Activity Based Costing: Analysis of Implementation and Improvement

VerifiedAdded on 2023/06/14

|12

|729

|253

Report

AI Summary

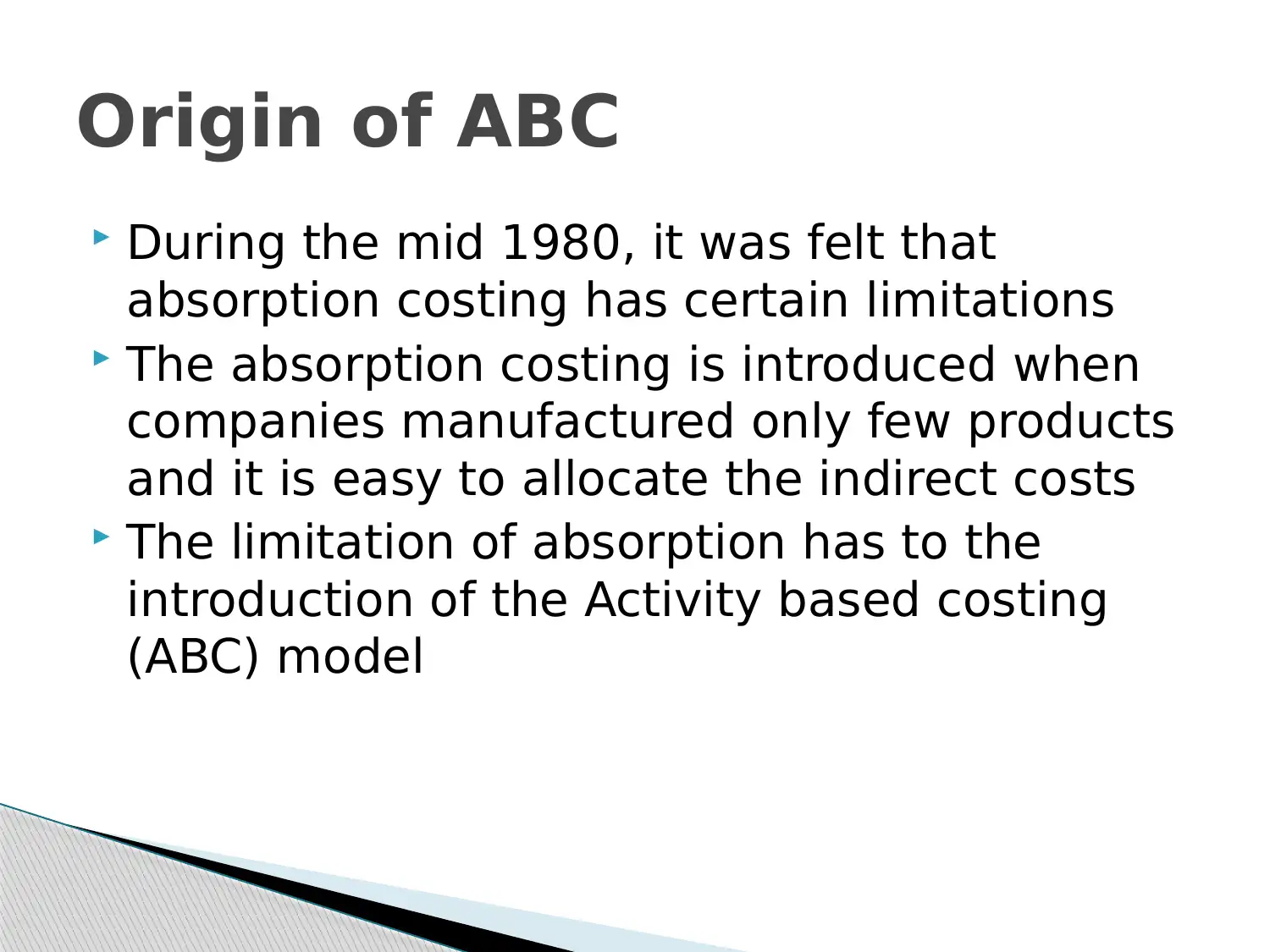

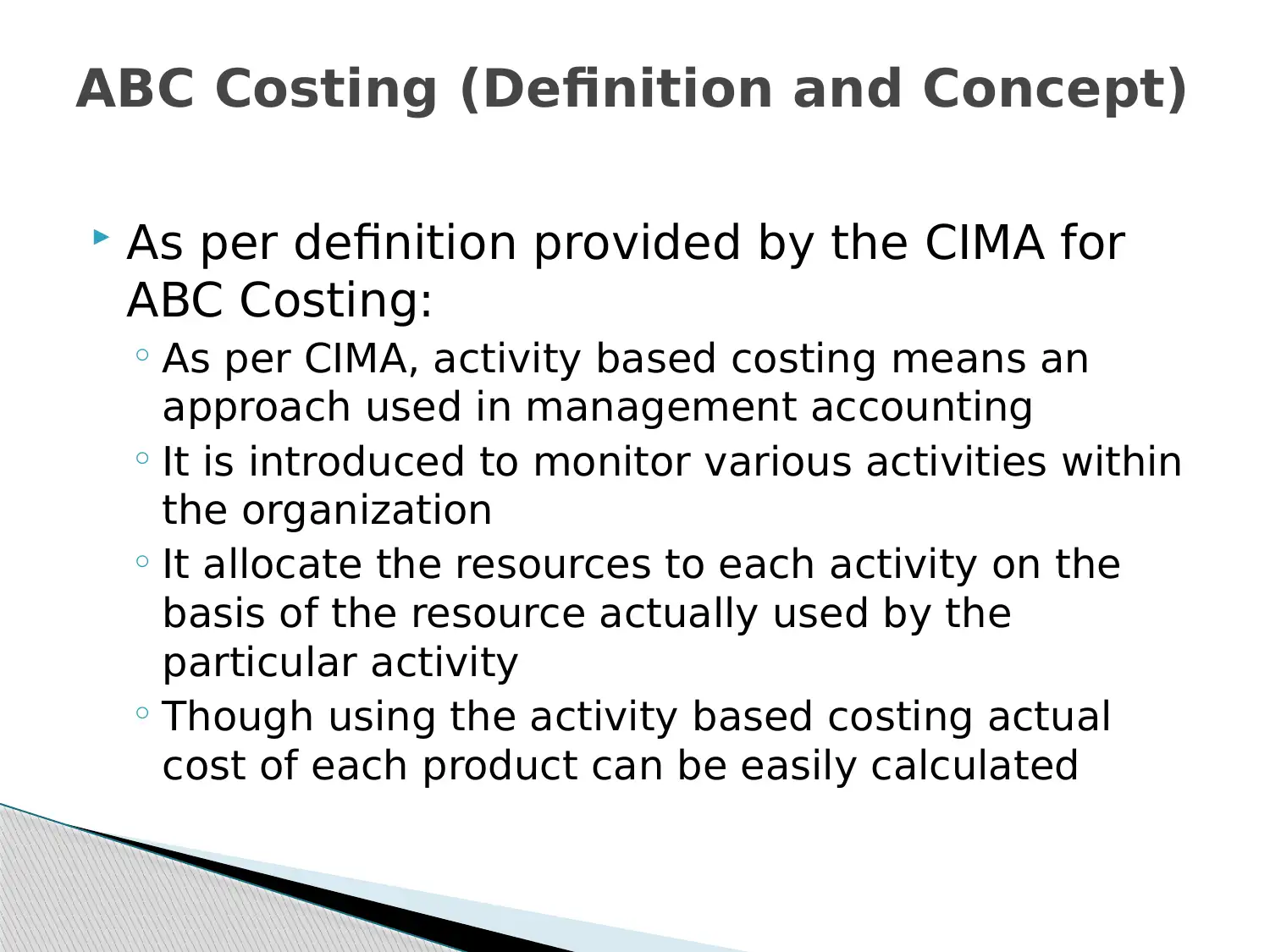

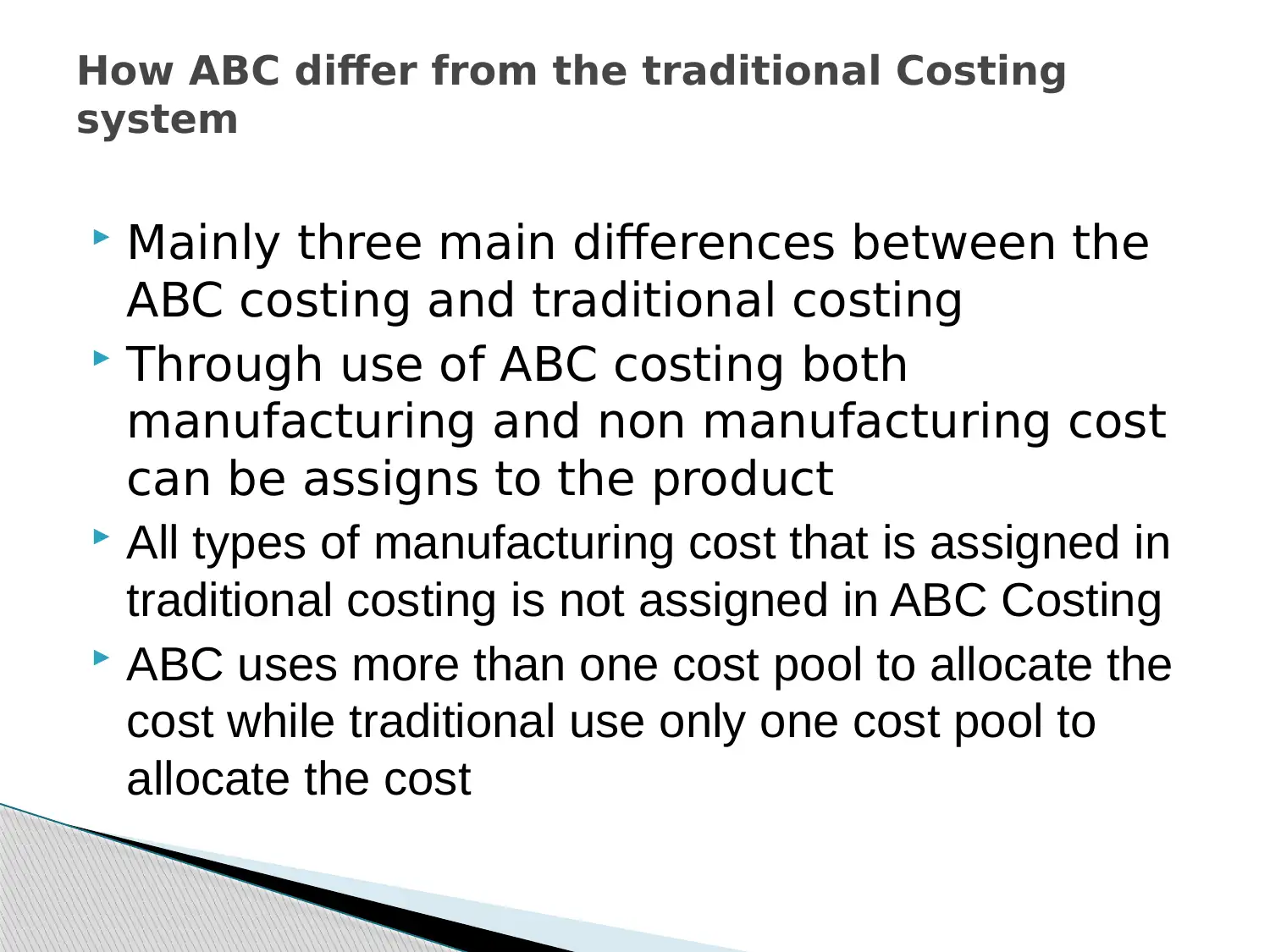

This report provides an overview of activity-based costing (ABC), tracing its origins to the limitations of traditional absorption costing methods. It defines ABC as a management accounting approach that monitors organizational activities and allocates resources based on actual usage, enabling accurate product cost calculation. The report highlights key differences between ABC and traditional costing, including the assignment of both manufacturing and non-manufacturing costs, the use of multiple cost pools, and the integration with Six Sigma. It discusses the advantages of ABC, such as accurate costing and systematic overhead allocation, as well as disadvantages like high initial investment and maintenance costs. Motivations for ABC adoption, exemplified by General Motors' use in energy consumption estimation, are explored. The report further examines ABC implementation for predicting operational costs, achieving realistic results, and identifying process improvement areas, particularly in waste reduction. It emphasizes the necessity for identifying non-value-adding activities and proposes using ABC in management accounting for in-depth cost understanding. The report concludes by referencing several academic sources.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.