Should ABC Department Store Drop the Clothing Line? Business Analysis

VerifiedAdded on 2023/04/20

|6

|592

|75

Presentation

AI Summary

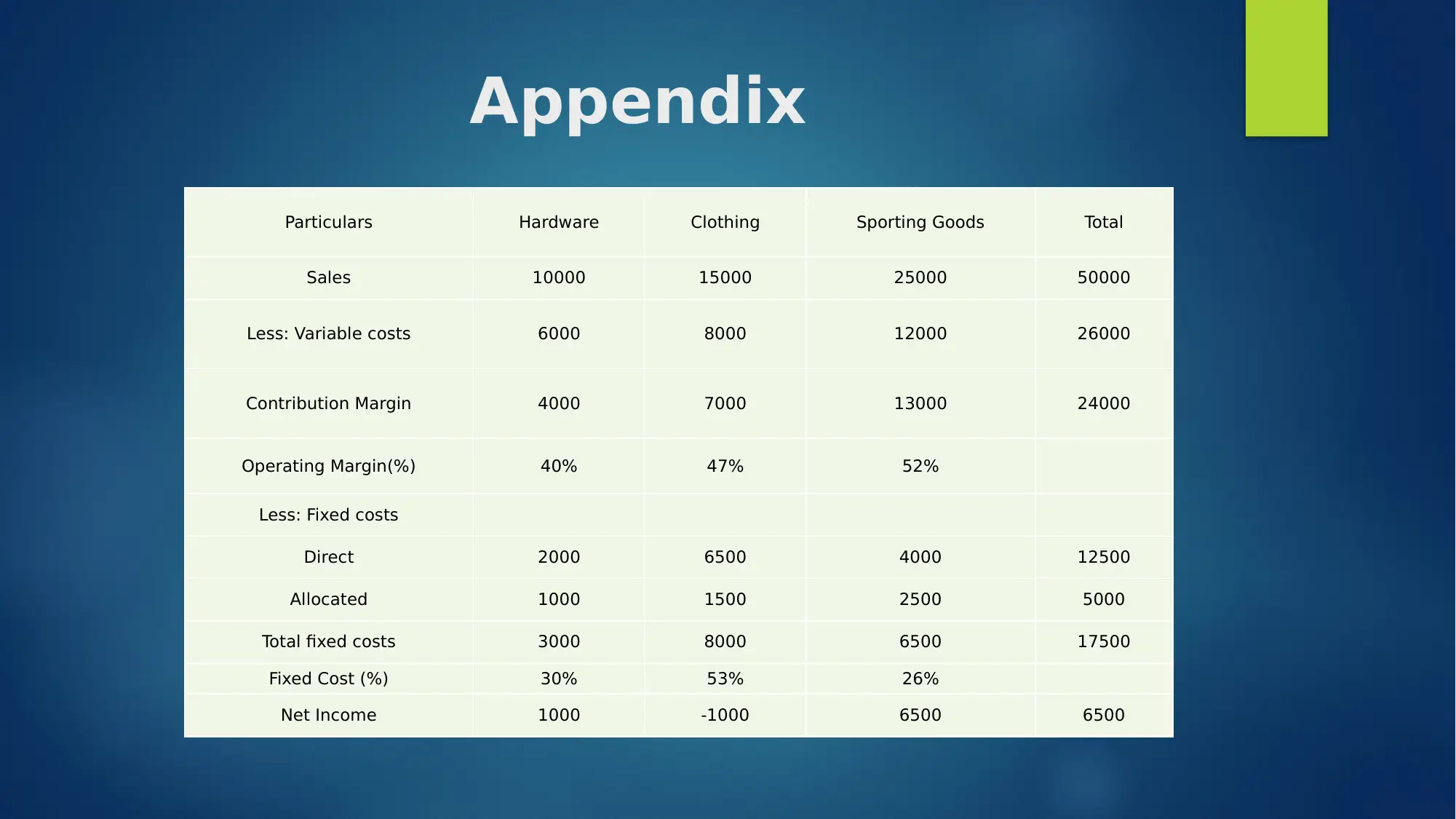

This presentation analyzes the profitability of the clothing line within the ABC department store, focusing on whether the line should be discontinued. The analysis begins by highlighting the importance of operating margins and the relationship between revenue, fixed costs, and variable costs in determining a business's profitability. The clothing business has a 47% operating margin, better than the hardware business, but it's experiencing negative cash flow due to high fixed costs. The analysis recommends increasing the revenue base for the clothing business to better utilize fixed costs, increase the operating margin, and stabilize the company's net profitability. Supporting data, including sales, variable costs, contribution margins, fixed costs, and net income, are presented to justify the recommendation. References in APA format are provided to support the analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.