Detailed Report: Implementing ABC Costing in Management Accounting

VerifiedAdded on 2023/06/06

|11

|2774

|122

Report

AI Summary

This report provides a comprehensive analysis of activity-based costing (ABC) within management accounting, contrasting it with traditional costing methods using Essendon Electronics as a case study. It examines the impact of ABC on the profitability of the Regal and Monarch divisions, detailing how ABC improves cost allocation through cost pools and drivers, leading to more accurate product costing and better decision-making. The report addresses concerns raised by Mr. Lockett, highlighting how ABC can enhance operational efficiency and transparency. Furthermore, it discusses the benefits of ABC, such as accurate product costing, improved cost behavior analysis, and better alignment with customer demand and pricing strategies. While acknowledging the advantages, the report also outlines the demerits of ABC, including its non-conformity with GAAP, complexity, challenges for small firms, high implementation costs, and potential for misinterpretation of data. The document concludes that while ABC offers significant improvements in cost management, its implementation requires careful consideration of its limitations and suitability for the specific organizational context. Desklib provides this and other solved assignments to aid students in their studies.

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING 0

Mana ement Acco nting u g

Mana ement Acco nting u g

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

Table of Contents

Change in numbers.....................................................................................................................2

Response to Mr Lockett.............................................................................................................3

Benefits of ABC.........................................................................................................................4

Accurate Product Costing.......................................................................................................4

Cost Behaviour.......................................................................................................................5

Tracing of the activities..........................................................................................................5

Segregation of activities.........................................................................................................5

Demand of the Customer........................................................................................................6

Pricing options........................................................................................................................6

Demerits.....................................................................................................................................6

No conformity with GAAP:...................................................................................................6

Complexity of the system:......................................................................................................7

Difficulties for small firms:....................................................................................................7

Consumes high cost and time:................................................................................................7

Not relevant for firms manufacturing only one product:........................................................8

Risk of misinterpretation of data:...........................................................................................8

References..................................................................................................................................9

Table of Contents

Change in numbers.....................................................................................................................2

Response to Mr Lockett.............................................................................................................3

Benefits of ABC.........................................................................................................................4

Accurate Product Costing.......................................................................................................4

Cost Behaviour.......................................................................................................................5

Tracing of the activities..........................................................................................................5

Segregation of activities.........................................................................................................5

Demand of the Customer........................................................................................................6

Pricing options........................................................................................................................6

Demerits.....................................................................................................................................6

No conformity with GAAP:...................................................................................................6

Complexity of the system:......................................................................................................7

Difficulties for small firms:....................................................................................................7

Consumes high cost and time:................................................................................................7

Not relevant for firms manufacturing only one product:........................................................8

Risk of misinterpretation of data:...........................................................................................8

References..................................................................................................................................9

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

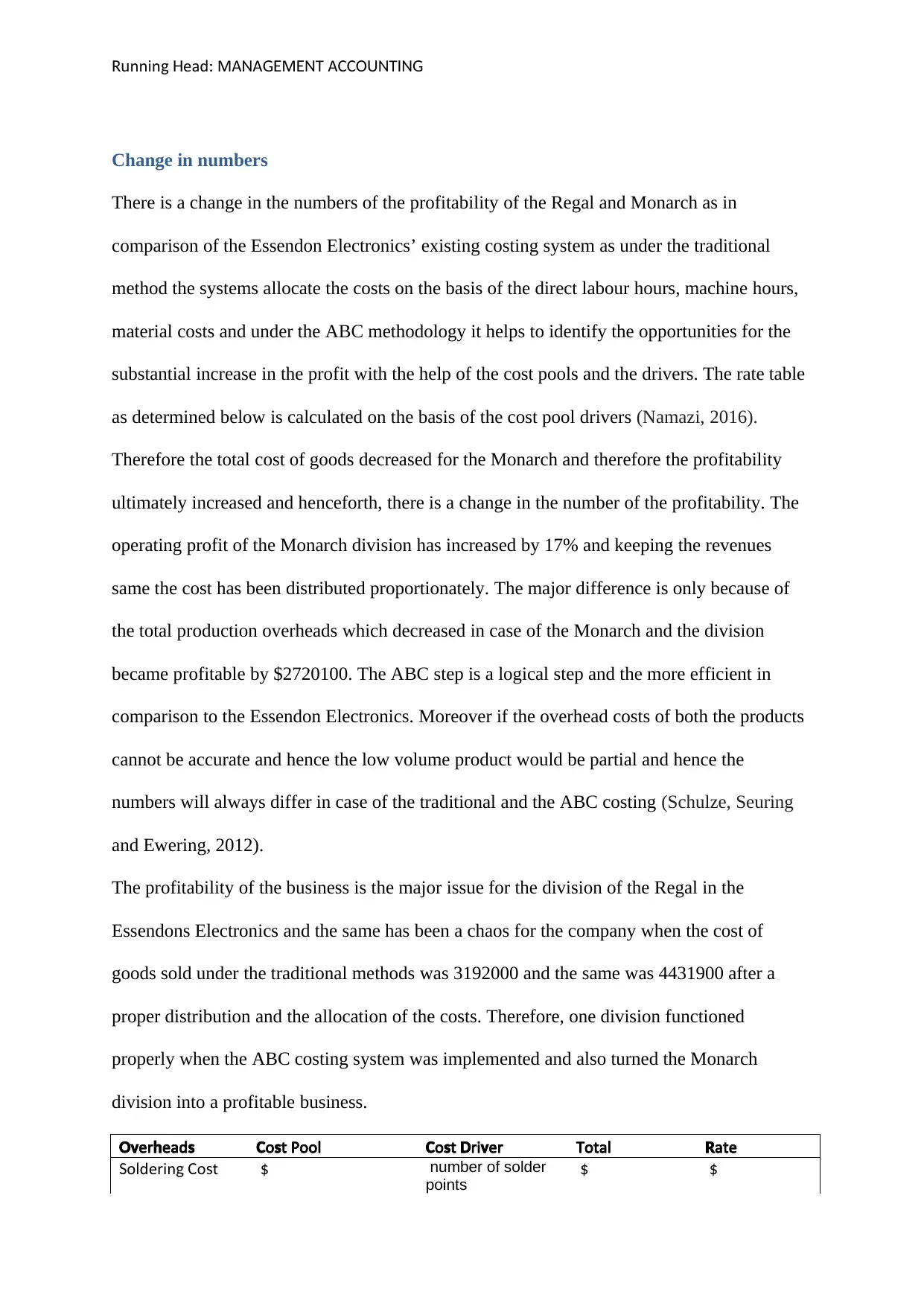

Change in numbers

There is a change in the numbers of the profitability of the Regal and Monarch as in

comparison of the Essendon Electronics’ existing costing system as under the traditional

method the systems allocate the costs on the basis of the direct labour hours, machine hours,

material costs and under the ABC methodology it helps to identify the opportunities for the

substantial increase in the profit with the help of the cost pools and the drivers. The rate table

as determined below is calculated on the basis of the cost pool drivers (Namazi, 2016).

Therefore the total cost of goods decreased for the Monarch and therefore the profitability

ultimately increased and henceforth, there is a change in the number of the profitability. The

operating profit of the Monarch division has increased by 17% and keeping the revenues

same the cost has been distributed proportionately. The major difference is only because of

the total production overheads which decreased in case of the Monarch and the division

became profitable by $2720100. The ABC step is a logical step and the more efficient in

comparison to the Essendon Electronics. Moreover if the overhead costs of both the products

cannot be accurate and hence the low volume product would be partial and hence the

numbers will always differ in case of the traditional and the ABC costing (Schulze, Seuring

and Ewering, 2012).

The profitability of the business is the major issue for the division of the Regal in the

Essendons Electronics and the same has been a chaos for the company when the cost of

goods sold under the traditional methods was 3192000 and the same was 4431900 after a

proper distribution and the allocation of the costs. Therefore, one division functioned

properly when the ABC costing system was implemented and also turned the Monarch

division into a profitable business.

er eadOv h s o t PoolC s o t ri erC s D v Total ateR

olderin o tS g C s $ number of solder

points

$ $

Change in numbers

There is a change in the numbers of the profitability of the Regal and Monarch as in

comparison of the Essendon Electronics’ existing costing system as under the traditional

method the systems allocate the costs on the basis of the direct labour hours, machine hours,

material costs and under the ABC methodology it helps to identify the opportunities for the

substantial increase in the profit with the help of the cost pools and the drivers. The rate table

as determined below is calculated on the basis of the cost pool drivers (Namazi, 2016).

Therefore the total cost of goods decreased for the Monarch and therefore the profitability

ultimately increased and henceforth, there is a change in the number of the profitability. The

operating profit of the Monarch division has increased by 17% and keeping the revenues

same the cost has been distributed proportionately. The major difference is only because of

the total production overheads which decreased in case of the Monarch and the division

became profitable by $2720100. The ABC step is a logical step and the more efficient in

comparison to the Essendon Electronics. Moreover if the overhead costs of both the products

cannot be accurate and hence the low volume product would be partial and hence the

numbers will always differ in case of the traditional and the ABC costing (Schulze, Seuring

and Ewering, 2012).

The profitability of the business is the major issue for the division of the Regal in the

Essendons Electronics and the same has been a chaos for the company when the cost of

goods sold under the traditional methods was 3192000 and the same was 4431900 after a

proper distribution and the allocation of the costs. Therefore, one division functioned

properly when the ABC costing system was implemented and also turned the Monarch

division into a profitable business.

er eadOv h s o t PoolC s o t ri erC s D v Total ateR

olderin o tS g C s $ number of solder

points

$ $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

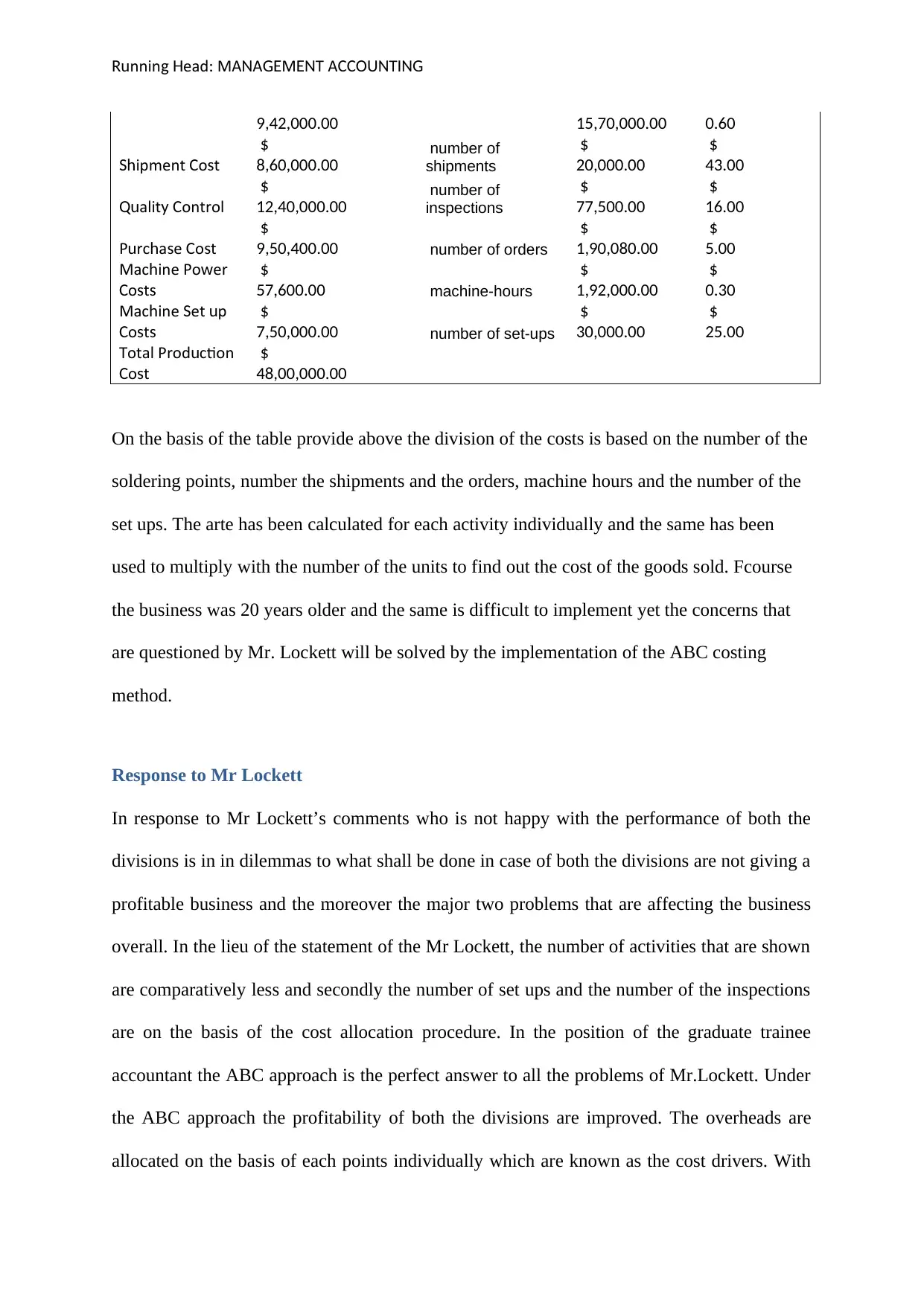

9,42,000.00 15,70,000.00 0.60

ipment o tSh C s

$

8,60,000.00 number of

shipments

$

20,000.00

$

43.00

alit ontrolQu y C

$

12,40,000.00 number of

inspections

$

77,500.00

$

16.00

P rc a e o tu h s C s

$

9,50,400.00 number of orders

$

1,90,080.00

$

5.00

Mac ine Po erh w

o tC s s

$

57,600.00 machine-hours

$

1,92,000.00

$

0.30

Mac ine et ph S u

o tC s s

$

7,50,000.00 number of set-ups

$

30,000.00

$

25.00

Total Prod ctionu

o tC s

$

48,00,000.00

On the basis of the table provide above the division of the costs is based on the number of the

soldering points, number the shipments and the orders, machine hours and the number of the

set ups. The arte has been calculated for each activity individually and the same has been

used to multiply with the number of the units to find out the cost of the goods sold. Fcourse

the business was 20 years older and the same is difficult to implement yet the concerns that

are questioned by Mr. Lockett will be solved by the implementation of the ABC costing

method.

Response to Mr Lockett

In response to Mr Lockett’s comments who is not happy with the performance of both the

divisions is in in dilemmas to what shall be done in case of both the divisions are not giving a

profitable business and the moreover the major two problems that are affecting the business

overall. In the lieu of the statement of the Mr Lockett, the number of activities that are shown

are comparatively less and secondly the number of set ups and the number of the inspections

are on the basis of the cost allocation procedure. In the position of the graduate trainee

accountant the ABC approach is the perfect answer to all the problems of Mr.Lockett. Under

the ABC approach the profitability of both the divisions are improved. The overheads are

allocated on the basis of each points individually which are known as the cost drivers. With

9,42,000.00 15,70,000.00 0.60

ipment o tSh C s

$

8,60,000.00 number of

shipments

$

20,000.00

$

43.00

alit ontrolQu y C

$

12,40,000.00 number of

inspections

$

77,500.00

$

16.00

P rc a e o tu h s C s

$

9,50,400.00 number of orders

$

1,90,080.00

$

5.00

Mac ine Po erh w

o tC s s

$

57,600.00 machine-hours

$

1,92,000.00

$

0.30

Mac ine et ph S u

o tC s s

$

7,50,000.00 number of set-ups

$

30,000.00

$

25.00

Total Prod ctionu

o tC s

$

48,00,000.00

On the basis of the table provide above the division of the costs is based on the number of the

soldering points, number the shipments and the orders, machine hours and the number of the

set ups. The arte has been calculated for each activity individually and the same has been

used to multiply with the number of the units to find out the cost of the goods sold. Fcourse

the business was 20 years older and the same is difficult to implement yet the concerns that

are questioned by Mr. Lockett will be solved by the implementation of the ABC costing

method.

Response to Mr Lockett

In response to Mr Lockett’s comments who is not happy with the performance of both the

divisions is in in dilemmas to what shall be done in case of both the divisions are not giving a

profitable business and the moreover the major two problems that are affecting the business

overall. In the lieu of the statement of the Mr Lockett, the number of activities that are shown

are comparatively less and secondly the number of set ups and the number of the inspections

are on the basis of the cost allocation procedure. In the position of the graduate trainee

accountant the ABC approach is the perfect answer to all the problems of Mr.Lockett. Under

the ABC approach the profitability of both the divisions are improved. The overheads are

allocated on the basis of each points individually which are known as the cost drivers. With

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

the help of the ABC approach, the cost pool driver is used to calculate the production cost.

Moreover the individual rates have been specified on the basis of each cost pool. The units

produced are also utilised to calculate the total production overheads of Monarch and Regal.

Under the traditional system of the Essendon Electronics the cost of goods are allocated

cumulatively whereas in the process of the Essendon Electronics the costs are pooled and

segregated on the basis of the cost drivers which help the department to assess the individual

costs of each department (Zimmerman and Yahya-Zadeh, 2011).

The operating profit under the traditional system of the Monarch is $7260000 and that of the

Regal is $1368000, but after the implementation of the ABC models the profit of the gross

profit of Monarch came to $8499900 which has been increased by 17% in comparison to the

previous approach and moreover the Regal which was profitable but not up to the mark

because of the fact that the cost of the goods sold increased from $3192000 to $4431900.

However the operating income per unit also increased from $65 to $121.36 in case of the

Monarch after adopting the ABC system of costing (Esmalifalak, Albin & Behzadpoor,

2015).

Benefits of ABC

Obviously the traditional system of the costing is slow and therefore the ABC costing system

is developed and the major benefits in relation to the activity based costing and henceforth

they are outlined below.

Accurate Product Costing

With the help of the ABC costing the accurate product cost can be formed and this can

happen due to stability in the cost and effect relationship within the cost occurrence. The

major difference found in the activity based costing and the traditional costing is the activities

the help of the ABC approach, the cost pool driver is used to calculate the production cost.

Moreover the individual rates have been specified on the basis of each cost pool. The units

produced are also utilised to calculate the total production overheads of Monarch and Regal.

Under the traditional system of the Essendon Electronics the cost of goods are allocated

cumulatively whereas in the process of the Essendon Electronics the costs are pooled and

segregated on the basis of the cost drivers which help the department to assess the individual

costs of each department (Zimmerman and Yahya-Zadeh, 2011).

The operating profit under the traditional system of the Monarch is $7260000 and that of the

Regal is $1368000, but after the implementation of the ABC models the profit of the gross

profit of Monarch came to $8499900 which has been increased by 17% in comparison to the

previous approach and moreover the Regal which was profitable but not up to the mark

because of the fact that the cost of the goods sold increased from $3192000 to $4431900.

However the operating income per unit also increased from $65 to $121.36 in case of the

Monarch after adopting the ABC system of costing (Esmalifalak, Albin & Behzadpoor,

2015).

Benefits of ABC

Obviously the traditional system of the costing is slow and therefore the ABC costing system

is developed and the major benefits in relation to the activity based costing and henceforth

they are outlined below.

Accurate Product Costing

With the help of the ABC costing the accurate product cost can be formed and this can

happen due to stability in the cost and effect relationship within the cost occurrence. The

major difference found in the activity based costing and the traditional costing is the activities

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

consume the costs and the products consume the activities. In the large environment of the

costs the ABC approach provides the more realistic approach (Durán & Durán, 2018).

Cost Behaviour

ABC basically helps to identify the real nature of the cost by segregating the activities and

classifying the activities in potential and the non-potential activities. The activities which do

not add value are not reliable for the organisation and therefore wasting the costs on them

would be inappropriate. With ABC, managers are able to control many fixed overhead costs

as well as the variable costs. With the assistance of the ABC approach the fixed costs are

separately shown and they become more transparent clear and visible (Namazi, 2016).

Tracing of the activities

ABC uses multiple ranges of the drivers and many of them are based on the transactions

rather than the production volume. Furthermore, ABC is concerned with all the activities

within and beyond the factory to trace more overheads to the different products (Molis,

2018). The trace of the activities are the primary in nature and the ABC costing helps to make

the approach easy for the organisation and henceforth, this saves time, costa and energy of

the company.

Segregation of activities

The activities are segregated in different manner when using the ABC costing and therefore it

not only helps to enhance the production of the organisation but also accounts for right

activity with right cost pool driver. This procedure helps the company to bifurcate the costs

for the individual activities and this shows the transparency of the costs between the activities

and the same reflection is not visible under the traditional method of the costing (Hada,

Chakravarty & Mukherjee, 2014). Moreover the segregation of the activities is easy to handle

consume the costs and the products consume the activities. In the large environment of the

costs the ABC approach provides the more realistic approach (Durán & Durán, 2018).

Cost Behaviour

ABC basically helps to identify the real nature of the cost by segregating the activities and

classifying the activities in potential and the non-potential activities. The activities which do

not add value are not reliable for the organisation and therefore wasting the costs on them

would be inappropriate. With ABC, managers are able to control many fixed overhead costs

as well as the variable costs. With the assistance of the ABC approach the fixed costs are

separately shown and they become more transparent clear and visible (Namazi, 2016).

Tracing of the activities

ABC uses multiple ranges of the drivers and many of them are based on the transactions

rather than the production volume. Furthermore, ABC is concerned with all the activities

within and beyond the factory to trace more overheads to the different products (Molis,

2018). The trace of the activities are the primary in nature and the ABC costing helps to make

the approach easy for the organisation and henceforth, this saves time, costa and energy of

the company.

Segregation of activities

The activities are segregated in different manner when using the ABC costing and therefore it

not only helps to enhance the production of the organisation but also accounts for right

activity with right cost pool driver. This procedure helps the company to bifurcate the costs

for the individual activities and this shows the transparency of the costs between the activities

and the same reflection is not visible under the traditional method of the costing (Hada,

Chakravarty & Mukherjee, 2014). Moreover the segregation of the activities is easy to handle

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

for the organisation. The managers can invest their time for the particular activities and the

same activities will not be under one umbrella.

Demand of the Customer

Customer demand also plays an important role in the management of life. With the idea of

ABC investigation, stock organizers can estimate the interest for items in advance and deal

with the stock levels as needs be. The development and decay period is diverse for various

items, with diminish sought after the deals will fall and in this manner it is astute to lessen the

stock levels to limit the conveying costs on the things and furthermore abstain from having

out of date stock external reports (Hada, Chakravarty & Mukherjee, 2014).

Pricing options

In light of that information, the organization can build the cost of these things by a couple of

additional dollars which will have a tremendous effect on the benefit. Another vital

estimating choice to consider is to unite providers or consider exchanging business to a

solitary provider. Buying more merchandise from a solitary provider will decrease conveying

expenses and many-sided quality expenses related with them (Molis, 2018).

Demerits

From the above discussion, it has been observed that activity based costing is management

accounting technique which provides numerous benefits to the entity. But, it suffers from

certain limitations which are discussed below:

No conformity with GAAP:

Reports that are generated under the system of activity based costing do not conform to the

generally accepted accounting principles. As a result of this, the organisation that implements

the said system of costing has to actually work on two costing systems – one for its internal

for the organisation. The managers can invest their time for the particular activities and the

same activities will not be under one umbrella.

Demand of the Customer

Customer demand also plays an important role in the management of life. With the idea of

ABC investigation, stock organizers can estimate the interest for items in advance and deal

with the stock levels as needs be. The development and decay period is diverse for various

items, with diminish sought after the deals will fall and in this manner it is astute to lessen the

stock levels to limit the conveying costs on the things and furthermore abstain from having

out of date stock external reports (Hada, Chakravarty & Mukherjee, 2014).

Pricing options

In light of that information, the organization can build the cost of these things by a couple of

additional dollars which will have a tremendous effect on the benefit. Another vital

estimating choice to consider is to unite providers or consider exchanging business to a

solitary provider. Buying more merchandise from a solitary provider will decrease conveying

expenses and many-sided quality expenses related with them (Molis, 2018).

Demerits

From the above discussion, it has been observed that activity based costing is management

accounting technique which provides numerous benefits to the entity. But, it suffers from

certain limitations which are discussed below:

No conformity with GAAP:

Reports that are generated under the system of activity based costing do not conform to the

generally accepted accounting principles. As a result of this, the organisation that implements

the said system of costing has to actually work on two costing systems – one for its internal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

use and the other one for the purpose of preparing the external reports (Mahal & Hossain,

2015).

Complexity of the system:

The overhead allocation under activity based costing system is undertaken taking into

account various cost pools and their cost drivers. Whereas, in traditional costing system,

overheads are allocated only on the basis of single pre-determined overhead recovery rate.

Therefore, cost allocation under ABC system is quite complex in nature than the conventional

costing system. Moreover, the selection of appropriate cost driver also involves requisite

amount of knowledge by the person dealing with the system (Jiménez, Duarte & Afonso,

2015).

Difficulties for small firms:

The significance of activity based costing also varies with the nature and size of the entity

that implements this system. For instance, it is more effective technique for the

manufacturing concern than the trading concern. Also, it is suitable of large sized

corporations than the small sized corporations. The implementation of this system requires

substantial resources such which are not available with all the entities. In small organisations,

the cost of adoption of activity based costing exceeds the benefits of such technique (Hada,

Chakravarty & Mukherjee, 2014).

Consumes high cost and time:

Adoption of activity based costing requires the company to hire skilled and knowledgeable

personnel who can perform the costing function using this advanced technique of

management accounting. Further, it is not practical to adopt ABC system in one or two days

because it requires proper provision of training to the existing staff of the company so as to

enable to work on this system in the smooth and efficient manner. Also, the collection of data

useful under ABC costing consumes more time. Both hiring of new as well as training of the

use and the other one for the purpose of preparing the external reports (Mahal & Hossain,

2015).

Complexity of the system:

The overhead allocation under activity based costing system is undertaken taking into

account various cost pools and their cost drivers. Whereas, in traditional costing system,

overheads are allocated only on the basis of single pre-determined overhead recovery rate.

Therefore, cost allocation under ABC system is quite complex in nature than the conventional

costing system. Moreover, the selection of appropriate cost driver also involves requisite

amount of knowledge by the person dealing with the system (Jiménez, Duarte & Afonso,

2015).

Difficulties for small firms:

The significance of activity based costing also varies with the nature and size of the entity

that implements this system. For instance, it is more effective technique for the

manufacturing concern than the trading concern. Also, it is suitable of large sized

corporations than the small sized corporations. The implementation of this system requires

substantial resources such which are not available with all the entities. In small organisations,

the cost of adoption of activity based costing exceeds the benefits of such technique (Hada,

Chakravarty & Mukherjee, 2014).

Consumes high cost and time:

Adoption of activity based costing requires the company to hire skilled and knowledgeable

personnel who can perform the costing function using this advanced technique of

management accounting. Further, it is not practical to adopt ABC system in one or two days

because it requires proper provision of training to the existing staff of the company so as to

enable to work on this system in the smooth and efficient manner. Also, the collection of data

useful under ABC costing consumes more time. Both hiring of new as well as training of the

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

existing involves considerable cost. Furthermore, the maintenance of ABC system after its

successful implementation is also a costly process (Angelopoulos & Pollalis, 2017).

Moreover reports that are produced under the arrangement of movement based costing don't

adjust to the sound accounting guidelines. Therefore, the association that executes the said

arrangement of costing needs to really take a shot at two costing frameworks – one for its

inward utilize and the other one to prepare the outside reports

Not relevant for firms manufacturing only one product:

Activity based costing method is relevant for the firms which are involved in the production

multiple products and not the single product because of its very nature.

Risk of misinterpretation of data:

The data used under activity based costing can easily be misinterpreted due to its complexity

and hence it requires to be handled with due care while using it to make sound decisions.

The major cost in relation to the implementation of system of activity based costing involves

following:

The hiring of new employees who are specialised in the use of ABC technique and

training the existing employees to work on the new system and;

The investment of considerable amount economic resources for the implementation of

ABC system is also required for the adoption of ABC.

existing involves considerable cost. Furthermore, the maintenance of ABC system after its

successful implementation is also a costly process (Angelopoulos & Pollalis, 2017).

Moreover reports that are produced under the arrangement of movement based costing don't

adjust to the sound accounting guidelines. Therefore, the association that executes the said

arrangement of costing needs to really take a shot at two costing frameworks – one for its

inward utilize and the other one to prepare the outside reports

Not relevant for firms manufacturing only one product:

Activity based costing method is relevant for the firms which are involved in the production

multiple products and not the single product because of its very nature.

Risk of misinterpretation of data:

The data used under activity based costing can easily be misinterpreted due to its complexity

and hence it requires to be handled with due care while using it to make sound decisions.

The major cost in relation to the implementation of system of activity based costing involves

following:

The hiring of new employees who are specialised in the use of ABC technique and

training the existing employees to work on the new system and;

The investment of considerable amount economic resources for the implementation of

ABC system is also required for the adoption of ABC.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

References

Christian, D. (2018). Building Cost Management: Case Study Using Costing Methods. New

York: Springer

Hada, M. S., Chakravarty, A., & Mukherjee, P. (2014). Activity based costing of diagnostic

procedures at a nuclear medicine center of a tertiary care hospital. Indian journal of

nuclear medicine: IJNM: the official journal of the Society of Nuclear Medicine,

India, 29(4), 241.

Horngren, C.T., Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T.

(2012). Management and cost accounting. 13(2), 25-28.

Jiménez, V., Duarte, C., & Afonso, P. (2015). Cost System Under Uncertainty: A Case Study

in the Imaging Area of a Hospital. In Enhancing Synergies in a Collaborative

Environment (pp. 325-333). Ney York: Springer

Mahal, I., & Hossain, A. (2015). Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting, 6(4), 66-74.

Molis, J., (2018) Advantages & Disadvantages of Traditional Costing. Retrieved from:

https://bizfluent.com/info-8645304-advantages-disadvantages-traditional-costing.html

Schulze, M., Seuring, S. and Ewering, C. (2012). Applying activity-based costing in a supply

chain environment. International Journal of Production Economics, 135(2), 716-725.

Schulze, M., Seuring, S. and Ewering, C. (2012). Applying activity-based costing in a supply

chain environment. International Journal of Production Economics, 135(2), 716-725.

Zimmerman, J.L. and Yahya-Zadeh, M. (2011). Accounting for decision making and

control. Issues in Accounting Education, 26(1), 258-259.

References

Christian, D. (2018). Building Cost Management: Case Study Using Costing Methods. New

York: Springer

Hada, M. S., Chakravarty, A., & Mukherjee, P. (2014). Activity based costing of diagnostic

procedures at a nuclear medicine center of a tertiary care hospital. Indian journal of

nuclear medicine: IJNM: the official journal of the Society of Nuclear Medicine,

India, 29(4), 241.

Horngren, C.T., Bhimani, A., Datar, S.M., Foster, G. and Horngren, C.T.

(2012). Management and cost accounting. 13(2), 25-28.

Jiménez, V., Duarte, C., & Afonso, P. (2015). Cost System Under Uncertainty: A Case Study

in the Imaging Area of a Hospital. In Enhancing Synergies in a Collaborative

Environment (pp. 325-333). Ney York: Springer

Mahal, I., & Hossain, A. (2015). Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting, 6(4), 66-74.

Molis, J., (2018) Advantages & Disadvantages of Traditional Costing. Retrieved from:

https://bizfluent.com/info-8645304-advantages-disadvantages-traditional-costing.html

Schulze, M., Seuring, S. and Ewering, C. (2012). Applying activity-based costing in a supply

chain environment. International Journal of Production Economics, 135(2), 716-725.

Schulze, M., Seuring, S. and Ewering, C. (2012). Applying activity-based costing in a supply

chain environment. International Journal of Production Economics, 135(2), 716-725.

Zimmerman, J.L. and Yahya-Zadeh, M. (2011). Accounting for decision making and

control. Issues in Accounting Education, 26(1), 258-259.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

nnin ead MA A M T A TRu g H : N GE EN CCOUN ING

Esmalifalak, H., Albin, M. S., & Behzadpoor, M. (2015). A comparative study on the activity

based costing systems: Traditional, fuzzy and Monte Carlo approaches. Health Policy

and Technology, 4(1), 58-67.

Durán, O., & Durán, P. (2018). Activity Based Costing for Wastewater Treatment and Reuse

under Uncertainty: A Fuzzy Approach. Sustainability, 10(7), 2260.

Namazi, M. (2016). Time Driven Activity Based Costing: Theory, Applications and

Limitations. Iranian Journal of Management Studies, 9(3), 457-482.

Esmalifalak, H., Albin, M. S., & Behzadpoor, M. (2015). A comparative study on the activity

based costing systems: Traditional, fuzzy and Monte Carlo approaches. Health Policy

and Technology, 4(1), 58-67.

Durán, O., & Durán, P. (2018). Activity Based Costing for Wastewater Treatment and Reuse

under Uncertainty: A Fuzzy Approach. Sustainability, 10(7), 2260.

Namazi, M. (2016). Time Driven Activity Based Costing: Theory, Applications and

Limitations. Iranian Journal of Management Studies, 9(3), 457-482.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.