ABC Costing Model and Strategies for National Tyre & Wheel Limited

VerifiedAdded on 2023/06/12

|10

|2584

|98

Report

AI Summary

This report analyzes the application of the Activity-Based Costing (ABC) model within National Tyre & Wheel Limited (NTD), an ASX-listed entity, to enhance strategic decision-making. It examines the company's mission, objectives, and strategies, demonstrating how ABC costing can align with corporate goals. The report details the features of ABC costing, emphasizing its role in accurately identifying operational costs, which enables management accountants to make informed strategic choices for future growth. Furthermore, it provides recommendations for the successful implementation of the ABC model within NTD, including employee training and benchmarking, and suggests the use of target costing as another suitable management accounting tool. The analysis highlights how ABC costing can improve operational efficiency, reduce overhead costs, and enhance customer satisfaction, ultimately supporting NTD's business strategy of growth and expansion.

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The present report is developed for demonstrating the importance of ABC cost

accounting model in gaining success in the present competitive business environment. The

report has enabled and examined the mission, objectives and strategies of National Tyre &

Wheel Limited an ASX listed entity. This is followed by provided an explanation of aligning its

corporate strategies with the ABC model. As a result, it has been concluded that the accurate

identification of the cost involved in the operational processes with the use of ABC costing

enables the management accountants of the company in taking accurate strategic decisions for

the future growth.

The present report is developed for demonstrating the importance of ABC cost

accounting model in gaining success in the present competitive business environment. The

report has enabled and examined the mission, objectives and strategies of National Tyre &

Wheel Limited an ASX listed entity. This is followed by provided an explanation of aligning its

corporate strategies with the ABC model. As a result, it has been concluded that the accurate

identification of the cost involved in the operational processes with the use of ABC costing

enables the management accountants of the company in taking accurate strategic decisions for

the future growth.

Contents

Introduction......................................................................................................................................4

a. ABC and its Features...................................................................................................................4

b. Aligning of ABC Model with the Current Goals & Strategies....................................................5

i. Identification of Company’s Mission & Objective..................................................................5

ii. Identification of Company’s Strategies...................................................................................6

iii. Explanation of ABC Model in Achieving Company Strategies.............................................6

c. Recommendations for Implementation of ABC Model in National Tyre And Wheel Limited

(NTD)..............................................................................................................................................8

d. Suggestion of other Management Accounting Tool Suitable for the Company..........................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Introduction......................................................................................................................................4

a. ABC and its Features...................................................................................................................4

b. Aligning of ABC Model with the Current Goals & Strategies....................................................5

i. Identification of Company’s Mission & Objective..................................................................5

ii. Identification of Company’s Strategies...................................................................................6

iii. Explanation of ABC Model in Achieving Company Strategies.............................................6

c. Recommendations for Implementation of ABC Model in National Tyre And Wheel Limited

(NTD)..............................................................................................................................................8

d. Suggestion of other Management Accounting Tool Suitable for the Company..........................9

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report is carried for providing a deep insight into the cost accounting model of

Activity Based Analysis (ABC) and its various features. This has been done through carrying out

an evaluation of the use of ABC model for attaining the corporate strategies of a company listed

on ASX. The company selected in this context is of National Tyre & Wheel Limited (NTD). Also,

the recommendations about the implementation of the model and other management

accounting tool suitable to be applied within the company are discussed in the report.

a. ABC and its Features

For the measurement of the overhead cost, one of the tools which are mostly used by

the companies and business organisations is ABC better known as activity based costing. By

using ABC tool, the business organisations measure the overhead cost as well as the several

other costs which are related to the business operations. The ABC approach is based upon the

cost of the products that is incurred while the companies undertook its business operations

ranging from manufacturing to finishing. Whenever the business organisation carries on with its

production there is a sort of cost which is added in every next step in the total cost of the

production. Therefore, to manage these added cost and the overhead cost; the companies

started taking use of the ABC tool (Wagener, 2008). Another aspect by which activity based

costing can be understood is the financial cost allocation. For achieving higher production and

improved performance with the minimum use of organisational resources and low cost, there is

used ABC tool so that there can be maintained an effective track of the activities and costs

which are related to the product and production. There are various activities in which the ABC

tool is used in the business organisation such as for the development of the products for the

manufacturing of goods for production as well as for identifying the required capital needed for

the manufacturing and production functions (Leitner, 2007).

Activity based costing has a number of features or characteristics that help the

businesses and the companies in the effective calculation of the overhead cost associated with

the final product. There is fixed cost as well as the variable cost which accumulated and

This report is carried for providing a deep insight into the cost accounting model of

Activity Based Analysis (ABC) and its various features. This has been done through carrying out

an evaluation of the use of ABC model for attaining the corporate strategies of a company listed

on ASX. The company selected in this context is of National Tyre & Wheel Limited (NTD). Also,

the recommendations about the implementation of the model and other management

accounting tool suitable to be applied within the company are discussed in the report.

a. ABC and its Features

For the measurement of the overhead cost, one of the tools which are mostly used by

the companies and business organisations is ABC better known as activity based costing. By

using ABC tool, the business organisations measure the overhead cost as well as the several

other costs which are related to the business operations. The ABC approach is based upon the

cost of the products that is incurred while the companies undertook its business operations

ranging from manufacturing to finishing. Whenever the business organisation carries on with its

production there is a sort of cost which is added in every next step in the total cost of the

production. Therefore, to manage these added cost and the overhead cost; the companies

started taking use of the ABC tool (Wagener, 2008). Another aspect by which activity based

costing can be understood is the financial cost allocation. For achieving higher production and

improved performance with the minimum use of organisational resources and low cost, there is

used ABC tool so that there can be maintained an effective track of the activities and costs

which are related to the product and production. There are various activities in which the ABC

tool is used in the business organisation such as for the development of the products for the

manufacturing of goods for production as well as for identifying the required capital needed for

the manufacturing and production functions (Leitner, 2007).

Activity based costing has a number of features or characteristics that help the

businesses and the companies in the effective calculation of the overhead cost associated with

the final product. There is fixed cost as well as the variable cost which accumulated and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

resulted in the overhead cost. The variable cost kept on changing according to the business

operations and the products. When there is any maintenance cost or the repair cost; the cost is

considered as the variable cost. It is also variable in nature because of the quality change as

well as the changing requirements of the customer. On the other hand the fixed cost does not

change and it remains same for all the production and business operations. It comprises of the

cost that is fixed such as the various labour cost, electricity cost, etc. the companies make clear

difference between the fixed cost as well as the various cost in the manufacturing unit. When

the cost is associated with the product then it is based upon the circumstances where the

production takes place as well as the quality of production (Zeuner, 2012). The manufacturing

plants are usually there at different units and because of this there is high level of variance that

occurs in the cost. There are number of challenges and issues that are associated with the cost

and it is essential to understand these issues before the initiation of the production process.

The cost relationship issues have a direct impact upon the budget. These issues are related to

the changing market needs and the customers' orders. Thus, it is essential that before the

actual calculation of the cost there must be identified and analyses the various factors that can

impact the cost. For customer satisfaction as well as for improved production, there is a need

that the production team must prepare a chart for all the activities (Goektuerk, 2007).

ABC tool of accounting is highly vital for the business organisations that deal in manufacturing

because due to the usage of old and traditional methods, there are extended costs that

incurred on final product. The companies use the ABC tool for better decision making and

improving performance by taking efficient use of minimum resources and by calculating the

overhead cost (Kim, 2017).

b. Aligning of ABC Model with the Current Goals & Strategies

i. Identification of Company’s Mission & Objective

National Tyre & Wheel Limited is a tyre and wheel wholesaler company involved in

providing tyres and wheel for passenger cars, light commercial vehicles and caravans. The

company provides its products across Australia & New Zealand. The company is recognized to

meet the tyre replacement needs of thousands of drivers on an annual basis. The company

operations and the products. When there is any maintenance cost or the repair cost; the cost is

considered as the variable cost. It is also variable in nature because of the quality change as

well as the changing requirements of the customer. On the other hand the fixed cost does not

change and it remains same for all the production and business operations. It comprises of the

cost that is fixed such as the various labour cost, electricity cost, etc. the companies make clear

difference between the fixed cost as well as the various cost in the manufacturing unit. When

the cost is associated with the product then it is based upon the circumstances where the

production takes place as well as the quality of production (Zeuner, 2012). The manufacturing

plants are usually there at different units and because of this there is high level of variance that

occurs in the cost. There are number of challenges and issues that are associated with the cost

and it is essential to understand these issues before the initiation of the production process.

The cost relationship issues have a direct impact upon the budget. These issues are related to

the changing market needs and the customers' orders. Thus, it is essential that before the

actual calculation of the cost there must be identified and analyses the various factors that can

impact the cost. For customer satisfaction as well as for improved production, there is a need

that the production team must prepare a chart for all the activities (Goektuerk, 2007).

ABC tool of accounting is highly vital for the business organisations that deal in manufacturing

because due to the usage of old and traditional methods, there are extended costs that

incurred on final product. The companies use the ABC tool for better decision making and

improving performance by taking efficient use of minimum resources and by calculating the

overhead cost (Kim, 2017).

b. Aligning of ABC Model with the Current Goals & Strategies

i. Identification of Company’s Mission & Objective

National Tyre & Wheel Limited is a tyre and wheel wholesaler company involved in

providing tyres and wheel for passenger cars, light commercial vehicles and caravans. The

company provides its products across Australia & New Zealand. The company is recognized to

meet the tyre replacement needs of thousands of drivers on an annual basis. The company

objective is to achieve positive consumer engagement by providing with high quality tyres

developed with the use of latest generation technology. The mission of the company is to

become a leading brand by development of innovating wheel products having long life, safety

and suitability.

ii. Identification of Company’s Strategies

The company strategy is to rapidly expand is type and wheel product portfolio and

therefore carried out its business operations through subsidiaries and controlled entities. The

different subsidiaries of the company pursue growth strategy and strive to introduce new range

of products for new market segments and driving the customer loyalty with the use of value-

adding services. The company strategy is to develop its wholesaling business for providing tyre

products and driving its continued growth by the development of its subsidiaries and controlled

entities (National Tyre & Wheel Limited, 2018).

iii. Explanation of ABC Model in Achieving Company Strategies

ABC costing model can largely facilitate the company in achievement of its corporate

strategies by its effective strategic positioning. The company is aiming to expand its product

portfolio for driving its continuous growth and creative positive engagement by providing them

high quality products. This can be achieved by the company with the use of ABC costing model

that will help NTD in redesigning of its manufacturing process. ABC costing model will enable

the company to gain a better understanding of real operational costs and returns and thus

supporting the management accountants to take key decisions for improving operational

efficiency. The company can review its products for price adjustment with the use of ABC

costing model that can lead to identification of the opportunities for reducing operational cost

through product redesigning and process improvement. The increase in the operational

efficiency will drive significant reduction improve of products and increasing customer

satisfaction for the company and thus helping it to attain its corporate strategy (Goektuerk,

2007).

NTD for evolving its product portfolio need to price many type of tyre products in

different amounts. Thus, the production of each product will incur varying amount of overhead

developed with the use of latest generation technology. The mission of the company is to

become a leading brand by development of innovating wheel products having long life, safety

and suitability.

ii. Identification of Company’s Strategies

The company strategy is to rapidly expand is type and wheel product portfolio and

therefore carried out its business operations through subsidiaries and controlled entities. The

different subsidiaries of the company pursue growth strategy and strive to introduce new range

of products for new market segments and driving the customer loyalty with the use of value-

adding services. The company strategy is to develop its wholesaling business for providing tyre

products and driving its continued growth by the development of its subsidiaries and controlled

entities (National Tyre & Wheel Limited, 2018).

iii. Explanation of ABC Model in Achieving Company Strategies

ABC costing model can largely facilitate the company in achievement of its corporate

strategies by its effective strategic positioning. The company is aiming to expand its product

portfolio for driving its continuous growth and creative positive engagement by providing them

high quality products. This can be achieved by the company with the use of ABC costing model

that will help NTD in redesigning of its manufacturing process. ABC costing model will enable

the company to gain a better understanding of real operational costs and returns and thus

supporting the management accountants to take key decisions for improving operational

efficiency. The company can review its products for price adjustment with the use of ABC

costing model that can lead to identification of the opportunities for reducing operational cost

through product redesigning and process improvement. The increase in the operational

efficiency will drive significant reduction improve of products and increasing customer

satisfaction for the company and thus helping it to attain its corporate strategy (Goektuerk,

2007).

NTD for evolving its product portfolio need to price many type of tyre products in

different amounts. Thus, the production of each product will incur varying amount of overhead

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and thus making it difficult for the management accountant to allocate the overhead cost on

individual product basis. In this context, the use of ABC model will provide large help to the

management accountants for gaining an accurate estimation of the overhead costs by assigning

them to each product manufactured accurately. This is done by the use of developing cost

pools and cots drivers that helps in allocating the costs as per the overhead resources

consumed in manufacturing process of the company (Kocakula, 2017). Cost drivers are

regarded as the factors that determine the number of activities that will be consumed by a

given product such as machine hours, size or complexity. The cost incurred in carrying out each

activity for the manufacturing of a product can be accurately identified by the management

accountants of the company with the use of ABC costing. The actual cost data relating to the

products manufactured by the company on the basis of volume of production will assist the

management in taking strategic decision regarding the its future growth and expansion plans

(Clifton, 2003).

Thus, the use of ABC costing method largely facilitates the business managers of the

company to take accurate decisions and therefore it act as a strategic management tool. The

decisions relation to elimination of non-value adding products largely helps in improving the

operational efficiency by reduction in the overhead costs consumed by the non-valuable

products. This can help the company in improving its profitability position and supporting its

business strategy of growth and expansion (Ness and Cucuzza, 2005). The strategic decision

regarding the product designs, product mix, marketing and product price all requires actual

product costing data provided with the use of ABC costing model. Therefore, a better

representation of the resources consumed by the activities involved in production of products

helps in accurate allocation of the cost to customers on the basis of activity consumed by them.

This can enable the company in attaining a competitive edge by creating positive customer

engagement through providing them with high quality and low priced products (Kannaiah,

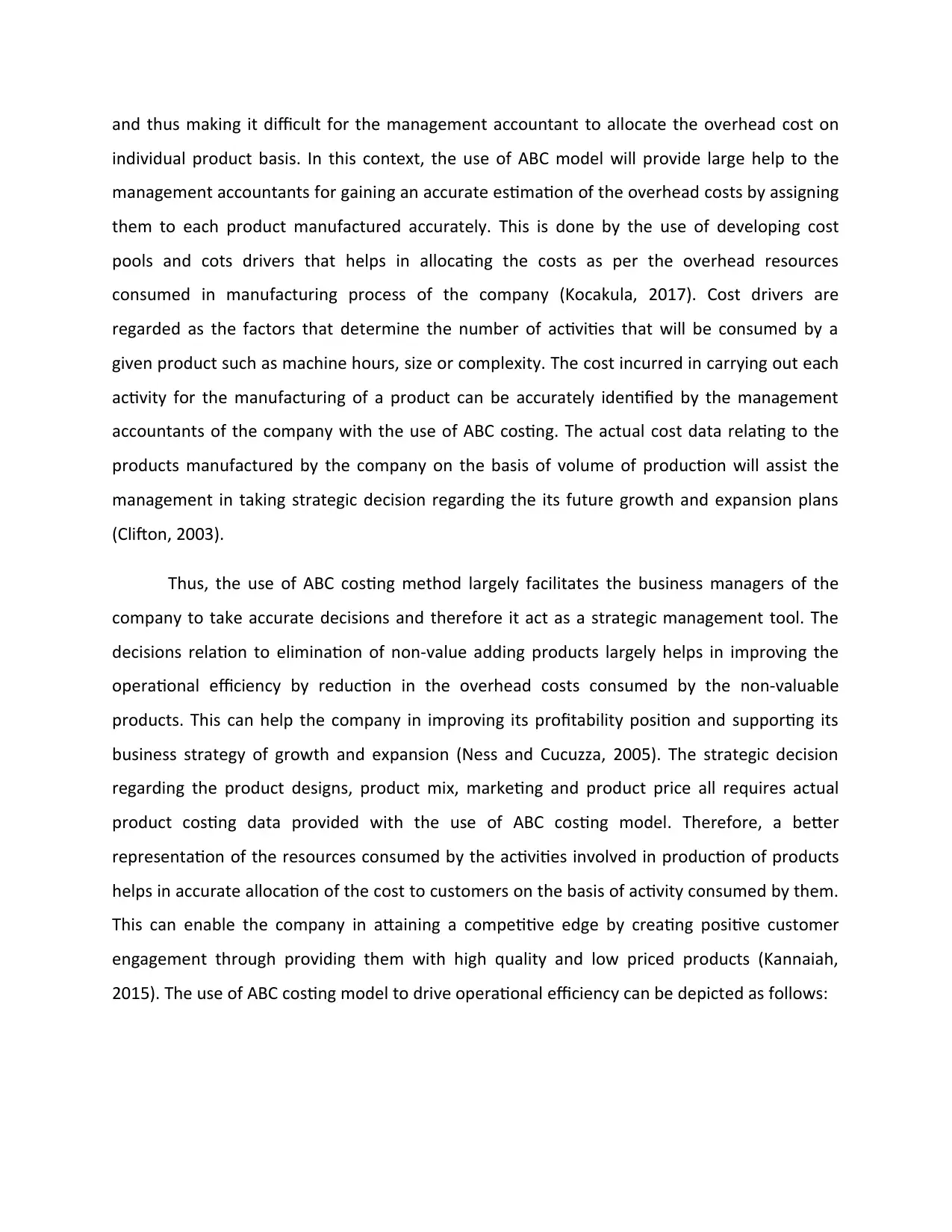

2015). The use of ABC costing model to drive operational efficiency can be depicted as follows:

individual product basis. In this context, the use of ABC model will provide large help to the

management accountants for gaining an accurate estimation of the overhead costs by assigning

them to each product manufactured accurately. This is done by the use of developing cost

pools and cots drivers that helps in allocating the costs as per the overhead resources

consumed in manufacturing process of the company (Kocakula, 2017). Cost drivers are

regarded as the factors that determine the number of activities that will be consumed by a

given product such as machine hours, size or complexity. The cost incurred in carrying out each

activity for the manufacturing of a product can be accurately identified by the management

accountants of the company with the use of ABC costing. The actual cost data relating to the

products manufactured by the company on the basis of volume of production will assist the

management in taking strategic decision regarding the its future growth and expansion plans

(Clifton, 2003).

Thus, the use of ABC costing method largely facilitates the business managers of the

company to take accurate decisions and therefore it act as a strategic management tool. The

decisions relation to elimination of non-value adding products largely helps in improving the

operational efficiency by reduction in the overhead costs consumed by the non-valuable

products. This can help the company in improving its profitability position and supporting its

business strategy of growth and expansion (Ness and Cucuzza, 2005). The strategic decision

regarding the product designs, product mix, marketing and product price all requires actual

product costing data provided with the use of ABC costing model. Therefore, a better

representation of the resources consumed by the activities involved in production of products

helps in accurate allocation of the cost to customers on the basis of activity consumed by them.

This can enable the company in attaining a competitive edge by creating positive customer

engagement through providing them with high quality and low priced products (Kannaiah,

2015). The use of ABC costing model to drive operational efficiency can be depicted as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: https://researchonline.jcu.edu.au/41020/1/41020%20Kannaiah%202015.pdf)

c. Recommendations for Implementation of ABC Model in National Tyre

And Wheel Limited (NTD)

NTD is recommended to adopt the use of following suggestions for successful

implementation of ABC cost accounting system:

Employees Training: It is essential for ensuring the success achieved with the use of ABC

cost accounting model to provide relevant information about its needs and benefits to

the employees. This is necessary for overcoming the employee resistance to change by

providing them adequate information about the need of ABC system to be implemented

within the work processes. In this context, employees need to provide training to

incorporate the use of ABC costing model in their jobs for providing accurate costing

information to the management for decision-making. This will improve their skills and

knowledge regarding the ABC and also overcoming their hindrance to adopt its usage in

performing their daily job roles. This is essential to redesign the manufacturing process

of the company with the use of ABC costing model to achieve the operational excellence

and driving its profitability (Ness and Cucuzza, 2005).

c. Recommendations for Implementation of ABC Model in National Tyre

And Wheel Limited (NTD)

NTD is recommended to adopt the use of following suggestions for successful

implementation of ABC cost accounting system:

Employees Training: It is essential for ensuring the success achieved with the use of ABC

cost accounting model to provide relevant information about its needs and benefits to

the employees. This is necessary for overcoming the employee resistance to change by

providing them adequate information about the need of ABC system to be implemented

within the work processes. In this context, employees need to provide training to

incorporate the use of ABC costing model in their jobs for providing accurate costing

information to the management for decision-making. This will improve their skills and

knowledge regarding the ABC and also overcoming their hindrance to adopt its usage in

performing their daily job roles. This is essential to redesign the manufacturing process

of the company with the use of ABC costing model to achieve the operational excellence

and driving its profitability (Ness and Cucuzza, 2005).

Benchmarking: The business managers can implement the ABC costing model in the

manufacturing process of the company by benchmarking each of the business processes

against the standard that they think is the best to be adopted. Thus, it will provide a

direction to the business managers regarding the target to be achieved by the use of

ABC costing model. ABC can drive continuous improvement in the manufacturing

process of the company by identifying the wasteful activities and improving the

operational efficiency. This in turn will facilitate the business manager to achieve the

standard business process that has been determined to be achieved (Kannaiah, 2015).

d. Suggestion of other Management Accounting Tool Suitable for the

Company

The company is also recommended to adopt the use of target costing method in order

to accurately determine the cost involves in production of new products by the company. The

method is efficient to be used for estimating the overall cost of product life cycle in advance

and thus facilitating in making advance plans for price points and margins that the business

manager wants to achieve for new product. The approach is largely beneficial for developing

the cost goals of a new product to be achieved by the company on the basis of market

conditions such as level of competition or switching cost of the customer and many others. It

will enable the company to attain a competitive edge by driving to achieve the determined

profit margin from each product by the use of suitable cost reduction strategies and actions

(Clifton, 2003).

Conclusion

The report concludes that activity based costing model is a highly efficient cost

accounting model that enables the management accountants to collect real time cost

information for taking accurate strategic decisions. The use of ABC cost accounting model can

prove to be highly useful for NTD to realize its growth strategies of business expansion by

targeting new customers segments through creation of new tyre and wheel products.

manufacturing process of the company by benchmarking each of the business processes

against the standard that they think is the best to be adopted. Thus, it will provide a

direction to the business managers regarding the target to be achieved by the use of

ABC costing model. ABC can drive continuous improvement in the manufacturing

process of the company by identifying the wasteful activities and improving the

operational efficiency. This in turn will facilitate the business manager to achieve the

standard business process that has been determined to be achieved (Kannaiah, 2015).

d. Suggestion of other Management Accounting Tool Suitable for the

Company

The company is also recommended to adopt the use of target costing method in order

to accurately determine the cost involves in production of new products by the company. The

method is efficient to be used for estimating the overall cost of product life cycle in advance

and thus facilitating in making advance plans for price points and margins that the business

manager wants to achieve for new product. The approach is largely beneficial for developing

the cost goals of a new product to be achieved by the company on the basis of market

conditions such as level of competition or switching cost of the customer and many others. It

will enable the company to attain a competitive edge by driving to achieve the determined

profit margin from each product by the use of suitable cost reduction strategies and actions

(Clifton, 2003).

Conclusion

The report concludes that activity based costing model is a highly efficient cost

accounting model that enables the management accountants to collect real time cost

information for taking accurate strategic decisions. The use of ABC cost accounting model can

prove to be highly useful for NTD to realize its growth strategies of business expansion by

targeting new customers segments through creation of new tyre and wheel products.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Clifton, B. 2003.

Target Costing: Market Driven Product Design. CRC Press.

Goektuerk, H. 2007.

Activity-Based Costing (ABC) - Advantages and Disadvantages. GRIN Verlag.

Kannaiah, D. 2015. Activity Based Costing (ABC): Is It a Tool for Company to Achieve

Competitive Advantage?

International Journal of Economics and Finance 7(12), pp. 275-281.

Kim, Y. 2017.

Activity Based Costing for Construction Companies. John Wiley & Sons.

Kocakula, M.C. 2017. Activity-Based Costing: Helping Small and Medium-Sized Firms Achieve a

Competitive Edge in the Global Marketplace.

Department of Accounting and Business.

Leitner, A. 2007.

Activity Based Costing. GRIN Verlag.

National Tyre & Wheel Limited. 2018. [Online]. Available at:

http://www.ntaw.com.au/companies [Accessed on: 25 May 2018].

Ness, J. and Cucuzza, T. 2005. Tapping the full potential of ABC. [Online]. Available at:

https://hbr.org/1995/07/tapping-the-full-potential-of-abc [Accessed on: 25 May 2018].

Wagener, D. 2008. Activity-Based costing and its later development into activity based

budgeting and management. GRIN Verlag.

Zeuner, P. 2012.

Activity-Based Costing. GRIN Verlag.

Clifton, B. 2003.

Target Costing: Market Driven Product Design. CRC Press.

Goektuerk, H. 2007.

Activity-Based Costing (ABC) - Advantages and Disadvantages. GRIN Verlag.

Kannaiah, D. 2015. Activity Based Costing (ABC): Is It a Tool for Company to Achieve

Competitive Advantage?

International Journal of Economics and Finance 7(12), pp. 275-281.

Kim, Y. 2017.

Activity Based Costing for Construction Companies. John Wiley & Sons.

Kocakula, M.C. 2017. Activity-Based Costing: Helping Small and Medium-Sized Firms Achieve a

Competitive Edge in the Global Marketplace.

Department of Accounting and Business.

Leitner, A. 2007.

Activity Based Costing. GRIN Verlag.

National Tyre & Wheel Limited. 2018. [Online]. Available at:

http://www.ntaw.com.au/companies [Accessed on: 25 May 2018].

Ness, J. and Cucuzza, T. 2005. Tapping the full potential of ABC. [Online]. Available at:

https://hbr.org/1995/07/tapping-the-full-potential-of-abc [Accessed on: 25 May 2018].

Wagener, D. 2008. Activity-Based costing and its later development into activity based

budgeting and management. GRIN Verlag.

Zeuner, P. 2012.

Activity-Based Costing. GRIN Verlag.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.