Activity-Based Costing (ABC) for Blackmores Limited

VerifiedAdded on 2021/06/16

|13

|3058

|31

Report

AI Summary

This report examines the application of Activity-Based Costing (ABC) for Blackmores Limited, a vitamin, mineral, and herbal supplements firm. The analysis includes an executive summary, introduction to ABC, and a detailed explanation of the model's features. It explores Blackmores' mission, objectives, and corporate strategies, assessing how ABC aligns with these goals. The report offers recommendations for implementing ABC within the company, emphasizing product differentiation and quality improvement. Additionally, it suggests financial planning as a key management accounting model. The report concludes with a discussion of ABC's benefits in cost management and strategic alignment, supported by references.

Activity-Based Costing for Blackmore LTD 1

ACTIVITY-BASED COSTING FOR BLACKMORE LTD

Student (Name)

Professor (Name)

College

Course

Date

ACTIVITY-BASED COSTING FOR BLACKMORE LTD

Student (Name)

Professor (Name)

College

Course

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Costing for Blackmore LTD 2

Contents

Executive summary.........................................................................................................................3

Introduction..................................................................................................................................3

Main body........................................................................................................................................4

Explanation of ABC model and its features.................................................................................4

Features....................................................................................................................................4

Blackmores LTD Mission and Objectives.......................................................................................5

Mission- What the company strives for.......................................................................................5

Objectives.................................................................................................................................5

Blackmores LTD corporate strategies.............................................................................................5

How activity-based costing (ABC) model aligns with the current goals and strategies of the

company...........................................................................................................................................6

Recommendations for the implementation of activity-based costing (ABC) model for

Blackmores Limited.........................................................................................................................7

Conclusion.......................................................................................................................................7

References…………………………………………………………………………………………

……………………………………………………8

Contents

Executive summary.........................................................................................................................3

Introduction..................................................................................................................................3

Main body........................................................................................................................................4

Explanation of ABC model and its features.................................................................................4

Features....................................................................................................................................4

Blackmores LTD Mission and Objectives.......................................................................................5

Mission- What the company strives for.......................................................................................5

Objectives.................................................................................................................................5

Blackmores LTD corporate strategies.............................................................................................5

How activity-based costing (ABC) model aligns with the current goals and strategies of the

company...........................................................................................................................................6

Recommendations for the implementation of activity-based costing (ABC) model for

Blackmores Limited.........................................................................................................................7

Conclusion.......................................................................................................................................7

References…………………………………………………………………………………………

……………………………………………………8

Activity-Based Costing for Blackmore LTD 3

ACTIVITY-BASED COSTING FOR BLACKMORE LTD

Executive summary

With the propagation of technology and computer related services, the outburst in data

communication systems, and the rapidly changing trends about globalization, the corporate

world and the mangers in various industries are searching for considerable new ways and

methods in managing and controlling costs. Despite the fact that most of the companies dealing

with online or IT related services have varying degrees of senselessness or intangibility, the

major challenge they face is measuring the costs of the services they deliver. Ideally, Activity-

based costing (ABC), an alternative approach to the traditional costs accounting systems, has

been used or applied to various industries, for example, the manufacturing and service industries.

Consequently, there has been successful enforcement of this system in the insurance, healthcare,

and transport industries over the few last years, but very few publications associate ABC to the

IT-related firms. This research reports on the cost management undertaking using ABC

framework focused on the management division of a vitamin, mineral and herbal supplements

firm (Blackmore). The requirement for the company to create accurate and explicit recharge

rates, aligning the model to the current goals and the strategies of the company in the corporate

domain, how the model helps company achieve its strategies and the recommendation about the

enforcement or implementation of this model for the company based on various findings

(Askarany et al., 2010). The modeling procedure needs the identification of resources, costs

objects, activities and the forces that correspond closely to the organizational obligations within

the management parameters. Finally, the resulting framework gives a managerial tool to quantify

productivity and efficiency for the firm.

ACTIVITY-BASED COSTING FOR BLACKMORE LTD

Executive summary

With the propagation of technology and computer related services, the outburst in data

communication systems, and the rapidly changing trends about globalization, the corporate

world and the mangers in various industries are searching for considerable new ways and

methods in managing and controlling costs. Despite the fact that most of the companies dealing

with online or IT related services have varying degrees of senselessness or intangibility, the

major challenge they face is measuring the costs of the services they deliver. Ideally, Activity-

based costing (ABC), an alternative approach to the traditional costs accounting systems, has

been used or applied to various industries, for example, the manufacturing and service industries.

Consequently, there has been successful enforcement of this system in the insurance, healthcare,

and transport industries over the few last years, but very few publications associate ABC to the

IT-related firms. This research reports on the cost management undertaking using ABC

framework focused on the management division of a vitamin, mineral and herbal supplements

firm (Blackmore). The requirement for the company to create accurate and explicit recharge

rates, aligning the model to the current goals and the strategies of the company in the corporate

domain, how the model helps company achieve its strategies and the recommendation about the

enforcement or implementation of this model for the company based on various findings

(Askarany et al., 2010). The modeling procedure needs the identification of resources, costs

objects, activities and the forces that correspond closely to the organizational obligations within

the management parameters. Finally, the resulting framework gives a managerial tool to quantify

productivity and efficiency for the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-Based Costing for Blackmore LTD 4

Introduction

During the past two decades activity-based costing (ABC) has been to rated in the

summit of the academic and journals and documented in management accounting textbooks as a

model that upholds accuracy of the product service costing and also guides mangers and the

chief executives of the companies in comprehending how resources are utilized across the

company’s value chains to give strategic results. Because of the activity-based costing, managers

are now at peace with the assessment of all the activities in their respective firms and allocate the

needed resources for their implementation with all the processes involved accounted for. This

system is very attractive and valuable to the companies in the competitive and stiff environments

that require a lot of cost reduction, especially when the traditional or the existing cost systems

fail to address such rational support (Baird 2007). Despite the fact that many firms are aware of

the contemporary advancements in technology and the global economic environment that has

rendered the traditional cost accounting systems irrelevant, the fact remains that they have to

perceive net benefits before enforcing activity-based costing. Because restructuring and

reconstructing the required systems are significant and expensive.

Regarding Blackmore LTD, in addressing the preempted matters, this study seeks to

assess and address the perceived success of ABC in this particular company. Therefore the paper

will address specifically; the requirement for the company to create accurate and explicit

recharge rates, aligning the model to the current goals and the strategies of the company in the

corporate competitive environment, how the model helps company achieve its strategies and the

recommendation about the enforcement or implementation of this model for the company based

on various findings.

Introduction

During the past two decades activity-based costing (ABC) has been to rated in the

summit of the academic and journals and documented in management accounting textbooks as a

model that upholds accuracy of the product service costing and also guides mangers and the

chief executives of the companies in comprehending how resources are utilized across the

company’s value chains to give strategic results. Because of the activity-based costing, managers

are now at peace with the assessment of all the activities in their respective firms and allocate the

needed resources for their implementation with all the processes involved accounted for. This

system is very attractive and valuable to the companies in the competitive and stiff environments

that require a lot of cost reduction, especially when the traditional or the existing cost systems

fail to address such rational support (Baird 2007). Despite the fact that many firms are aware of

the contemporary advancements in technology and the global economic environment that has

rendered the traditional cost accounting systems irrelevant, the fact remains that they have to

perceive net benefits before enforcing activity-based costing. Because restructuring and

reconstructing the required systems are significant and expensive.

Regarding Blackmore LTD, in addressing the preempted matters, this study seeks to

assess and address the perceived success of ABC in this particular company. Therefore the paper

will address specifically; the requirement for the company to create accurate and explicit

recharge rates, aligning the model to the current goals and the strategies of the company in the

corporate competitive environment, how the model helps company achieve its strategies and the

recommendation about the enforcement or implementation of this model for the company based

on various findings.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Costing for Blackmore LTD 5

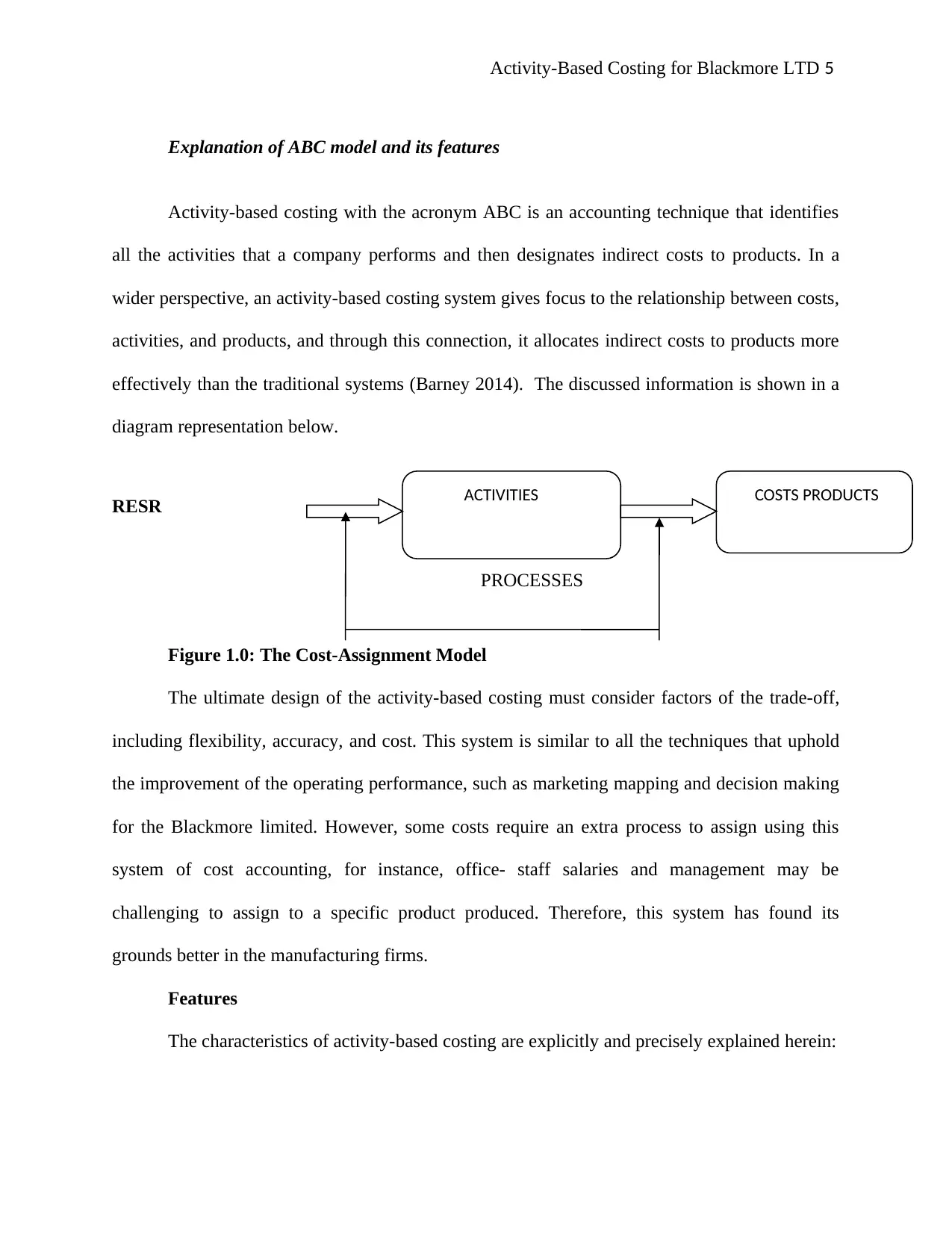

Explanation of ABC model and its features

Activity-based costing with the acronym ABC is an accounting technique that identifies

all the activities that a company performs and then designates indirect costs to products. In a

wider perspective, an activity-based costing system gives focus to the relationship between costs,

activities, and products, and through this connection, it allocates indirect costs to products more

effectively than the traditional systems (Barney 2014). The discussed information is shown in a

diagram representation below.

RESR

PROCESSES

Figure 1.0: The Cost-Assignment Model

The ultimate design of the activity-based costing must consider factors of the trade-off,

including flexibility, accuracy, and cost. This system is similar to all the techniques that uphold

the improvement of the operating performance, such as marketing mapping and decision making

for the Blackmore limited. However, some costs require an extra process to assign using this

system of cost accounting, for instance, office- staff salaries and management may be

challenging to assign to a specific product produced. Therefore, this system has found its

grounds better in the manufacturing firms.

Features

The characteristics of activity-based costing are explicitly and precisely explained herein:

COSTS PRODUCTSACTIVITIES

Explanation of ABC model and its features

Activity-based costing with the acronym ABC is an accounting technique that identifies

all the activities that a company performs and then designates indirect costs to products. In a

wider perspective, an activity-based costing system gives focus to the relationship between costs,

activities, and products, and through this connection, it allocates indirect costs to products more

effectively than the traditional systems (Barney 2014). The discussed information is shown in a

diagram representation below.

RESR

PROCESSES

Figure 1.0: The Cost-Assignment Model

The ultimate design of the activity-based costing must consider factors of the trade-off,

including flexibility, accuracy, and cost. This system is similar to all the techniques that uphold

the improvement of the operating performance, such as marketing mapping and decision making

for the Blackmore limited. However, some costs require an extra process to assign using this

system of cost accounting, for instance, office- staff salaries and management may be

challenging to assign to a specific product produced. Therefore, this system has found its

grounds better in the manufacturing firms.

Features

The characteristics of activity-based costing are explicitly and precisely explained herein:

COSTS PRODUCTSACTIVITIES

Activity-Based Costing for Blackmore LTD 6

-The total or the overall cost is subdivided into two, for example, variable costs and fixed

cost which is very useful in giving quality and reliable information for designing of a suitable

cost model in a manufacturing arena (Baykasoğlu and Kaplanoğlu 2008).

-The significant difference is drawn between the cost behavior patterns.

-The cost behavior patterns are related regarding volume, density, time and events or

occurrences.

-The relevant cost force has to be recognized for accounting for the overhead to a product

or service.

-The cost behavior patterns are determined and dictated by the cost drivers.

Blackmore’s LTD Mission and Objectives

Mission- What the company strives for

Blackmore Limited mission statement states that; "Blackmore's success is premised on

the way we focus on our clients, be innovative, responsible actions with one another at the firm,

the environment and the community around us and strive to demonstrative our values through

innovative ways. We aim to discover, create and develop the best quality natural health formulas

and establish a sustainable market base to prevent disease, to encourage community wellness,

and to improve individual’s lives. We also want to raise the reward shareholders who invest their

finances, believes, trusts and performance of Blackmore’s in the long run.”

Objectives

A target of a minimum of fifty percent rise in the operational capacity by the end of the

year 2017 to focus on supply problems of pharmacies, healthy food stores and by extension e-

commerce paths in Australia.

-The total or the overall cost is subdivided into two, for example, variable costs and fixed

cost which is very useful in giving quality and reliable information for designing of a suitable

cost model in a manufacturing arena (Baykasoğlu and Kaplanoğlu 2008).

-The significant difference is drawn between the cost behavior patterns.

-The cost behavior patterns are related regarding volume, density, time and events or

occurrences.

-The relevant cost force has to be recognized for accounting for the overhead to a product

or service.

-The cost behavior patterns are determined and dictated by the cost drivers.

Blackmore’s LTD Mission and Objectives

Mission- What the company strives for

Blackmore Limited mission statement states that; "Blackmore's success is premised on

the way we focus on our clients, be innovative, responsible actions with one another at the firm,

the environment and the community around us and strive to demonstrative our values through

innovative ways. We aim to discover, create and develop the best quality natural health formulas

and establish a sustainable market base to prevent disease, to encourage community wellness,

and to improve individual’s lives. We also want to raise the reward shareholders who invest their

finances, believes, trusts and performance of Blackmore’s in the long run.”

Objectives

A target of a minimum of fifty percent rise in the operational capacity by the end of the

year 2017 to focus on supply problems of pharmacies, healthy food stores and by extension e-

commerce paths in Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-Based Costing for Blackmore LTD 7

- In comparison with the previous years, the company expects at least seventy percent

increase in the overall sales in the coming years.

-The growth of twenty-five percent of the operating cash flows over the 12 months

periods from 2016 to date.

-The growth of the Asian consumers to make the group sales increase to eighty percent in

the coming years.

-To raise or increase the number of research symposia and clinical trials at the company.

And subsequently, to increase the number of research institutions and double education touch

points in the coming three years (Horngren 2009).

Blackmore LTD corporate strategies

Basing on the market niche and the company’s nature and the brand repute, improving

the distinctions or the differentiation of the products is the major cooperate strategy and the

competitive advantages. Supposing, the cost leadership strategy is not well enforced, it may

have negative impacts on the company’s wonderful reputation and make people suspect the

functionality and the quality of the company’s products. According to some researchers, the

differentiation strategy empowers the firm to posses’ better sustainability of performance as

compared to cost leadership strategy (Kallunki and Silvola 2008). Consequently, another

corporate strategy of the company is the adoption of the premium prices, which makes their

products and services unique and attracts customers. Despite the fact that investing in R&D may

be too costly, the company should consider the strategy.

Similarly, a total comprehension of the domestic and global markets is also a strategy the

company is exploiting basing on their product differentiation. This will ensure growth since the

company's products and services are channeled to a wider customer base. To be on the vantage

- In comparison with the previous years, the company expects at least seventy percent

increase in the overall sales in the coming years.

-The growth of twenty-five percent of the operating cash flows over the 12 months

periods from 2016 to date.

-The growth of the Asian consumers to make the group sales increase to eighty percent in

the coming years.

-To raise or increase the number of research symposia and clinical trials at the company.

And subsequently, to increase the number of research institutions and double education touch

points in the coming three years (Horngren 2009).

Blackmore LTD corporate strategies

Basing on the market niche and the company’s nature and the brand repute, improving

the distinctions or the differentiation of the products is the major cooperate strategy and the

competitive advantages. Supposing, the cost leadership strategy is not well enforced, it may

have negative impacts on the company’s wonderful reputation and make people suspect the

functionality and the quality of the company’s products. According to some researchers, the

differentiation strategy empowers the firm to posses’ better sustainability of performance as

compared to cost leadership strategy (Kallunki and Silvola 2008). Consequently, another

corporate strategy of the company is the adoption of the premium prices, which makes their

products and services unique and attracts customers. Despite the fact that investing in R&D may

be too costly, the company should consider the strategy.

Similarly, a total comprehension of the domestic and global markets is also a strategy the

company is exploiting basing on their product differentiation. This will ensure growth since the

company's products and services are channeled to a wider customer base. To be on the vantage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Costing for Blackmore LTD 8

side due to the stiff competition in the market, the company should also consider, instead of

raising the prices of their products which is risky, but rather focus or concentrate on increasing

the perceived quality while holding their price at the very level. Finally, the company is on the

move to short-term differentiation without necessarily considering the price premium strategy

and focus on the additional investment in R&D which may seem expensive (Briers and Chua

2009). Blackmore has got a competitive advantage to create and develop its product portfolio

and enlarge its brand into the new market segments because almost a quarter of its population is

regarded as qualified health personnel who are based in both Australian and the Asian markets

segments. Since the company has got a wonderful reputation concerning its products like

vitamin and supplement brands gives it the leverage for sustainable growth. The management

using activity-based costing should ensure that the products are maintained at the very vantage

point through provisions, allocations and thorough assessments throughout the entire time.

How activity-based costing (ABC) model aligns with the current goals and strategies

of the company.

Blackmore Director reports that revenue for the last two years registered and increment

of 13.7%. In fact, the profit margin after the tax increased by 7.1% on the last year. This report

was reviewed and audited by the company’s auditor. Again in my analysis of the company's

condensed consolidated statement of cash flows, over the past years was made by historical cost

and activities except for revaluation of certain financial factors (LaLonde and Pohlen 2007). The

analysis of the company is premised on its critical factor; the cooperate strategies like differential

of the products and the goals the company wants to achieve. Therefore, in this case, the focus is

based on the analysis of the company's value chain, which presents relevant data or information

for the activity-based costing to be defined. In Blackmore limited, the output is quantified by

side due to the stiff competition in the market, the company should also consider, instead of

raising the prices of their products which is risky, but rather focus or concentrate on increasing

the perceived quality while holding their price at the very level. Finally, the company is on the

move to short-term differentiation without necessarily considering the price premium strategy

and focus on the additional investment in R&D which may seem expensive (Briers and Chua

2009). Blackmore has got a competitive advantage to create and develop its product portfolio

and enlarge its brand into the new market segments because almost a quarter of its population is

regarded as qualified health personnel who are based in both Australian and the Asian markets

segments. Since the company has got a wonderful reputation concerning its products like

vitamin and supplement brands gives it the leverage for sustainable growth. The management

using activity-based costing should ensure that the products are maintained at the very vantage

point through provisions, allocations and thorough assessments throughout the entire time.

How activity-based costing (ABC) model aligns with the current goals and strategies

of the company.

Blackmore Director reports that revenue for the last two years registered and increment

of 13.7%. In fact, the profit margin after the tax increased by 7.1% on the last year. This report

was reviewed and audited by the company’s auditor. Again in my analysis of the company's

condensed consolidated statement of cash flows, over the past years was made by historical cost

and activities except for revaluation of certain financial factors (LaLonde and Pohlen 2007). The

analysis of the company is premised on its critical factor; the cooperate strategies like differential

of the products and the goals the company wants to achieve. Therefore, in this case, the focus is

based on the analysis of the company's value chain, which presents relevant data or information

for the activity-based costing to be defined. In Blackmore limited, the output is quantified by

Activity-Based Costing for Blackmore LTD 9

every individual activity to better define the required or relevant activity rates for the overall

calculation and accounting of the product cost.

The undertakings of Blackmore's company like a strategic move to establish the premium

prices for their products, or otherwise enhance the quality of their products and services while

maintaining the very market prices for competitive advantage, reflect all the dimensions of

strategic cost management, ranging from market mapping to establishing the ideal products and

prices. Also in this context, there is an explicit explanation on how activity-based costing or cost

management was used to achieve the company’s objectives for the previous years, where

sustainable growth had been recorded (Wegmann 2008). Perhaps sometimes through striving to

implement this system, for instance, tracking down activity costs and processes to products and

market the cost drivers are not properly measured in spite the fact that they drive critical

organizational costs. The managers should be well acquainted with the following two alternative

options: disregard all the significant drivers or alter the system to include them.

Recommendations for the implementation of activity-based costing (ABC) model for

Blackmore Limited

Based on the research findings, without any reasonable doubt, from my perspective I

would to categorically state the following two recommendations for the company: first of all, the

managers or the management division of this company should entirely improve the

differentiation of all their products to enable the company a competitive advantage in both the

domestic and international market segments. Secondly, the company should greatly focus on

improving the perceived quality of their products while holding their prices at the very level to

attract a wider customer base (Ward 2012).

Another recommended mode

every individual activity to better define the required or relevant activity rates for the overall

calculation and accounting of the product cost.

The undertakings of Blackmore's company like a strategic move to establish the premium

prices for their products, or otherwise enhance the quality of their products and services while

maintaining the very market prices for competitive advantage, reflect all the dimensions of

strategic cost management, ranging from market mapping to establishing the ideal products and

prices. Also in this context, there is an explicit explanation on how activity-based costing or cost

management was used to achieve the company’s objectives for the previous years, where

sustainable growth had been recorded (Wegmann 2008). Perhaps sometimes through striving to

implement this system, for instance, tracking down activity costs and processes to products and

market the cost drivers are not properly measured in spite the fact that they drive critical

organizational costs. The managers should be well acquainted with the following two alternative

options: disregard all the significant drivers or alter the system to include them.

Recommendations for the implementation of activity-based costing (ABC) model for

Blackmore Limited

Based on the research findings, without any reasonable doubt, from my perspective I

would to categorically state the following two recommendations for the company: first of all, the

managers or the management division of this company should entirely improve the

differentiation of all their products to enable the company a competitive advantage in both the

domestic and international market segments. Secondly, the company should greatly focus on

improving the perceived quality of their products while holding their prices at the very level to

attract a wider customer base (Ward 2012).

Another recommended mode

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-Based Costing for Blackmore LTD 10

Financial Planning

Now, a part from the activity-based (ABC) as a model of management account, I would

like to particularly suggest ‘Financial Planning’ as yet another very important model used in

management account. Financial planning in management account is based on budgeting and

budget processes. As matter of fact, the main aim or the ultimate goal for any business entity is

the maximization of profits but to minimize on cost. Therefore, for managers to detect

tremendous increase in the profit margin, they have to make, and comply with the proper and

sound financial planning. Financial planning therefore must be one of the most fundamental

management tools for realizing the business objectives. It involves activities like: evaluating the

business environment, ascertaining the vision and the obligations of the business, identification

of the relevant resource needed to execute the business objectives, budget for every single

activity within the business, calculate the total cost, identify the risks associated with the cost

products then allocate the required capital for each activity. This is essentially what financial

planning entails in management accounting.

Conclusion

In conclusion, activity-based costing (ABC) has proved to be the best cost management

tool for various companies and more particularly for Blackmore Limited. Through this cost

management to the company has achieved the very sustainable growth, wide profit margins and

the positive reputation for its macro environment. The company has established a wide market

base for their natural herbs, vitamins and supplements brands both within the domestic segment

and the global one including a market segment in the Asian continent. Through this system, the

management division of the company has adopted the best corporate strategies and develops

realistic objectives which as ultimately given them the competitive advantage over other

Financial Planning

Now, a part from the activity-based (ABC) as a model of management account, I would

like to particularly suggest ‘Financial Planning’ as yet another very important model used in

management account. Financial planning in management account is based on budgeting and

budget processes. As matter of fact, the main aim or the ultimate goal for any business entity is

the maximization of profits but to minimize on cost. Therefore, for managers to detect

tremendous increase in the profit margin, they have to make, and comply with the proper and

sound financial planning. Financial planning therefore must be one of the most fundamental

management tools for realizing the business objectives. It involves activities like: evaluating the

business environment, ascertaining the vision and the obligations of the business, identification

of the relevant resource needed to execute the business objectives, budget for every single

activity within the business, calculate the total cost, identify the risks associated with the cost

products then allocate the required capital for each activity. This is essentially what financial

planning entails in management accounting.

Conclusion

In conclusion, activity-based costing (ABC) has proved to be the best cost management

tool for various companies and more particularly for Blackmore Limited. Through this cost

management to the company has achieved the very sustainable growth, wide profit margins and

the positive reputation for its macro environment. The company has established a wide market

base for their natural herbs, vitamins and supplements brands both within the domestic segment

and the global one including a market segment in the Asian continent. Through this system, the

management division of the company has adopted the best corporate strategies and develops

realistic objectives which as ultimately given them the competitive advantage over other

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-Based Costing for Blackmore LTD 11

companies. It is through activity-based costing that the company has attracted more holders and

increased their rewards, also improved the perceived quality of their products giving them the

best reputation internally and externally. From this research, therefore, various conclusions can

be made to give rise to the future research undertakings. Otherwise, in general, cost theory, the

accounting costs, and the model concepts present a very important role in what concerns the

appropriate establishment of company goals and strategies. Thumbs up for the technological

advancement that has given various companies new costing approaches particular activity-based

costing (ABC).

companies. It is through activity-based costing that the company has attracted more holders and

increased their rewards, also improved the perceived quality of their products giving them the

best reputation internally and externally. From this research, therefore, various conclusions can

be made to give rise to the future research undertakings. Otherwise, in general, cost theory, the

accounting costs, and the model concepts present a very important role in what concerns the

appropriate establishment of company goals and strategies. Thumbs up for the technological

advancement that has given various companies new costing approaches particular activity-based

costing (ABC).

Activity-Based Costing for Blackmore LTD 12

References

Askarany, D., Yazdifar, H. and Askary, S., 2010. Supply chain management, activity-based

costing, and organizational factors. International journal of production economics, 127(2),

pp.238-248.

Baird, K., Harrison, G. and Reeve, R., 2007. The success of activity management practices: the

influence of organizational and cultural factors. Accounting & Finance, 47(1), pp.47-67.

Barney, J.B., 2014. Gaining and sustaining competitive advantage. Pearson higher ed.

Baykasoğlu, A. and Kaplanoğlu, V., 2008. Application of activity-based costing to a land

transportation company: A case study. International Journal of Production Economics, 116(2),

pp.308-324.

Briers, M, and Chua, W.F., 2009. The role of actor-networks and boundary objects in

management accounting change: a field study of an implementation of activity-based costing.

Accounting, organizations and society, 26(3), pp.237-269.

Cadez, S. and Guilding, C., 2008. An exploratory investigation of an integrated contingency

model of strategic management accounting. Accounting, organizations and society, 33(7-8),

pp.836-863.

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education India.

References

Askarany, D., Yazdifar, H. and Askary, S., 2010. Supply chain management, activity-based

costing, and organizational factors. International journal of production economics, 127(2),

pp.238-248.

Baird, K., Harrison, G. and Reeve, R., 2007. The success of activity management practices: the

influence of organizational and cultural factors. Accounting & Finance, 47(1), pp.47-67.

Barney, J.B., 2014. Gaining and sustaining competitive advantage. Pearson higher ed.

Baykasoğlu, A. and Kaplanoğlu, V., 2008. Application of activity-based costing to a land

transportation company: A case study. International Journal of Production Economics, 116(2),

pp.308-324.

Briers, M, and Chua, W.F., 2009. The role of actor-networks and boundary objects in

management accounting change: a field study of an implementation of activity-based costing.

Accounting, organizations and society, 26(3), pp.237-269.

Cadez, S. and Guilding, C., 2008. An exploratory investigation of an integrated contingency

model of strategic management accounting. Accounting, organizations and society, 33(7-8),

pp.836-863.

Horngren, C.T., 2009. Cost accounting: A managerial emphasis, 13/e. Pearson Education India.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.