Cost Accounting Report: ABC Costing and Profitability

VerifiedAdded on 2020/12/18

|10

|2672

|305

Report

AI Summary

This report provides a comprehensive analysis of cost accounting, specifically focusing on Activity-Based Costing (ABC) and its implications on profitability. It begins with an introduction to cost accounting and the importance of accurate product costing, followed by a detailed explanation of ABC costing, including the identification and calculation of cost drivers. The report then calculates the cost of goods sold under the ABC system and performs a profitability analysis, comparing the results to traditional costing methods. Furthermore, it offers strategic advice to Kay, based on the findings, and discusses the APES 110 Code of Ethics. Finally, it addresses predetermined overhead rates and methods for dealing with under and over absorption of overhead costs, providing a well-rounded understanding of cost accounting principles and their practical applications.

COST ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

1. Importance of Accurate Product Costing...........................................................................1

2. Calculation of Cost Drivers as per ABC costing................................................................3

3.Calculation of Cost of Goods Sold under ABC costing......................................................3

4. Profitability analysis under ABC system...........................................................................4

5. Advise to Kay from Smith..................................................................................................4

6. Predetermined Overhead Rate............................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

1. Importance of Accurate Product Costing...........................................................................1

2. Calculation of Cost Drivers as per ABC costing................................................................3

3.Calculation of Cost of Goods Sold under ABC costing......................................................3

4. Profitability analysis under ABC system...........................................................................4

5. Advise to Kay from Smith..................................................................................................4

6. Predetermined Overhead Rate............................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Cost analysis in a process where reporting of different cost proposals that can be labor,

equipment or material etc. that make up product ad its proposed profits. They are often referred

as cost-effective analysis and requires specific skill to conduct and it can be a useful tool for

different aspects of business planning. Activity Base Costing is a method that identifies and

assign cost driver to different overhead activities and then assign these to products. Traditional

method depends upon volume count of machine or labor hours etc. to allocate overheads costs to

products. So as case study provided which involves comparison between traditional method and

ABC system of Costing. This report will provide different ways for utilizing of under and over

absorption of overheads.

Task 1

1. Importance of Accurate Product Costing

Management accounting is process of analyzing, interpreting, and presenting of

accounting related information collected with help of financial and cost accounting. So,Cost

accounting is a part of management accounting i.e. why it is important to find accurate cost of

product as that assist organisation in decision making.

The following are importance of accurate product costing-:

1. Impact in Budgets-: Budget totally depends upon accurate forecast of expenses and

revenues for next period of accounting. So, if it is miscalculated significant errors may

occur in the process of budget (Catrini and et.al., 2017). In the above case the cost

calculated by traditional method, overhead charged to lexton was much higher than it was

so profit of Lexton product decrease so they thought to phase out that product which

could have made a huge losses to them.

2. Income Statement-: It is dependent on accurate calculation of product cost or cost of

goods sold as the product which is sold is subtracted from total profits revenue generated

during accounting period to calculate net revenue. If that calculations are incorrect, net

revenue may be higher than reported (Dunuwila, Rodrigo and Goto, 2018). In this case

Gross margin is affected as because of traditional method, product cost ascertain is much

higher from ABC costing.

3. Decision Making-: Better the costs are ascertain it helps in determining financial

viability of projects. Here in this case costs are not determined accurately so they thought

1

Cost analysis in a process where reporting of different cost proposals that can be labor,

equipment or material etc. that make up product ad its proposed profits. They are often referred

as cost-effective analysis and requires specific skill to conduct and it can be a useful tool for

different aspects of business planning. Activity Base Costing is a method that identifies and

assign cost driver to different overhead activities and then assign these to products. Traditional

method depends upon volume count of machine or labor hours etc. to allocate overheads costs to

products. So as case study provided which involves comparison between traditional method and

ABC system of Costing. This report will provide different ways for utilizing of under and over

absorption of overheads.

Task 1

1. Importance of Accurate Product Costing

Management accounting is process of analyzing, interpreting, and presenting of

accounting related information collected with help of financial and cost accounting. So,Cost

accounting is a part of management accounting i.e. why it is important to find accurate cost of

product as that assist organisation in decision making.

The following are importance of accurate product costing-:

1. Impact in Budgets-: Budget totally depends upon accurate forecast of expenses and

revenues for next period of accounting. So, if it is miscalculated significant errors may

occur in the process of budget (Catrini and et.al., 2017). In the above case the cost

calculated by traditional method, overhead charged to lexton was much higher than it was

so profit of Lexton product decrease so they thought to phase out that product which

could have made a huge losses to them.

2. Income Statement-: It is dependent on accurate calculation of product cost or cost of

goods sold as the product which is sold is subtracted from total profits revenue generated

during accounting period to calculate net revenue. If that calculations are incorrect, net

revenue may be higher than reported (Dunuwila, Rodrigo and Goto, 2018). In this case

Gross margin is affected as because of traditional method, product cost ascertain is much

higher from ABC costing.

3. Decision Making-: Better the costs are ascertain it helps in determining financial

viability of projects. Here in this case costs are not determined accurately so they thought

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of shut down there product which is more profitable than new product (Bai, Lam and Li,

2018).

4. Budget Impact: Budget process completely depends upon the accurate calculation of

expenses and incomes so that educated forecast could be made of the next accounting

period by company (Huang, 2018). If it is not done accurately, this may lead to creation

of financial strains which are created by overspending against budget figures.

Further, problems of using traditional costing systems are stated below:

1. Overhead recovery rates such as; labour hour rate, machine hour rate, etc. are used for

absorption of overhead costs. This system is not useful for taking decisions because

decisions that are implicated are continued for over 3 to 5 years. Some fixed costs are

also variable as well in the long run.

2. Separating theses costs into variable and fixed in often unrealistic because splitting of

cost gives inaccurate costs of products in case if business grows.

3. In case where some companies manufactures and sells more than single product, these

companies are bound to take decisions on pricing, advertisements, product mix, sales

promotion campaign, etc. based on the estimated cost information.

4. In this era of modern technology, most of the labour work is done with the help of

automated system. This automation resulted in reduction in direct costs and increase in

indirect costs. It may create a problem if cost structure of a product is changed when

automation is taking place in any products.

5. Another problem that arises is that, indirect costs are allocated and reallocated at product

level only after manufacturing of a product. As it is mandatory now to complete work

with accurate indirect costs incurred and is not possible under traditional cost accounting

system (Hoque, 2005).

6. Traditional costing system does not provide company with that ability to reduce waste by

showing every indirect cost for each specific product because it looks forward at

overhead costs in general.

2

2018).

4. Budget Impact: Budget process completely depends upon the accurate calculation of

expenses and incomes so that educated forecast could be made of the next accounting

period by company (Huang, 2018). If it is not done accurately, this may lead to creation

of financial strains which are created by overspending against budget figures.

Further, problems of using traditional costing systems are stated below:

1. Overhead recovery rates such as; labour hour rate, machine hour rate, etc. are used for

absorption of overhead costs. This system is not useful for taking decisions because

decisions that are implicated are continued for over 3 to 5 years. Some fixed costs are

also variable as well in the long run.

2. Separating theses costs into variable and fixed in often unrealistic because splitting of

cost gives inaccurate costs of products in case if business grows.

3. In case where some companies manufactures and sells more than single product, these

companies are bound to take decisions on pricing, advertisements, product mix, sales

promotion campaign, etc. based on the estimated cost information.

4. In this era of modern technology, most of the labour work is done with the help of

automated system. This automation resulted in reduction in direct costs and increase in

indirect costs. It may create a problem if cost structure of a product is changed when

automation is taking place in any products.

5. Another problem that arises is that, indirect costs are allocated and reallocated at product

level only after manufacturing of a product. As it is mandatory now to complete work

with accurate indirect costs incurred and is not possible under traditional cost accounting

system (Hoque, 2005).

6. Traditional costing system does not provide company with that ability to reduce waste by

showing every indirect cost for each specific product because it looks forward at

overhead costs in general.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

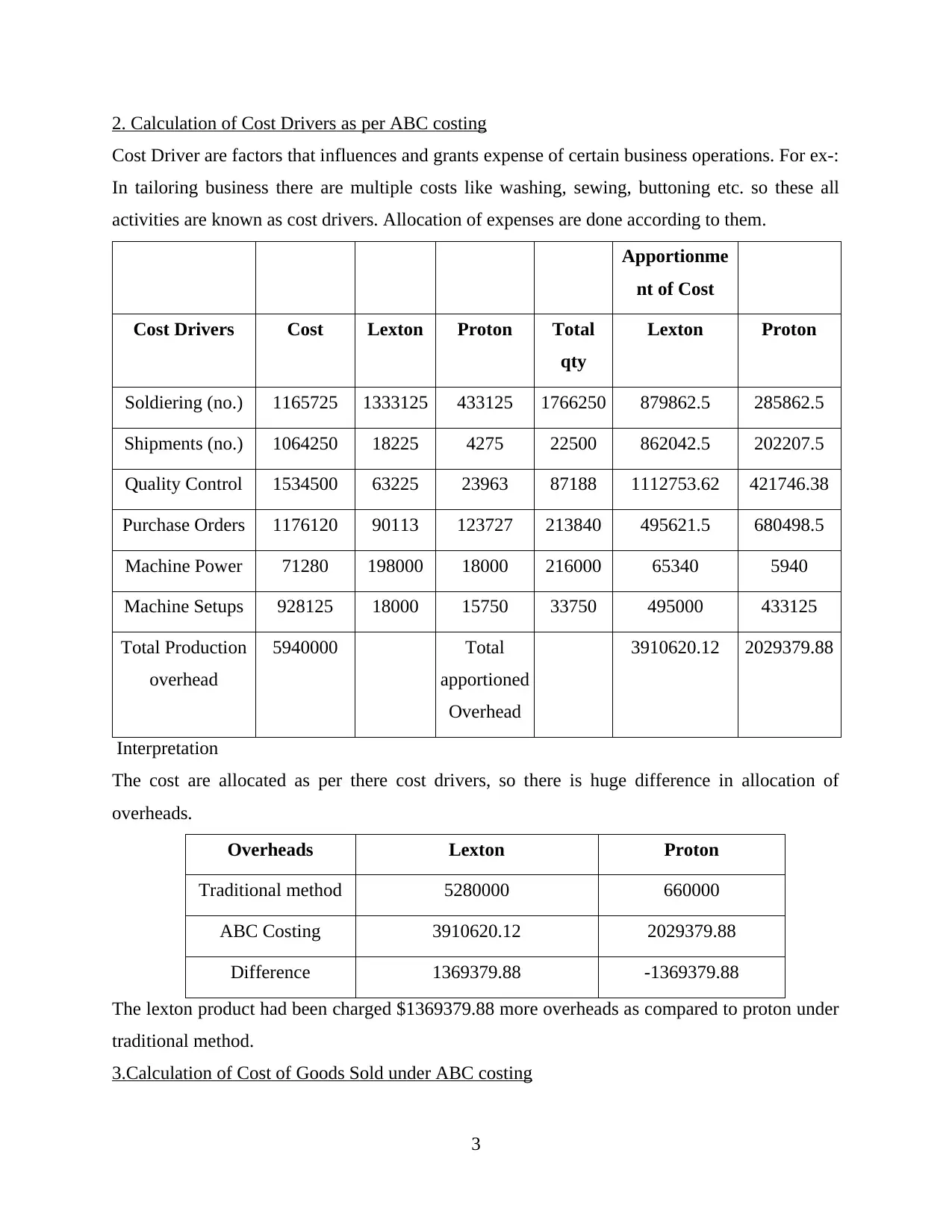

2. Calculation of Cost Drivers as per ABC costing

Cost Driver are factors that influences and grants expense of certain business operations. For ex-:

In tailoring business there are multiple costs like washing, sewing, buttoning etc. so these all

activities are known as cost drivers. Allocation of expenses are done according to them.

Apportionme

nt of Cost

Cost Drivers Cost Lexton Proton Total

qty

Lexton Proton

Soldiering (no.) 1165725 1333125 433125 1766250 879862.5 285862.5

Shipments (no.) 1064250 18225 4275 22500 862042.5 202207.5

Quality Control 1534500 63225 23963 87188 1112753.62 421746.38

Purchase Orders 1176120 90113 123727 213840 495621.5 680498.5

Machine Power 71280 198000 18000 216000 65340 5940

Machine Setups 928125 18000 15750 33750 495000 433125

Total Production

overhead

5940000 Total

apportioned

Overhead

3910620.12 2029379.88

Interpretation

The cost are allocated as per there cost drivers, so there is huge difference in allocation of

overheads.

Overheads Lexton Proton

Traditional method 5280000 660000

ABC Costing 3910620.12 2029379.88

Difference 1369379.88 -1369379.88

The lexton product had been charged $1369379.88 more overheads as compared to proton under

traditional method.

3.Calculation of Cost of Goods Sold under ABC costing

3

Cost Driver are factors that influences and grants expense of certain business operations. For ex-:

In tailoring business there are multiple costs like washing, sewing, buttoning etc. so these all

activities are known as cost drivers. Allocation of expenses are done according to them.

Apportionme

nt of Cost

Cost Drivers Cost Lexton Proton Total

qty

Lexton Proton

Soldiering (no.) 1165725 1333125 433125 1766250 879862.5 285862.5

Shipments (no.) 1064250 18225 4275 22500 862042.5 202207.5

Quality Control 1534500 63225 23963 87188 1112753.62 421746.38

Purchase Orders 1176120 90113 123727 213840 495621.5 680498.5

Machine Power 71280 198000 18000 216000 65340 5940

Machine Setups 928125 18000 15750 33750 495000 433125

Total Production

overhead

5940000 Total

apportioned

Overhead

3910620.12 2029379.88

Interpretation

The cost are allocated as per there cost drivers, so there is huge difference in allocation of

overheads.

Overheads Lexton Proton

Traditional method 5280000 660000

ABC Costing 3910620.12 2029379.88

Difference 1369379.88 -1369379.88

The lexton product had been charged $1369379.88 more overheads as compared to proton under

traditional method.

3.Calculation of Cost of Goods Sold under ABC costing

3

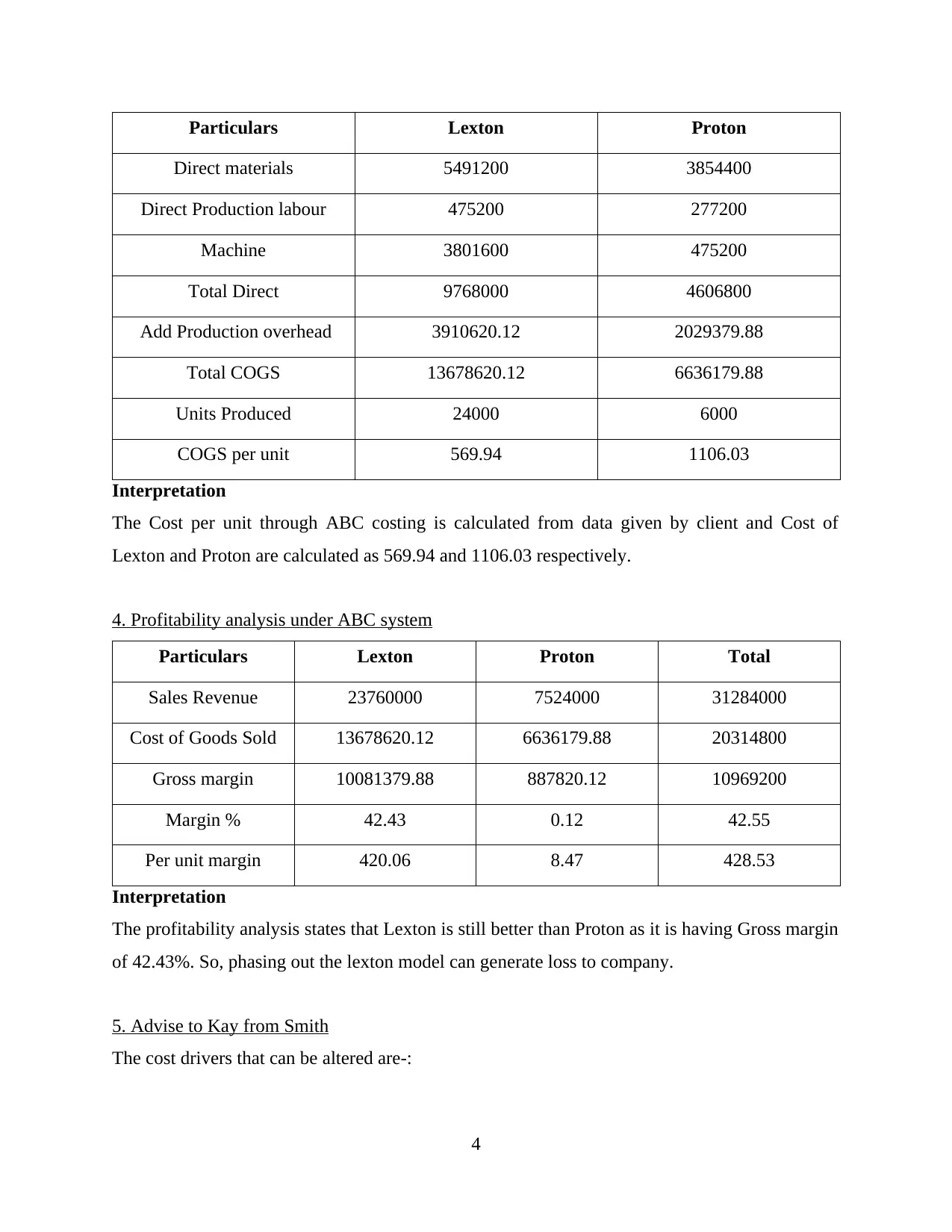

Particulars Lexton Proton

Direct materials 5491200 3854400

Direct Production labour 475200 277200

Machine 3801600 475200

Total Direct 9768000 4606800

Add Production overhead 3910620.12 2029379.88

Total COGS 13678620.12 6636179.88

Units Produced 24000 6000

COGS per unit 569.94 1106.03

Interpretation

The Cost per unit through ABC costing is calculated from data given by client and Cost of

Lexton and Proton are calculated as 569.94 and 1106.03 respectively.

4. Profitability analysis under ABC system

Particulars Lexton Proton Total

Sales Revenue 23760000 7524000 31284000

Cost of Goods Sold 13678620.12 6636179.88 20314800

Gross margin 10081379.88 887820.12 10969200

Margin % 42.43 0.12 42.55

Per unit margin 420.06 8.47 428.53

Interpretation

The profitability analysis states that Lexton is still better than Proton as it is having Gross margin

of 42.43%. So, phasing out the lexton model can generate loss to company.

5. Advise to Kay from Smith

The cost drivers that can be altered are-:

4

Direct materials 5491200 3854400

Direct Production labour 475200 277200

Machine 3801600 475200

Total Direct 9768000 4606800

Add Production overhead 3910620.12 2029379.88

Total COGS 13678620.12 6636179.88

Units Produced 24000 6000

COGS per unit 569.94 1106.03

Interpretation

The Cost per unit through ABC costing is calculated from data given by client and Cost of

Lexton and Proton are calculated as 569.94 and 1106.03 respectively.

4. Profitability analysis under ABC system

Particulars Lexton Proton Total

Sales Revenue 23760000 7524000 31284000

Cost of Goods Sold 13678620.12 6636179.88 20314800

Gross margin 10081379.88 887820.12 10969200

Margin % 42.43 0.12 42.55

Per unit margin 420.06 8.47 428.53

Interpretation

The profitability analysis states that Lexton is still better than Proton as it is having Gross margin

of 42.43%. So, phasing out the lexton model can generate loss to company.

5. Advise to Kay from Smith

The cost drivers that can be altered are-:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7. Quality Control-: As cost of inspection that been taken is much higher for both

products, so there can be chance of controlling that cost which will lead in improving

product overhead (Mahmoudi, Jodeiri and Fatehifar, 2017).

8. Shipment Cost-: This can easily be varied as because shipment of which product is done

can't be ascertain accurately. So there is chance there they can alter.

9. Machine Setups-: As machine setups could not be known for which product they are

doing, alterations can easily be possible (Lutilsky, Liović and Marković, 2018).

The APES 110 Code of Ethics for Professional Accountants states that-:

There are general fundamental principles which are defined in the APES which are

applicable for every professional-:

Integrity-: It imposes an obligation to be straight forward and be honest in all professional

and business dealings. Member must not associate where they believe that information is-:

having material misleading statements

furnished recklessly

Omit any information where such omission would be misleading.

If any time they think that they are associated with this type of information so they must take

steps for disassociating from that information (Nagirikandalage and Binsardi, 2017).

Objectivity-: These imposes an obligation to all members for not compromising there

professional or any business judgment in undue influence of others.

Professional Competence and Due Care-: These imposes following obligations on

members-:

Maintain professional knowledge and skill to ensure clients receive competent

professional service.

Acting diligently in accordance with technical and professional standards.

Confidentiality-: It imposes obligations to avoid-:

Disclosing of confidential information outside firm or organization acquired because of

professional engagement unless there is legal duty to disclose.

Using that information for their personal advantage or the profits of third parties.

Professional Behavior-: this imposes an obligation regarding compliance of relevant laws and

regulation to avoid any action that member knows that may discredit their profession (Biondi and

et.al, 2017).

5

products, so there can be chance of controlling that cost which will lead in improving

product overhead (Mahmoudi, Jodeiri and Fatehifar, 2017).

8. Shipment Cost-: This can easily be varied as because shipment of which product is done

can't be ascertain accurately. So there is chance there they can alter.

9. Machine Setups-: As machine setups could not be known for which product they are

doing, alterations can easily be possible (Lutilsky, Liović and Marković, 2018).

The APES 110 Code of Ethics for Professional Accountants states that-:

There are general fundamental principles which are defined in the APES which are

applicable for every professional-:

Integrity-: It imposes an obligation to be straight forward and be honest in all professional

and business dealings. Member must not associate where they believe that information is-:

having material misleading statements

furnished recklessly

Omit any information where such omission would be misleading.

If any time they think that they are associated with this type of information so they must take

steps for disassociating from that information (Nagirikandalage and Binsardi, 2017).

Objectivity-: These imposes an obligation to all members for not compromising there

professional or any business judgment in undue influence of others.

Professional Competence and Due Care-: These imposes following obligations on

members-:

Maintain professional knowledge and skill to ensure clients receive competent

professional service.

Acting diligently in accordance with technical and professional standards.

Confidentiality-: It imposes obligations to avoid-:

Disclosing of confidential information outside firm or organization acquired because of

professional engagement unless there is legal duty to disclose.

Using that information for their personal advantage or the profits of third parties.

Professional Behavior-: this imposes an obligation regarding compliance of relevant laws and

regulation to avoid any action that member knows that may discredit their profession (Biondi and

et.al, 2017).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6. Predetermined Overhead Rate

These are measures that are used to allocate estimated manufacturing cost to different

products. They are generally estimated at beginning of reporting period (Dias Maragno and et.al.,

2017). The allocation base includes direct labor hours, machine hours, direct material etc.

The reasons for under and over absorption of overheads are as follows-:

Amount that is actually incurred in not same amount as expected

Expected amount of work done is substantial less than it was anticipated

There may be change in proportion of work done by machine or labor

If nature of work is seasonal than overhead may fluctuate according to period

Over or under utilization of capacity

As the number of machine hours increases the fixed costs which are consisted by much of

the overhead do not grow.

There may not be a control over spendings that are done on overhead items.

Cost of labour is included in the overhead that is directly used to create a product or a

service that is being sold. There are chances that they may not know specifically what

tasks are need to be completed.

Costs may fall below the estimated costs of renovations or renting facilities.

If the buyer is able to find strong deals for good and materials, overhead costs also will

decrease.

If it is expected that production in a particular month or quarter will increase and there is

an increase in overhead costs proportionately this also could be the reason for over

applied overhead.

The amount is not same as the amount expected of the overhead incurred.

Basis upon which overhead is applied is in an amount different from expected (Kaplan

and Anderson, 2003). For example, if there are 2,000 hours of direct labour and

$1,00,000 of standard overhead are expected to be incurred in the period, $50 per hour

overhead application rate is set at. However, 1,900 hours are the actually number of hours

incurred, then $5,000 of overhead associated with the missing 100 hours will not be

applied.

The three ways by which under or over absorption of overheads can be disposed off-:

6

These are measures that are used to allocate estimated manufacturing cost to different

products. They are generally estimated at beginning of reporting period (Dias Maragno and et.al.,

2017). The allocation base includes direct labor hours, machine hours, direct material etc.

The reasons for under and over absorption of overheads are as follows-:

Amount that is actually incurred in not same amount as expected

Expected amount of work done is substantial less than it was anticipated

There may be change in proportion of work done by machine or labor

If nature of work is seasonal than overhead may fluctuate according to period

Over or under utilization of capacity

As the number of machine hours increases the fixed costs which are consisted by much of

the overhead do not grow.

There may not be a control over spendings that are done on overhead items.

Cost of labour is included in the overhead that is directly used to create a product or a

service that is being sold. There are chances that they may not know specifically what

tasks are need to be completed.

Costs may fall below the estimated costs of renovations or renting facilities.

If the buyer is able to find strong deals for good and materials, overhead costs also will

decrease.

If it is expected that production in a particular month or quarter will increase and there is

an increase in overhead costs proportionately this also could be the reason for over

applied overhead.

The amount is not same as the amount expected of the overhead incurred.

Basis upon which overhead is applied is in an amount different from expected (Kaplan

and Anderson, 2003). For example, if there are 2,000 hours of direct labour and

$1,00,000 of standard overhead are expected to be incurred in the period, $50 per hour

overhead application rate is set at. However, 1,900 hours are the actually number of hours

incurred, then $5,000 of overhead associated with the missing 100 hours will not be

applied.

The three ways by which under or over absorption of overheads can be disposed off-:

6

1. Supplementary rates can be used-: If there is significant under or over absorption due to

which base mentioned is not coming true than another rate can be used. Mismatch arises

because of normal errors of business planning (Catrini and et.al., 2017). Calculation of

supplementary rates are nothing but it is a process where under or over absorption are

brought up or down as the case may be to correct figure of actual overhead. The

supplementary rates are of two types

1. Positive-: Under absorption are corrected by positive rates as unrecovered amount

is added back to cost of sales, work in progress.

2. Negative-: By this over absorption are corrected and excess recovery of overhead

is deducted from cost of sales, work in progress.

2. Carry over Overheads-: The following are circumstances where they can be carried to

next year in hope that they will be neutralized.

1. In case the industry is of seasonal nature than it carried to next season for

neutralization.

2. Where there is under absorption in initial years these may be carried forward for

neutralizing later when project is established.

3. Transfer to Costing Profit and Loss-: Following are cases where they must be transferred

to costing P&L-:

1. where the absorption's are relatively of small value and unnecessary to adjust to

cost of sales

2. In case where it arises because of abnormal factors like fires, strikes, plant

breakdown etc.

CONCLUSION

On the basis of above report, it acne concluded that there had been implication of various

tools and techniques which were being addressed to have proper determination of relevant facts.

Similarly, implicating various cost analysis techniques which will be useful for better

determination on ascertainment of all the relevant facts.

7

which base mentioned is not coming true than another rate can be used. Mismatch arises

because of normal errors of business planning (Catrini and et.al., 2017). Calculation of

supplementary rates are nothing but it is a process where under or over absorption are

brought up or down as the case may be to correct figure of actual overhead. The

supplementary rates are of two types

1. Positive-: Under absorption are corrected by positive rates as unrecovered amount

is added back to cost of sales, work in progress.

2. Negative-: By this over absorption are corrected and excess recovery of overhead

is deducted from cost of sales, work in progress.

2. Carry over Overheads-: The following are circumstances where they can be carried to

next year in hope that they will be neutralized.

1. In case the industry is of seasonal nature than it carried to next season for

neutralization.

2. Where there is under absorption in initial years these may be carried forward for

neutralizing later when project is established.

3. Transfer to Costing Profit and Loss-: Following are cases where they must be transferred

to costing P&L-:

1. where the absorption's are relatively of small value and unnecessary to adjust to

cost of sales

2. In case where it arises because of abnormal factors like fires, strikes, plant

breakdown etc.

CONCLUSION

On the basis of above report, it acne concluded that there had been implication of various

tools and techniques which were being addressed to have proper determination of relevant facts.

Similarly, implicating various cost analysis techniques which will be useful for better

determination on ascertainment of all the relevant facts.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Biondi, L. and et.al, 2017. Accounting costs without a cost accounting system: the case of a

small Italian winery of excellence. Piccola Impresa/Small Business, (3).

Catrini, P. and et.al., 2017. Exergy analysis and thermoeconomic cost accounting of a Combined

Heat and Power steam cycle integrated with a Multi Effect Distillation-Thermal Vapour

Compression desalination plant. Energy Conversion and Management. 149. pp.950-965.

Dias Maragno, L. M. and et.al., 2017. The (ir) relevance of cost accounting in leading accounting

Journals. CUSTOS E AGRONEGOCIO ON LINE. 13(3). pp.254-286.

Huang, Q., 2018. Skylar, Inc.: Traditional Cost System vs. Activity-Based Cost System–A

Managerial Accounting Case Study. Applied Finance and Accounting. 4(2). pp.55-66.

Kaplan, R. and Anderson, S., 2003. Time-driven activity-based costing. Pearson.

Lutilsky, I. D., Liović, D. and Marković, M., 2018, January. THROUGHPUT ACCOUNTING:

PROFIT-FOCUSED COST ACCOUNTING METHOD. In International Conference

Interdisciplinary Management Research XIV, Opatija–Croatia. 18–20 May 2018..

Nagirikandalage, P. and Binsardi, B., 2017. Inquiry into the cultural impact on cost accounting

systems (CAS) in Sri Lanka. Managerial Auditing Journal. 32(4/5). pp.463-499.

Online

Traditional Cost Accounting System. 2018. [Online]. Available Through:

https://accountlearning.com/weaknesses-traditional-cost-accounting-system/>.

8

Books and Journals

Biondi, L. and et.al, 2017. Accounting costs without a cost accounting system: the case of a

small Italian winery of excellence. Piccola Impresa/Small Business, (3).

Catrini, P. and et.al., 2017. Exergy analysis and thermoeconomic cost accounting of a Combined

Heat and Power steam cycle integrated with a Multi Effect Distillation-Thermal Vapour

Compression desalination plant. Energy Conversion and Management. 149. pp.950-965.

Dias Maragno, L. M. and et.al., 2017. The (ir) relevance of cost accounting in leading accounting

Journals. CUSTOS E AGRONEGOCIO ON LINE. 13(3). pp.254-286.

Huang, Q., 2018. Skylar, Inc.: Traditional Cost System vs. Activity-Based Cost System–A

Managerial Accounting Case Study. Applied Finance and Accounting. 4(2). pp.55-66.

Kaplan, R. and Anderson, S., 2003. Time-driven activity-based costing. Pearson.

Lutilsky, I. D., Liović, D. and Marković, M., 2018, January. THROUGHPUT ACCOUNTING:

PROFIT-FOCUSED COST ACCOUNTING METHOD. In International Conference

Interdisciplinary Management Research XIV, Opatija–Croatia. 18–20 May 2018..

Nagirikandalage, P. and Binsardi, B., 2017. Inquiry into the cultural impact on cost accounting

systems (CAS) in Sri Lanka. Managerial Auditing Journal. 32(4/5). pp.463-499.

Online

Traditional Cost Accounting System. 2018. [Online]. Available Through:

https://accountlearning.com/weaknesses-traditional-cost-accounting-system/>.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.