1139

|210

Report

AI Summary

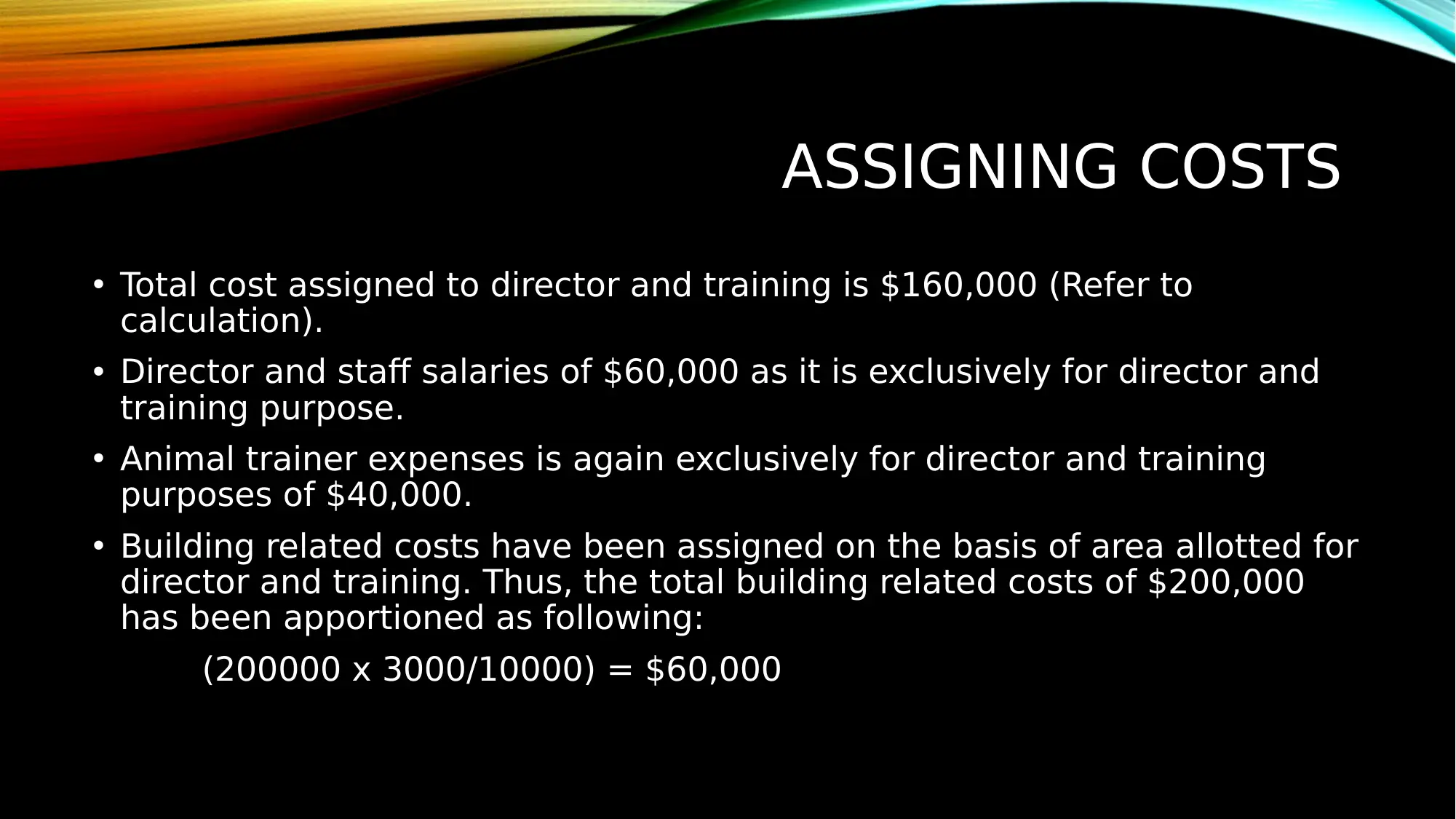

This report provides an Activity Based Costing (ABC) analysis for the Baulkham Hills Shire Council, focusing on the animal shelter, director and training, and veterinarian clinic facilities. It identifies cost pools, assigns costs, and determines cost drivers to allocate overheads and expenditures effectively. The analysis includes calculations of total costs assigned to each facility, the determination of appropriate cost drivers, and the allocation rates for each cost pool. The report highlights the benefits of ABC over conventional costing, emphasizing its ability to allocate costs on a rational basis and improve cost management. The findings show that ABC provides a more accurate method to ascertain the cost of different services and products. The report also includes references to relevant academic sources supporting the analysis.

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.