Analysis of ABC Company Limited's Financial Performance and Budgeting

VerifiedAdded on 2023/04/08

|9

|1618

|500

Report

AI Summary

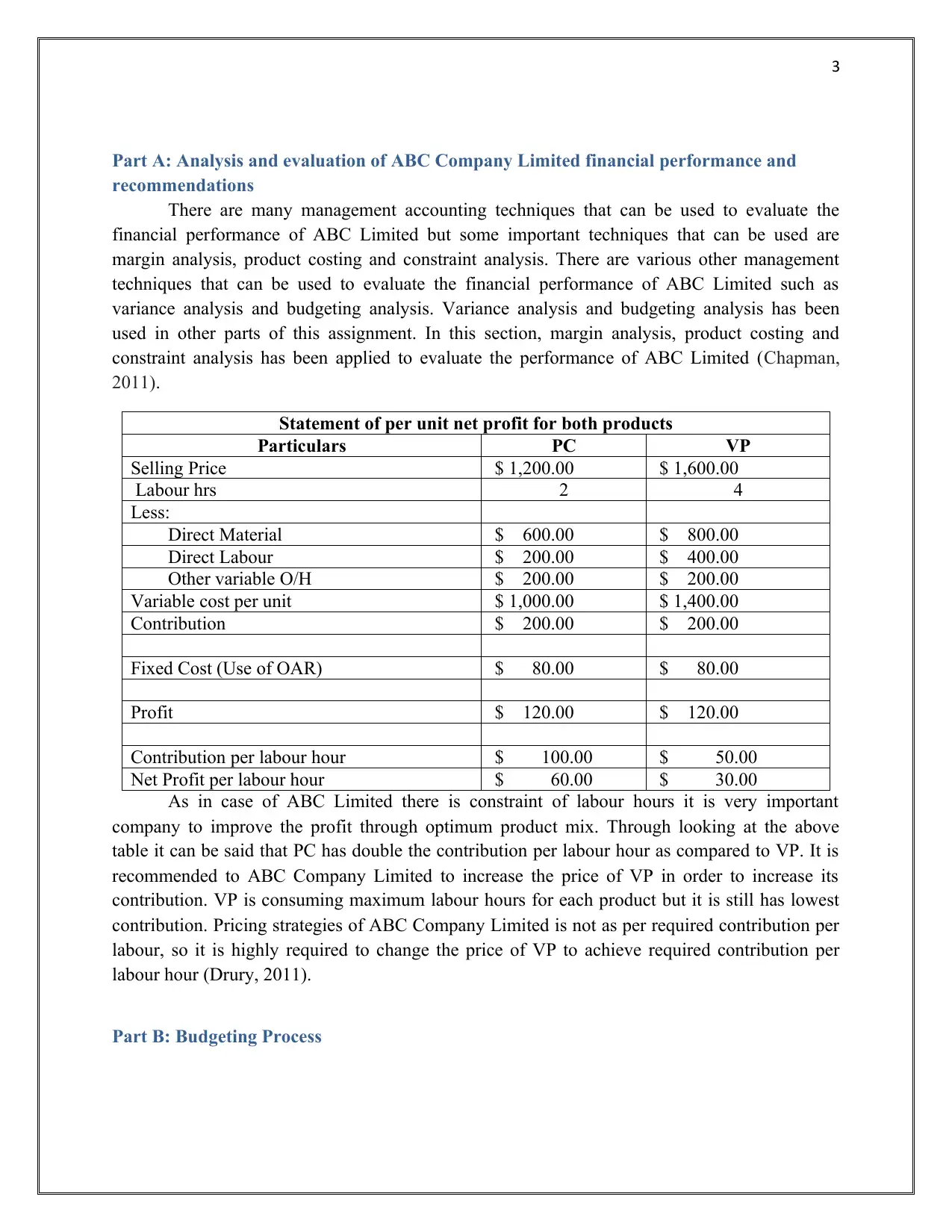

This management accounting report analyzes the financial performance of ABC Company Limited, focusing on margin analysis, product costing, and constraint analysis to evaluate profitability. The report delves into the budgeting process, outlining its major functions and the advantages and disadvantages of budgetary control systems. It includes a detailed budgetary planning section with sales, cash collection, production, and raw material purchase budgets. Furthermore, the report applies budgetary control techniques, calculating raw material variances, including price and usage variances, and provides a cost reconciliation statement. Finally, the report offers recommendations to management based on the findings of the analysis, particularly concerning raw material procurement and cost control. The report is well-structured, using relevant formulas and providing detailed calculations and recommendations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.