ABC Learning's Collapse: Accounting, ASA 701, and Government Response

VerifiedAdded on 2019/11/29

|16

|3209

|344

Report

AI Summary

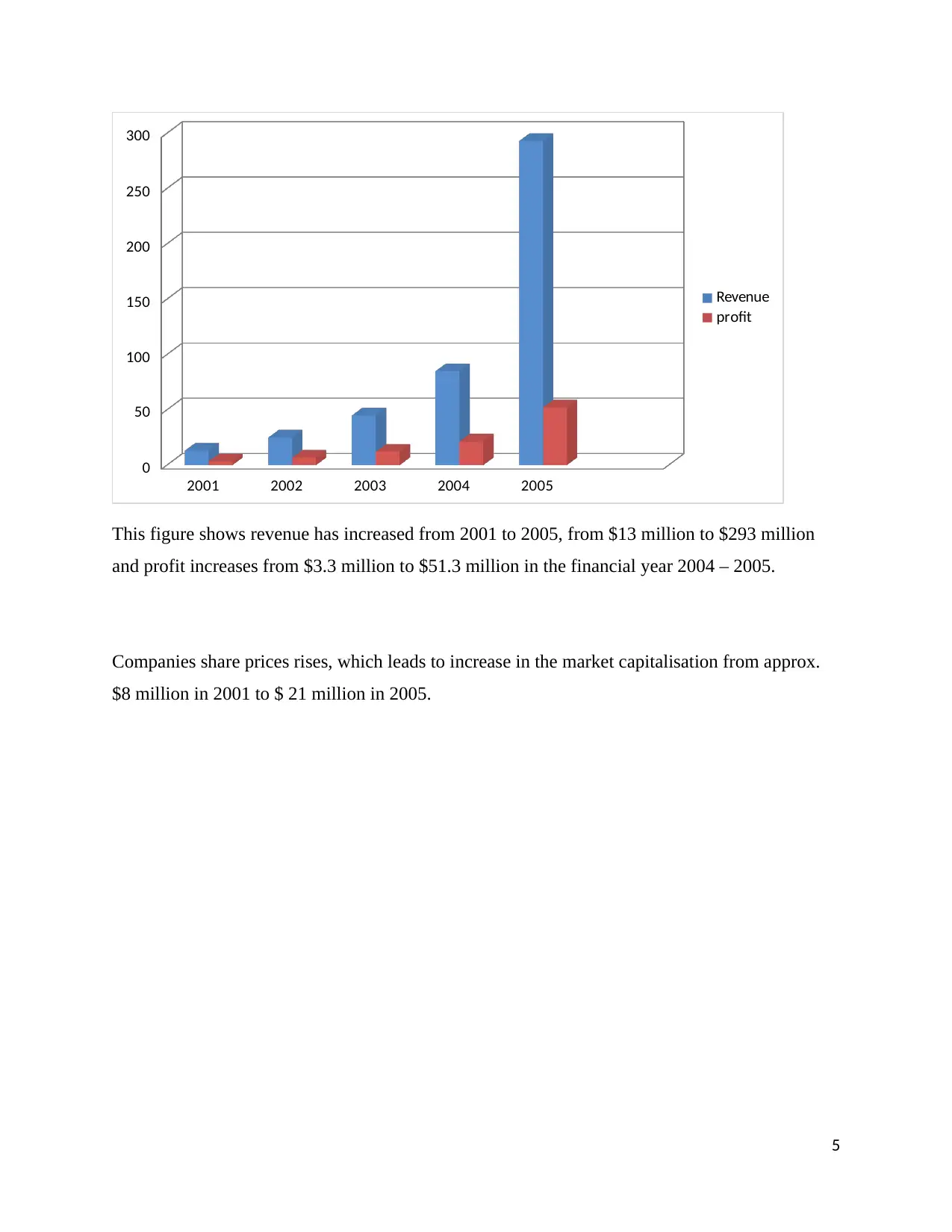

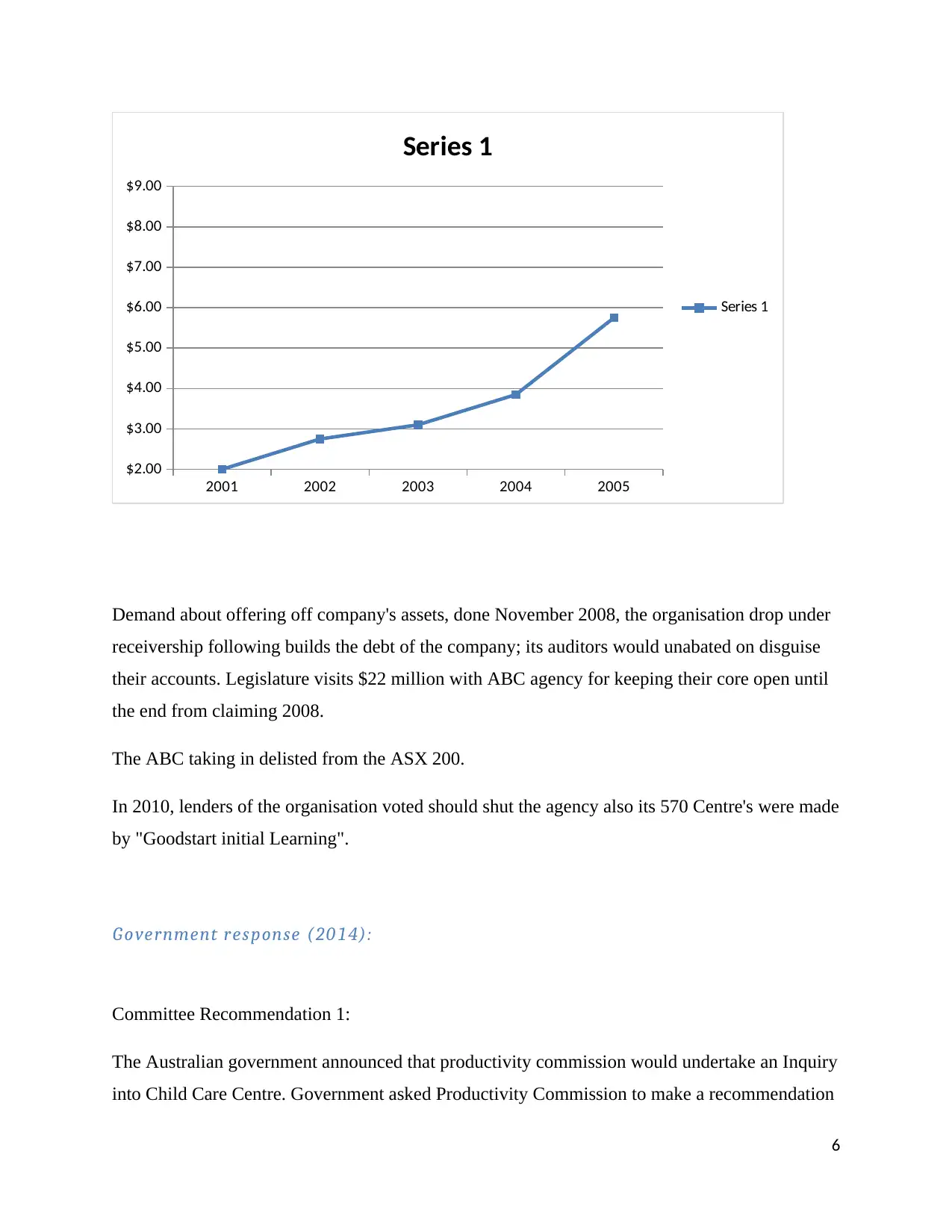

This report provides a comprehensive analysis of the ABC Learning collapse, a major corporate failure in Australia's childcare industry. The study examines the company's history, rapid expansion, and subsequent financial difficulties, highlighting significant accounting issues such as the overvaluation of intangible assets and declining profitability. It explores the government's response, including inquiries and policy changes, and discusses the role of ASA 701, the auditing standard, in addressing financial irregularities and ensuring auditor accountability. The report delves into the operational date and application of ASA 701. It also covers the lessons learned from the collapse, offering insights into corporate governance, financial reporting, and the importance of independent auditing. The report also includes a detailed financial analysis, providing data on assets, debts, shareholder funds, and profitability trends, alongside a discussion of revenue and profit fluctuations, and the company's eventual delisting from the Australian Stock Exchange. The study concludes by emphasizing the significance of robust financial practices and regulatory oversight in preventing similar corporate failures.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.